Abstract

Strategic contracting is based on the fundamental condition of risk and gain sharing in the course of relational rent creation. The mutual application of hardship and gain provisions implies that if such an instance occurs after the conclusion of the contract, the parties have an obligation to renegotiate the contract in a fair manner. However, even though strategic contracting strives to ensure the alignment of incentives, there might still be a risk of hold-up and perhaps even efficient breach of contract. We apply the classical microeconomic risk-preference theory of expected utility and transaction cost theory in order to develop a form of strategic contracting that entails the use of a reciprocal hardship and gain provisions, which helps the contracting parties deal with such instances. We outline three necessary and cumulatively sufficient conditions under which hardship and gain provisions make economic sense.

Keywords

Introduction

The purpose of strategic contracting is to use the contract as a dynamic and proactive management tool in order to achieve relational rents (Dyer and Singh, 1998) and – at best – a sustained competitive advantage (DiMatteo, 2010; DiMatteo et al., 2012). Strategic contracting is still a relatively new area of research that emphasizes the interdisciplinary relationship between law and economics (Petersen and Østergaard, 2018: 267). Petersen and Østergaard (2018) define strategic contracting as follows: We view strategic contracting as characterized by the aim of generating relational rent through the use of both proactive and reactive provisions that, based on resource complementarity and strategic fit between the contracting parties, protect knowledge exchange and relationship-specific investments from opportunistic behavior. Hence, a strategic contract is a partnership arrangement through which the contracting parties aim to achieve joint competitive advantage.

Central to research on strategic contracting is how economic theory can qualify the content of commercial contracts. If a contract is silent about an issue that arises after the conclusion of a contract, the default rules will traditionally include whether the contract in question falls under a lex specialis or the law of obligations. Thus, the basic idea of using economic theory as an alternative to the default rules is to examine whether that theory provides a better outcome than the default rules derived from the prevailing law in question – the contract’s lex causae.

At the time of a contract’s conclusion, the parties are unable to predict all future events that may affect the performance of the contract (Grossman and Hart, 1986; Hart and Moore, 1990). In principle, there could be an infinite number of transaction costs associated with deducing all unanticipated circumstances that might influence the contract’s performance. This is not an effective approach in strategic contracting – from an ex ante perspective, it is better to insert a combined mutual hardship and gain clause in the contract in order to reduce transaction costs, increase the likelihood that the contract will be upheld, and reduce opportunistic behavior. Strategic contracting is based on the fundamental condition of risk and gain sharing in the course of creating increased value, minimizing burdensome circumstances, and aligning incentives.

In short, hardship can be defined as a (ex post) circumstance in which either it becomes more onerous to fulfill the contract or the equilibrium of the contract fundamentally changes. A regular gain provision can be defined as a mutual obligation to exchange strategic information during the course of the contract in order to achieve relational rents or even supernormal relational rents that the parties were not able to articulate before signing the contract. In the following, we look further into the concepts of hardship and gain provisions. Even if the parties to a contract do not wish to pursue strategic contracting, the transaction costs associated with trying to define the regulation of all future circumstances and their legal implications are exorbitant, such that doing so makes little economic sense.

Thus, the purpose of this article is to analyze how economic theory can provide key insights that must be taken into consideration in order to escape pitfalls, achieve relational rents, and design an efficient contract. We are aware of the risks of excessive haggling over costs and opportunistic behavior, especially in the form of hold-up during renegotiation processes, which we consider necessary if a hardship or an opportunity for a gain arises. However, strategic contracting aims to help contracting parties minimize the costs, including transaction costs, associated with hardships that arise during the course of a contrast and to maximize value related to possible gains.

In strategic contracting, the use of proactive clauses (see, e.g. Berger-Walliser, 2012) should be aimed at achieving relational rents by employing relevant economic theories to help qualify the content of the proactive clauses. Hardship and gain provisions are viewed as proactive.

Given the theoretical framework of strategic contracting, another purpose of this article is to analyze how economic theory can help improve current examples of hardship provisions derived from lex mercatoria and substantive law (depending on the contract’s lex causae). Some jurisdictions do not have provisions in substantive law that deal with hardship, including England and the Scandinavian countries. However, numerous important jurisdictions have adapted rules about hardship (Schwenzer and Munoz, 2019). 1 Moreover, to the best of our knowledge, no jurisdiction has specific rules about gain provisions in business contracts. Thus, in order to claim hardship, many jurisdictions require the inclusion of a hardship provision in the contract. In addition, a gain provision must be included in the contract to take effect.

In light of this background, the paper proceeds as follows. The next two sections account for the concepts of hardship and gain provisions, respectively, primarily in judicial terms. We do not address every detail from a legal perspective, as the literature is quite substantial, especially in relation to hardship. Instead, our aim is to examine why the parties to a contract should apply a mutual hardship and gain provision within the framework of strategic contracting.

We then discuss the renegotiation of hardship and gain provisions before we apply an economic perspective on hardship and gain provisions and outline the conditions that must be met in order to make such provisions economically rational. Thereafter, we discuss whether hardship and gain provisions are inseparable and reciprocal. With insights from utility theory and given relaxed conditions, we show that the reciprocal use of hardship and gain provisions may be mutually beneficial when the risk profiles of the contracting parties differ to some degree. Our conclusions are presented in the final section.

The hardship provision

The inclusion of a hardship clause represents a departure from the general principle in contract law that agreements are binding even if they become onerous – the principle of pacta sunt servanda. Furthermore, the inclusion of a hardship clause implies that the parties do not invoke relief rules under the lex causae of the contract, which may cause the contract to be wholly or partially invalid (Hondius and Grigoleit, 2011). Moreover, in such cases, the risk associated with unexpected circumstances is not exclusively allocated to one party (Madsen and Østergaard, 2017), even if such a principle exists in accordance with the contract’s lex causae. Many jurisdictions have rules that might make it possible to claim relief if an occurrence goes beyond the reasonable expectations of the parties and makes it unreasonable to uphold the contract (Edlund, 2009).

Most jurisdictions have rules concerning the occurrence of force majeure or occurrences beyond the control of the parties, as stated, for instance, in CISG Article 79 (United Nations Convention on Contracts for the International Sale of Goods). In such cases, the obligor in question will not be obligated to pay damages or carry out specific activities. There might be cases in which certain aspects of the contract cannot be carried out for a short period of time, such as in the instance of an export ban or a strike. Consequently, the performance debtor is obliged to perform as expected after the occurrence impeding proper performance comes to an end. When the wording of CISG Article 79 was negotiated, the inclusion of unexpected circumstances covering hardship was discussed. However, this wording was left out in the end. Nevertheless, the interpretation of CISG Article 79 in case law has shown that hardship falls within the article’s scope. Schwenzer and Munoz (2019) argue that hardship can be considered a special case that falls under force majeure, which implies that hardship is within the scope of CISG Article 79 and other international harmonization projects.

Force majeure and hardship have similar prerequisites in common. First, the subsequent circumstance could not be taken into account at the time of the contract’s conclusion. Second, the subsequent circumstance is exogenous. Finally, there is the question of the threshold to overcome. Some jurisdictions, like Denmark, require impossibility in order to establish force majeure in accordance with Section 24 of the Danish Sales of Goods Act, 2 while the threshold in accordance with CISG Article 79 is somewhat lower. In general, it seems difficult to clearly and accurately distinguish between force majeure and hardship. Even in cases of price fluctuations, the courts have been reluctant to establish hardship, but there have been cases in which the seller and buyer have been exempted from liability due to hardship under CISG Article 79 (Schwenzer and Munoz, 2019: 157). The risk of price fluctuations must be considered as a calculated risk between business parties.

As mentioned above, a party can initiate proceedings claiming that a contract is wholly or partially invalid, even though the unexpected circumstance cannot be characterized as force majeure, as it would be unreasonable to claim that the specific performance of the contract or the equilibrium of the contract have changed substantially. It is difficult, if not impossible, to determine whether all jurisdictions would treat a certain case of hardship in the same manner by either applying the relevant provision about hardship from substantive law or applying the hardship provision in the contract in question. There are numerous differences among jurisdictions. For instance, some jurisdictions have adopted specific rules about labor contracts in which the employee has the right to terminate a contract if that contract is materially changed (Hondius and Grigoleit, 2011). There seem to be substantial differences among jurisdictions, even though the jurisdictions initially appear similar.

Among the Scandinavian countries, there are obvious differences. For example, Sweden is considered an open jurisdiction in the sense that it has a general exceptional doctrine that specifically addresses the issue of unexpected circumstances that can lead to an adjustment of a contract. Denmark does not have such a doctrine (Hondius and Grigoleit, 2011). All of the Scandinavian countries have similar wording dealing with unfair contractual stipulations in the Contracts Act Section 36, 3 which takes subsequent circumstances that might make it unreasonable to uphold the contract into consideration. However, if we compare the application of Section 36 across the countries, the Norwegian courts have been more reluctant to apply it than Sweden and Denmark.

Even though hardship is not directly a part of substantive law in all jurisdictions, rules of hardship have been developed in different fora. Rules about hardship can, for instance, be found in: ▪ The Commission on European Contract Law, including the revision undertaken by the Association Henri Capitant des Amis de la Culture Juridique Francaise and the Société de Législation Comparée, ▪ UNIDROIT – The Principles of International Commercial Contracts (latest edition released in 2016). ▪ The Gandolfi Project – The Avant-projet de Code européen des contracts.

In 2003, the International Chamber of Commerce (ICC) published a suggestion for a combined hardship and force majeure provision (see ICC Publication 650). According to this suggestion, the parties might be obliged to renegotiate alternative contractual terms to reasonably allow for the consequences of the event. Failure to agree to alternative provisions would then entitle the party invoking the provision to terminate the contract.

Article 6.111(2) of the PECL (Principles of European Contract Law; see https://www.jus.uio.no/lm/eu.contract.principles.parts.1.to.3.2002/portrait.pdf) includes a provision on hardship, even though this term is not directly used. In Article 6.2, UNIDROIT contains a provision on hardship, the definition of which is given in Article 6.2.2 (see https://www.unidroit.org/english/principles/contracts/principles2016/principles2016-e.pdf): There is hardship where the occurrence of events fundamentally alters the equilibrium of the contract either because the cost of a party’s performance has increased or because the value of the performance a party receives has diminished, and (a) the events occur or become known to the disadvantaged party after the conclusion of the contract; (b) the events could not reasonably have been taken into account by the disadvantaged party at the time of the conclusion of the contract; (c) the events are beyond the control of the disadvantaged party; and (d) the risk of the events was not assumed by the disadvantaged party.

As such, the application of a hardship provision in strategic contracting implies that the contract is upheld but the economic risks are reallocated both ex tunc and ex nunc, as it may be that the economic return in the contract relationship declines if a hardship event occurs. In this context, the economic return in an alternative contractual relationship would also fall, as there must be strategic fit (party specificity) in order to engage in strategic contracting. Thus, there is already an economic reasoning for including a hardship clause, ceteris paribus.

In cases in which one party is a performance debtor and the other is a payment debtor, the latter will typically require a risk premium to accept a hardship provision, as the payment debtor is less likely to be affected by hardship than the performance debtor. In contracts in which both parties are performance debtors, there will be greater mutual interest and, therefore, an incentive to accept a hardship provision, as both parties are assumed to have the same risk of being affected by a subsequent circumstance that causes the contract to become more onerous.

As mentioned above, if a party wishes to claim hardship, the subsequent circumstance has to be exogenous. If the parties are pursuing strategic contracting, whether endogenous circumstances should be included in the wording of the hardship provision must be considered. We argue that when the proper performance of the contract relies on the skills of the individuals involved in the contract’s fulfillment, it is relevant to consider endogenous factors in the hardship provision. Take, for instance, a pharmaceutical research project involving two pharmaceutical companies developing a drug to cure a certain type of cancer. In such situations, it is relevant to apply strategic contracting and to include endogenous factors related to the individuals involved in the research, as the skills of the individuals are typically crucial for carrying out the project. A proactive hardship provision would for instance offer a solution if an individual involved in the research project were to leave one of the pharmaceutical companies, get sick for a longer period, or take maternity leave. In such cases, the obvious solution is for the affected company to hire an individual with at least the same skills and experience. However, what if the company cannot find such an employee? The non-affected company might have an employee available with the skills and experience needed to carry out the research project. From an economic point of view, this solution makes sense in terms of ensuring that the project is carried out in an appropriate period of time, even if the affected company has to compensate its partner.

The inclusion of a hardship provision implies that the contract can be continuously carried out, although possibly at a higher cost. The question then becomes how such a provision should be designed to take economic theory, including the risk profiles of the parties, into account.

The gain provision

At present, there seems to be no clear and unambiguous definition of a gain provision. Within the theoretical framework of strategic contracting, we find it beneficial to distinguish between irregular and regular gain provisions. It should be noted at the outset that turnover-based royalty payments that are included in, for instance, franchise, publishing, record, or movie contracts cannot be considered gain provisions within the framework of strategic contracting. Such provisions can be referred to as irregular gain provisions, as the parties are aware that there might be an opportunity to achieve success in terms of, for example, record sales by a particular artist, after the contract is concluded between the parties. In practice, there is a possibility of using a flat royalty rate, a progressive royalty rate, or a digressive royalty rate given the turnover/number of records sold. Such agreements are often linked to the fact that the performance debtor receives an ex ante guarantee of remuneration, which is subsequently recouped on the basis of the royalties.

The application of regular gain provisions in connection with strategic contracting recognizes the fact that when a contract is written, there is imperfect and at least somewhat asymmetrical information on future opportunities to increase relational rents. Thus, the use of regular gain provisions represents an attempt to achieve dynamic efficiency. The actual wording of the gain provisions will depend on the nature of the contract. However, they must be designed so that the parties are mutually obliged to notify each other if an opportunity to exploit a business opportunity arises during the term of the contract. Within the framework of strategic contracting, this is considered an exchange of strategic information, which in legal terms is a mutual obligation to communicate between the parties. This might include, for instance, an opportunity to reduce costs by applying new methods in the construction of a bridge or to use a drug for a new purpose. The latter was the case with Viagra, which was originally invented to help patients with heart disease but was eventually used to help patients with erectile dysfunction.

Similar to the application of the hardship provision, the application of a regular gain provision reflects the existence of imperfect and asymmetrical information when the contract is written. As discussed above, the parties can encounter endless transaction costs if they try to predict future business opportunities before the contract comes into force. The combination of these two provisions related to subsequent unexpected circumstances helps to create an incentive structure in which the parties use the contract as a management tool for joint optimization that, at best, achieves additional relational rents. In relation to the preparation of a regular gain provision to ensure incentive alignment, one may consider whether a breakdown that would be key for the economic value added should be included in advance based on the regular gain provision. We discuss this issue below in conjunction with our examination of contract renegotiations in cases of hardships or gains.

Thus, we define a regular gain provision as a mutual obligation to renegotiate parts of the existing contract or supplement the contract when an economic option that was not part of the original contract emerges (ex post). Thus, it refers to a case in which, in recognition of their own limited rationality, the parties use a relatively abstract provision to create a mutual obligation to communicate for the purpose of realizing profit opportunities ex post that were not known ex ante.

The application of a regular gain provision in strategic contracting is considered valid in most, if not all, jurisdictions in accordance with the principle of freedom of contract. Similar to the application of hardship provisions, the application of a regular gain provision reflects the application of a conditional promise to renegotiate the contract provided that a new business opportunity arises after the conclusion of the contract.

In two cases, the Danish Supreme Court has decided on the question of whether a predetermined payment was unreasonable in accordance with Section 36 of the Contracts Act. The Tintin case (U.2003.23 H) involved a translation agreement in which the translator was paid a fixed sum of DKK 10 for each page of the famous Tintin cartoon series translated from French to Danish. In our view, a fixed payment cannot be considered as either a regular or irregular gain provision. However, this case illustrates the role of imperfect and asymmetrical information from a legal and economic perspective. In the Pandora case (U.2012.3007 H), an agreement was concluded between the jewelry company Pandora and a glass artist to pay royalties to the glass artist for all glass beads, regardless of origin, sold by Pandora. The case deals with an irregular gain provision. From an economic point of view, both cases fulfilled a key prerequisite in strategic contracting: the parties had complementary resources. However, in both cases, one party was a single person, which made it difficult to fulfill the other prerequisites for strategic contracting.

The fact that at least one party may not be aware of the economic opportunity offered by the contract at the time of its conclusion is clearly illustrated in the Tintin case. As mentioned above, the publisher and the translator had agreed on a fixed payment for each page translated, which was customary in the Danish publishing industry at the time. In subsequent years, the Tintin comic books became a commercial success in Denmark, which led the translator to file a case with reference to Section 36 of the Contracts Act, asking that the publisher had to pay an extra consideration of DKK 500,000 to the translator. The Supreme Court found that the publisher did not have to pay any extra remuneration, as it had followed the practice of paying a certain amount per translated page. Moreover, the court stated that given the translator’s in-depth knowledge of the Danish publishing industry, he could have entered into a different agreement in which his remuneration would have depended on the number of Tintin comic books sold. This would typically require an irregular gain provision indicating that the publisher would pay the translator a guarantee sum as well as royalties, which seems to be the customary procedure in this industry today.

The Tintin case illustrates how limited rationality can be expressed in connection with a contract that probably cannot be considered incomplete in relation to calculation of remuneration. From the translator’s point of view, the contract had an unintended economic outcome in which the majority of the financial gain that was not anticipated at the time of the contract’s conclusion subsequently accrued to the publisher. When the information available at the time of contracting is imperfect, it is more difficult to determine the degree of asymmetrical information. The translator had probably never imagined the number of copies of the comic books that would be sold in Denmark.

In the second case, the Danish jewelry manufacturer Pandora entered into an agreement with a glass artist in early 2005. According to the agreement, the glass artist was obliged to design a collection of glass beads that matched the bracelets made by Pandora. The contract could not be cancelled for 20 years from the date of conclusion of the contract. Point 3.1 of the agreement stated: 3.1. Pandora pays the following royalty to Lise Aagaard. The royalty is agreed to be 12.5% of Pandora’s total net sales of glass beads, whether designed by Lise Aagaard or others.

Thus, according to Danish law, the general clause on unfair contract terms in the Contracts Act in the capacity cannot be used as a leverage to a professional party to make a subsequent (ex post) aggravation or relaxation of a commitment, despite the relatively sparse case law on this issue. This must be considered the prevailing law when the parties act as professionals, which is the case in strategic contracting. 4 These contracts involve calculated risk, which the translator and Pandora should have taken into consideration while negotiating and drafting the contracts in question.

Thus, the application of either a regular or irregular gain provision in a contract offers both parties to the contract an opportunity to solve the problem of imperfect and asymmetrical information. It also enables them to align incentives in order to avoid opportunistic behavior.

To the best of our knowledge, there are no large, comparative analyses covering numerous jurisdictions regarding the extent to which a gain provision can be considered unreasonable. This applies to both actual and irregular gain provisions. However, in the EU, the Common Core of European Private Law research project conducted a comparative study of the state of law in the European member states in relation to unexpected circumstances in contract law. The study did not directly include questions relating to gain provisions in the individual European jurisdictions, but the following question was asked in “Case 4”: Y leases business premises from X for a fixed period of fifteen years. Shortly after concluding the contract, the character of the area changes strongly and unexpectedly a military airport located nearby is shut down and an enormous amount of public funds is invested in the area (infrastructure etc.). As a consequence, Y’s business soars and his profits are 500 per cent of what he could reasonably have expected. By the same token, the value of comparable business premises in the same area rises to 500 per cent of the amount X and Y have agreed upon. X claims that the rental price should be adjusted accordingly or, alternatively, that the agreement should be terminated. Is X’s claim justified?

Although the above case does not relate to the interpretation of an actual gain provision, the court’s decision in such a case could have an impact on the interpretation of a gain provision. Therefore, in the event of a dispute between the parties on the interpretation of the payment provision, whether prevailing law affects the interpretation of that provision will be decisive. Therefore, the gain provision must be made as clear and unambiguous as possible, regardless of the fact that it may be a provision that cannot be explicitly formulated because the parties do not know the details of the potential gain.

The renegotiation of hardship and gain provisions

As mentioned above, neither PECL nor UNIDROIT contain gain provisions. In Article 6:111 (2), PECL contains a provision in which the disadvantaged party is entitled to request renegotiation in the case of hardship. The same is true for UNIDROIT. In accordance with UNIDROIT’s Article 6.2.3., the disadvantaged party is entitled to request renegotiation:

In case of hardship the disadvantaged party is entitled to request renegotiations. The request shall be made without undue delay and shall indicate the grounds on which it is based.

The request for renegotiation does not in itself entitle the disadvantaged party to withhold performance.

Upon failure to reach agreement within a reasonable time either party may resort to the court.

If the court finds hardship it may, if reasonable, (a) terminate the contract at a date and on terms to be fixed, or (b) adapt the contract with a view to restoring its equilibrium.

In order to request renegotiation in accordance with Article 6.2.3., the disadvantaged party must prove that the hardship event has fundamentally altered the contract’s equilibrium because either the cost of a party’s performance has increased or the value of the performance the party receives has diminished.

The mutual application of a hardship and gain provision implies that the contract must be renegotiated in a fair manner if such an instance occurs after the conclusion of the contract. The obligation to renegotiate is based on willingness and trust (Schwenzer and Munoz, 2019). Furthermore, the obligation to renegotiate can be perceived as an obligation to remain loyal to the other party, which is an obligation in most jurisdictions. Schwenzer and Munoz (2019: 162) point out that most jurisdictions do not have direct rules about redress if a party is unwilling to renegotiate a contract in case of hardship. Even though this is the case in most jurisdictions, a party’s refusal to renegotiate in case of hardship could represent a breach of the obligation to remain loyal to the other party. 5 However, even though strategic contracting strives to align incentives, there might still be a risk of hold-up and, perhaps, even a risk of efficient breach of contract. In an attempt to uncover a way to avoid such instances, we apply the classical microeconomic risk-preference theory of expected utility (Shavell, 1979; Von Neumann and Morgenstern, 1953) that involves the use of reciprocal hardship and gain provisions. However, we first establish the conditions under which hardship and gain provisions make economic sense.

The conditions under which hardship and gain provisions make economic sense

We can think of three necessary and cumulatively sufficient conditions under which hardship and gain provisions make economic sense. The first condition is that the contract parties find it uneconomical, or not worth the effort, to specify all possible contingencies for hardship and gain-sharing ex ante. Alternatively, aware of their bounded rationality (i.e. their inability to collect and process overly abundant information), the parties recognize that such specification is a futile task, such that an incomplete contract (Grossman and Hart, 1986; Hart and Moore, 1990) is the best available option. The contract could specify that the parties share any hardships and gains equally thereby enshrining the principle of full economic solidarity, as in a fifty-fifty equity joint-venture. However, such unconditional solidarity disregards internal causation issues (i.e. hardships and gains that are predominantly or exclusively caused by or attributable to one of the parties). This may induce incongruous behavior of various kinds. For instance, one party may behave in an incautious manner or be outright irresponsible when hardship solidarity is assured, or one party may only make a half-hearted attempt to pursue gains. At best, full economic solidarity would work in cases where the hardship or the gain was exclusively attributable to exogenous factors beyond the control of the contract parties. However, this situation would call for a standard force majeure paragraph rather than a hardship clause.

As a second necessary condition, the parties have a vested interest in maintaining the contractual relationship. This interest may be acknowledged when entering into the contract, but it is more likely to be recognized when the relationship develops into a locked-in situation (Klein et al., 1978; Williamson, 1975) in which the parties realize that a break-up and partner replacement are likely to entail high switching costs. In the course of a “fundamental transformation” (Williamson, 1975, 1985), the parties go from a large-number bargaining situation to a small-number bargaining situation that favors a continued exchange relationship over involvement with other potential exchange partners. To the extent that the contractual parties invest in relation-specific assets (e.g. capital, knowledge, skills), they are better prepared than other firms for additional transactions. Hence, the exchange partners build social and business interdependencies that shape their future behavior. Conversely, if good partner alternatives are available, there is only a weak incentive to adopt benevolent behavior in order to uphold the relationship. In other words, it is in the interest of the individual contract party to deny the other party a share of an (unexpected) gain or extend any absolution or latitude to a party in the face of hardship.

The third and final necessary condition is that the contract parties have excluded the formation of an equity joint-venture as an alternative to a contractual arrangement. The equity joint-venture is a governance mode that is often used when it seems relatively futile to write a complete contract, for example, because the assets to be exchanged are highly idiosyncratic and do not easily lend themselves to ordinary market transactions (Hennart, 1988). Hence, the raison d’être for the formation of equity joint-ventures is somewhat similar to the first condition – that the parties are unable to write a complete contract (Grossman and Hart, 1986; Hart and Moore, 1990). However, while the drafting of incomplete contracts is associated with the inability to foresee contingencies, equity joint-venture formation primarily has to do with the absence of market prices for the assets to be exchanged.

There might be many reasons for the dismissal of a joint venture as an alternative to a contractual arrangement: the magnitude of the collaboration may not justify the considerable set-up costs associated with this type of governance structure (Williamson, 1975), or the bounded-rational (or cognitive-limited) parties may not consider the joint-venture solution due to unfamiliarity with such arrangements (Welch et al., 2018). In addition, the corporate governance policies of (one of) the parties may forbid this type of committed cooperation – perhaps in anticipation of disagreements about the venture’s management. In particular, fifty-fifty ownership assumes the risk of ending up in deadlocked decision-making situations (Greiner and Woodcock, 1995; Salbu, 1993; Thomas, 1987). However, despite these reservations, an equity joint-venture appears to be a universal solution to both hardship and gain-sharing challenges.

Are hardship and gain provisions inseparable and reciprocal?

There are no economic arguments against disentangling hardship and gain provisions. Hence, the contract parties may include a hardship provision but not a gain provision and vice versa. In principle, a hardship or gain-sharing provision could be granted to only one contract party – usually the agent in a principal/agent relationship. For example, a large producer may include hardship and gain provisions as general clauses in its contracts with suppliers and distributors. It is difficult to see why the parties should not favor a principle of reciprocity in this regard. After all, it would seem odd to deny the other party a renegotiation option in case that party experiences hardships or notices that unexpectedly high gains were allotted to the other party as a result of the collaboration. However, we are not arguing for one-to-one reciprocity, meaning that one contract party offers the other party a hardship and/or gain-sharing opportunity and receives one in return. As we demonstrate below, there might be strong economic arguments for not pursuing such one-to-one reciprocity, especially in contract situations where the risk profiles of the parties differ to some degree.

Hence, a special and interesting case is the situation in which one contract party benefits from a gain provision but extends one of hardship in return. In order to justify such an arrangement, we must relax the conditions for regular provisions discussed previously and assume away completely unpredictable hardship and gain situations. Instead of such complete – or Knightian – uncertainty (Knight, 1921) about future gains and hardships in contractual relations, we assume a moderate degree of uncertainty. By this, we mean the presence of quantifiable potential benefits and risks to which estimated probabilities can be assigned. The contract parties agree on these estimates ex ante (i.e. as part of the contract negotiations). In the following, we exemplify this in the context of a hypothetical franchise contract, but the principles apply to most other collaborative contractual arrangements, such as licensing, outsourcing, and distributor agreements as well as equity joint-ventures. Therefore, our franchise example finds parallels in a broad range of other types of collaborative contexts, suggesting a fairly high degree of generalizability.

In our franchise example, the franchisee is assumed to be risk-averse while the franchisor is risk-neutral. Hence, the franchisee attaches relatively high and low values to a hardship provision and a gain provision, respectively. In contrast, the risk-neutral franchisor assigns the same utility to the two provisions. In this example, the hardship provision comes in the form of a put option – the right, but not the obligation, to sell specified assets to a (contractual) partner at a pre-negotiated price (the strike or transfer price). Conversely, the gain provision takes the form of a call option – the right, but not the obligation, to acquire specified assets from a (contractual) partner at a pre-negotiated price. The franchise agreement typically obliges the franchisee to sell only the licensed products. Hence, all of the rents derived from the franchisee’s assets are associated with sales of the franchised goods and services. Furthermore, franchising serves as an example of interfirm collaboration characterized by considerable initial and irrevocable investments, most of which are undertaken by the franchisee, which must be considered the relatively risk-averse party in the collaboration.

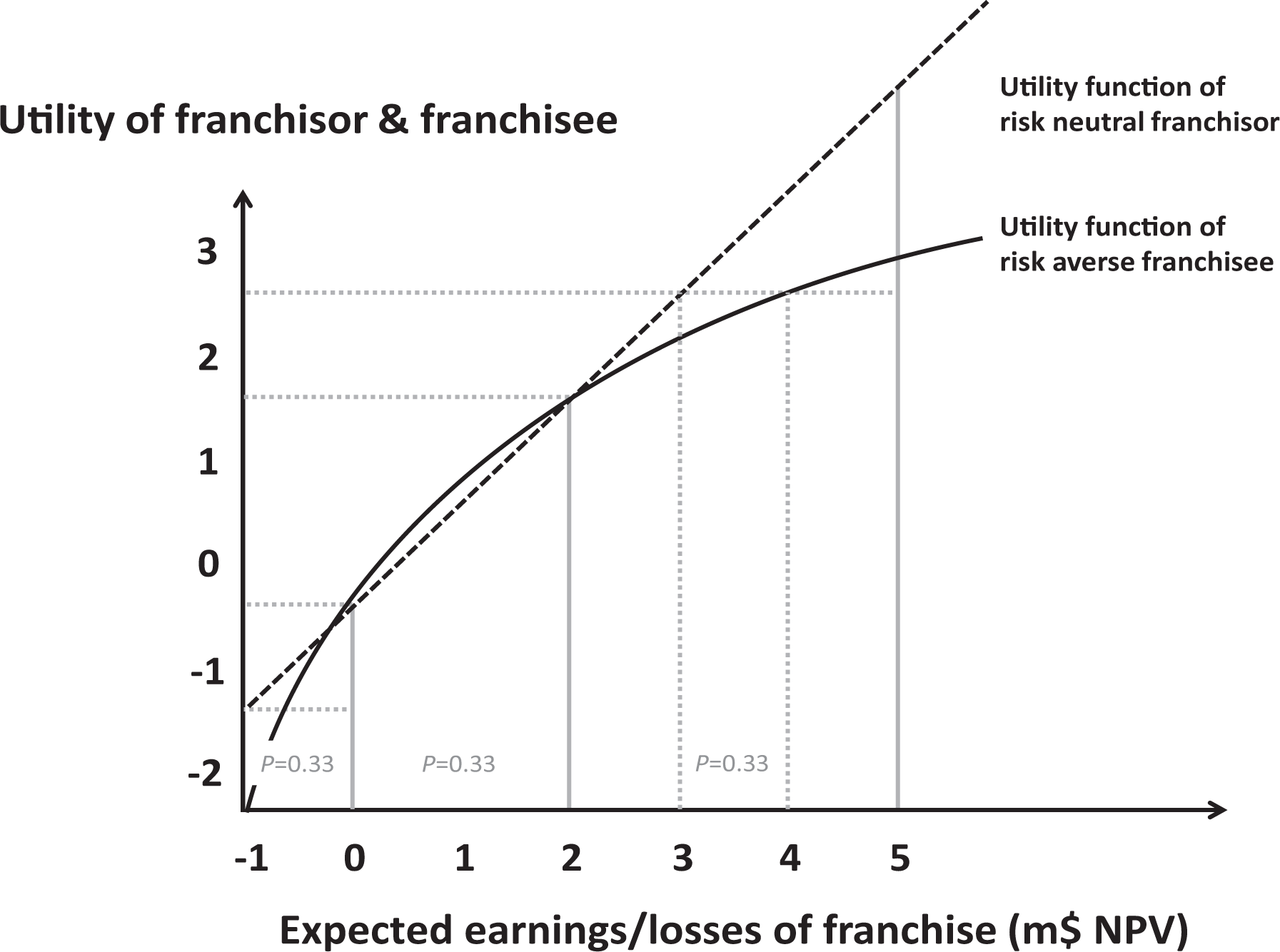

Given its various attributes, franchising stands out as a form of interfirm collaboration in which the use of reciprocal real options seems to make sense. A fictitious, illustrative example of the reciprocal use of real options in franchise collaboration is shown in Figure 1.

A utility model assuming asymmetrical risk preferences in franchising.

In this example, the risk-willing (risk-neutral) franchisor holds a call option and the risk-averse franchisee holds a put option. In conventional international franchising contracts, the entrant firm (the franchisor) is usually entitled to a certain percentage of the turnover (a royalty fee) that is generated in the foreign market. If the market turns out to be more lucrative than expected (i.e. the turnover exceeds the market prognoses on which the contract was based), then the entrant firm will receive a minor share of this “windfall gain” until the contract expires. The introduction of a call option in exchange for a put option may secure the franchisor a larger part of this windfall gain without making the franchisee worse off. 6 Hence, Figure 1 condenses the reasoning behind the reciprocal use of call and put options. The context is franchising, but it could, as mentioned, be other collaborative ventures as well.

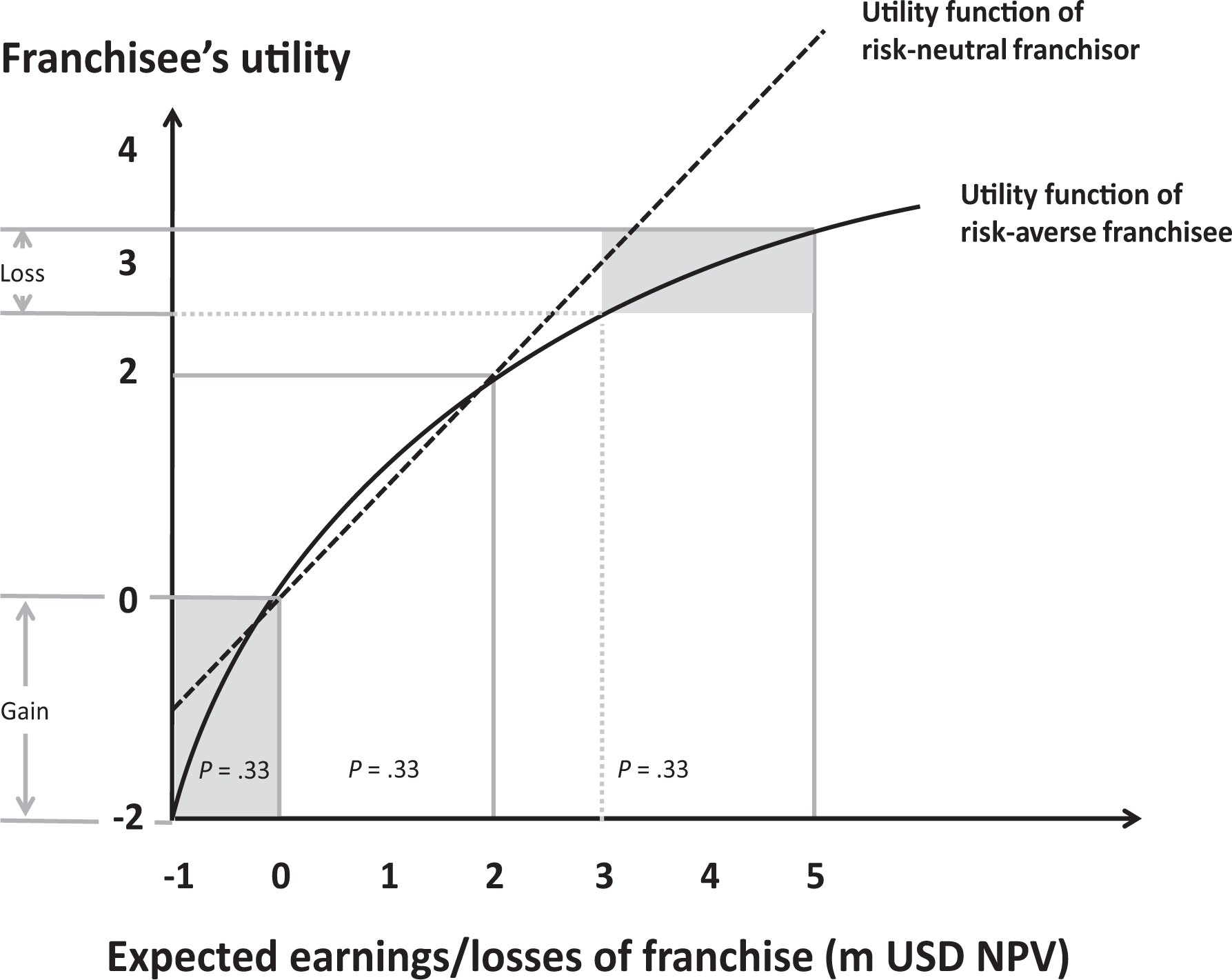

The horizontal axis indicates the expected losses or earnings in a foreign market. The two parties, the franchisor and the franchisee, are both uncertain about the market prospects but agree on the probabilities of different possible outcomes (Triantis, 2000). More specifically, they jointly estimate that there is a probability, p = .33, of earning US$2m net present value and similar probabilities, p = .33, of losing US$1m or earning US$5m. The vertical axis indicates the utility that the franchisee and the franchisor attach to these three market outcomes. We assume that the franchisor is risk-neutral and that its risk-preference curve is therefore a straight (45°) line. At the same time, we assume that the franchisee is risk-averse. Therefore, the franchisee’s risk-preference curve is concave, such that the marginal utility value diminishes with decreasing losses and increasing earnings. In the example depicted in Figure 1, the franchisee attaches a relatively high negative utility value (–2) to the likelihood of a US$1m loss and a relatively low positive utility value (around 1) to the likelihood of a US$5m gain. In other words, the franchisee is willing to trade, for instance, two-thirds of the potential for extra earnings of US$3m (going from US$2m to US$5m) for a downside risk of losing US$1m (see Figure 2).

Franchisee’s gain and loss when swapping a call option for a put option.

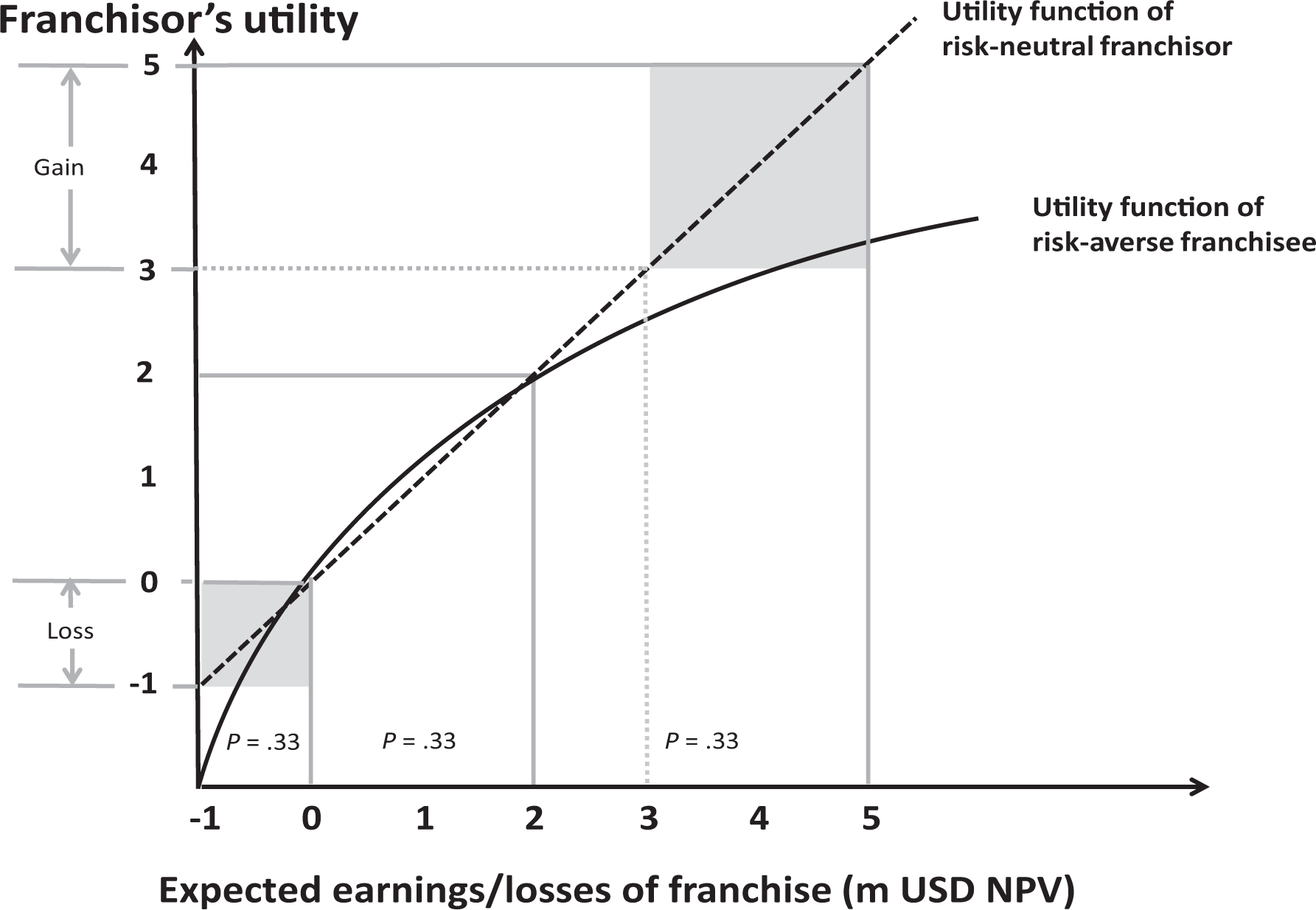

This tradability is in accordance with the expected utility theorem (Von Neumann and Morgenstern, 1953) and can be translated into a real option reciprocity arrangement: the risk-neutral franchisor receives a call option in return for extending a put option to the risk-averse franchisee. Through this exchange of real options, the (expected) utility of both parties improves: the franchisee renounces extra earnings of US$2m (equivalent to 0.75 utility units) by extending a call option to the franchisor, but the exchange also eliminates any risk of losses and, thereby, gains two utility units by obtaining a put option in exchange. Conversely, the franchisor agrees to assume any loss that may occur (equivalent to one utility unit) by extending a put option to the franchisee, but the franchisor obtains the right to appropriate two-thirds of the franchise earnings between US$2m and US$5m (more precisely, the franchisor would take over the franchise and pay one-third of the earnings as a transfer fee to the franchisee), which corresponds to two utility units (see Figure 3).

Franchisor’s gain and loss when swapping a put option for a call option.

The franchisee and the franchisor attach approximately the same utility value (around 2) to the mid-range prospect of earning US$2m. If this market scenario is realized, then neither of the parties has an interest in exercising their options. It is worth noting that even though the franchisee is likely to lose in terms of the quantity of dollars earned, the franchisee doubles its utility from 1.25 units (3.25 minus 2) to 2.5 units (2.5 minus 0) by swapping real options.

In this example, the franchisor is also better off not only in terms of utility but also in terms of expected dollar earnings. Compared with a standard franchise contract (e.g. an irrevocable 10-year contract with a turnover-based royalty income of 5%), the extra earnings may be considerable.

Conclusion

The existence of incomplete contracts can to a great extent be remedied through the use of hardship and gain provisions when undertaking strategic contracting. However, the wording of the hardship and gain provision must be carefully considered in order to achieve relational rents. In accordance with the lex mercatoria, “hardship” covers only exogenous circumstances but whether it should also include endogenous circumstances must be taken into account depending on the nature of the contract.

As strategic contracting sharpens the commitment to remaining loyal to the other party, the application of a reciprocal hardship and gain provision as well as a mutual obligation to renegotiate the contract must be enforced in most jurisdictions if one of the parties refuses to renegotiate. It is difficult, if not impossible, to imagine the arguments that would lead a court to reject such an obligation to renegotiate (Madsen and Østergaard, 2019; especially, The Danish Supreme Court in U.2011.138 H). This must be considered prevailing law across most jurisdictions.

Future research could examine the extent to which the industry is aware of the possibility to apply strategic contracting – including the use of hardship and gain provisions – instead of conventional contracting. This research could also analyze awareness of the prerequisites related to achieving relational rents as well as current obstacles.

Our account of the conditions under which hardship and gain provisions make economic sense led to a discussion of when an extension of a hardship provision in return for a gain-sharing provision would be beneficial for both parties. By applying the classical microeconomic risk-preference theory of expected utility, we found that such an exchange of provisions should be beneficial when the risk profiles of the contract or joint-venture partners differ to some degree and the venture requires the relative risk-averse partner to undertake irrevocable and risky investments upfront.

Footnotes

Declaration of conflicting interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.