Abstract

Safeguarding specific investments and mitigation of potential opportunistic behaviours are among the most prominent functions of formal contracting in buyer–seller relationships. Extending the extant literature, the present study investigates the relationship between specific investments and the extent of formal contracting in cross-border and domestic relationships. Based on a sample of 156 buyer–seller relationships, the analysis shows that there is a positive association between specific investments and the extent of formal contracting. However, the emphasis on formal contracting is stronger in cross-border relationships than in the domestic ones. Interestingly, the association between specific investments and formal contracting becomes even stronger in cross-border relationships.

Keywords

Introduction

Buyer–supplier relationships are dynamic and susceptible to a range of pressures during the implementation of contractual arrangements (Rogers and Fells, 2017). To achieve collective goals of the relationship and minimize conflicts, exchange partners use contracts to specify responsibilities and roles for the parties involved in an exchange relationship. According to Schepker et al. (2014), contracts serve three main functions. Firstly, they serve as a safeguarding mechanism, whereby the focus is to mitigate potential opportunistic behaviours. Secondly, they provide a coordination mechanism through functions such as clarifying authority/responsibilities and providing mechanism for solving disputes. Thirdly, they stipulate an adaptation mechanism, that is, a clarification of the procedures to be followed if unforeseen contingencies arise. Considering these functions, contracts constitute a governance mechanism, which, according to Jap and Ganesan (2000: 230), is mainly a collection of “safeguards that firms put in place to govern interorganisational exchange”. Among other things, the safeguards are instilled to protect relationship-specific assets (Schepker et al., 2014).

Previous studies have addressed numerous aspects related to formal contracting and relationship-specific assets. To name a few, the extant literature on formal contracting addresses aspects such as the strategic role of contracting (Cummins, 2015), contract specificity and performance implications (Mooi and Ghosh, 2010), approach to good contractual agreements (Tomlinson and Lewicki, 2015), and the effect of detailed contracts on the level of interfirm conflicts (Mwesiumo et al., 2019). As for research on relationship-specific assets, previous studies have addressed aspects such as the contingent effects of asset specificity on offshore relationship performance (Wang et al., 2019), specific investment and supplier’s vulnerability to shocks experienced by customer’s business (Chen and Wang, 2017), and the use of asset-specific investments to increase customer dependence (Lin et al., 2017). Notably, previous studies have mostly explored formal contracting and specific investments separately. As such, an exploration of the nature of the relationship between formal contracting and specific investments warrants attention. This is because while investment in relationship-specific investments places the receiver in a position to act opportunistically and exploit the investor (Rokkan et al., 2003), detailed formal contracts can prevent exchange disruptions and misbehaviours (Zhang et al., 2018).

To contribute to the literature on both formal contracting and investment in specific investments, this paper empirically examines the impact of supplier’s specific investments on the level of formal contracting in its relationship with the buyer. By testing a theory-driven conceptual framework, the paper contributes in two main ways. Firstly, it provides additional insights regarding differences in the use of formal contracting between domestic and cross-border buyer–supplier relationships. Secondly, it addresses the impact of specific investments on formal contracting across domestic and cross-border relationships. Given that in practice many suppliers continue to invest in specific assets to meet the requirements of their major customers (Lin et al., 2017), the analysis of the impact of supplier’s specific investments on formal contracting in domestic and cross-border relationships is interesting. To the best of our knowledge, this question has so far received little scholarly attention.

The remainder of the paper is divided into six sections. First, we present a theoretical background of the study. Next, the conceptual framework of the study and its respective hypotheses are presented. The section on methods describes the sampling strategy, measurement of focal constructs and control variables, and validation of the constructs. Subsequently, we present the analysis and results. The discussion section places the results of the study into a wider context by providing theoretical and managerial implications. Finally, we outline the limitations of the study and provide potential avenues for future research.

Theoretical background

Transaction cost analysis (TCA) (Williamson, 1975, 1985) is among the prominent frames of reference used to explain various aspects related to interfirm exchanges. The framework is concerned with efficiency implications of adopting alternative mechanisms of coordinating transactions. The type of costs addressed by TCA are only associated with coordinating transactions and do not include production costs. These costs are distinguished into two types, ex ante and ex post costs. Ex ante costs are the costs incurred prior to embarking on a transaction, while ex post costs are costs incurred after embarking on a transaction. Examples of ex ante costs include costs involved in drafting, negotiating, and safeguarding exchange agreements. As for ex post costs, examples include costs of maladaptation, haggling costs incurred on bilateral efforts to correct misalignment, setup and running costs associated with the governance structures, and the boding costs of effecting secure commitments.

TCA predicts an appropriate/efficient governance mechanism for an interfirm exchange relationship based on three transaction characteristics – namely, the frequency of exchange, uncertainty, and asset specificity involved in the exchange. Although each of these characteristics has business implications that influence the amount of transaction costs incurred, asset specificity – physical or intangible assets dedicated to a particular exchange relationship – is regarded as the most imperative. As Williamson (1985: 56) notes, it is “the big locomotive to which transaction cost economics owes much of its predictive content”. This is understandable considering that relationship-specific assets create substantial switching costs to the firm that has made the investment (Wu et al., 2015). The high switching costs create dependence, which, in turn, may create an avenue for the other party to engage in opportunistic behaviour. Consequently, investment in specific assets requires appropriate safeguarding measures.

TCA makes two assumptions about economic actors – namely, bounded rationality and prevalence of opportunism. Regarding bounded rationality, TCA assumes that decision makers have constraints on their cognitive capabilities, which in turn limit their rationality (Williamson, 1985). As for opportunism, the theory assumes that whenever circumstances allow, decision makers may seek to serve theirself-interests even with guile, and that it is difficult to determine a priori who is trustworthy and who is not. Based on the three transaction characteristics and these two assumptions, the original transaction cost framework suggested two alternative governance mechanisms – market governance and hierarchy. According to Williamson (1985), market governance corresponds to classical contract law, meaning that the transactions are governed by formal rules. The transactions between the independent exchange partners can be described as “sharp in by clear agreement; sharp out by clear performance” (Macneil, 1974: 738). The identity of the exchange partners is irrelevant. Market-mediated exchange is characterized by high-powered incentives and the absence of administrative involvement (Tadelis and Williamson, 2012), where each party performs autonomous adaptation during the execution of the contract in order to maximize individual profits. Hierarchy is the organization of transactions through a unified authority, which involves the use of mechanisms such as rules and procedures, involving exercise of control and power. As such the party that has the legitimacy to make decisions is entitled to apply the authority (Caniëls et al., 2012). As such, rather than applying incentives, vertical integration is characterized by proactive/unilateral planning, ex-ante/explicit mechanisms for change, measurements of output and behaviour, and legitimate authority.

Appropriateness of a particular governance mechanism is assessed in terms of its efficacy to mitigate problems associated with interfirm exchanges. Being characterized by discreteness of transactions and ruled by market forces, pure market governance would seem quite effective in alleviating problems in buyer–supplier relationships. This is because no bond is formed between exchange partners and their interaction ends when a transaction is closed. The only problem is that market governance can be quite costly or even impossible to implement when it comes to transactions involving complex products and high uncertainties. When uncertainty and complexity characterize transactions, pure market governance is likely to cause inefficiencies. On the other hand, while pure hierarchy eliminates the risk of opportunistic behaviour from an exchange partner, it can be difficult to attain due to the high administrative costs involved.

One of the criticisms the original transaction cost framework faced was its failure to account for the social structures within which inter-firm transactions are embedded. That is, rather than being dichotomous – market-based or internally organized – coordination of transactions can be relational-based. Over time, there has been widespread consensus that formal and relational-based governance mechanisms complement each other. This is exemplified in an extensive meta-analysis by Cao and Lumineau (2015), which established that “contracts, trust, and relational norms jointly improve satisfaction and relationship performance and jointly reduce opportunism”. Besides complementarity of the governance mechanisms, it is also important to recognize that governance mechanisms are dynamic structures rather than static. That is, governance mechanisms deployed in inter-organizational relationships tend to evolve over time. Thus, a relationship may start with a market governance mechanism and evolve into more dedicated modes of governance. Ness (2009) suggests that governance mechanisms evolve due to learning effects and other aspects inherent to the process itself.

Conceptual framework and hypotheses

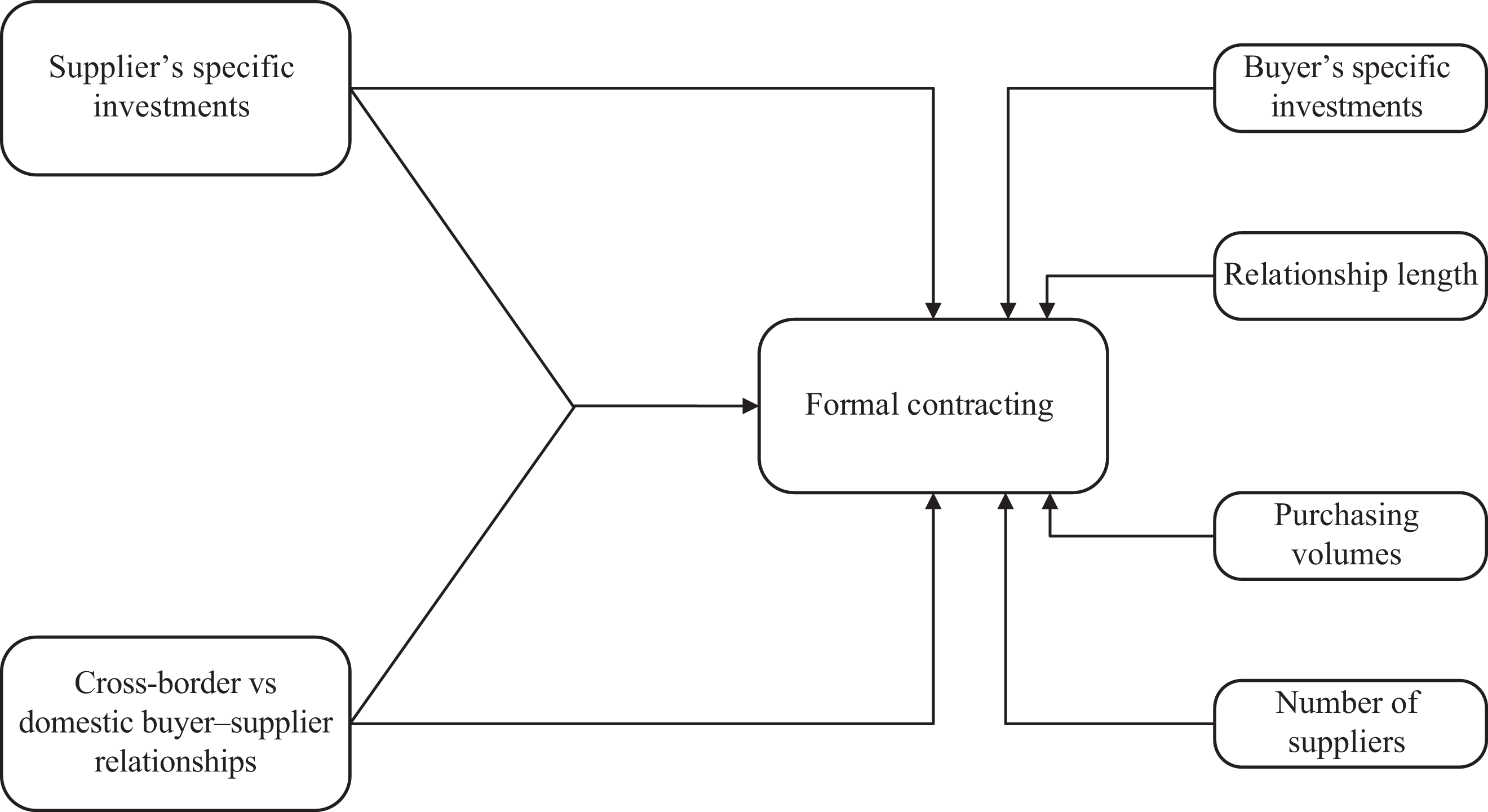

Building on TCA and relevant extant empirical work, this section provides arguments regarding the effect of specific investments and cross-border buyer–supplier relationships on the level of formal contracting. Figure 1 presents the conceptual framework and the corresponding hypotheses of the study.

Conceptual framework.

Supplier-specific investments and formal contracting

Specific investments, by their definition, have none or limited value outside of the relationship to which they are dedicated. Since they are tailored to a specific exchange partner, these investments become less valuable when deployed in alternative uses. Recurrent transactions between exchange partners are likely to involve specific investments in human and physical assets that have limited value beyond a particular relationship. This study focuses on supplier’s specific assets because in practice, suppliers tend to make much more specific investments to meet the demands of their suppliers, especially in cross-border relationships (Jean et al., 2010). For instance, a supplier of components must learn about the product-specific technical and quality assessment procedures, but also physical investments such as tailoring of production equipment and/or logistics needed to deliver the customized product. Indeed, buyers often tend to require their foreign suppliers to invest in relationship-specific assets (Kang et al., 2009). Investment in relationship-specific assets may have positive results such as increasing joint learning capacity between exchange partners (Lin et al., 2017) and making it possible for small firms to co-create value with large partners (Pérez and Cambra-Fierro, 2015). Nevertheless, when such investments are asymmetrical – that is, only one of the partners makes specific investments, which is often the case – they may create a lock-in situation and raise the probability that the other party will behave opportunistically (Mesquita and Brush, 2008). Besides creating an avenue for opportunistic behaviours, Chen and Wang (2017) demonstrate that the presence of specific assets can make a supplier vulnerable to large negative shocks experienced by its customer. Thus, as noted in the preceding section, specific investments should be protected by appropriate safeguarding measures.

One of the methods that can be used to safeguard specific investments is to write a formal contract and elaborate it as comprehensively as possible. In such case, the exchange partners would consider in advance all imaginable events and the appropriate responses. Writing detailed contracts allows exchange partners to explicitly stipulate roles and responsibilities to be performed, define outcomes to be delivered, and state adaptive processes for handling unforeseeable events (Kashyap et al., 2012). Furthermore, detailed contracts can include comprehensive specification of the tasks to be completed and contingency planning clauses – that is, parts of a contract designed to provide an adaptation mechanism within the contract. These may include clauses that protect relationship-specific investments. By imposing explicit and legally enforceable contractual terms, contracts address problems associated with interfirm exchanges such as opportunism. This occurs through the creation of a shared set of rules, responsibilities, procedures, and expectations between exchange partners. In some cases, contracts can also serve as “prenuptial agreements”, with the primary goal of enabling smooth dissolution of the relationship (Petersen and Østergaard, 2018). While contracts are often viewed as a means for addressing exchange problems (Mwesiumo et al., 2019), it is important to note that contracts can also be used for strategic purposes, serving as a vehicle for creating competitive advantage (Petersen and Østergaard, 2018). In their recent analysis, Hurmerinta-Haanpää and Viding (2019) argue that in addition to safeguarding, adaptation, and coordination, firms use contracts to codify deals, steer internal work, plan, promote, and steer collaboration. Although we recognize the multiple roles of contracts, our analysis focuses on the safeguarding role.

Against the above backdrop, two assertions are plausible. First, a supplier’s specific investments increase its vulnerability to potential opportunistic behaviour by their buyer, which, in turn, would raise the supplier’s concern and the need for safeguarding mechanisms. Second, since formal contracts facilitate the alignment of incentives, specification of roles, and closure of loopholes for noncompliant behaviour, the presence of relationship-specific investments and the need for safeguarding mechanisms will consequently increase an emphasis on detailed formal contracting. Thus, the following hypothesis is proposed:

H1: There is a positive association between specific investments made by the supplier and the level of formal contracting in its relationship with the buyer.

Domestic versus cross-border buyer–supplier relationships

According to Leonidou et al. (2014), the role of governance mechanisms has been one of the central directions in previous research on cross-border buyer–supplier relationships. Several studies have addressed the impact of different antecedents on cross-border buyer–supplier relationships (e.g. Leonidou et al., 2014; Samaha et al., 2014). It has been established that contextual factors may affect governance arrangements and that cross-border buyer–supplier relationships face different challenges compared to their domestic counterparts (e.g. Abdi and Aulakh; 2014; Bidault et al., 2018). Furthermore, the international business literature suggests that the level of information asymmetry is higher in cross-border inter-firm exchanges than it is in the domestic relationships (Gençtürk and Aulakh, 2007). Two arguments are provided to support this suggestion. Firstly, it is argued that domestic buyers will find it more difficult to interpret the behaviour and performance of foreign suppliers due to differences in language, way of communicating, business practices, norms, values, habits, and customs (Katsikeas et al., 2009). Secondly, environmental uncertainty is likely to create more problems in cross-border relationships due to partners’ lack of embeddedness into the institutional framework of each other’s country (Abdi and Aulakh, 2017).

Institutional theory, which describes how an organization adopts practices that are considered acceptable and legitimate within its organizational field, is widely used to understand business differences across countries (Jackson and Deeg, 2008). New institutionalism distinguishes between formal and informal institutions. Formal institutions are characterized by openly codified rules and constraints that are established and communicated through official channels (Helmke and Levitsky, 2004), while informal institutions are “humanly devised constraints that are not formally codified but embedded in the shared norms, values and beliefs of a society” (Estrin et al., 2009: 1175). Thus, informal institutions may include culture, routines, and decision-making processes. Nevertheless, formal and informal institutions are intertwined, and therefore examining the impact of institutions requires consideration of their interplay. For instance, the use of a contract may promote the evolution of common norms between the exchange partners, while informal institutions, such as culture, provide a foundation for shaping and developing formal institutions (Peng et al., 2008). Williamson (1991) treats the institutional environment as a set of parameters – property rights, contract law, reputation effects, and uncertainty – and investigates how changes in these parameters affect the comparative costs of governance. These parameters are also likely to have an impact on the contractual design (Luo, 2005). Thus, the extent to which formal contracting will be delineated depends on the operation of formal as well as informal institutions (Handley and Angst, 2015). For instance, some studies have found that to a large extent business transactions in emerging economies are based on relational exchanges built on mutual trust and cooperative norms (Li et al., 2010), mainly due to institutional voids (Zhou and Peng, 2010: 357).

Conceivably, exchange partners in domestic relationships are likely to be familiar with standards, rules, constraints, and expectations that form the basis for the performance evaluation of inter-firm transactions. Consequently, domestic buyer–supplier relationships are less likely to experience distorted communications and amplified misunderstandings, which in turn should decrease suspicion of unfair exchange or opportunistic behaviour. On the contrary, firms in cross-border buyer–supplier relationships are more likely to experience distorted communications and amplified misunderstandings due to psychic distance. Psychic distance are the perceived differences regarding legal and political environment, economic environment, business practices, language, and industry or market sector structure that may exist between someone’s home country and a foreign country (Terpstra and David, 1991). Accordingly, we argue that domestic relationships will tend to have less emphasis on formal contracting, while cross-border relationships will tend to emphasize a detailed specification of acceptable and agreeable terms and standards for performance evaluation. Formally, the following hypothesis is proposed:

H2: There is a stronger emphasis on formal contracting in cross-border buyer–supplier relationships than in the domestic ones.

Specific investments and domestic versus cross-border relationship

While most TCA-based empirical studies have analysed the main effects of specific investments and uncertainty on formal contracting, Williamson (1985: 60) suggests the potential likelihood of an interaction effect of these dimensions. A further argument put forward is that whenever substantial specific assets are involved, increased uncertainty makes it more imperative that the parties devise an approach to “work things out”. This is because, under such circumstances, there will be larger contractual gaps, and occasions for sequential adaptations will increase in number and importance parallel to the increased degree of uncertainty.

Carson et al. (2006) use the concept of ambiguity to describe the level of uncertainty in perceptions of the environmental state based on present and past experience. They note that even when firms are able to measure the exchange partner’s performance, they might still be unable to evaluate it with certainty due to ambiguity in their environment. This ambiguity consists of a lack of clear information, uncertainty about the importance of environmental variables as well as uncertainty about the best governance strategies and their potential effects. For instance, a buyer may be able to find out which sub-suppliers the supplier is using, but unable to evaluate with certainty whether other sub-suppliers should be used or not. Such ambiguity increases the opportunity for the supplier to behave opportunistically without the buyer’s knowledge of the behaviour.

Uncertainties can be distinguished into aleatory and epistemic uncertainties (Quigley et al., 2018). Aleatory uncertainty refers to the inherent random variation in a system and, therefore, it is generally regarded as irreducible. Conversely, epistemic uncertainty is the extent of ignorance or incomplete information about the system or elements of the system. Thus, epistemic uncertainties can be reduced through collection of information. Typically, firms can differ in their perceptions of the same environment and the level of ambiguity is likely to be greater in cross-border relationships than in domestic ones. Thus, given the incidence of psychic distance involved in international business, the nature of uncertainty experienced by cross-border buyer–supplier relationships is mostly epistemic. This implies that the partners in a cross-border relationship need to expend much more effort in order to interpret and understand their partner’s behaviour.

To sum up, the preceding discussion suggests that firms are likely to be more knowledgeable about their domestic partners than they are about their overseas partners. The limited knowledgeability signifies epistemic uncertainty between cross-border exchange partners. Accordingly, we argue that the heightened epistemic uncertainty in cross-border relations will increase the perceived vulnerability of the specific investments made by the supplier, which, in turn, will increase the desire for protecting the investment. Thus, we propose the following hypothesis:

H3: The positive relationship between supplier-specific investments and formal contracting becomes even stronger in cross-border buyer–supplier relationships than in domestic ones.

Methods

Sampling strategy

The sampling frame for the survey was members of the Norwegian National Association of Purchasing and Logistics, and questionnaires were mailed to the census of the 684 purchasing professional members. Among these, 114 reported that they fell out of the scope of the study because their firm had gone out of business or were no longer engaged in manufacturing. Among the remaining informants, 180 (32%) responded to the questionnaire after two call-backs. Comparison of size was made between the responding firms and a sample of 160 non-responders. No significant difference between these two groups was detected. The extent and direction of non-response was estimated by comparing early responders (64%) with late responders (36%), using a cut-off period of three weeks (Armstrong and Overton, 1977). No significant differences between those two groups were detected with respect to the variables included in our conceptual framework. Our key informants’ perception of their involvement with the selected suppliers had an average rating of 6.1 on a seven-point Likert scale. In total, 45 firms reported about their focal relationship with an international supplier, while 111 reported about a focal domestic supplier. There was no significant difference across domestic and cross-border relationships with respect to the international involvement of the buying firms (export share and experience with international trade).

Measures

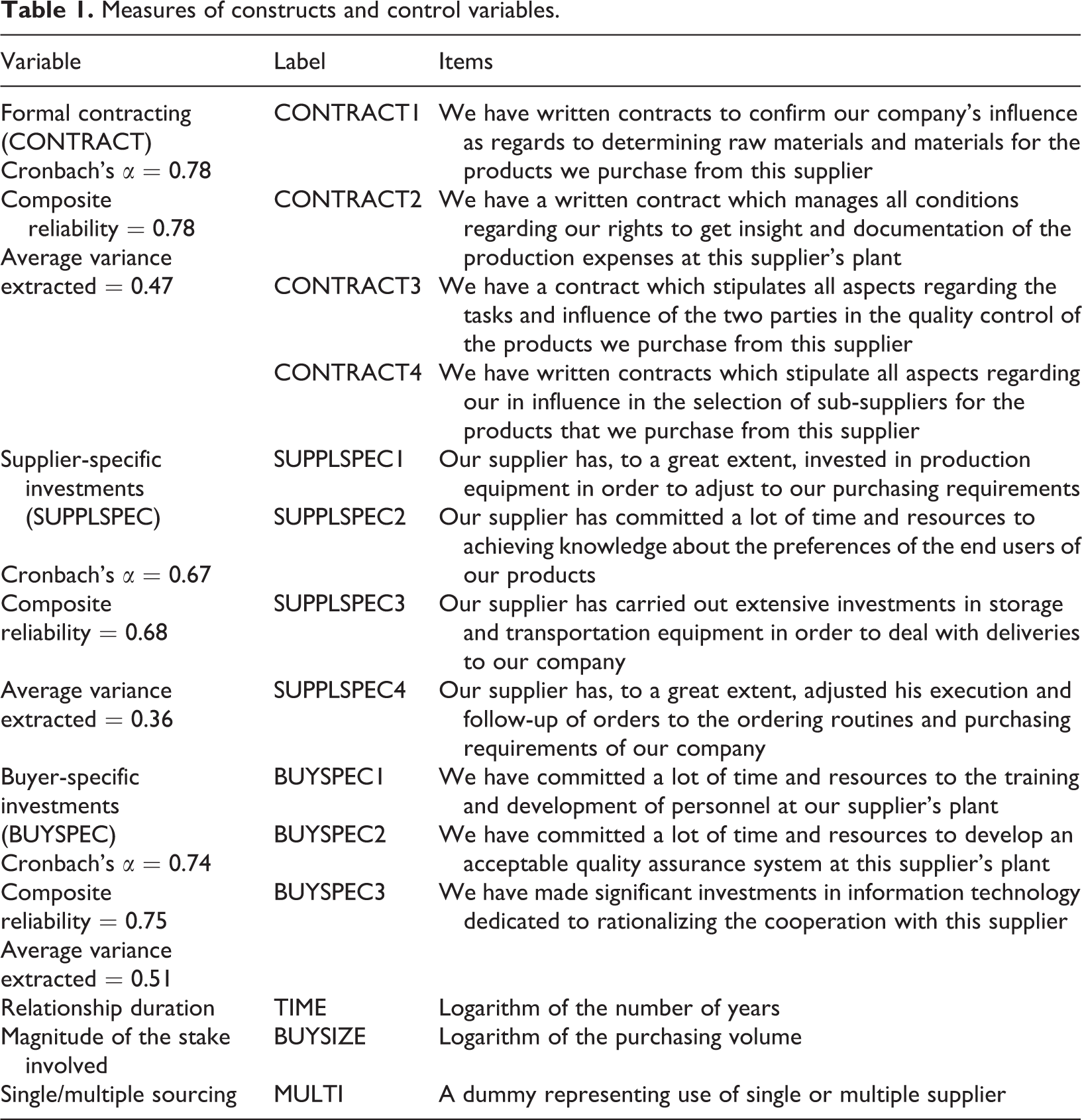

Except for domestic/cross-border relationship, the variables in the conceptual framework were measured by a seven-point Likert-type scale, with end points “inaccurate description” and “accurate” description. Table 1 reports the measures, fit indexes, and Cronbach’s alpha values of the focal constructs, followed by a description of how each construct is operationalized.

Measures of constructs and control variables.

Formal contracting is operationalized as the extent to which inter-firm flows of activities, resources, and information are regulated by way of fixed policies and standard procedures. Thus, formal contracting considered in this study is a legally enforceable voluntary agreement between two firms, achieved through negotiation (Mallor et al., 2013). As such, the formal contract protects both the buyer and the supplier against possible opportunism by the other party. Note that the use of the pronoun “we” in the items refers to the protection afforded to both the buyer and the supplier. Items for this construct were developed based on Heide and John (1990) and Noordewier et al. (1990), and the resulting construct is labelled “CONTRACT”. Supplier-specific investments are operationalized as investments dedicated by the supplier to the relationship. In line with Lin et al. (2017), we identified three categories of specific assets that were relevant for the context of the study – namely, physical assets, production facilities, and knowledge tailored to the relationship. The construct was measured by using a set of four items and the resulting construct is labelled “SUPPLSPEC”. A dummy variable was used to identify domestic buyer–supplier relationships (0) and cross-border relationships (1), and the resulting construct is labelled “INTER”.

Control variables

In order to increase robustness of the estimated model, four control variables were included – namely, buyer-specific investments, length of the relationship, purchasing volume, and the use of single versus multiple suppliers. Buyer-specific investments are operationalized as the investments and/or adoptions made by the buyer in physical assets and knowledge development tailored to the relationship. While most empirical studies mainly assume that the supplier makes specific investments on behalf of the buyer, specific investments made by the buyer may also increase the need for formal contracting (Rindfleisch and Heide, 1997). The three items used for measuring this construct (see Table 1) are derived from Heide and John (1990, 1992) and Anderson and Weitz (1992). The resulting construct is labelled “BUYSPEC”. Length of relationship was included as a proxy for the development of relational norms that may have developed over time (Ness, 2009). This reasoning is supported by Aulakh and Gençtürk (2008), who found that relationship duration is negatively related to formal contracting, signifying the development of relational norms. The time dimension allows our model to capture both formal and informal elements of governance. The length-of-relationship variable is measured as the logarithm of the number of years the buyer has worked with the supplier, and the resulting variable is labelled “TIME”. The purchasing volume was measured as the magnitude of the stake involved in the buyer–supplier relationship. This way, the purchasing volume serves as a proxy for the frequency of transaction. We considered it because TCA suggests that parties involved in an exchange with high stakes will face higher exposure to opportunism, which will make them insist on formal contracting. We computed the logarithm of purchasing volume and the resulting variable was labelled “BUYSIZE”. Finally, we included a dummy variable representing the use of single versus multiple suppliers because the extant literature suggests that the number of suppliers serving the buyer may have impact on the buyer’s need for and emphasis on formal contracting (Carson et al., 2006). The resulting variable is labelled “MULTI”.

Validation of constructs

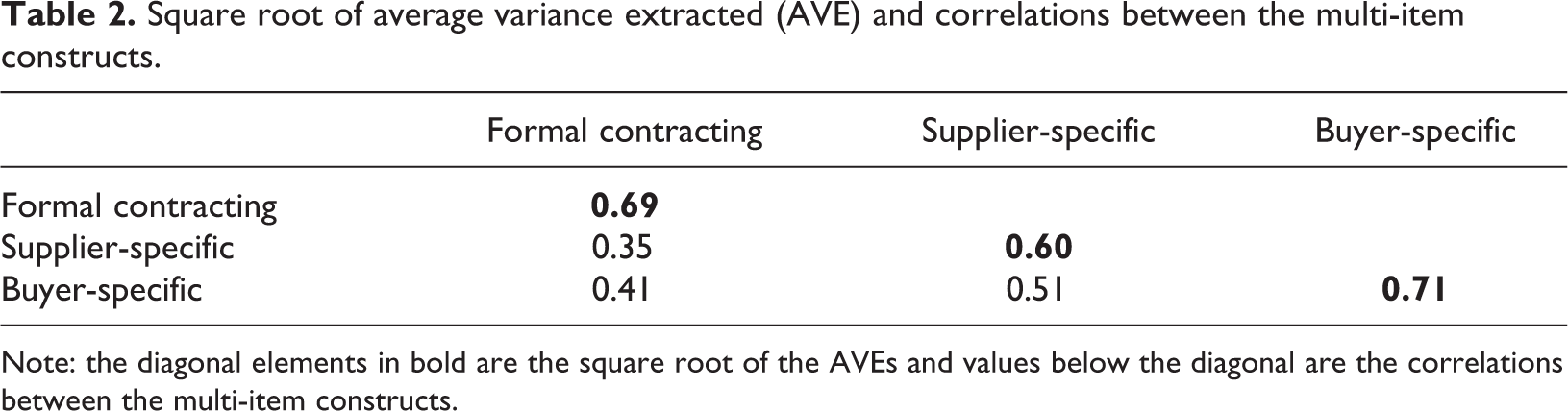

First, each of the three multi-item measures (formal contracting, supplier-specific investments, and buyer-specific investments) was analysed by inspecting the item-to-total correlations. All item-to-total correlation values were between 0.358 and 0.646, implying that all were above the 0.33 recommended cut-off point by Ho (2006). Confirmatory factor analysis (using IBM Amos22) revealed that no items had standardized residuals greater than the recommended value of 2.58 (Byrne, 1998). The final measurement model of these three concepts indicated adequate fit to the data: χ 2 = 42.99; df = 41; p = 0.39; goodness-of-fit index = 0.962; root mean square error of approximation = 0.016; Tucker–Lewis index = 0.995; and comparative fit index = 0.996. The values of the construct reliability (CR) in the measurement model were 0.78, 0.75, and 0.68, respectively. Concerning convergent validity, all the factor loadings were significant. Two of the factor loadings were, however, slightly below 0.5 and would, therefore, be candidates for potential elimination. We decided, however, to keep them in the model, since the CR also indicates convergent validity and the items have been extensively used in previous studies, suggesting their face validity. Furthermore, Hair et al. (2017) recommends that researchers can sometimes retain certain items in order to maintain the content validity of their respective latent variables. To test for discriminant validity, we used Fornell and Larcker’s (1981) criterion. The results reported in Table 2 indicate that there is no significant problem with discriminant validity because the square root of average variance extracted for each construct is greater than its highest correlation with any other construct.

Square root of average variance extracted (AVE) and correlations between the multi-item constructs.

Note: the diagonal elements in bold are the square root of the AVEs and values below the diagonal are the correlations between the multi-item constructs.

Reliability was tested by checking the item-to-total correlations (should exceed 0.50 by rule of thumb) and inter-item correlations (should exceed 0.30). We also evaluated the constructs for their internal consistency reliability by assessing the value of the Cronbach’s alpha (α). As indicated in Table 1, the values for Cronbach’s alpha for formal contracting and buyer-specific investments are above the generally accepted lower limit of 0.7 for Cronbach’s alpha (Nunnaly, 1978), while for supplier-specific investments the alpha is slightly below 0.7. However, Hair et al. (2010) note that alpha values as low as 0.60 are acceptable in exploratory research. To conclude, the overall results of the measurement model and validity and reliability assessments are satisfactory.

Analysis and results

Model estimation

To test the hypotheses, the study implemented ordinary least squares (OLS) regression analysis. The estimated OLS regression model consists of both focal and control variables as follows:

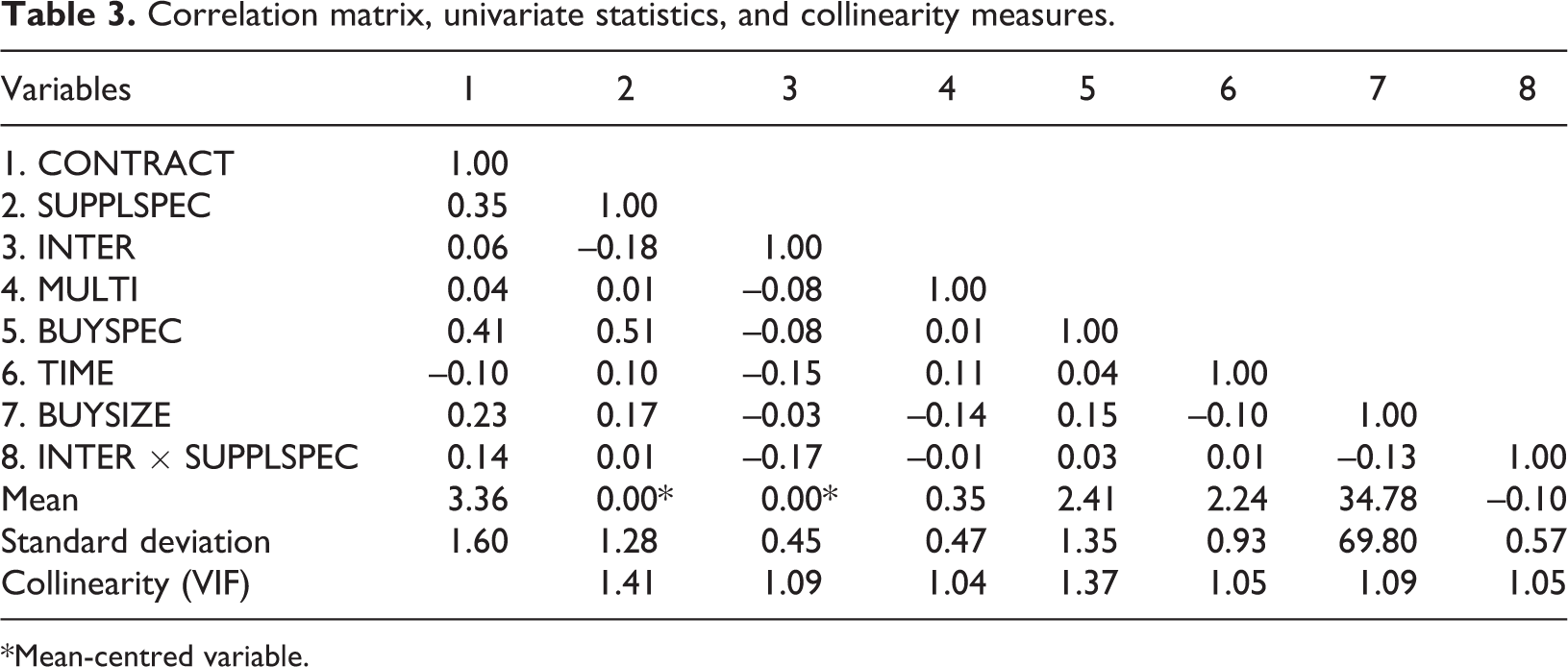

Table 3 presents the descriptive statistics, correlations, and collinearity measures. Following Cronbach (1987), the values of the variables entering the interaction term were mean-centred in order to avoid multicollinearity. The fit measures suggest that the estimated model provides an adequate description of the dataset (R 2 Adj = 0.24, F(7, 149) = 8.09, p < 0.001).

Correlation matrix, univariate statistics, and collinearity measures.

*Mean-centred variable.

Results

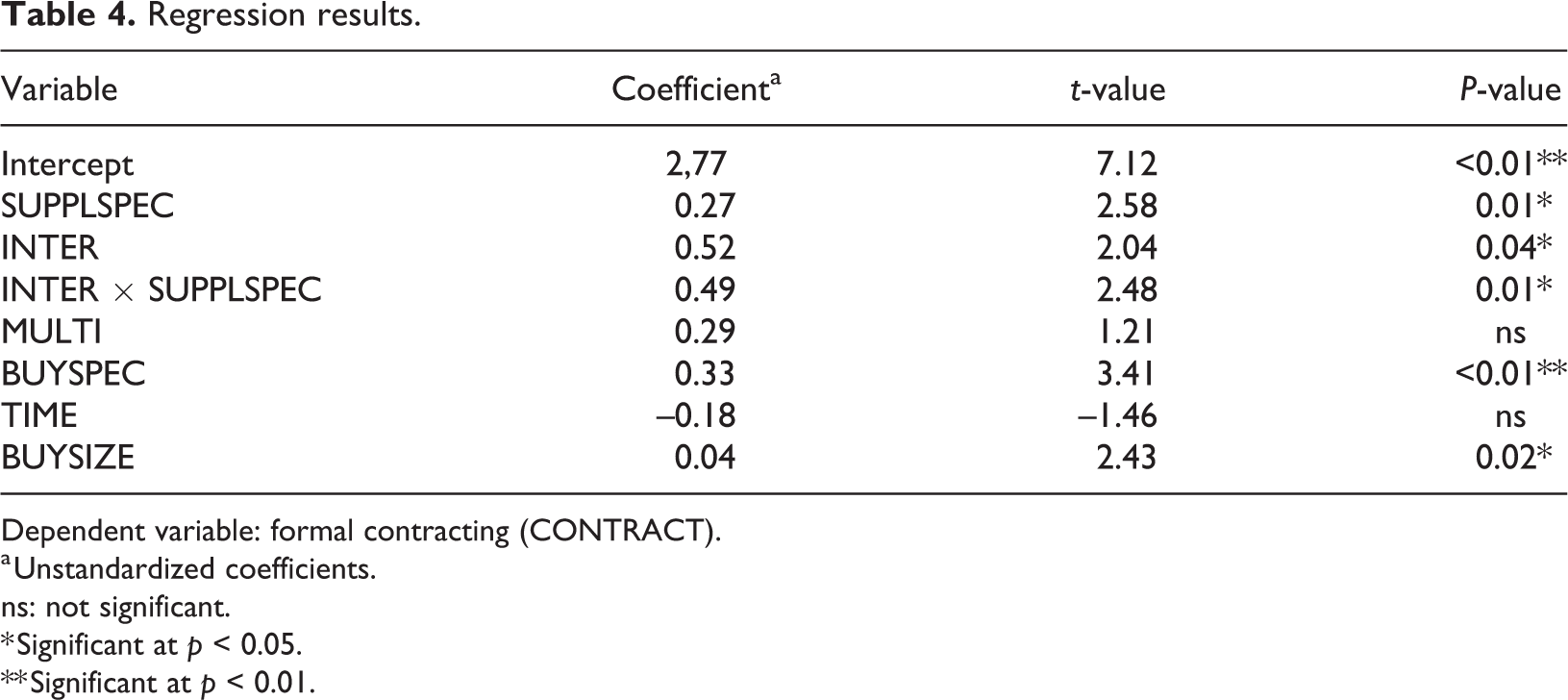

The results of the analysis, including values of coefficients, t-values, and the corresponding probability values, are presented in Table 4.

Regression results.

Dependent variable: formal contracting (CONTRACT).

a Unstandardized coefficients.

ns: not significant.

* Significant at p < 0.05.

** Significant at p < 0.01.

Hypothesis 1 suggested a positive relationship between supplier-specific investments and formal contracting. The results presented in Table 4 show that this hypothesis is supported (β 1 = 0.27; t = 2.58, p = 0.01). Likewise, Hypothesis 2 is supported, as we find that the extent of formal contracting is greater in international buyer–supplier relationships than in the domestic ones (β 2 = 0.52; t = 2.04, p =0.04). Hypothesis 3 proposed that the positive relationship between supplier-specific investments and formal contracting is stronger in cross-border buyer–supplier relationships than in domestic ones. First, we see that the interaction term is positive and significant (β 3 = 0.49; t = 2.48, p = 0.01). To ensure robustness of our analysis, we implemented moderated regression analysis to test this hypothesis. This method is generally regarded as a conservative method for identifying interaction effects, because the interaction terms are not tested for significance until the main effects of the independent variables are estimated in the regression equation. The interaction effect is significant only if it adds explanatory power to the regression model (Jaccard et al., 1990). Accordingly, we first compared the model that included the interaction term with the model that excluded it. The observed F-value was 6.15 (d.f. = 1, 149), indicating a significant interaction effect (p = 0.01). We then measured the strength of the interaction effect by assessing the difference in R 2 between the complete model and the model without the interaction term. This turned out to be 0.03, which means the interaction term accounts for 3% of the explained variance in formal contracting. Accordingly, hypothesis 3 is supported.

Contrary to our expectation, the control variable single versus multiple sourcing was not significant. However, we found a significant positive relationship between buyer-specific investment and formal contracting. As such, the need for formal contracting seems to be present independent of which exchange partner makes the specific investments. Furthermore, our results indicate a negative relationship between length of relationship and the extent of formal contracting; however, the magnitude of the effect is not significant. Finally, the results show that large purchasing volume, which was included as a proxy for the frequency of transaction and, thus, the stake involved, is significantly associated with increased emphasis on formal contracting. As argued earlier, high stakes make it more imperative for exchange partners to emphasize comprehensive contracts.

Discussion and implications

Notwithstanding the importance of relational governance that may promote flexibility, solidarity, and information exchange, the use of formal contracts is an important mechanism for governing exchange in marketing. As noted by Williamson (2003), formal contracting represents an important alternative to hierarchy in protecting specific investments and mitigating uncertainty.

While previous studies have considered several other factors based on both TCA and relational contracting theory to predict the use of contracts versus relational governance, this study focused on asset specificity. It investigated how the impact of asset specificity may vary in a domestic versus an international buyer-supplier context. According to Leonidou et al. (2006), international exchanges are subject to higher uncertainty, greater psychological distances, more unfavourable conditions, and much higher failure rates. As such, the dynamics of buyer–supplier relationships in international exchanges may not be congruent with those in domestic settings (Cavusgil et al., 2004; Johnston et al., 2012; Nes et al., 2007). Research within cross-border interfirm relationships suggests that exchange partners often find it difficult to evaluate accurately each other’s conduct and behaviour (e.g. Abdi and Aulakh, 2017). Under such circumstances, the exchange partners are likely to insist on detailing terms of trade, procedures, mutual obligations, and administrative and dispute-resolution processes, in order to avoid evaluation problems. The findings of this study provide additional insights into the stream of research that addresses issues related to contracting, particularly in cross-border interfirm exchanges. To the best of our knowledge, the key question addressed in the present study – whether the impact of specific investments on formal contracting varies between domestic and cross-border relationships – has received little attention in the extant literature. Given the relevance of this question, our findings provide both theoretical and managerial implications, as explained in the next two subsections.

Theoretical implications

Consistent with the logic of the TCA framework, the findings of the present study suggest that transaction-specific assets elevate the degree of formal contracting. This was found for specific investments made by both the supplier and the buyer. Thus, formal contracting appears as a safeguarding mechanism when an exchange relationship involves specific investments. Additionally, the level of detail in the specification of formal contracts is higher in cross-border relationships than it is in the domestic ones. Hence, our results suggest that relationships involving partners from different countries are more complex and subject to high levels of uncertainty. The most important theoretical contribution of our study is the finding that when specific investments are present the degree of formalization increases significantly more in international buyer–supplier relationships than in the domestic ones. This observation provides empirical evidence for the interaction effect of asset specificity and uncertainty. Although a meta-analysis by Geyskens et al. (2006) failed to establish empirical evidence for such interaction effect, it is important to note that the vast majority of the studies included in their analysis were based on domestic relationships. One possible explanation is that the information asymmetry is more pronounced in cross-border relationships than in domestic relationships, hence the heightened concern for specific investments and, consequently, increased formal contracting.

Managerial implications

In addition to the theoretical insights, the results of the present study provide insights that are relevant to the practice of management. As noted previously, a formal contract would typically specify terms and conditions governing the exchange relationship. In practice, however, contracts tend to be incomplete (Macaulay, 1963) – that is, often contracts fail to address comprehensively and in an enforceable manner, all aspects related to the relationship. Klein (1980) suggests two reasons that lead to incomplete contracts. First, it is difficult to identify and specify in advance appropriate responses to the various exogenous disturbances that exchange partners may face while doing business. Second, verifying the performance of an exchange partner on certain activities may be costly. As such, creating and enforcing detailed contracts is resource demanding. To reduce costs associated with formal contracting, managers of buyer–supplier relationships that involve specific investments may consider developing relational behaviours. These are supportive and constructive actions directed at promoting the development of a cooperative relationship between exchange partners (Lusch and Brown, 1996; Yilmaz et al., 2005). Heide and John (1992) identified three relational behaviours critical for interfirm relationships: information sharing, solidarity, and flexibility. Previous studies suggest that relational behaviours can sufficiently facilitate smooth attainment of the goals of exchange and, hence, reduce the need for heightened formal contracting (e.g. Bercovitz et al., 2006; Zhang et al., 2003).

An interesting question, however, is how exchange partners, especially in cross-border relationships, can develop relational behaviours, and hence reduce the need for increased formal contracting to protect specific investments? Considering the essence of relational behaviours, it is obvious that their incidence requires trust. Interestingly, a recent study by Bidault et al. (2018) found that the surveyed executives were less likely to rely on trust when dealing with partners that they perceived as being “not like them” with respect to important demographic and contextual variables. In light of this, we recommend that managers of cross-border interfirm exchanges that involve specific investments should make deliberate efforts to increase their knowledge of their exchange partner’s operating environment. We argue that the more each partner is knowledgeable of their counterpart’s operating environment, the shorter the psychic distance between them will be, which, in turn, can potentially promote trust, and, hence, the incidence of relational behaviours. For instance, firms that are knowledgeable of their exchange partner’s operating environment should be more likely to show solidarity and flexibility when the partner’s performance is below expectation due to circumstances beyond their control.

While some previous studies suggest that relationship length can significantly reduce the extent of formal contracting, the present study finds that the magnitude of the effect is not significant. This observation echoes findings by Gulati and Sytch (2008), which showed that translating joint history into a stock of trust is not straightforward; rather, it is contingent upon other factors. The results of a study by Paparoidamis et al. (2019), conducted across three European countries, suggest that performance in product quality and sales service quality is critical for building trust. Combining these insights with the findings of our study, we recommend that managers of cross-border buyer–supplier relationships should take deliberate initiatives to learn and acclimatize to the partner’s operating environment along with improvement of their performance in order to foster trust over time. They should do so rather than wait and hope that the psychic gap and trust will diminish and develop, respectively, as time passes. It is important to emphasize, however, that increasing the knowledge of exchanging a partner’s operating environment is just one of the factors that can contribute to developing trust. Examples of other factors that drive trust include perceived distributive fairness and partner similarity in the relationship (Robson et al., 2008) and international experience, management commitment, and resource commitment (Lu, 2009).

Limitations and future research

Despite the insights provided by this study, some limitations that provide opportunities for further research are worth noting. First, the present study did not take into account the role of the legal institution framework in the country in which the supplier is located. It is argued that relational contracting could be more important than formal contracting in some emerging countries, due to a lack of formal legal and regulatory frameworks (Zhou and Peng, 2010). This is because the state of legal institution framework in the supplier’s country could potentially have an impact on the formal contracting. Future studies may consider exploring the impact of specific investments on formal contracting in different legal environments. Secondly, the impact of specific investments on formal contracting could also be contingent on informal institutions, such as culture. For instance, Yang et al. (2014) suggest that legitimacy pressure has a positive impact on formal contracting, while Svendsen and Haugland (2011) found a weak negative association between export market ethnocentricity and formal contracting. Taken together, the findings of these two studies and those of the present study suggest that further research from different institutional environments is required in order to explain comprehensively the predictions of TCA regarding formal contracting. Among other things, such research will most likely require development of measures that capture relevant aspects of formal and informal institutions. Thirdly, the study relied on data collected on one side of the dyad – the buying firm – reported by one informant in each firm. Since some of the measures used in the study are mainly perceptual, future studies should consider collecting data from both sides of the dyad and, if possible, collect data from multiple informants. Fourthly, our findings are based on a cross-sectional study and as a result it is not possible to conclude the existence of causal links between focal variables. For instance, while we suggest that an increase in supplier-specific investment leads to an increased level of formal contracting, one could understandably argue that increased supplier-specific investment is a result of high-level formal contracting. As such, we suggest that future studies should consider a longitudinal design in order to capture are temporal precedence, which is one of the necessary conditions for making causal inference.

Footnotes

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.