Abstract

Sustainability and social responsibility (SR) have emerged as a new way of managing all types of organizations. It is necessary that the resulting policy be integrated transversely in the control processes. The environment is especially demanding of higher education institutions (HEIs) and universities when it comes to behaving in a socially responsible manner due to their great influence in society. Many universities have adhered to the United Nations Global Compact (UNGC) principles to prove their commitment and gain legitimacy. The Communication on Progress (COP) is a management tool that helps to understand the level of implementation of the principles. Furthermore, COP analysis aids in establishing a process of continuous improvement in the management of the impacts that institutions have on their stakeholders. The aim of this study was to analyze the Spanish universities that have joined the Global Compact. Through a descriptive methodology, we identified the aspects that reflect this commitment and how this is integrated into their operational and educational processes. The results have shown that it is necessary to promote the integration of different international initiatives to guide the SR of universities. There are deficiencies in their SR management systems that prevent them from being more transparent, and it was found that in some cases, they are not aware of the implications the commitment can have in developed countries.

Introduction

The assumption of social responsibility (SR) by different types of organizations requires the integration of commitment in their management systems. On an international level, various initiatives have emerged to guide this process, such as the Organisation for Economic Co-Operation and Development (OECD; 2006), World Bank Group (2007), AccountAbility (2008a, 2008b), the Global Reporting Initiative (GRI; 2006), and the United Nations Global Compact (UNGC; 2013), among others. On a national basis, we can cite the Ethical and Socially Responsible Management System (SGE 21) Standard development by Forética (2008).

In general, these commitments are translated into a series of social, environmental, ethical, and governmental objectives. Transparency and disclosure of information regarding the behavior in relation to these objectives are keys to achieve credibility and legitimacy.

The UNGC requires participants in this initiative to develop annual Communications on Progress (COPs) to identify and communicate progress annually to their stakeholders, which could affect the credibility of both the participants and the initiative.

Currently, all types of organizations are under pressure to demonstrate SR, as evidenced by the number of publications, forums, and initiatives that exist in this regard. More specifically, there is a greater demand for SR at HEIs and/or universities, given that they hold an important role both in the impact they can have by incorporating SR in scholarly activities, as well as in their mission, vision, and strategy, manifesting themselves in their management and the multiplier effect this would have on their relationship with all stakeholders (Muijen, 2004; Universia España, 2008). Academic institutions have a special responsibility to lead by example. It is not sufficient to integrate theories into the education programs, but rather, they have to link theory with practice, as reflected in the incorporation of these principles in all of their operations.

To serve as an example, it is important to communicate how the implementation process is being carried out, in spite of the fact that in the case of Global Compact participants from the education sector, only production and dissemination are recommended.

Therefore, the objective of this research is to analyze the proposed contents of the Progress Report for HEIs (United Nations Global Compact, 2012b) and, more specifically, if the participating Spanish universities meet the process and structure that make up the proposed management control system. The analysis will allow us to identify the best practices as well as the challenges that they will face.

Theoretical Framework

According to Rasche and Esser (2006), the accountability of an organization refers to the availability of an organization to provide an explanation to its stakeholders of its intentions, actions, and omissions. All activities generate a series of impacts, which results in all types of organizations being required to respond to the demands of society, and analyze and manage those impacts, and thus “account for” their doings and omissions (Burris, 2001).

To meet this requirement, the organization has to have the necessary management structure to examine the behavior with respect to standards and to analyze whether it meets the expectations of its shareholders.

For years, managers and researchers have been concerned with analyzing the management control systems that allow companies and organizations to perform well (Anthony, 1989; Davila, Foster, & Li, 2009; Epstein, 2004; Long, Cardinal, & Sitkin, 2004; Maciariello & Kirby, 1994; Sandino, 2007; Simons, 1995), thus confirming that the choice of a control system depends on a company’s strategy and size, stability of the processes, new product launches to the market, the influence on the choice of the pressures of time, and the experience of managers. They also found that changes in the systems affect organizational effectiveness.

In the field of sustainability or SR, there is little research on the integration of social, economic, environmental, and corporate governance aspects in management control systems. Epstein and Roy (2001) showed how to proceed and also demonstrated the importance of integrating these aspects into organizations’ control systems to implement the SR strategy. They explained the effects this would have on the performance of the businesses, as a result of reduced impacts. In addition, Epstein and Roy highlighted how information derived from the control system allows managers and stakeholders to understand the effects of impacts and how to manage future impacts.

Epstein and Roy (2001) proposed three types of activities of any control system: (a) formulate the sustainability or SR strategy, (b) develop plans and programs, and (c) design control instruments to obtain the information to exercise control, perform the evaluation, and propose improvement actions.

The control systems include the control instruments used to obtain management information on key aspects. The analysis of these impacts is done through non-financial information (mainly) as well as financial information that the organizations offer to their stakeholders through internal and external reports. These measures by international bodies such as United Nations Educational, Scientific, and Cultural Organization (UNESCO; 2001), OECD (2012), and the Standards Committee of the American Accounting Association feel that they should comply with the principles of relevance, reliability, and comparability (Maines et al., 2002).

The preponderance of non-financial information is a result of the need to report on the intangible aspects that make up SR objectives. More specifically, Arévalo, Aravin, Ayuso, and Roca (2013) found that the increased presence of intangible assets in business is a motivation for adhering to initiatives such as Global Compact because this provides credibility that shows that they see this initiative as a way to enhance the value of the intangibles.

Research such as that conducted by Bescos, Cauvin, Decock Good & Westlund (2007), or Hackston and Milne (1996), revealed that the disclosure of non-financial information was incomplete, heterogeneous, and unsuitable for most items analyzed, and according to Cauvin and Bescos (2005), there is evidence that this information meets specific demands. Likewise, Bescos et al. (2007) detected the presence of barriers to the disclosure of non-financial information such as information of interest to competitors, the lack of measurement and objectivity, or the fact that the information is declarative, and therefore difficult to evaluate, or generally qualitative. Bruce, Michael, and Cauvin (2008) drew attention to how evaluators give more importance to the financial measures as opposed to non-financial measures, and that the number of measures used and the weight given vary between evaluators and also depend on their experience and values.

The different reporting standards have been made more general to counter all of these inconveniences. These standards guide and help that the information that explains the impacts generated by the organizations, which is generally non-financial, is of a higher quality and comparable. Different international organizations such as Federation des Experts Compatbles Européens (FEE; 2000), GRI (2006, 2010), AccountAbility (2008a, 2008b), and the OECD (2006), among others, have spoken about the need for this information, from the point of view of the contents meeting the following principles: sustainability, inclusiveness, materiality (Zadek & Merme, 2003), and completeness. From the point of view of quality, it should meet the following principles: balance, comparability, accuracy, timeliness, clarity, and reliability, as documented in G4 (GRI, 2013).

SR is a new way of thinking, of doing business and relating to one another. It affects all types of organizations and people, and involves consideration of a series of values such as freedom, respect for the law, justice, utility, and responsibility, among others. Consideration of these values is what leads organizations to be concerned about the management of their impacts on stakeholders. One manifestation of these impacts is included in the UNGC in 1999, in the description of the 10 principles related to four areas: Human Rights, Labor, Environment, and Anti-Corruption (UNGC, 2013). The signatories commit to respect these principles in their processes and, therefore, to be socially responsible.

Global Compact, unlike other initiatives, does not measure the behavior of the member institutions but rather emphasizes the importance for organizations to integrate the principles into their activities and report on how they are doing. In addition, they are transparent and allow for those interested to know about their developments. This provides a platform to understand and go into further depth on the 10 principles (Kell, 2005; Williams, 2004) and raises the need for regular COP. The COP policy is based on the concepts of public accountability, transparency, and continuous improvement.

Previous research on the information provided in these reports (Ruiz-Lozano & Wigmore-Álvarez, 2011) revealed often a generic description of the activities carried out by the companies in relation to the four Global Compact areas, and in the specific case of Spanish companies, Ayuso and Mutis (2010) pointed out that companies report a high level of compliance with the indicators selected for analysis but nevertheless do not provide specific information on actions undertaken with regard to the activities or with suppliers located in developing countries, which are the situations that pose a higher risk.

In the field of Global Compact, there is an academic institution work group that has developed specific guidance for the implementation of the principles for HEI (Global Compact, 2012).

The Principles for Responsible Management Education (PRME), another UN initiative, was launched in 2007 as a result of the recognition that the integration of the 10 principles in strategy and operations is good for business and society (Kell & Haertle, 2011), making it necessary for management education to adapt to this new reality. Now it is endorsed by more than 498 business schools and management-related academic institutions from more than 70 countries.

Both initiatives could be defined as policies that will guide the SR in the institutions against those considered as accountability, auditing, or reporting (Rasche, 2009).

In the case of the academic institutions, Global Compact encourages them to publish their first COP in the 2 years following their signature on the commitment to the initiative. Furthermore, in the spirit of achieving continuous improvement with regard to both implementation and transparency, Global Compact suggests that in the very least, they prepare one COP every 2 years.

For Global Compact (2012), a COP is a public communication to stakeholders (i.e., students, administrators, faculty, staff, community partners and civil society, employers, media, government) on the progress the HEI has made in implementing the 10 principles and, where appropriate, in supporting UN goals through partnerships.

As previously mentioned, management control (Anthony, 1989; Maciariello & Kirby, 1994) is the process by which managers influence the whole organization to fulfill the objectives. These objectives derive from a strategic planning process, which in the field of SR will be the result of the communication process with stakeholders and linked to the overall business strategy.

This process involves a series of activities such as planning, coordination, communication, evaluation, and corrective action. This process will occur in cycles that will in turn imply an improvement process.

The proposed COP responds to a continuous improvement process that addresses the activities that make up all management control processes, which provides for the following phases (UNGC, 2012a):

Commit. The drafting of the report in itself is a renewal and declaration of a commitment, but it is also expected that the first part will include a letter from the senior management in which they state this commitment. This part of the report defines the scope of the entity’s management and therefore, the corresponding control process.

Assess. It allows for the identification of the risks and opportunities of the entity’s management with respect to the 10 principles. This phase was developed by the UNGC (2012b), which resulted in the proposal of key aspects for the HEI to analyze in relation to the four areas (see Table 2), which should be analyzed in the COP.

Define. The identification of the lines of action in relation to the fulfillment of the objectives linked to the overall strategy of the organization and in accordance with the expectations of stakeholders. These will be reflected in a formal document called Social Responsibility (or Sustainability) Policy, Social Responsibility Plan, Code of Conduct, or Ethics Code, among others. Its definition will in turn require the identification of corresponding control instruments for its management and mechanisms to prevent and control the risks identified.

Implement. The planning of actions in relation to the defined policies allow for entities to monitor and evaluate the implementation of the commitment. The definition of indicators for each one of them will be the control instrument. These actions respond to the phase of short-term planning, and regular review is a manifestation of the remedial action process.

Measure. The definition of the objective and the level of compliance of each of the indicators related to the planned actions will track the implementation of the commitment level of the organization, so it is essential that this information is part of the contents of the report. This phase facilitates the evaluation process for those responsible and the stakeholders.

Communicate. The report is the communication too but in turn requires the disclosure of the report for which Global Compact incorporates on its website following review. In the case of Spanish institutions, their reports are published on the website of the Global Compact Network Spain.

As a goal of this research, we propose to follow Rasche’s (2009) analysis, addressing the three dimensions: content, process, and context. From the point of view of the management control process, we want to analyze the contents of the COP to define the responsiveness of universities to the issues involved in the implementation of the 10 principles proposed by Global Compact (2012), reflected in Table 2. We also analyze the management process proposed by the Global Compact (2012) guide to determine whether the Spanish universities’ COPs reveal whether they have integrated their commitment with the Global Compact principles in their management control system and whether they have signed adherence to PRME. In relation to the context, in general, the geographical scope is Spain, given that the sample analyzed refers to Spanish universities, although there may be exceptions due to activity carried out in other countries. It would be interesting to know the scope, taking into account the diversity of stakeholders that HEI have, which is why we considered identifying the degree of implementation of the principles in relation to their stakeholders.

Method

Since its launch in 2000, the UNGC initiative has won the support of thousands of organizations of all kinds. As of May 15, 2013, 705 academic institutions worldwide had joined the Global Compact, of which 85 are Spanish institutions. In general, more than 10% of the member institutions are Spanish. The institutions are engaged at all levels of training, both formal and informal, university and non-university. We defined the field of study to those that offer university degree programs or post-graduate programs, which were a total of 55 entities, 16 of which became members in 2003 and the rest gradually over the years. As for the preparation of the COPs, of the 55 entities, only 17 (31%) have drafted this document since they became members, with 14 (25.45%) reporting for the 2011 period (Table 1) and therefore becoming the subject of our analysis.

Academic Institutions That Presented the COP for the 2011 Period.

Note. COP = Communication on Progress.

The content analysis corresponds to the Diagnosis phase regarding the level of implementation of the entities’ commitment to comply with the UNGC principles, and more specifically, the aspects adapted by the UNGC (2012b) for HEIs, which are included in Table 2. A more detailed listing of all aspects analyzed can be found in Appendix A.

The methodology for the study of aspects has been qualitative in nature, based on a content analysis from reference documents. The process that was carried out was as follows:

Aspects Proposed by the Global Compact HEI Group.

Note. HEI = Higher Education Institutions.

The proposed items were revised and adapted to the field of study, Spain, and to the type of information that was analyzed, as derived from the COPs. For some aspects, epigraphs were added to the initial proposal to ensure that general information is disclosed, in addition to the specific information proposed in the sub-sections (see Appendix B). The number of items to analyze by area were the following: Human Rights (21), Labor (18), Environment (18), and Anti-Corruption (21), resulting in a total of 78 items.

As for the scoring system of items, we used a dummy variable that takes the value 1 if the information to which each item refers appears in memory, regardless of the depth, and the value 0 if no related information appears. The methodology allowed us to carry out a frequency analysis that led to the following types of results:

In a first approximation, we proceeded to check whether the reference aspects appeared explicitly in the COPs available; this allowed us to identify the aspects of the proposal that are given attention in each of the companies analyzed, see whether there is a common pattern among the entities studied, and detect possible differences. This methodology has been used in qualitative studies by Wood (2000) and Singh, Carasco, Svensson, Wood, and Callaghan (2005), among others. From a methodological point of view, it is debatable because, as noted by Wood (2000), there are concepts that can be expressed in different ways and, therefore, there is no certainty that any concept has not gone unnoticed. However, there has been an effort to monitor the semantic homogeneity of concepts.

Second, following Donker, Poff, and Zahir (2008), we developed a CV Index, in which CV Index = ΣEij, with Ej = 1 if the proposed aspect is included in the COP of the organization i, by subject areas and total. This index gives us an overview of the level of closeness of the reports of the institutions analyzed according to the Global Compact (2012) proposal for universities, as well as the degree of dispersion between them with respect to the whole sector.

In the case of presence of each of these aspects, we tried to assess the level of attention to each of them but ultimately were unable to conduct the study because in general, a descriptive analysis of the institution was presented with regard to the different aspects. We only found qualitative information on the consumption of electricity, water, and paper, and the evolution of this indicator in recent years was not shown.

Process analysis has been summarized in a series of issues (Table 3) that seek to respond to all key aspects of the entire management control process and are expressly recommended by Global Compact, as well as if the institutions have signed to the PRME, implying their consideration as part of the policies to follow. The methodology used was similar to that proposed in the previous analysis, the Assessment of 0 or 1, to record the absence or presence of information in the COP analyzed.

Items Considered in the Process Analysis.

Note. COP = Communication on Progress; PRME = Principles for Responsible Management Education.

Context analysis was performed through the identification of the geographical area and the level of application described in relation to stakeholders in each aspect of contents analyzed. Therefore, it is merely a descriptive analysis of information that will identify the scope of the principles and the depth with which it was done to respond to the Global Compact commitment by Spanish universities.

Results

Content Analysis

The university institutions analyzed drafted the COP for the 2011 period in accordance with the Global Compact guidelines given to all participants. Materiality was one of the principles that guided the preparation of the COPs analyzed, as generally revealed in the introduction. However, we chose to compare the disclosure of the proposal made for the HEI for the necessary adaptation of the disclosure of information to the education sector and the particular characteristics of the organizations.

The results show (see Table 4) that the information disclosed by the various institutions is below average (40% of the items analyzed), although in all the institutions, the situation is very dispersed, ranging from 21% to 59% of the items analyzed, far from what is desirable considering that all institutions are committed to the implementation of the principles and to gain credibility, need to be transparent about their performance.

Results of the Content Analysis.

Note. HEI = Higher Education Institutions.

If we perform the analysis according to the different areas of Global Compact, we find that the greatest disclosure of information regarding the proposal is primarily on environmental issues (51%). This is due to increased information available from the application in most institutions of environmental management systems, particularly in the larger ones, and as a consequence of the widespread sensitivity about reducing energy, water and paper consumption, as well as waste management.

However, it is noteworthy that the proposal referred to the possibility that institutions report on the results of comparisons with international initiatives such as the Association for the Advancement of Sustainability in Higher Education (AASHE) and Green Campus Report Card 1 in the United States or the Higher Education Funding Council for England (HEFCE), not having found any information in this regard, which leads us to believe that the Spanish universities are not in line with the international initiatives in this field.

For information related to Human Rights, we would like to highlight that the majority refers to the attention to the right to non-discrimination and the right to freedom of expression and association, which is not surprising considering that Spain is the reference in terms of availability of information from application of the principles.

We found the lowest disclosure of information in the area of Labor. One would expect greater disclosure of aspects related to health risks and well-being, as well as forced labor, but the institutions have not thought it necessary to provide information in this regard on finding themselves in a context in which all these aspects are highly regulated. However, we would like to emphasize the increased attention given to aspects about Disability Issues and Compliance, and those actions carried out in favor of work–life balance, perhaps as a consequence of increased pressure from stakeholders at this time.

The other area in which it is necessary to continue advancing is in the fight against corruption. In general, risks have not been identified and information is lacking as a consequence of the public institutions’ belief that there is either a lot of regulation and control of activity or because the private institutions rely on their teams in corporate governance. Codes of conduct and values are present in all of the institutions, and in the majority, there is even a channel for complaints or an ethics hotline, in addition to having identified responsible purchasing policies as a control instrument or referring to responsible criteria during a purchase.

In general, it is necessary to highlight the lack of analysis of the implementation of the various aspects for students, contrary to what one might think given the mission of institutions analyzed.

Process Analysis

The identification of the activities related to the stages of a control process in the COP results in all institutions in general referring to the different actions (see Table 5).

Results of the Management Control Process Analysis.

Note. DCP = developing country projects; GRI-C = Global Reporting Initiative, Level C; COP = Communication on Progress; PRME = Principles for Responsible Management Education.

All institutions, except Grupo Valero, followed the proposal made by Global Compact. For this reason, all but this institution includes the indicators proposed by this initiative as well as the relation of the GRI indicators to the information provided in the report so as to obtain the GRI Level C classification.

The Grupo Valero report differs from the rest in that it does not provide indicators similar to the others nor reference to GRI. This does not necessarily imply that they do not follow their own management control system nor provide information in this regard through other reports.

Despite following the steps of the control process, we found that information is disclosed without analyzing the connection between the goals of institutions (usually not explicit in this report but reference is made to the corresponding instrument or there is a link to the other document) and the actions described and proposed corrective actions.

With regard to adherence to PRME, of the 14 institutions analyzed, only 5 state they are adhered to this initiative, with some having been very recent, which leads us to believe that it is necessary for Spanish universities to advance in their knowledge and integration in their management control systems to better manage their impacts on stakeholders, as this initiative is specific to education.

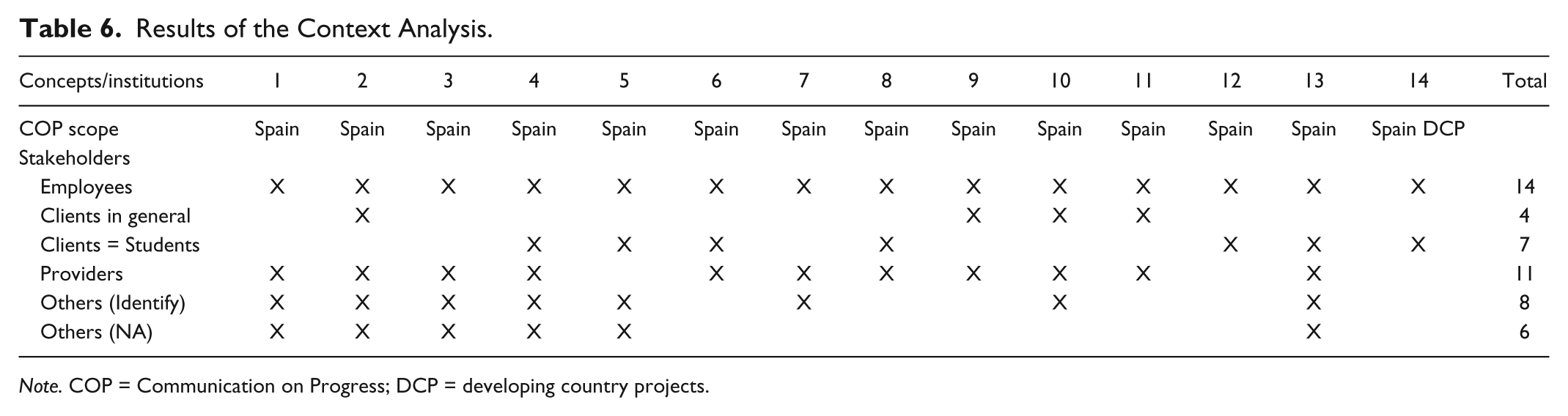

Context Analysis

The institutions analyzed exclusively reveal information relating to the application of the Global Compact principles in Spain, although, as seen in Table 5, they are active not only in Spain but some of them also participate in or carry out projects in developing countries. We found only one case, The College for International Studies (CIS), in which they apply the principles to their Mozambique Service Project, perhaps because it is formed by an NGO (non-governmental organization).

As seen in Table 6, the institutions analyzed define their stakeholders in a clear and accurate manner. In general, all identified employees as one of them, but not all make the effort to specify their actions regarding students or alumni despite being educational institutions.

Results of the Context Analysis.

Note. COP = Communication on Progress; DCP = developing country projects.

For providers, consideration prevails for the majority of them, perhaps influenced by the Global Compact Principle 2 that makes a special reference to the need to respect their rights. This in turn highlights the need for some institutions, especially smaller ones, to make the effort to clarify their responsibility in this area.

It is noteworthy that most of the institutions that identified stakeholders as “Other” did not consider them in their management process, or at least did not disclose information in this regard (nor instruments, actions, or corrective measures), as seen in the results in the row that refers to the lack of implementation of “Other.”

In general, universities have started to be transparent about how they are managing their impacts with the drafting of the COP but have a long way to go as shown on the Global Compact website. This is due to either a lack of transparency on formalizing their adhesion to the initiative but not drafting the COP or to a lack of continuity in its development.

Conclusion

The increased demand from society for educational institutions to be socially responsible and assume their role for their management as organizations and as part of the training process for society has led us to analyze how Spanish universities are managing their impacts on stakeholders.

Universities, like other organizations, adhere to the Global Compact principles because they believe they can help them in their management and thus can gain a competitive advantage (Carlson, 2008).

The information on compliance with the Global Compact principles that is being provided can be a benchmark for analyzing universities’ sustainability approach, and set an example for other institutions in the education and research sector, to improve accountability. However, we consider it necessary to promote a common SR policy management format for universities, an integration of UN initiatives (Global Compact and PRME), along with other international initiatives, to favor and facilitate the implementation of sustainability criteria.

The 2012 Global Compact proposal is much more comprehensive than the initial COP proposal that universities follow, which was based on the 2011 report that suggested a format for all organizations.

The main institutions analyze their employees as stakeholders, without distinguishing between the functions of teaching and research. There is practically no mention of the “student” stakeholder and if mentioned, it is from the point of view of education that is offered on some aspects of SR.

The proposal of the COP to serve the phases of assessing, defining, implementing, and measuring impacts is a success because it facilitates and guides the institutions on the process of analyzing the level of integration of management principles.

It is, however, necessary to have a clear distinction of the issues that are included in each of the four areas against an analysis by principles to avoid redundancy or overlap between them, as there are aspects such as health and safety that are reflected in different areas.

Some institutions mentioned the difficulty of knowing all the information about the management of SR, which highlights the importance of improving the management of SR transversely.

In many aspects, the institutions declare no risk. In line with the conclusions found by Ayuso and Mutis (2010), we can see that the institutions are not aware of the risk of default of the principles in developed countries and the importance of identifying best practices to meet the demands of stakeholders beyond legal obligations.

As a result of the lack of integration between goals, actions, and corrective measures, we believe it is necessary to advance in this direction in the dissemination of information in line with what is being done on an international level toward integrated reporting (International Integrated Reporting Council [IIRC], 2011; KPMG, 2010) so that the stakeholders can have a clear vision of how the universities are managing their impacts.

Footnotes

Appendix

Frequency Analysis of Disclosure in Relation to the Proposal for HEI

| Institutions | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 | 11 | 12 | 13 | 14 | Total |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Human Rights (21) | |||||||||||||||

| Student admissions | 0 | 0 | 1 | 0 | 0 | 0 | 0 | 1 | 1 | 0 | 0 | 0 | 0 | 0 | 3 |

| Safe and healthy work and study conditions | 1 | 0 | 0 | 2 | 0 | 1 | 1 | 2 | 1 | 2 | 2 | 1 | 0 | 0 | 13 |

| Non-discrimination | 3 | 2 | 4 | 2 | 2 | 2 | 2 | 4 | 3 | 3 | 3 | 2 | 3 | 2 | 37 |

| Freedom of expression and association | 3 | 1 | 3 | 3 | 3 | 3 | 3 | 3 | 3 | 3 | 3 | 2 | 3 | 2 | 38 |

| Diversity: Accommodation (allowance) of differences | 1 | 1 | 1 | 1 | 1 | 1 | 1 | 1 | 1 | 1 | 1 | 1 | 1 | 2 | 15 |

| Fair decision-making practices | 2 | 0 | 2 | 4 | 0 | 2 | 2 | 2 | 2 | 3 | 3 | 2 | 2 | 1 | 27 |

| Respect of local cultures/intercultural learning | 0 | 1 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 1 | 2 |

| Subtotal: Rights | 10 | 5 | 11 | 12 | 6 | 9 | 9 | 13 | 11 | 12 | 12 | 8 | 9 | 8 | 135 |

| Disclosure degree: Rights | 48% | 24% | 52% | 57% | 29% | 43% | 43% | 62% | 52% | 57% | 57% | 38% | 43% | 38% | 46% |

| Labor (18) | |||||||||||||||

| Freedom of association for staff and students | 1 | 1 | 1 | 1 | 1 | 1 | 1 | 1 | 1 | 1 | 1 | 1 | 1 | 1 | 14 |

| Forced/compulsory labor controversies | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 |

| Commitment to fair trade | 0 | 0 | 0 | 0 | 0 | 0 | 1 | 1 | 0 | 1 | 0 | 1 | 0 | 0 | 4 |

| (Sub-) contracted labor policies | 0 | 0 | 0 | 0 | 0 | 1 | 0 | 1 | 1 | 1 | 1 | 1 | 0 | 0 | 6 |

| Disability issues and compliance | 1 | 0 | 0 | 1 | 1 | 1 | 1 | 1 | 1 | 1 | 1 | 1 | 1 | 0 | 11 |

| Student labor policies | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 1 | 0 | 0 | 0 | 1 |

| Hiring and advancement practices/policies discrimination | 0 | 0 | 1 | 1 | 0 | 1 | 1 | 1 | 1 | 1 | 1 | 1 | 1 | 1 | 11 |

| Work–life balance | 1 | 1 | 2 | 1 | 2 | 2 | 2 | 2 | 1 | 1 | 2 | 1 | 1 | 1 | 14 |

| Workplace health and safety issues | 2 | 0 | 1 | 1 | 1 | 4 | 2 | 2 | 2 | 2 | 2 | 1 | 0 | 0 | 20 |

| Subtotal: Labor | 5 | 2 | 5 | 5 | 5 | 10 | 8 | 9 | 7 | 8 | 9 | 7 | 4 | 3 | 81 |

| Disclosure degree: Labor | 28% | 11% | 28% | 28% | 28% | 56% | 44% | 50% | 39% | 44% | 50% | 39% | 22% | 17% | 32% |

| Environment (18) | |||||||||||||||

| Environmental footprint: Programs and policies | 4 | 3 | 4 | 5 | 5 | 5 | 5 | 5 | 4 | 5 | 5 | 3 | 6 | 1 | 60 |

| Green/responsible purchasing practices | 0 | 0 | 1 | 0 | 0 | 1 | 1 | 1 | 1 | 1 | 1 | 0 | 0 | 0 | 7 |

| Waste removal and treatment | 1 | 1 | 1 | 1 | 1 | 1 | 1 | 1 | 1 | 1 | 1 | 1 | 1 | 0 | 13 |

| Pollution | 0 | 0 | 0 | 0 | 1 | 0 | 0 | 0 | 1 | 1 | 0 | 1 | 0 | 4 | |

| Natural resources/energy preservation | 2 | 2 | 2 | 2 | 3 | 2 | 2 | 2 | 2 | 3 | 3 | 3 | 3 | 1 | 32 |

| Climate change issues | 0 | 0 | 0 | 0 | 1 | 1 | 1 | 1 | 0 | 0 | 1 | 0 | 0 | 0 | 5 |

| Biodiversity (on and off campus) | 0 | 0 | 1 | 0 | 1 | 1 | 1 | 1 | 1 | 1 | 1 | 0 | 0 | 0 | 8 |

| Compare with existing tools for higher education | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 |

| Subtotal: Environment | 7 | 6 | 9 | 8 | 11 | 12 | 11 | 11 | 9 | 12 | 13 | 7 | 11 | 2 | 129 |

| Disclosure degree: Environment | 39% | 33% | 50% | 44% | 61% | 67% | 61% | 61% | 50% | 67% | 72% | 39% | 61% | 11% | 51% |

| Anti-Corruption (21) | |||||||||||||||

| Financial transparency and accountability | 2 | 0 | 2 | 1 | 0 | 1 | 1 | 2 | 1 | 0 | 0 | 2 | 1 | 0 | 13 |

| Responsible purchasing practices | 1 | 1 | 1 | 1 | 0 | 1 | 1 | 1 | 1 | 1 | 1 | 1 | 1 | 1 | 13 |

| Recruitment and admissions/selection | 0 | 0 | 0 | 0 | 0 | 1 | 1 | 2 | 2 | 3 | 3 | 1 | 1 | 1 | 15 |

| Contracting and policy | 1 | 1 | 1 | 1 | 0 | 1 | 1 | 3 | 1 | 1 | 1 | 0 | 1 | 0 | 13 |

| Research and human subject-related issues | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 1 | 0 | 0 | 0 | 1 |

| Assessment challenges—for students, faculty, researchers, etc. | 0 | 0 | 2 | 0 | 0 | 0 | 0 | 1 | 0 | 0 | 0 | 0 | 2 | 0 | 5 |

| Intellectual property issues | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 |

| Fraud prevention practices | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 1 | 1 | 1 | 1 | 0 | 1 | 0 | 5 |

| Transparency in promotion and tenure | 0 | 0 | 0 | 0 | 1 | 1 | 1 | 1 | 1 | 1 | 0 | 1 | 0 | 7 | |

| Fair–due process | 2 | 2 | 2 | 1 | 1 | 2 | 2 | 2 | 2 | 2 | 2 | 1 | 2 | 1 | 24 |

| Subtotal: Anti-Corruption | 6 | 4 | 8 | 4 | 1 | 7 | 7 | 13 | 9 | 9 | 10 | 5 | 10 | 3 | 96 |

| Disclosure degree: Anti-Corruption | 29% | 19% | 38% | 19% | 5% | 33% | 33% | 62% | 43% | 43% | 48% | 24% | 48% | 14% | 33% |

| Total (78) | 28 | 17 | 33 | 29 | 23 | 38 | 35 | 46 | 36 | 41 | 44 | 27 | 34 | 16 | 441 |

| Disclosure degree: Total HEI proposal | 36% | 22% | 42% | 37% | 29% | 49% | 45% | 59% | 46% | 53% | 56% | 35% | 44% | 21% | 40% |

Note. HEI = Higher Education Institution.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research and/or authorship of this article.