Abstract

Driven by the need of an economic model that can explain the foreign direct investment (FDI)–export relationship, especially in post-liberalized context, we make a special inquiry on whether FDI has a significant export-promoting impact in India under a time-varying parameter model with vector autoregressive specification. The Johansen’s co-integration test suggests a significant and positive long-run co-movement between FDI and export. The vector error correction model (VECM) confirms a unidirectional long-run causality from export to FDI. However, the Granger causality test establishes a bi-directional causal relationship between these variables in short run. Further, the foreign trade (FT) is found to be a strongly exogenous variable as per the variance decomposition analysis. Again, the impulse response function analysis suggests that the responses generated from a positive shock of FT to FDI and vice versa are small and initially negative, afterward remain steadily positive at a constant level. The study finally recommends the policymakers to channelize the inward-FDI into tradable goods industries rather than only linking it to service sector growth to reap the long-term benefit. In this regard, China’s effort to channelize inward-FDI into manufacturing sectors and the resultant momentous success in export performance can be taken as a classic example for FDI-led foreign trade promotion.

Introduction

The relevance of inward-foreign direct investment (FDI) to foreign trade (FT) growth has been endorsed worldwide by the development economists of modern times. There is sufficient empirical support to the fact that FDI and export can form an economic model of empirical relationship, and the same may alter with changing context in economies. According to Harrison (1996), FDI can have the potential to stimulate exports through creating industrial linkage or spill-over effects, which further instigates high demand stimulus for domestic enterprises and results in export promotion. FDI is also believed to enhance export-oriented productivity that further improves export performance (Jana et al., 2017). There is a commonly perceived view that FDI augments domestic capital for export, enables technology transfer, and facilitates access to new and large foreign markets and training for the local workforce to enhance technical and managerial skills (Zhang, 2005). Notably, the FDI in both forms, that is, horizontal and vertical, are generally supposed to come with some distinct advantages to the economy.

However, India by its very tradition went with the swadeshi ideology that postulates national economic self-reliance (Wolf & Houseman, 1997). Consequently, Indian policymakers have for long relied on the import substitution industrialization (ISI) strategy. It is the remarkable economic success of the East Asian tigers, which stimulates the neoclassical economists of India and the world to subscribe to the doctrine of export-led growth model. Notably, the Indian policymakers have learnt a lesson on how these economies have utilized the necessary infrastructure and international linkage developed by the colonial government (Gulati, 1992) in executing their export-oriented industrialization strategy. Subsequently, the development economists and academicians worldwide, for example, Feder (1982), Krueger (1990), Trost and Bojnec (2016), have highly endorsed the export-led economic growth hypothesis.

Notably, until a couple of years back, India did not see the FDI and export as two complementary forces though referred by the economics scholars worldwide (Andersen & Hainaut, 1998; Pfaffermayar, 1996). According to Panagariya and Krishna (2019), if we make a comparison of export of India and China, we observe that Indian policymakers have not been able to attain the sophistication of its export to the same extent that China has. A lot of that is due to the poor FDI–export link. The Chinese economy, being a classic example of export-led growth, has managed to drive their exports through multinational firms in a big way. About 60 per cent of China’s export to the USA is undertaken by multinational firms. Therefore, Indian policymakers must learn the lesson and take the possibility to increase the sophistication of its exports by channelling inward-FDI into the right direction. Now, looking at the current scenario, we see the Indian policymakers to be much more fascinated about export-led economic growth through liberalized FT, the establishment of special economic zones (SEZs) and export processing zones (EPZs). Besides, they have been gradually dismantling economic restrictions and relaxing FT policies since the economic liberalization of 1991 to have a magnified effect on export and economic growth. At this point of time, a reassessment of FDI–export nexus, especially during the post-liberalized period, is worthwhile to carry out.

Considering the genuine lack of empirical evidence and an economic model, which can exhibit the actual channel of linkage between these two macroeconomic variables in the context of Indian liberalized period, we make a subsequent attempt after the study of Jana et al. (2020) to establish the empirical nexus between FDI and export for the period of 1991–1992 to 2019–2020 under a time-varying parameter model with vector autoregressive specification. The rest of the study is organized into five subsections. The second section discusses review of some related literature to find out research gaps; the third section discusses the data and methodology used in the study, that is, the research design; the fourth section analyses the data and presents the findings of the study; while the fifth section discusses the result of the study; and, finally, the sixth section summarizes the result and concludes the study.

Literature Review

Establishing the true impact of inward flow foreign capital and resources on the promotion of foreign trading performance of a nation has been a never-ending debate among the development economists and economic policymakers of emerging and developed economies worldwide. In many cases, the scholars are keenly interested to understand whether the economic policy liberalization could bring any significant changes in foreign trading scenario of the economies. Zhang and Song (2001) highlight a crucial fact that, after the implementation of the open-door policy by China, in the late 1970s, the country witnessed a dramatic upsurge in exports, especially in the manufacturing Industry and inward-FDI. The findings endorsed the common belief that increased levels of FDI positively affect provincial manufacturing export performance. Subsequently, Zhang (2005), in the context of the Chinese economy, shows how FDI plays a significant role in China’s export performance. According to the study, the effect of FDI is significantly stronger than that of domestic capital, and it is also momentous in labour-intensive industries in China.

Hsiao and Hsiao (2006) in the context of eight rapidly developing East and Southeast Asian economies (Hong Kong, Singapore, Malaysia, China, Korea, Taiwan, Philippines and Thailand) suggest that FDI has a unidirectional and direct influence on gross domestic product (GDP) and also an indirect effect through promotion of export.

The export-promoting effect of FDI is also highlighted by Jongwanich (2010) in context of eight Asian countries for a period of 1993–2008. Jevcak et al. (2010) in their study on 10 new European Union (EU) member countries refer to a modest contribution to productivity growth and export potential of FDI as a large volume of such FDIs went to the non-tradable sector. Haq (2013) also endorses the export-promoting impact of FDI in Pakistan. Several other studies like Kugler (2006), Samsu et al. (2009), Enimola (2011) and Bhatt (2013) also find a positive long-run relationship between FDI and FT in the form of export in different countries’ perspective. Mitic and Ivic (2016), emphasizing on European transition economies, suggest a significant level of correlation between FDI and export of goods in general, and a strong FDI and high-tech export nexus in particular.

Besides, there is empirical evidence that suggests the presence of a bidirectional relationship between FDI and export in various developed and developing economies. Andersen and Hainaut (1998) in the context of the USA, Japan and Germany; Pfaffermayar (1996) in context of Austrian markets; Liu et al. (2002) in context of China; Pacheco-Lopez (2005) in context of Mexico; and Keho (2015) on sub-Saharan African economies document a bidirectional causal link between the variables.

Among the limited empirical studies conducted in the context of India, we must refer to the study of Prasanna (2010), which shows inward-FDI to have a significant export-magnifying effect of India between 1991–1992 and 2006–2007. Similarly, Barua (2013) sees FDI in India as a complement to local developmental efforts that can boost export competitiveness, and it acts as a vehicle for accelerating the pace of export. On the contrary, in the contemporary studies by Dash and Sharma (2011), Mohanty and Sethi (2019) find a unidirectional causality between FDI and export, where it runs from the later to the former. Again, Sultan (2013) finds a similar result as observed by Dash and Sharma (2011) applying Johansen co-integration method and VECM. However, Chakraborty et al. (2016) refer to FDI as an insignificant factor to export promotion. Other studies like Sharma (2000) and Singh and Tandon (2015), etc., establish a non-significant statistical association between the variables. The study of Arslan et al. (2018) suggests significant bidirectional causality between the variables. One of the most recent studies by Jana et al. (2020) establishes a bidirectional but short-run causality between FDI and export in the context of India. However, the study does not make a special emphasis on liberalized FDI–export scenario, and therefore the reference drawn could not serve the specific research interest as addressed by this subsequent study. Thus, this empirical study is initiated to model the FDI–export nexus during the post-liberalization period of India. The study follows a robust and penetrating approach to ensure the addition of incremental value to the existing set of literature on this topic.

Data and Methodology

Data

The study uses quarterly data of FDI and FT from the year 1991–1992 to 2019–2020 to determine the relationship. After the liberalization policy adopted by the Government of India in 1991, the Indian economy has opened up considerably so as to allow even the foreign investors to invest their fund in India. This period has witnessed the most profound changes in the Indian economic scene. The forces of liberalization, globalization and privatization have altered the basic nature of the Indian economy. Foreign investments, both direct and portfolio, are now welcomed with open hands. Quantitative restrictions are history, while import tariffs are being reduced significantly. Opening up of the economy ensures more choice to the investors for taking their investment decision (Sahu, 2015). In this circumstance, the empirical investigation is being carried out, using quarterly data of FDI and FT from the year 1991–1992 to 2019–2020, to determine the relationship. In this study, the volume of export is used as a proxy of FT in India. The required data are collected and composed from various issues of Handbook of Statistics on the Indian Economy and the Reserve Bank of India Bulletin, published by the Reserve Bank of India and the data base of Economic and Political Weekly (EPW) Research Foundation.

Methodology

Before using the vector autoregression (VAR) estimation to determine the dynamic relationship between the volume of FT and the flow of FDI, the study applies two popular and commonly used tests, namely Augmented Dickey–Fuller (ADF) test and Phillips–Perron (PP) test to check the unit root property of the variables. After that, to determine the long-run co-integrating relationship between the variables, the study uses VAR-based approach of co-integration test suggested by Johansen (1988).

where Yt is a vector consisting of n variables, which are integrated of order one, and the subscript t indicates the time period. μ is an (n × 1) vector of constants, Ap is an (n × n) matrix of coefficient, where p is the maximum lag included in the model, and ut is an (n × 1) vector of error terms.

The nature of the relationship between FDI and FT in the short run is explored by considering the vector error correction mechanism. More precisely, where X and Y are integrated of order one or I(1), the VECM can be formulated as

where

Moreover, to validate the existence and nature of the causal relationship between the variables, the study uses Granger causality test. The error correction term of VECM represents the direction of long-run causality, whereas the short-run causality between the variables is examined through VEC Granger causality test or Block Exogeneity Wald test.

Although causality test is important to determine the causal relationship, the empirical inferences based on these tests do not establish the strength of the causality and the relationship between the variables over time (Sahu & Pandey, 2020). Hence, the variance decomposition test is used to investigate the degree of exogeneity of the variables used in the study. The result of variance decomposition shows how one variable explains a significant part of the variation of another variable over time. Again, the empirical inferences based on the Granger causality test help to qualify the flow of influences, but the estimates of the impulse response analysis provide a quantitative idea about the impacts for several periods in the future (Jana et al., 2020). The responses of FT to shock in the FDI and vice versa are examined through impulse response function analysis. It will help to capture the magnitude, direction and length of time that a variable is influenced by a shock of another variable in the system, holding all other variables are constant. Finally, the study conducts different diagnostic tests to check the existence of serial correlation, normality, heteroscedasticity, etc., which will help to judge the robustness as well as the stability of the estimated model.

Analysis and Findings of the Study

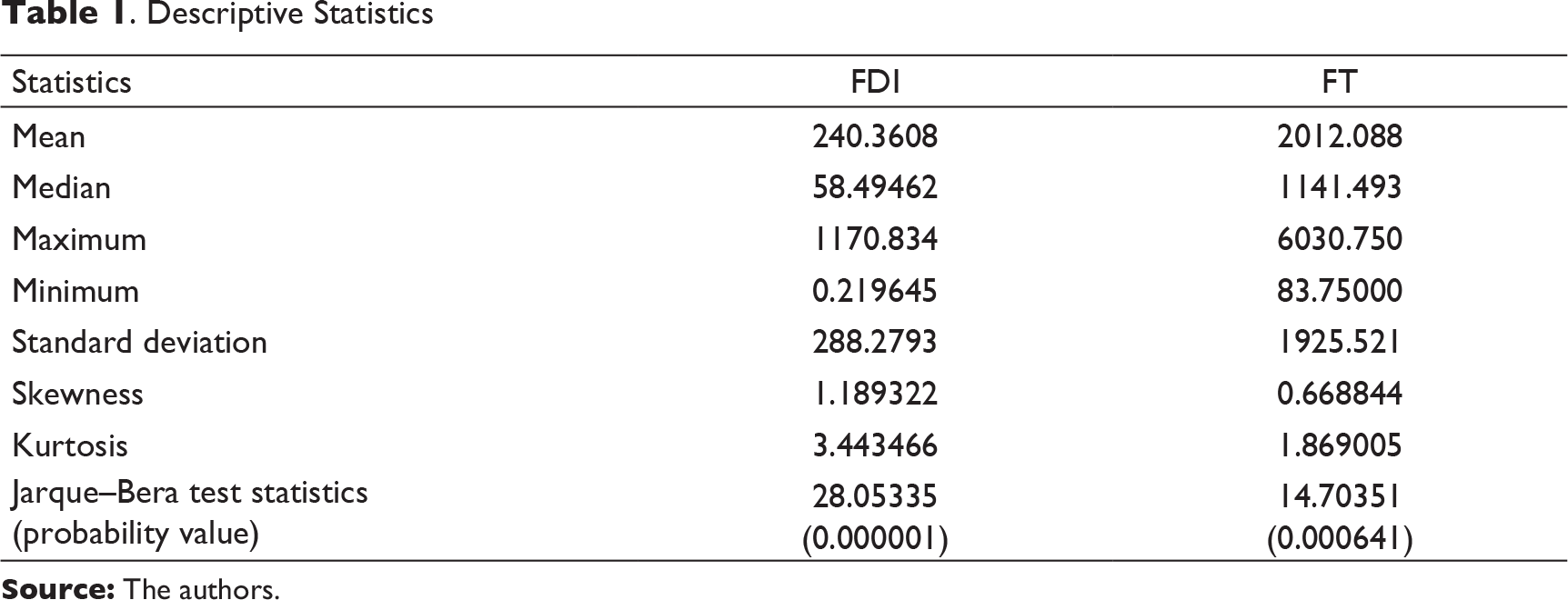

Descriptive Statistics

In respect of FT, the high difference between the maximum value and minimum value also signifies its instability during the study period. The high value of standard deviation in this regard also confirms the instability.

Findings from Long-run Analysis

As already stated, the long-run relationship between the variables is tested through the Johansen’s co-integration test. The Johansen co-integration test is based on three general steps. First, establish whether all variables in the model are integrated of the same order other than the stationary level, which can be examined by unit root tests. Second, ascertain the optimal lag length for the VAR model to verify that the estimated residuals are not serially correlated. Lastly, estimate the VAR model to shape the co-integration vectors, in order to investigate the co-integrating relationship.

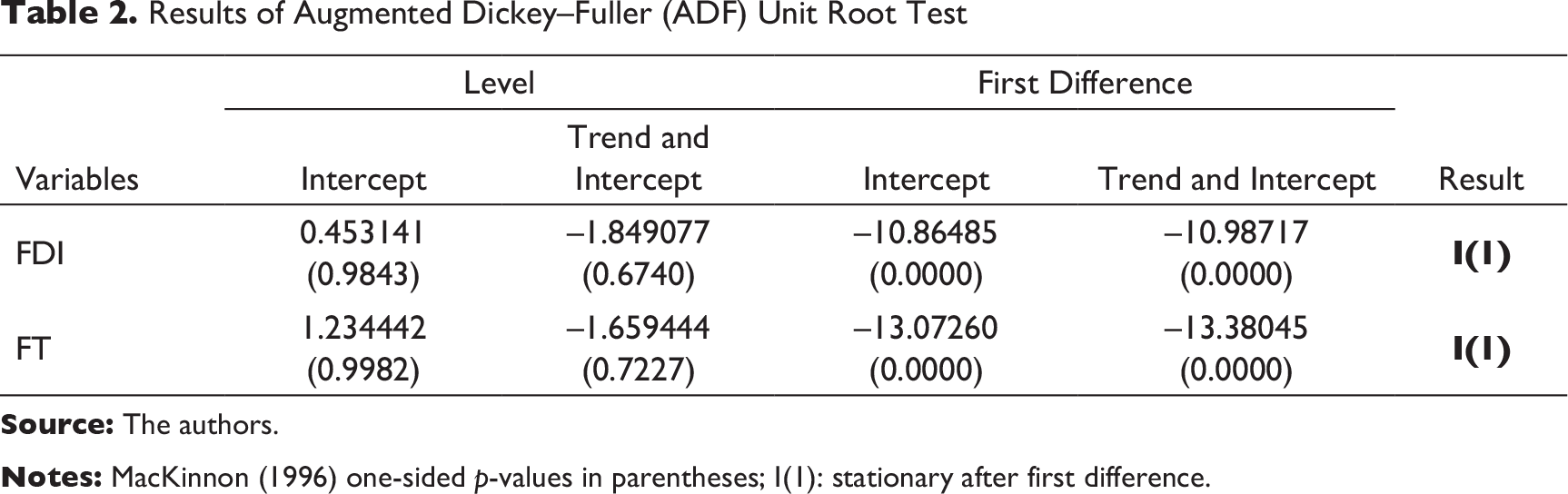

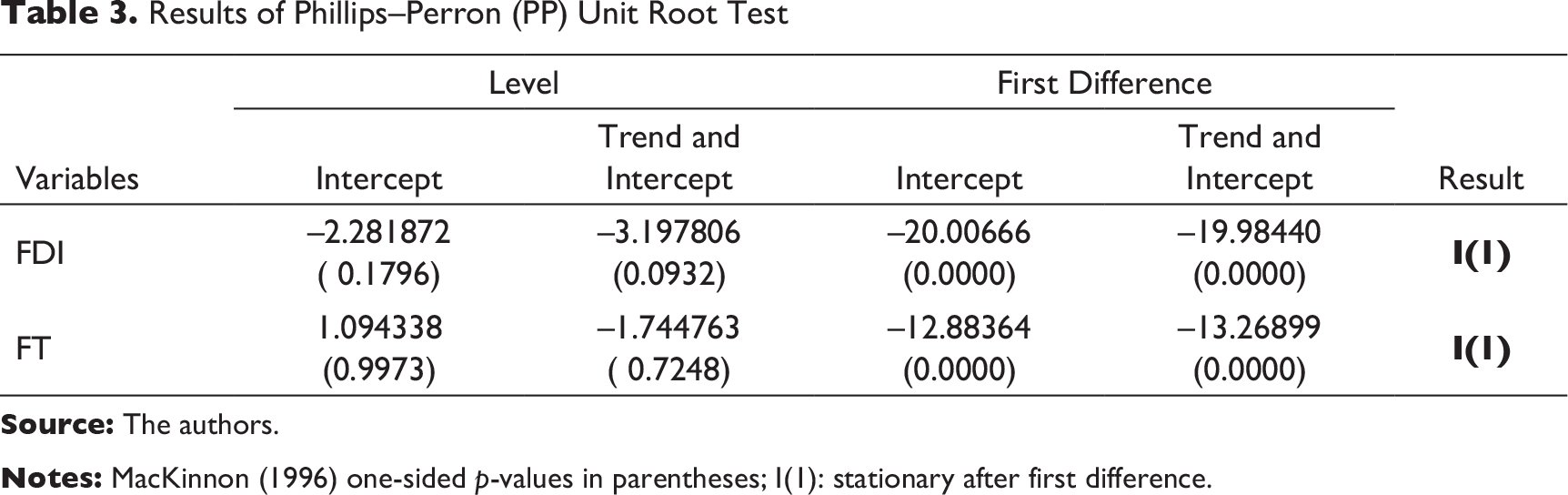

Results of Unit Root Test

As mention earlier, examining the unit root property is a prerequisite for drawing meaningful inferences in a time series analysis. It enhances the accuracy and reliability of the models formed. Therefore, it is essential to determine the unit root property and order of integration for both the variables included in the VAR.

In this respect, both unit root tests (ADF and PP) are used to testify the unit root property with intercept and time trend and intercept for both the variables in their levels, first difference values, etc., until they become stationery. The results of ADF and PP unit root test of FDI and FT at the level and first differences are reported in Tables 2 and 3.

Results of Augmented Dickey–Fuller (ADF) Unit Root Test

Results of Phillips–Perron (PP) Unit Root Test

Selection of Optimum Lag Length

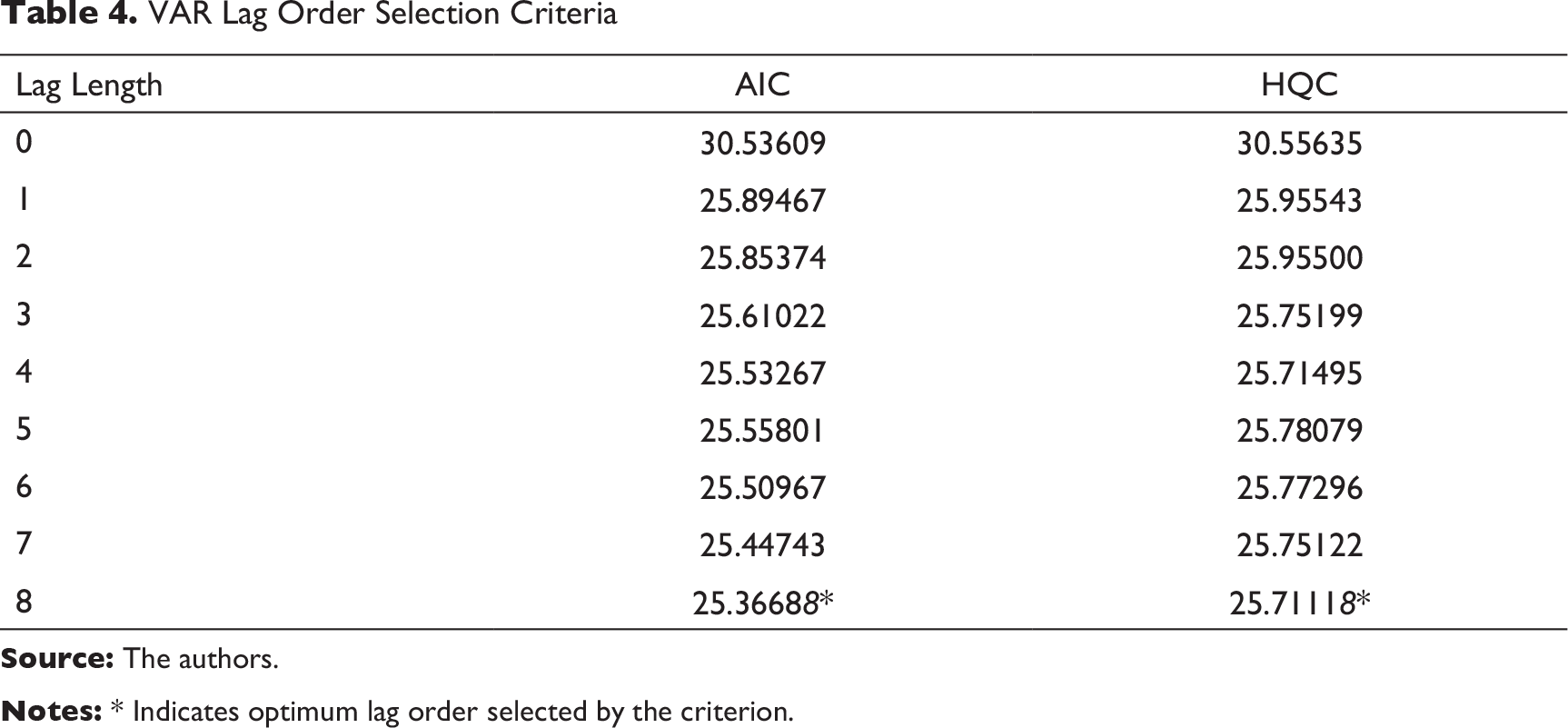

Before using the co-integration technique in line with Johansen, the study is conducted to determine the appropriate lag length, as VAR model is sensitive to the selection of appropriate lag length.

Table 4 reports the optimum lag length based on the two commonly prescribed criteria, namely Akaike information criteria (AIC) and Hannan–Quinn information criteria (HQC). The AIC and HQC criteria suggest 8 as optimum lag length for the VAR model.

Results of Johansen Co-integration Test

VAR Lag Order Selection Criteria

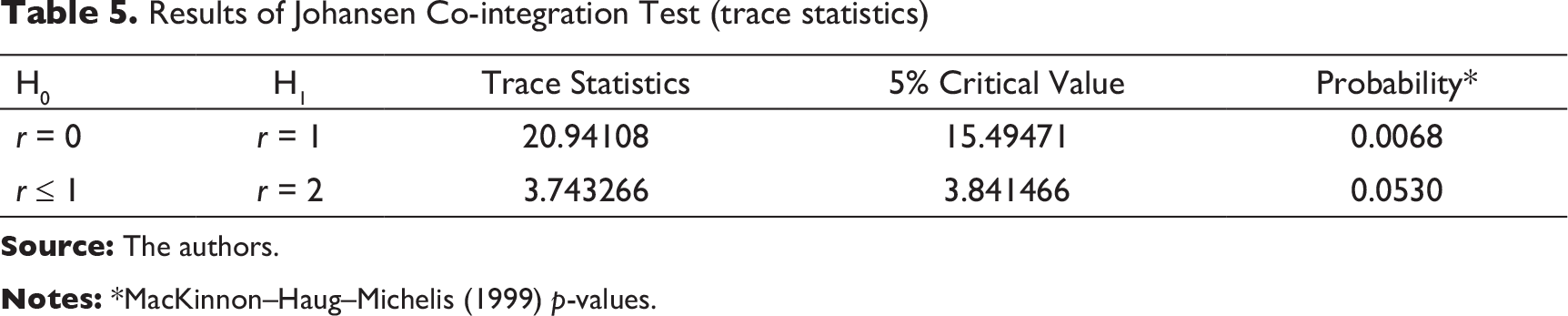

Results of Johansen Co-integration Test (trace statistics)

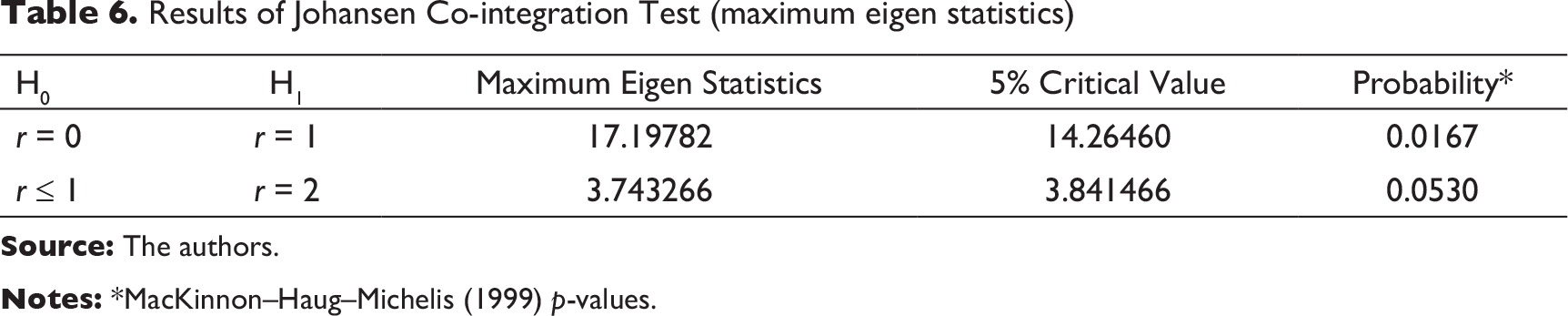

Results of Johansen Co-integration Test (maximum eigen statistics)

The results presented in Tables 5 and 6 report that the null hypothesis of no co-integration between the variables is rejected at the 5 per cent level of significance as the Mackinnon–Haug–Michelis critical values (15.49471 and 14.26460, respectively) are less than the observed value of trace statistic (20.94108) and maximum eigen statistic (17.19782), respectively, at 5 per cent level of significance. From the co-integration results, it is a clear that a long-term common stochastic trend exists between the variables with only a co-integrating vector. However, the Johansen’s co-integration test result concludes about the existence of co-movement between FDI and FT in the long run in post-liberalized India. Notably, the long-run co-integrating equation is formulated as:

On the basis of the above co-integrating equation, the study confirms that in long-run, there is a significant and positive long-run relationship between FDI and FT, that is, they move together in the same direction, as the t-value coupled with the coefficient in co-integrating equation is significant at the 5 per cent level of significance.

Findings from Short-run Analysis

As both the series, FDI and FT, are found to be co-integrated, the analysis proceeds to document the short-run dynamics between the concerned variables, employing the vector error correction mechanism.

Result of the Vector Error Correction Model

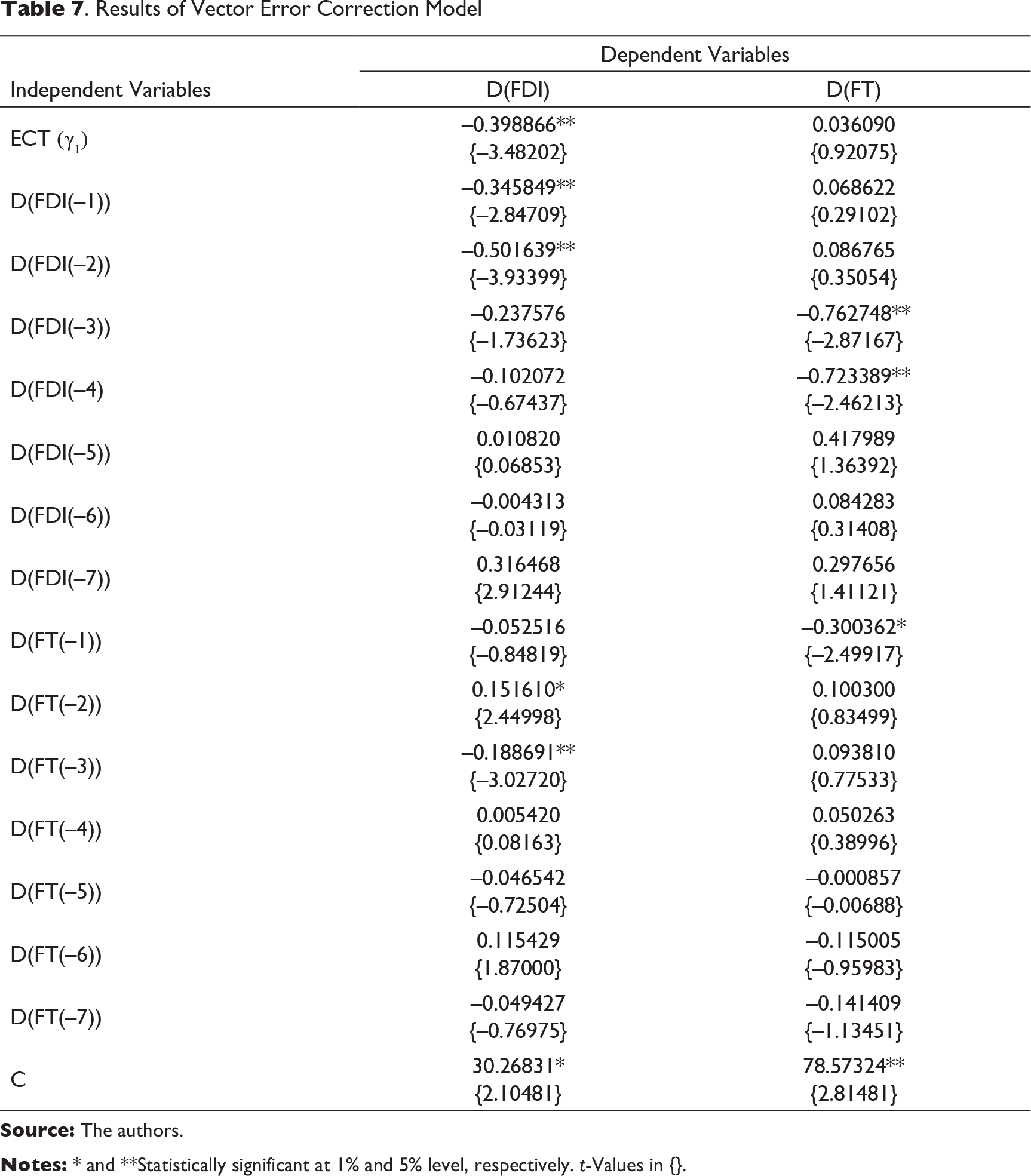

Results of Vector Error Correction Model

It indicates that in the very short run, the FDI has a significant and negative impact on the volume of FT. Considering FDI as a dependent variable, the VECM result evidences a striking relationship between the variables where t-value of second lag is significant with a positive sign, and in the very successive lag, it becomes significant with negative sign. So, in the short run, the FT has a mixed influence on the flow of FDI. The t-values of error correction term of the VECM indicate that the value of FDI adjusts the disturbances to converge towards long-run equilibrium significantly and in right direction at the 1 per cent level, but the values of FT do not respond significantly. The coefficients of error correction term –0.398866 is significant at the 1 per cent level. This coefficient evidences the speed of adjustment per quarter, that is, almost 40 per cent; at this rate, it corrects the disequilibrium of the previous period.

Results of Diagnostic Tests

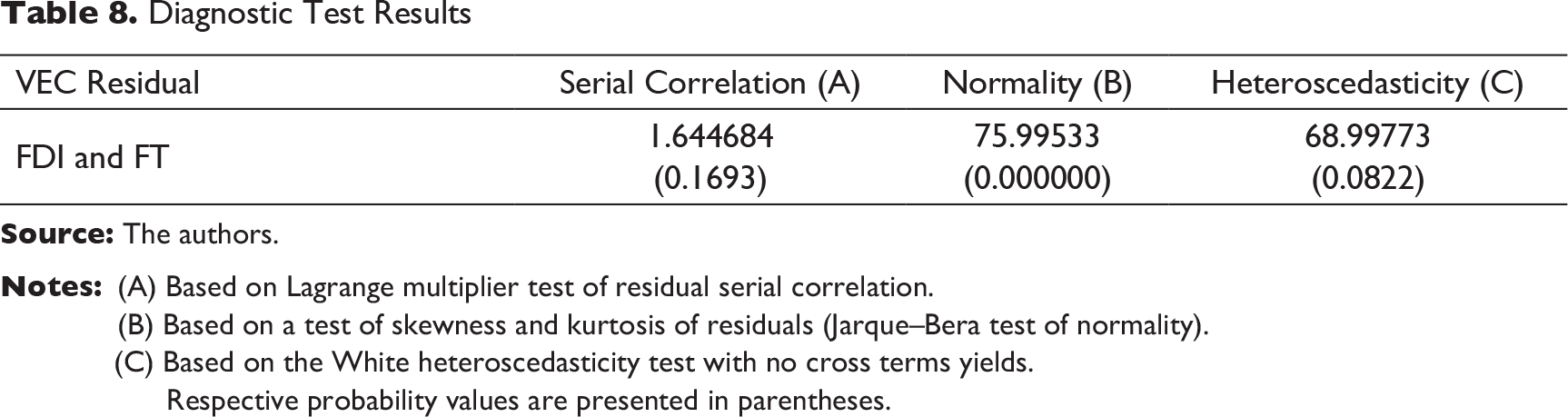

Diagnostic Test Results

(B)Based on a test of skewness and kurtosis of residuals (Jarque–Bera test of normality).

(C)Based on the White heteroscedasticity test with no cross terms yields.

Respective probability values are presented in parentheses.

Result of VEC Granger Causality/Block Exogeneity Wald Test

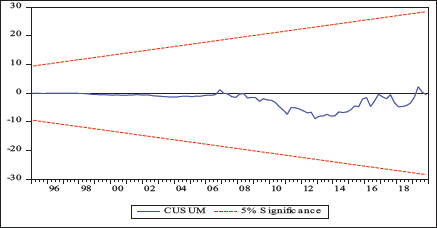

Further, the study estimates cumulative sum (CUSUM) of recursive residuals to testify the stability of the estimated coefficient of the VECM model. The results of the CUSUM test plots in Figure 1 suggest that at 5 per cent level of significance, the parameters of the model are stable during the study period. Therefore, this part of investigation ensures the acceptability of the model.

Findings from Causality Test

Since FDI and FT have common stochastic trend, the standard Granger test is mis-specified, and the error correction strategy suggested by Engle and Granger (1987) is applied to capture the long- and short-run causal relationship between the variables. The outcomes of the long-run and the short-run causality tests under VECM framework are documented separately under the following two headings:

Long-run Causality

The t-values associated with the coefficients of error correction terms of VECM presented in Table 7 indicate the existence of long-run unidirectional causality running from FT to FDI. It is justified by the coefficient of the error correction term –0.398866, which is statistically significant at 1 per cent level, considering FDI as a dependent variable. But the t-values connected with the coefficients of error correction term is insignificant, while FT is treated as dependent variable. So, this part of investigation confirms that any change in the value of FT causes change in the flow of FDI in long run, but reverse is not true.

Short-run Causality

The results of short-run causality test between FDI and FT based on VEC Granger causality test are reported in Table 9.

The probability values associated with the χ2 values confirm the short-run bidirectional causality between the variables, that is, in a short span, the flow of FDI and the volume of FT significantly impact each other.

Results of Variance Decomposition Test and Impulse Response Function Analysis

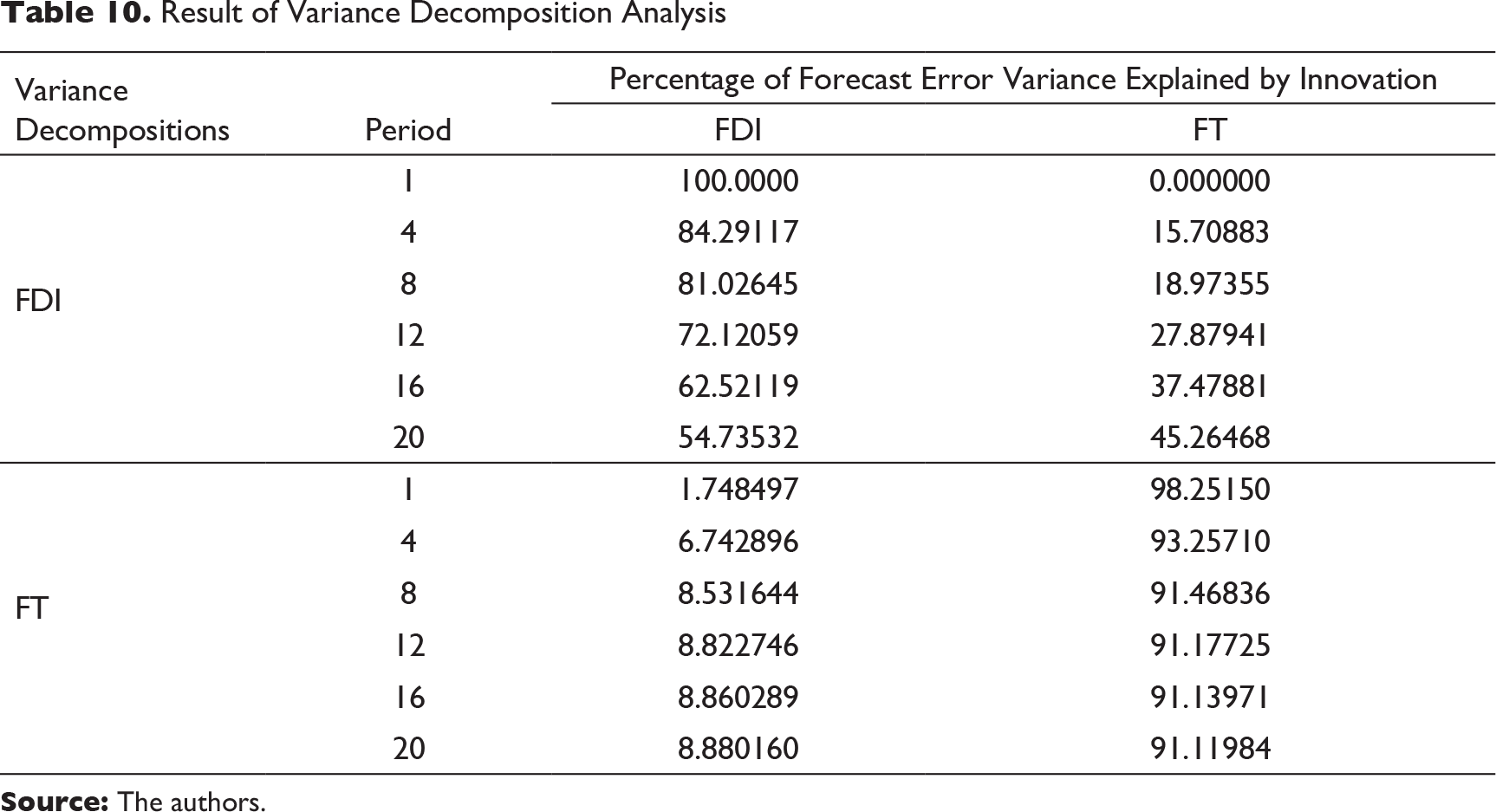

After determining the long-run and short-run causality, the analysis extended variance decomposition and impulse response function under the VECM framework to investigate the degree of exogeneity and direction of the relationship between the variables beyond the sample period.

Result of Variance Decomposition Analysis

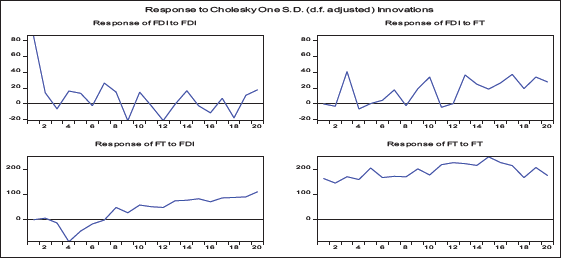

Figure 2 depicts the results of the impulse response analysis, which sketch out the dynamic response paths for a time horizon of 20 periods to a one standard deviation impulse or shock in both FT and FDI. The second figure of the first row exhibits the responses generated from a positive innovation of FT to FDI, which depicts overall inconsistent responses. Besides, the first figure of second row imprints the responses generated from shock of FDI to FT, which shows an inconsistent negative response for the first few quarters, and after the eighth quarter, it generates positive response till the 12th quarter. However, in both the cases, it is observed that responses are inconsistent and a positive trend for the last half of the time span.

Discussion

There are very few studies (e.g., Prasanna, 2010) that focus on establishing the empirical nexus between FDI and export during the liberalized period of the Indian economy. Although, Jana et al. (2020) undertake rigorous time series estimation on FDI and export in the context of India, it makes a general emphasis on FDI–export scenario since the mid-1990s, and therefore the results could not serve the present purpose. This subsequent research effort is instigated by the felt need of addressing the much-neglected research area, that is, effect of inward-FDI, especially that which comes and increases in leaps and bounds after the sweeping economic reforms of 1991, on export promotion of the country. The study uses quarterly data of FDI and export from the year 1991–1992 to 2019–2020 to confirm the actual dynamics of these two variables. The most suitable time series estimation techniques like Johansen’s co-integration test, vector error correction estimation, Granger causality test, impulse response function analysis, etc., are employed to arrive at the robust estimates. The study finds a bidirectional short-run relationship between the two macroeconomic variables. However, in the long run, only export is found to influence the volume of inward-FDI and not vice versa. Therefore, the effect of FDI on export promotion of the economy, especially during the liberalized period, is not found to be so profound. Now, it is also to be admitted that the study cannot produce considerably different evidence on the topic from Dash and Sharma (2011), Sultan (2013) and Jana et al. (2020), etc. However, the study does not subscribe to the views of Kishore (2012), Sing and Tandon (2015), etc., which find FDI and export to be statistically unrelated.

Conclusion

The present study makes a subsequent attempt after Jana et al. (2020) to examine the much debated FDI–export nexus in the context of India’s liberalized economy. The study confirms that FDI can promote the export of liberalized India only for the short run, whereas the export is found to have an FDI-promoting effect for both short and long run. The findings of this study are quite similar to the studies of Dash and Sharma (2011), Sultan (2013), Jana et al. (2020) that find a long-run unidirectional causality from export to FDI. Now, an important inference that can be drawn from the set of findings is that the inward FDI has the potential to boost the export performance of the economy, but, somehow, this effect is not sustaining for long. When we probe into causes, we see that the reason why FDI fails to exert a sustainable impact on export performance of the country is the lack of a proper channelization of foreign funds to export-oriented industries of the economy. Thus, Indian policymakers need to revise their economic policy to ensure optimum FDI-led export growth in the country. In this regard, China’s policy to channelize inward-FDI into manufacturing sectors and the resultant momentous success in export performance should be considered as a classic example for FDI-led FT promotion. We must understand the fact that the key difference between the inward-FDIs in China and India lies in their approach of channelization and utilization. In China, the FDIs mainly feed the manufacturing industries that deal with tradable goods, whereas, in India, FDI is encouraged mostly in services. The highest amount of FDI in India comes from the service sector (62.47% of total FDI in the year 2016–2017 as per Department of Industrial Policy and Promotion, Government of India), which has a very small contribution to the export of the country. While the merchandise export of India stood at US$275.9 billion, it reached only US$164.2 billion in the year 2016–2017 for service export (Source: Annual Report 2018–2019, Ministry of Commerce and Industry, Dept. of Commerce, Government of India).

Moreover, the continuous efforts from the policymakers to remove many trade barriers to services make the sector much more attractive avenues for foreign investors. For example, recently, the Government of India has tabled a draft legal text on trade facilitation in services to the World Trade Organization (WTO) in 2017. Therefore, India must learn to push substantial amounts of FDI into the export-oriented industries to reap maximum benefits. Towards this development, in addition to horizontal form of FDI, the vertical form of FDI in which a multinational corporation expands its business to a new foreign land by moving to a different level of the supply chain may be encouraged into manufacturing industries to revitalize the sector for propelling export performance.

Policy Implications

When the objective is to push manufacturing exports, the FDI policy needs to be properly aligned with such an objective. In this regard, inviting FDI from multinational and transnational corporations may be instrumental (Kumar, 1998; Lall & Narula, 2004; Pradhan, 2011). In addition, it is also suggested that the government stipulate performance regulations, impose provisions like local sourcing of intermediate goods to intensify local linkages and export obligations to ensure the quality of FDI (Kumar & Pradhan, 2002). Besides, as the country witnessed phenomenal growth in export from SEZs under its Foreign Trade Policy 2015–2020 (Source: Ministry of Commerce & Industry, Government of India), the government should undertake further efforts to channelize the FDI flow to SEZs to achieve maximum export performance.

However, the most recently emerged moderating factor that can abhorrently alter almost all macroeconomic equations, is the COVID pandemic. Amidst the worldwide outbreak of coronavirus pandemic and the resulting global economic slowdown, foreign investors have already pulled out an estimated US$26 billion from developing Asian economies (Source: Outlook, May, 2020). However, India may turn this global threat into an opportunity by proving itself a comparatively safer destination for foreign investors than its neighbouring nation China. The economic analysts are pegging a luring outlook of India’s inward-FDI scenario in the years to come as the changing foreign investors’ sentiments caused an abrupt rolling-back of investments from economies like China due to the lingering uncertainty about the health scenario, loss of confidence and resultant straining in relationship with the Chinese government. With respect to policy implications, at this time of huge distraction among global entrepreneurs, the Government of India must strategically invite their attention. The country must ensure necessary mechanism and institutional set-up to utilize the upcoming bonanza in the form FDI in boosting national production and export. Most importantly, the suggested short-run causality between FDI and export may turn into a stronger long-run relationship should the government succeed to administer preferential policies to attract specific FDIs, that is, FDI in export-oriented manufacturing sector.

Footnotes

Acknowledgement

The authors are grateful to the anonymous referees of the journal for their extremely useful suggestions to improve the quality of the article.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.