Abstract

The hybrid annuity model is relatively new in the Indian economy as the private investors are still reluctant to adopt this public–private partnership model. This paper aims at developing and proposing a suitable hybrid annuity model for a highway project in Gujarat, India. A detailed financial analysis has been carried out to compute the net present value and internal rate of return. It has been observed that the breakeven and payback period is obtained after about 8 to 9 years. The corresponding net present value is about 28.253 million Indian rupee. The corresponding internal rate of return as observed from the analysis is about 20%. Thereby, the HAM model has been found to be techno-economically suitable and feasible for the development of new highways in Indian subcontinent particularly in the stretches of low traffic density.

Keywords

Introduction

India's rapid industrialization has resulted in a considerable increase in the demand for high-quality transport systems, including roads, bridges, tunnels, highways, etc. By the late 1970s, the Indian government became conscious of highway construction's importance for its socio-economic development (Patwardhan 2016). Ever since, it is spending substantial amounts for the development of ambitious and large-scale national highway (NH) projects. However, as included in each 5-year plan, infrastructure projects’ construction is critical for national development.

In India, road projects are typically awarded on the following models: design, service, transmission build–operate–transfer (BOT) contracts, BOT-free contracts, and engineering, procurement, and construction (EPC) contracts. In January 2016, the government approved a hybrid annuity model (HAM) to construct NH to accelerate road construction. HAM is superior to the previous BOT models, because of low traffic and leverage balance sheets, by renewing interest among the private developers (Patwardhan 2016). HAM aims to increase the number of projects carried out within the government's resources and revive the private sector's involvement. Under HAM, the government authorities are responsible for collecting highway projects built under the hybrid rate model. The government's latest HAM combines two current public–private partnership (PPP) models—EPC and BOT annuity. The primary characteristics of current PPP models are discussed in more detail to understand the HAM model (Ministry of Road Transport and Highways, 2016).

HAM combines EPC and BOT models, with the government and private sector sharing the overall project cost in a 40:60 ratio. As a result, during the construction phase, the government shares 40% of the total project cost and releases funds based on the work's success. On the other hand, the private player acquires capital in the form of equity and loans. As a result, the private player is forced to put less equity since the total need is less than 60% (Jain et al. 2019). The money is then paid to the concessionaire in semi-annuities by the government. As a result, the government assumes all risks, including toll collection, and ensures that the private player's recovery amount is paid within a specified time frame. The following are the PPP models which are quite popular in an Indian scenario. Some major salient features of these models are as follows.

Build–operate–transfer toll

In this toll-based BOT model, a developer constructs the road and can recover his investment through toll collection (Yescombe 2007). This toll collection will be over a long period of nearly 30 years in most cases. There is repayment of the government's amount to the developer as he earns his money invested from tolls (Asian Development Bank, 2008). Sometimes, due to more miniature toll collection per annum, the developers face issues recovering the money (Delmon 2017).

Build–operate–transfer annuity

In BOT annuity, a developer builds a highway, operates it for a specified duration, and transfers it back to the government (Asian Development Bank, 2008). The government starts payment to the developer after the project launches commercially. Payment will be made on a semi-annual basis (Yescombe 2007; Delmon 2017).

Engineering, procurement, and construction

Under this model, the project's detailed engineering design, procurement of all the equipment and materials, and then construction to deliver a functioning facility or asset are carried out by the developer and transferred to authority (Delmon 2017). Under this model, the developer must deliver the facility for a guaranteed price within the specified period, or else the failure may incur monetary liabilities (Yescombe 2007; Asian Development Bank, 2008).

Viability gap funding scheme

Viability gap funding is the Government of India's provision to financially support the PPP project's viability gap during the construction period. Viability gap funding of about 20% of the total project cost, may be obtained from Asian Development Bank (ADB, 2008). The private sector is selected from the open public bidding, and hence, the scheme is only confined to the PPP projects. In the first 2 years of the scheme's operation, a project meeting the eligibility criteria will be funded first (Yescombe 2007; Delmon 2017).

So, the objective of the paper is to propose a PPP model framework which suits the requirements of Gujarat. It has been observed that for state highways (SH) and NH in Gujarat, HAM appears to be quite feasible, thereby a detailed analysis for the development of the model framework has been carried out in this paper.

Literature review

India's highway sector has received BOT annuity as a suitably adopted model before testing it over a decade in 2006. Project viability depends on private funding via toll collection for commercially viable projects. Similarly, viability gap funding and annuity are also granted when a project is not feasible via toll collection. After 2012, private ventures evaporated with unviable offers and got for more than 40 projects, requiring the government's strategy negotiation. As a prompt reaction, the government moved to standard EPC contracting. Crucial public finance commitments from the stressed private consortium are required (Patwardhan 2016).

Prospects of infrastructure project finance for large valued projects

Esty (1999) recommended improved techniques for valuing large-scale projects. Author has stated that the project sponsors usually use one of the two methods to value equity investments in projects. Either they value equity indirectly by discounting free cash flows or weighted average cost of capital. Complex tools are required for valuing complex investments. Three ways to improve the discounting process in equity cash flow valuation include (a) multiple discount rates, (b) quasi-market valuation, and (c) cash flow adjustment. Monte Carlo simulation and real option analysis would make the valuation more accurate. All these recommendations would enable better decision-making for implementation of complex projects (Esty 1999).

Furthermore, Kumar, Srivastava, and Tabash (2021) carried out a systematic literature review for finding out and outlining the existing research in the field of infrastructure project finance. Authors highlighted the advantages of adopting infrastructure project finance structures in risky and highly uncertain environment. The findings of their study indicate that adequate research in the area of infrastructure project finance is also lacking. Also, with increased usage of infrastructure project finance, in developing and underdeveloped economies, the infrastructure financing is linked to overcome institutional voids, socio-economic risks, and inter-partner differences. This research would open up avenues for future research.

Hybrid annuity model

This model is a variant of PPP and may be adopted for successfully viable BOT (toll) mode. Under this model, inflation-adjusted construction support of 40% is given by the government to the concessionaire during the construction period, in the five-equal installment of 8% each of the bid project cost, and the rest of the 60% of the bid project cost is arranged by the concessionaire during the construction period. During the operation period, the government paid this 60% cost to the concessionaire in semi-annuities within the specified concession period, and interest in reducing balance, operation, and maintenance cost is also paid semi-annually by the government (Jain et al. 2019). The growth of the infrastructure industry and budgetary constraints has prompted the creation of numerous PPP models in emerging nations. The implementation of current PPP models is fraught with financial difficulties in the Indian highway industry. The purpose of the research is to create a financial risk model for HAM in road infrastructure projects from the viewpoint of the government (Gilbile and Vyas 2021). HAM takes into account the participation of both the public and private sectors. Different risk allocations and mixed initial investments set HAM apart from other PPP models. Since PPP models are frequently long term, both parties must assess the project's financial viability. Using the net present worth (NPW)-at-risk technique, this study seeks to construct a financial risk model. By allocating probability distributions to risk parameters, the at-risk tool performs Monte Carlo simulation. Additionally, the study contrasts the HAM's federal and state regulations. The results from the constructed financial model demonstrate variation in both essential risk factors and NPW. Public authorities can use this financial model as a decision-making tool, and specific mitigation approaches can be implemented to optimize project features for the selected significant risk parameter (Gilbile and Vyas 2022).

Mahalingam (2009) discussed how to formalize and express the fundamental difficulties that PPP accomplishments face explicit to the urban Indian perspective and investigate a portion of the current techniques proposed to deliver these obstructions. He recommends a constrained arrangement of different methodologies that can be utilized later to advance enormous sustainable PPP ventures. According to Shrestha et al. (2017), government officials’ risk mitigation in developing countries is less, as they are unaware of PPP projects’ risk compared to developed countries. Various experts have used different methodologies for identifying risk in PPP modes and their responsibility. Kumar et al. (2017) discussed different PPP models used in highway construction in India. They concluded that the model's choice is based on risk allocation and the project's financial viability. For 30 years, PPP models have been immensely used to fulfill goals related to accomplish sustainability. PPP is the only way to handle risk and rewards between public and private partners using contractual arrangements. Garg and Mahapatra (2019) studied the HAM model's risk allocation in the Indian PPP context. They analyzed the risk involved in HAM compared to other models and its distribution. Combinatorial aspects of bid also play an essential role in awarding contracts. Jain et al. (2019) studied PPP and its challenges with adopting the HAM model and its alternative. They identify 13 factors for evaluating HAM and conclude using public response and survey that funding through government and lack of transparency leads to avoiding parameter for HAM. The other two criteria are that financial risk and funding of HAM are a challenge for the government for a shorter span. They suggested the adoption of the new model after modification in the existing HAM model.

Singh and Madurwar (2019) compared the model features of the concessionaire agreement between HAM and design, build, finance, operate, and transfer and concluded that HAM is a potential solution for road development. Also, it gives pace for awarding a contract by addressing earlier toll and annuity base models.

Due to the greater convergence across the different methods and also that there was greater consensus among project stakeholders on the critical success or failure factors of road PPP projects (Nallathiga et al. 2018). We identified that no study was taken for a particular region as factors affecting the project's viability and failure are local and regional. So, here we had a scope for identifying the risk and success factors commonly known as critical factors for Gujarat, a state in western India. Existing Indian and specific Gujarat research on the subject has significant flaws, highlighting the necessity for an India (Gujarat)-based study to explain road PPP project (Vasudevan, Goenka and Garvin 2018).

Reviewing the available literature, it was observed that BOT (toll) is the best suitable model for PPP road implementation in the world. The same applies in the Indian context, but the scenario observed is pessimistic for adopting the BOT (toll) model in India and especially in the Gujarat region to develop the new road construction and maintenance of existing roads in certain places. Therefore, the need to introduce a new PPP model is arising and implemented in January 2016, known as HAM. In contrast to prior PPP models, which sought risk transfers, the HAM model sought risk sharing. It also aimed to make both the public and private sectors more accountable to their responsibilities by implementing a slew of sanctions for failing to keep pledges (Garg and Dayal 2020).

After implementing the new model study, many researchers started working on the feasibility and requirement of modification in the existing HAM model. As suggested by Jain et al. (2019), this HAM may be used after few modifications lead to developing a new framework implemented with HAM in the Gujarat region. The main objectives for choosing this particular study are as follows: (a) existing empirical studies are limited and somewhat out of date, (b) few studies have taken into account the sector-specific factors that play an essential role in explaining project success and failure, and (c) no studies focused on a specific mode have examined project issues and performance.

Evaluation of PPP models through MCDM techniques

According to Garg and Dayal (2020), there was a complete revamp in the PPP models in the later part of the last decade. The effect of critical success factors on early, intermediate, and late stage of the project has been identified. The changes in policies, strategies, and practices have been discussed. Comparing with the existing literature, authors observed that there were significant changes in the drivers which determine the development of business models. Jokar, Aminnejad, and Lork (2021) proposed a framework for risk management of PPP highway projects. Fuzzy multi-criteria decision-making (MCDM) was used for risk analysis. Quantitative analysis was carried out by fuzzy analytical hierarchy process and fuzzy technique for order preference for similarity to ideal solution. Authors observed that legal, political, construction, operational, and financing risks have the maximum impact on the PPP highway projects. The work carried out by Dolla and Laishram (2020) was primarily on the sustainability component which can be incorporated into the PPP models. Procurement process can be made sustainable which would compel the private partner to develop mechanisms that would make the project sustainable. Authors applied MCDM techniques like analytical network process for bid evaluation. Furthermore, Sarkar and Sheth (2021) were the main proponents to work on sustainable mass rapid transit systems. Authors proposed a sustainable PPP model for bus rapid transit system for Ahmedabad, India. The proposed model would use clean and green technologies and reduce the carbon emissions.

Basar et al. (2021) worked on the obstacles faced by the PPP projects particularly in China. Authors also have recommended appropriate mitigation measures that would enable more successful implementation of the PPP model. The study carried out by Ramadhanti, Karsaman, and Wibowo (2022) was primarily on development of HAM models by the Government of India in 2016 with the objective of reducing the concessionaire's risk on toll road project funding. Authors made an attempt to study the feasibility of the HAM model on the toll road in Indonesia. Their findings reveal that from stakeholder's perspective, HAM can be implemented in Indonesia toll roads particularly the roads located in the rural areas.

Shadow toll models

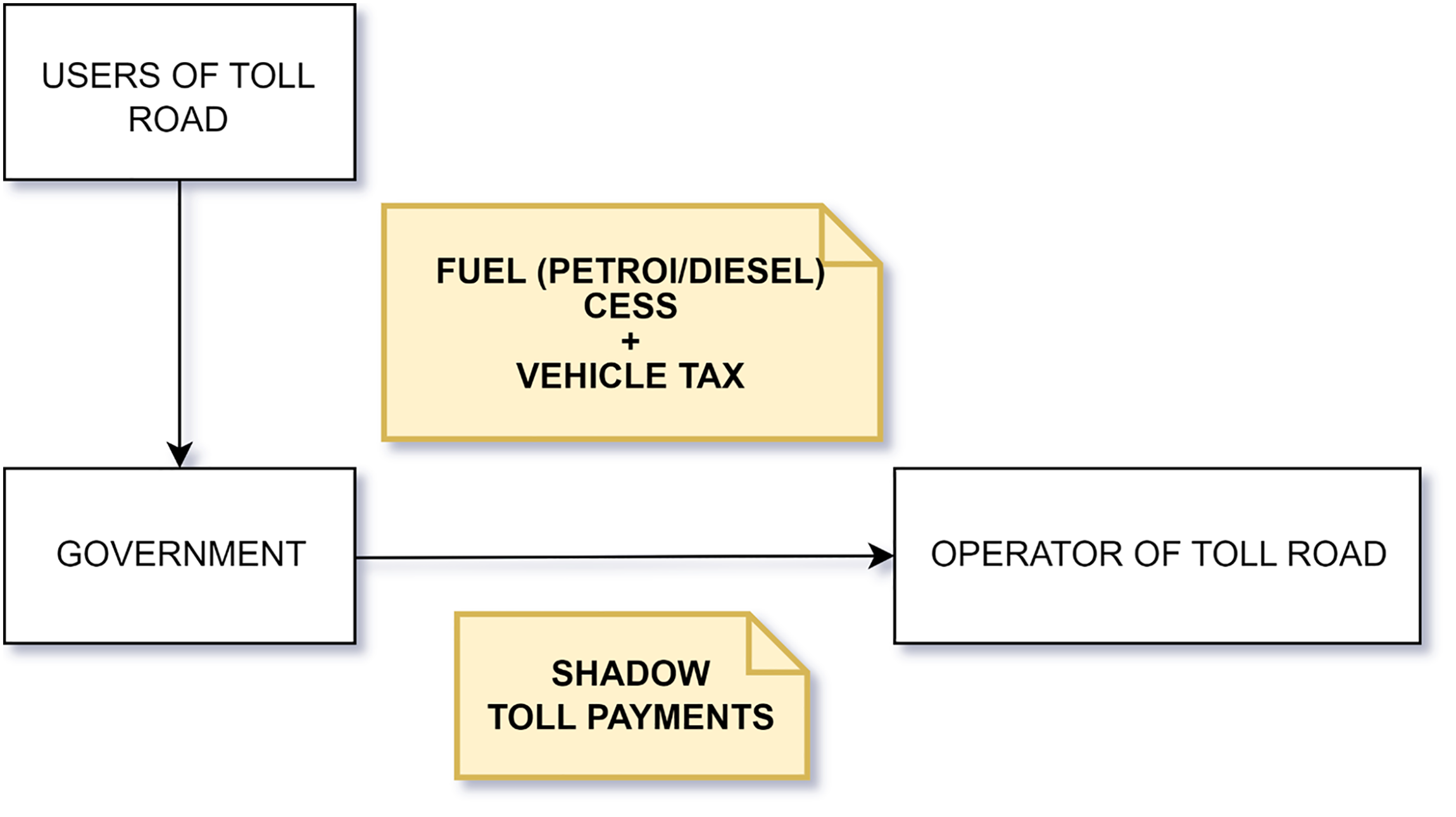

Shadow toll is a type of payment structure, where the user of the toll road does not pay any toll. In this model, the concessionaire collects the revenue from the government according to the number of vehicles which are using the toll road. Government generally collects this revenue in the form of vehicle tax and fuel (petrol/diesel) cess from the citizens. The cess imposed on the citizens would be minimal as it would spread over a huge number of citizens. Thereby, this shadow toll model would work quite effectively as the road users are not required to pay any toll. This model has several benefits over the conventional toll models. The traffic risks are minimized by shadow toll, as the government pays for the traffic and for the users the road is free to use. The private partners who have invested in the project have more confidence about the traffic flow on the road. In case if the number of traffic is less than that estimated or forecasted, then the government extends the concession period. The operational cost for the concessionaire is also reduced as the cost for operating the toll booths is not required. This cost may be as high as 20% of the revenue collected (Ranganathan et al. 2010). A framework of the shadow toll model is presented in Figure 1.

Framework for shadow toll model (Ranganathan et al. 2010).

According to Figure 1, the users of the road have free access to the road and are not required to pay any toll. The concessionaire gets the revenue of the traffic using the toll road from the government. In turn, the government collects the required amount by charging vehicle tax and fuel (petrol/diesel) cess from the citizens.

Reviewing the available literature, it has been observed that many past researchers have developed PPP models for highway projects about BOT (toll) and BOT (annuity). These models face a considerable number of risks and challenges, which drastically reduced their viability. In the Indian scenario, it has been observed that users are still very reluctant to pay the specified toll for using a particular road. They tried to find out alternative ways and means for avoiding the payment of toll. These issues are challenging to be shorted out by the private party or the government. The proposed HAM for Indian roads may provide solutions for the concessionaire or the government's current problems. The work on developing the HAM model in the Indian context is also in a very nascent stage. The present research will contribute to the existing body of knowledge by developing a suitable HAM model for Indian highways. This model will also be strengthened by incorporating associated FIDIC contract clauses wherever applicable.

Methodology for development of HAM framework

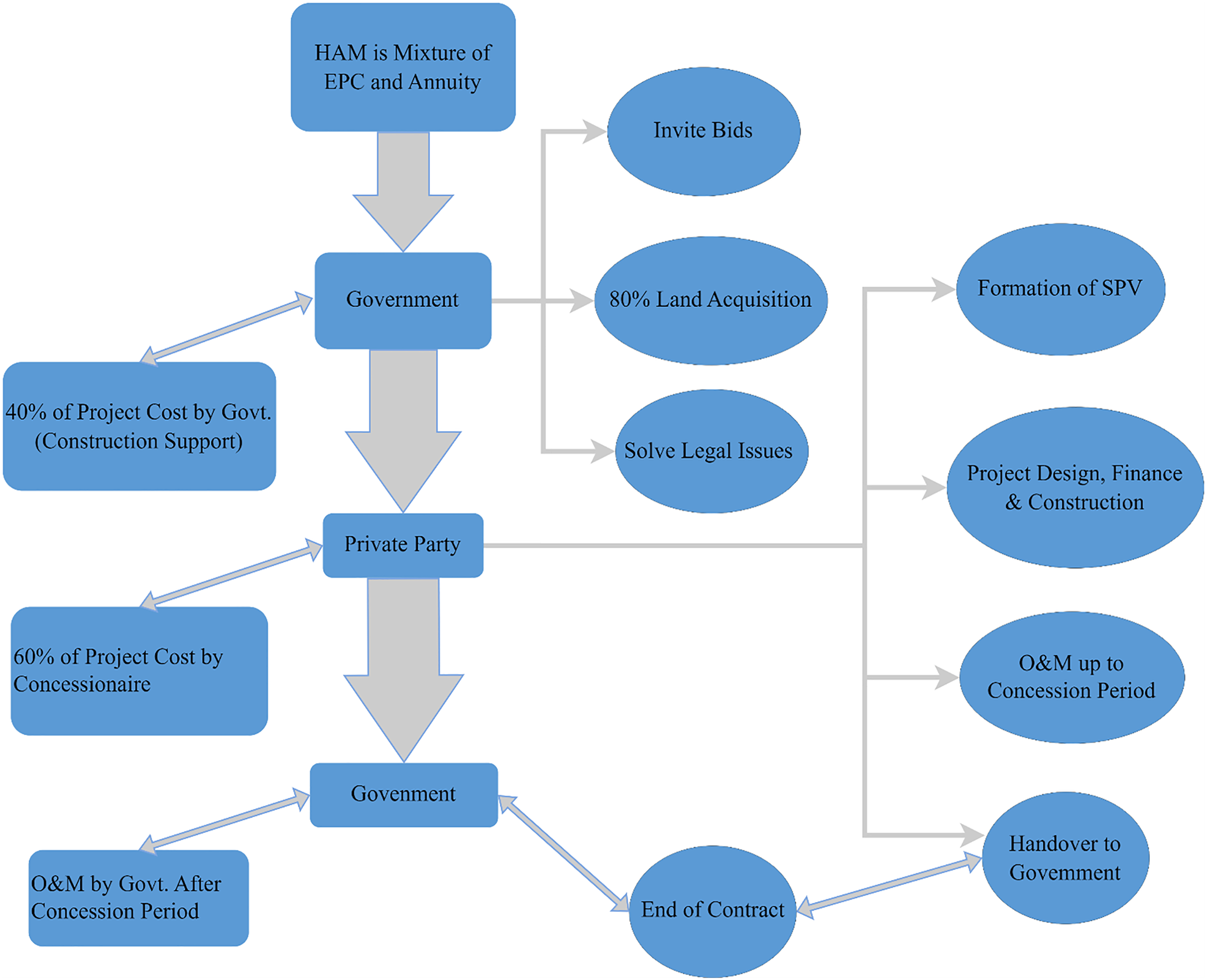

This model is best suited for attracting private investors when low traffic is observed, and there is a need to develop a specific corridor for some important reason. As cash support during the construction period, 40% of the bid project cost is payable to the concessionaire by the authority after achieving specified milestones mentioned in the agreement. The concessionaire bears the remaining 60% of the bid project cost during the constriction period. Project cost shall be inflation-indexed, a weighted average of wholesale price index and consumer price index for industrial workers in the ratio of 70:30. Toll collection is the government authority's responsibility, and O&M payments are made by the authority as quoted in agreement after adjusting it for inflation. The concessionaire period consists of two major parts: (i) construction period and (ii) fixed 1-year operation period. Table 1 represents the risk allocation for typical PPP model. Figure 1 represents the process flow chart for a typical HAM.

Risk allocation for typical PPP models (Patwardhan 2016).

According to Table 1, for BOT (Toll) model, the risks associated during the construction of the project must be borne by the “private partner.” Any mishap during the construction period including the occurrence of any accidents needs to be borne by the “private partner.” The risks during the operation and maintenance and also toll collection from the traffic using the toll road need to be borne by the “private partner.” Thereby, it has been observed that all the risks during the project life cycle need to be borne by the “private partner.” This is definitely very much challenging for the “private partner.” For BOT (annuity) model, the risks associated during construction, operation, and maintenance must be borne by the “private partner.” But the risks associated with the toll collection are borne by the “authority/public partner.” Thereby, BOT (annuity) model is better than the BOT (toll) model. Finally, in HAM model, the risks associated with construction are borne by “private partner or the authority/private partner.” The risks associated with the operation and maintenance is borne by the “private partner,” but the risks associated with the toll collection are borne by the “authority/public partner.” Thereby, HAM is definitely better and has advantages over BOT (toll) and BOT (annuity) model.

Figure 2 represents a flow chart representing a typical HAM model in Indian scenario. The Indian National Road Authority has launched the hybrid annuity and funded nearly 120 projects from 2017 on the first bid to this end of the year. As a result, a significant financial stranglehold of about 75% was set with a total length of 6670 km in HAM projects given to the NHA financing the course of the 2016–2019 financial year. The HAM helps determine the annuity funding required for the project and the potential risks and identify the most suitable financing method (Singh and Madurwar 2019).

Flow chart for typical structure of HAM (Ghayal and Salgude 2019).

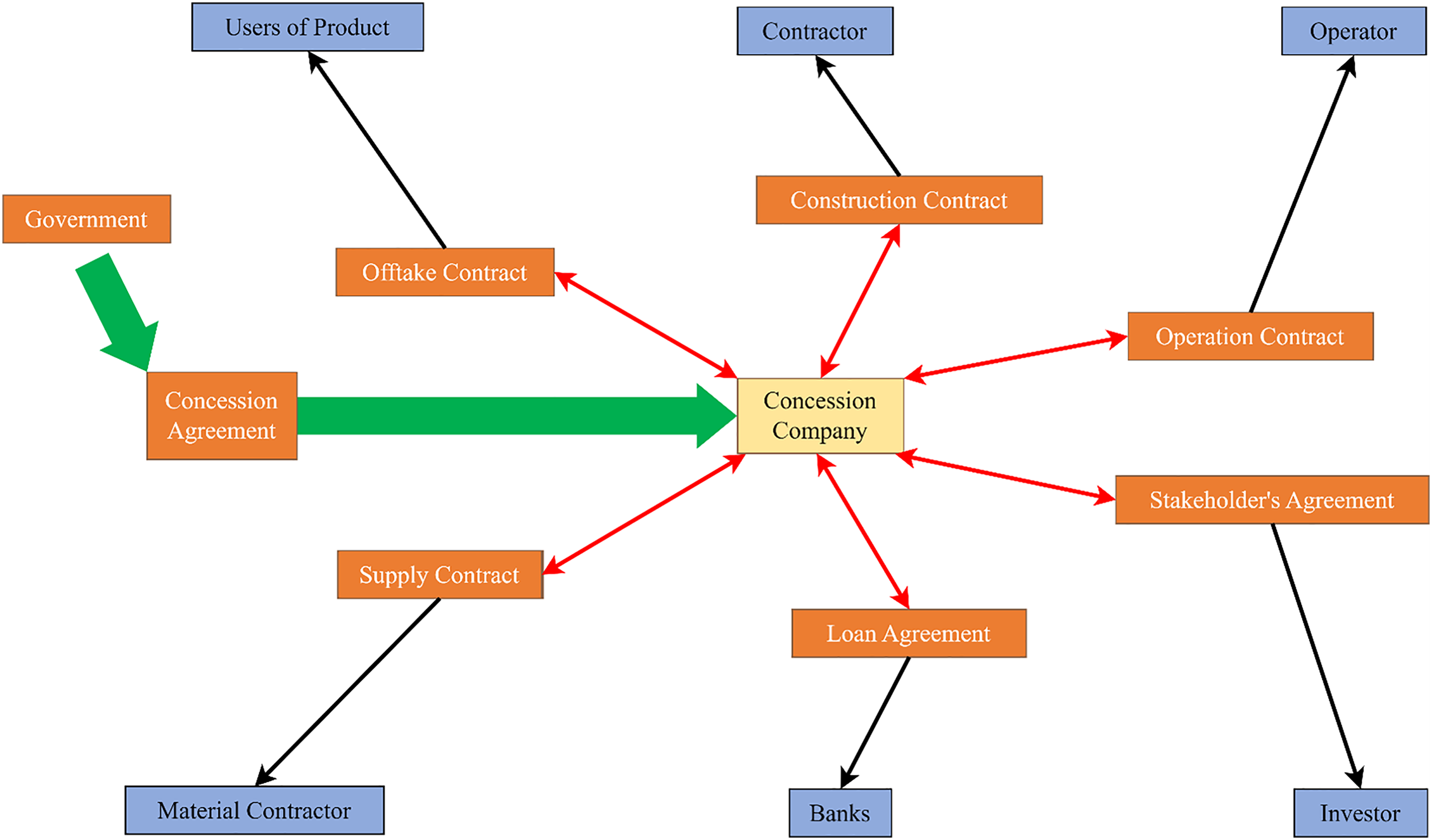

Figure 3 represents a typical structure of a BOT model. This mechanism is a complicated structure comprised of numerous, interdependent agreements between diverse participants. The government, a private company, called the concessionaire, lenders (banks), equity investors, contractors, manufacturers, operators, and financial advisers, are all significant participants in the BOT project. Typically, the government gives the private sector concessions (concessionaire). A concession arrangement is used to grant the concession. The concessionaire is responsible for the facility's design, financing, development, and service. The concessionaire maintains title to the property during the concessionary era, usually 10–50 years, after which the government reclaims ownership. The following are the few agreements generally adopted for the BOT (Kumar and Agrawal 2019):

Concession agreement Loan agreement Shareholder's agreement Construction contract Supply contract (equipment/material/fuel supply contract) Off-take agreement

Standard contractual structure for BOT.

Salient features and perspective of the various partners under the HAM

Private partner

During the operation and maintenance period, the government makes semi-annual payments to ensure a cash flow of 60% of the total project cost and interest that the concessionaire invested during the construction period (Garg and Mahapatra 2019).

Eighty percent of the land acquisition is completed by the government on time, alongside National Highway Authority of India (NHAI)'s efforts to expedite clear and approve and partially reduce the construction risk. Another significant fact that protects lenders and developers to a great degree is the inclusion of terms for the delay and deemed completion in the concession to issue the final commercial activity if 100% of the acquisition work is done within the targeted 80-day window.

There is a risk associated with the operation and maintenance payment since the government pays the concessionaire a fixed amount of money in an inflation-adjusted annuity over the O&M period. However, if there are substantial wear and tear, the concessionaire may be at risk of a significant rise in O&M costs (Garg and Mahapatra 2019; Taneja and Kalra 2019).

The concessionaire is somewhat spared from price increase by inflation-adjusted bid programs. However, at financial closure, the price increase is difficult to identify and is thus financed through NHAI subsidies and sponsor contribution in the amount of 40–60, which debt/equity lenders can repay after they have reached the final project value once the debt/equity lenders enter into the project have reached the final project value after COD.

Authority/public partner

According to the set milestone, the government has to make payments to the concessionaire in rent. As a result, cash flow is facilitated, and the authorities have less financial pressure on construction and operation.

After the construction phase is finished, the government has the right to receive toll money during the service period, making it a convenient source of revenue to cover the concessionaire's annuity payments (Ministry of Road Transport and Highways, 2016; Taneja and Kalra 2019).

To fulfill the concession agreement, the authority needs to speed up the land acquisition process and obtain additional permits and clearances.

Competition is interested in private operators with more significant experience, better facilities, better operation, and better efficiency (Garg and Mahapatra 2019; Taneja and Kalra 2019).

Primary salient features

Case study and analysis

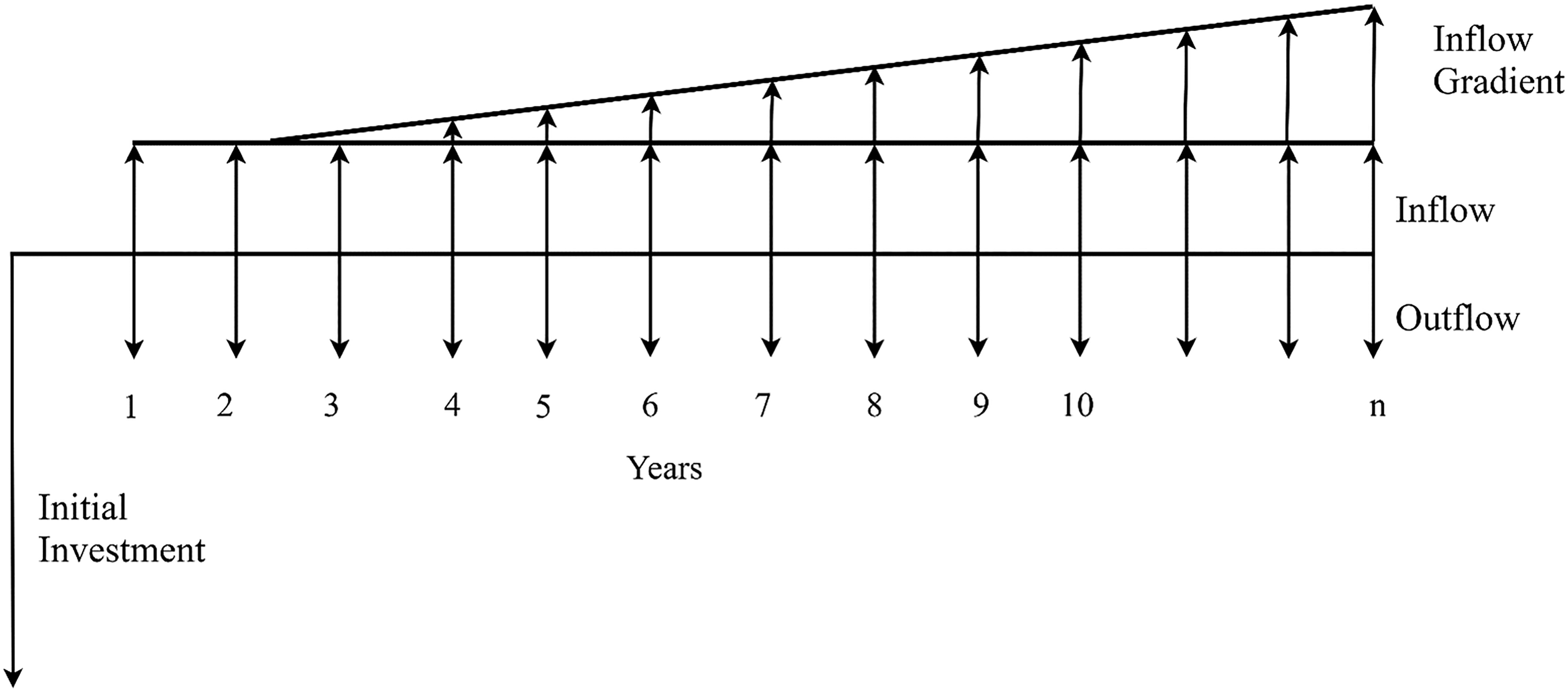

Cash flow needs to be determined for project evaluation, and it must follow increment after and before tax consideration. Direct investment, working cash flow, and incurable cash flow are the three primary components of a conventional project. The project cash timing (be it inflows of cash or outflows of cash) clarifies graphically with a cash flow diagram. There are two major parts in the cash flow chart, and one is a horizontal line, which indicates time divided into equal parts shown in Figure 4. Cash inflow represents payment or receipt, and cash outflow indicates disbursements or expenses. Cash flow can be positive or negative, separately symbolized by arrows either in ascendant or descendant direction by timeline taking as reference or baseline.

Typical cash flow diagram for PPP ownership structure.

Several PPP models are available for the project's different categories. In the present case study, three PPP models are analyzed for a particular road project's financial feasibility. The case study road project under PPP is between Porbandar and Dwarka, two districts of Gujarat, and both districts have limited industrial importance. The project is developed under the HAM, adopted in January 2016 to develop new roads for under-developed places in India. BOT (toll), BOT (annuity), and HAM are three financially compared models for adopting the best-suited road development model for Porbandar and Dwarka not having a good industrial background. Net present value (NPV) and internal rate of return (IRR) are calculated for the entire project to compare a particular model's feasibility under given conditions.

Project details

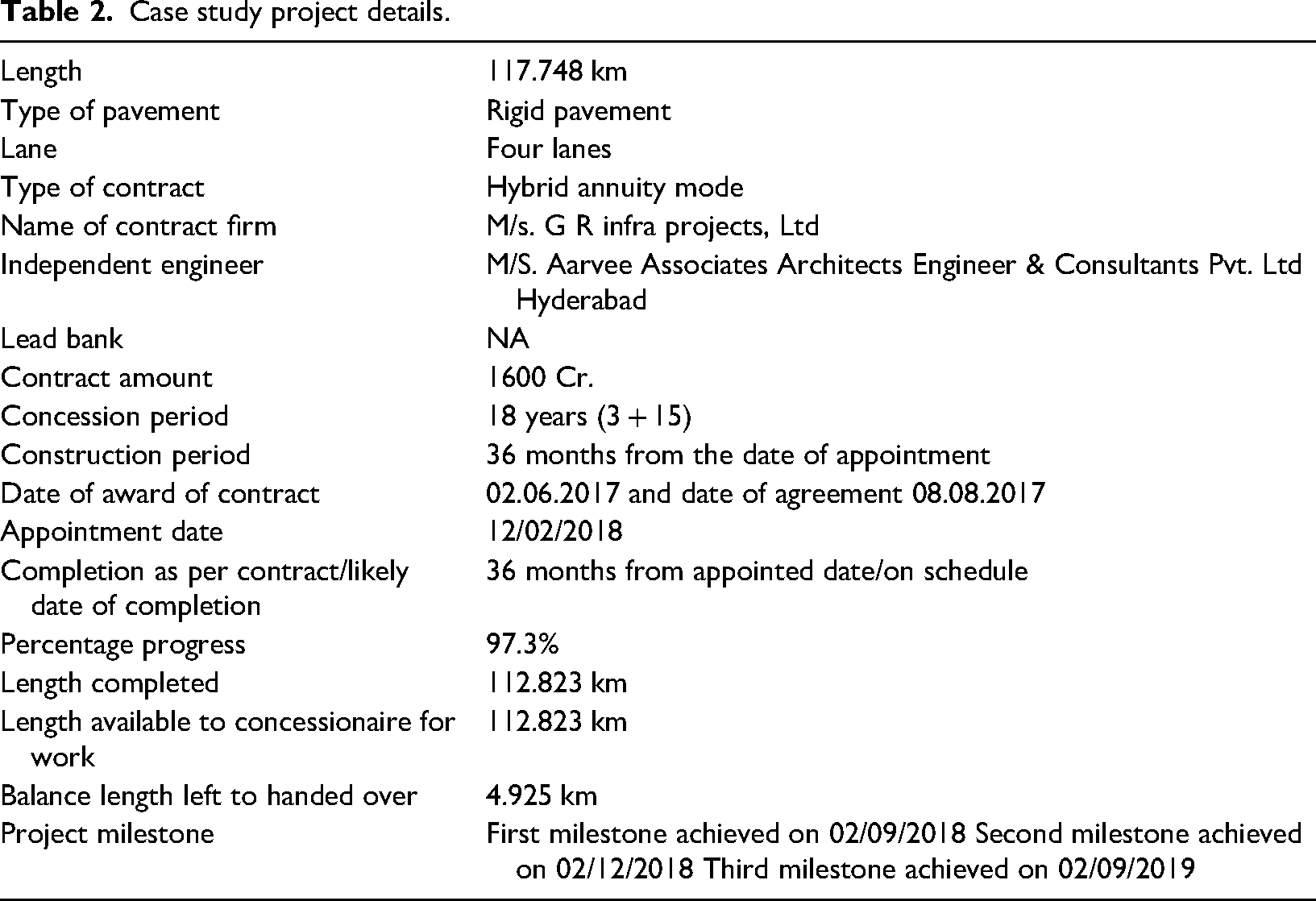

The project details are as follows: Four laning of Porbandar–Dwarka section of NH-8E from km 356.766 to km 473.000 and from km 379.100 to km 496.848, Gujarat state highway through hybrid annuity mode under NHDP Phase IV (Table 2).

Case study project details.

Route map and feasibility

As a consequence of liberalization and rapid socio-economic development in India, opening various central/state undertakings and bank offices, there has been a tremendous economic growth in the urban centers. These have resulted in a spurt of freight and passenger transport activities. NHAI has decided to develop various national highways. NHAI has taken up the rehabilitation and strengthening of the existing two-lane road to six/four/two lanes with Bhavnagar–Pipava–Porbandar's paved shoulder configuration Dwarka section from km 3.200 to km 473.000 of NH8E in the state of Gujarat. The length of the project stretch is 470 km. Keeping the above requirement in mind, NHAI had invited proposals to prepare feasibility reports from various consultants.

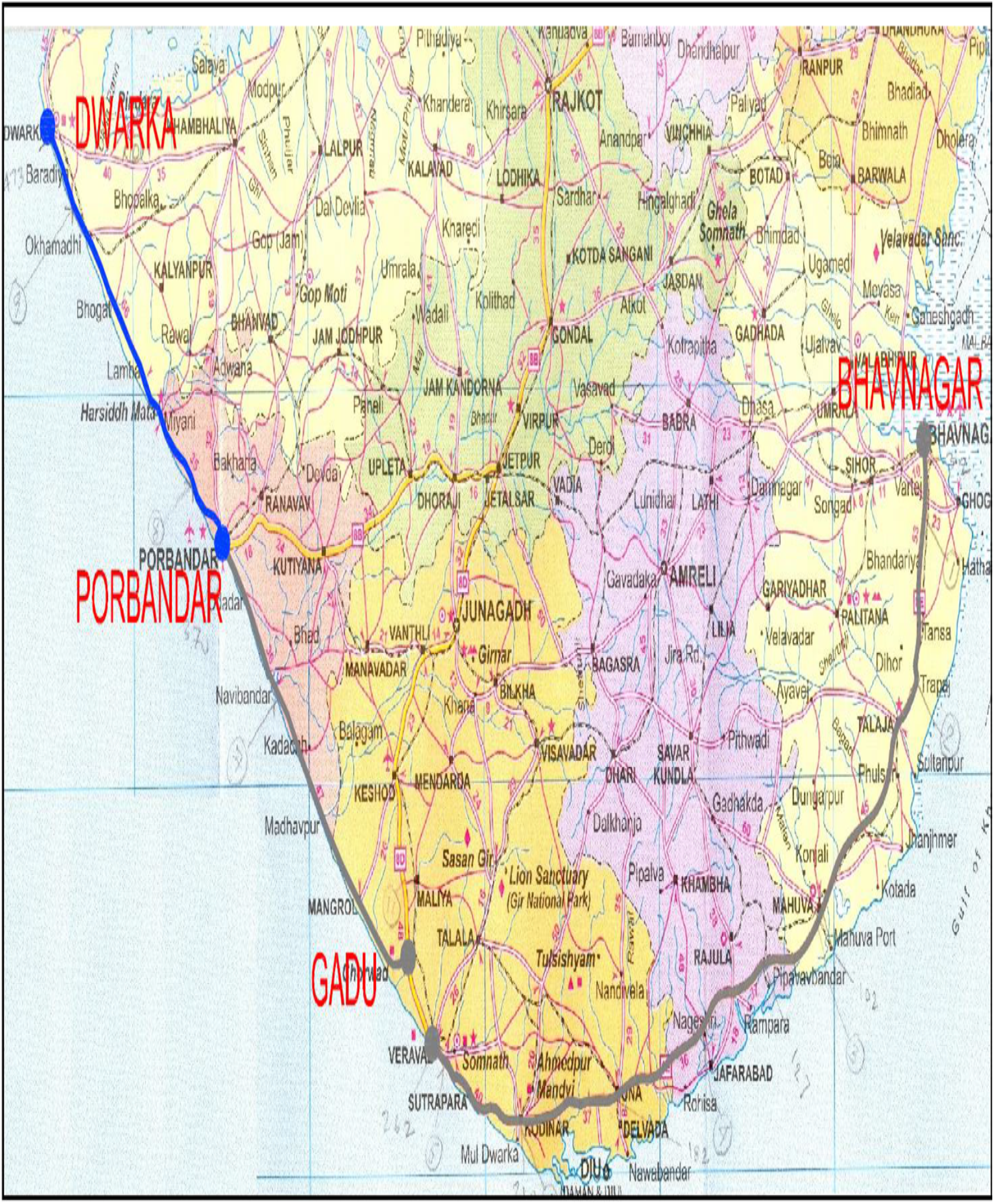

The socio-economic analysis's primary purpose is to provide an overview of the state's socio-economic setup and the related status of the project's influence area. The details include the present status, the past performance, and the perspective of the economy, population, and urbanization. The profile depicts the spatial distribution of economic activities. It is observed that over 80% of the vehicular traffic on the project corridor originates or terminates in the state of Gujarat. Therefore, the socio-economic analysis of the broad influence area is confined to this state. The project road section mainly passes through two districts of Gujarat, namely, Porbandar and Dwarka. All these districts contribute traffic to the project road section in varied proportions. These districts thus form an immediate influence area of city road. This influence area is termed as project influence area. Figure 5 represents the route map of the case study considered for this research work.

Route map of case study.

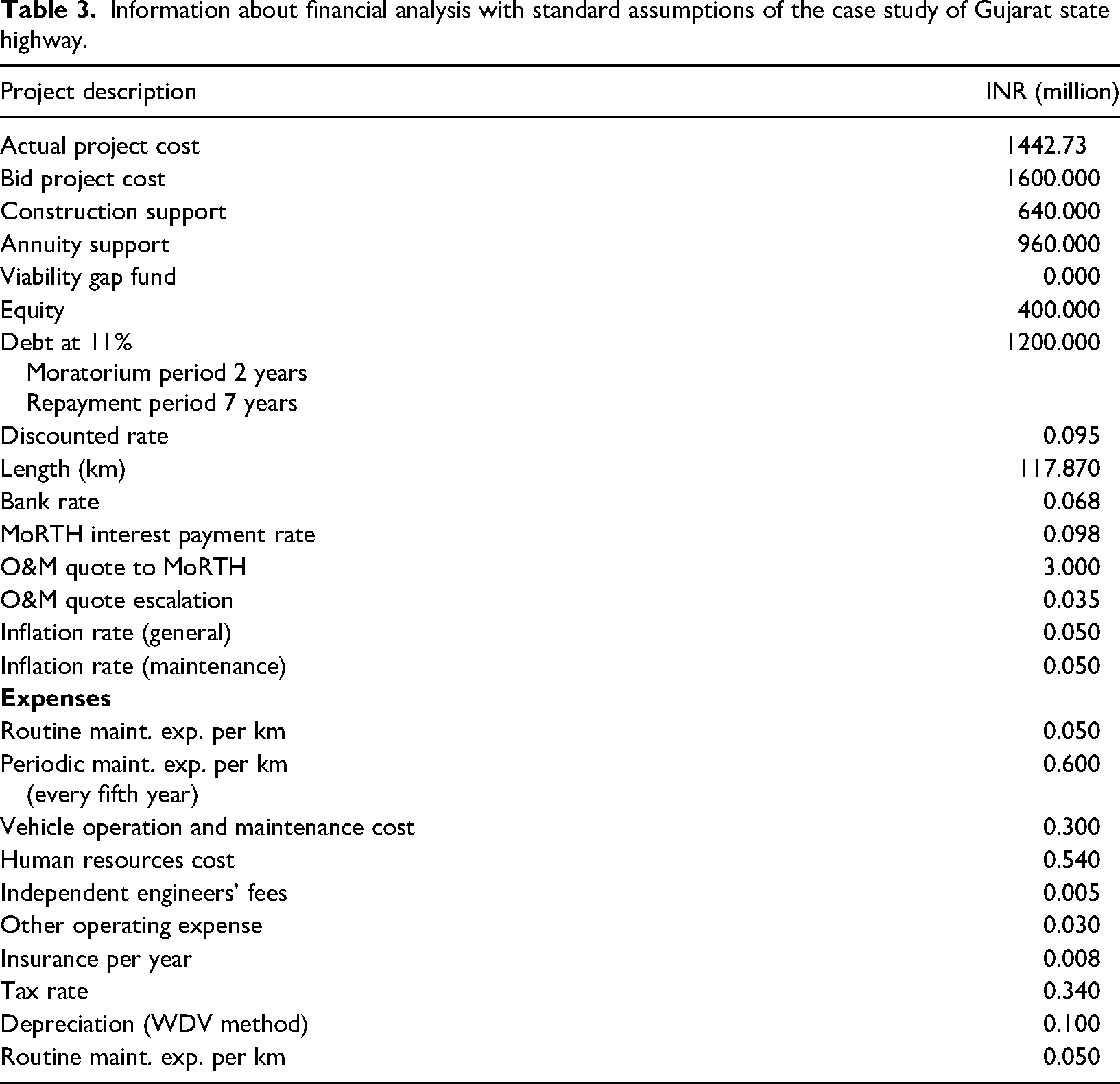

Table 3 represents the information pertaining to the financial analysis of the case study considered for this research work.

Information about financial analysis with standard assumptions of the case study of Gujarat state highway.

Financial analysis of hybrid annuity model

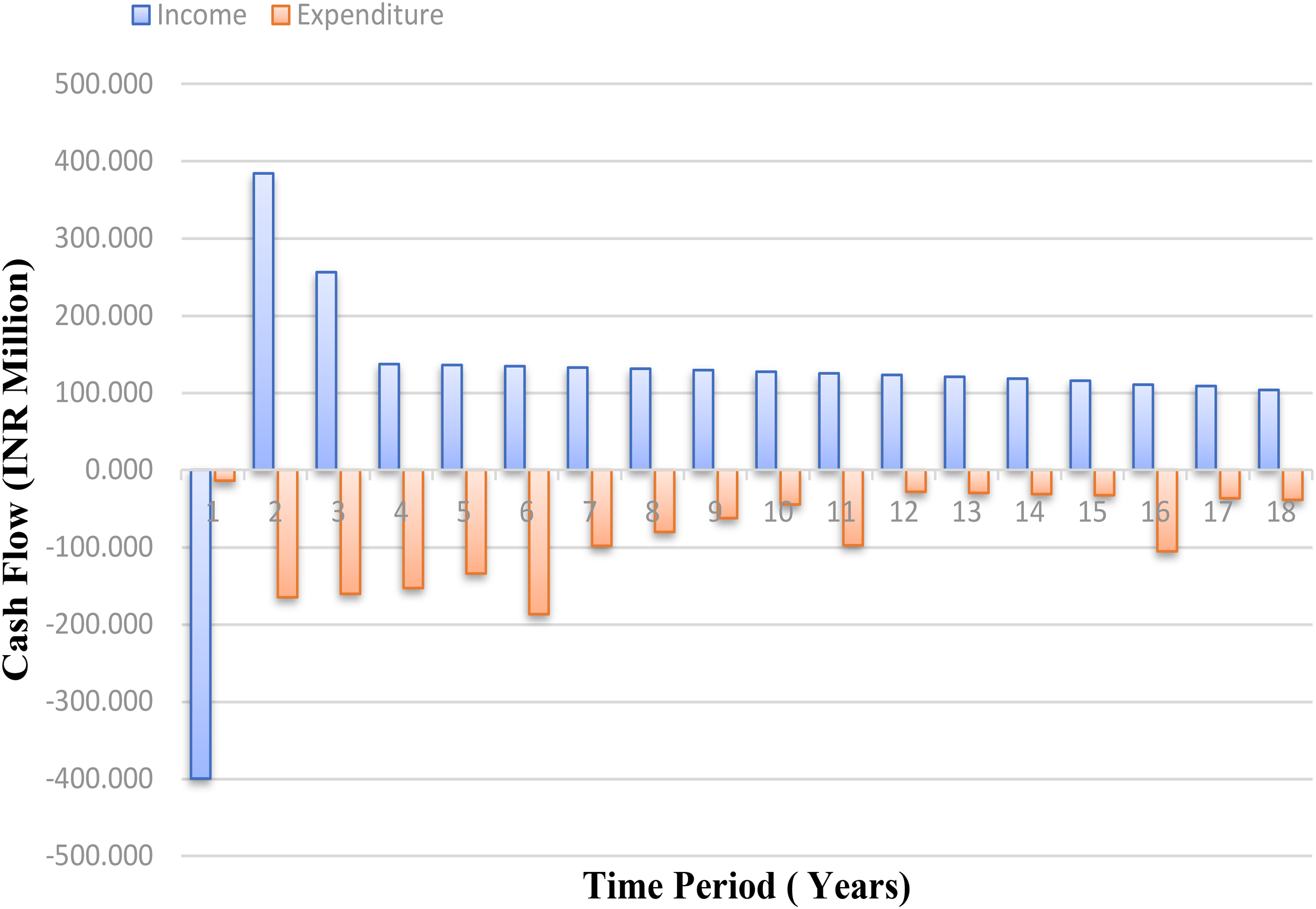

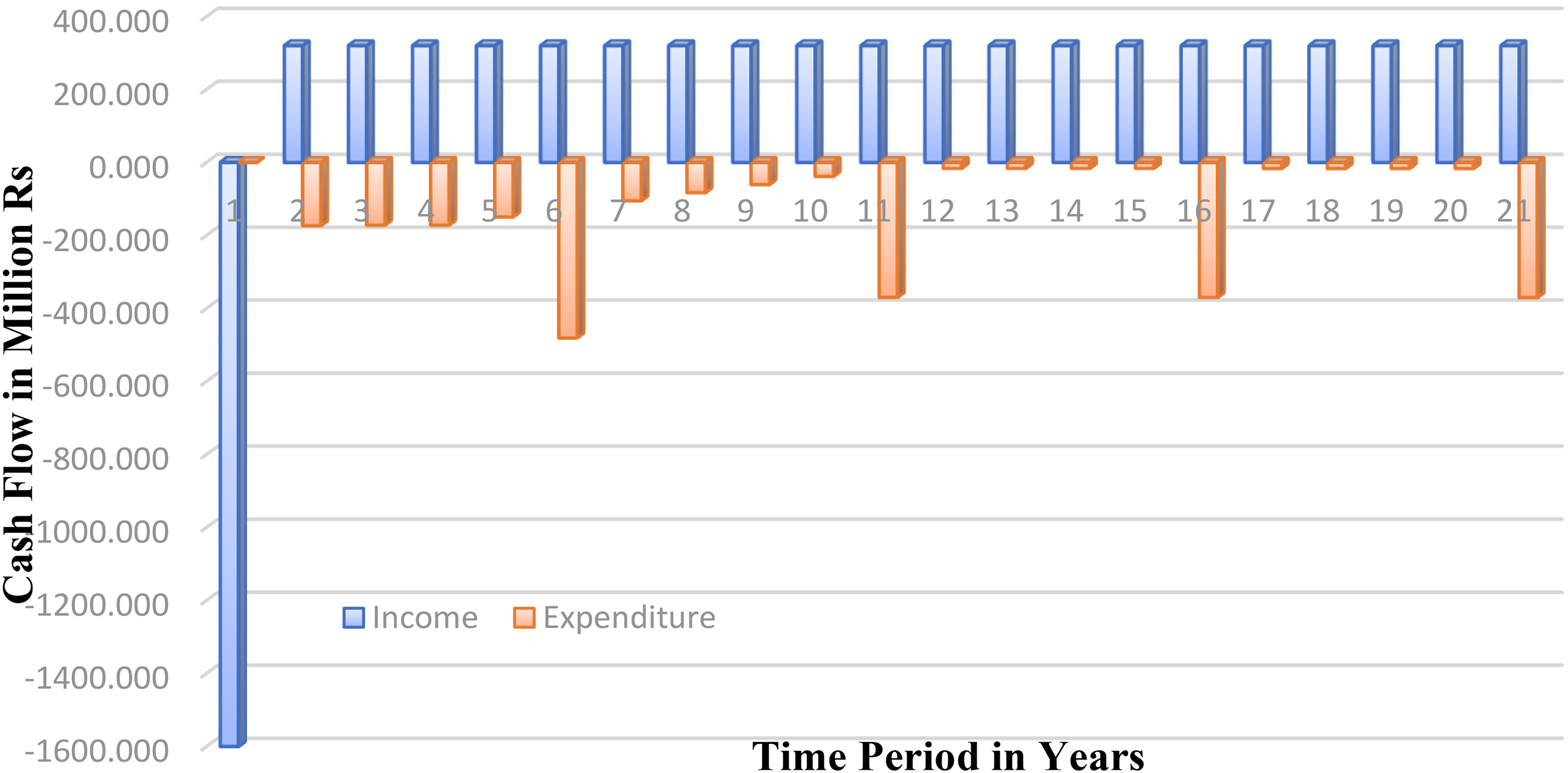

Figure 6 represents the cash flow diagram for the newly adopted HAM model. Blue lines in Figure 6 represent the cash inflow for the HAM, which includes the annuity amount paid by the authority after the construction period and construction support given by the authority during the construction period. Red lines represent different expenditures made by the concessionaire during the concession period. As shown in Figure 6, the blue lines decrease because the concessionaire's amount as an annuity, and other payment is reduced every year due to interest paid on the remaining amount. The subsequent cash flow diagrams of BOT (toll) model and BOT (annuity) model are presented in Figures 7 and 8, respectively. It has been observed that the cash inflow of the BOT (toll) model increases in a geometric gradient which has a nominal increase at the end of every year. The cash outflow at end of year 1 is maximum in BOT (toll) model followed by BOT (annuity) model. The cash outflow at the end of year 1 is minimum for the HAM. The cash inflow for the BOT (annuity) model is fixed at the end of every year and is constant up to the concession period. The cash outflow for BOT (toll) and BOT (annuity) is fluctuating in comparison to HAM.

Cash flow diagram for HAM.

Cash flow diagram for BOT toll.

Cash flow diagram for BOT annuity.

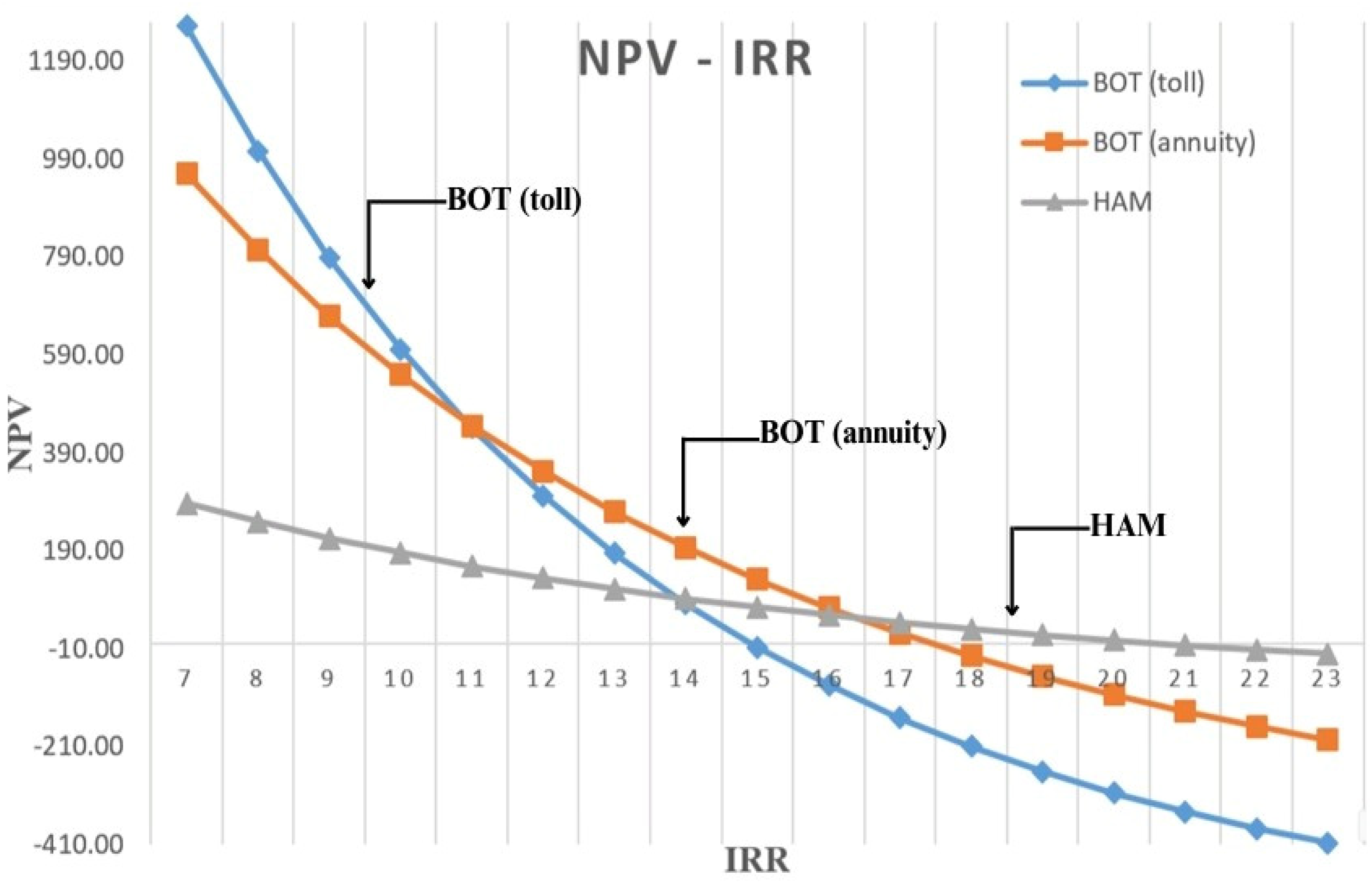

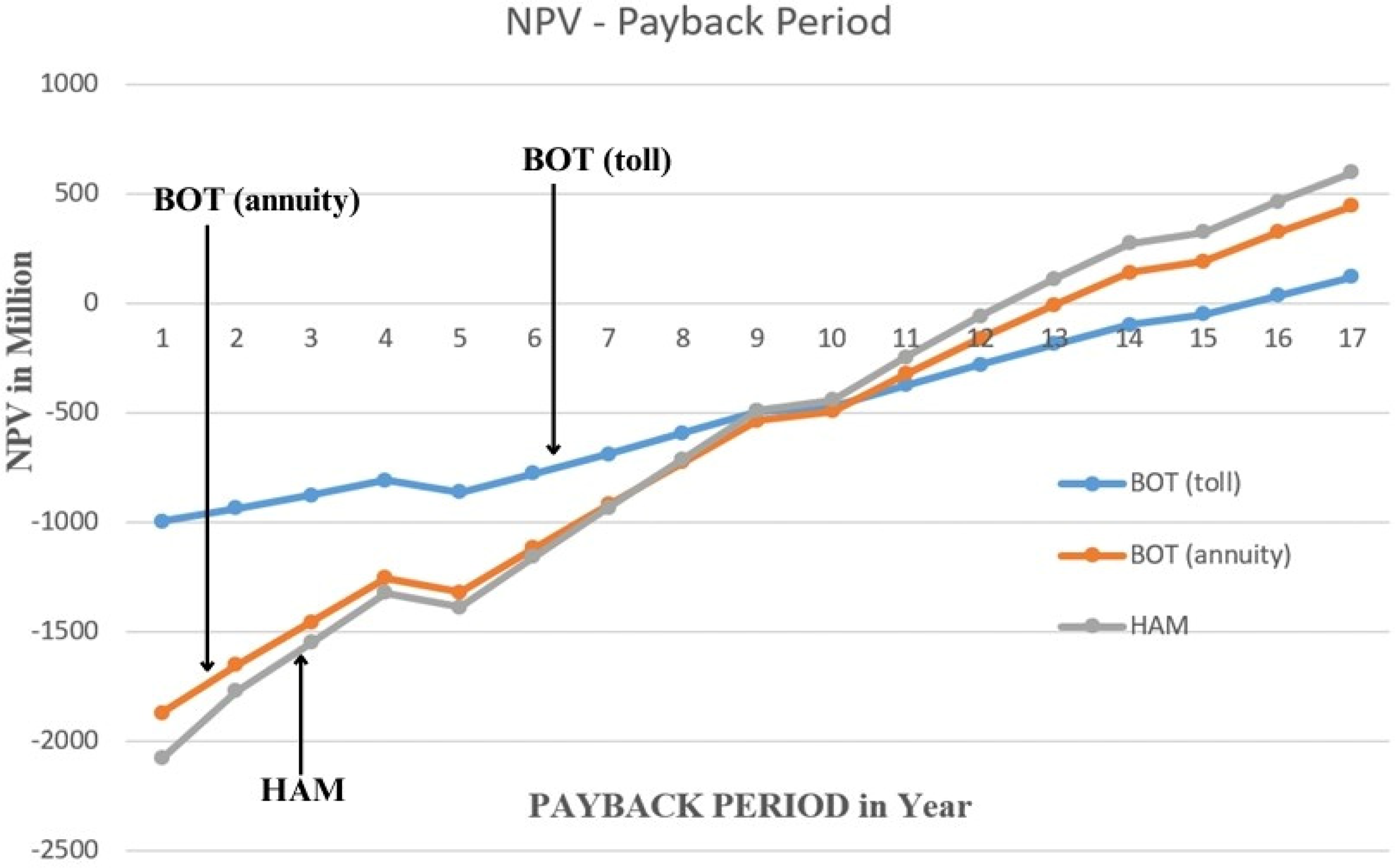

HAM is a newly adopted model, and NPV and IRR are also calculated for that model. The graph in Figure 9 shows the details of the NPV and IRR computed from the cash inflow and cash outflow data for the HAM. NPV value varies from 53.53 INR in a million to −72.05 INR in a million, respectively, for 12% to 23% return rate. The IRR value for HAM is higher than the other two models and is around 15% before tax consideration and 21% after tax. The comparative analysis of the NPV and IRR for BOT (toll) and BOT (annuity) is also presented in the same figure. It has been observed that the performance of HAM with respect to NPV and IRR is better than the BOT (toll) and BOT (annuity) models. Figure 10 represents the payback period of the proposed HAM under study. The payback period of the HAM is about 12 years. The payback period of the BOT (annuity) and BOT (toll) model are about 13 and 15 years, respectively. Thereby, financially, HAM model performs the comparative BOT (toll) and BOT (annuity) models better.

Net present value (NPV) versus internal rate of return (IRR), for HAM, BOT (toll), and BOT (annuity).

Net present value (NPV) versus payback period (years) for HAM, BOT (toll), and BOT (annuity).

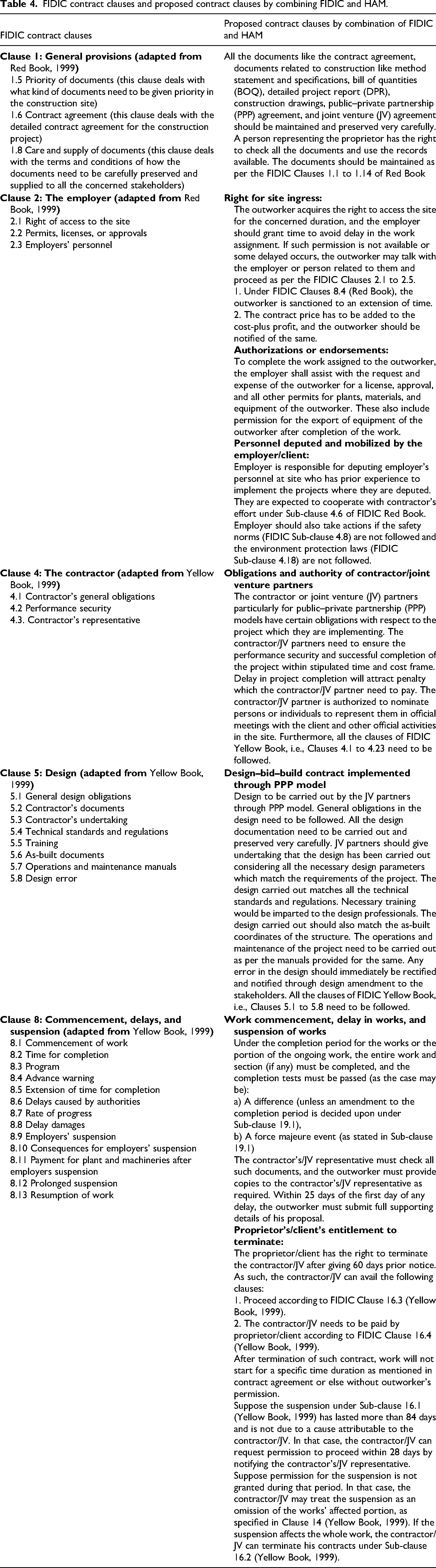

Comparative study of the FIDIC contract clauses and proposed clauses for model concession agreement of HAM

FIDIC 1999 Yellow Book (the conditions of contract for plant and design–build) and FIDIC 1999 Red Book (conditions of contract for construction) have been used for developing the contractual framework for the proposed HAM. Non-FIDIC contract clauses have been observed to be more biased and supportive toward employer/client. The contractor most of the times is in the receiver's end. FIDIC 1999 Red Book has brought in some modifications in the general conditions of contract. Its principles of balanced risk sharing between the employer/client and contractor give more confidence to the contractor during the implementation of risky projects.

On request of FIDIC, the contracts committee had set up a special Task Group (TG15). The contractual principles of each form of FIDIC contract may be considered as in-avoidable and sacrosanct. These principles are called as “FIDIC Golden Principles (GPs).” The principle of freedom of contract ensures that parties are free to agree on the terms of their contract, provided it complies with the law and public policy. Following the publication of GPs which identified the essential elements of a FIDIC contract, it would be misleading and inappropriate to refer to a contract using the FIDIC General Conditions (GCs) of contract that does not comply with GP. To promote the acceptance and understanding (a), the GPs are formulated at a conceptual level to encapsulate the essence of a FIDIC contract, (b) each GP expresses a single, readily understood, and generally accepted concept, and (c) the GPs are limited to the minimum number necessary for completeness. The following key considerations underpin the GPs:

The terms of the contract are comprehensive and fair to both contracting parties. The legitimate interests of both contracting parties are appropriately considered and balanced. Best practice principles of fair and balanced risk/reward allocating between the employer and contractor are put into effect in accordance with the provisions of GCs. No party shall take undue advantage of bargaining power. The contractor/sub-contractor is paid adequately and timely in accordance with the contract to maintain its cash flow. The employer obtains the best value for money. To the extent possible, cooperation and trust between the contracting parties are promoted, and adversarial attitudes are discouraged and should be avoided. The contract provisions are not unnecessarily onerous on either party. The contract provisions can be practically put into effect.

The comparison of the FIDIC contract clauses and the proposed clauses for developing the model concession agreement (MCA) of HAM is presented in Table 4. It is expected that if the below-mentioned contract clauses are included in the MCA of HAM, more public and private investors would show their interest for HAM.

FIDIC contract clauses and proposed contract clauses by combining FIDIC and HAM.

Discussion

In the present paper, the benefits of HAM implemented in the Indian PPP highway sector and specifically in the Gujarat region have been discussed. HAM is one of the potential solutions for road construction because it divides the financial risk between the government and private parties. HAM is anticipated to benefit the road sector by increasing the rate at which contracts are awarded and resolving the shortcomings of earlier toll-based and annuity-based projects. While the HAM resolves the majority of issues affecting project development under earlier models such as BOT (toll), future concerns may include the amount of government funding that could be made available on an annual basis to finance such massive, resource-intensive projects. Such government funding is limited, as seen with projects founded on annuities. A second risk could be the government's ability to collect tolls on specific initiatives despite local/political pressure, which could lead to enormous corruption possibilities (Singh 2020). A case study of the highway project in the Gujarat state was taken for analyzing the financial feasibility of the newly adopted HAM. In the financial analysis, it has been observed that the return on the investment in IRR is more favorable and in good amount in the HAM than the other two BOT (toll) and BOT (annuity) models. Furthermore, it is also noticed that the range of the NPV values changing from positive to negative is comparably low in the case of HAM, while in other cases of BOT (toll) and BOT (annuity) is higher. Along with the financial analysis, it has been suggested that the proposed model framework is quite feasible for implementing HAM in the state of Gujarat. In the proposed framework, FIDIC clauses are incorporated to improve the quality of the PPP highway projects, which meets the need for an international standard. The findings of this study will assist highway agencies and private firms in significantly enhancing the construction process and project management, which will ultimately result in improved highway project planning, reduced exposure to litigation, and risk minimization for the concern players.

Conclusions

The consideration and acceptance of the HAM model are superior than any other model for the provided case study, as evidenced by the following points. On such a road, Porbandar and Dwarka both have solely social and religious traffic and a very low traffic census. Using BOT (toll) and BOT (annuity) models to build such a road does not operate well. Due to the lack of traffic, private investment will not generate a sufficient return, and the route will stay undeveloped. In this circumstance, HAM provides a good return on investment, and the private concessionaire in the PPP method is also responsible for road construction. As described in the results section, the HAM's financial analysis shows a lesser difference in NPV for the higher return rate, ranging from 53.53 INR in a million to −72.05 INR in a million, indicating that there are much fewer odds of annuity payment inflation. In comparison, the value of NPV for the other two models with lower returns on investment is greater. HAM is a hybrid model of the two most appealing models like EPC and annuity, in which the concessionaire receives 40% of the invested amount during the construction time and the remaining 60% as an annuity determined by the authority during the concessionaire period of about 15 years.

The IRR is used to calculate the return on investment, and as previously stated, the value of IRR in the HAM is roughly 15% before tax and 21% after tax. The maximum value of IRR in BOT (toll) is around 9% before tax and 12% after tax, whereas the highest value of IRR in BOT (annuity) is around 14% before tax and 18% after tax. As a result, when compared to the other two models, HAM provides a good IRR. HAM is a solution for developing new road infrastructure for locations with low traffic flow, and a case study indicates that the HAM is only paradigm that can be used to create road infrastructure in such places. The payback period of the HAM model is about 12 years. The payback period of the BOT (annuity) and BOT (toll) model are about 13 and 15 years, respectively. Thereby, financially, HAM performs the comparative BOT (toll) and BOT (annuity) models better.

From the above analysis of the financial model, it has been observed that BOT (toll) projects are facing severe challenges in the state of Gujarat. Thereby, a substitute model in the form of HAM could be more effective for state highways (SH) and NH of Gujarat state. The financial analysis including NPV and IRR is suggesting that the HAM is more feasible in Gujarat. The payback period lies between 8 and 9 years. Thereby, the future upcoming project authorities are requested to consider these issues before taking a final decision for their projects.

The scope for future research lies in carrying out a detailed sensitivity analysis for the proposed HAM. It needs also to be explored if this model can be made techno-economically for the stretches which have higher traffic congestion. The risks and challenges associated with the HAM need to be studied, and a proper detailed risk management model needs to be prepared. This would enable the project authorities to develop and formulate proper risk mitigation measures which would increase the feasibility of such projects.

Footnotes

Acknowledgements

The authors highly acknowledge the cooperation of Gujarat state highway authorities for providing us the necessary data for carrying out this research work.

Availability of data and material

All data pertaining to this research will be made available on demand.

Code availability

All the software codes used in this research will be made available on demand.

Declaration of conflicting interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.