Abstract

When planning is possible, as in predictive environments, comprehensive contracting is not only desirable, but also useful. However, under conditions of fundamental uncertainty, as is the case in non-predictive environments, incomplete contracting approaches likely prevail. In this study, we explore how trust in such environments affects the way in which venturing professionals negotiate, and how the outcome subsequently manifests itself in the negotiated agreement. In particular, building upon a sample of Norwegian firms, we find that stewardship relationships are more prone to incomplete contracting approaches than agency relationships, paving the way for a relational approach to contracting when uncertainty is high. Implications for theory and practice are discussed.

Introduction

Managers often operate in uncertain and risky circumstances and must make numerous choices in organizing their firms. One of the most important choices made by entrepreneurial managers relates to the structuring of control rights and contracts in an exchange (Alvarez and Barney, 2005). In an entrepreneurial context, exchanges include, amongst others, ownership negotiations (vertical arrangements), supplier and customer interactions, and partner relationships (lateral arrangements, such as public-private partnerships).

In a search for new foundations for the theory of the firm, Zingales (2000) asserts that a renewed approach to the firm is needed and advocates that time has come to move from the firm as a nexus of complete contracts, to the firm as a nexus of complete and incomplete contracts. A similar view is held by Kor and Mahoney (2015) who argue that new governance approaches within management are needed beyond the complete contracting approaches, calling for more implicit, and incomplete contracting related research. More recently, Alvarez and Porac (2020) address similar ideas when they look forward and make a call for more research into management under conditions of fundamental uncertainty, as management in unpredictable environments is a very different task than management in more predictable environments.

At the same time, while the management and governance literatures have dedicated significant attention to complete contracting approaches (such as agency relationships), there is less research taking an incomplete contracting approach. One notable exception is the study by Poppo and Zenger (2002) indicating that formal contracts and trust complement each other (when addressing lateral arrangements). This is likely also the case with vertical arrangements when negotiations serve as a mediating mechanism. In the current study, we start from the understanding that stewardship theory embraces co-operation and collaboration (Sundaramuthy and Lewis, 2003) and a trusting relationship between shareholders and managers, in contrast to agency theory (Davis et al., 1997). Agency theory states that managers are agents whose interests may diverge from those of principals (shareholders), whereas stewardship theory is concerned about situations in which managers are not driven by individuals goals, but are stewards whose motives are in line with those of principals (Davis et al., 1997). In situations where social relations prevail, implicit, and incomplete contracting approaches will tend to dominate (Kor and Mahoney, 2015). The theoretical underpinning of stewardship theory is not jurisprudence, nor economics, as with agency theory, but social relationships from a joint psychological and sociological point of view.

Overall, we conjecture that if parties employ an agency theoretical approach to contracting, they will typically seek to specify the content of the relationship as much as they can ex ante, resulting in more covenants. But, if the parties employ a stewardship theoretical approach, they will not, which will result in fewer covenants. This is because, while agency theory is primarily concerned with minimizing potential agency costs, and is attentive to monitoring and control, stewardship theory, in contrast, relies on trust, and is preoccupied with maximizing shareholders’ and managers’ joint utility, that is, potential organizational performance (Davis et al., 1997; Donaldson and Davis, 1991).

The extent to which a contract is incomplete does not only depend on the level of trust, but it also reflects the party's attitude towards uncertainty. In a context where uncertainty prevails, it is only human to try to safeguard against potential losses, but the very action of safeguarding is also limiting and even restricting opportunity exploration and pursuit. For instance, Cummins (2015) captures the very essence of this assertion in the following quote: “For many, the purpose of contracts and negotiation has been more about avoiding risk than creating value. And […] business leaders have failed to grasp the true significance of contracts and the process that surrounds them” (Cummins, 2015:11).

Although Alvarez and Porac (2020) considered fundamental uncertainty as Knightian uncertainty (the “unknown knowns” according to Phan and Wood (2020)), we also pay attention to what Knight (1921) labeled as “risk” (the “known unknowns” according to Phan and Wood (2020)). 1 That is, the more safeguarding the parties are the more covenants they tend to include. In contrast, the less safeguarding, the less covenants.

In analyzing the relationship between uncertainty, trust, and the nature of contracts, we draw on unique data from entrepreneurial firms seeking venture capital, as we deem the context of venture capital investing particularly interesting for a number of reasons. First, venture capital investing is a context characterized by high levels of uncertainty (the presence of both “known unknowns” and “unknown knowns”), and thus information asymmetry, in which “internal” and “external” risks and uncertainties prevail (Kaplan and Strömberg, 2004). The “known unknowns” and “unknown knowns,” or the information gaps, work in both ways, in which entrepreneurs are often knowledgeable about elements internal to the firm, whereas venture capitalists are often knowledgeable about elements external to the firm, for instance, the industry or broader context. It is further acknowledged as a context in which financial contracts can mitigate potential principal-agent problems arising from such information asymmetries (Kaplan and Strömberg, 2001).

Second, trust is considered an important element in venture capital investing (Meuleman et al., 2010, 2017; Sorenson and Stuart, 2008). Indeed, in studying the role of trust in venture capital transactions, scholars have differentiated between generalized trust and personalized trust (Bottazzi et al., 2016). Generalized trust is then understood as “the preconception that people of one identifiable group have for people from another identifiable group” (p. 2284), whereas personalized trust is understood as a “set of beliefs that one person has about the behavior of another specific person” (p. 2287). In studying the role of trust in venture capital transactions, studies have focused on understanding the role of generalized (also known as “thin,” impersonal) trust, and, in doing so, have shed some light on how this type of trust affects the likelihood of investment (e.g. Bottazzi et al., 2016; Meuleman et al., 2017). Generalized trust is expected to mitigate “external risks,” whereas (“thick”) personalized trust may mitigate “internal risks” (Kaplan and Strömberg, 2004; Ring and Van de Ven, 1992). The two different trust types have different antecedents. For instance, Delhey and Newton (2005) conceptualize “thin” trust as a function of social structure, whereas “thick” trust can be understood through human agency.

In this paper, we deal with the latter type of trust only, i.e. personalized (or interpersonal) trust as a relational governance mechanism. Specifically, this paper aims at shedding light on the role of trust, taking a stewardship theoretical point of view. That is, we address the relationship between interpersonal trust and contract design, and particularly the incompleteness of negotiated contracts. The focus is however not only on the relationship between interpersonal trust and contract designs, but also on the negotiations that lead towards signed contracts and their levels of completeness. In doing so, we aim at disentangling the process through which interpersonal trust and contract design are related, alongside the contingencies that affect this relationship. In doing so, we particularly focus on an interesting context, namely that of venture capital contracting.

In approaching our research objectives, we contribute to the literature in a number of ways. First, our paper contributes to the economics literature, which has called for field studies in the incomplete contracting domain (Foss and Klein, 2016). It further contributes to this literature by identifying contingency factors affecting the trust-contract relationship, as such responding to one of the calls by Welter (2012) to contextualize the interplay between trust and control mechanisms in entrepreneurship. Second, our study contributes to the stewardship literature and the knowledge on the role of interpersonal trust specifically, as such also responding to a call by Bottazzi et al. (2016) to provide a deeper understanding of the role of trust in economic transactions. Whereas they studied the effects of generalized trust on investment decisions, we address the role of interpersonal trust under conditions of fundamental uncertainty. As such, our study contributes to the literature by providing insights into the deal negotiation process, which has received little attention so far, while crucial in understanding stewardship relationships. Finally, our study contributes to the negotiation literature, in which few studies have looked into the negotiation behavior of managers of high-growth companies (for an exception, see Artinger et al., 2015).

Our paper also has a number of important practical implications. Particularly, it provides deeper insights into the process through which investment negotiations lead to more comprehensive contracts, as such potentially helping investors and entrepreneurial managers (hereafter “entrepreneurs”) to understand the process of contract design and contingencies affecting it. Such insights can help practitioners in avoiding critical mistakes in this process (Mason and Harrison, 2002), especially under conditions where the future is unknown and/or unknowable.

The remaining paper unfolds as follows. First, we present our theoretical framework, hereby developing hypotheses on the relationship between interpersonal trust and contract design, alongside hypotheses for understanding the process and contingencies of this relationship. Second, we present the research methodology. Then, we elaborate on our findings, followed by a discussion of the results, alongside implications for theory and practice and directions for further research.

Theoretical development

Research on venture capital has so far covered the entire investment life cycle, including deal flow generation and selection, appraisal, contracting, monitoring, and exiting of portfolio companies (Burchardt et al., 2016). In this study, we are particularly concerned with contracting, and the factors that affect the extent to which incomplete contracts are developed. In doing so, we particularly focus on the eventual outcome of the contracting process, namely the contract itself (what is typically referred to as “term sheet” in venture capital contracting (Brown and Wiles, 2016)). While we apply our theorizing to the venture capital context, we would like to highlight that it would also likely hold for other contracts, e.g. when these are formed under uncertain circumstances in which fundamental uncertainty is present.

The relationship between interpersonal trust and contract design

As we argue in what follows, in contrast to agency theory, stewardship theory would encourage less complete contracting. According to Kaplan and Strömberg (2004), venture capitalists face four generic agency problems in the investment process. These problems relate to the effort of the entrepreneur post-investment, the information asymmetry between entrepreneur and investor in terms of the quality of the venture, post-investment conflicts between entrepreneur and investor, and the threat of the entrepreneur leaving the venture post-investment (i.e. managerial and competitive opportunism). It is generally accepted that venture capital contract design will be contingent on the likelihood of such agency problems occurring (Kaplan and Strömberg, 2004). At the same time, trust is said to reduce the risk and uncertainty of inter-organizational exchanges (Meuleman et al., 2010, 2017; Sorenson and Stuart, 2008) and to reduce the need for safeguarding (McEvily et al., 2003). Such trust reflects the absence of monitoring, favorable or forgiving predilections, and discreteness (Mahoney, 2005), and is viewed as an important social lubrication system as it “saves a lot of trouble to have a fair degree of reliance on other people's word” (Arrow, 1974; cf. Mahoney, 2005: p. 92). Along the same lines, Welter (2012) argues that trust can substitute for control mechanisms and monitoring. These assertions follow the notion of incomplete contracting which is central to property rights theory (Hart, 1995). This theory assumes that exchanging parties will revise and renegotiate contracts ex post if required, and therefore, not all contingencies have to be specified ex ante to safeguard investor's interest (Mahoney, 2005). As a result, if the entrepreneur- venture capitalists relationship is characterized by high levels of interpersonal trust, parties may settle for more incomplete contracts, which are contracts consisting of fewer covenants. By consequence, we offer the following hypothesis:

Hypothesis 1: Higher levels of interpersonal trust between the entrepreneur and the venture capitalist will positively relate to fewer contractual covenants (i.e. less complete contracts).

Disentangling the process through which interpersonal trust affects contract design

A contract in a principal-agent theoretical model is complete, or comprehensive, if it specifies all parties’ obligations in all future states of the world (Mahoney, 2005). According to this model, there will never be a need to revise a contract as the future unfolds, as these revisions could have been anticipated on and built into the initial, complete contract. In such a comprehensive contracting world, legal disputes are non-existing (Hart, 1995; Mahoney, 2005). There is further no need for trust as all relevant matters are specified in the contract ex ante. Therefore, investors will focus on securing their own rights and preferences if they have reasons to expect opportunistic behavior in the relationship with the entrepreneur. By consequence, they will spend much time clarifying contract covenants (Barney et al., 1994), and will therefore seek to write more complete, or more comprehensive, contracts.

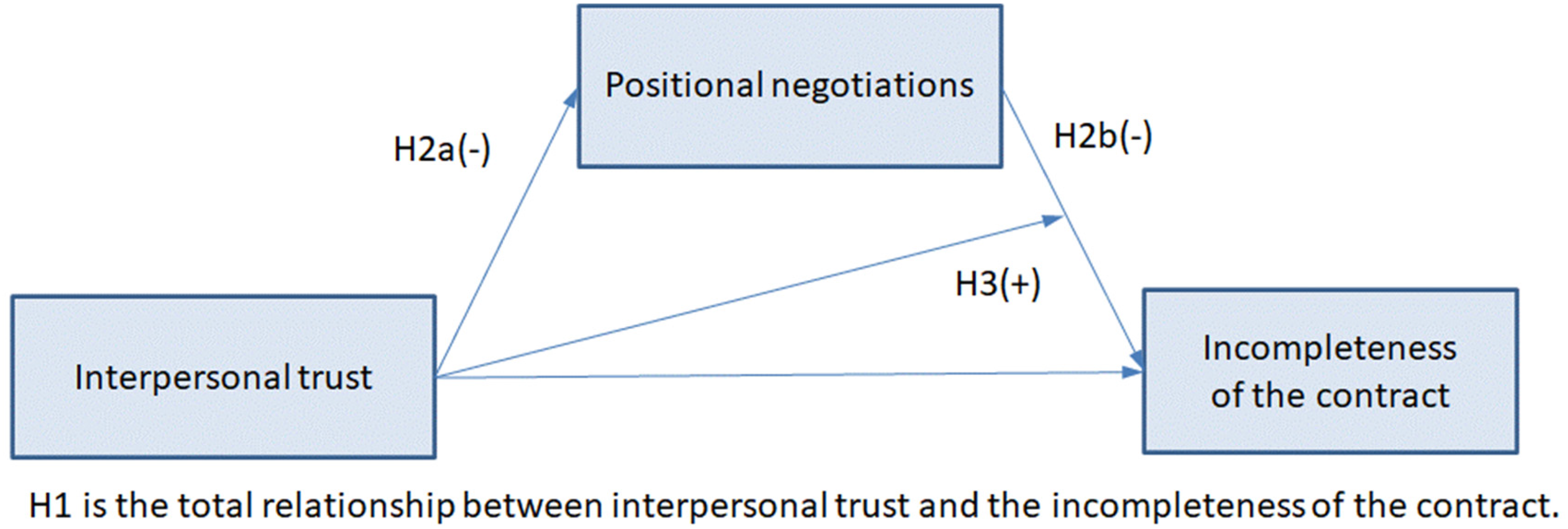

In contrast, the incomplete contracting approaches advocate fewer covenants, taking into consideration real-world settings with imperfect markets, imperfect information, and bounded rationality (Mahoney, 2005). We may also add true or fundamental uncertainty (Alvarez and Porac, 2020; Knight, 1921; Phan and Wood, 2020) to the equation, as the outcome of the situation the parties are facing are not only unknown, but also unknowable. This point of departure indicates that contracts are likely to be incomplete because of the high transaction costs affiliated with the difficulty to think and plan far ahead, negotiate future plans, and write these plans down in an enforceable manner (Coase, 1988; Mahoney, 2005; Williamson, 1985). Instead, parties must rely on each other, and are not likely to negotiate extensively ex ante (or they will simply prioritize, and concentrate on, the most important covenants). Put differently, they will to a lesser extent scrutinize contract covenants—or engage in what we label as rights-based negotiations. Furthermore, they will deal with the circumstances ex post This is the case when trust is high as under stewardship conditions, in which the need to safeguard own interests is felt to be less of a concern. By consequence, we argue that higher levels of interpersonal trust will relate negatively to engagement in rights-based negotiations. Negotiation parties will tend to dedicate much effort to rights-claiming negotiations when trust is low (or absent). In contrast, investors who rely more on interpersonal trust in their relationship with the entrepreneur, will engage to a lesser extent in such power-based, or positional-based, or rights-based, negotiations. In contrast, a stronger engagement by negotiating parties will result in more comprehensive (that is, less incomplete) contracts. Hence, we offer the following hypothesis:

Hypothesis 2: Positional negotiations will

Interpersonal trust as a contingency factor in the negotiation process

As articulated above, interpersonal trust is relevant in real-world settings with imperfect (asymmetric) information, and bounded rationality. In such settings, contracts can be renegotiated if the conditions changes, and do not have to be comprehensive from the outset. As we argued above, we expect interpersonal trust to affect rights-based negotiations, in turn affecting the incompleteness of the negotiated contract.

However, trust is not only expected to influence the extent of positional negotiations, but also the negotiation process and its outcomes. Indeed, as parties engage in positional negotiations, the extent to which such negotiations are reflected in contract design will be contingent on interpersonal trust. While rights-based bargaining will help in clarifying all covenants in a contract, the extent to which the venture capitalist will insist on having explicit and detailed covenants and thus a comprehensive contract design will be contingent on the extent to which the venture capitalist trusts the entrepreneur. This is because, as parties engage in positional negotiations under circumstances of high trust, the reciprocity element of trust (Lewicki and Brinsfield, 2011) signals to both trustor and trustee the high probability that both parties will behave in a way that is expected and benevolent, as such mitigating the need for more comprehensive contract covenants (Welter, 2012). Hence, we offer the following moderating hypothesis:

Hypothesis 3: Interpersonal trust will

Figure 1 graphically illustrates the hypothesized relationships.

The conceptual framework.

Research methodology

Data collection and analytical approach

Our analyses build upon survey data obtained from 59 venture capital-backed technology-based firms in Norway. The data was collected in March 2004 through a survey that was distributed by mail to the CEOs of 240 venture capital-backed companies, representing all portfolio companies of the members of the Norwegian Venture Capital Association at the time of the data collection. As such, our dataset contains 25% of the population. We contacted the CEO as this person is typically considered to possess the most comprehensive knowledge on the history, strategy and processes within the organization (Carter et al., 1994).

In order to test our hypotheses, we employed the PROCESS macro developed by Hayes (2013). It is a statistical tool that is now also integrated in the IBM SPSS Statistical software package which facilitates moderated and mediation analysis, and even more advanced moderated mediation analysis. The current study is a moderated mediation analysis. With bootstrapped confidence intervals, we also avoid the typical problems caused by non-normal sampling distributions of an indirect effect (Cole et al., 2008). We chose to apply 10,000 bootstraps due to the relatively small sample size. The bootstrap method resamples the data, and runs a simulation that identifies confidence intervals as a supplement to traditional statistical testing. As such, it is a viable analytical tool that complements the traditional statistical testing methods. In other words, it is an excellent tool in field research with relatively small sample sizes.

Measures

The dependent variable “Incompleteness of the contract” was measured by assessing the number of covenants that occurred in the investment contracts the CEO closed with the venture capitalist Measuring contract incompleteness is challenging, and we could have used the length of the contract (in number of words) as a relative proxy (Poppo and Zenger, 2002). Instead, we employed a more active proxy and offered the respondents fourteen items which commonly occur in investment contracts (based on the covenants from Busenitz et al. (1997) and Barney et al. (1994)), and asked the CEOs to respond to the following question: “To which extent are the following mechanisms significant in the contract between the management team and the venture capitalist?” Examples of the fourteen covenants listed in the questionnaire are anti-dilution clauses; the binding of key personnel, restrictions on management salaries, etc. In our questionnaire, the respondents had to indicate the presence and the deemed significance of these mechanisms on a 7-point Likert scale (from to a very little extent “1,” to a very large extent “7”). The aggregate of these scores form the proxy measure of the comprehensiveness (or, the completeness) of the contract, and the reversed score reflects the dependent variable “Incompleteness of the contract” As such, the higher the score, the fewer covenants, and the lower the score, the more covenants. Cronbach’s alpha of this scale is 0.839.

The independent variable. Trust can be measured and understood in multiple ways, as has been shown by Blomqvist (1997), and therefore, McEvily et al. (2003) recommend providing sufficient insights into how the trust construct in research is measured. In our study, the relationship between agency theory and stewardship theory (applied to vertical arrangements) is similar to the debates regarding contractual and relational governance (applied to lateral arrangements). For instance, Lee and Cavusgil (2006) depart from relational governance and the facilitating role of trust in these relationships as opposed to contractual governance. Relational-based governance highlights the role of mutual trust, and we therefore seek to capture not only the mutuality element of trust, but also the behavioral and process dimensions of trust Henceforth, we drew on measures from Heide and John (1992), later employed by Zhang et al. (2003), and related them to the venture capital setting. The relevant items employed for assessing interpersonal trust were: The business relationship to the venture capitalist is characterized by a high level of trust; The parties expect to be able to make adjustments in the ongoing relationship to cope with changing circumstances; The exchange of information occurs frequently and informally, not only on the basis of prior agreements. These three items were scored on a 7-point Likert scale where “1” represented a very low agreement with the statement and “7” represented a very high agreement. The scores were all summarized and averaged. Cronbach’s alpha is 0.708.

As a measure for positional negotiations, we employed the validated items from Erikson and Berg-Utby (2009). The employed items gravitate around the claiming of rights, and captures the concern for securing rights in a working relationship. It may also be regarded as a power mechanism. This variable was operationalized using the following three items: We used a lot of time working out details in the contract; the venture capital firm was very concerned about securing its own interests; the negotiation focused on rights to a large extent. A 7-point Likert scale was used, with “1” representing very low agreement with the statement and “7” representing very high agreement. Cronbach’s alpha of this construct is 0.667.

As control variables, we asked the CEO about the experience levels of the CEO, the stage of development the firm was in, and New Venture Team (NVT) size. We control for the experience of the CEO as such experience is central to the way in which CEOs negotiate agreements. Specifically, “CEO industry experience” represents the number of years the CEO has working experience in the same industry as the focal company and “CEO firm-specific experience” represents the number of years the CEO had been CEO of the focal company at the moment of completing the survey. We took the natural logarithm of these first two measures based on years of experience (in response to the linearity expectations of the regression method applied). Further, “CEO entrepreneurial experience” indicates whether or not the CEO had been active in any prior start-ups, and was dummy coded, taking the value of “1” in case the CEO had been active and “0” otherwise. Almost two-thirds of the CEOs had been active in other start-up firms. As to what the firm development stage was concerned, we used a dummy variable, taking the value of “1” in case the CEO indicated the firm was in a later stage of development and “0” otherwise. Most of the CEOs (86%) indicated that their firm was in the later firm development stage, in contrast to the more earlier development stage. Finally, we controlled for NVT size as the size of the NVT is likely to affect firm strategy and performance (Eisenhardt and Schoonhoven, 1990). The size then represents a proxy for the capabilities of the venturing team, and particularly its human and social capital (Ucbasaran et al., 2003).

Results

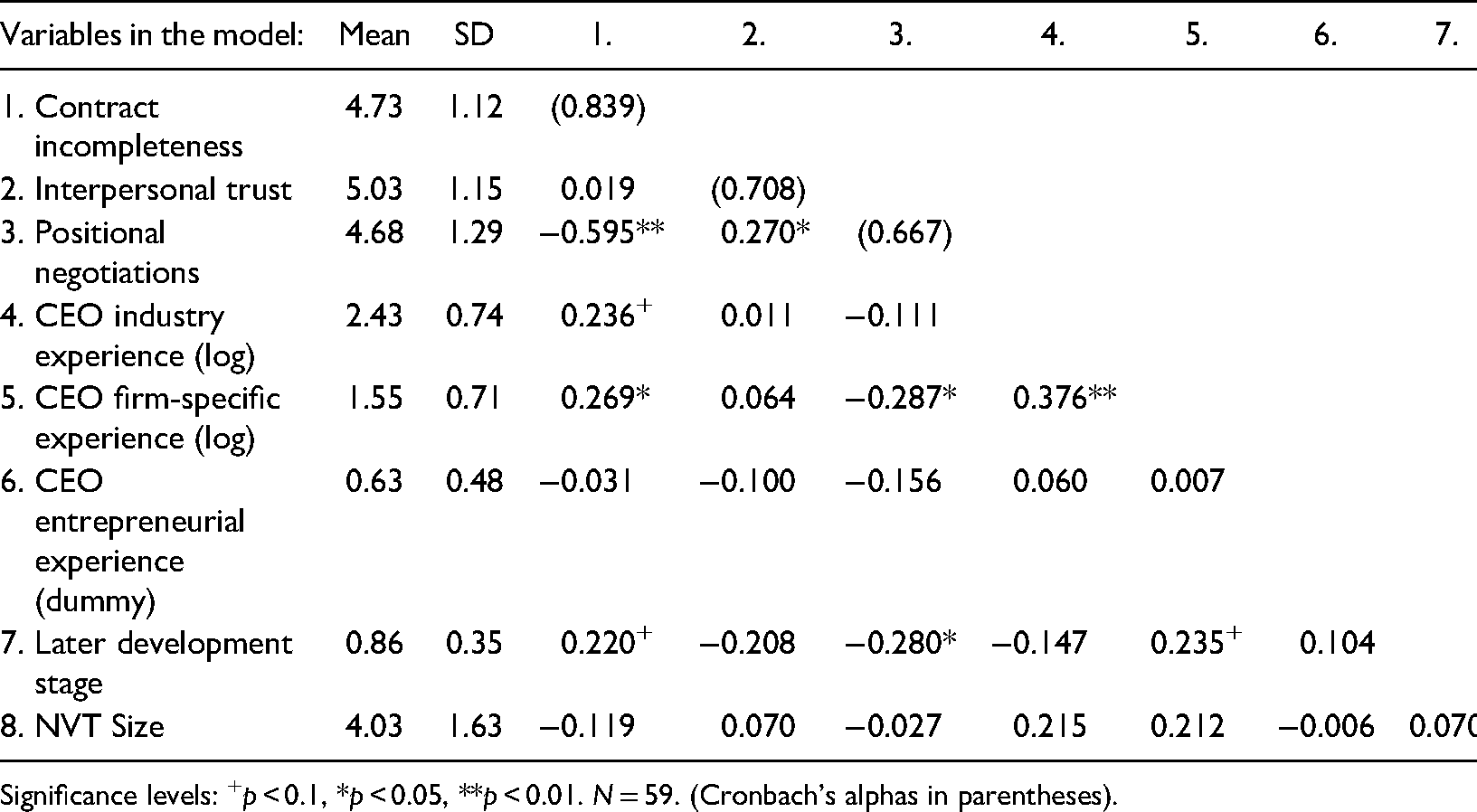

Table 1 presents the descriptive statistics for the variables used. It indicates that contract incompleteness is negatively correlated to positional negotiations. The table also shows that contract incompleteness is positively correlated to the CEO's firm-specific experience. Further, interpersonal trust correlates positively to positional negotiations, and the latter is again significantly negatively correlated to the CEO's firm-specific experience.

Descriptive statistics and correlations.

Significance levels: +p < 0.1, *p < 0.05, **p < 0.01. N = 59. (Cronbach’s alphas in parentheses).

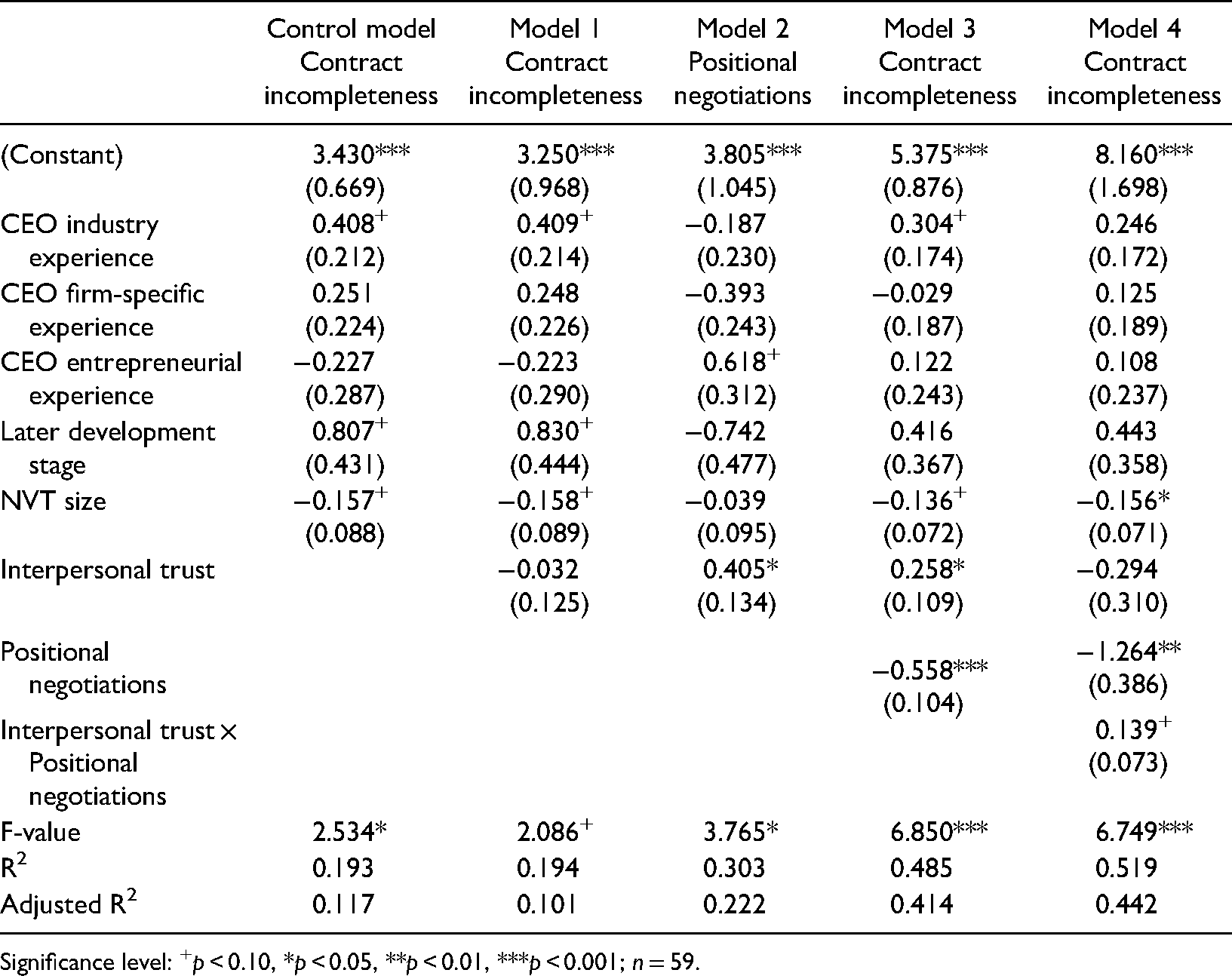

Table 2 shows the findings of our main analysis. The first column shows the control model for incomplete contracting. In Model 1, we added interpersonal trust to the regression equation, allowing us to assess the total relationship (i.e. uniting direct and indirect effects) between interpersonal trust and contract incompleteness, and thus to test hypothesis 1. Models 2 and 3 facilitate the assessment of whether or not mediation occurs, and thus allow for testing hypothesis 2. Finally, Model 4 introduces interpersonal trust as a moderator on the second leg of the mediation model, allowing us to assess the moderation effect introduced in hypothesis 3.

Regression results with unstandardized coefficients (standard errors in parentheses).

Significance level: +p < 0.10, *p < 0.05, **p < 0.01, ***p < 0.001; n = 59.

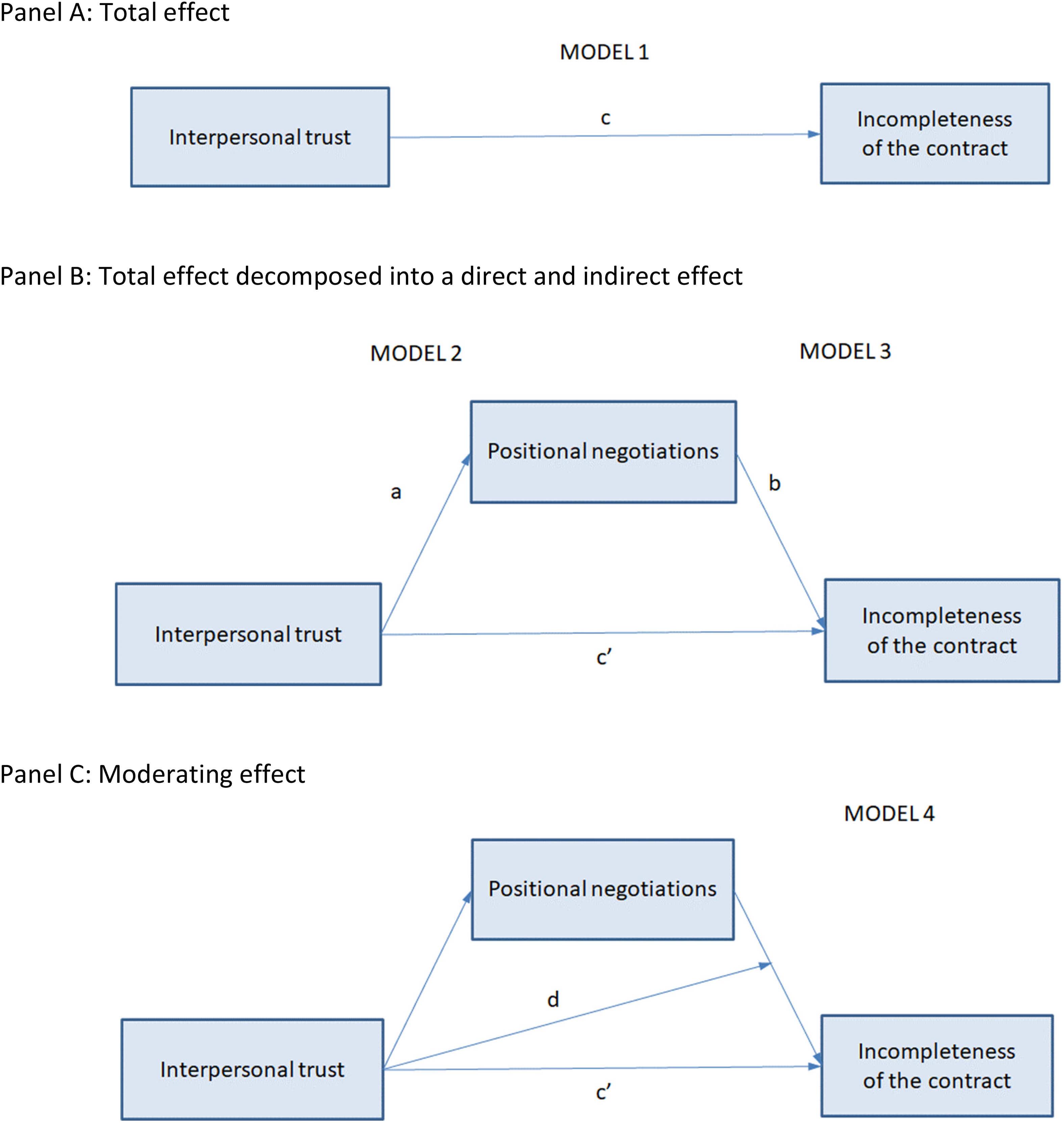

Figure 2 presents a figurative illustration of the path structure reported in Table 2, and of the conceptual model offered in Figure 1. Panel A in Figure 2 relates to the total effect, which is decomposed in Panel B into the direct and indirect effects (hypothesis 2), and Panel C captures the moderation hypothesis (hypothesis 3).

The reported path structure.

Model 1 shows that the total relationship between interpersonal trust and incomplete contracting is statistically insignificant (B = −0.032; p > 0.10; coefficient c). As such, we cannot accept hypothesis 1. Further, Models 2 and 3 (exhibited in Figure 2 (panel B), and shown in Table 2) provide partial support for hypothesis 2 regarding the mediation effect. Specifically, contrary to our expectations, we find interpersonal trust to positively relate to positional negotiations (B = 0.405; p < 0.01; coefficient “a”). At the same time, as expected, we find a negative relationship between positional negotiations and incomplete contracting in Model 3 (B = −0.558; p < 0.001; coefficient “b”). The Sobel test is statistically significant (Sobel z = −2.595 (p < 0.01)), indicating that mediation through positional negotiations occurs. The bootstrapped results also support this finding (as the bootstrapped 95% confidence interval does not contain zero (−0.4578; −0.0499)).

Interestingly, the direct effect of interpersonal trust is statistically significantly positive (B = 0.258; p < 0.05; coefficient “c’”). As such, our analyses provide a plausible explanation for the non-significant total effect of interpersonal trust on contract incompleteness: whereas the direct relationship between the two variables is statistically significant (and positive), this relationship gets neutralized by the indirect relationship through positional negotiations (as c = c’ + a*b). Put differently: while the direct effect indicates that higher levels of interpersonal trust are positively related to more incomplete contracts, this effect disappears when the total effect of interpersonal trust is considered as higher levels of interpersonal trust are also related to more engagement in positional negotiations, which is related to less incomplete contracts.

As to what the moderation hypothesis is concerned, we find that interpersonal trust also moderates the relationship between positional negotiations and the incompleteness of the contract (B = 0.139; p < 0.10; coefficient “d”). The interaction term is significant at the 0.10 level, which is the standard cut-off for interaction effects, balancing Type I and Type II errors (Aguinis et al., 2011). The Variance Inflation Factors were all below 2 indicating that multicollinearity is not a problem. The interaction effect indicates that, while the relationship between positional negotiations and contract incompleteness is negative, this is less the case as interpersonal trust increases. Put differently, when parties engage in positional negotiations, this leads to more complete contracts, but this is to a lesser extent the case when interpersonal trust increases, as trust seems to alleviate the concern to stipulate all details in a contract.

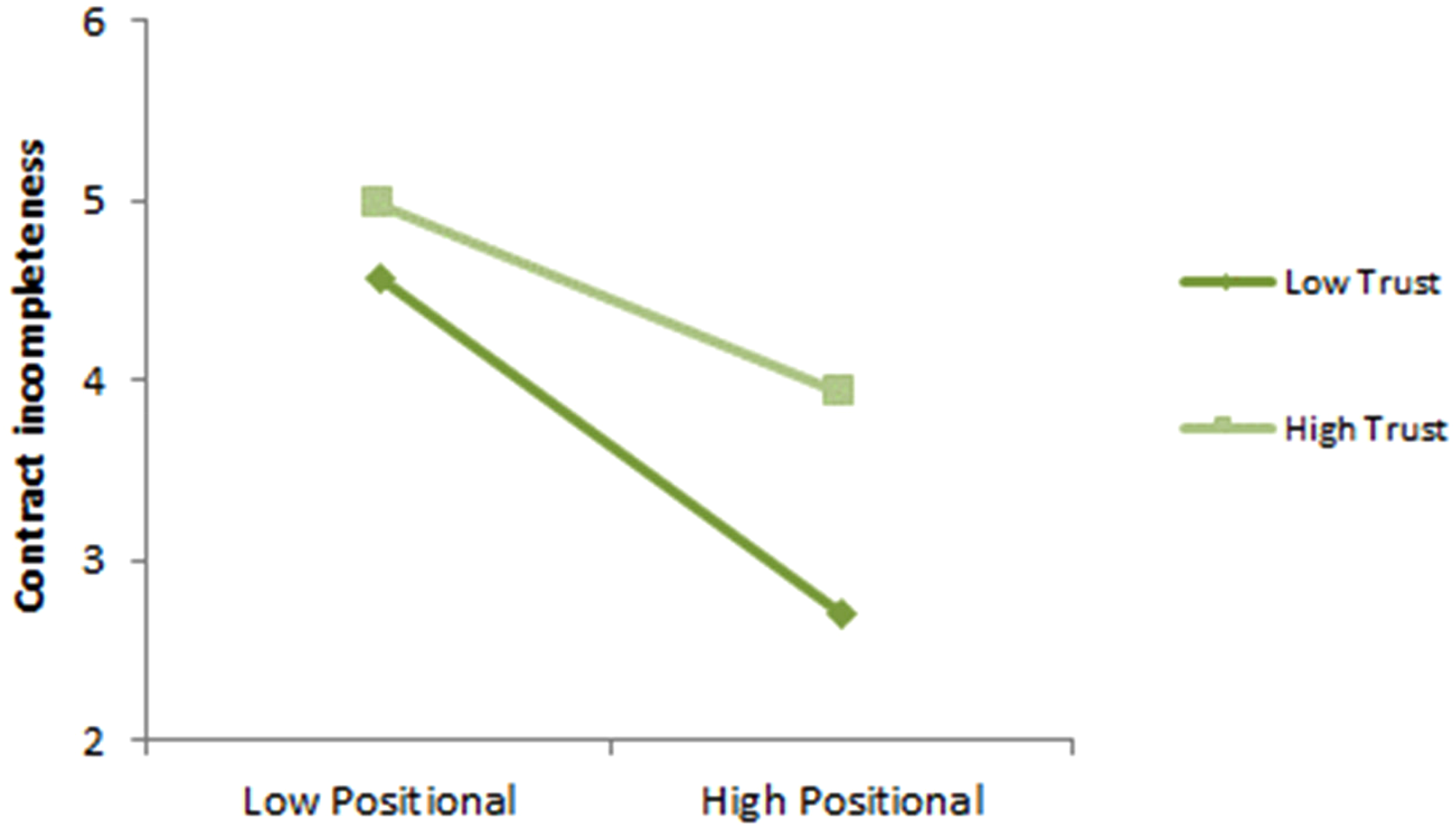

Figure 3 illustrates the moderation effect. It shows that high levels (mean + 1 s.d.) of interpersonal trust relate to more incomplete contracts, and that this is particularly the case when positional negotiations are low (mean – 1 s.d.).

Interaction effects of interpersonal trust with positional negotiations.

In contrast, low levels of interpersonal trust are associated with less incomplete contracts, and this is more pronounced when positional negotiations are high. As such, although we do not find a total effect between interpersonal trust and contract incompleteness, as initially expected, we do find that interpersonal trust plays an important role in contract designs, particularly through its direct, indirect, and moderating relationships.

Discussion with implications, limitations, and future research

Our findings show that interpersonal trust likely affects the negotiation process and its outcome. Particularly, interpersonal trust is directly positively related to contract incompleteness, and it relates indirectly to contract incompleteness through positional negotiations. Furthermore, interpersonal trust also positively moderates the relationship between positional negotiations and contract incompleteness. By consequence, these findings give more meaning to the label of “thick” trust, as this type of trust apparently works in various, and often contradictory, ways.

Furthermore, contrarily to our expectations, as to what the total relationship between interpersonal trust and contract incompleteness is concerned, we found that interpersonal trust-related positively, and not negatively, to the claiming of rights. This finding can be explained by the fact that interpersonal trust and the willingness to negotiate are related to each other in a positive manner, or that interpersonal trust and negotiations have the same underlying inclination to share or exchange information. This is because negotiations are a type of relational exchange, which requires a certain degree of trust, or faith in the negotiating parties, in order to be successful (Macneil, 1980; Zaheer and Venkatraman, 1995). Furthermore, trust facilitates the exchange of information in such negotiations (McEvily et al., 2003). By consequence, whereas higher levels of interpersonal trust lower the need for comprehensive contracts (i.e. the direct and the moderating effect), they also facilitate the exchange of information between parties, as such facilitating positional negotiations, leading to more complete contracts (i.e. the indirect effect). These findings corroborate stewardship theory that suggests that trust and incomplete contracting are related. Stewardship theory is however rather vague as to what the measurement of trust and the incompleteness of contracts is concerned. By putting concepts of stewardship theory into practice, we have taken a few steps in trying to unravel some of the theoretical underpinnings of stewardship theory.

Contribution to theory and practice

Our study contributes to the literature in several ways. In line with Myers’ (1977) famous pecking order on equity financing, Aghion and Bolton (1992) recommend a pecking order of governance structures (starting with entrepreneur control, then contingent control, and finally investor control). Our paper dealt with flexible contingent control. That is, the incomplete contracting approach requires and depends on trust whereas complete and more comprehensive contracting approaches do not, as all covenants are then specified to the full ex ante. As such, we contribute to an understanding that includes interpersonal trust, and we show the flexible nature of control when trust is involved. Second, our study contributes to the stewardship literature by providing insights into the origin of incomplete contracts, as such contributing to a better understanding of incomplete contracting (Kim and Mahoney, 2010; see also Parhankangas et al., 2005; Landström, 2006). As such, this study shows some of the managerial dynamics involved in growth, and the current study situates in between the theory of the early growth of the firm (Garnsey, 1998), which is an elaboration of Edith Penrose's (1959, 1995) resource-based and managerial theory of the growth of the firm and the latter mentioned theory itself. Whereas principal-agent theory is associated with complete contracting approaches, the more subjective components of both the theory of the early growth of the firm, and the theory of the growth of the firm may fruitfully be subsumed under the incomplete contracting approaches. Third, this study contributes to the venture capital and trust literatures by specifically focusing on the role of interpersonal trust in the negotiation process. Particularly, whereas Bottazzi et al. (2016) examined the role of generalized trust in investment decisions (mitigating some of the “external risks” associated with such investments), we departed from interpersonal trust (mitigating some of the “internal risks” associated with these types of investments). Fourth, the study also contributes to enlighten the negotiation literature which has understudied negotiation behavior in an entrepreneurial setting. The only exceptions are the studies by Artinger et al. (2015) who used an experimental research design to study how entrepreneurs negotiate, and Mason and Harrison (1996, 2002) who studied the interaction between informal private investors and entrepreneurs in the pre- and post-investment stage. Finally, the study shows that stewardship theory and incomplete contracting are related. Furthermore, by integrating the process, and more specifically, by shedding light on the role of negotiations in contract design, we also contribute to the negotiation literature.

Our study is particularly relevant to parties involved in the negotiation process. Specifically, it is relevant to entrepreneurs and venture capitalists, as it shows in which situations incomplete contracts are more likely to originate. When future outcomes not only are uncertain, but also unknowable, it may be a viable route to rely not only on the matters specified in the contract (or mentioned in the investor's contract templates), but also on the relational contract reflected by relational norms, such as interpersonal trust

Limitations and future research

Despite these contributions, our paper also has a number of weaknesses which lead to future research recommendations. First, this study suffers from the traditional weaknesses associated with correlational designs. Future research could further disentangle the negotiation process by using quantitative longitudinal designs, or by using qualitative, observational research designs. It could, for instance, study the different contracting stages, and assess the relevance of trust in each of them. Second, this paper intentionally focused on interpersonal trust, in contrast to prior studies which have exclusively studied generalized trust Future research could assess how interpersonal and generalized trust interact, and how these simultaneously affect contract designs. Alternatively, it could assess the effects of interpersonal trust under various contingencies. For instance, it could assess the impact of such trust in circumstances of low or high distributive, procedural, and interactional justice (Luo, 2007). Or, it could ask: what role does such trust play in the appropriate and fair distribution of control and decision rights over residual outcomes? What division principles are typically employed (the principle of need, the principle of equality (equal sharing), or the principle of equity)? In reality, a combination of these principles is normally employed, but with different weights attached to them for various reasons; what are these? Third, future studies may purposefully uncover the consequences of interpersonal trust and incomplete contracting. For instance, it could study the impact on firm governance effectiveness, or study the relevance of dispute resolution mechanisms such as voluntarily mediation, or arbitration, which may become more important than juridical procedures in the case of incomplete contract designs. Fourth, we only measured trust from one perspective, future studies should include measures from both sides - the dyad, but we acknowledge the challenge with such data collection. Finally, our study was conducted in a particular setting, namely Norway, which has a high generalized trust score on the Eurobarometer. While we do not have any reason to believe that our results would not hold in other high generalized trust settings, future research could purposefully assess the role of interpersonal trust in other countries and regions, in particular those with low generalized trust.

Despite these limitations, our study was unique in unraveling the relationship between relational norms such as interpersonal trust and contract design, through the negotiation process.

Conclusion

Foss and Klein (2016) made a call for an “entrepreneurial theory of contracting,” as the complete contracting theories, do not properly explain the entrepreneurial process. In this study, we departed from realistic exchange situations where parties have limited knowledge about the future, and where the uncertainty is high, and we looked into what role interpersonal trust plays in the negotiation of new ownership arrangements. As such, we contrasted agency approaches with stewardship approaches, and we saw that agency relationships were associated with more comprehensive contracts, whereas stewardship relationships are not. Moreover, we showed how contracts and trust likely complements each other (as is also the case with contractual and relational governance), and the role of negotiations in facilitating these complements. As such, our study is situated in and contributes to not only stewardship theory, but also to the emergence of what we may label as an entrepreneurial theory of contracting.

Footnotes

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship and/or publication of this article.