Abstract

This article critiques the mainstream management control theory with a view to highlighting its gaps and to suggesting a direction for its future development. Management control theory has undergone lopsided development due to the dominance of accounting-based approaches to the study of management controls. Thus, management control theory has failed to explain complex issues that are interwoven with deep-rooted, sociocultural context within which these issues emanate. Although the influence of organizational theory, particularly systems theory, cybernetics, and contingency theory, resulted in a marginal outward shift of the boundaries of the mainstream management control theory, the main drawbacks of the theory remained unresolved. Alternative theoretical perspectives rooted in disciplines such as political economy, sociology, and anthropology can enrich the mainstream management control theory. Management control issues emanating from non-Western contexts would remain largely unexplained or poorly explained, unless alternative theoretical perspectives were used.

Keywords

Background

The mainstream management control theory known as classical theory originated and evolved in an accounting-dominant environment. Except for few nonaccounting approaches to the theory, accounting perspectives continue to dominate. As a result, management control theory has undergone lopsided development. An important implication of this is that the mainstream management control theory has failed to explain complex issues that are interwoven with sociocultural aspects unique to non-Western countries. Objectives of this article are twofold. First, the article provides a critique to the mainstream management control theory showing its origin, evolution, and gaps. Second, it argues for alternative theoretical perspectives to bridge these gaps.

Rest of the article is organized into five sections. First, the term management control is explained from diverse perspectives with a view to illustrating its multifacedness. Second, the main tenets of the mainstream management control theory are reviewed highlighting the genesis, development, and gaps. Third, the influence of organizational theory on management control theory is elaborated with a view to mapping the direction of management control theory. The main aim of this exercise is to illustrate the underdeveloped areas of the theory. Fourth, alternative theoretical perspectives are suggested followed by concluding comments.

Management Control: Multiple Perspectives

Management control is a generic term for a wide range of formal and informal approaches and mechanisms that aim to regulate the behavior of members of an organization. It is the process of assuring that resources are obtained and used effectively and efficiently in the accomplishment of an organization’s objectives (Anthony, 1965). Formal management control mechanisms include organizational structure, reward systems, budgeting, standard operating rules and procedures, strategic planning systems, and operational controls. Informal techniques comprise leadership, culture, values, and norms (Macintosh, 1994). The term organizational controls is used to denote management controls that generally comprise technical controls, such as management accounting controls and other nonaccounting controls (Chenhall, 2003). Management controls in its plural meaning connote a collection of control systems aimed to achieve management control. The term management control systems is also used to denote the interrelated whole of controls in an organization. Although managers do other things, the exercise of control is a dominant part of the manager’s job (Alvesson & Karreman, 2004; Mintzberg, 1989; Tangbald, 2001). Management control has been defined in numerous ways, and most definitions stress the exercise of influence to secure sufficient resources, and to mobilize and orchestrate individual and collective action toward given ends (Alvesson & Karreman, 2004; Langfield-Smith, 1997). Management control generally includes a mechanism for specifying, monitoring, and evaluating individual and collective action.

From a sociological perspective, management control is seen as the process by which managers influence other members of an organization to implement the organization’s strategies (Anthony & Govindarajan, 1998; Flamholtz, Das, & Tsui, 1985; Ouchi, 1977). Power and influence are instrumental in effecting control over employee thoughts and actions, and they form an integral part of management control. Regulation and control of employee behavior require diverse forms of power and influence. For example, Anthony and Govindarajan (1998) described management control as the process by which managers at all levels ensure that people whom they supervise implement their intended strategies. Macintosh (1994) emphasized the instrumentality of management control in motivating, monitoring, and measuring the sanctions and actions of managers and employees. Motivating, monitoring, and measuring functions are considered indispensable for the effective control of organizational activities.

From an organizational performance perspective, management control can be viewed as a distribution of means used by an organization to elicit the performance it needs and to check whether the quantities and qualities of such performances are in accord with organizational specifications (Etzioni, 1960). Management control is used to regulate behavior of organizational members so that organizational goals are accomplished with minimum use of resources. As it is argued that organizational effectiveness, measured by goal accomplishment, is largely dependent on similarity of individual and organizational goals (Anthony & Govindarajan, 1995), it can be said that this synchronization is made possible through management control.

From an information management perspective, management control defines the decision space of the individuals within an organization to affect their behavior (Brinberg & Snodgrass, 1998). Management control enables organizations to increase the probability that employees make decisions and take actions that are in the organizations’ best interest (Chow, Shields, & Wu, 1999). It can be argued that central to all controls is the information that links managers and employees. Information systems and control systems are found to be interwoven. For example, Simons (1995) viewed management control as formal, information-based routines and procedures that managers use to maintain or alter patterns in organizational activities.

In general, it can be said that management control encompasses the human and technical (machines and processes) systems of an organization. The harmonious functioning of both of these systems tends to ensure the achievement of organizational aims with minimum deviations. However, the control of human behavior may pose complex management issues, as reactions to the same stimuli are likely to produce variable responses depending on the unique social, cultural, and political context and on organizational and individual differences. Personal goals of employees and managers can differ from organizational goals, and therefore the task of management control is largely to achieve synchronization of personal and organizational goals. Based on this, I argue that management control can be viewed as a process involving the controller, the controlled, and the method of control. The space within which this process operates can be regarded as the control environment or control context. It can be said that the controller, the controlled, and the method of control are connected through a chain of power, authority, rules, regulations, norms, values, and information within the boundary of the control context. The aggregate of the relationships between the controller, the controlled, the method of control, and the control context can collectively be referred to as management controls. Figure 1 illustrates the proposed relationships among these concepts.

Elements of management control

Genesis of Mainstream Management Control Theory

Management control theory is a relatively young body of knowledge. Although some traits of early works on management control are found in the management literature (Chua, Lowe, & Puxty, 1989), the seminal theoretical work of Robert Anthony (1965) is said to have laid the foundation for modern management control theory (Otley, 1994) and is commonly referred to as the classical model or classical theory (Berry, Broadbent, & Otley, 2005). Anthony distinguished management control from strategic planning and operational control. He viewed management control as an intermediate function that was sandwiched between the process of strategic planning and operational control, and all these processes were assumed to be located in the distinct levels of the organizational hierarchy showing the managerial levels in which they operate (Otley, Broadbent, & Berry, 1995). Anthony stated that management control was needed to link strategic and operational levels. This, in his time, was considered to be a major theoretical contribution as it supported a clear demarcation of the domain of management control theory (Chenhall, 2003; Otley, 1994). One advantage of this view could be that it facilitated the study of management control as a middle level (in between strategic and operational levels) organizational process.

Anthony’s idea of control mainly revolved around fixing responsibility centers (revenue, expenses, and profit) as a means of control by the manager over worker behavior. One implication of this was that it promoted accounting-based controls (Puxty, 1989). The management control techniques suggested by Anthony consisted of programming and budget preparation, analyzing and reporting financial performance and executive incentive compensation plans (Chenhall, 2003; Hopper & Powell, 1985; Otley et al., 1995). The issues that were addressed in Anthony’s accounting-based controls were the utilization of accounting performance measures to control large diversified firms, in particular, the construction of responsibility centers using a system of cost allocation. This tendency may have been caused by the fact that the large multidivisional, Anglo-American industrial organizations were used as the basis for developing this framework.

This accounting-based approach to management control was, it was argued, rightly suited to the upper echelons of large hierarchical organizations involved in manufacturing during the 1960s (Otley, 1994). This was evidenced by the types of accounting-based research carried out by management control researchers during this period. For example, dimensions of budgeting such as participation, importance of meeting budgets, formality of communication and systems sophistication, links to reward systems, budget slacks (hidden buffers), variance analysis, activity-based costing, activity-based management, accounting performance measures, capital budgeting, and strategic interactive controls were representative areas of accounting-based management control research utilized at that time (Burns & Waterhouse, 1975; Dunk, 1993; Emsley, 2000; Merchant, 1981, 1985; Van der Stede, 2000; also see Chenhall, 2003, for a detailed review).

A main assumption underlying classical management control theory was that economic activities in the developed industrial societies were organized into well-bounded corporations in which managers coordinated the work and subunits through systematic rules and procedures (Whitley, 1999). The main task of the management control system in these organizations was to ensure that the work activities and subunits conformed to the top managers’ objectives and to supply the information to enable the managerial hierarchy to correct any deviations from set plans. The controllers were assumed to be the elite group at the apex of an administrative pyramid acting in the interest of organizational efficiency and effectiveness (Whitley, 1999).

The relationship between owners, managers, and workers was largely seen from the principal–agent perspective. This principal–agent relationship was a main theoretical foundation of the classical theory and it was largely derived from neoclassical economics (based on the concept of rational maximizing economic agent; Scapens, 1994). Agency theory (Baiman, 1990; Jensen & Meckling, 1976) was frequently used by early researchers to explain the principal–agent dynamics that underlined management control issues. Therefore, it is necessary to examine the main concepts that underpin agency theory to gain insights into its impact on management control theory.

Agency theory assumes a world of two-person explicit or implicit contracts between owner and employee in which both parties behave in a rational utilitarian manner motivated solely by self-interest. It illustrates the agency relationship manifested as a contract under which the owner or principal delegates decision-making authority to the manager or agent who performs services on behalf of the owner. Agency theory holds that being a utility maximizer, the agent will not always act in the best interest of the owner, and therefore the owner needs auditing, accounting, and other controlling methods to regulate the behavior of the agent (Macintosh, 1994). It is assumed that the information systems of an organization, thus, are needed to provide necessary information to the owner to achieve management control. The contractual relationship between the owner and manager or employee is assumed to be influenced by factors such as self-interest, adverse selection, moral hazard, incentive schemes, asymmetric information, and signaling (Macintosh, 1994). The self-interest of the agent (manager or employee) creates the need for control, as the owner’s interest may not be congruent with that of an agent. The agents are assumed to be self- serving and opportunistic (Chenhall, 2003). Thus, it is argued that the accounting-led controls were necessary to safeguard the interests of the owner against possible self-interest mismatches between the owner and the manager (Macintosh, 1997). The incentive schemes are, therefore, needed to induce managers or employees (agents) to conform to the desirable behavior that is needed to achieve organizational objectives (wishes of the principal).

Agency theory, however, has been viewed as inadequate in the sense that it focused solely on the simple contractual relationship between principal (owner) and agent (manager or employee). It has been argued that the intricate power relations between the principal and agent have been omitted by agency theory (Armstrong, 1991). For example, the power struggle between owners and managers tends to determine the nature of principal–agent relationship. Neglect of this phenomenon could be considered an important gap in agency theory. Furthermore, the agency theory perspective was criticized on the ground that it did not consider the context in which principals and agents contract (Merchant & Simons, 1986; Shields, 1997). For example, the historical, cultural, political, and social contexts within which the principal–agent contract is entered into tend to have a strong influence over the outcome of the contract.

Drawbacks of the Mainstream Theory

Dependence on an accounting-based approach invited numerous criticisms to the classical (pioneered by Anthony) management control theory. For example, Parker (1986) criticized accounting models for offering only an imperfect reflection of the management model of control. The most influential criticisms of this classical model were offered by Hofstede (1978) and Lowe and Puxty (1989). Hofstede (1978) criticized its incapacity to capture social and psychological aspects of management control. Lowe and Puxty emphasized the problem of the narrow focus of management control theory due to its strong accounting orientation. Otley’s (1994) criticism was based on the argument that Anthony’s overemphasis on responsibility centers where a single manager can be held accountable for the performance of his or her division was not practical. According to Otley, the concept of independence of responsibility centers was not valid, as a considerable degree of interdependence among various departments exists in practice. This criticism could be viewed as an important drawback of the classical theory as a main premise of Anthony’s classical theory, the responsibility center control, was argued to be too simplistic.

Regarding the responsibility centers, the principle of accountability was used to hold managers accountable for only those activities which could be controlled by them. However, it is argued that in practice, managers are held accountable for activities outside of their control (Whitley, 1999). For example, in an actual work scenario, to effectively perform a job function, a manager may be required to perform certain tasks that are not included in his job tasks. In this case, it may not be realistic to focus on strictly defined responsibility centers. This tends to negate the practical validity of the principle of responsibility centers as proposed by Anthony. Even in this decade, the management control literature is not free from the drawbacks of the overemphasis of accounting controls. This is illustrated by Whitley (1999):

This approach has been criticised for being too narrow, for assuming managerial consensus over objectives, for taking worker acquiescence and passivity for granted and for generating universal-recipes when it has become increasingly clear that patterns of work organisation differ greatly across sectors, regions and countries, as does the nature of firms and economic actors more generally, in ways that have significant consequences for how economic activities are coordinated and controlled. (p. 508)

Apart from being too accounting oriented, classical theory has been criticized for limitations that were partly caused by its association with organizational theories, such as systems theory, which are discussed below.

Influence of Organizational Theory on Management Control Theory

Management control theory was strongly influenced by organizational theory. It appears that the management control theory has passed three distinct periods of evolution, namely, classical management era, modern control theory dominated by accounting, and the postaccounting era. Table 1 depicts key contributors and their contributions at each time period.

Three Distinct Periods of Evolution of Management Control Theory

During the period when Anthony’s accounting-based approach to management control gained popularity (1960s), the organizational theory literature largely inclined toward a systems theory perspective (Chua et al., 1989; Hopper & Powell, 1985). This tendency influenced management control theory and it (management control theory) became inseparable from organizational theory in general and systems theory in particular (Otley et al., 1995). To understand the depth of influence that systems theory had on management control theory, it is necessary to discuss the main tenets of systems theory. Moreover, it is important to examine the key aspects of the systems perspective as it influenced the way in which classical theory evolved. The systems perspective was rooted in cybernetics and general systems theory (GST). Norbert Wiener’s (1948) cybernetics concept explains the process of communication and control among people and machines to attain desirable objectives and to map the self-regulating principles found in human biological systems onto machines systems (Berry et al., 2005). Cybernetics is concerned with automatic regulation and control of organisms and organizations. It is said that cybernetics uses a negative feedback loop represented by setting goals, measuring achievement, comparing achievement with goals, feeding back information about unwanted variances into the process to be controlled, and correcting the process (Hofstede, 1978). According to this view, a management control process in its most simplified form is similar to a technical control process, resembling the control of the heat of a room by a thermostat (Hofstede, 1978). Anthony’s accounting control ideology was easily interwoven with the concept of cybernetic controls.

However, the GST seeks to explain behavior by studying the interrelationship of parts rather than the nature of those parts. A system is a collection of interrelated parts working as a whole. Specifically, a system is an organized or complex whole; an assemblage or combination of things or parts forming a complex or unitary whole (Mockler, 1970; Skyttner, 1996). An organization, therefore, can be considered a collection of interrelated parts working as a whole. There may be different subsystems that can be connected to form much larger systems. The systems perspective holds that to fully understand the function of the whole system, the interrelationships among different components have to be understood. A system is said to have a boundary, and depending on the level of interaction by the system with its outer boundary, a system can be considered either an open system or a closed system (if it does not interact with the environment). From the system perspective, an organization is composed of input, process, and output components, as well as connected subsystems with a clearly defined system boundary. As evident from the literature, the system theorists and the cyberneticians joined both theories to explain functions of organizations and more specifically the function of management control systems. The extent of the influence by cybernetics theory on management control studies was so evident that a review of management control articles published in books and journals between 1900 and 1972 revealed that all these articles were based on cybernetics paradigm (Berry et al., 2005).

The systems theory perspective together with cybernetics was extensively used in understanding complex organizational interrelationships, the way organizations adapt and respond to their environment, the influence of environmental contingency factors on organizations, and goal-seeking behavior of organizations. It was argued that the systems theory approach contributed to the study of management control in various ways (Berry et al., 2005); for example, it aided analysis of management control in organizations, developing a theory of management control and understanding of other approaches to management control such as open systems and sociotechnical systems approaches used in organization theory. It can be said that GST strongly influenced the philosophical and theoretical underpinnings of management control theory. As such, management control theory derived from these theoretical underpinnings was often referred to as mainstream management control literature (Hopper & Powell, 1985; Otley et al., 1995; Parker, 1986; Scott, 1981).

Mapping the Direction of Management Control Research From Systems Theory Perspective

Given the pervasiveness of the systems perspective in management control theory and research, the systems theory perspective can be used to map the direction of management control research. By doing this, I intend to highlight the gaps in the mainstream (classical) management control theory.

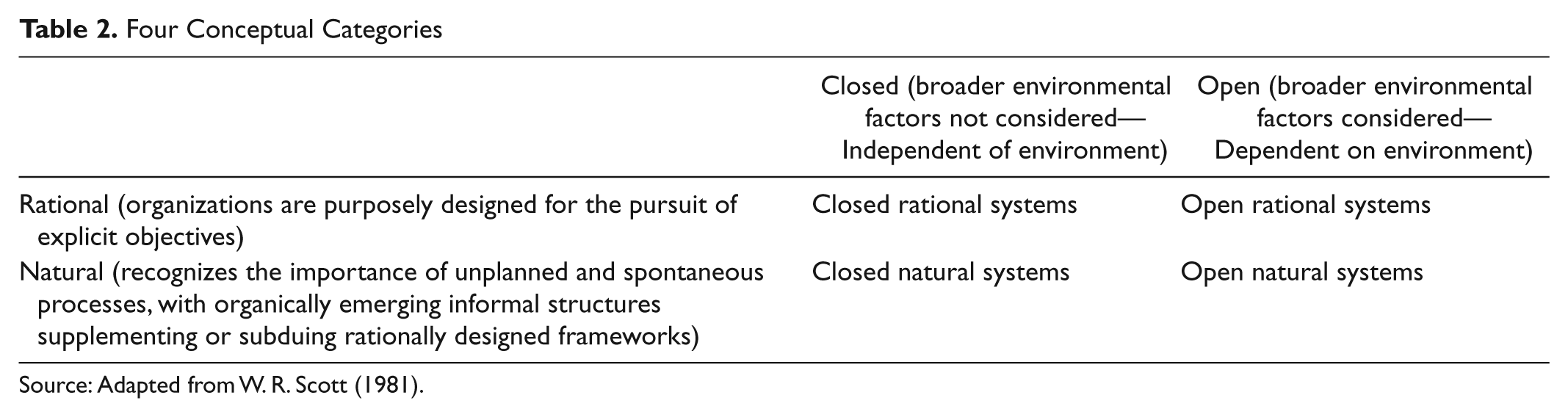

As has been stated earlier, systems can be rational, natural, open, or closed (Otley et al., 1995; Scott, 1981). By combining these four concepts, four distinct conceptual categories can be identified (Otley et al., 1995). They are closed rational systems, closed natural systems, open rational systems, and open natural systems (Table 2).

Four Conceptual Categories

Source: Adapted from W. R. Scott (1981).

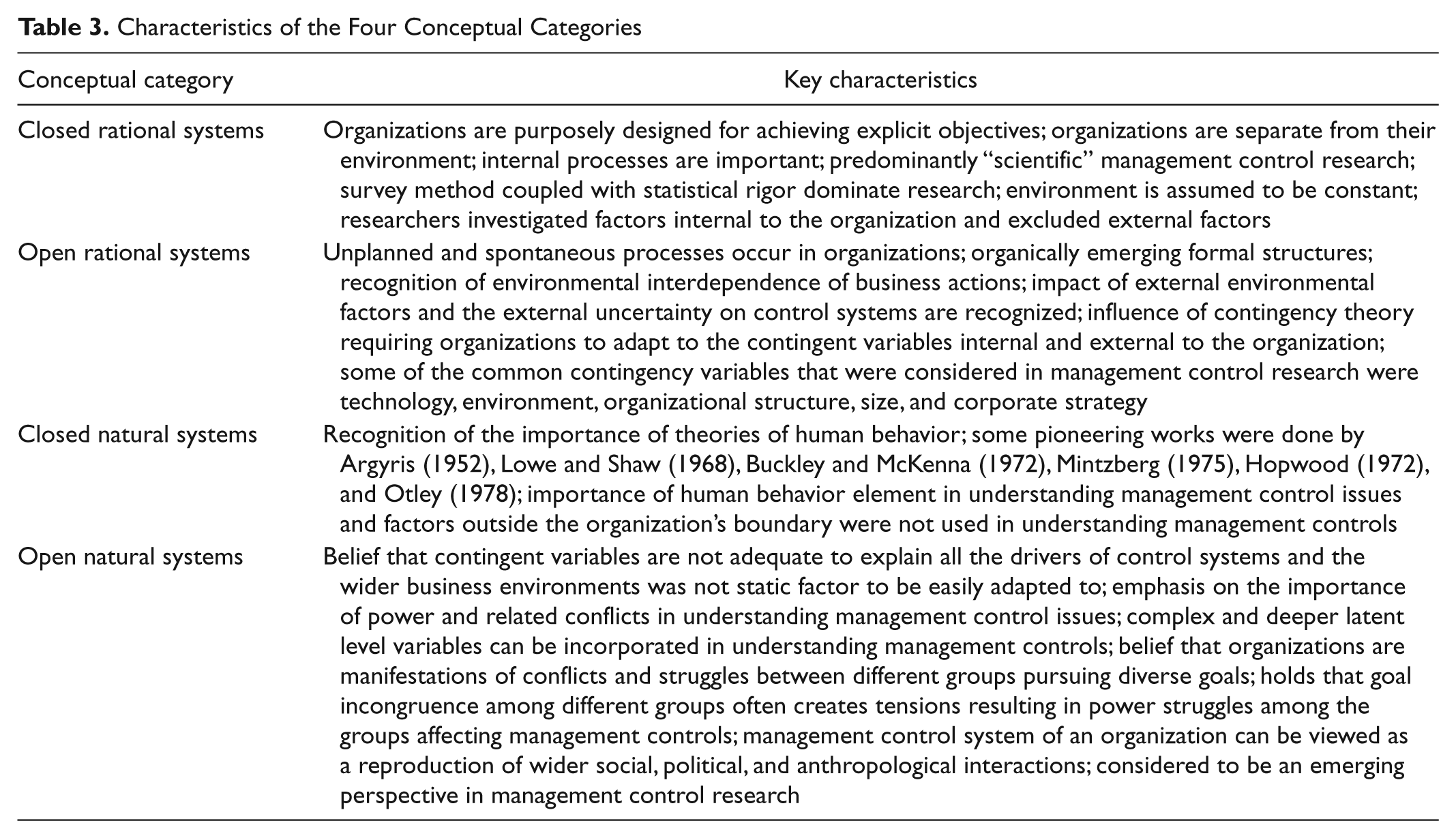

Table 3 details the defining characteristics of the four conceptual categories.

Characteristics of the Four Conceptual Categories

The open natural systems perspective can be considered an emerging perspective in management control research. This may be attributed to two main reasons. First, researchers using this perspective call for a wider social theoretical approach to form conceptual frameworks to better understand management control issues. Second, they argue for alternative research methodologies that can better explain deep-rooted, complex management control issues. Recent trends in the literature have provided evidence to confirm this (e.g., Ansari & Bell, 1991; Bhimani, 1999; Bijlsma-Frankema & Koopman, 2004; Cowton & Dopson, 2002; Efferin & Hopper, 2007; Hewege, 2006, 2007; Hopper, Tsamenyi, Uddin, & Wickramasinghe, 2009; Macintosh & Hopper, 2005; Macintosh & Scapens, 1991; Uddin & Tsamenyi, 2005; Wickramasinghe & Hopper, 2005; Wickramasinghe, Hopper, & Rathnasiri, 2004).

The Way Forward: Justification for Alternative Theoretical Approaches

As a response to the criticisms leveled against classical theory, non-accounting-based approaches to study management control began to emerge. It seemed that the overreliance on accounting controls triggered management control researchers to broaden the scope of their research by encompassing interdisciplinary and multidisciplinary perspectives such as anthropology, social theory, organization theory, and development economics.

Hopwood (1974) pioneered the nonclassical or modern tradition calling for different approaches to study management control issues other than the accounting approach that had the underpinning of the systems theory approach. He emphasized the social and self-control aspects of management control. In doing so, Hopwood provided a link between the classical theory and the sociological and psychological ideas in the organization theory literature more generally (Berry et al., 2005). Following Hopwood, Etzioni (1960) and Ouchi (1979, 1980) further contributed toward this end by introducing management control concepts based on social and psychological aspects of employee behavior.

With the advent of the social perspective into the management control literature, the deficiency of the accounting-based approach became more prominent. It was argued that the management control literature did not include much broader and appropriate theoretical and methodological insights (Chua, 1986; Chua et al., 1989; Cowton & Dopson, 2002; Hopper et al., 2009; Whitley, 1999). These researchers argued that management control represented the surface-level manifestations of much deeper issues rooted in the social, cultural, historical, and anthropological aspects of organizations and that to have a comprehensive understanding of the way in which management controls operate, these variables needed to be included in research frameworks. Given this argument, the inadequacy of the classical theory has become much prominent.

First, perspectives such as power, conflicts, and social and organizational anthropology require theoretical models different to the cybernetic model. As explained earlier, it is clear that systems theory and cybernetics clearly demarcated the boundary of the organization’s internal operations and the external environment. Management control research using systems and cybernetics approaches treated deeper social and cultural issues as contingency variables that belonged to the external environment. This led to the preclusion of these variables from management control studies.

The contingency research approach (based on contingency theory) that emerged with the open system theory approach and that dominated the management control research until recently appeared to have loosely considered the deep-rooted cultural, social, political, and anthropological contextual factors affecting management controls of non-Western nations (Efferin & Hopper, 2007; Hewege, 2011; Hopper et al., 2009). Contingency theory considered contextual variables only at the organizational level, not at the extraorganizational level. The main criticism of the contingency research approach is its neglect of the importance of social processes and subjective meanings of actors within the context of management control (Chenhall, 2003; Hoque & Hopper, 1997). As such, the need for a new approach has been reiterated in recent literature. For example, Cowton and Dopson (2002) explained,

The study of management control has been undergoing a series of significant challenges and reorientations in recent years. Two strands have been particularly evident in this process of reorientation. First, there has been a concern to investigate the ways in which management control actually takes place in organisations . . . Second, often recognising the need for, and indeed inevitability of, conceptual lenses drawn upon a variety of theories with the social sciences. (p. 191)

The preclusion of deeper contextual variables such as sociocultural, political, and anthropological processes in understanding management control rendered classical theory-based contingency research inadequate. Given the argument that management control theory has suffered from an “impoverished philosophy” (Hofstede, 1978) and has developed quite narrowly, research using broader philosophical and theoretical frameworks is considered timely. To support this claim, Chua et al. (1989) stated that management control studies needed to capture social and (or) moral conditions under which management controls operate and the issue of power and conflicts. Furthermore, Cowton and Dopson (2002) expressed that the management control studies should not ignore the issue of power and conflict and should not treat organizations as unitary entities with well-defined and essentially agreed purposes. To realize these aims, diverse alternative theories are required. Some of these salient theories are explained below.

Alternative Theories

As a response to the call for broader theoretical perspectives, recent years have witnessed the development of alternative theoretical perspectives on management control. These studies have addressed issues of power, conflict, and culture with sufficient depth using extant social theories, namely, Foucauldian theory of power (Hopper & Macintosh, 1993; Roberts & Scapens, 1985; Walsh & Stewart, 1993), structuration theory of Giddens (Conrad, 2005; Roberts & Scapens, 1985; Uddin & Tsamenyi, 2005), theories of political economy (Alam, 1990; Armstrong, 1987; Hopwood & Miller, 1994; How & Alawattage, 2012; Neimark & Tinker, 1986; Uddin & Hopper, 2001; Wickramasinghe & Hopper, 2005), and anthropology (Ahrens & Mollona, 2007; Efferin & Hopper, 2007; Hewege, 2011).

As an alternative theory, structuration theory has been used (Macintosh & Scapens, 1990, 1991; Roberts & Scapens, 1985) to study the influence of power relations on management controls. In particular, the suitability of this theory to study organizations in developing countries rests on its ability to reveal social and political structures that often dominate rational decision-making processes in these environments (Larbi, 2001; Schick, 1998). According to structuration theory, power is domination derived from the command over resources. This gives individuals or groups the facility that eventually creates power in their relations with others. There are two types of resources: allocative and authoritative. The allocative resources are material resources, whereas authoritative resources are nonmaterial ones derived from the capability of harnessing the activities of human beings. These resources are the media through which power is exercised. Power is a dialectical control process that involves a two-way affair between the controller and the controlled (Macintosh, 1994). It is argued that a management control system of an organization would serve as a domination structure because it would provide managers with certain resources that they could draw on to influence the power distribution (Macintosh & Scapens, 1990). Uddin and Tsamenyi (2005) illustrated the politicization of decision making in the operation of the state-owned enterprises in developing countries and the pervasive role of political and social relations in decision making. Moreover, Larbi (2001) applied this theory to understand the power play through unnecessary political interventions in state-owned enterprises in Ghana.

The second theory considered here draws on the concept of surveillance and power (Foucault, 1977). It has been applied in management control research for the purpose of understanding the complex power dynamics that underpin management controls. According to Foucault, power and knowledge are the two sides of the same social relationship. He argued that the method of punishment by torture to acquire power disappeared and was replaced by a pervasive and impersonal system of surveillance that concentrated attention on the psychology of the individual. Disciplinary power moves the focus of control to individuals themselves. By being aware that individuals are constantly under surveillance, they begin to oversee themselves by regulating their own behavior in the light of its assumed visibility to others. This concept is further elaborated by the idea of the panopticon prison. Surveillance and discipline initially was applied in organizations such as prisons, mental asylums, army barracks, hospitals, schools, and factory systems. Modern organizations and their controls can be viewed from the same perspective. Cowton and Dopson (2002) applied this theory to explain how management controls were established and operated in an organization of an automotive distributor. They found that the images and metaphors of Foucault could be analogous to controls in a large business organization.

Viewed from the perspective of anthropology, there have been criticisms that management control literature has adopted an objectivist position with the contingency approach and treated national culture as a simple external environmental variable. Therefore, significant factors in the national cultural context within which management controls operate have been neglected (see Bhimani, 1999, for a detailed review of this assertion). Recently, several attempts have been made to use anthropology in understanding deep-rooted and enduring individual and organizational practices that form the basis and context of management controls. This view can be useful in many ways. For example, it can capture the impact of historical and external organizational factors involving political and economic institutions and struggles relating to culture and control (Bhimani, 1999). Moreover, it can explain how the dynamics of cultural change influence controls. The anthropological approach can be used to view cultural diversity in societies and interactions between cultures (Efferin & Hopper, 2007). This is essential in understanding the national context within which organizations and their controls function. Efferin and Hopper (2007) demonstrated how culture and ethnicity in a Chinese-owned Indonesian company played a key role in forming the management controls of the organization. This study revealed that the intricate cultural differences among Javanese and Chinese employees had created complex power struggles that underpinned the operation of the organization’s management controls. The insights gained from this approach would have been impossible if the objectivist, contingency research approach had been followed, due to the preclusion of extraorganizational variables (Efferin & Hopper, 2007). Ahrens and Mollona (2007) showed the usefulness of the anthropological approach to understand the control of a steel mill. Similarly, the political economy approach that includes theories of mode of production was used by Wickramasinghe and Hopper (2005) to understand management control of a textile mill in a traditional Sinhalese village in Sri Lanka. This study revealed that the traditional culture emanating from kingship-based social relations was still prevalent in the organization and that the practices of this culture largely shaped the operation of management controls in the company.

Concluding Comments

The main purpose of the article was to offer a critique to the mainstream management control theory illustrating its gaps and suggesting a way forward. One of the functions of theories is to act as a tool to make sense out of issues. The higher the level of enrichment of the theories, the deeper is the ability to shed more light on the issues being investigated. Management control issues of modern organizations are interwoven with social, psychological, political, anthropological, economic, technological, and geopolitical aspects. Multiple theories that are derived from multiple disciplines can enhance a researcher’s understanding of management control issues. It is within this context that this article endeavored to highlight directions for future development of the management control theory.

It was shown that management control theory was heavily influenced by accounting-based approaches resulting in lopsided development of the theory. Intricate power dynamics among organizational members and other complex extraorganizational factors that cause management control issues could not be captured by the accounting-based approaches. Management control theory borrowed heavily from organizational theory and as a result, organizational theory had a profound impact on the evolution of management control theory over the last four decades. To elaborate further, three distinct periods of evolution of the management control theory were suggested: (a) classical management era, (b) era of modern control theory dominated by accounting, and (c) era of postaccounting management control theory. Theoretical works of organization theorists such as Max Webber and F. W. Taylor formed the theoretical basis of management controls before the accounting control approaches became prominent. The advent of accounting domination of the management control theory did not sever the link between management control theory and organization theory. Instead, the proponents of accounting controls overly used the systems theory perspective that was considered a part of organization theory. As a result, the systems theory perspective overwhelmingly influenced management control theory. One ramification of this impact was that management control research was not able to fully explain and understand deep-rooted contextual variables causing management control issues. This triggered the need for broader, alternative theories that can shed more light on the management control issues interwoven with social, cultural, political, and historical aspects.

As the influence of the systems theory perspective on the development of management control theory was pervasive, the direction of the development of management control theory was mapped using four conceptual categories derived from the systems perspective. One of the advantages of this categorization is that it can be used to illustrate the direction the management control theory ought to progress. Management control research that assumes a world of purposefully designed organizations pursuing explicit objectives and organizational events taking place independent of external environment tend to possess the characteristics of closed rational systems perspective. The open rational systems perspective differs from the closed rational systems perspective when it is assumed that the organizational events can be influenced by contingency variables. Management control research belonging to both these categories is not able to fully explain the deep-rooted issues that are caused by the dynamics of power and conflicts internal as well as external to the organization. As a result, many aspects of the management control issues tend to remain unexplained. The drawbacks of the management control theory can partly be explained in relation to these two categories. On the other hand, when the influence of intricate human relations on management control issues is taken into consideration by researchers acknowledging the importance of unplanned and spontaneous processes, with organically emerging informal structures supplementing or subduing rationally designed frameworks, those researches tend to possess the characteristics of natural systems perspective. The research falling into this category tends to reflect the true nature of management control issues. Intricate relations among organizational members and the extraorganizational factors can well be explained when multiple theoretical perspectives are used. Toward this end, management control theory can be enriched by incorporating multidisciplinary theoretical perspectives from social theories, psychology, anthropology, and political economy.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research and/or authorship of this article.