Abstract

Soon after implementing reforms to the tax-sharing system, the People’s Republic of China (PRC) implemented public budgeting reform, and thus formed a new kind of state governance system, the program system (PS). There are three categories of program expenditures available to local governments: “earmarked grants” from higher-level authorities; “non-grant program funds” from higher-level authorities; and program funds from same-level government departments. The convergence and reorganization of these three categories of program expenditure at the local level has, to a great extent, molded the fiscal structure of grassroots government in the PRC. The PS in essence does not mean discarding or surpassing the bureaucratic state system, rather, it is the active improvement and supplementing of the bureaucratic system by the state: a continuation and development of state regime construction. The overt purpose of the PS is to “solidify” budgetary constraints, while the underlying purpose is to enhance the government’s ability to respond to society. The two purposes present some tension in practice, as the rationalized and professionalized forms of governance that result do not necessarily enhance the ability to respond to public needs; in fact the reverse is quite possible.

Finance is the nervous system of a country.

—— Jean Bodin (1975, quoted in Wang, 2002a)

The budget is the skeleton of the state, stripped of any misleading ideologies.

Introduction

The rise of the program system (PS) (xiangmu zhi) in the People’s Republic of China (PRC) is related to the evolution of the country’s public finance system. After reforming the tax-sharing system in 1994, the absorptive capacity of the Chinese government was greatly enhanced, and “big government” grew up quickly against the background of the market economy. In order to spend the huge amount of fiscal revenue it had collected in an effective, rational, and normative manner, the central government carried out a series of reforms in the field of public expenditure and established a public budgeting (PB) system centered on government departments as the budgetary units and programs as the units of expenditure. The PS was adopted during this process, as a pivot in the PB system, and has shaped a kind of new state governance system on this basis.

In recent years, research on the PS has become a controversial subject in sociological circles. Since it is pervasive in the practice of government departments at different levels, it offers a good entry point for analyzing the behavioral mechanisms of the government. However, affected by factors such as availability of resources, existing studies have mainly discussed the consequences of the implementation of the PS at the grassroots level, while there is lack of comprehensive and clear knowledge about the systematic origin and organizational mechanism of the PS; thus, this article attempts to make a systematic exploration on this topic.

Research question and approach: “Returning” the PS to the analysis of internal government mechanisms

Management studies was the first discipline to conduct systematic research on program, or project, management. 1 It is asserted that that, “A program is a temporary work to create a unique product, service or result”. It is set up to achieve the strategic goals of an organization. For this purpose, a program group or portfolio 2 can also be established (Project Management Institute, 2013: 3–10). Program/project management is “the planning, organizing, directing and controlling of company resources for a relatively short-term objective that has been established to complete specific goals and objectives. Furthermore, project management utilizes the systems approach to management by having functional personnel (the vertical hierarchy) assigned to a specific project (the horizontal hierarchy)” (Kerzner, 2010: 5), and the management of a project portfolio, project group, and projects is driven by organizational strategy. Such studies on project management within the category of company management have provided helpful references to us in discussing the organizational operation of the PS within the government.

In the PRC, some sociologists have made elaborations on the PS. In general, these studies can be divided into two categories, the first is those which are about the PS as a mechanism. She and Chen (2011) made a systematic analysis on the phenomenon of “Programs to Villages” (xiangmu jincun). They integrated both top-down and bottom-up perspectives and described the “contracting mechanism” of the central government, the “packaging mechanism” of the local government, and the “grabbing mechanism” of villages in the process of “Programs to Villages”, demonstrating the tension between the concentration of power by the higher authorities and the resistance to control by the bottom strata, especially the emphasis on the response mechanism of the villagers to the PS. Zhou (2012) made an in-depth analysis on the “specializing” process and mechanism of financial funds from the perspective of public finance, and his study revealed the origin, categories, and scale of “earmarked grants” (zhuanxiang zijin zhifu) and their flow path within the government. In addition, by taking “county-based” compulsory education funding reform after the rural tax-for-fee reforms as an example, the study analyzed the practical logic and unexpected outcomes of earmarked fiscal funds at the grassroots level. Qu (2012) upgraded the PS to the status of a new level of the state governance system and believed that it was a manifestation of a “new double-track system” emerging in the reform process. Compared with the discussion by She and Chen (2011) and Zhou (2012), Qu’s (2012) study put more emphasis on the systematic spirit of the PS, while related research has been more “holistic”.

Thereafter, the PS quickly became a hotspot, prompting another round of studies. These studies have mainly been concerned with the practical implementation of the PS in the provision of public goods, poverty alleviation, and social management. Such studies mainly took a case-study approach, focusing on the practical consequences of programs rather than the process of program organization and allocation; that is to say, paying more attention to the “end” of program practice rather than the operation mechanism of the PS in the government (Chen, 2013, 2014, 2015; Di, 2015; Feng, 2009; Fu and Jiao, 2015; Gong, 2015; Gui, 2014; Huang et al., 2014; Li, 2015; Shi, 2015; Xun and Bao, 2007). At present, such studies have become the chief path by which academics have addressed the PS. However, there is an intrinsic defect in these studies, namely, they failed to analyze the PS within the government itself and had the research intention of “talking about programs themselves”. Zhou pointed out that: In all aspects of the program system, academic research focuses on the response strategies and behavioral consequences for grassroots governments when they are competing for programs. We know very little about the principal’s contracting process, program design and goals, and [as such] it can be said that we know nothing about them … Although the packaging behavior of local governments has been discussed in the research literature, most of them are speculative and general rather than close and detailed observations and analyses … The gaps in these studies reflect that research in this area is still in its infancy. (Zhou, 2015)

How, then, can we deepen our understanding of the PS from the perspective of the government? The studies of foreign scholars on companies’ internal project/program management can provide us with some inspiration. They found that, although project/program organization is specialized and task-oriented, it seldom, if ever, exists apart from the traditional organizational structure of the company. The entire project-/program-management structure and the company organizational structure overlap (Kerzner, 2010: 86, 108). Therefore, the key to project/program management is to build an organizational mechanism that effectively serves the project/program based on the company’s organizational structure and according to the different characteristics of the project/program. The relationship between the project/program’s organizational form and the company’s organizational structure is key (Kerzner, 2010; Project Management Institute, 2013: 21–27).

Like a company’s internal program/project management, the PS is deeply embedded in the government’s bureaucratic organizational system. The existing organizational structure and personnel network within the government will have a significant impact on the actual operation of the PS. Meanwhile, the comprehensive expansion of the PS within the government will inevitably cause “disturbance” to the government’s operational processes and mechanisms. As a matter of fact, academic discussion on the PS has been fully aware of this problem in theory. For example, Qu et al. (2009) pointed out that “the dynamic operation of the administrative system” is “embedded on the basis of ‘specialized and program-based’ financial relation after the tax-sharing system reform”. Qu (2012) also pointed out that, “the program system functions in mutual embeddedness with the original bureaucracy” and “it is impossible to get rid of the inherent administrative law of the bureaucracy”.

Some scholars have made some productive attempts in the empirical study of the PS. Zhou’s (2012) study has set the standard among them. He took the role of the PS in the pattern of relations between county-level departments and township governments as the key point of analysis, and found that the county–township relations experienced an alternation from the “L-model” to the “seven model”. He especially pointed out the possible consequence of such inter-governmental relations on program practice: due to the absence of township government, public finance might be retained at the county level and can hardly “cover the countryside”. Chen (2015) and Shi (2015) also intentionally situated the PS within the government for discussion. Chen found that the PS changed the traditional mode of mobilization of grassroots governments. Within the government, “hierarchical mobilization” was changed to “multi-sector mobilization”, which greatly improved the mobilization ability of higher authorities, and the operation of the government changed from “following the prescribed order” to “providing resources to programs”. Chen (2015, 2017) also discussed the restructuring of the PS on the authority–responsibility relationship in the PS, as well as the structural form and evolutionary mechanism of program-oriented governance within governments, which are of significance to deepening the studies on the PS. Fu and Jiao (2015) put the PS within the context of grassroots government and found the paradox of “structural weakening” and “functional strengthening” of township governments in response to the PS.

However, restricted by some factors, such as the availability of analytical perspectives and materials, academics are still at the early stage in studying the operational mechanism of the PS within the government, and many blind spots in thinking about this issue are yet to be revealed. Two of the most typical aspects are: first, what is the systematic origin of the PS within the government? Empirically, existing studies believe that “earmarked grants” from higher authorities are the systematic origin of the PS; yet how can this explain the fact that the eastern regions of the PRC have generally been the ones to adopt the PS? Furthermore, is there any common systematic origin for the PS across the eastern regions and the central and western regions? What are the differences between them? Second, among the miscellaneous programs implemented by the government (especially local governments), what are the specific categories? What are the similarities and differences among them? What is the relationship between programs of different categories and the systematic basis of the PS? This is the foremost difficulty that researchers encounter in empirical studies. They are not only the problems that need to be solved immediately in deepening the study of PS, but also the premise for analyzing the “packaging” and “contracting” of the PS after situating it within the government.

In order to answer the two categories of urgent and important problems above, this article attempts to start from the PB system, and explores the evolution and organizational mechanism of the PS. Some scholars in the public administration management field have provided a good basis for the systematic study of PB reform in the PRC (Lin and Ma, 2012; Ma, 2005, 2010; Ma and Hou, 2014; Yu, 2010). However, regardless of the large number of studies on the PS by sociologists, or the exploration in the public administrative management field on the Chinese PB system, they have failed to effectively explain the relationship between the PB system and the PS. It is worth noting that, following the discussion of the PS in sociology, some research on the PS has also appeared among economists, with some scholars occasionally showing concern about the relationship between the PS and the program expenditure budget (Wang and Li, 2018; Zheng, 2016). Unfortunately, this research has not been carried out systematically; notably, the similarities and differences between the earmarked grants and the program expenditure budget have not been discussed.

This article shows that, from the perspective of the PB system, we cannot only acquire clearer knowledge about the system within the government, but also must clarify the different program categories of local government and their relationships, and obtain a clearer understanding on the flow path of programs in the government. After revealing the fact that the PS is the core of the PB system, the problem of program categories and their similarities and differences can be readily solved. Therefore, the above-mentioned two research problems, namely, the analysis of the systematic origin of the PS and its organizational mechanism in local government, overlap with each other; as such, they can provide a more solid foundation for the deepening of empirical study on the PS.

This article is divided into seven sections: the first section is introduction part; the second section is a literature review, which proposes the research approach of “returning” the PS to the government for analysis and clarifies the two problems that need to be immediately resolved; the third section is a discussion of the financial and systematic background of the PS. After reforming the tax-sharing system, the Chinese government stepped into the “big government” era within a short period; for this reason, the PRC carried out PB reform, which directly resulted in the “programification” of the public expenditure system, which became the systematic basis for the PS; the fourth section discusses the categories of program expenditures of local governments and their relationship; the fifth section analyzes the combination process of some categories of program expenditures in local governments and the difficulties therein, so as to further understand the formation mechanism of the PS; the sixth section attempts to make a more in-depth analysis on the systematic goal and intrinsic dilemmas of the PS; and the seventh section is the conclusion of the article.

The rise of “big government” and the origin of the program-centered public expenditure

The rise of “big government”: The systematic effect of the tax-sharing system

In the 1980s, the PRC implemented reforms to the “financial contracting system”, centered on “delegating power and transferring profits” (Jin et al., 2005; Qian and Weingast, 1996, 1997; Zhou, 2007). In giving certain autonomy to local governments and enterprises, the reform stimulated economic development but gave rise to many political and economic problems. Among them, the most serious was the rapid decline of the absorptive capacity and efficiency of the government, causing serious inefficiency of the financial capacity of the central government and threats to central authority (Wang, 1997). To reverse the financial dilemma, the central government carried out reforms to the tax-sharing system, which immediately enhanced absorptive capacity and efficiency and strengthened the financial capacity of the central government (Zhou, 2006).

With the stable and rapid economic growth of the Chinese economy, the systematic impact of the tax-sharing system was fully unleashed. After the reform, the government’s general budget revenue began to increase rapidly, as did its proportion of overall gross domestic product (GDP). Meanwhile, the governmental funds budgetary revenue and state-owned capital operating budgetary revenue also increased rapidly. Taken together, the general public budget, governmental fund budget, social security fund budget, and state-owned capital operating budget are called the “four budgets” (siben yusuan), which constitute the unified government revenue budgetary system. After 1994, the government’s “four budgets” grew rapidly in terms of proportion of GDP, from 16.43% at the lowest point, in 1995, to 37.45% in 2014. 3 In 2014, the absolute scale of the total revenue of the “four budgets” was also as high as 23,565 billion yuan, and the absolute amount of the government’s unified fiscal revenue and its proportion in GDP was astonishingly high. In general, the public revenue of the Chinese government accounts for nearly 40% of GDP, reaching the average level of the Organization for Economic Co-operation and Development countries, and a “big government” under the market economy system has grown in relative importance in the PRC (Jiao and Jiao, 2018; Li and Zang, 2017; Lü et al., 2020; Naughton, 2017).

Western developed countries have also experienced the rise of “big government” (Tanzi, 2014: 9–10; Tanzi and Schuknecht, 2005: 10–11; Walker and Vatter, 2001). In order to guide and restrict the behavior of this “big government”, Western countries have established modern PB systems, using standardized budgeting systems to allocate huge amounts of fiscal funds in an effective and standardized manner, to provide public products and public services for society. This is called the process of establishing a “budget state” (Cleveland, 1915, 1916; Wang, 2002b, 2007; Wang and Ma, 2008).

Similarly, after the Chinese government became “rich” in a short period of time, the question was would it be able to expend the huge amount of fiscal funds it had gathered in an effective, standardized, and reasonable manner in order to provide valid public products and services to society? This posed a great challenge to the governance system and the capacity of the government.

PB reform and the “programification” of financial expenditure

The PRC has been also trying to respond to the challenges of the “big government” era through the reforms of the PB system and the establishing of a modern “budget state”. Congruent with reforming the tax-sharing system, the central government began to plan the reform of the PB system. The Budget Law, implemented in 1995, initially regulated the government’s budgetary behavior (Liu, 2012: 43–48). In 1999, the central government began to comprehensively launch a new round of PB reforms. The first was department-based budgeting reform, which is the basis for the modern PB system.

The department-based budgeting system requires that government budgets be compiled on the basis of government departments as budgetary units, incorporating departmental responsibilities, work objectives, and fiscal budgets. Specifically, it includes two aspects. First, departmental budgets use a comprehensive budgeting method. All fiscal revenues and expenditures of a department are included into the departmental budget, and the extra-budgetary revenues which were not included before are all included in the “one budget”, that is, “independent accounting for each department”. The second is to standardize and elaborate budgeting methods. Departmental revenue mainly includes financial appropriation revenue, government fund revenue, and other revenues. Departmental expenditure can be divided into two parts: basic expenditures; and program expenditures. Basic expenditures refer to the annual expenditure plan prepared by various departments to ensure the normal operation of the organization and the fulfillment of daily tasks. They include personnel expenditures and daily public expenditures, and their budget is made based on a prescribed number of the staff and a fixed amount of funds. Program expenditure is an annual expenditure plan prepared in addition to the basic expenditures to complete a specific work target. The basic expenditure is the “daily expenditure”, the budget for which is determined according to headcount and standards. The program expenditure is the “service expenditure” and is the core of the departmental budget.

Taking the central government departments as an example, the declaration, examination, and the reply to projects are the key links of budgeting. Program expenditure budgets are prepared by grassroots-level budget units. After level-by-level review and collection, the central government departments report their budgets to the Ministry of Finance in the form of “first-level programs + second-level programs”, 4 and propose projected “first-level program” demands according to the specific number of “second-level programs”. The budget of the “second-level program” is prepared according to economic classification subjects, and the program category is proposed by the department when reporting the budget. The Ministry of Finance is in charge of the review. After the “second-level program” is included in the budgeting, the program category shall not be adjusted during the program implementation cycle. The Ministry of Finance reviews the program expenditure budgets submitted by the departments, and issues a budget controlling amount according to the “first-level programs”, and the departments arrange the “second-level program” budgets according to the reviewed program categories and rankings.

The core of the program declaration is the construction of the program libraries. The Ministry of Finance, other departments of the central government, and affiliated units have set up program libraries to maintain and manage first-level and second-level programs. The Ministry of Finance’s program library is composed of programs reported by various departments of the central government. The central department’s program library is composed of programs reported by same-level and lower-level units. The grassroots unit program library is composed of programs initiated and implemented by the same-level units.

The program library adopts an open management system. Each unit can set up “second-level programs” as required, and include them in the unit’s program library after review, and report them in real time or at regular intervals. After level-by-level review, they can be included in the central department’s program library as alternative programs for departmental budgets. When preparing the annual department budget and the department’s three-year rolling planning, based on the expenditure control amount issued by the Ministry of Finance, the central department selects the preferred program from the budget alternatives and submits it to the Ministry of Finance. In principle, programs that are not included in the department’s program library shall not be reported to the Ministry of Finance. The programs declared by various departments altogether form the program library of the Ministry of Finance, which serves as the basis upon which the Ministry of Finance conducts program management, reviews the annual department budget, and determines the department’s three-year rolling planning. The programs included in the departmental program library require the fulfillment of standardized program texts, including the basis for program establishment, implementation subject, expenditure scope, implementation cycle, budget requirements, performance targets, and review results, which serve as the basis for program review and management. For the programs included in the budget arrangement, the central departments and units maintain and update the program implementation, adjustment, performance, carryover balance, and other information in the program library in a timely manner. The ongoing programs included in the budget arrangement shall, in principle, be rolled into the next annual budget. Alternative budget programs that are not included in the budget arrangement can be rolled into the annual program library of future years.

Local governments at all levels have formulated budget implementation measures for their respective departments with reference to the central department’s budget plans. Their budget-management mechanism is similar to that of the central government. The departmental budgets are the basis of the public budget, and the program expenditure budget is the core of the departmental budget and thus the hub of the entire public budget system. The collection of the departmental budgets forms the first-level government public budget.

Program expenditure budgets in the PRC’s departmental budgets bear similarities with Program-Budgeting (McCaffery, 1998: 1768–1769) or the Planning–Programming–Budgeting system that emerged in Western countries such as the United States in the 1960s and 1970s (Jones, 1998: 294–301; Lee et al., 2011: 108–110; Ma and Zhao, 2011: chap. 12).

Compared with the traditional mode, which takes the expenditure department as the unit for disbursing budget funds, the most prominent feature of the program budget lies in its arrangement based on a program structure. Many programs contained in the program structure can be subdivided again, or divided into even smaller components. This breaks down inter-departmental barriers in terms of financial funds and makes the program the core of public funding budgetary arrangements. The key to the program budget is to establish “program packages”, that is, putting the information of various budget items into the program package, so that the program reviewer can clearly determine which programs should be supported by budgetary funds.

The most prominent feature of “program planning and budgeting” (PPB) is the combination of the annual budget with the mid-term and long-term strategic plan on a program basis. It emphasizes budgeting within the framework of a multi-year plan, combining the mid-term and long-term plan with the annual budget, constructing programs to achieve multi-year policy goals. The program here refers to the decomposition and implementation of the plan. The first step of PPB is to develop a target plan. The decision-maker must first determine the basic goals of the organization, and then break them down into some secondary goals; the second step is to construct and select the program according to the target plan. At this stage, the basic goals and secondary goals need to be implemented on the program, and each program is designed to achieve a certain goal. Programs can be further broken down into “program categories”, that is, for all programs that help achieve the same goal, the program categories can be further broken down into “program elements”—which, under the given resource conditions, are helpful to realize all alternative plans for the same problem. Their costs and benefits are compared to select programs. This is a process of “program-orientation” for strategic plans and making choices (Ma and Zhao, 2011: 327–328).

Since the implementation of many programs involves multiple organizations or departments, under PPB, resource allocation generally crosses the boundaries of traditional organizations and departments. As a result, many government agencies are working on multiple programs at the same time, and most programs are implemented by more than one government agency (Ma and Zhao, 2011: 324). In short, program budgeting or PPB emphasize the use of rational analytical tools to construct and select the best programs and to guide and implement fund expenditures through programs; in this way, competition for funding occurs among programs. After the 1970s, although the United States and other countries have abandoned PPB, the program is still the basic unit for government departments to apply for and prepare the budget.

The program review, program ranking, and performance management in the PRC’s program expenditure budget all bear similarities with these countries. The greatest difference is that the PRC’s program expenditure budget is still the result of the expenditure departments’ arrangement of programs after the issuing of a control amount of budget by the financial departments to the expenditure departments. That is to say, the competition for funds occurs between different programs within the department, but under the PPB, the competition for funds occurs between “real” alternative programs, or among the programs of the same category that are established to achieve a common goal. Therefore, the PRC’s program expenditure budget is essentially a department-based PPB system. The various national master plans (programs) are strategic plans that guide the budgets of various departments, and special plans (programs) for departments and industries take the national master plan (program) as their direction. The policies issued by the government and departments signify the implementation of various plans, and the program expenditure budget is the “program-based” operation of the plans and policies.

The direct consequence of the program-centered PB system is this “program-oriented” model of fiscal expenditure. “Program-oriented” fiscal expenditure means that the budget and expenditure of all fiscal funds, other than basic government expenditures, need to be carried out through specific programs. “Programs go before the budget, and the budget goes before expenditures”. Programs become the absolute main body of the fiscal expenditure and budget management of government departments. This is the case whether it is in the central government or local areas (eastern, central, or western PRC). After the “programification” of “service expenditure” at all levels and departments of the government, the actions of the government too became “programified”, and programs became the axis of the operation of the government departments.

Based on departmental budgets, the central government has also successively carried out reforms to collections and payments by the Treasury Department of the Ministry of Finance, centralized government procurement, and government revenue and expenditure classification systems. Centralized collections and payments of the Treasury Department and centralized government procurement are important reforms of the PB system from the aspects of budget implementation and financial fund management, strengthening the entire process of monitoring budget execution and financial funds. The newly established government revenue and expenditure classification system puts a huge amount of fiscal revenue and expenditure classification into a sophisticated grid system, which promotes the rationalization of fiscal management. Supplemented by computer software and information network technology, public budget reform has raised the meticulousness of financial management, but it has also caused great dependence on technical governance in financial management.

Program-based expenditure of local governments: Types and composition

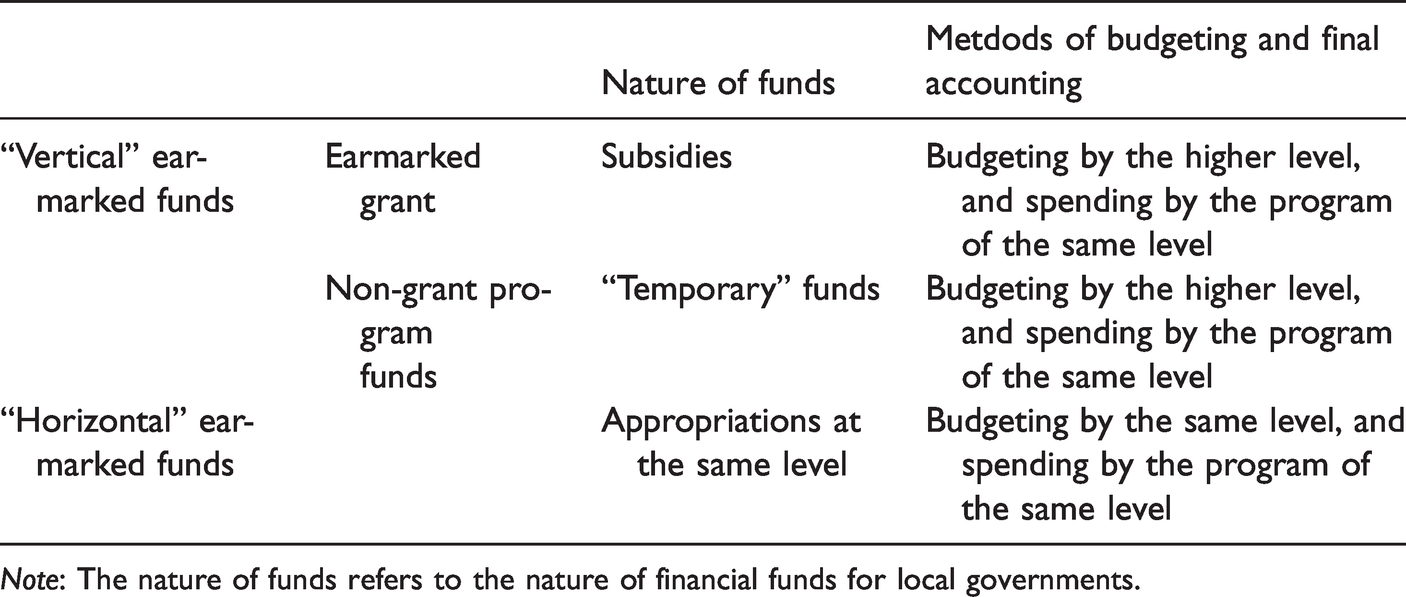

For local governments, in the face of a more complex financial assistance system, the program-based expenditure system is much more complicated than that of the central government, but it is mainly composed of two types of program expenditures, each of a different nature. One is the program expenditures budgeted by government departments at the same level, which can be called “horizontal” earmarked funds; and the other is the program expenditures allocated by higher-level government departments, which can be called “vertical” earmarked funds. Vertical earmarked funds can be divided into two categories: earmarked grants from higher authorities; and non-grant program funds.

Earmarked grants

In multi-level governments, each level of government will set up some grant programs to lower levels. For example, as far as the PRC’s county-level government is concerned, it will receive various grant payments from the central, provincial, and municipal governments, most of which are earmarked grants (Zhou, 2012).

The earmarked grants made by higher-level governments to lower-level governments are not carried out by the finance departments alone to complete the fund review and appropriation procedures. On the contrary, different types of earmarked grants will be managed by different business departments due to their different functions, and the business departments and finance departments jointly conduct fund review and appropriation. Therefore, earmarked grants are also called “shared funds” (Zhou, 2012).

As a result, all central government departments 5 that manage the transfer of earmarked grants from the central government to local governments have two types of earmarked funds: program expenditures in the budgets of the central departments; and earmarked grants allocated by their supervisors. For example, in 2014, the Ministry of Agriculture budgeted program expenditures of 20.368 billion yuan, but this is not all the earmarked funds it holds (Ministry of Agriculture, 2014). It also manages four major items (18 sub-items) of agriculture-related earmarked grants (National Audit Office of People’ s Republic of China, 2015; State Council, 2015). Other departments involved in the management of earmarked grant funds are similar. 6 The earmarked grants of provincial and municipal governments to lower-level governments also operate in accordance with this management system.

In essence, earmarked grants are a form fund “transfer”, and the middle-level government departments only play the role of transmission and transfer. Therefore, strictly speaking, for middle-level governments, earmarked grants do not constitute fiscal revenue. The accounting staff of the financial department records it as a “temporary deposit” in the “current account”, indicating that it is only temporarily “deposited” in the financial system at the same level. Only after the fund is given to the expenditure department, it can be counted as the “subsidy income” of the department by the superior, and it is calculated as the “program expenditure” of the department in the final calculation. For example, when the central government’s earmarked grant for the new rural cooperative medical service reaches the provincial and municipal financial departments, it will be recorded as “temporary funds” by the accounting staff. Only after reaching the county level will it be transferred to the county health department (the county Health and Family Planning Commission). At this time, the final expenditure will be counted as the “subsidy income” of the higher authorities to the county health and family planning commission, and it will be counted as the “program expenditure” of the county Health and Family Planning Commission in the final calculation. The main reason that such a strict distinction is necessary is mainly to avoid double counting of fiscal revenue and expenditure and to ensure accuracy. However, earmarked grants are not necessarily all distributed to the grassroots government to be spent. In some cases, program funds may be spent at the provincial and municipal levels. For example, a central government grant for local water conservancy and transportation programs may be organized and implemented by corresponding provincial departments directly. However, in general, the county-level government is still the final implementer of most earmarked grants.

Non-grant program funds

Another type of “vertical” earmarked funds is non-grant program funds by higher-level government departments to lower-level departments. The so-called “non-grant program funds” of the higher-level government is also called the “direct program expenditures” of the higher-level government (Lee et al., 2011: 425). Simply speaking, most of the program expenditures budgeted by various departments of the higher-level government will eventually be implemented within the different jurisdictions of the lower-level government, which forms a substantial program expenditure for it. For example, each department of the central government budgets a large number of program expenditures every year, but the central government does not have an exclusive administrative jurisdiction. Most of these program expenditures are eventually spent in different provinces (or province-level cities) and regions, which offer great support to the economic and social development of these regions. 7

Due to the covert operational path of such earmarked funds, it is generally difficult for researchers to observe, leading to discussions about fiscal relations between governments which “mostly focus on fiscal transfer payments, while ignoring the importance of direct expenditures (by the higher authorities)” (Lee et al., 2011: 425). In fact, the central government has a large number of program expenditures, and how many of them are allocated to certain provinces (or province-level cities) and districts, and how much of a provincial government’s program expenditures are spent in certain cities (or counties), will have a great impact on different regions. The reason why it is called “non-grant program funds” is related to the nature of earmarked funds and the relationship between budget and final accounts. From the perspective of the budget and final accounts, earmarked funds belong to program expenditures in the budget of the higher-level government departments, rather than the earmarked grants from the higher level to the lower level. In the specific implementation process, if these programs are directly organized and implemented by the higher-level government departments, the funds will also be directly allocated by the higher-level financial departments. If it is allocated to lower-level government departments for organization and implementation, the program management process and earmarked grant are basically in line with each other. However, for local governments, the nature of the funds is not the earmarked grant of the higher-level government, but the direct program expenditure of the higher-level government. It cannot be included in the “subsidy income”, nor can it be finalized as the “program expenditures”. It can only be counted as “temporary receipts” or “temporary payments”.

Compared with earmarked grants, non-grant funds by higher-level government departments constitute a more sophisticated funding system. Earmarked grants are limited to some departments for management, but almost any central government department has a large number of program expenditure budgets, most of which will be implemented by local organizations. Therefore, the coverage of non-grant program funds is more extensive than that of earmarked grants.

For local governments, there is not much difference between earmarked grants and non-grant program funds. They all need to be acquired in accordance with the procedures of program application and approval, and they must also be subject to the supervision and inspection of higher-level authorities. They are all “programs” obtained by local officials from higher authorities. In terms of the program management process of the higher-level government departments, the difference between the two is not significant; only that the earmarked grant must be allocated to the expenditures of lower-level government departments, with a faster speed of allocation than that of the program expenditures budgeted by the department at the same level, so as to set aside more time for the local government to implement the programs. For this reason, there has been a violation of the central government’s compilation and reporting of its earmarked grants to local governments into the budget items of the departments at the same level. 8

Horizontal program expenditures at the same level

Compared with the “vertical” earmarked funds allocated by higher-level government departments, the program expenditures of local government departments are “horizontally” allocated to business departments by same-level financial departments, a situation in which local government departments have more flexibility and autonomy. The “horizontal” earmarked funds obtained by local government departments also include earmarked funds allocated to other departments “horizontally” by some departments with the right to allocate secondary budgets at the local level. Typically, the National Development and Reform Commission and the Science and Technology Bureau allocate earmarked funds to other government departments at the same level.

The sources and operating mechanisms of the two types of earmarked funds, vertical and horizontal, are quite different (see Table 1), but they are essentially program expenditures of different levels of government departments. In terms of “vertical” earmarked funds, whether they are earmarked grants or non-grant program funds, both are essentially program expenditures budgeted by higher-level government departments, with similar program allocation and management mechanisms, except that the former is carried out by the higher-level government, but must be transferred to lower-level government departments for expenditure and final accounting by lower-level governments, while the latter is directly subject to budgeting and final accounting by higher-level government departments. Therefore, we should not separate the earmarked grant from the overall government budget system for discussion, as it is an important part of the higher-level government budget. It is essentially a special item of expenditure in the budget of the higher-level government department; it is budgeted in the form of program expenditure in the department budget, but it must be allocated to lower-level government expenditures and be included in its income and expenditure final accounts of lower-level government departments; it separately belongs to two levels of government in terms of budget and final accounts, and the budget unit and final account unit are separated from each other.

Three types of earmarked funds for local governments.

Note: The nature of funds refers to the nature of financial funds for local governments.

It can be observed that the two types of “vertical” and “horizontal” earmarked funds are two different “fund flows” that complement each other in terms of function. They can be assembled and reorganized at the local government level, and the composition of the two “fund flows” determines the fiscal structure of the local government (Jiao, 2020).

The program expenditure of the local government is much larger than earmarked grants by higher-level government departments, and these earmarked grants are only a part of the expenditure of the local government. From the perspective of the budgeting management system, the “vertical” earmarked grant is a relatively special program expenditure of a higher-level government department. Like “vertical” non-grant program funds, it is part of the government’s overall PB system and is not separated from the government budgeting system. Non-grant program funds and local department budget program expenditures are also important sources of local government program expenditures. Of course, the composition differs in different regions: in the eastern region, program expenditures mainly come from “horizontal” earmarked funds in the budgets of same-level departments. While in the central and western regions, they rely more on “vertical” earmarked funds such as earmarked grants from higher authorities and non-grant program funds.

As a result, fiscal expenditure is also highly “program-oriented”, and the fiscal autonomy of local governments in the eastern region is significantly stronger than that of the central and western regions. Moreover, even for grassroots governments (municipal and county-level governments) that are highly dependent on “vertical” earmarked funds, the fiscal autonomy of the eastern region is stronger than that of the central and western regions. The reason is that “vertical” earmarked funds of municipal and county-level governments in the eastern region mainly come from the provincial government, while the central and western regions mainly rely on the central government. Earmarked funds from the central government generally have to be “rechecked” by the provincial government, and that aggravates the constraints on the application and implementation of local government programs. Therefore, the reason for the differences in the fiscal autonomy of different regions and different levels of government departments does not lie in the program expenditure budgeting system itself, but in the differences in the operating mechanisms of different types of program expenditures.

From program expenditure to the PS

Can these “horizontal” and “vertical” program expenditures be effectively integrated in the PB process by local governments?

In an ideal and standard sense, it is better to budget most of the local government’s program expenditures at the beginning of the year, and government departments will implement the budget report during the year. The financial department is responsible for the entire process of fund management. Except in special circumstances, there should be no large-scale adjustments or additional budgets. In fact, the public budgets of governments at all levels are far from meeting this requirement. The most important point is that the disbursement rate for the so-called “start-of-the-fiscal-year itemized budget” for various program expenditures is not high.

The disbursement rate for the “start-of-the-fiscal-year itemized budget” refers to the proportion of funds that can be directly budgeted and implemented to the total annual budget approved by the financial department to the expenditure department. Simply speaking, in the various expenditures of government departments, it refers to how much funding can be clearly budgeted at the beginning of the year to specific programs that can be directly organized and implemented. Affected by various factors, the start-of-the-fiscal-year itemized budget report is very approximate. Many funds have not been detailed to specific departments and programs. Instead, they are reserved in financial departments or departments with budget allocation rights for secondary distribution in the middle of the year. For example, in the budget of the Ministry of Finance at the beginning of the year, it is confirmed that a certain ministry has expenditure funds for a certain program, but because it has not been directed to specific items, it will be reserved by the Ministry of Finance, and the ministry in question together with the Ministry of Finance will negotiate and allocate them to the specific programs in the middle of the year. For another example, if the central government budgeted an earmarked grant to a local government at the beginning of the year, which was centrally managed by a particular ministry, but it was not itemized to specific regions and programs at the beginning of the year, it would be subject to secondary allocation by the particular ministry and the Ministry of Finance in the middle of the year, and only then would it be given itemized implementation to specific regions and programs.

Following PB reform, the disbursement rate of central government departments’ start-of-the-fiscal-year itemized budgets has not been high. For example, in the expenditure budget of the central government in 2011, 201.054 billion yuan failed to be detailed to specific departments and programs at the beginning of the year, accounting for 12% of the total budgetary expenditure; the central government-level infrastructure expenditure managed by the National Development and Reform Commission was refined at the beginning of the year. The disbursement rate was only 47%, which did not meet the requirement of 75% (State Council, 2012). In recent years, the central government has adopted various measures to increase the disbursement rate of start-of-the-fiscal-year budgets. However, by 2015, the central government’s expenditures on same-level programs that had failed to be detailed to specific departments and programs was still 205.275 billion yuan (accounting for 13% of total expenditure) (State Council, 2016).

The disbursement rate at which the central government’s budget for earmarked grants to local governments at the beginning of the year was lower. Most of the central government’s budgets for local tax refunds and general transfer payments are “formula” budgets, which can easily be detailed to specific regions at the beginning of the year. The case for an earmarked grant is different. The funds are allocated according to the “program approach” and the proportion that is detailed to specific regions and programs at the beginning of the year is very low. For example, in 2011, in the budget of transfer payments from the central government to local governments, 1,630.969 billion yuan (50%) was not detailed and implemented in specific regions, most of which were earmarked grants, accounting for more than 80% of the total amount that was not detailed to specific regions and programs (State Council, 2012). By 2015, 1,458.006 billion yuan of transfer payments from the central government to local governments were still not budgeted to the regions at the beginning of the year, accounting for about a quarter of the total transfer payments, of which nearly 70% were earmarked grants, accounting for 47% of the total earmarked grants (Ministry of Finance, 2015).

The departmental budgets of local government departments at the beginning of the fiscal year are especially affected by the status of funds from higher-level authorities, therefore, the disbursement rate of their itemized budgets tends to be lower. Since only a small part of the “vertical” earmarked funds (including earmarked grants and non-grant program funds) to the local governments can be clearly detailed and funded at the beginning of the year, the local government must consider the uncertainties of “vertical” earmarked funds when arranging the budget. Therefore, local governments often make alternative plans for some programs when budgeting. First, they actively prepare to apply for earmarked funding support from the higher levels, and if this fails, then they attempt to acquire the public budget from the same-level government. As a result, in areas with low levels of local financial self-sufficiency, the local government budget at the beginning of the year is bound to be incomplete, and most programs can only be adjusted and determined in the middle of the year based on the support of the vertical earmarked funds. Large-scale adjustments and additions to departmental budgets are inevitable. For example, the total basic expenditure and program expenditure approved by Yinchuan city, Ningxia Hui Autonomous Region, in early 2013 was 1.701 billion yuan, which accounted for only 14.84% of the total budgetary expenditure approved by the National People’s Congress (Yinchuan Municipal Auditing Bureau, 2013). Among this, basic expenditure was 1.32 billion yuan and program expenditure were only 0.38 billion yuan, which made the departmental budget effectively useless. In 2014, the Ministry of Finance started to include “government invested programs” into the departmental budget for approval at the beginning of the year, which increased the disbursement rate of the budgets. In 2015, the approved budget to the department at the beginning of the year was 8.62 billion yuan, and the budget approval rate at the beginning of the year was only about 65%.

Therefore, whether it is the expenditure budget of the government at the same level or the vertical transfer payment budget from the central government, there is a large proportion of funds at the beginning of the year that cannot be itemized and funded, so they are retained in financial departments, only after which are they divided into parts for secondary distribution in the middle of the year. In addition, even for the budgets approved by the government departments at the beginning of the fiscal year, there are many funds that have not been itemized to specific programs. For example, in 2011, in the budget approved by the central government departments at the beginning of the year, 87.45 billion yuan (45%) of the expenditure budget for 85 programs of 30 departments failed to be fully itemized, and a secondary allocation was made during implementation (State Council, 2012). Although some earmarked grants were itemized to specific areas, they were not refined to specific projects, and a second round of distribution was still required.

It is thus clear that the practical form of the PB system has deviated from the original system design. A large amount of government funding cannot be normatively budgeted to specific departments, regions, and programs at the beginning of the year, and is only able to be reserved in the Ministry of Finance in divided portions. In essence, this is a “relic” of the pre-reform budgeting system. However, compared with the situation before the reform, the current expenditure process of reserved funds has been greatly changed. Before the reform, the government budget was prepared according to the functional budget, and the fiscal funds were divided and allotted to government departments, so that they could decide the specific expenditure items. The financial departments were only responsible for the supervision of funds. After the reform, although many funds are still reserved in certain portions at the beginning of the year, they are not directly approved to the government departments but reserved in the finance departments. In the middle of the year, the finance department and the expenditure departments negotiate the expenditure plan, and then proceed with spending the funds on specific programs. In fact, it is an action that postpones the program expenditure budget from the beginning to the middle of the year. Specific programs are indispensable to apply for expenditure funds from the finance departments. In the practice of governance, program expenditures are reflected in the various governance programs we encountered in field research.

As far as the local government is concerned, the various “vertical” and “horizontal” earmarked funds it organizes and implements each year have only partially refined the budget for specific programs at the beginning of the year, and there are still many funds that have to be acquired by “running for programs” in the middle of the year. A typical result is the behavior of local governments, which is called “paobu qianjin” (running to ministers for money). This means that in order to obtain more “vertical” earmarked funds, local cadres must make great efforts to lobby these ministries and apply various informal relations and rules. Moreover, since the local government also set aside a large amount of fiscal funding in portions in budgeting at the beginning of the year, government departments also constantly lobbied the budgeting department at the same level (the finance departments) and the department with budget-allocation power (the Development and Reform Commission) in the middle of the year, to obtain more program funds. Furthermore, even for those program expenditures that had been refined to specific programs at the beginning of the year, they were the result of complicated interactions between the financial department and the expenditure department, between the higher-level and lower-level business departments, and between the supervisors and department leaders. These programs actually have the distinctive feature of “running for programs”, only that they were earlier, that is, before the budget preparation at the beginning of the year.

Therefore, whether it is a program with a detailed budget in place at the beginning of the year or a program for secondary allocation in the middle of the year, it cannot do without the complex lobbying of and negotiation with government officials at all levels. In the process of “running for programs”, various formal and informal factors overlap and form an extremely complex political landscape. The practical form of the public budget system deviates from the normative form, which in fact further strengthens the informal operation of the program budget allocation process, and further gives the program a “magical” quality: whether for the program’s “contract-issuing party” or the program’s “contractor”, the program seems to be the “magic ring” in their hands. They have the power to attract competition from multiple parties, so that local officials must do their best to “run for the program”. At the same time, it is the focus of supervision, and the program may lead to tragedies due to carelessness. It is the deviation of the public budget system from a normative form that directly aggravates the complexity of the operation of the PB system. The complex interaction of various formal and informal factors makes the PS stand out from the PB process and become the pivot in the operation of the entire government organization.

It can be seen that the so-called “program” here has the meaning of “program system”, that is, although the program has the characteristics of a temporary organization with an expected goal in the budget and implementation process, the budgeting, application, allocation, adaptation, implementation, supervision, and response of the program have gone beyond the characteristics of the fact of a single program and have become the mechanism for the joint operation of the national social system (Qu, 2012). In general, the program-centered PB system 9 has in practice rapidly incorporated multiple formal and informal factors such as administration and personnel, forming a comprehensive and thorough program organization network, and shaping a new structural form and governance system within the government. It is not only the pivot of the PB system, but also transcends the PB process, becoming an overall governance mechanism that “affects the whole body through a slight move” in the operation of the government.

From the perspective of structural form, as Qu (2012) stated, the PS possesses the structural characteristics of a new double-track system. The PB reform has established a PB system with the PS as the core in all levels of governments and various departments. As the core budgeting agency of each level of government, the Ministry of Finance and the subnational financial departments are responsible for coordinating the public budget of the government at their same level; as such, their status and power have been greatly strengthened. A well-structured and well-organized PB system has “grown” within the government. As a result, two mutually embedded structures have been formed within each government: the original institutionalized bureaucratic system of the government and the program-centered PB system, together molding a “dual-track system” organizational structure.

From the perspective of the operating mechanism, on the one hand, the PS is highly dependent on the government bureaucracy. Whether for program budgeting or program organization and implementation, they are carried out on the basis of government departments, rather than completely restructuring the government’s organizational structure based on programs. Generally speaking, the PS is a system based on government departments, thus it adopts a so-called “departmental” program-management model (Kerzner, 2010: 86) In the case of inter-departmental communication and cooperation required in some large-scale programs, higher-level leaders would take the lead, or a comprehensive department would organize and coordinate the programs. On the other hand, the introduction of the PS, especially in the process of program organization and implementation, has also had a great impact on the operating mechanism of government departments. In order to smoothly promote the application, organization, and implementation of programs, various government departments and staff would be assigned to specific programs, and programs would become the central task of the department.

Apparently, the PS has been highly embedded in the government bureaucracy, regardless of its structure or operating mechanism. The PS and the bureaucratic system operate in mutual embeddedness. On the one hand, the organizational structure, personnel network, and incentive mechanism of the government bureaucracy will have a profound impact on the operation of the PS. At the same time, the full spread of the PS within the government will inevitably “disturb” the original operational and governance processes of the government. In practice, the means of correlation and interaction between the PS and the state bureaucracy have become the focus of the problem. The PS has actually become an institutional platform that accommodates multiple political relationships (between central and local governments, political and administrative bodies, financial and expenditure departments, formal rules and informal operations, etc.). These factors have intertwined, superimposed, exhibited, and collided to become “power containers” (Giddens, 1998), therefore, it has a significant equivalent to that of the “total social fact” referred to by Mauss (2002).

Systematic objectives and intrinsic dilemmas of the PS

In summary, the PS is the core and basis of the PRC’s PB system, and as a budget-management system it has been commonly adopted by governments at all levels across the country. The central-to-local earmarked grant system is an organic part of the national PB system, an important link in the fiscal expenditure relationship between the central and local governments, and an important component of the PS, but we cannot understand it separately from the overall budgeting system.

The main task of the program-centered PB system is to respond to the challenges of the era of big government, and to effectively spend the huge public financial funds in a normative manner to establish a modern “budget state”. Therefore, seen from the perspective of systemic content and organizational targets, the PS is not merely a dual-track logic of “storing” and “increment”, since its original intention was not to get rid of the constraints of bureaucracy to “cultivate” a kind of “incremental” reform (Qu, 2012), and it was not meant to establish another administrative system that transcends the competitive authorization in bureaucracy (She and Chen, 2011). In essence, the PS is not a way of getting rid of or surpassing the bureaucracy, as it serves as the state’s initiative to improve and supplement the government bureaucracy, but a continuation and a developed version of modern state power construction in the new era (Ma, 2005).

To be specific, the program-centered PB system attempts to respond to the great challenges from the big government era in two aspects: the first is to effect guidance, restriction, and control over government actions and improve the accountability of said actions; and the second is to enhance the government’s capacity to respond to the demands of society and to promote a “service-oriented” government construction. However, in practice, the two objectives of the PS have obvious tension and fall into an intrinsic dilemma.

The foremost target of program-centered PB reform is to use a refined budget-management system to guide and restrict the government’s arbitrary actions, that is, “solidifying budget constraints” to improve government transparency and accountability. Schick (1990) believed that the government’s governance capacity depends to a great extent on the government’s budgeting capacity. Without restrictions and regulations on budgeting, it is impossible to have a huge and active government. It is precisely based on this consideration that specific reform practices put more attention on how to guide and restrain government behavior and “solidify budget constraints” (Xie, 2011).

The PB reform attempts to establish a “control-oriented” and a “technology-oriented” budgeting management system. It has established administrative control in the budget field within the government, that is, through departmental budgeting reforms the financial department is transformed into a real “core budget organization” which centralizes the power of fiscal allocation, controls the budget of each department, and realizes the “horizontal centralization” 10 of the right of budget allocation, in order to alter the previous chaos and disorder in the dispersion and management of fiscal funds. The centralized collection and payment system of the Treasury Department and the centralized government procurement system enable the Ministry of Finance and subnational finance departments to “externally control” the spending behaviors of expenditure departments and realize the whole-process monitoring of financial funds. Its “technical orientation” is embodied in its dependence on program specifications, expertise, and modern information network technology. The newly established government revenue and expenditure classification system is an exquisite and complex classification grid of fiscal funds. The government’s annual fiscal revenue and expenditure must be included in classification system as required, which lays the foundation for the granular management of fiscal funds. The network construction represented by the “Government Finance Management Information System” 11 makes financial management a highly informatized and technical process. It attempts to record in details the ins and outs of any financial fund revenue and expenditure of any unit at any point in time, and gradually realize the automatic compilation of the state budget, the instant summary of the execution of revenue and expenditure and the final account. Program budget management activities represented by program declaration, budget review, and performance target management decompose the core process of the public budget into highly normative and standardized administrative activities. The “third-party institutions” and expertise comprehensively enter the PB process, providing an “objective basis” for legitimacy of government behaviors.

The program-centered PB system is a governance mechanism that takes refined public budgets as the core and relies on modern information network technology to improve the rationality of the full cycle of financial management (budgeting, execution, and supervision). Although the practice of public budgets deviates to a certain extent from the normative form, the measures of the reform have greatly strengthened the constraints on fiscal funds and expenditures compared with those before the reform, and the degree of standardization of public budgets and expenditures has also been greatly improved. Therefore, the PS is a typical technology governance mechanism, with rationalization is its basic spirit, professionalization and standardization as its main characteristics, and the “program-oriented” performance in grassroots governance as the general consequence.

The underlying goal of the PB reform is to try to use the PS as a carrier to respond to the public’s common demands, hoping to operationalize these demands as specific programs that can be “identified” and absorbed by the government, and ultimately improving the government’s capacity to respond to public demand.

The public budget is an important link for the government in providing public goods and services. The key is to establish an accurate matching/correspondence relationship between people’s needs and preferences and the government’s public expenditures. As Key (1940) stated, the biggest problem with the budget is “to determine how much money should be distributed to activity A instead of activity B and give the reason for it”. The process of PB is designed to respond to and absorb the common demands and preferences of society and the public. The government’s budget statement is ultimately a package of choices and programs which should be a comprehensive response to the public needs and preferences of the people. The real needs and preferences of the people precisely corresponding to the package of programs of government budget is one of the core purposes of public budgets, which is called “preference-matching” by Lockwood (2002, 2006). The academic community calls the government’s ability to effectively implement “preference-matching” and use fiscal funds in a responsible manner as the “capacity to budget” (Ma, 2011). Effectively establishing preference matching is the foundation and core of budgeting. This is also the internal driving force for the Chinese government’s transformation from an “omnipotent regime” to a “service-oriented regime” and from “construction-based finance” to a “public finance” (Gao, 2008). During the planned-economy period, the government was the direct organizer of and participant in economic production, and government actions covered almost all aspects of social production and life. The government was an “omnipotent regime”. Since reform and opening-up, the market economy has developed rapidly. The government has gradually changed from a direct organizer of economic production to a provider of public services, and government finance has gradually marched from “construction-based finance” to “public finance”.

As a provider of public services, only through the PB system can the government collect the public/society’s demands and preferences, transform them into administrative decisions, and ultimately output effective public products and services. However, the “primitive” demand for public goods by society and the people is only a “natural fact”, which cannot be naturally recognized and absorbed by government departments. Only through “program-oriented” packaging can it become an “administrative fact” recognized and adopted by government departments. The needs of society and the people are packaged in accordance with the requirements of a standardized and normative PS, so that they can become specific programs that can be absorbed and identified by the government’s public budget system. This is the “program-based” process of grassroots governance, and also a process of identifying and collecting public demand preferences, to transform them from “natural facts” to “administrative facts”. The “program-based” process of grassroots governance requires the standardization and unification of irregular and diversified public needs, making it a public program that can be recognized and absorbed by government departments.

From the operational point of view, although the practice of the PB system has deviated from the normative form, the degree of rationality in government financial management has been significantly improved, and the guidance and restraint enacted on government actions by public budgets has been significantly enhanced. However, the government’s ability to respond to the needs of society and the people has not been effectively improved. Mismatches between the PS and the public’s demands are still very common, which is the main intrinsic dilemma of the current program system.

There are three main reasons for this dilemma. First, there is inherent tension between “solidifying budget constraints” and improving the ability to respond to public needs. In order to better respond to the public needs and preferences, the PS must maintain strong flexibility in the budgeting and implementation of each program. It is necessary to fully stick to the principle of “one case, one meeting”, and be fully sensitive to the rapidly changing external conditions and take corresponding actions in a timely manner, especially for the PRC, a country in a rapidly changing economic and social environment. However, there is an intrinsic contradiction between the flexibility requirements of the PS and the goal of “solidifying budget constraints”. The objective of “solidifying budget constraints” is to overcome the “soft budget constraints” that have always existed in government operations, that is, that government budgets cannot guide and restrict government operations, and government budget reports become “invalid documents” that can be adjusted and changed at any time. The solidifying of budget constraints is intended to make the public budget truly become the government’s action guide. Government departments can only act within the scope of budget. The “project list” determined by the budget report cannot be adjusted and added to at will, which should strengthen the comprehensive budget implementation and the monitoring of the whole process. Therefore, the program-centered PB system is essentially a system that integrates flexibility and restraint, but its restraining aspect is particularly emphasized in the reform practice, which will affect the government’s sensitivity and flexibility in response to public demands.

Second, the combination of characteristics in rationalization and technical governance of the PS with a highly motivated government governance system often leads to selective “neglect” of public needs. The PS emphasizes standardized, digital, and normative governance processes, trying to fulfill “administrative goals and responsibilities stepwise on a professionally designed indicator system, so as to obtain the legitimacy basis of the administrative process”; this is a typical technical governance mechanism (Qu et al., 2009). However, technology-based governance processes and mechanisms do not necessarily mean that the state’s ability to respond to public needs is enhanced. On the contrary, the excessive rationalization and professionalization of the political machinery may often lead to “idling” in the system, and it will become increasingly “suspended” above society and the people. Therefore, “a major problem faced by the bureaucratized technological governance mechanism is how to place a huge administrative system above the specific experiences and problems of social and economic life, instead of losing its affinity with the grassroots society” (Qu et al., 2009). Especially in the PRC, the technological governance mechanism of the PS is operated on the basis of a strong incentive system that combines political centralization and economic decentralization (Blanchard and Shleifer, 2001; Zhang, 2006; Zhou, 2007). The combination of a technological governance mechanism and a highly incentivized system often leads to the interaction of the disadvantages of both aspects, resulting in the worst effect in governance. The main reason is that, after the combination of the PS and the strong incentive system, standardized, normative, and technology-based governance mechanisms pretend to have “procedural legitimacy” on the performance goals of the strong incentive system, while the public needs of the society and people that the PS should respond to are often “absorbed” by the performance goals of the highly incentivized system, causing a serious dislocation between the PS and public demand preferences.

Finally, for the rationalization and technical governance characteristics of the PS, there is tension between the “locality” and the mobility of grassroots society. The PS as a rational and technology-based governance mechanism has the main advantage of adopting and utilizing standardized technological knowledge, while the biggest drawback is the shielding and expulsion of local practical knowledge. 12 Technical knowledge is not the whole body of knowledge. Some knowledge about a specific time and place may be disorganized or difficult to be organized. But this kind of knowledge is very important to human life. Moreover, it is difficult to turn this kind of knowledge into statistics, thus it cannot be passed to any central authority in the form of statistical data (Hayek, 2003: 96–101). However, in the context of grassroots society, Chinese society still has a strong feature of “localism”: the grassroots society itself has not formed a highly regularized and standardized society, and the current grassroots society still has strong characteristics of mobility. These irregular, localized, fragmented, and mobile public needs are very difficult to turn into “programs” through technical and standardized methods. It is very difficult for the PS to fully respond to and effectively absorb them, but they are very important to the daily life of people. How to improve the ability of the PS to respond to the quotidian and mobile public needs of the grassroots society is one of the difficulties that needs to be overcome in the practice of the system.

Conclusions and discussions

After reforming the tax-sharing system, the absorptive capacity and efficiency of the Chinese government was greatly expanded and the PRC rapidly stepped into a “big government” era. The government’s potential for providing public products and services has been greatly enhanced; however, in the meantime, tremendous challenges to government’s governance system and governance capacity have been posed.

Through learning from the historical experiences of Western countries, the PRC has also tried to establish a modern “budget state” through PB reforms to respond to the challenges of the “big government” era. To this end, the PRC has promoted and established a PB system centered on departmental budgets and program-based expenditure. Program expenditure is not only the core of departmental budgets, but also the hub of the PB system, thus forming a new state governance system, the PS. It can be concluded that, in essence, the PS is not a way of getting rid of or surpassing the bureaucracy, but serves as the state’s initiative to improve and supplement the government bureaucracy, and it is a continuation and a developed version of modern state power construction in the new era. The PS is a typical technological governance mechanism, with rationalization is its basic spirit, professionalization and standardization as its main characteristics, and “program-oriented” performance in grassroots governance as the general outcome.