Abstract

Funding agreements are the legal foundation for government-nonprofit funding relations and specify the terms and expectations for both parties. Yet little attention focuses on the funding agreements themselves, which vary in structure, form, compensation arrangements, and amount of risk each party bears in the funding relationship. Using data on human service nonprofits in the U.S., we examine whether the type of funding agreement—cost-reimbursement versus fixed-cost—influence the reliability of government funding during the Great Recession and the level of engagement by nonprofit providers. We find those who bear the burden of the risk at the outset have less reliable funding during recessionary times and nonprofit providers with a flat amount agreement are less engaged with government funders. Findings have implications for public and nonprofit managers to carefully consider risks and relationships to implement effective funding agreements.

Governments have increasingly turned to nonprofit providers to deliver public services (e.g., Bel et al., 2010; Brown et al., 2018; Durant et al., 2009; Hefetz and Warner, 2012; Page, 2006; Radin, 2012; Savas, 2000; Sclar, 2000). Across all levels of the U.S. government—federal, state, and local—government agencies contract out services in pursuit of greater efficiency through market competition (e.g., Savas, 1987). However, this increased use of nonprofit organizations to provide traditional government services resulted in nonprofits becoming dependent on government funding, especially human service nonprofits (Smith, 2012; Smith and Lipsky, 1993). Nearly two-thirds of U.S. human services nonprofits rely on government contracts and grants as their largest source of revenue (Boris et al., 2010). As such, researchers have examined many facets of the government-nonprofit funding relationship from the government perspective: accountability (e.g., Brown et al., 2018; Girth, 2014; Hefetz and Warner, 2012; Romzek and Johnston, 2005) and cost savings (e.g., Bel et al., 2010; Johnston and Girth, 2012) and the nonprofit perspective: funding challenges (e.g., Boris et al., 2010), governance (e.g., O’Regan and Oster, 2002; Smith, 1996), collaboration and community relations (e.g., Miltenberger and Sloan, 2017; Smith, 1996), and advocacy (e.g., Fyall, 2017; Leroux and Goerdel, 2009; Mosely, 2012; Suarez, 2009). Yet most research fails to consider government’s choice of funding agreement, cost-reimbursement or fixed cost, to contract with nonprofits.

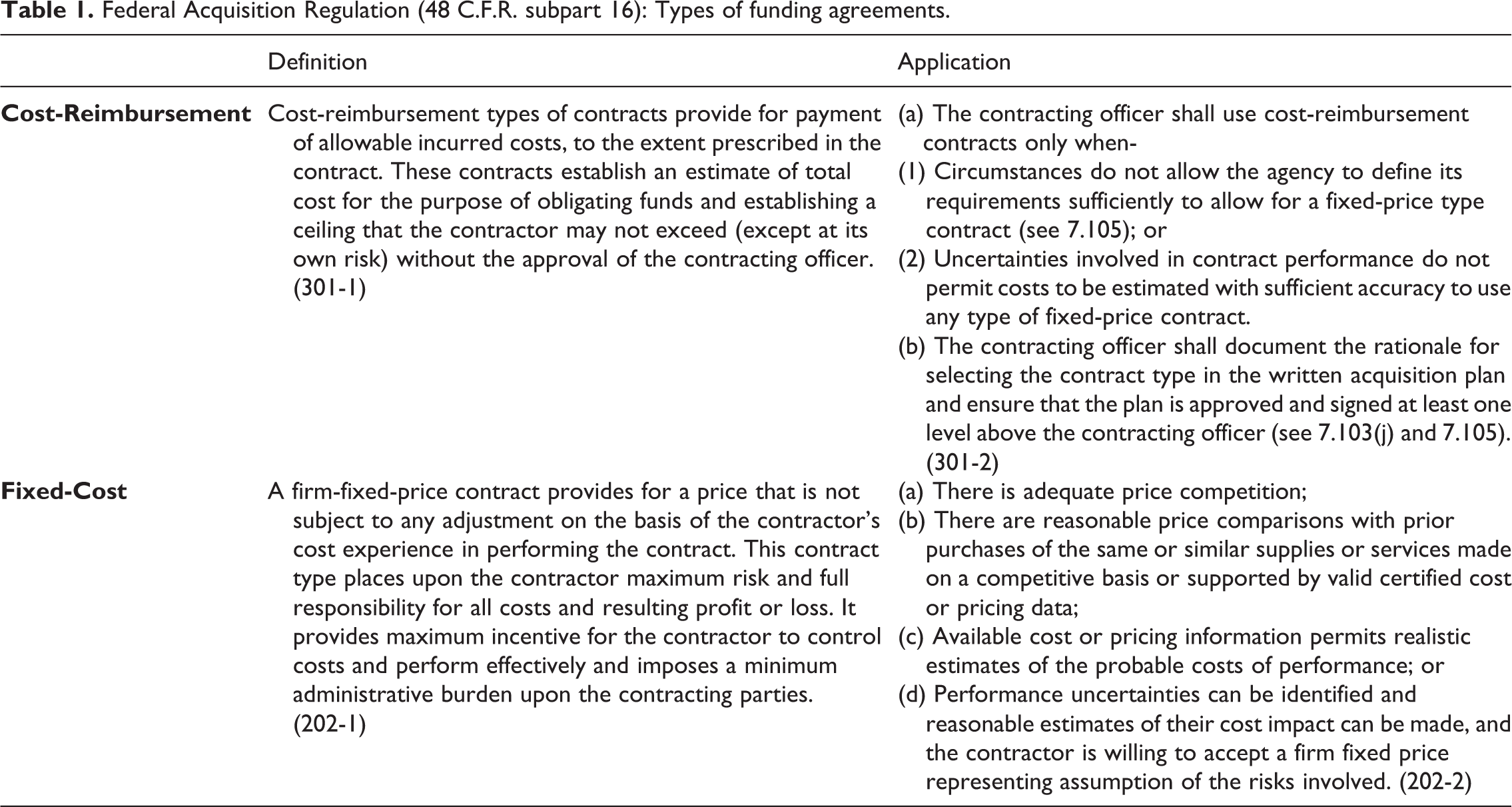

The legal foundation for the government-nonprofit funding relationship is the formal funding agreement, which specifies the services the nonprofit will provide and the amount the government will pay for those services. It also outlines the rules of the relationship and specifies the rights and obligations of both the government funder and the nonprofit service provider. Yet, not all funding agreements are created equally. According to the Federal Acquisition Regulation (FAR, 2020), the type of funding mechanism used dictates the amount of oversight federal agencies must dedicate to the project as well as which party bears the financial burden if the project costs more than expected. Table 1 below provides the definition of cost-reimbursement and fixed-cost contracts. The burden of risks for cost-reimbursement contracts is on the principal, government funder, whereas for fixed-cost contracts the burden falls on the agent, the nonprofit delivering public services.

Federal Acquisition Regulation (48 C.F.R. subpart 16): Types of funding agreements.

Despite the importance of formal funding agreements in shaping the roles and responsibilities of government agencies and nonprofit organizations in funding relationships, little attention focuses on how the type of funding arrangement influences the relationship. Cooper (2003) describes how “little attention is paid to the contract itself despite the fact that it is the core of the relationship and is legally enforceable against both parties” (p. 95). Kim et al. (2016) examine why federal government agencies choose certain types of contracts and call upon scholars to examine “the impact of different contract types on the managerial imperatives governing the transaction” (p. 805). This study responds to these calls (Cooper, 2003; Kim et al., 2016) to examine the influence of funding agreement type on government-nonprofit relations.

Drawing upon principal-agent theory, we examine how government agencies can shape the roles and responsibilities of the government principal and nonprofit agent through the formal contract specifications for future uncertainty. More specifically, does the type of funding agreement—fixed-cost versus cost-reimbursement—influence the reliability of government funds during the Great Recession? Whether nonprofits have a way to provide feedback in implementation is especially vital when contracting for complex services, such as human services as contracts are less complete (Brown et al., 2016, 2018) and require more of a partnership (DeHoog, 1990; Girth, 2017; Van Slyke, 2007). Does the type of funding shape nonprofit engagement in the funding relationship?

The next section describes the context of the study and the complexity of contracts in delivering human services. We then present the theoretical framework drawing upon principal-agent theory, where human service nonprofit agents deliver public services on behalf of government principals, and relational contracting, which is based on mutual trust between the government and the nonprofit provider. This is followed by the hypotheses, data and methods, and findings. We close with a discussion of the results and implications for public and nonprofit management research and practice.

Complexity of human services

Problems facing individuals and communities are often “called ‘wicked problems’—those that are complex, unpredictable, open-ended, or intractable” (Head and Alford, 2013: 712). Since government and nonprofits have similar missions and goals, nonprofits are often the preferred provider for tacking these wicked problems over their for-profit counterparts. First, nonprofits are often perceived as more trustworthy than for-profit organizations and are preferred for the provision of human services because they are unable to distribute profits (Hansmann, 1987). Second, according to Salamon’s (1987) theory of voluntary failure, nonprofits are the preferred venue for collective goods, such as education and other human services. Indeed, scholars have found nonprofit organizations provide higher quality services in the nonprofit and public sectors compared to the for-profit sector in examinations of nursing homes in the U.S. (e.g., Amirkhanyan et al., 2008, 2018). As a result, human service nonprofits are increasingly providing public services and depending on government funding for their operations (Smith and Lipsky, 1993).

The difficulty of specifying the contract and monitoring implementation influence who local governments contract with to deliver public services (Hefetz and Warner, 2012). Simple services, like trash collection, are easier to specify and monitor than more complex services, like human services. For example, the government can easily track whether garbage was collected, but is much more difficult to monitor whether people were effectively served.

Complete contracts, those clearly outlining all roles and responsibilities, can lead to the government achieving its privatization goal of long-term cost-savings. However, complete contracts are more difficult for complex services like human services. Since the government can only reap cost savings from contracting when monitoring costs plus the cost of the contract do not exceed the cost of government providing the service directly of service, agents must be chosen from a competitive market (Prager, 1994; Savas, 2000; Sclar, 2000). FAR (2020) even states that “adequate price competition” is a requirement for fixed-cost contracts (§16.202-2a). Yet, there is often weak competition where contract managers are left to manage the market (Johnston and Girth, 2012). In addition, human services carry a great deal of uncertainty (i.e., Brown et al., 2016, 2018), so it is nearly impossible to define the scope and services required to meet the complex demands of human services. As a result of this uncertainty, human service funding agreements are inherently incomplete. Incomplete contracts involve frequent transactions between principals and agents and high levels of uncertainty about the process or service provision.

Incomplete contracts of complex services are characterized by a lack of information, ex ante investment of resources, and discretion. Petersen et al. (2019) find ex ante costs vary due to the complexity of the product. Agents lack information about the value they will receive from providing the services and principals lack information about the cost of the services. As a result, both principals and agents must make specialized investments prior to entering the exchange (Williamson, 2005). Government agencies may invest resources into creating and implementing the contract, while nonprofit organizations may invest resources into creating or modifying a program to be able to provide the public services. The lack of information and the need for investments before implementing the contract contribute to its incompleteness that allow for discretion from both the government funder and nonprofit provider in its implementation.

In addition to the incompleteness of the contract, human services face complexity in service delivery in achieving intended outcomes. In providing social services, factors outside of the agent’s control tend to influence service provision (DeHoog and Salamon, 2002), such as changes to the economy or target population. Human services also pursue multiple goals, where performance is difficult to measure (Heinrich and Fournier, 2004), quality inputs do not guarantee quality outputs (Moynihan, 2005), and organizations are often jointly responsible for achieving outcomes (Unruh and Hodgkin, 2004). These factors add to complexity of government-nonprofit funding relationships.

Theoretical framework

At the core of government-nonprofit funding arrangements is a principal-agent relationship. In the case of human services, the principal (government) provides funds to the agent (nonprofit) to provide a public service. As a result, government agencies and nonprofit organizations who enter into funding agreements with one another face issues that accompany principal-agent relationships. Two major challenges arise in principal-agent relations due to the lack of certainty (Coase, 1937): conflict of interest and information asymmetry (e.g., Agranoff and McGuire, 2001; Brown et al., 2006).

First, principals and agents tend to have different preferences and will act out of their own self-interest (Williamson, 1979, 1981). Principals want to provide funded services in the most effective way possible to meet the public’s needs. On the other hand, agents may want to provide services in the most efficient way possible to maximize the payment received. In the case of government contracting with agents providing public goods and services, principals can reduce this potential conflict of interest with agents by considering its goal alignment with the agent. Government principals contract with nonprofit agents when government needs personalized service, small scale operations, or community control (Salamon, 1987). For example, government tends to contract with nonprofits that have the service expertise for complex services and those with high citizen interest, like human services (Hefetz and Warner, 2012). Compared to for-profit agents, conflict of interest may be less of a concern in government-nonprofit funding arrangements as nonprofit organizations are more likely to be concerned about service quality (Hansmann, 1987). Government contracts with nonprofits tend to be longer and involve less monitoring than those with for-profit providers (Witesman and Fernandez, 2013).

Second, information asymmetry, where the agent has more information than the principal since the agent is the one on the ground performing the service, is another major challenge in the relationship (e.g., Bendor et al., 1987; Waterman and Meier, 1998). The government principal has no way of completely ensuring that the nonprofit agent is acting in the government’s best interest. For example, a government agency may contract with a nonprofit organization to provide job training for the unemployed. The nonprofit agency has perfect information about the cost of the service since it is providing the service. However, the government agency can only estimate the cost of services based on the outcome or it must trust the nonprofit is honest in reporting the cost of providing the service. If a job-training program has a significantly larger start-up cost than initially thought, perhaps it needs more time and money to hire and train the trainers, a nonprofit agent may try to reduce those costs and potentially cut corners to do so. This creates a serious challenge: it is costly to the agent and difficult for the government principal to observe the agent directly.

Information asymmetry may result in moral hazard, where the agent engages in risky behavior because the principal bears the burden of the risks, or adverse selection, where the agent may choose clients who are easier to serve. Arrow (1968) comments on how complete reliance on economic incentives fails to lead to optimal allocation of resources due to moral hazard: “by definition the agent has been selected for his specialized knowledge and the principal can never hope to completely check the agent’ performance” (p. 538). An example of a moral hazard would be if the funding mechanism shield the nonprofit agent from consequences of providing job training by inadequately prepared trainers because the nonprofit has a long-term contract to provide job-training services for the government.

Adverse selection, deciding to serve only certain populations, may also result from information asymmetry. This is also called “creaming,” when an organization chooses those individuals who are easy to serve by skimming the “best” potential clients off the top to improve service outcomes (Rothschild and Stiglitz, 1978). For example, a nonprofit that screens unemployed individuals may decide to provide job-training services to only those individuals who are most likely to gain/regain employment within a month. Evidence of adverse selection has been found in areas with large information asymmetry, such as nursing homes, where public nursing homes serve a greater proportion of Medicaid recipients than both for-profit and nonprofit nursing homes (Amirkhanyan et al., 2008; Spector et al., 1998). Funding relationships inherently involve risks due to the lack of certainty, especially for human services, but risks can be shifted from principals to agents and agents to principals depending on the type of funding agreement.

The contract itself outlines the rights and responsibilities of the principal and agent in the exchange relationship. The exchange rules of the contract detail who bears the burden of risks (Lamothe and Lamothe, 2012; Miller and Whitford, 2007), where compensation terms determine who bears the risks of the final cost of providing a service (Bajari and Tadelis, 2001). Contracting allows government “to export its uncertainties” (Milward, 1994: 75). In contracting with nonprofit organizations to provide public services, government agencies have the option to shift the financial risks of providing those services to the nonprofit that is dependent on the government funding (FAR, 2020).

Risk shifting is one means to combat principal-agent problems, where the contractor is expected to have a vested interest in keeping production costs low (Sclar, 2000). However, government principals shifting risks to agents providing the service can result in financial instability or loss for the agents if conditions change considerably from the initial contract negotiation (Romzek and Johnston, 2000). This tends to be the case in human services, where the actual cost of providing a service may be higher than nonprofit’s bid due to lack of information on costs and unanticipated start-up costs (Unruh and Hodgkin, 2004). Such risk shifting scenarios would only exacerbate principal-agent concerns of adverse selection and moral hazard and may influence the agent’s ability to meet performance expectations or monitoring requirements. Risk shifting undermines accountability despite the intent to enhance contract effectiveness (Romzek and Johnston, 2005) and can create significant problems for contractors, including bankruptcy (Johnston et al., 2004). Despite the drawbacks of risk shifting, organizations choose the type of funding agreement that reduces uncertainty (Malatesta and Smith, 2011). By using a cost-reimbursement compared to a fixed-cost agreement, government agencies send a signal about who—the government principal or the nonprofit agent—should (and will) bear the burden of risk in the funding relationship. Cost-reimbursement agreements put the risk on the government principal, while fixed-cost agreements place the risk on nonprofit agents (FAR, 2020).

Hypotheses

The two most prevalent types of funding agreements are fixed-cost, which designate funds for outputs, and cost-reimbursement, which designate funds for inputs (Kelman, 2002; Kim et al., 2016). Definitions and applications for each are shown in Table 1. At the outset, government principals take on greater risks in fixed-cost agreements and nonprofit agents take on greater risks in cost-reimbursement agreements.

In fixed-cost arrangements, the risk is on the nonprofit organization that is providing the service (FAR, 2020), since the price was established when the agreement was put in place. However, the actual costs of service delivery may be higher. Fixed-cost contracts identify a final cost prior to service delivery, where a principal may pay an agent a set price on a monthly or yearly basis to provide a service. Fixed-cost contracts are suitable when prices can be reasonably attained in advance and when the costs of performance are relatively known (Malatesta and Smith, 2011). In fixed-cost arrangements, the agents take on much of the risk as the price has been set regardless of future conditions.

Short-term, fixed-cost contracts take advantage of the benefits of the market, but tend to be used for simple products whereas cost-reimbursement arrangements are used for more complex services (Kim and Brown, 2012). For cost-reimbursement arrangements, the government agency does not shift the risk associated with purchasing the services to the funder, since the funder pays the difference in production costs if they are higher than originally estimated (FAR, 2020). The final cost for cost-reimbursement arrangements are calculated after the service has been provided, where a principal reimburses an agent for actual allowable costs of providing the service. As a result, the costs of monitoring cost-reimbursement arrangements tend to be higher than in fixed-cost arrangements as agents may inflate the cost of providing the services.

The choice of funding agreement is a balancing act of risks. Government principals have the option of shifting risks to nonprofit agents through fixed-cost funding agreements, where there is no way for the nonprofit agents to be aware of the full cost of providing the service at the outset when the price is agreed upon. Meanwhile, government principals assume most of the risks in cost-reimbursement funding arrangements as the government agrees to reimburse the nonprofit for the whole cost of providing the service at the outset of the agreement, prior to service delivery. Consequently, Kim and Brown (2017) find federal government agencies use cost-reimbursement contracts for complex services and fixed-cost contacts for simple services. This public management decision is driven by product characteristics and market conditions (Kim et al., 2016), but what influence does the type of funding agreement have on the nonprofit carrying out the public services? More specifically, we ask: Do the bearers of initial risk take bear the brunt of future risk when the economy faces a recession? Are government agents and nonprofit principals more communicative in certain types of funding arrangements?

Fixed-cost

In human services, fixed-cost contracts take one of three forms: a flat amount fixed-cost for providing a service, a fee for service arrangement, or performance-based (FAR, 2020). A nonprofit organization may receive a flat amount for providing job-training services for a government agency for a year. Whereas in a fee for service arrangement, a nonprofit organization may receive a certain amount per person trained or for each time a person receives a service provided by the nonprofit. Fee for service contracts may be time or individual based, but regardless these arrangements incentivize quantity over quality since the government pays the contractor based on the number of services provided.

In addition, incentive or performance-based agreements have also grown in popularity (Behn and Kant, 1999; Heinrich, 2007). One way to overcome the issue of information asymmetry and the disparate preferences of principals and agents is to incentivize the agent by providing a financial bonus if the agent achieves the principal’s desired outcome. FAR (2020) describes how “the contracting officer may use a firm-fixed-price contract in conjunction with an award-fee incentive (see 16.404) and performance or delivery incentives (see 16.402-2 and 16.402-3) when the award fee or incentive is based solely on factors other than cost. The contract type remains firm-fixed-price when used with these incentives” (§16.202-1). Performance-based agreements focus on outcomes by clearly specifying the desired result and giving providers flexibility in the process. Sometimes government principals may find it easier to specify inputs, activities and processes, and outputs, while other times principals may find it easier to specify outcomes (Heinrich and Choi, 2007). For example, government may want to provide after-school care to keep children off the streets without specifying the end outcome. On the other hand, government may want to address homelessness, but may not specify how to do so.

Issues with performance-based systems in the U.S. date back to human service contracts under the Job Training and Partnership Act of 1982 (Barnow, 2000; Heckman et al., 2002). Performance-based arrangements shift the risks to the agent as compensation will be lower if performance goals are not met. Here performance-based arrangements make two major assumptions: first, performance measures accurately capture intended outcomes, and second, agents will not game the system through adverse selection or inaccurate reporting. As such, performance incentives tend to be used for more simple services (Girth, 2017). While performance-based contracts tend to increase measured performance, creaming and gaming occur (Koning and Heinrich, 2013), performance on unmeasured outcomes is trivial (Lu, 2016), and penalty provisions increase costs (Shetterly, 2000). A goal of performance-based contracts is to combat principal-agent problems, but they are not without their drawbacks and concerns.

In fixed-cost funding arrangements agents bear the burden of the risk. A flat amount or per time or per individual price is set ex ante, but the actual cost of providing the service may end up being significantly higher due to start-up costs and the lack of information in estimating the costs at the outset of the funding agreement. Performance-based systems also shift the risk from the principal to the agent because the agent will receive a lower payment if it fails to obtain outcomes, which incentivizes nonprofits to meet performance targets.

Fixed-cost agreements work best for simple services, where the nonprofit will accept the risks of providing the service since it knows what will be needed to provide the service (Kim et al., 2016). For contracts where mission criticality and complexity are low, Eckerd and Girth (2017) find suppliers bear most of the risk in fix cost contracts. Since fixed-cost arrangements shift the burden of financial risks from the government principal to the nonprofit agent, nonprofits with these types of contracts will be more likely to face an increase in costs and late payments during an economic downturn.

Cost-reimbursement & relational contracting

Meanwhile, cost-reimbursement funding agreements shift the burden of risk from the agent to the principal as principals enter into an agreement to repay the actual costs of services ex post. Cost-reimbursement agreements are more appropriate and preferred for complex services (Eckerd and Girth, 2017), where nonprofits may be reluctant to enter into an agreement due to the uncertainty of providing the service. Since government principals bear much of the financial risk in cost-reimbursement agreements with nonprofit agents, government principals are less likely to transfer financial risk in times of budget uncertainty.

Principal-agent theory alone is insufficient to explain the complex exchange relationship. Macneil (1978, 1981) calls for the need to examine the relational aspect rather than merely the transactional (Williamson, 1981) aspect of contracting. The transactional perspective assumes the exchange can be reduced to an economic transaction and neglects the human aspect (Hofstede, 1994). Contract law introduces the idea of long-term contractual relations with the need for planning and flexibility, but relational contracting focuses on the irrational human and social aspect of the exchange (Macneil, 1983). Relational contracts follow several norms, or patterns of accepted behavior: role integrity or long-term obligations, preservation of the relation or contract solidarity, harmonization of relational conflict or the need for planning and flexibility, propriety of means or acceptable practices, and supracontract norms or the reflection of broader social principles (Macneil, 1980, 1983). As such, relational contract theory, in part, helps explain why nonprofits may be the preferred provider for human services.

One way to reduce uncertainties is to share information. Requiring principals and agents to share information can enhance the efficacy of exchanges by clarifying reporting and monitoring (Brown et al., 2016). While public managers often have tools to hold contractors accountable, such as sanctions, Girth (2014) found a lack of willingness to use discretion, the hurdles to use sanctions, and the dependence on poor performing agent to limit their use. For complex services, like human service provision, communication is vital (Carnochan et al., 2019). Government principals and nonprofit agents enter into a partnership to develop and implement a relational contract (Brown et al., 2006).

With the complexity of human service delivery, the contracting relationship between government and nonprofits is relational and collaborative (McBeath et al., 2017). The relational or informal aspect rather than what is written in the formal agreement play a major role in accountability (Girth, 2017; Romzek et al., 2014). In this sense, trust can serve as a substitute for monitoring (Edelenbos and Klijn, 2007; Van Slyke, 2009). Relational contracting allows contract terms to evolve over time (Campbell and Harris, 1993; Fernandez, 2007, 2009) and trust to build (Van Slyke, 2007). Such joint dependence of funders and providers lead parties to choose more flexible contracts (Malatesta and Smith, 2011). Contracting for complex services necessitates building a reciprocal relationship and establishing a mutual understanding (Brown et al., 2016, 2018). One aspect of a reciprocal and collaborative funding relationship is nonprofit engagement in accountability dynamics.

While principal-agent theory suggests agents will shirk responsibility, Schillemans and Busuioc (2015) identify the paradox that many agents try to enhance accountability by instructing their principals or setting up their own accountability mechanisms. Additionally, agents are more satisfied when they participate in contract implementation (Amirkhanyan et al., 2010). Complex services tend to turn to collaboration to address performance issues (Girth, 2017; Van Slyke, 2007). Since cost-reimbursement agreements are preferred for complex services, we expect nonprofits with cost-reimbursement funding arrangements will be more likely to be involved in contract implementation. Government principals will want to keep in contact with nonprofit agents in order to keep costs low and ensure the public services are being provided effectively. Cost-reimbursement funding arrangements also begin with a foundation of trust as government agencies assume most of the risk in the funding relationship with the nonprofit. In line with relational contracting, those with cost-reimbursement funding agreements will be more involved in implementation.

Data and methods

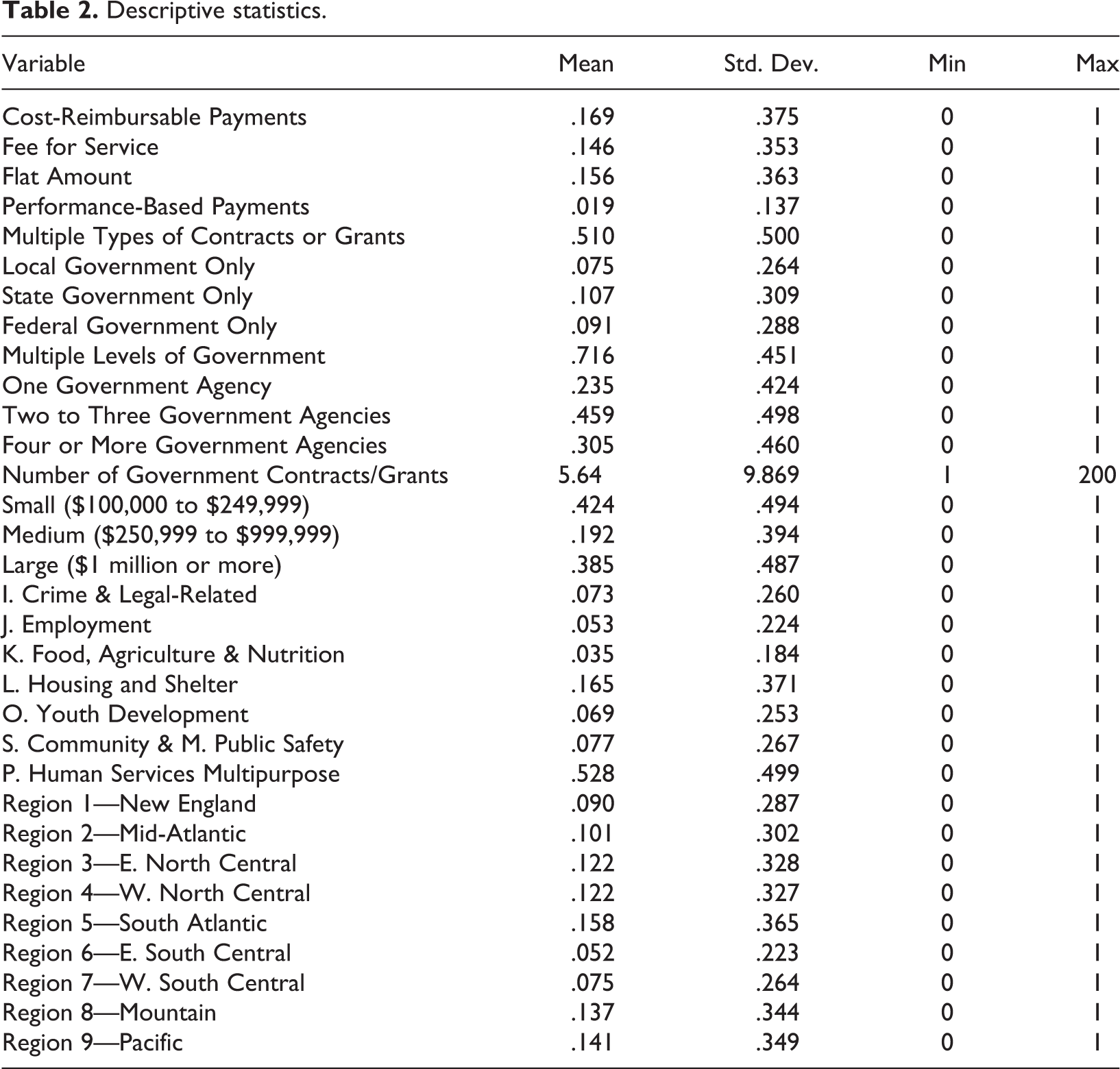

To examine the influence of contract type on the government-nonprofit funding relationship, this study draws upon data from the Urban Institute’s 2010 National Survey of Nonprofit Government Contracting and Grants. This national survey randomly drew 501(3)(c) human service nonprofit organizations with at least $100,000 in expenditures, those required to file a Form 990 with the U.S. Internal Revenue Service, using the 2007 Core Files from Urban Institute’s National Center for Charitable Statistics. The national, random sample consisted of 55,785 direct human service nonprofits, which was narrowed down to a random stratified sample of 9,000 organizations stratified by region, type, and size in order to ensure a representative sample was obtained. The survey data was collected by the Social and Economic Sciences Research Center at Washington State University, where organizations completed the survey either online or by mail. The final response rate was 36% with 2,497 human service organizations (Boris et al., 2010). This study focuses on the responses from the 2,153 human service nonprofit organizations that received government funding in the form of grants or contracts.

The survey was administered in 2010 asking respondents to reflect on the previous year, during the Great Recession where the unemployment rate peaked at 10% in October 2009 (U.S. Bureau of Labor Statistics 2012). Hypotheses 1 and 2 examine the influence of the type of funding agreement on the reliability of government funding during the Great Recession. We examine two measures of government funding reliability: increased costs and late payments. First for increased cost, respondents were asked: “In 2009, did local or state government impose new, or increasing existing, fees, taxes, or other director costs your organization had to pay?” Second for late payments, respondents were asked: “In 2009, were government agencies late (i.e., past due date) in paying your organization?” About 14% of the human service nonprofits had new or increased direct costs from the government and nearly 62% faced late payments.

The third dependent variable examines the relational aspect of the funding relationship to see if contract type influences whether nonprofit organizations are given a say in the implementation of the funding agreement. Here respondents were asked, “Does your organization provide feedback to government on contracting issues and procedures?” Nonprofits engaged in the funding relationship by providing feedback, such as through meetings, indirect advocacy, or official government feedback mechanisms, account for nearly 62% of the sample.

Funding agreement type is measured by the type of payment nonprofit organizations received from their government funders. Here nonprofits were asked: “Which of the following pay methods apply to your organization’s government contracts/grants?” and given the options: “Unit cost payments/Fee for service ($ per time unit),” “Unit cost payments/Fee for service ($ per individual/family),” “Cost reimbursable payments,” “fixed-cost (flat amount),” “Performance-based payments,” and “Other.” Respondent organizations were allowed to check all of the types of funding arrangements that apply to their government contracts or grants. This study examines indicator variables for nonprofit organizations that only have one type of payment method (fee for service, cost-reimbursable payments, fixed-cost, or performance-based payments) compared to organizations have multiple types of funding agreements with government agencies. We are interested in the differences between cost-reimbursement funding agreements and fixed-cost agreements. As such, we compare nonprofits who only receive cost-reimbursable payments (16.9% of the sample) and nonprofits who only receive fixed-cost payments, in the form of fee for service (14.6%), flat amount (15.6%), or performance-based payments (1.9%), to nonprofits who receive multiple types of government contracts or grants. Our descriptive statistics are below in Table 2.

Descriptive statistics.

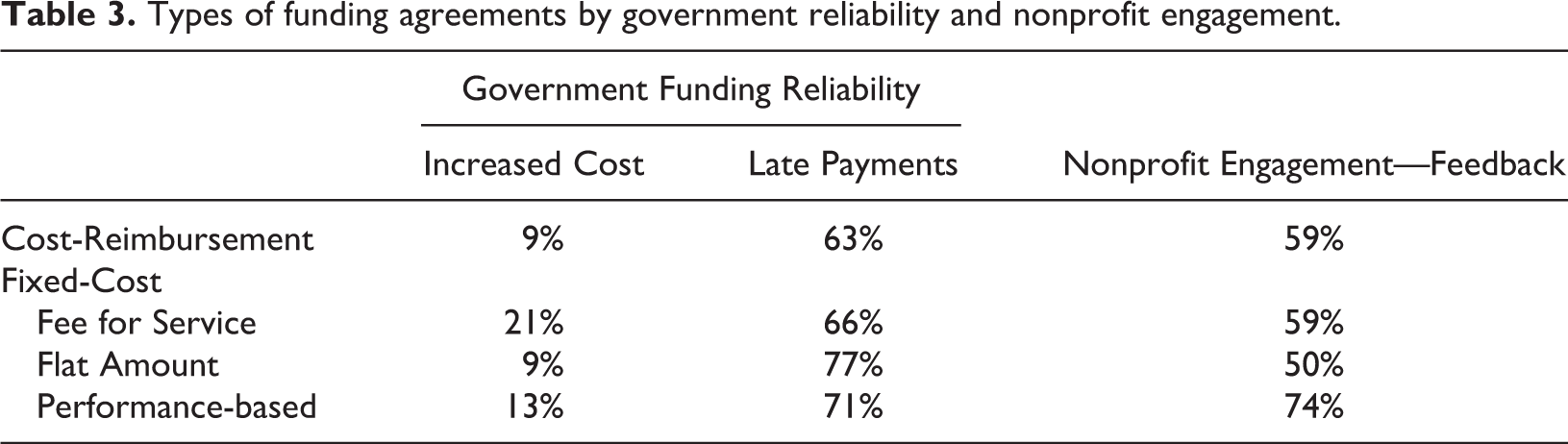

All three dependent variables, increased cost and late payments for government funding reliability and feedback for nonprofit engagement, are yes/no questions so take on a 1 if the nonprofit respondent answered yes and a 0 otherwise. The correlation between the types of funding agreements and dependent variables are below in Table 3.

Types of funding agreements by government reliability and nonprofit engagement.

In order to isolate the impact of the type of funding agreement on government-nonprofit funding relations, a number of variables are included in the analysis to control for funder and organizational characteristics. The level of government a nonprofit organization partners with may influence both contract type and the funding relationship. Johnston et al. (2004) found state governments focused on contract type due to the financial stakes and nature of the services provided. The level of government nonprofits receive funding from are included with indicator variables for nonprofits receiving funding from the federal government only, state government only, or local government only, compared to those receiving funds from multiple levels of government.

Funding agreements create principal-agent relationships, but according to stewardship theory, government-nonprofit relations evolve over time as trust builds (Van Slyke, 2007). Long-term relationships develop through repeated interactions (Ansell and Gash, 2008; Ostrom, 1998). Trust plays an important role in contract type as contracts are less complete with high levels of trust (Brown et al., 2007). To understand long-term funding relationships better, the number of funding partners, with indicators for one or two to three compared to four or more, and the number of government contracts or grants, ranging from 1 to 200, are included.

Organizational characteristics also play a role in funding agreements. Organizational size may influence funding agreements. Larger nonprofits receive more government grants (Ashley and Van Slyke, 2012; Okten and Weisbrod, 2000), while smaller nonprofits often perceive obstacles to collaborating with government agencies (Foster and Meinhard, 2002; Gazley, 2008). Indicator variables are included for organizational expense size with indicators for $250,000 and $999,999 and $1 million or more compared to the smallest category with budgets between $100,000 and $249,999.

Differences have been found in both financial management strategies and how strategies work across nonprofit industries and organizational types (Chang and Tuckman, 1996; Greenlee and Trussel, 2000; Hager, 2001). To account for these organizational differences indicator variables are included for the National Taxonomy of Exempt Entities (NTEE) category for the type of human services the nonprofit organizations provide. Public safety and disaster relief organizations are combined with community and economic development since both groups are focused on community issues. The NTEE types included are: crime and legal-related; employment; food, agriculture, and nutrition; housing and shelter; youth development; and the combined community and economic development and public safety and disaster relief, compared to multipurpose human service organizations.

Lastly, the geographical location of a nonprofit organization may also influence funding agreements as different areas may have different social, political, economic, and cultural climates, especially during the Great Recession. Census regions are included to account for these locational differences. Descriptive statistics for each variable may be found in Table 2.

Logistic regression is used to examine the three models since each dependent variable—government funding reliability measured by increased costs and late payments and nonprofit engagement measured by feedback to government—is a dichotomous variable. Odds ratios and robust standard errors are reported. All analyses are weighted to represent the entire human services nonprofit sector with government funding across the United States.

Results

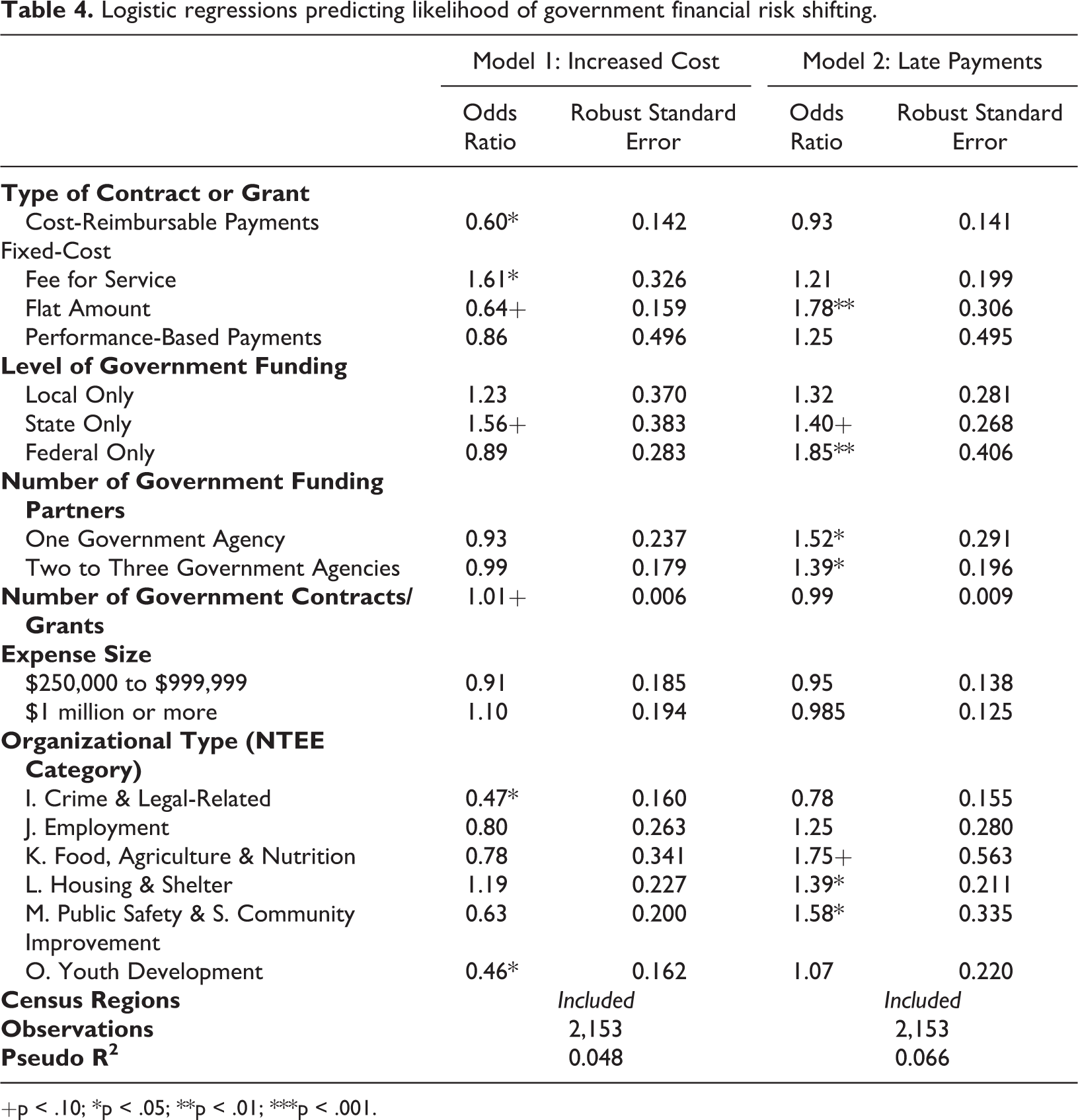

The results for the logistic regression models predicting the influence of funding agreement type on funding reliability during the Great Recession are shown in Table 4. In partial support of H1, nonprofit organizations with fee for service agreements are more likely to face increased costs from their government funding partners as shown in model 1, but the other fixed-cost arrangements, flat amount and performance-based, are not substantially different from nonprofits with multiple funding agreement types. However, nonprofit organizations with cost-reimbursable payments are less likely to have government funders raise costs, supporting H2.

In model 2, only nonprofit organizations with flat amount fixed-cost agreements are more likely to face late payments from their government funders. In partial support of the H1, fee for service and flat amount fixed-cost funding agreements shift the financial risk from the government principal to the nonprofit agent, as shown through increased costs for fee for service and late payments for fixed-cost during the recession. Meanwhile, cost-reimbursable funding agreements did not have a significantly different risk of receiving late payments during the Great Recession compared to nonprofits receiving government funds through multiple types of agreements.

In terms of funder and organizational characteristics, the type of organization influences both the odds of incurring additional costs, crime and legal-related and youth development are less likely, and the odds of facing late payments, housing and shelter as well as public safety and community improvement are more likely than multipurpose human service organizations. Nonprofit organizations who partner with fewer government agencies, compared to four or more, and the federal government only, compared to partnering with multiple levels of government, were more likely to face late payments.

Logistic regressions predicting likelihood of government financial risk shifting.

+p < .10; *p < .05; **p < .01; ***p < .001.

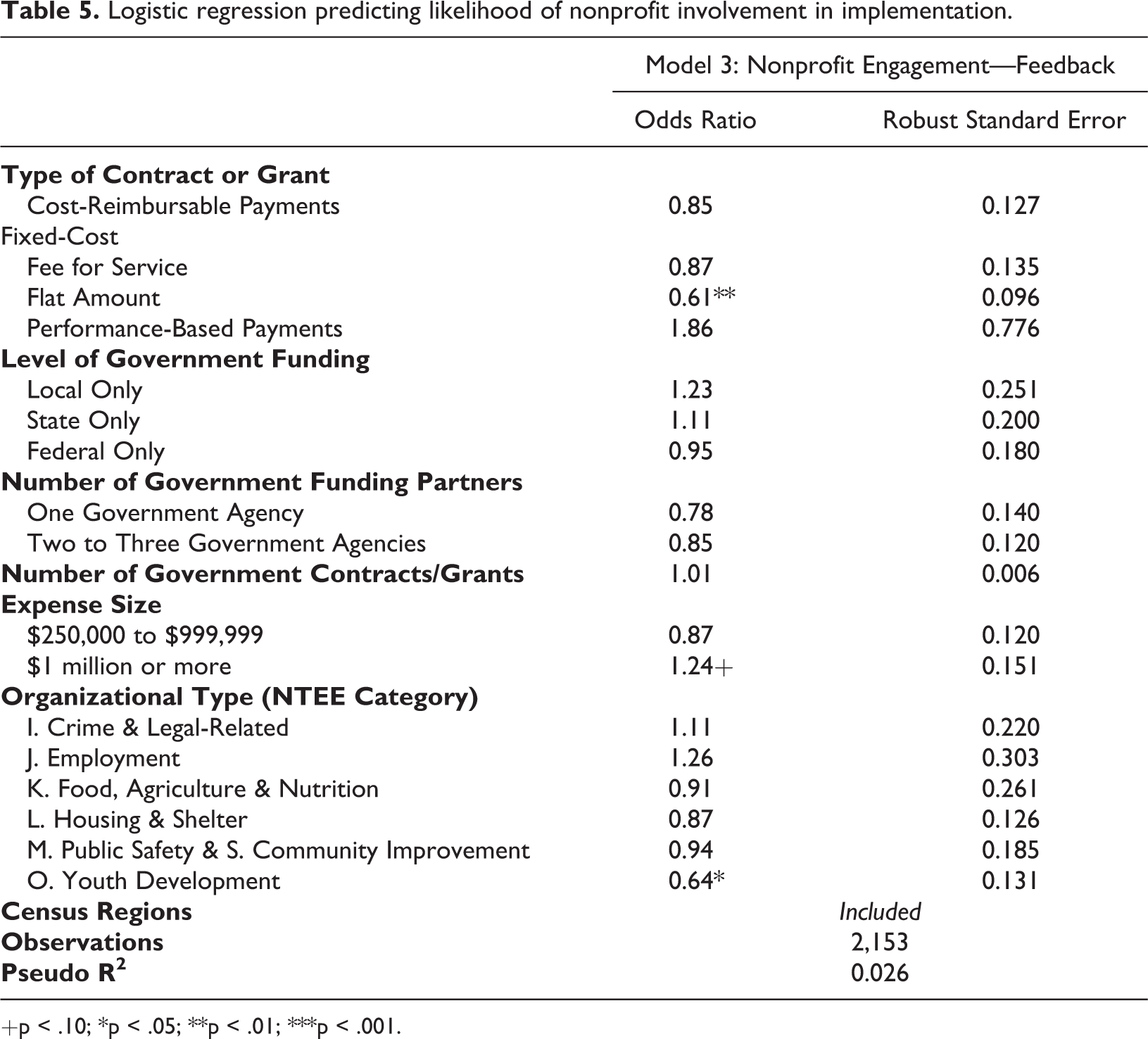

The results for the logistic regression model predicting the likelihood of nonprofit engagement with government funders are shown in Table 5. As shown in model 3, only nonprofit organizations with flat amount fixed-cost funding agreements are less likely to provide feedback to government funders during the implementation of the funding agreement. Contrary to the hypothesized relationship, nonprofits with cost-reimbursable funding arrangements were not found more or less likely to provide feedback in implementation. However, funding agreements that shift the risk from government principals to nonprofit agents are even more risky if nonprofits are not given a say in the implementation process. For example, nonprofits with flat amount fixed-cost funding agreements were found more likely to face late payments yet less likely to provide feedback to government funders during contract implementation.

Logistic regression predicting likelihood of nonprofit involvement in implementation.

+p < .10; *p < .05; **p < .01; ***p < .001.

Discussion

This study sheds light on whether the type of funding agreement influences government-nonprofit relations since we know little about how contracts or grants themselves affect the funding relationship. We examine government funding reliability that is whether government shifts risks to the nonprofit during times of uncertainty through increased costs and late payments and nonprofit engagement that is whether nonprofits provide feedback to the government funders. Nonprofits with fixed-cost fee for service funding agreements not only bear the burden of risks at the outset of the grant or contract, but were also found more likely to face cost increases in times of uncertainty. Meanwhile, nonprofits with cost-reimbursable funding agreements not only benefit from the government taking on a majority of the risks at outset, but also benefit from lower chances of future risk shifting. For flat fixed-cost funding agreements, which shift the burden of risks to nonprofit providers, government was more likely to make late payments and the nonprofits were less likely to provide feedback to the government funders. The type of funding agreement is not only the legal foundation for government-nonprofit funding relations, but also plays a significant role in specifying the exchange relationship between principals and agents.

This study answers the call of scholars to examine the formal funding agreement itself (Cooper, 2003; Kim and Brown, 2012; Kim et al., 2016) as the type of agreement plays a role in the allocation of risks and incentives to nonprofit providers, especially for complex services. Risk shifting is one way government principals can address potential principal-agent problems by shifting risks of the unknown to nonprofit agents. However, risk shifting can unduly burden nonprofit agents if conditions change considerably between the establishment of the formal funding agreement and its implementation. Nonprofit agents may under bid due to lack of information on true costs or unanticipated start-up costs, where bearing the burden of risk can have significant consequences for contractors, including bankruptcy (Johnston et al., 2004; Romzek and Johnston, 2000, 2005; Unruh and Hodgkin, 2004).

The type of funding agreement not only influences the amount of risk government principals shift to nonprofit agents at the outset of the formal funding agreement, but also influences future risk shifting. Fixed-cost, both fee for service and flat amount, arrangements shift the burden of risk to the nonprofit agent since the exact costs of providing the service may end up being higher than the estimated ex ante costs. Nonprofits with fixed-cost funding agreements were also more likely to face future risk shifting. Nonprofits with fee for service arrangements were more likely to face increased costs and nonprofits with flat fixed-cost arrangements were more likely to face late payments. Meanwhile, cost-reimbursable funding agreements place the burden of risk on the government principal who promises to repay the nonprofit agent for the full amount of providing the service ex post. Nonprofits with cost-reimbursable arrangements may also be less likely to take on future risks from government funders.

For complex services, like human services, relational contracting tends to be more effective where government principals and nonprofit agents enter into a partnership with more flexible contracts (DeHoog, 1990; Girth, 2014; McBeath et al., 2017; Macneil, 1980; Malatesta and Smith, 2011; Van Slyke, 2007). Not only may more of a partnership be needed for delivering complex services effectively, but agents are also more satisfied when they participate in contract implementation (Amirkhanyan et al., 2010). We find the type of funding agreement corresponds to both risk shifting and nonprofit engagement through feedback mechanisms. We find not only do nonprofits with flat fixed-cost arrangements tend to bear the burden of both initial and future risks, but are also less likely to provide feedback to government funders. Nonprofit organizations take on the largest risk with the least amount influence with flat fixed-cost arrangements. With the cost of the services detailed ex ante when the parties form the formal funding agreement, nonprofits take on the risks of the costs changing in the process of implementation. Yet are also less engaged and less likely to provide feedback to government funders, where nonprofits may be left to face changing conditions alone in bearing the brunt of the financial risks. Fixed-cost contracts are the most risky for nonprofits, especially where nonprofits are less likely to have a voice in the implementation of what should be a less complete and more relational contract for complex services.

This study takes a first step at examining the influence of the formal funding agreement type on government-nonprofit relations. However, like most studies, it is not without limitations. First, due to data constraints, the comparison groups are nonprofits with multiple types of formal funding agreements. This study provides a glimpse into the relationship between contract type and risk shifting, but future work could more fully examine these dynamics with a more specific comparison. Second, the data are limited to human services, which is useful to examine to shed light on a common complex service, but contract type may have a different influence in other settings. For example, contract type may have a very different influence on funding relationships for simple services, such as trash collection. Future research should examine formal contracts in other contexts.

Conclusion

This study fills a gap in the literature by examining differences between two types of contracts, which is at the heart of the boundary spanning funding relationship. In selecting a type of formal funding agreements, government principals have the option of shifting the burden of risk to nonprofit agents and of providing incentives, both to overcome the issues that arise in principal-agent relationships. However, government not only exports uncertainties and risks at the outset of the contract, but also shifts future risks when faced with financial instability by increasing costs to the nonprofit agent or providing late payments.

Nonprofits that enter into fixed-cost arrangements, both fee for service and a flat amount, bear the burden of risk in the formal funding agreement and face additional risks in the implementation of the contract. Yet, nonprofits with flat amount fixed-cost funding agreements were also less likely to participate in the implementation process. Cost-reimbursable funding agreements, on the other hand, leave the bulk of the risks with the government principal, where nonprofit agents are also less likely to face future risks. Both government principals and nonprofit agents should carefully consider the risks involved in different types of contracts when entering into formal funding agreements.

Risk shifting in the initial formal funding agreement influences future risk shifting in times of uncertainty. Government principals can shift uncertainties to nonprofit agents or can retain a majority of the financial risks in contract type. Risk shifting is one means to address principal-agent problems in contracting, but can have serious consequences, especially for nonprofit agents bearing the brunt of the risks. Public and nonprofit managers should carefully consider the risks and uncertainties involved in contract type and the influence such decisions have in maintaining effective funding relations in contract implementation.

Footnotes

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.