Abstract

China's state-owned enterprises are among the largest firms in the world, dominating key sectors of the Chinese economy and playing a major role in Chinese projects abroad through the Belt and Road Initiative. This article describes a system of “managed competition” among China's state-owned enterprises that attempts to harness the forces of competition while intervening to ensure a robust field of capable competitors. This system is implemented through a multi-level structure where parent state-owned enterprises coordinate and balance competition among a set of similarly resourced subsidiaries through the allocation of management personnel and resources. This article examines how this approach works in practice through an in-depth empirical case study of two of China's largest infrastructure construction firms: China Railway Group Limited and China Railway Construction Corporation. Understanding the internal structure and operations of China's state-owned enterprises sheds light on a crucial part of China's political economy and on China's efforts to extend its influence globally.

Introduction

China's state-owned enterprises (SOEs) matter more than ever. As some of the largest companies in the world, making up 92 of the Fortune Global 500 (Kennedy, 2020), China's SOEs form the backbone of the Chinese economy, making up roughly a quarter of gross domestic product (GDP). 1 While China's dynamic private firms tend to dominate news headlines, it is China's SOEs that run key sectors from energy to telecommunications and build most of China's modern infrastructure. These same SOEs are also major players in China's efforts to exert influence abroad, including infrastructure projects associated with the Belt and Road Initiative (BRI). The scale and reach of China's largest SOEs, not to mention their influence in shaping China's domestic politics (He, 2019; Ye, 2019), render them a geopolitical force in their own right. Moreover, SOEs lie at the heart of China's industrial policy and technology upgrading efforts, featuring prominently in the “Made in China 2025” program (Zenglein and Holzmann, 2019). Yet, despite their far-reaching global impact, China's SOEs continue to be understudied.

This article sheds light on the internal structure and operations of China's powerful central SOEs (known as yangqi) and their system of “managed competition”. While mega-mergers and consolidation among China's central SOEs have received significant attention (Leutert, 2016; Li, 2016; O’Connor, 2018), a closer look inside these corporate giants reveals an elaborate multi-level structure of parent companies and subsidiaries. It is often the subsidiaries that are the primary operating entities, vying directly for business and carrying out project work with a significant degree of autonomy. Their parent SOEs play a coordinating role, reallocating resources and managerial personnel across subsidiaries to maintain a balance in competitive capabilities across firms. Through this multi-level structure, China's SOE system attempts the difficult balancing act of harnessing the forces of competition while intervening to ensure a robust field of competitors.

To understand how China's approach to managed competition works in practice, this article takes an in-depth look at China's infrastructure construction sector where this system can be seen most clearly. This sector is dominated by two large SOEs, China Railway Group Limited (CREC) and China Railway Construction Corporation (CRCC), currently the 42nd- and 51st-largest companies in the Fortune Global 500, respectively (Fortune Magazine, 2020). Formerly part of the Ministry of Railways, CREC and CRCC are not only the principal builders behind China's high-speed rail system but are in fact the main civil engineering firms for many types of infrastructure projects, including highways, subways, bridges, tunnels, and buildings. CREC and CRCC are also major players in BRI projects abroad, from high-speed railways in Malaysia and Saudi Arabia to highways and subway lines in Kenya and Pakistan.

This article begins by describing existing work on China's SOEs, which is often framed by the question of whether China's SOEs are moving toward a private-sector model or returning to a more statist approach. This article then describes an alternative approach I call “managed competition”, which fits neither model but better characterizes China's current SOE system. The next section shifts to an empirical case study of CREC and CRCC, drawing on interviews with dozens of industry participants and experts as well as thousands of pages of project documentation, contract records, bond prospectuses, and other corporate materials gathered during a year of fieldwork in China. A detailed examination of these firms shows how managed competition works in practice, including key processes such as the performance evaluation system and the allocation of management personnel. This article concludes by discussing the implications of this system of managed competition for China's domestic economy and China's influence on the global stage.

China's SOEs: Beyond “state versus market”

Much research on China's SOEs is framed around the question of whether China is moving toward a more market-oriented model or bringing back elements of its former statist approach. A wave of SOE reforms in the 1990s and 2000s led some observers to believe that China was heading toward a more market-oriented economic model (Lardy, 2014; Lau et al., 2000; Prasad and Rajan, 2006). Scholars pointed to the receding role of SOEs in the economy, giving way to a dynamic and rapidly growing private sector (Lardy, 2014). At the same time, SOEs themselves were being restructured in ways that resembled their private sector counterparts. In the late 1990s and early 2000s, a wave of “decoupling” separated administrative entities from the Communist Party of China (CPC) or the Chinese state bureaucracy and converted them into more autonomous “corporations” (Aivazian et al., 2005; Li, 2016). Subsequently, many SOEs listed shares publicly on the Hong Kong and Shanghai stock exchanges, although in reality this mainly served to bring in passive private capital while preserving state control (Wang, 2015). Following a new set of corporate laws in 2002, the corporate governance structures of China's SOEs began to resemble those of the private sector, including the formation of corporate boards and external directors (Rosen et al., 2018).

More recently, however, analysts have observed several trends that suggest a possible return to elements of the statist approach of the pre-reform era. The first trend is a wave of mega-mergers among central SOEs that began in the early years of the central State-Owned Assets Supervision and Administration Commission (SASAC) in the early 2000s 2 and has accelerated in recent years (Leutert, 2016; Yu, 2019). The second trend is an increase in references to the centrality of the state's role in the economy in official discourse, signaling a continuing if not expanding role for SOEs (Lardy, 2019: 19–20). While China has begun to soften its official rhetoric on industrial policy after international backlash to its “Made in China 2025” program (Martina et al., 2018), there is little indication that the substance of China's push for greater state involvement in core sectors of the economy has changed. The third trend is the rise of party cells within private firms, including some foreign firms (Thomas, 2020). While this shift does not directly affect SOEs, it has been interpreted as a possible reassertion not only of the state but specifically party control in all aspects of the economy. While the question of whether China's SOEs are moving toward a more market-oriented or statist approach can provide a useful framing, it runs the risk of overlooking major changes in the structure and operations of China's SOEs that do not fall neatly within either paradigm. 3

Managed competition

The usefulness and dangers of competition feature prominently in Chinese state discourse. On the one hand, competition is seen as a useful tool for motivating improvement and innovation in both government administration and commercial activity. On the other hand, “vicious competition” or “excessive competition” — such as unsustainable price wars or wasteful overinvestment – are seen as harmful to industry stability and society at large. Thus, China's leaders have a preference for what is often referred to in official language as “orderly competition”, particularly in critical sectors of the economy such as energy and industrial goods. 4

The idea of “managed competition” has been previously discussed in the scholarly literature on China's SOEs but never formally defined. Scholars have observed that competition within strategic sectors — such as defense, telecommunications, and commercial aviation — tends to be limited to a small number of core SOEs (Naughton, 2010; Nolan, 2001a; Pearson, 2005). Margaret Pearson (2005: 316) used the term “structured competition” to describe a set of unwritten “normative preferences” for the “state-driven creation of market structure”. Barry Naughton (2010) used the terms “managed competition” and “structured competition” to describe the Chinese state's “precarious balancing act” between harnessing the productive forces of market competition and ensuring that state firms ultimately serve the “public interest”. Beyond China, the idea of managed competition has a history in the post-World War II development experiences of several East Asian countries, including Japan and South Korea (Kushida and Oh, 2007). Bai Gao has traced a connection between Japan's postwar industrial strategy of “organized competition” (Gao, 1997: 51–56) and China's current preference for “oligopolistic competition” in the train manufacturing sector (Gao, 2016).

Building on these ideas, I argue that China's current SOE system is best characterized as a system of “managed competition”, which can be understood as consisting of two complementary parts. First, there is an effort to ensure that there exists more than one viable SOE in each sector and that there is meaningful competition among these SOEs within the domestic market. This contrasts with the pre-reform system of sector-level state monopolies, which suffered from weak incentives for innovation and soft budget constraints (Kornai, 1986). Second, competition among SOEs is managed through the reallocation of personnel and resources across firms to ensure a core set of competing firms with relatively similar capabilities. While the idea of limiting competition to a handful of firms with sufficient scale and capabilities has been previously discussed (Naughton, 2010; Nolan, 2001a; Pearson, 2005), less attention has been paid to the process of active balancing. In order to maintain a robust level of competition and prevent any single firm from becoming too dominant, several levers are used by state agencies and SOEs to ensure that there are multiple, similarly capable competitors in a given sector. These levers include management reshuffling, controlling access to financial resources (e.g. state bank loans), reallocating material resources (e.g. machinery and equipment), sharing intellectual property and technical know-how, and demand-side balancing (e.g. through the awarding of contracts for public projects).

Multi-level structure

At the heart of China's system of managed competition is a multi-level structure for SOEs consisting of parent SOEs and multiple tiers of subsidiaries. At the highest level, there are typically a limited number of large first-tier parent SOEs within a given sector. Each parent SOE oversees a set of second-tier subsidiaries that tend to be relatively similar in size, structure, and capabilities. It is these second-tier subsidiaries that are the key operating actors, enjoying significant autonomy and competing with one another directly for business. Parent SOEs “manage” competition among subsidiaries in two ways. First, they monitor the performance of their subsidiaries and hold them accountable through a formal evaluation system. Second, they allocate management personnel and redistribute resources across subsidiaries to maintain a balanced playing field, ensuring that all subsidiaries remain similarly competitive and that no subsidiary becomes too strong to dominate the market or too weak to survive. Second-tier subsidiaries are often large corporate “groups” (jituan) themselves that in turn oversee their own sets of third-tier subsidiaries. These third-tier subsidiaries, however, are not autonomous corporate entities and function more like departments or branches of the second-tier subsidiaries. 5

One forerunner to this multi-level structure was the “general corporation” (zonggongsi) system of the 1980s (Li, 2016). During this period, industry-wide umbrella SOEs were formed to provide a degree of coordination across production units but were also seen as another unnecessary layer of bureaucracy (Li, 2015: 49–56). Another forerunner was the “group company system” (Hassard et al., 1999, 2010; Meyer and Lu, 2005; Morris et al., 2002), also known as “enterprise groups” (qiye jituan) (Nolan, 2001a, 2001b; Nolan and Wang, 1999; Wu, 1990), that began in the steel industry in the early 1990s. These enterprise groups consisted of a parent SOE and a set of subsidiaries that were “connected through capital” (Nolan and Wang, 1999). Subsidiaries were “responsible for their profits and losses”, operating with “some degree of management autonomy” and “free to look for markets anywhere” (Hassard et al., 1999: 71). At the same time, subsidiaries maintained “a fairly close relationship with the parent company”, which in turn retained ultimate control and allocated personnel across subsidiaries (Hassard et al., 1999). 6

While some features of these early SOE systems have continued to the present, there are important differences with today's multi-level structure. One difference is the role of the subsidiaries. When enterprise groups first emerged, group subsidiaries were “mainly supplier firms” to the parent company (Nolan and Wang, 1999). Today, however, the subsidiary SOEs are the primary business operators and are often corporate groups themselves with their own networks of subsidiaries and suppliers. Another difference is the role of the parent SOEs. China's earlier push for enterprise groups focused on generating sufficient economies of scale to produce “national champions” in the mold of Japan's powerful business conglomerates (Nolan, 2001b). While the fostering of national champions remains a key goal (Lin and Milhaupt, 2013; Yu, 2019), the role of parent SOEs has evolved to include both a unified outward-facing profile and the active management of “internal” competition within the industry.

This section has provided a brief sketch of China's multi-level SOE structure. The next section looks in detail at how this works in practice through the case of China's two main infrastructure construction SOEs.

Case study: China's infrastructure construction SOEs

A three-level structure

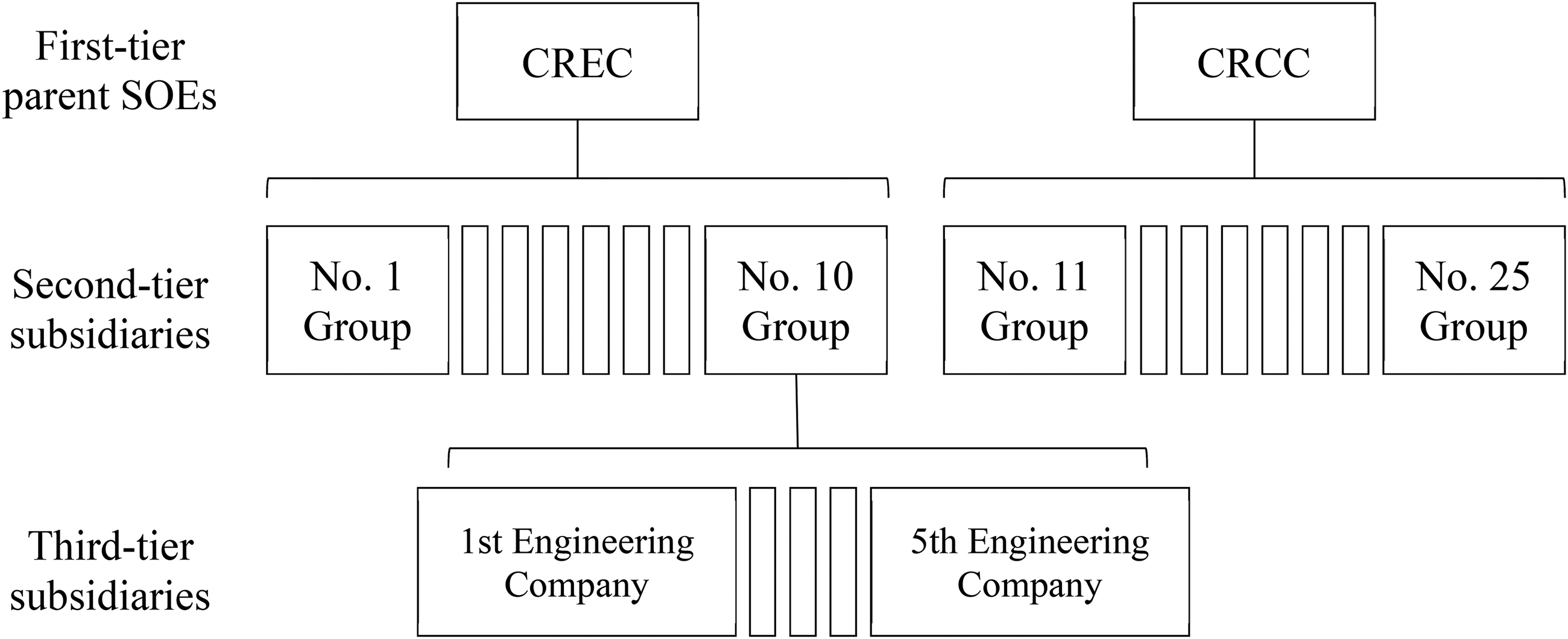

Much of China's modern infrastructure, including its high-speed railway system, has been built by a set of infrastructure construction SOEs with a three-level structure (see Figure 1). 7 The first level consists of two large SASAC-owned parent SOEs: CREC and CRCC. 8 CREC and CRCC were formerly part of the Ministry of Railways with roots extending back to the Railway Corps of the People's Liberation Army during the War of Liberation. 9 As part of a broader wave of administrative “decoupling” in the late 1990s and early 2000s (Li, 2016), these civil engineering organizations were separated from the Ministry of Railways and converted into autonomous SOEs. 10 Today, CREC and CRCC are sprawling conglomerates with a global presence, playing a key role in BRI projects from highway construction in Kenya and Bangladesh to railway development in Serbia and Indonesia. Because both CREC and CRCC are publicly listed on the Hong Kong and Shanghai stock exchanges, they are often referred to as the “share companies” (gufen gongsi) in the industry shorthand.

The three-level structure of China's infrastructure construction state-owned enterprises.

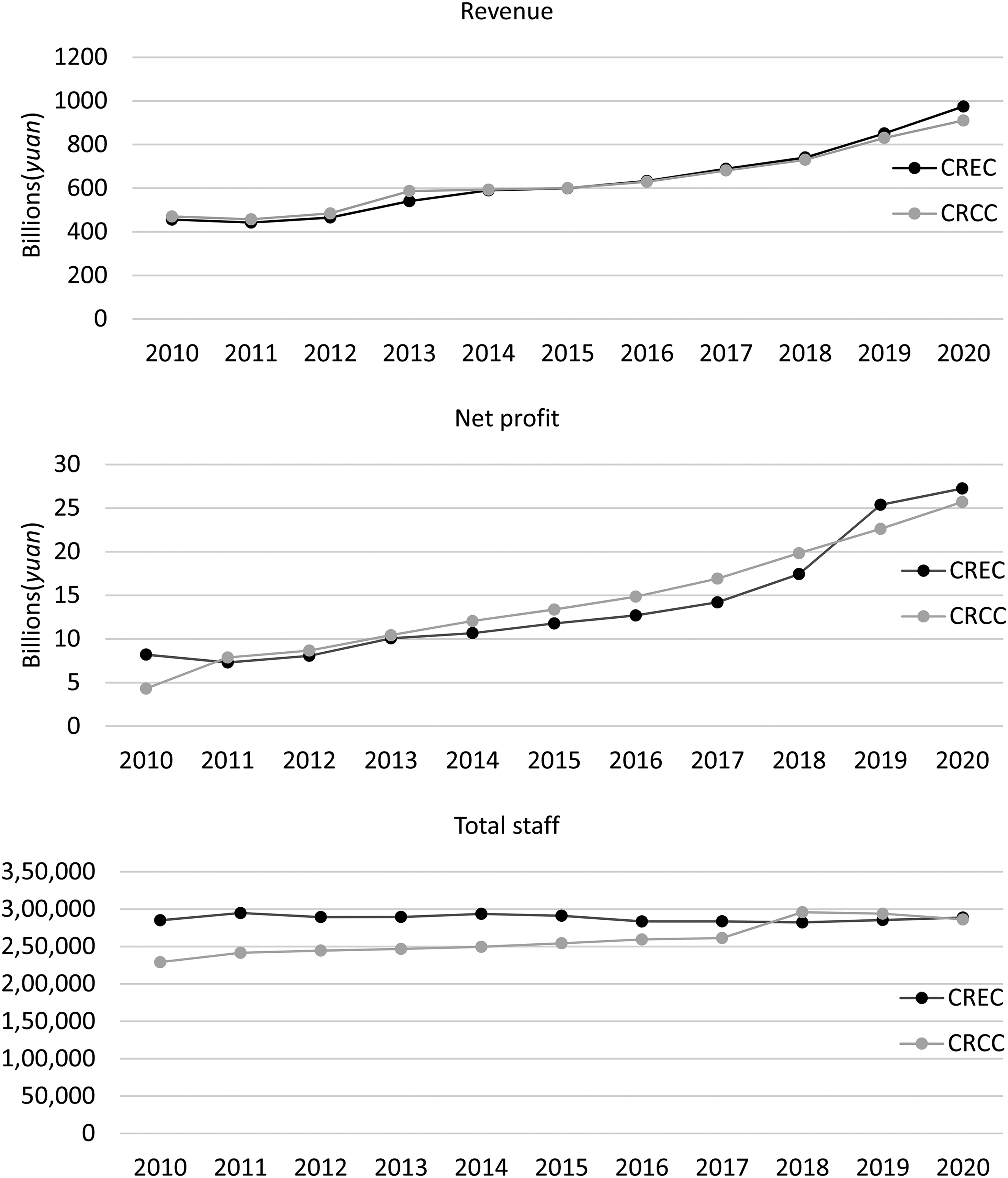

Already at the level of the parent SOEs we find some indication of managed competition at work: CREC and CRCC are strikingly similar on a range of dimensions and remain relatively balanced over time as the industry's two main rivals. CREC and CRCC each have annual revenues of approximately 1000 billion yuan and a total staff of around 280,000 (see Figure 2). Indeed, CREC's and CRCC's annual revenues remain remarkably similar over time, staying within 10% of each other from 2010 to 2020. Their net profits and number of employees also remain comparable to each other over time. While direct evidence for active balancing between CREC and CRCC is lacking, their convergent growth trajectories in a rapidly changing industry suggest some degree of intervention.

Revenues, net profits, and total staff for China Railway Group Limited (CREC) and China Railway Construction Corporation (CRCC), 2010–2020.

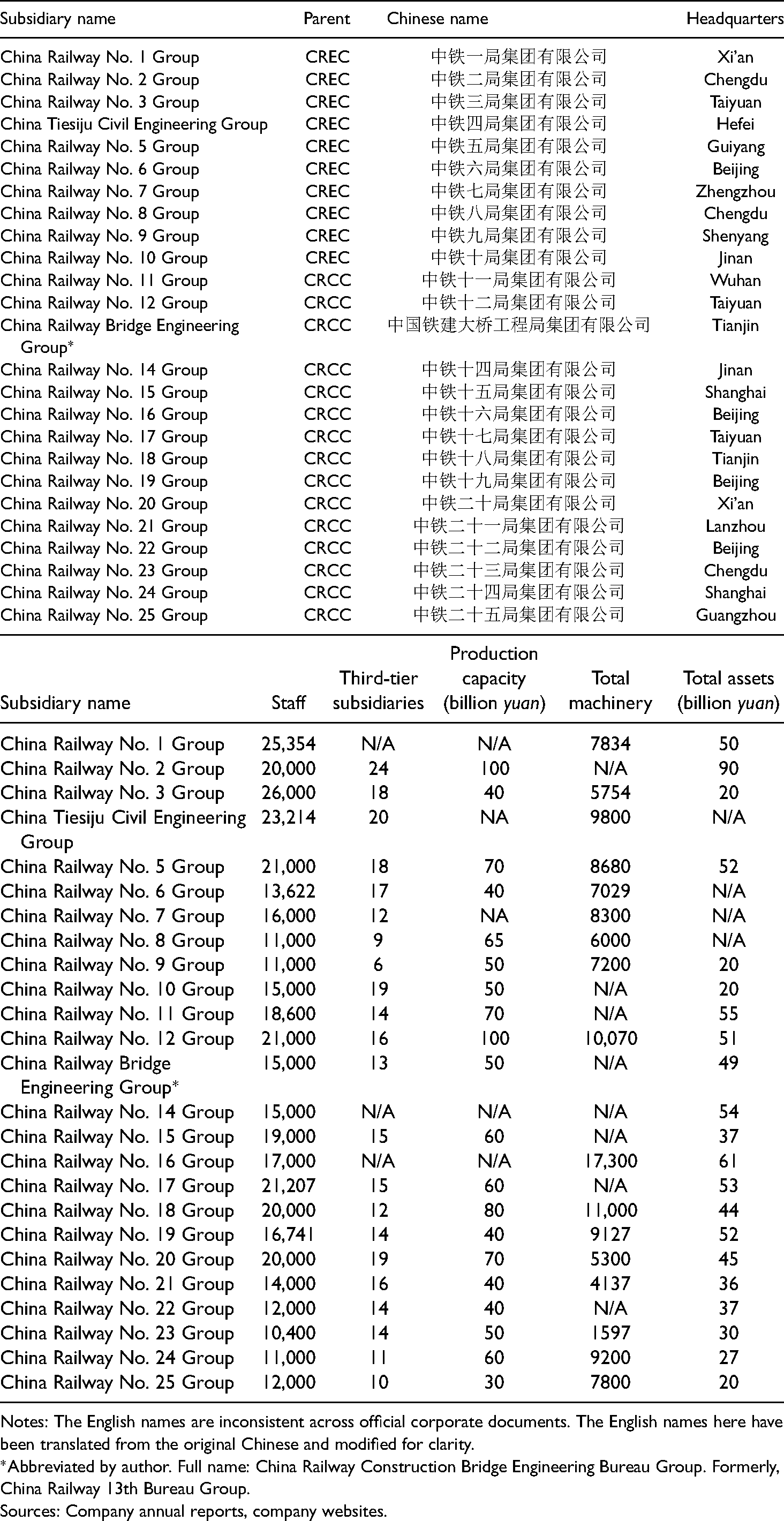

The second level in this multi-level SOE structure consists of CREC's and CRCC's subsidiaries. These subsidiaries are the primary operating companies in China's infrastructure construction sector, carrying out the actual construction work itself and competing directly for project contracts. Across both CREC and CRCC, there are 25 core infrastructure construction subsidiaries along with a set of non-core subsidiaries that include survey and design firms, machinery and equipment manufacturers, and financing and real-estate groups. Table 1 provides a list of the 25 core subsidiaries and a summary of their key characteristics. The names of core subsidiaries follow a numerical naming convention that reflects their historical roots as engineering bureaus within the former Ministry of Railways. The first 10 subsidiaries (No. 1 Group to No. 10 Group) belong to CREC, and the last 15 subsidiaries (No. 11 Group to No. 25 Group) belong to CRCC. 11

Core subsidiaries of China Railway Group Limited (CREC) and China Railway Construction Corporation (CRCC).

Notes: The English names are inconsistent across official corporate documents. The English names here have been translated from the original Chinese and modified for clarity.

*Abbreviated by author. Full name: China Railway Construction Bridge Engineering Bureau Group. Formerly, China Railway 13th Bureau Group.

Sources: Company annual reports, company websites.

These core second-tier subsidiaries are similar in size, resources, and capabilities. As Table 1 shows, their numbers of employees, annual production capacity, total assets, and even total pieces of construction equipment all lie within a narrow range with no single firm appearing exceptionally strong or weak. As parent SOEs, CREC and CRCC play a crucial role in assuring that competition among these subsidiaries remains robust and relatively balanced through the redistribution of resources and personnel. One means of achieving this is through investment by parent SOEs in the acquisition of certain types of expensive machinery on behalf of subsidiaries. Another perhaps more important means is the sharing of technical expertise and construction know-how by parent SOEs across subsidiaries. For example, in the early years of China's high-speed rail program, second-tier subsidiaries were often paired with foreign firms such as Germany's Max Bögl Group and the Obermeyer Group to learn construction techniques for ballastless track and specialized railway switches (Wuhan–Guangzhou High-Speed Rail Corporation, 2012). This knowledge was then diffused across subsidiaries via formal technical manuals as well as informally through the circulation of personnel between firms. The net result of this large number of similarly well-qualified subsidiary competitors is not only a competitive bidding market for construction contracts but also a deep reserve of “interchangeable parts” should one firm need to be replaced for any reason after project work is already underway.

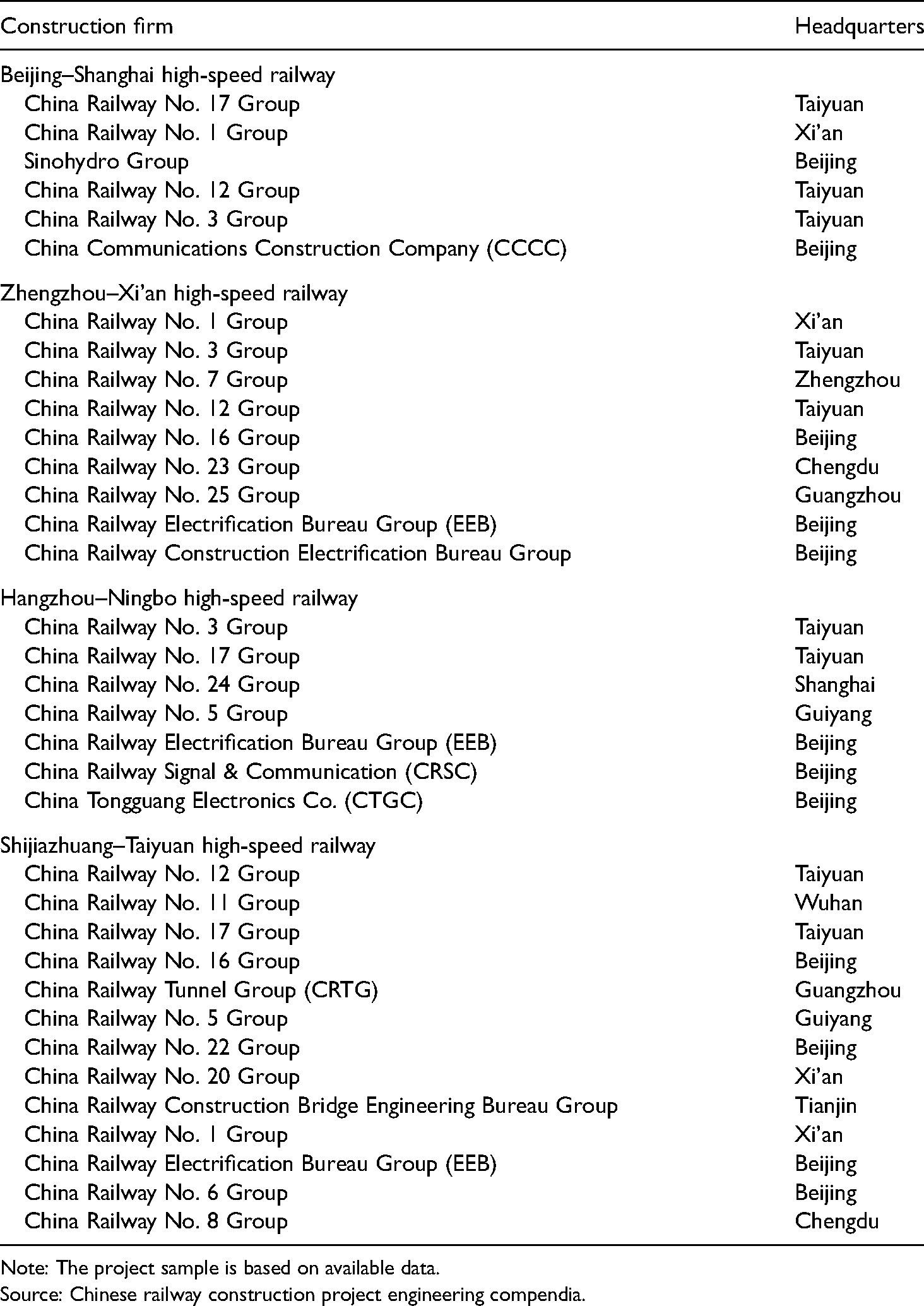

Core second-tier subsidiaries are sizeable SOEs in their own right, each employing over 10,000 staff. Structured as corporate groups (jituan gongsi), these second-tier subsidiaries oversee their own set of subsidiaries and branches and operate with a significant degree of autonomy. Second-tier subsidiaries are not limited in their geographic scope and bid on project contracts across the country and around the world. Table 2 shows a sample of Chinese domestic railway projects and the second-tier subsidiaries that were involved in their construction. From this table, we can see that the location of projects and the geographical headquarters of their construction firms are not related. Indeed, every second-tier subsidiary has a presence in multiple parts of the country through third-tier subsidiaries based in different locations and through various “regional operations command posts” (quyu jingying zhihuibu) or “regional headquarters” (quyu zongbu). For example, the second-tier subsidiary No. 15 Group, which is headquartered in Shanghai, has 5 third-tier subsidiaries based in Xi’an, Shanghai, Chengdu, Zhengzhou, and Tianjin as well as 12 regional offices distributed across the country.

A sample of Chinese railway projects and their construction state-owned enterprises (SOEs).

Note: The project sample is based on available data.

Source: Chinese railway construction project engineering compendia.

Lastly, the third level of this multi-level SOE structure consists of another level of subsidiaries below the second-tier subsidiaries. Each second-tier subsidiary has its own set of core engineering subsidiaries with numbered names (e.g. 1st Engineering Company, 2nd Engineering Company, etc.) as well as several auxiliary subsidiaries. These third-tier subsidiaries are referred to as third-tier companies (sanji gongsi) or engineering companies (gongcheng gongsi) and function like departments or branches of the second-tier subsidiaries, receiving work assignments rather than competing directly for business. Taken together, the operation of this three-level structure can be summarized as follows: first-tier parent SOEs are responsible for high-level coordination, second-tier subsidiaries are the primary industry operators, and third-tier subsidiaries provide support. Indeed, this division of labor across SOE levels is frequently emphasized in corporate documents and speeches. 12

Performance evaluation and accountability

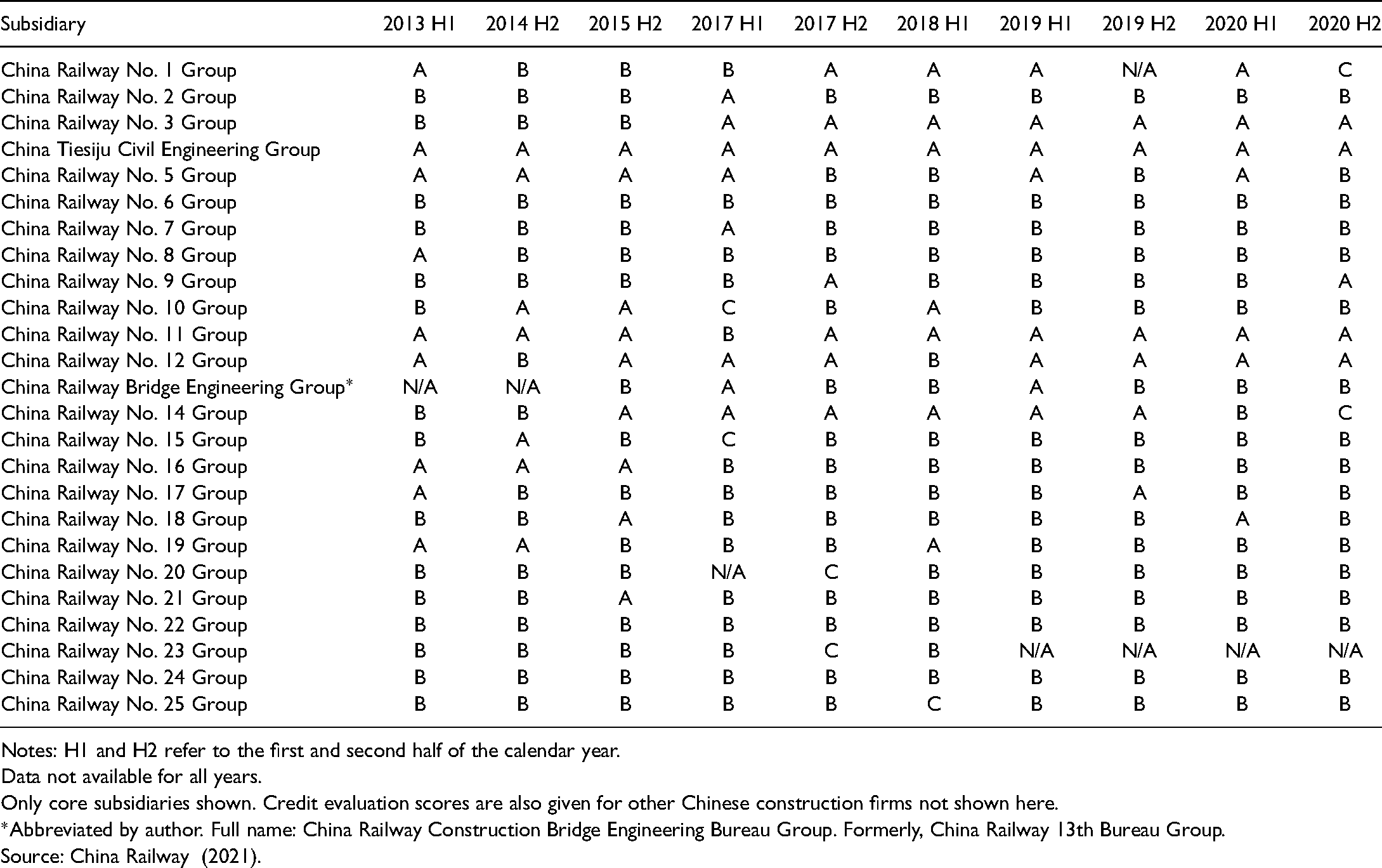

CREC’s and CRCC's core second-tier subsidiaries are monitored and assessed for their work on railway construction projects through a formal performance evaluation system called the “railway construction firm credit evaluation” system. 13 Twice each year, China State Railway Group Company (China Railway) publishes credit evaluation results for each firm in the form of an A, B, or C letter grade. 14 The distribution of these grades is generally fixed: the top 10 firms receive As, the lowest three receive Cs, and all other firms, which include the vast majority, receive Bs.

While this grading system bears some resemblance to the performance evaluation system used by SASAC, 15 the railway credit evaluation system is significantly more complex and tailored specifically for the railway sector. Credit evaluation letter grades are derived from a numerical scoring system. Each firm starts with a base score and then has points deducted for “harmful actions” according to a lengthy schedule that describes each type of “harmful action” and its corresponding penalty. Minor violations, such as failing to adhere to the latest version of the project design blueprints, may result in a one- or two-point deduction whereas major problems, such as a train accident due to poor construction quality, can result in an automatic C grade regardless of numerical score. 16 Bonus points can also be earned for positive actions, such as outstanding railway standardization practices.

Table 3 shows the credit evaluation grades for core second-tier subsidiaries from 2013 to 2020. As can be seen in this table, credit evaluation grades for each subsidiary vary over time. While some subsidiaries tend to receive more As, such as Tiesiju Civil Engineering Group and No. 11 Group, it is uncommon for any firm to consistently score at the top or bottom of the rankings. Even relatively strong performers can suddenly receive a C grade due to an accident, as was the case with No. 1 Group in 2020. This remarkable balance in credit evaluation grades over time suggests that competition among second-tier subsidiaries is managed not only in terms of resources and capabilities but also in terms of final results.

Railway construction firm credit evaluation results, 2013–2020.

Notes: H1 and H2 refer to the first and second half of the calendar year.

Data not available for all years.

Only core subsidiaries shown. Credit evaluation scores are also given for other Chinese construction firms not shown here.

*Abbreviated by author. Full name: China Railway Construction Bridge Engineering Bureau Group. Formerly, China Railway 13th Bureau Group.

Source: China Railway (2021).

Managerial appointments and career paths

Within CREC's and CRCC's multi-level structure, a similar leadership arrangement is replicated at each corporate level, one that mirrors that of other Chinese SOEs and other parts of China's political system. The top leader is the company's party secretary (dangwei shuji), who is also the chairman of the board (dongshizhang). The second-in-command and head of day-to-day operations is the general manager (usually titled zong jingli), who is also the company's party deputy secretary (dangwei fu shuji). Just below the general manager are several deputy general managers (fu zongjingli), which typically includes the chief engineer (zong gongchengshi).

For each corporate level, leadership personnel appointments are made by a specialized personnel department in the next corporate level up in the hierarchy. The leaders of second-tier subsidiaries are appointed by the parent SOE's Party Committee Cadre Department (dangwei ganbubu), also referred to as the Human Resources Department. Likewise, the leaders of third-tier subsidiaries are appointed by the corresponding personnel departments of second-tier subsidiaries one level up. 17 At the parent SOE level, the leaders of CREC and CRCC themselves are appointed by higher levels within the state and party hierarchy, including SASAC and the party's Central Organization Department. 18

The career paths of subsidiary leaders typically follow either a “single-group track”, rising up through the ranks within a single corporate group, or a “multi-group track” involving transfers across multiple subsidiaries. This single- versus multi-group track career progression mirrors that of Chinese SOE leaders in other industries (Lin, 2017). An example of a “single-group track” career is that of No. 2 Group's top manager Yuanfa Deng, who served as a deputy chief engineer of a No. 2 Group subsidiary before rising to the position of general manager and eventually party secretary of No. 2 Group itself (CREC, 2008). An example of a “multi-group track” career is that of former No. 13 Group head Yongjun Jiang, who served as a deputy general manager of No. 6 Group and general manager of No. 20 Group before becoming No. 13 Group's party secretary. Regardless of career path, managers at any level of CREC or CRCC share one common characteristic: they are nearly all engineers by training, often spending their entire careers within the railway or construction industry. 19

Chinese infrastructure construction SOEs abroad

While much attention for Chinese projects abroad focuses on China's large parent SOEs, a closer look reveals the important role that their multi-level structure plays in international projects. In the case of CREC and CRCC, their core second-tier subsidiaries are again the primary builders while the parent SOEs play a coordinating role and may take the lead on interfacing with foreign governments and foreign firms. For example, CREC's work on Indonesia's high-speed rail project is mainly carried out by its second-tier subsidiaries, including No. 3 Group, No. 4 Group, China Railway Electrification Bureau Group, and China Railway International Group (CREC, 2021). In 2021, CREC established an Indonesian regional office to serve as an “operation platform for major projects” and a “sharing platform for CREC's secondary units” that “will perform the functions of leadership, organization and coordination, business management, operation and development, performance management, compliance risk management and tax planning” (CREC, 2021).

CREC’s and CRCC's relationships with foreign governments can vary in terms of which corporate level in their multi-level structure is involved. 20 Sometimes the host country will contract with the parent SOE, as was the case with a 2008 mining and infrastructure project in the Democratic Republic of the Congo involving CREC. At other times, the host country will contract with a CREC or CRCC subsidiary that specializes in international work. For the Hungarian–Serbian railway project, Serbia's Ministry of Construction, Transport, and Infrastructure contracted with China Railway International Group, a CREC subsidiary. Occasionally, the host country will contract directly with second-tier subsidiaries themselves, as was the case in a 2017 road-building deal between Guyana's Ministry of Public Infrastructure and No. 1 Group.

In fact, second-tier subsidiaries can play a very active role in international projects, establishing a long-term presence in certain regional markets. No. 18 Group, for example, has a strong presence in the Middle East and played a key role in building the Mecca–Medina high-speed railway (Wu et al., 2018). No. 18 Group also has an established presence in West Africa, winning a joint bid to build a light-rail system in Nigeria's Kano state (Reuters, 2016) where it worked directly with Kano state political leaders (China Railway No. 18 Group, 2019). The World Bank has long recognized the importance of these subsidiaries and often identifies them individually when debarring Chinese contractors for poor business practices, such as No. 23 Group in Georgia (World Bank, 2019a) and No. 1 Group in Pakistan (World Bank, 2019b). While the activities of second-tier subsidiaries tend to receive less attention, their actions have broader repercussions for China's reputation abroad.

It is worth contrasting the geographical specificity of second-tier subsidiaries’ operations in domestic versus international markets. While second-tier subsidiaries are relatively location-agnostic within the Chinese domestic market and bid on projects across the country, there are several factors that contribute to “stickier” geographical relationships in international markets where a single second-tier subsidiary may operate in the same country or region for years, as is the case with No. 18 Group in the Middle East. First, the complexities of operating in international environments — including language, local market knowledge, differing political systems, and cultural know-how — along with competition from local and international players make it challenging for more than one Chinese SOE subsidiary to enter and remain viable within a given foreign market. Second, SOE subsidiaries that remain in one geographic location over years benefit by gaining market knowledge and establishing local relationships. Third, China's push for SOEs to compete internationally may still be in its early stages. As more SOE subsidiaries look to sources of growth beyond China, their geographical scope may expand internationally as it did domestically during the early decades of SOE reform.

“Managed competition” in other state-controlled sectors

Besides infrastructure construction, a similar system of “managed competition” can be found in other state-controlled sectors, albeit with variation in the number of parent SOEs, their comparability in terms of size and capabilities, and the degree of specialization among them. Like the infrastructure construction sector, China's petroleum industry is also dominated by two similarly sized central SOEs, China National Petroleum Corporation (2020 revenue: 2.09 billion yuan) and Sinopec (2020 revenue: 2.10 billion yuan), 21 along with a third, more specialist firm, China National Offshore Oil Corporation (CNOOC). A similar duopolistic structure appears within certain subsectors of China's defense industry, such as land-based systems where two major parent SOEs each oversee a collection of second-tier subsidiaries: China North Industries Group Corporation (NORINCO) and China South Industries Group Corporation (CSGC). However, in the case of land-based arms, there is a persistent imbalance between the two primary competitors: NORINCO tends to be about twice the size of CSGC by revenue (Tian and Su, 2020). Similar imbalances can be found in other sectors. For example, China's telecommunications sector is dominated by three central SOEs, but the leading service provider — China Mobile — has long held twice as much market share as each of the other two, China Telecom and China Unicom. 22

Variation in SOE structure across state-controlled sectors is driven by several factors. In some cases, the persistent dominance of one SOE over other competitors may be the result of legacy decisions by state regulators. China Mobile's dominance in the domestic telecom market stemmed in part from its inheritance of mobile communication assets during the transition from fixed-line to cellular telecommunications services (Liu and Whalley, 2011; Zhang and Liang, 2011). In other cases, industry structure may be the result of fragmented interests among state regulators. China's train manufacturing sector was dominated for years by two parent SOEs: China South Locomotive and Rolling Stock Corporation (CSR) and China North Locomotive and Rolling Stock Corporation (CNR). Efforts by SASAC to merge these two SOEs into a single firm faced resistance from the Ministry of Railways, the National Development and Reform Commission, and the Department of Commerce who all feared that a monopoly would cause train manufacturing prices to surge (Huang, 2018).

Conclusion

Peering into the internal structure of some of China's most prominent SOEs reveals a system that conforms neither to the image of state firms as the lumbering giants of the pre-reform era nor to the profit-maximizing model of private firms. Instead, China has pursued a different path altogether, attempting to leverage competitive forces within a state-managed system. This article has shown how this system of managed competition operates in practice through a multi-level structure comprised of parent SOEs who play a coordinating role and subsidiaries who compete directly for business. While there are clear echoes of the industrial policy experiments of other East Asian countries with its emphasis on “national champions” and control of the “commanding heights”, China's SOE system retains its own distinctively Chinese characteristics.

How effective is China's system of managed competition in terms of the productivity and competitiveness of Chinese SOEs? What are the implications for China's economy and the rest of the world? Executed properly, China's system of managed competition may be able to achieve the “precarious balancing act” (Naughton, 2010) of fostering vigorous competition while supporting broader public goals. Indeed, an optimistic interpretation might view this SOE system as not only the foundation for China's entire domestic economy but also a key instrument for carrying out China's foreign policy goals, particularly under the BRI. This is certainly the vision articulated in China's official state and party discourse.

At the same time, China's system of managed competition faces many potential risks and challenges. If the “managed” aspect of managed competition becomes too dominant, true competition and performance-based accountability may be undermined. In a classic case of soft budget constraints (Kornai, 1979, 1986), uncompetitive subsidiaries may come to rely on bailouts from their corporate parents. 23 Moreover, a carefully designed system of managerial and firm-level incentives is worth little if it is riven by corruption and political cronyism. 24 As with so many policy questions, success hinges on the basics of sound implementation and enforcement.

Ultimately, the answers to these questions lie beyond the scope of this article, and much more research on China's SOEs is needed. More in-depth case studies of particular SOEs and SOE-dominated industries are required to better understand the internal mechanisms of China's approach to managed competition. Quantitative studies of China's industrial programs using new econometric tools that better account for effects on downstream industries can shed light on the question of efficacy. 25 Moreover, industrial policy has come back into fashion around the world, partly in response to China's own state-led modernization push (Aiginger and Rodrik, 2020; Chang and Andreoni, 2020). A better understanding of China's experiences may offer a useful point of reference for other countries attempting state-led industrial programs of their own. These issues are all the more pressing as China's SOEs appear poised to further expand their domestic and global influence.

Footnotes

Declaration of conflicting interests

The author declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author received no financial support for the research, authorship, and/or publication of this article.