Abstract

Rural–urban migrants in China often experience poor living conditions and are less likely to be homeowners than urban–urban migrants. This study aims to investigate whether the homeownership gap between rural–urban migrants and urban–urban migrants in China vary by income. We explore the homeownership gap between the two migrant groups using the National Migrants Population Dynamic Monitoring Survey in 2014. Our findings show that the homeownership gap between rural–urban migrants and urban–urban migrants vary by income, and this gap is larger for high-income groups than for low-income groups. The estimations also demonstrate that social security insurance may act as the transmission channel, indicating a stratification process.

Keywords

Introduction

Homeownership symbolizes a path to the promotion of economic well-being, accumulation of wealth, and attachment to the community. For immigrants, homeownership is also a part of the integration process in the destination society (Abramsson et al., 2002). Thus, owning a home in destinations has often been portrayed as the fulfillment of many individuals’ dreams (Alba & Logan, 1992). Homeownership also represents an outcome of long-term economic progress in the destinations (Sinning, 2010). The decision to purchase a house may signify a long-term commitment to remain in the new country and become a permanent resident (Clark & Dever, 2001; Krivo, 1995).

Since the reform and opening-up in 1978, many rural laborers migrated from mid-western to eastern China. They became the mainstay of the industrial workers. Specifically, they provided significant contributions to China’s urbanization and economic growth in the past decades. However, most rural migrants in destination cities still suffer from poor living conditions and experience a low homeownership rate (Y. Huang, 2003; Logan et al., 2009; Li et al., 2018; L. J. Ma & Xiang, 1998; Niu & Zhao, 2018; Tang et al., 2017). Previous studies focused on the determinants of housing tenure or living conditions of rural migrants. Although these studies have inconsistent conclusions, they have uniformly viewed urban institutional restrictions (Hukou) and other discriminatory treatments as the main factors of the low homeownership rate and poor living conditions of rural migrants in urban destinations (Fang & Zhang, 2016; Hui, 2005; Li et al., 2018; Tang et al., 2017; Tao et al., 2015).

Several empirical studies also discussed the homeownership between rural migrants and the locals. Cui et al. (2016) examined homeownership differences between skilled migrants and their local counterparts using the life histories of 804 skilled workers in Nanjing. Similarly, Li et al. (2018) applied a nationwide micro-level data set from the Chinese Family Panel Studies to explore the overcrowding differential among migrants and native residents. However, they mainly focused on the housing attainments among migrants and natives, thereby leaving the homeownership gap between rural–urban and urban–urban migrants unexplored.

The current study addresses this gap in two distinct ways: First, we use the neoclassical consumer choice model to explore the determinants of homeownership in the internal migration context. Then, we incorporate the discrimination for rural–urban and urban–urban migrants in the housing and credit market to discuss the heterogeneous effect of income on homeownership. Finally, we discuss the transmission and perceive that social insurance may link the income differentials and homeownership gap.

Literature Review

Owning a house in destinations symbolizes the achievement of the stability and success of immigrants (Davidov & Weick, 2011). However, they predominantly become tenants and are unlikely homeowners in the developed market (Borjas, 2002; Constant et al., 2009; Coulson, 1999; DeSilva & Elmelech, 2012; Painter et al., 2001). Previous studies demonstrated that homeownership is a result of various sociodemographic and household characteristics (Davidov & Weick, 2011). Evidence from the microeconomic perspective shows that household income, employment status, savings, citizenship status, family size, education, marriage status, and family composition are closely associated with the entry to homeownership among immigrants (Mundra & Oyelere, 2018). Moreover, Davidov and Weick (2011) identified income as a significant factor affecting unaffordability to homeownership. Thus, success in the labor market reflected at the level of income or income brought along from the country of origin influences the migrants’ decision to buy a home.

A significant homeownership gap remains between natives and immigrants (Zorlu et al., 2014). Considerable literature explores this gap and considers demographic and socioeconomic factors as the main causes (Fesselmeyer et al., 2012; Magnusson Turner & Hedman, 2014; Painter et al., 2001). Some studies also argued that the differences in demographic and socioeconomic characteristics could not fully explain this gap (Bråmå & Andersson, 2010; Kauppinen et al., 2015; Krivo, 1995; Painter & Yu, 2010; Sinning, 2010; Zorlu et al., 2014). In addition to the weak socioeconomic position, they also attributed the unexplained residual to unobserved factors, such as ethnic preferences and discrimination in the credit and housing markets (Constant et al., 2009; Coulson & Dalton, 2010; DeSilva & Elmelech, 2012; Haan, 2007).

From the microeconomic consumer choice model, households choose to purchase following their needs, preferences, and financial resources (Alba & Logan, 1992). The socioeconomic situation, especially income viewed as one of the most powerful causes, can explain low homeownership rates for immigrants (Garcia & Figueira, 2020). Previous studies mostly assumed that income is homogeneous, and the income effect is equal for immigrants and natives. Specifically, they argued that the ethnic gap in homeownership is as large for high- and low-income groups (Uunk, 2017). However, the income effect may be heterogeneous because the ethnic gap of homeownership may show different influences between high- and low-income groups. Empirical studies demonstrate that racial homeownership differentials in high-income groups are smaller than in low-income groups (Gyourko et al., 1999; Haurin et al., 2007). Using the data from the first wave of the Netherlands’ Life Course Survey, Uunk (2017) demonstrated that the ethnic homeownership gap between immigrants and natives is smaller within high-income groups than low-income groups. He also argued that low-income immigrants might experience ethnic discrimination from the lenders. The above studies were not able to explore how discriminatory practices can account for the ethnic gap in low-income groups (Uunk, 2017). The transmission channel on how the discriminatory institutional practices link the income differential and homeownership gap remains unclear, thereby suggesting that future studies should extend these issues to other contexts.

Background and Conceptual Framework

Housing for Urban–Urban and Rural–Urban Migrants in China

Since 1978, China has experienced a rapid and unprecedented process of urbanization where a floating population moved from less developed regions to the developed eastern coastal areas. According to China’s floating population development report conducted by the National Health and Family Planning Commission of China in 2016, 247 million migrants were working in the destinations without local Hukou, comprising about one sixth of China’s total population. Migrant workers roughly accounted for 35% of the Chinese labor force (C. Ma et al., 2020). Although they have contributed to economic development, most of them do not share the same benefits as urban residents (Liang et al., 2014).

Migrants in China often experience disadvantages in the housing market. Previous studies confirmed that rural–urban migrants commonly suffer from poor living conditions and a low rate of homeownership (Y. Huang, 2003; Tang et al., 2017; W. Wu, 2002). Moreover, rural–urban migrants working in cities either rely on employer-provided dormitories or turn to the rental market for cheaper options with usually poor conditions (Song et al., 2008). Housing for rural–urban migrants remains a challenge and has just recently become a hot scholarly topic (Y. Huang & Tao, 2015). Urban–urban migrants, who are also less likely to be homeowners than native residents, still suffer high degree of housing deprivation in China (Li et al., 2018).

The potential explanation for the housing disadvantages mainly focuses on the institutional barriers, such as Hukou (Chan & Zhang, 1999; X. Huang et al., 2014; Y. Huang & Jiang, 2009; Tao et al., 2015). Migrants are less of a homeowner than natives not just because they are less able to afford a house but also because they are not treated as “official” residents (Liu et al., 2013). They are excluded from the public housing project and have less access to obtain housing-related subsidies. A study perceived the Hukou system, especially institutional constraints associated with local urban Hukou, as the underlying cause of the low level of homeownership and poor living conditions among migrants in destinations (L. Wu & Zhang, 2018).

Conceptual Framework

The neoclassical microeconomic model of consumer choice argues that homeownership is a result of household needs and preferences of individuals, who are constrained by their financial resources (Alba & Logan, 1992). As the first requirement for owning a home, the accumulation of financial resources is necessary to make a down payment, qualify for a mortgage, and meet monthly payments (Burr et al., 2011). Generally, income is a direct and critical factor affecting unaffordability to homeownership. Individuals with high salaries have more potential to cover the initial costs and are more likely to qualify for mortgages than those with low income (Garcia & Figueira, 2020; Krivo, 1986; Yap & Ng, 2018).

Income also plays an important role in the entry to homeownership for rural–urban and urban–urban migrants (Cui et al., 2016; W. Wu, 2004). Previous studies in China provided a consistent conclusion that household income was significant in predicting migrants’ homeownership (Fang & Zhang, 2016). However, rural–urban and urban–urban migrants in different income groups may experience varied discrimination in the housing and credit market. The low-income households of rural–urban and urban–urban migrants have limited affordability to purchase homes (Y. Huang & Tao, 2015). Thus, the effect from the structural constraints such as granting mortgage applications and housing qualifications is undifferentiated; that is, the income effect may be equal for rural–urban and urban–urban migrants in the low-income group.

For high-income households, they have enough payment ability to purchase the commodity, and thus the eligibility to afford a house turns to be critical. Most of the destination cites adopt the home-purchase restriction. Nonlocal families can buy houses if they can provide proof of a social insurance premium paid for 1 year or more; otherwise, they cannot purchase any house. In this case, rural–urban migrants may suffer disadvantages in terms of access to purchase a house and unlikely to afford it because they have a low likelihood to participate in social insurance.

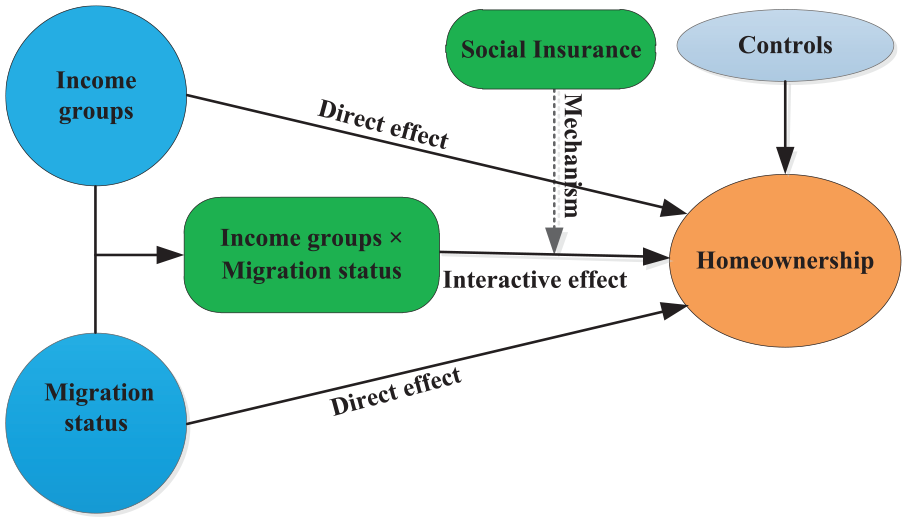

The interaction between income groups and migrant status captures the heterogeneous effect of income. Accordingly, we expect that the homeownership gap between rural–urban and urban–urban migrants may vary by income. Specifically, this gap may be more evident in high-income groups than in low-income groups.

Social insurance may act as the transmission mechanism that differentiates the housing choice among rural–urban and urban–urban migrants. In the past decade, China has implemented strict home-purchase restrictions to squeeze out speculative demand and dampen soaring home prices (Sun et al., 2017). To gain purchase eligibility, nonlocal residents must continue to participate in the social insurance or pay the personal income tax for at least 1 year in the small- and medium-sized cities, and 3 or 5 years in the large cities. Rural–urban migrants cannot have purchase eligibility because most of them do not have urban social insurance projects. According to the 2014 annual survey of migrant workers conducted by the National Bureau of Statistics, only 16.7% and 17.6% of rural migrants had participated in pension and health insurance projects, respectively. Even for the high-income groups, migrants remain less covered by urban social insurances than natives (Ning & Qi, 2017). Although rural migrants with high incomes are more capable of purchasing a house than those with low income, under the home-purchase restrictions policy, they still experience difficulties in obtaining eligibility to purchase. Conversely, although urban–urban migrants have no local Hukou, most of them may have a stable job in the urban labor market and participate in social insurances. In this case, their opportunity to obtain eligibility in the urban housing market is higher than rural–urban migrants. The superiority in social insurance attainment may be more significant in the high-income group. For the low-income group, rural–urban and urban–urban migrants have less affordability to own a house. Thus, the eligibility constraints derived from social insurance are undifferentiated for the two groups.

Data and Sample Description

We used the data from the 2014 National Migrants Population Dynamic Monitoring Survey (NMPDMS-2014) conducted by the National Health and Family Planning Commission of China. The NMPDMS is open access, and it is a nationally representative cross-sectional survey of internal migrants aged 15 to 59 years who did not have the local Hukou and had been living in local cities for more than 1 month. We obtained our sample using a stratified multistage random sampling method with the probability proportional to size approach. The survey covered 348 cities from all 31 provincial units in China. In 2014, the survey data included approximately 200,000 households. The NMPDMS-2014 is useful for this research because it collected a wide variety of data relating to the demography of household-head and housing experience of migrant families and detailed information on migrating or staying family members.

The Hukou system in China is a governmental household registration system used to limit the local public service access. This system designates the status of a resident as being either rural or urban and local or nonlocal on the basis of his or her registered birthplace. A migrant is not entitled to public services in the destination city, despite working and living in the city. Hence, we separated the sample into two migrant groups: rural–urban and urban–urban migrants. We defined the migrants as individuals who have resided at the place of destination for at least 1 month without local Hukou. Rural–urban migrants are those who moved from rural to urban areas but still keep their rural Hukou status, whereas urban–urban migrants are those with urban Hukou moved among cities but without local Hukou in the local city.

Homeownership is the outcome variable, which is measured using a dummy variable. If migrants own a house in urban destinations, then a value of 1 is given. Otherwise, a value of 0 is provided. To accord with the Constant et al. (2009) and Uunk (2017), controls include a set of variables, such as demographic and life cycle (i.e., age and household migration status), socioeconomic status (i.e., household income, education attainment), immigration-specific variable (i.e., migration experience and permanent settlement intention), institutional status and housing price (i.e., housing purchases restriction and local house price), and geographic location (dummy variables).

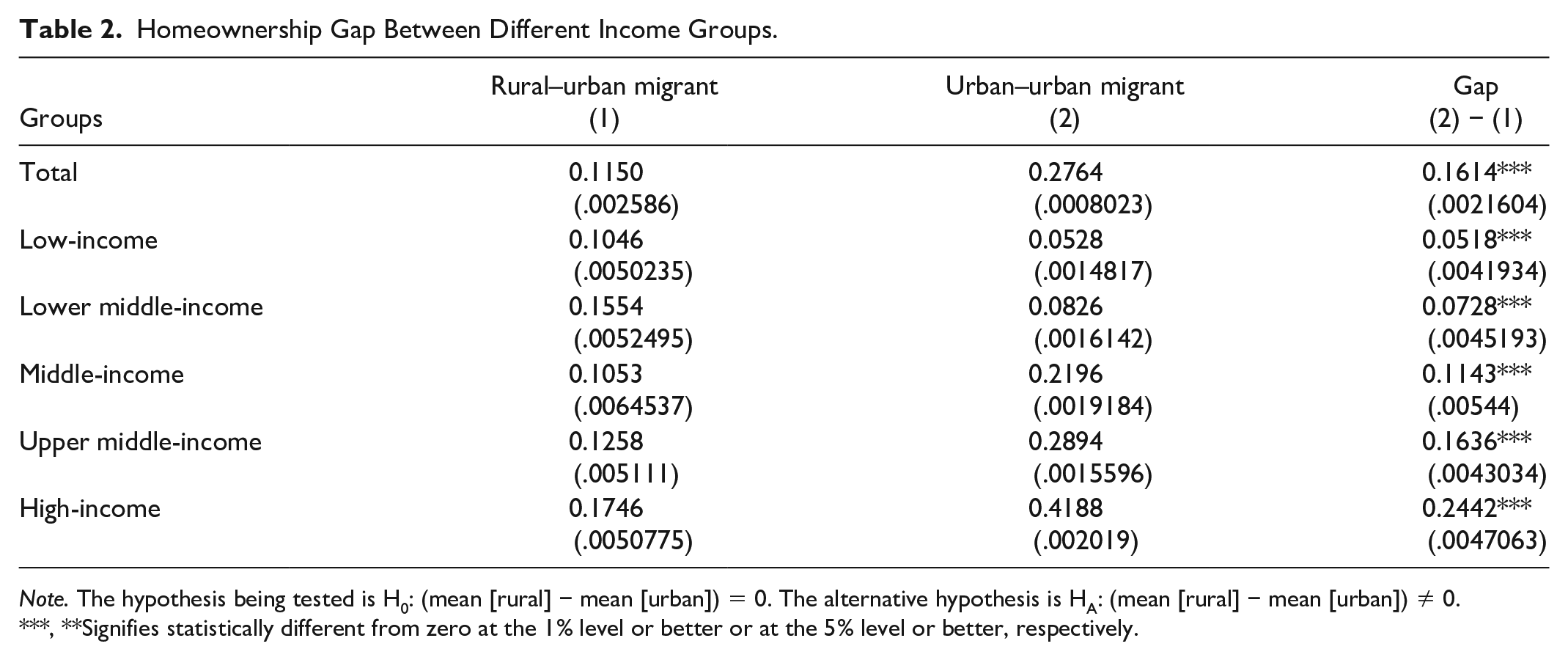

Table 1 presents the mean of the main variables of rural–urban and urban–urban migrants. The homeownership rate for the migrants is approximately 14%, which is much less than the residents in 2014 (95.4% for the residents). We find a significant homeownership gap between urban–urban and rural–urban migrants. Specifically, 27.64% of urban–urban migrants purchased a house in the local city, whereas only 11.5% of rural–urban migrants were homeowners.

Sample Description by Hukou.

The average household income of rural–urban migrants is also lower than the urban–urban migrants, indicating that the latter may have higher housing affordability than the former. The average education years for the two groups are more than 9 years, and the educational achievement for the urban–urban migrants was higher than the rural–urban group. With regard to life cycle traits, approximately half of the households migrated with all of their family members, revealing that household migration has become common in the labor migration process.

Household income is regarded as the most uniformly important determinant of homeownership, and families with high incomes are more likely to own a home than those with low income (Alba & Logan, 1992; Kauppinen et al., 2015). The homeownership gap between rural–urban and urban–urban migrants may vary across varied income groups. To address these concerns, we divided our sample into five equal income groups. We categorized those with a household income below the 20th percentile as the low-income group, those within the 20th to 40th percentiles as the lower middle-income group, those within the 40th to 60th and 60th to 80th percentiles as the middle-income and upper middle-income group, and those within the top 20th percentile as the high-income group.

Table 2 presents the results of the two-sample t-test. For rural–urban and urban–urban migrants, homeownership increases with the income increase. Migrants with high incomes have a higher likelihood of owning a house than those with low incomes. Moreover, urban–urban migrants are more likely to be a homeowner in all five groups than rural–urban migrants. The results of the two-sample t-test also reveal that the homeownership gap between rural–urban and urban–urban migrants are significant across all five income levels, and this gap is wider in the high-income group than the low-income group. The homeownership gap is only 0.0518 at the low-income level, and this gap at the high-income level reaches 0.2442, which is nearly 5 times that of the former.

Homeownership Gap Between Different Income Groups.

Note. The hypothesis being tested is H0: (mean [rural] − mean [urban]) = 0. The alternative hypothesis is HA: (mean [rural] − mean [urban]) ≠ 0.

, **Signifies statistically different from zero at the 1% level or better or at the 5% level or better, respectively.

Estimation and Analysis

Following Constant et al. (2009) and Uunk (2017), we use logit models to explore the determinants of homeownership. Equation 1 serves as a benchmark model:

where the homeownership Hi is assumed to be a function of

The homeownership gap between rural–urban and urban–urban migrants may vary among the high- and low-income groups. Accordingly, we incorporated the interaction between income groups and migrant status to capture this effect as follows:

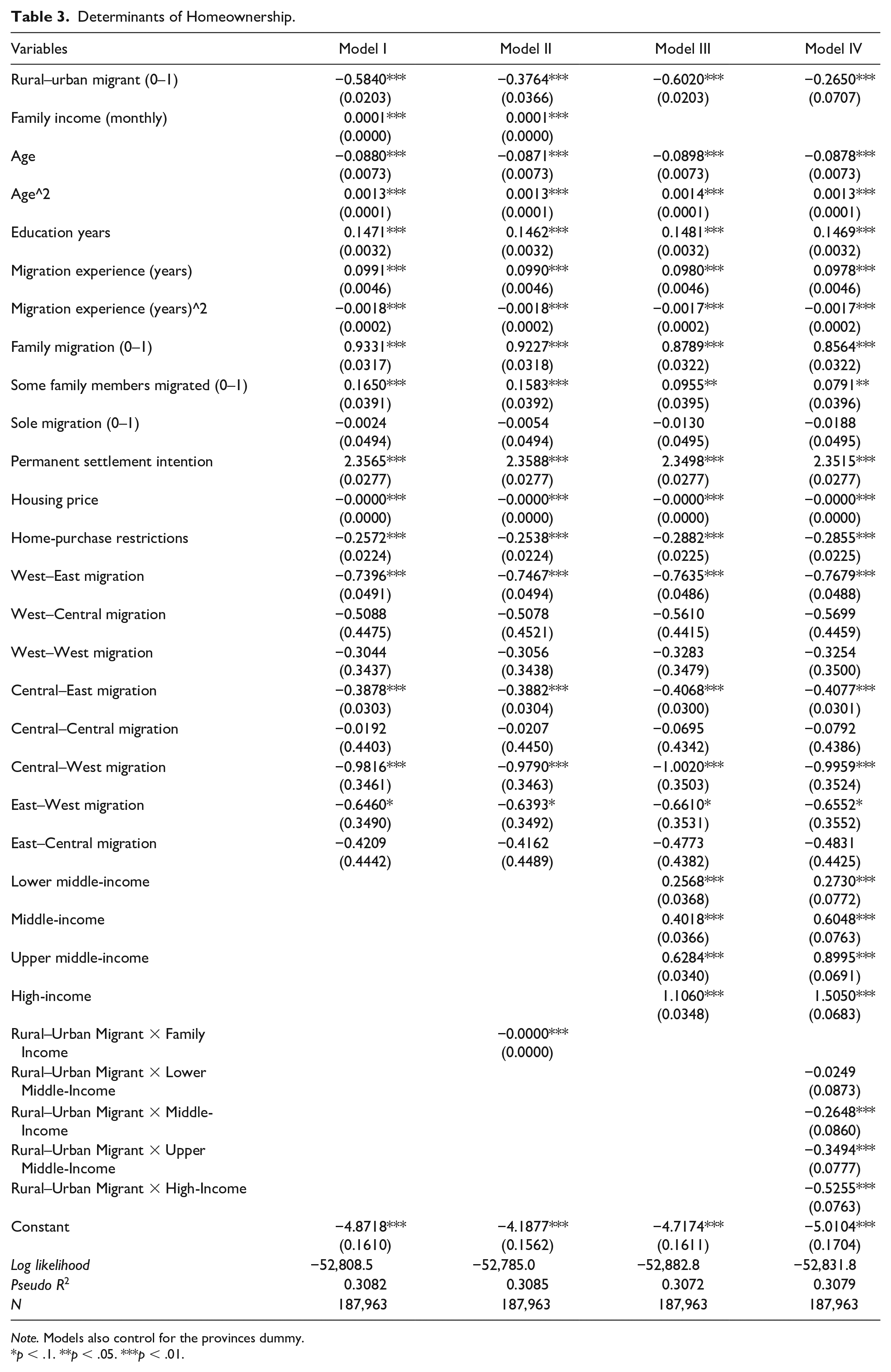

Table 3 presents the estimation results. We incorporated family income as a continuous variable in Models I and II and the five income groups in Models III and IV. Then, we introduced the interaction between family income groups and immigrant status in Models II and IV.

Determinants of Homeownership.

Note. Models also control for the provinces dummy.

p < .1. **p < .05. ***p < .01.

The estimations for demographic and socioeconomic controls in Model I are consistent with the theory and existing empirical results; that is, rural–urban migrants are less likely to be homeowner than urban–urban migrants. This finding implies that the latter may have more advantages in the urban housing market than the former despite both of them having no local Hukou. The results also reveal that income and education achievements are positively related to homeownership. Migrants with high income and education are likely to own a house, which is consistent with existing evidence from the developed market (Alba & Logan, 1992; Painter et al., 2001; Painter & Yu, 2010; Zorlu et al., 2014). Consistent with Constant et al. (2009), we find that migration experience has a positive influence on homeownership. This finding indicates that high-quality employment determines migrants’ housing capability to purchase a home. The regression results also demonstrate that older migrants are more likely to own a house than their younger counterparts. This finding is consistent with that of Colom Andrés and Molés Machí (2017) and Tang et al. (2017), who showed a positive relationship between age and homeownership in Spain and China. Accordingly, we argue that old migrants have more advantages in acquiring wealth for a down payment to purchase a house than their younger counterparts.

As for the migration status, we find that those who migrated with their whole family have a high probability of owning a house, whereas sole migrants are unlikely to be homeowners. This finding is consistent with that of Alba and Logan (1992) and Kauppinen et al. (2015), thereby confirming that housing needs also exert a large effect on homeownership. The migrants with permanent settlement intention have more likelihood to own a house, which is consistent with Tang et al. (2017), which confirmed that migrants’ settlement intention are positively related with the housing attainment of rural migrants’ in the urban destinations. The context controls also show that housing price and home-purchase restriction are negative with the homeownership, revealing that high housing price and strict home-purchase restriction will weaken the migrants’ housing access and affordability.

The estimation results from Model I demonstrate that household income is positively associated with homeownership, and rural migrants are unlikely to own a house. We added the interaction between migrant groups and continuous family income into the estimation to confirm whether the homeownership gap between the two groups varies by income. The results in Model II show that the interaction term is significant and negative. They confirm that the effect of family income on the homeownership for urban–urban migrants is greater than rural–urban migrants. Hence, the latter experiences more disadvantages in the housing market under the same financial budgets than the former (Magnusson Turner & Hedman, 2014).

We further divided the family income into five equal income groups and added the interaction terms of income groups with the migrant groups to capture the group differences in homeownership. The results from Model III demonstrate that with the increase of income, the probability of homeownership is high in the high-income groups, and this probability increases accordingly. This finding is consistent with expected theory and previous studies (e.g., Painter et al., 2001). Then, we made the five income groups interact with the migrant groups and incorporated the four interaction terms into the estimation equation to explore the interaction effect. As shown in Model IV of Table 3, the results confirm that most of the interaction terms are significant, especially for high-income groups.

Scholars typically used two ways to interpret the significant outcomes of interaction effects. First, these three significant interaction terms indicate the effect of income on homeownership is stronger for urban–urban migrants than for rural–rural migrants. For urban–urban migrants, the coefficients of income effect for the middle-income, upper middle-income, and high-income groups are 0.6048, 0.8995, 1.5050, respectively, upon the low-income. However, for rural–rural migrants, these group differences are smaller. Specifically, the effect of income decreases to 0.3400 (0.6048 – 0.2648), 0.5501 (0.8995 – 0.3494), and 0.9795 (1.5050 – 0.5255). The second interpretation is that the homeownership gap between rural–rural and urban–urban migrants is increasingly negative as the income level increases. The gap coefficient is only 0.2650 for the low-income group but rose to −0.5298 (−0.2650 – 0.2648), −0.6144 (−0.2650 – 0.3494), and −0.7905 (−0.2650 – 0.5255) for the middle-income, upper middle-income, and high-income groups, respectively. These results differ from the conclusion of Uunk (2017), who argued that the ethnic homeownership gap is strong for low-income groups. Although we obtained contradicting results with Uunk (2017), we still present the same potential explanations that housing preference and discrimination may cause a large gap. This explanation is slightly different because we believe that in China, the rural–urban migrants in the high-income groups confront discrimination and institutional constraints in the housing market, indicating a more serious stratification process than the assimilation process in the rural migrants housing trajectories. This condition may be a unique phenomenon in China, wherein the housing tenure of rural migrants does not synchronously increase as the socioeconomic status rises. Although they can improve their socioeconomic status, they still have little opportunities to acquire informal citizenship or Hukou status, especially in large cities.

The homeownership gap between rural–urban and urban–urban migrants varies by income, which is larger in high-income than in low-income groups. This conclusion is a little different from that of Uunk (2017) and other previous studies. How can the ethnic gap in high incomes be accounted for by looking into the role of discriminatory practices? What are the transmission channels that link the income difference and the homeownership gap? We claimed that the social insurance project might act as the transmission channel that limits the income effect. Thus, we added the social insurance project and its interactions with migrant status and income groups into Equation 2 and assumed that rural–urban migrants who attend the social insurance project could improve their income effect on the housing attainment.

We incorporated the main forms of social insurance schemes such as social health insurance, pension insurance, and housing provident funds into Models I, II, and III, respectively. Table 4 presents the estimation results. The interaction terms of social insurance schemes with migrant status and income groups in the three models are significant and positive, providing clear evidence that social insurance may enhance the income effects of rural–urban migrants on their homeownership. This finding is consistent with the conclusion of Tang et al. (2017). They confirmed that participation in the urban pension insurance scheme clinches the decision of migrants to buy a dwelling and settle down permanently. Under the regulation of home-purchase restrictions, rural–urban and urban–urban migrants must participate continuously in social insurance or pay the personal income tax for several years to gain purchase eligibility. However, the coverage of social insurance for rural–urban migrants is much lower than urban–urban migrants, especially in the high-income groups. Thus, the social insurance gap may widen the homeownership gap between the two migrant groups.

Mechanism: The Effect of Social Security.

Note. The controls include age, education achievement, migration experience, life cycle characteristics, permanent settlement intent, housing price, home-purchase restrictions, differences between origin and destinations, and provinces dummy.

p < .1. **p < .05. ***p < .01.

We provided a mean comparison of social insurance under different income groups. Table 5 shows that the social and medical insurance gaps between rural–urban and urban-urban migrants increased with income decrease. In the low-income group, the insurance gap was only 0.3865, but for the high-income group, the gap reached 0.6928. The same conclusion also holds for the pension insurance and housing provident funds groups; that is, the participation gap of pension insurance and housing provident funds is wider in the high-income group than the low-income group. These differentials between migrant groups may cause different income effects on housing attainment. Thus, the institutional constraints such as the social insurance system may deteriorate the homeownership segregation more seriously in the high-income group than the low-income group.

Homeownership Rates by Income Group.

Note. RUM = rural–urban migrants; UUM = urban–urban migrants.

Conclusion

Homeownership is widely perceived as a path to improve the economic well-being, social assimilation, and attachment of immigrants to the destination country. Owning a home in the destination has always been considered as a milestone for rural migrants’ integration process. However, migrants often experience poor living conditions, and only a few of them have a house of their own. Rural–urban migrants may face more disadvantages in the housing market than the locals in urban areas. In this study, we use a nationally representative cross-sectional survey in China (NMPDMS-2014) to explore the effects of income differences on the homeownership gap between rural–urban and urban–urban migrants. The multivariate regression demonstrates that rural–urban migrants are less likely to own homes than urban–urban migrants, thereby confirming that the former is more disadvantaged in the housing market than the latter. The estimation results also present evidence predicted by theory and previous works that being old, having high levels of education, high incomes, more migration experiences, and whole family members migrating together increase the probability of owning a house.

The interaction regression between migration status and continuous household income provides evidence that the effect of family income on homeownership for urban–urban migrants is larger than rural–urban migrants. To estimate whether the housing gap differentials vary across different income groups, we further divide family income into five equal income groups and add the interaction terms of income groups with the migrant groups into the equation to estimate this effect. The results confirm that the homeownership gap between rural–urban and urban–urban migrants vary by income, which is larger in high-income groups than in low-income groups. Our finding is a little different from Uunk (2017) and other previous works, which indicated a more serious stratification process than the assimilation process in the rural migrant housing trajectories. Moreover, we discuss the potential transmission channel that the social insurance scheme may act as the transmission mechanism that constrains the income effect on the homeownership of rural–urban migrants. We find that social insurance can promote the influences of rural–urban migrant’s income on their homeownership, and the social insurance differentials between the migrant groups may cause different income effects. Finally, the institutional constraints such as the social insurance system may segregate the homeownership more heavily in the high-income group than the low-income group.

The disadvantages that rural–urban migrants suffered in the housing market may be due to their weak socioeconomic resources. However, discriminatory practices, such as a shortage of social insurance coverage, have an indirect effect on the home-purchase restrictions. Our findings suggest that policies aimed at improving the living conditions of rural–urban migrants should focus on institutional constraints that limit access to homeownership. Moreover, policymakers should promote the Hukou reform and expand the coverage of public services in urban areas to all their permanent residents, including rural–urban migrants (Figure 1).

Migration status, income, and homeownership.

Our research has some limitations. First, it is difficult to find valid IVs to explore the causal effect in the estimation with A*B*C interactions terms, we only explore the association of the income on the homeownership. The causal effect should be extensively discussed in the future. Second, the NMPDMS has no related information on the family assets and employer’s traits; those factors are important determinants for housing tenure choice and should be explored in the subsequent research.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: Thanks for the support from the National Social Science Fund of China (17BJY044&&18ZDA081).