Abstract

This article aims to study the influence of customer reference marketing on capital buying decisions in the context of firms with highly complex contractual frameworks. It presents the case of a thermoelectric power plant in which customer referencing did not influence a relevant buying decision. Evidence suggests that the implicit governance mechanism of project financing nullified the referencing effect. Project finance restricts managerial discretion over free cash flow, which influences organizational buying behaviour at the level of capital equipment goods. This research identifies the presence of this singular kind of governance system and draws managerial consequences for suppliers who wish to sell to project firms. A clear understanding of the legal and contractual framework can help suppliers to fulfil the potential customer’s needs and expectations.

Introduction

The field of strategic contracting and negotiation seeks to extend our knowledge of how actors form and manage relationships for successful trading outcomes (Pitsis et al., 2015). The alignment of interests and agents for the purposes of forming trading networks and partnerships with successful outcomes is a complex and difficult task (Cummins, 2015). While many companies aim to increase their procurement capabilities, few are able to transform the purchasing function into a source of competitive advantage (Carpi et al., 2016). According to Cummins (2015), risk avoidance has been one of the key purposes of contracting and negotiation. Purchasing professionals are focused on achieving the best price; at the same time, however, they aim to reduce procurement-associated risk. Risk reduction is relevant in the context of industrial buying decisions (Choffray and Johnston, 1979; Greatorex et al., 1992; Hawes and Barnhouse, 1987; Puto et al., 1985). Industrial buyers attempt to reduce uncertainty by gathering additional information (Puto et al., 1985; Webster and Wind, 1972). The greatest impact on risk reduction is made by positive opinions from informal influencers outside the buyer’s firm (Henthorne et al., 1993). Customer references are effective tools for reducing ambiguity about the value promised by a supplier’s offer (Anderson and Wynstra, 2010). The practice of requesting customer references emerged as a way to decrease buyer uncertainty and perceived risk (Jalkala and Salminen, 2010), and it is often adopted in tendering activities. Jalkala and Salminen (2010) define customer references as the customer-vendor relationships and the related value-creation activities externally or internally leveraged by a firm in its marketing efforts. In the same way, these authors also view customer reference marketing as a means of demonstrating and illustrating a solution’s potential value and the business benefits that a supplier may be able to deliver. A deeper understanding of customer referencing is therefore crucial to the improvement of the body of knowledge on strategic contracting and negotiation.

The literature on strategic contracting and negotiation is silent on the influence of customer referencing on capital buying decisions, especially in firms with highly complex contractual frameworks. This gap in the literature prompted us to ask the following question: ‘Does customer reference marketing influence the behaviour of project firms when it comes to capital goods purchasing, and if so, what role does it play in this process?’ When we observed that referencing had no effect, we followed up with an additional research question: ‘What factors may inhibit the expected effects of customer reference marketing?’ This article aims to deepen our understanding of the referencing phenomenon by considering the case of a firm from the Portuguese energy sector. The following study explores the influence of customer reference marketing on a capital goods transaction within a project firm. Project finance involves a highly complex contractual framework. The study of project firms is relevant to our understanding of strategic contracting and negotiation. Tejo Energia is the owner of a coal power plant (Pego) in Portugal and is an international consortium. The company holds the necessary licences and permissions to operate the plant. The Pego power plant has all the attributes of a project finance endeavour. The European Union Large Combustion Plant Directive requires that the impact of gaseous emissions must be minimal. To achieve this aim, Tejo Energia invested close to 170 million euros in 2008. The two operating units from the Pego power plant were retrofitted with: (i) a flue gas desulphurization system; (ii) a selective catalytic reduction system; and (iii) an electrostatic precipitator control system. The following study rests on an implicit conceptual framework (shown in Figure 1), which emerges from the literature review. The framework illustrates the idea that customer reference marketing impacts capital buying decisions. This study begins with a review of the literature on customer referencing and project finance, and moves on to describe the adopted methodology and the studied case of Tejo Energia. To the extent that it brings together the topics of customer referencing and project finance, it constitutes a novel contribution to the field.

The ex-ante theoretical framework.

Customer referencing

‘Customer reference’ is a concept seldom used in the literature on business-to-business marketing (Jalkala and Salminen, 2009a, 2010; Salminen and Möller, 2006). However, customer referencing is an important component of marketing practice and is recognized as such by practitioners and managers (Jalkala and Salminen, 2009a). Salminen and Möller (2006) argue that this practice is theoretically understudied and consider its relevance to management practice. The authors present a theory, which they call the Normative Theory of Referencing, which aims to provide a better understanding of customer references (Salminen and Möller, 2006). This article views the Normative Theory of Referencing (Salminen and Möller, 2006) as the major stream of thought on customer referencing. It is an approach to which other authors have contributed additional ideas, thus enhancing our comprehension of it.

It is possible to mention the existence of a discernible body of knowledge that deals with the customer referencing practice. Contributions to this theory come from several authors but emanate primarily from within the Industrial Marketing and Purchasing Group (Axelsson and Easton, 1992; Ford et al., 2003; Håkansson, 1982; Håkansson and Snehota, 1995; Turnbull and Valla, 1986) due to the concept of business relationships rooted at the heart of this conceptual framework.

Jalkala and Salminen (2009b) recommend that future research should consider industry sectors that have yet to be studied. According to these authors, following this recommendation will broaden the scope of the theory of referencing. Ruokolainen and Mäkelä (2007) acknowledge the influence and significance of ‘reference business’. In ‘reference businesses’, corporate customers typically buy complex, high-tech products or services. Tejo Energia has the features of a reference business.

According to Salminen (2001), customer references play an important role in capital equipment industries. This idea is also defended by Salminen and Möller (2004), who claim that references play a key role in capital equipment bidding processes. Additionally, Salminen and Möller (2006) describe the contextual factors that affect the significance of references. They argue that high-tech and market uncertainty raise the relevance of customer references by augmenting the potential customers’ perceived risk. Among other things, these uncertainties are propelled by the total amount of investment and by the innovation embedded in the offered product or system.

Customer referencing has been the focus of work by various authors with different research strategies (Godes, 2008; Jalkala, 2009; Rese et al., 2012; Ruokolainen, 2008b; Salminen, 1997). This stream of research stems from two different geographical regions which adopt opposing research strategies. In general, Northern European authors sustain their fieldwork by adopting qualitative research, most often in the form of case studies, while North American authors take a more positivist approach. In reality, contributions from non-Northern European regions are scarce. Research in this area has thus been dominated by authors from the Northern European stream. This fact confirms the importance of empirical research from other countries, such as Portugal, and thus of the sort presented in this study.

The sharing of customer references is a marketing activity in which relationships are of immense importance insofar as the communicated message is based on the portfolio of the relationships that the company has established with its customers (Jalkala and Salminen, 2009a). Such relationships involve at least three actors: the supplier, the reference customer, and the existing customer. This is why the theory of referencing has established the notion of triadic value creation. The seminal studies on triads took place within the field of sociology (Thibaut and Kelley, 1959) and moved into the fields of management and marketing. Holma (2009) asserts that a ‘triadic business relationship setting consists of three dyadic relationships, i.e. relationships between actors A, B, and C. Adaptations occur in the dyadic relationships A-B, B-C, and A-C, which are interconnected, either directly or indirectly’. According to Holma, a ‘triadic relationship setting’ consists of three actors that may have both direct and indirect connections. The following study relies on the following definition: it is a ‘phenomenon which exists at the firm level between three actors, and it consists of three independent actors (firms) that are connected to each other, either directly or indirectly, for the purpose of doing business’. Holma (2009) stresses that this triadic setting exists at the firm level between three independent actors who are linked by the goal of doing business. Co-operation among actors is a voluntary and intentional action. That is to say, it is deliberately designed to meet specific purposes and is therefore not the outcome of coercion.

Helm and Salminen (2010) claim that ‘a purely dyadic supplier-buyer perspective no longer serves the needs of firms embedded in network structures’. The additional relationship with the reference customer comes into play – especially in the so-called ‘reference business’ – and gives rise to a new construct: the reference triad. In short, the reference relationship constitutes a reference triad.

Helm and Salminen (2010) present a framework which aims to integrate customer referencing relationships and reputation building. To be more precise, it describes the process of reputation building based on reference relationships within a reference triad. Despite its simplicity, it is consistent and aligned with the model proposed by Salminen and Möller (2006) since it incorporates the three elements that were also present in the foundational model. Moreover, it considers the established relationships among these three actors, and its focus is not the supplier but the established network in which all the actors are present.

The reference triad is a small network ‘in which three dyadic business relationships are embedded’ (Helm and Salminen, 2010). The relationship that takes place between the seller and its reference customer therefore becomes a foundation for reputation building. Nevertheless, the reputational effect only becomes effective when the relationship between the seller and the potential customer is established. Additionally, it takes several deals with different customers to generate credibility and build a reputation.

According to Helm and Salminen (2010), dense reputation transfer takes place in three distinct domains in reference triads. The first domain is the individual features of the three actors of the reference triad. The second domain is the factors affecting the relationship between the three actors. The last domain is the market determinants of reference-driven reputation formation.

Aarikka-Stenroos and Jalkala (2012) argue that customer references are active network actors, not parts of marketers’ toolkits. The authors claim that value is generated reciprocally among all the actors present in the network. This means that if it is true reference customers create value for new customers and for the seller, it is also true that new customers and the seller generate value for the reference customers. These conditions result in the creation of triadic value. Based on their work, it is possible to collect useful insights which help to define the concept of a reference network. This study therefore assumes that a reference network is a network that (i) includes at least three actors (a seller, a potential buyer and a reference customer) who create value for each other and (ii) enables interaction through the co-creation of marketing messages that resonate with customers’ problems and needs.

Aarikka-Stenroos and Jalkala (2012) describe what potential customers, reference customers and suppliers experience as ‘co-created value outputs’ of a reference network. They argue that reference customers provide credible business data on the acquired solution. This information is evidence for the realized value-in-use. It demonstrates and concretizes the content of the solution and its benefits to potential customers.

The theoretical framework presented above highlights a body of knowledge that deals with the practice of customer referencing. This is known as the ‘theory of customer referencing’, and it provides not only a description but also an explanation of this phenomenon.

The literature on customer referencing raises the hypothesis that customer references have a positive impact on vendor marketing activity (Helm and Salminen, 2010; Jalkala and Salminen, 2005, 2009a, 2010; Ruokolainen, 2008a; Ruokolainen and Mäkelä, 2007; Salminen, 2001; Salminen and Möller, 2004, 2006). Empirical work in the field of referencing undertaken thus far has focused largely on the supplier as the main unit of empirical observation and has ignored the other constituents of the reference triad: the reference customer and the potential customer (Helm and Salminen, 2010). Just how customer reference marketing influences the buying centre in the acquisition of goods from a specific vendor remains unclear. Accordingly, the purpose of this study is to contribute to the literature on strategic contracting by describing the facts and circumstances associated with the customer reference practice and to explore the ways in which they take place from the potential customer’s point of view.

Project finance

Project finance emerged in the 1970s in the energy generation sector; nowadays, however, it is used to finance diverse industries, including telecommunications, transportation and healthcare. Project finance emerged as a financing mechanism as a result of the energy supply shortfall in the US and around the world. At that time, high energy prices prompted the US Congress to approve new forms of public regulation as a way of promoting investment in additional power plants. Equity investors created stand-alone companies that owned electric power generators and financed them with nonrecourse debt. Investors chose project finance as the mainstream instrument for financing these assets, most often in association with long-term power purchase agreements. These ‘off-take’ contracts guaranteed the ‘bankability’ of projects.

Governments and private sector firms continue to use project finance to fund large infrastructure investments such as power plants (Brealey et al., 1996; Esty et al., 2014), as is the case with Tejo Energia. In 2013, firms financed circa US$415 billion worth of capital expenditure using project finance (Esty et al., 2014). It is expected that worldwide capital investment in the form of project finance will continue to grow (Scannella, 2012). The total demand for infrastructure investment might surpass US$70 trillion by 2030 (OECD, 2007). According to Esty (2004), the main motivation for studying project finance hinges on the idea that financial structure matters and that financing and investment are not separate decisions. Research on project finance generates new insights into risk management; from an educational standpoint, however, project finance should be taught in contract theory courses (Esty, 2004).

Project finance combines high leverage with nonrecourse to the investor’s balance sheet. Creditors only have recourse to the project firm’s cash flows, as debt is structured without any recourse to the sponsor’s cash flows or assets. This is only possible because of the specific nature of the project firm, which must be legally independent. John and John (1991) define project finance as: [t]he financing of a project by a sponsoring firm where the cash flows of the specific project are earmarked as the source of funds from which the loan will be repaid and where the assets of the project serve as the collateral for the loan. [t]he raising of funds to finance an economically separable capital investment project in which the providers of the funds look primarily to the cash flow from the project as the source of funds to service their loans and provide…a return on their equity invested in the project.

Complex contracting frameworks are characteristic of project firms. Kayser (2013) identifies contractual arrangements and the related legal frameworks as one of the main areas of academic interest in the field of project finance. Contractual arrangements concern the set of rules negotiated by the project stakeholders, whereas the legal framework is the stakeholders’ jurisdiction. The majority of contracts are written under UK or US law (Esty et al., 2014). Negotiations between shareholders and lenders are often costly and time consuming, as they require the contribution of fiscal, technical, legal and financial consultants to estimate the amount of cash flow generated by the project company (Borgonovo et al., 2010). Project finance demands detailed and highly complicated contractual agreements among multiple parties. Four primary contracts are signed to establish an independent power-producing company (Esty, 2003): (i) the construction and equipment contract, which defines the terms and conditions for the building of the facilities; (ii) the fuel supply contract; (iii) the power purchase agreement (often called the ‘off-take’ contract); and (iv) the operating and maintenance contract, which governs the day-to-day operation of the project company. Dozens of other contracts follow these four key agreements, rendering the legal framework highly complex. This is the case both with contracts aiming to raise debt and equity to finance the project and with supply contracts, which ensure adequate sources of supply (Scannella, 2012). According to Esty (2004), a standard project can involve 15 or more parties and 40 or more contracts. Because of the extensive contracting that supports project finance, it is common to speak of ‘contract finance’ and to describe the firm as a ‘nexus of contracts’, where the legal existence of the firm serves as a platform for contracting relationships (Jensen and Meckling, 1976). Contracts bind cash flows to previously defined destinations and therefore limit managerial discretion to a large extent (John and John, 1991).

A project finance contractual framework acts as a governance structure by restricting the managerial use of funds, which guarantees the payment of loans and returns on the invested capital. Project finance affords a contractual substitute for investor protection laws where weak legal protection is given to investors, as in the case of embezzlement and creditor rights in bankruptcy (Subramanian and Tung, 2016). Project finance drives economic growth, not only in developed countries but also in the least developed economies – where financial development is weakest – since it emulates the features of a well-developed market (Kleimeier and Versteeg, 2010). Project finance is a preferred means of limiting the exposure of investors’ balance sheets to high risk foreign markets (Borgonovo et al., 2010). Independent legal incorporation reduces the cost of monitoring managerial performance. In addition, project finance allows for cash flow verification (single purpose assets) while reducing agency conflicts (Subramanian and Tung, 2016), mainly due to its contractual framework. It works as a governance structure and reduces both agency costs (cf. Fama and Jensen, 1983; cf. Jensen and Meckling, 1976) and project cash flow volatility (Esty, 2003). However, adopting a project finance framework involves high transaction costs (cf. Coase, 1937; cf. Williamson, 1975, 1981, 2007), in particular when paralleled with standard corporate finance investment. These costs can constitute 5–10% of a project’s total expenditure (Esty, 2004). Project finance has a key disciplinary role to the degree that it prevents managers from wasting or misallocating free cash flow. This leads to managerial risk aversion; project managers have an incentive to engage in risk-free behaviour, with the ultimate goal of ensuring a return to capital providers. As a result, this complex framework reduces agency conflict between capital providers (the principal) and project managers (the agent).

Methodology

The field of referencing is in need of additional qualitative research (Ruokolainen and Mäkelä, 2007; Salminen and Möller, 2004, 2006). The present work adopts a case study research strategy (Darke et al., 1998; Dul and Hak, 2007; Easton, 1998, 2010; Eisenhardt, 1989; Eisenhardt and Graebner, 2007; Gummesson, 2007; Halinen and Törnroos, 2005; Patton and Appelbaum, 2003; Shanks, 2002; Stake, 1995; Woodside and Wilson, 2003; Yin, 1989, 2009; Yin and Zajac, 2004) which is particularly suitable for addressing the specific purpose of the study, because it allows for increasing our understanding of the customer references phenomenon and providing additional and far-reaching insights into the related variables.

Several authors (Ruokolainen and Mäkelä, 2007; Salminen and Möller, 2004, 2006) recommend case studies as a key research strategy in customer referencing research. Interest in case-study-based research has been growing, especially in contexts where researchers seek to understand a social phenomenon in its natural environment (Darke et al., 1998). Darke et al. (1998) warn about the practical difficulty of ensuring that this kind of research has sufficient scientific rigour. Perry (1998) confirms this by noting the lack of scholarly publications based on this method. Johnston et al. (1999) emphasize that case-based research has traditionally been the target of criticism from the scientific community due to its lack of objectivity and scientific rigour. However, these authors acknowledge its relevance in exploratory phases. Woodside and Wilson (2003) argue that the research paradigm in organizational behaviour needs to change. Macpherson et al. (2000) argue that case studies produce consistent data and deepen our understanding of rich social contexts. Similarly, Rowley (2002) highlights the most challenging aspect of case studies: their role in elevating the investigation from a purely descriptive stage to a higher level of contribution to the body of theoretical knowledge. Patton and Appelbaum (2003) suggest that case studies represent an important option when conducting scientific research in organizational sciences, not only as a method of generating hypotheses for quantitative studies, but also as a way of generating and testing theories. Eisenhardt and Graebner (2007) suggest that the growing popularity and relevance of case studies can be traced to their ability to establish links between qualitative evidence and mainstream deductive research.

The unit of analysis selected for this research is the potential customer, a subset of the reference triad (Helm and Salminen, 2010). Holma (2009) addresses the complexity of business relationships and focuses on ‘adaptation’ within the context of a ‘triadic relationship setting’. According to the author, the triadic approach to business relationships is relevant not only in situations where an intermediary is involved, but also where the three actors are directly connected to each other, which is the case with customer referencing. The focus of that study was the triads in the context of corporate travel management. It integrated theories from the industrial network approach and theories from the sociological landscape, which were used to understand the triadic relationship setting. However, the author states that only a few studies take a full triadic approach due to its difficult application in research practice. This conclusion supports the argument presented in the current work to the effect that research into this area can safely focus on just one side of the reference triad.

As noted above, the triads investigated in this research are reference triads. The concept of a reference triad is based on the idea that interaction takes place between three key actors: the seller, the buyer and the reference customer (Helm and Salminen, 2010). The broad objective of theoretical inquiry in this research is therefore the reference triad, although we will study this through the lens of a specific actor: the potential customer. Fieldwork is carried out by tackling the buyer’s perspective, which means that the potential customer is selected as the unique source of data. In short, the present research has the potential customer as the unit of empirical observation.

The collection of primary data for the case-creation process involved semi-structured interviews that followed a generic predefined outline (supported by a case protocol). Authors interviewed 14 professionals, such as industry experts, and the procurement & contract manager and the production manager of PEGOP; the CEO and the sales director of Tejo Energia; and the deputy director for energy markets of EDP. Interviews took place face-to-face and by phone. Some professionals were interviewed more than once. On average, each interview lasted for around 2½ hours. Side comments and additional relevant elements (e.g. reference material, brochures, press releases, web pages, etc.) were also valued as secondary data. This approach is considered effective, especially when investigation into more subtle issues and long answers are required in order to deeply understand the topics being reported by respondents (Ackroyd and Hughes, 1992). The interviews were taped and transcribed verbatim. A guided visit to the power plant was also given by a member of the production team. In response to a formal letter requesting research access to Tejo Energia, the firm formally agreed to participate in this study. The case was reviewed and commented on by members of the firm, including the CEO and the sales director. The presented case was approved for disclosure within the academic community by the firm’s representative.

The data collected from the interviews provide the strong empirical foundation for the theoretical contribution made by this research. Interviews took place in Portuguese. Tape recordings and field notes were transcribed, edited and converted into text for further analysis. Data were disassembled via formal coding (Yin, 2011: 186). The software MAXQDA 12 (release 12.1.0) 1 was used to code the data retrieved from the interviews. The data coding was completed prior to translating the interviews’ content into English. The choice to run the analysis in the original Portuguese was made with an eye to preserving useful insights embedded in the original interviews.

The case of the Pego thermoelectric power plant

The Pego power plant is located in the centre of Portugal. It was built by EDP (the old incumbent firm) from 1988–1995 in order to satisfy the requirement to provide more diverse sources of energy. It is operated by PEGOP on behalf of Tejo Energia. Tejo Energia is responsible for the management of the Power Purchase Agreement signed with REN (the ‘off-taker’).

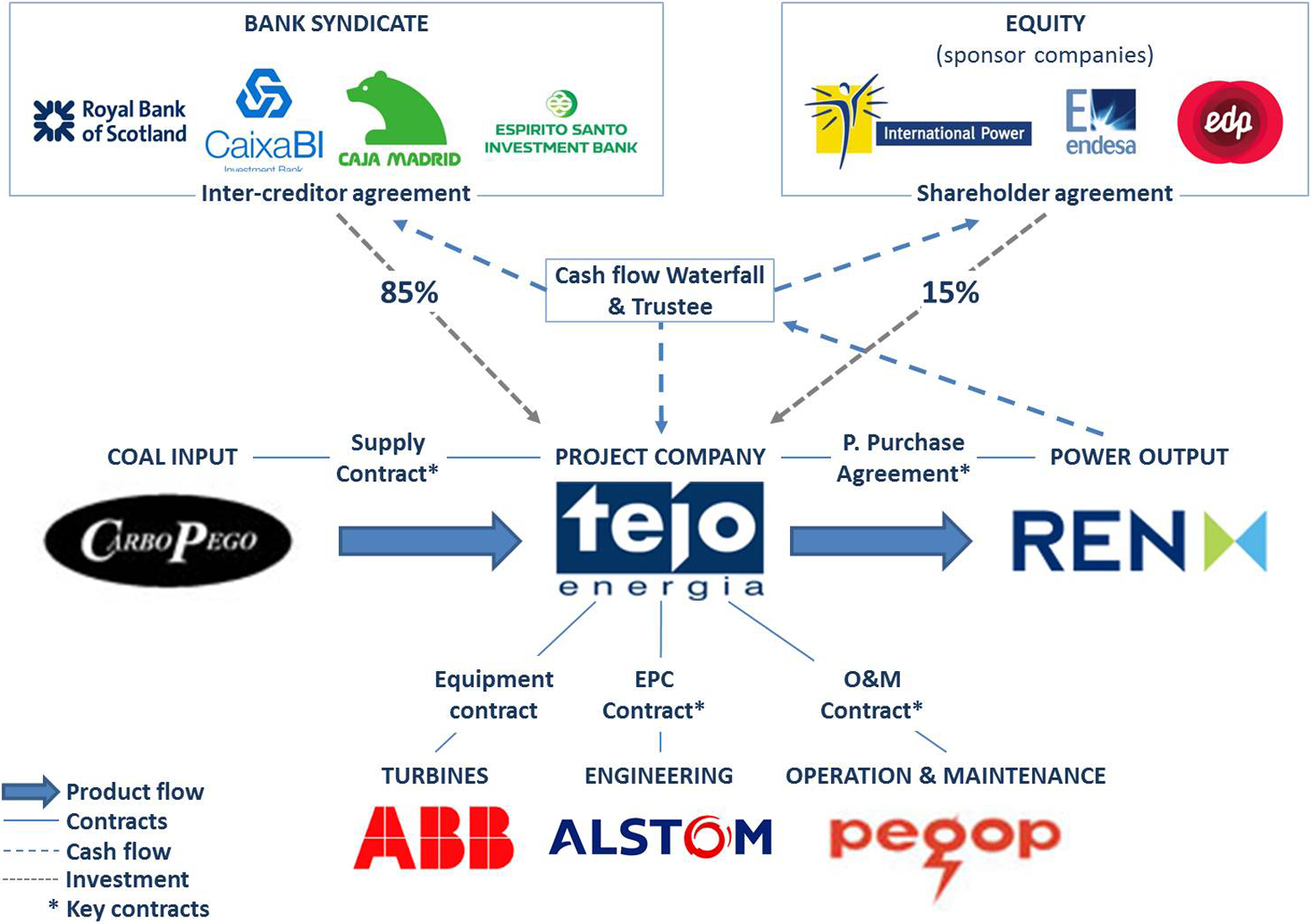

In 1990, as part of a government initiative to restructure EDP and encourage private sector investment in the electricity sector, the Pego power plant was marketed for sale in an international bid. The purchase of the Pego power plant by Tejo Energia took place in 1993. The sale resulted in the infusion of around 755 million euros into the national treasury. At the time, this was the largest financial transfer across European international borders. It represented the first case of large-scale ‘project finance’ in southern Europe, and its framework is described in Figure 2. It involved some of the largest Portuguese and international banks. Today, Tejo Energia is one of the largest Portuguese private companies in terms of its assets. When Tejo Energia was established in 1993, over 100 contracts regulated the company’s legal and financial activities (Estrutura Financeira da Tejo Energia, 2015). At the time of its foundation, the percentage of borrowed capital was around 85% – that is to say, the total project cost was funded by a mix of debt and equity, in an 85/15 split. In 2006, the business was re-financed with a consortium of 13 banks, including some of the largest national and international financial institutions in the world. The mandated lead arrangers were: (i) Royal Bank of Scotland; (ii) Caixa Banco de Investimento; (iii) Caja Madrid; and (iv) Banco Espirito Santo de Investimento. Alongside the shareholders, the banks played an important role in monitoring the project’s technical and financial performance. According to the procurement and contract manager, the fact that this was ‘project finance’ meant that specific adaptations from many business activities had to be made. For instance, in procurement activities special care must be given to contracts and legal requirements. These demands are mainly set by the consortium of banks running the ‘project finance’ agreement.

Project finance framework for Tejo Energia.

PEGOP was incorporated in Portugal as a joint venture between National Power (UK) (with 50% of the shares) and Endesa (with the other 50%). The company is responsible for operating and maintaining the Pego power plant (also known as ‘O&M’). The company manages a broad set of contracts with external companies, but it also employs its staff in direct operations or maintenance activities. This outsourcing option is taken in cases where PEGOP is not able to provide highly complex or specialization services. Sometimes, contracting an external provider for maintenance services is mandatory, most often due to formal equipment guarantees that are requested by the consortium of banks managing the project financing.

Purchasing and general buying behaviour at Pego

Among other responsibilities, PEGOP runs the production and maintenance departments at the Pego power plant. Both departments, as well as other staff units, are supervised by the head of the power station. The objective of the production department is to conduct the power plant productive units so as to fulfil REN’s despatch instructions. For instance, it starts and stops each of the productive units. PEGOP’s maintenance department guarantees the power plant’s working conditions and is responsible for managing maintenance activities, including: (i) corrective maintenance; (ii) planned maintenance; (iii) predictive maintenance; and (iv) preventive maintenance.

Pego’s procurement office is a subset of the maintenance department. It is responsible for running major procurement processes, including the acquisition of: (i) spare parts; (ii) contracts (maintenance or others); (iii) Engineering Procurement and Constructions (EPC) (‘turn-key’ contracts, also called ‘special projects’); and (iv) other non-critical goods. Purchasing is normally done via tender, and more aggressive purchasing tactics (such as reverse auctions) are not used. Among other staff, the office is composed of one procurement and contract manager and two operational buyers. The office is governed by processes that, according to its manager, are well designed and set the rules and boundaries for its operation. Nevertheless, according to the same source, due to its small dimensions the procurement office is highly flexible, adopting different procedures according to the relevance and complexity of the items being bought. The firm trusts each member of its purchasing staff and expects them to act in its interests.

Downtime is the most critical factor in this industry, as replacement parts are difficult to procure. Even if this were not so, however – that is to say, even if replacement parts were easily obtainable – the process of replacement would be too lengthy and expensive due to the costs of halting production. Such costs are several thousand times higher than the costs of intervention and maintenance. In this context, the price is not the principal criterion when selecting a vendor, either for equipment or services. Instead, the primary criterion is the economic value of the adopted solution.

PEGOP’s purchasing manager argues that there is an imbalance of power in this sector between the buyer (the power plant) and the vendor. He claims that once a decision to buy a critical element from a specific vendor has been taken, the maintenance services and spare parts must be bought from the same vendor. This reality is even harsher in the context of project financing – as is the case with the Pego power plant – where a formal guarantee of all production equipment is requested. According to the same source, several tactics can be adopted to overcome this hazard. One option is to conduct buying negotiations based on future business expectations. Another option is to rely on shareholders’ support to gain information on prices and increase negotiating power.

The handling of customer references

The purchasing office assesses a vendor’s experience by obtaining reference lists, which are then confirmed. Overall, the checking of customer references is an informal process. It is only done when necessary, for instance in order to give greater credibility to the buying decision. When it is necessary, contact with counterparts may have three objectives: (i) to learn about a previous solution; (ii) to ascertain how much it cost; and (iii) to gain knowledge on the extent to which the solution was successful. Vendors are not requested to provide reference lists, since they deliver them by default. Customer reference checks are often conducted via email, telephone or site visit. Nevertheless, there is no formal process for handling them. According to the purchasing manager, this informality is not an obstacle, as in purchasing there are only three elements that carry any objectivity: (i) the price; (ii) the expected delivery date; and (iii) the extension of the guarantee. Accordingly, the rest remains subjective. Generally, the maintenance department checks customer references, although this is sometimes done by the purchasing office. Once again, no formality or rigid processes apply. The information obtained via customer references is incorporated into the buying process as it is collected. It is ultimately an ad-hoc, interactive and dynamic process.

At the extreme, customer references can reverse the direction of a buying decision. During customer referencing, diverse questions of the following sort arise: (i) ‘Is this company working for you?’; (ii) ‘What have they been sourcing from you for the last five years? Where and what values have been involved?’; (iii) ‘Was it ok? What problems arose?’; (iv) ‘Are they delivering what they agreed to? How do they behave?’; and (v) ‘Is the price aligned with the market?’

PEGOP’s procurement and contract manager argues that when a vendor is good, honest and transparent (that is to say, it does not hide behind false excuses for delays or mistakes), it is common to hear reference customers say positive things about it. In fact, he claims that if one can speak to the technician responsible for running the equipment operation or its maintenance, the truth about the vendor will immediately come out. The purchasing manager argues that his immense trust in technicians’ accounts is grounded in the fact that technicians do not have a ‘commercial filter’; their situation is not affected by sales incentives.

The purchasing manager argues that customer references do not help in assessing either vendors’ reputations or their credibility because ‘they are much more than what their references say about them’ (this is even more valid now due to the present concentration of vendors, which is considered oddly high). With this said, customer references do help to reveal the problems (expected or unexpected) and outcomes (what went right or wrong) associated with a given investment. Above all, references help in the assessment of a supplier’s ability to deliver a specific contract or technology and reduce project risks (they validate a solution proposed by a vendor). This same manager argues that risk reduction is the most important benefit of customer references. He also suggests that customer references help firms to implement new technology and estimate returns on investment, as well as other related key performance indicators. Requests for information (RFIs) are often triggered by analysis of customer references.

Following the installation of the new flue gas desulfurization (FGD), selective catalytic reduction (SCR) and electrostatic precipitator (ESP) units, the Pego power plant has received many visits from other coal plant managers who want to know more about the adopted solution and the quality of the relationship with the vendor. The plant welcomes these managers, providing them with information and dedicated site visits. Of all these visits, no more than three were organized by Alstom, the solution vendor.

The FGD/SCR and ESP purchase

Under the European Union’s green legislation, member states had until 2008 to reduce emissions of acidifying pollutants, particles and ozone precursors from power plants. Tejo Energia invested approximately 170 million euros in order to comply with the new regulation requirements. This investment took place between 2007 and 2008. The Pego power plant installed a new FGD unit that used wet limestone forced oxidation (LSFO) technology. FGD units use a set of technologies to remove sulphur dioxide from exhaust flue gasses from fossil-fuel power plants. Because of environmental regulations, the FGD, SCR and ESP units are considered critical; the power plant is not able to operate without them. When it comes to NOX control, the power plant relied on SCR equipment. In addition, an ESP was acquired in order to control the emission of particulates.

The entire contract was awarded to Alstom in the form of an EPC arrangement. This contract was executed by the Italian and Swedish technology centres in consort with Alstom’s unit, based in Portugal. Alstom is a French vendor that had already provided the coal power plant’s core elements. 2 According to the purchasing manager, the relationship with Alstom is ‘regular’ and ‘without any quarrel, just the normal conflicts between people who buy and sell’. When we do not take into account the cost of coal, Alstom is the Pego power plant’s top supplier, even when EPCs are not considered. According to the purchasing manager, Alstom’s role as an incumbent supplier may have had an influence on the strength and competitiveness of its offer, above all given its experience and know-how.

Almost all Pego power plant EPCs have benefitted from the external support of both technical and legal consulting firms. This was also so when it came to the recent FGD/SCR and ESP acquisition. Tejo Energia contracted the services of an independent consulting firm, which helped to establish the technical specifications, assess the solutions offered by different competing vendors and manage the contract implementation after it had been signed off. In addition, the company received support from technical teams from their shareholders (Endesa and International Power). A legal firm also supported the buyer in this contract. This firm had already worked with Tejo Energia and had developed a solid relationship with it. PEGOP acted on behalf of Tejo Energia, leading the procurement process. This EPC dealt with the acquisition and installation of the new FGD/SCR and ESP units. Nevertheless, it did not involve maintenance services, as these were to be performed by PEGOP. Staff from Tejo Energia were also involved in defining the specifications and assessing the solutions presented by competitive bidders (for instance by tracking their status with rating agencies such as Dun & Bradstreet). Meetings took place on a weekly basis in order to assess the EPC’s progress.

The initial stage of the buying process involved ‘theoretical analysis of several alternative solutions’. The goal of this buying decision was to comply with the European directive. Different technical options were assessed, and project constraints were identified, for instance the space available to implement the solution (considered scarce). After completing the initial phase, the team listed European power plants that had already installed similar solutions. Their goal was to gather feedback from owners and other relevant information that could provide insights. Several power plants located in France were therefore visited. Alternative viable solutions became available, as did a rough estimate of their costs. Next, a technical solution was chosen, and the tender dossier (set of specifications) was completed. The owner’s engineering team (shareholders) supported the local team with advice and guidance.

At the time of the issuing of the Large Combustion Plant Directive, the expertise in the technology needed to comply with it was largely unavailable. Neither Portugal nor Spain had this kind of equipment. The technology was therefore new to Endesa, although GDF SUEZ had already deployed units in France. The visits to French FGD and ESP units were not organized by potential vendors. Nevertheless, they allowed for the gathering of information and other benefits as if they had been organized by potential vendors.

Formal requests (RFIs) for potential vendors to present references for similar projects were made. Potential suppliers were required to provide the details of the installation date and the amount of work hours. The goal was to assess the vendors’ experience with similar projects. Any claim on the vendor’s part to owning a new technology does not entail that it has already been able to sell it, or, more importantly, that it has implemented it successfully. This is important, according to the procurement and contract manager, since no bank is willing to pay for a technological trial in the context of project finance. None of the references presented by the vendors was checked.

The entire buying process took almost two years. According to the procurement and contract manager, the major difficulty faced by the team in charge of managing the EPC concerned the technical issues. Once this difficulty was overcome – that is to say, once the engineering team came up with the solution design – the rest of the process was straightforward (e.g. the preferred bidder selection, which was completed in approximately four months). The contract negotiation and agreement also took about four months to complete.

The tender for the EPC had two distinct parts: one related to providing the ‘core’ equipment and another related to contract works. Consortium leaders who replied to the call for tenders were all main providers of contract works. Offers from Alstom, Mitsubishi and Hyundai were among the several received.

In EPC acquisitions, shareholders generally have something to say about prospective vendors since they often have past experiences that they can share with local companies. This influence comes in the form of ‘soft power’ but never reaches ‘hard power’. That is to say, it is common to hear expressions like ‘this is a good vendor’; when it comes to the Pego power plant, however, ‘there is no memory of hearing the expression “we would like this vendor to be chosen”’, according to the purchasing manager. To sum up, shareholders’ informal recommendations about whom to choose as vendors are not followed as would be the case if they were formal recommendations.

Discussion

The case of Tejo Energia presents a buying situation where a significant amount was invested in capex by awarding an EPC contract to a vendor. It was Tejo Energia’s largest investment following the power plant’s initial opening. This EPC had the features of a reference business since it involved innovative technology and a complex solution. Also, it was the first purchase of this kind of equipment in Portugal – equipment with which the sponsor companies of Tejo Energia were not familiar. Moreover, the total investment almost equalled the firm’s annual revenue. These facts allow us to categorize this transaction as a reference business where, according to the previously reviewed literature, the referencing phenomena should be observable. The literature on referencing contends that customer references should have played an important role in this transaction. However, evidence for the relevance of references was not found. On the contrary, case analysis suggests that customer references did not play a key role in the buying decision under consideration.

Within the specific context of this EPC, the firm’s buying centre requested customer references from potential vendors. These references were presented in the form of reference lists. Generally speaking, the firm seems to have had a positive attitude towards customer referencing. The firm’s official view on customer references is in line with the theory of referencing. The purchasing officer pointed out the benefits of including customer references in buying decisions at Tejo Energia. Nevertheless, analysis of a concrete buying situation reveals that customer reference information was not considered by the decision centre of the electrical company. In fact, the case analysis suggests that the buying firm dealt with the reference information in a highly informal way. Moreover, references were not confirmed by members of the buying centre; no contact was established between members of the buying firm and the reference customer. Therefore, a relationship (formal or informal) between the buying customer and the potential vendor was neither initiated nor established. This reveals that the reference triad did not play a role in the complex capital investment buying decision. The implicit conclusion is that, in this buying decision, customer reference marketing did not influence the organizational buying behaviour. Likewise, no adaptation took place in this situation. The findings suggest that there is high uncertainty regarding the influence of customer reference marketing on organizational buying behaviour.

The irrelevance of customer reference marketing in the context of the studied case can be explained by the following suppositions: (i) the previous buying relationship with the selected vendor affected the relevance of customer reference marketing; (ii) Tejo Energia shareholders interfered with the buying decision; (iii) the informal handling of reference information rendered customer references ineffective; and (iv) the project finance feature of Tejo Energia affected the firm’s purchasing behaviour.

In the studied transaction, the selected vendor already had a past relationship with the buying firm. To what extent did this relationship affect the firm’s purchasing buying behaviour? The case suggests that the relationship between Alstom and Tejo Energia developed in a positive (or at least neutral) environment, Alstom being a relevant supplier to the Pego power plant. This status might have provided Alstom with a privileged position in the EPC tender. On the other hand, the buying firm considers Alstom a qualified vendor for the new equipment. Nonetheless, the Pego power plant has also successfully installed equipment from other vendors, e.g. turbines from ABB. Apart from Alstom, other privileged relationships do exist. To the degree that this is so, these relationships should have equally influenced the buying behaviour of Tejo Energia. Authors acknowledge this consideration and inferred neutrality on relationships with core vendors and their impact on the firm’s buying behaviour.

Did Tejo Energia shareholders interfere with the buying decision? This question is highly pressing for scholars who focus on equal research circumstances. The authors of this article made a considerable effort to find any piece of evidence which could suggest that Tejo Energia shareholders influenced the EPC buying decision. However, they were unable to find any evidence for this line of argument.

The case reveals that PEGOP acted on behalf of Tejo Energia, leading the EPC procurement process. In addition, the case also reveals that the resources available to fulfil the buying activity were minor, which led to a certain amount of informality in the handling of customer references. Did the informal handling of reference information undermine the value of customer references? There is surely an argument for the idea that a more formal handling of reference information would have enhanced its benefits. Moreover, a more comprehensive and committed approach in the field of customer reference analysis would have further strengthened the buying decision taken by the power plant. In any case, the evidence suggests that the handling of customer references during the studied transaction was generally quite informal.

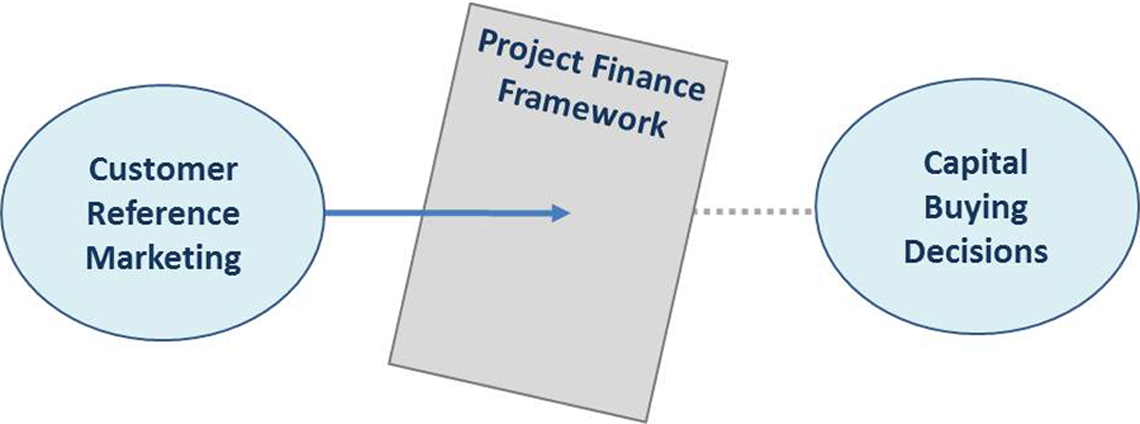

The studied case highlights the project financing undertaken by Tejo Energia. Does this characteristic affect the influence of customer reference marketing on the firm’s purchasing behaviour? The long-term financing of the Pego power plant is based on its projected cash flows. The project financing structure involves a syndicate of banks. They are secured by the involved assets and paid entirely from the generated cash flow. Therefore, cash flow assurance lies at the heart of the firm’s buying behaviour. All decisions are subject to this criterion. This explains the relevance of the economic value of the adopted solution. Downtime is the most critical factor because it strongly impacts the cash flow of the firm. This project finance context motivates conservative and risk-free buying behaviour. Customer references provide evidence in support of a decision of this kind. Previous studies on customer reference marketing indicated that customer referencing is important and should have played a role in the studied decision. According to the literature on customer referencing, the project finance nature of Tejo Energia should have enhanced the relevance of customer references. However, the evidence suggests that customer references were ultimately irrelevant to the decision. Hence, this article ends by concluding that project finance acts as a mechanism that neutralizes the role of customer referencing. Figure 3 represents the ex-post theoretical framework where the implicit governance mechanism of project financing nullifies the referencing effect.

The ex-post theoretical framework.

Conclusion

Empirical evidence for the existence of a reference relationship was not found. The findings suggest that the reference relationship might not always play a role in the acquisition of capital goods, even in the context of a reference business. As a result, theories of customer reference should be reviewed accordingly and should include this aspect of the reference network phenomenon. New avenues for research featuring the potential buyer and its decision centre should be followed, as this will contribute positively to the present theory of customer referencing.

Nevertheless, the current literature on customer references remains relevant to future research to the extent that most of it was confirmed in the case under examination. For instance, this case study suggests that the procurement and contract director of PEGOP genuinely appreciates the benefits of customer referencing. Moreover, concepts such as ‘reference customer’, ‘success stories’ and ‘reference lists’ played a role in the case. By contrast, the ‘reference triad’ model was not observed in the field work. Future research on strategic contracting should aim to understand the circumstances under which customer reference marketing influences organizational buying behaviour. This future research should take place from the point of view of the potential customer – that is to say, the potential customer should be the empirical unit of analysis, and, if possible, new research should select and observe its buying centre.

As noted above, project finance restricts managerial discretion over free cash flow. Investor return is guaranteed by (i) contracts; (ii) independent legal incorporation; and (iii) limited managerial discretion. Capital providers use project firms to reduce costly agency conflicts between ownership and control. This motivation speaks in favour of a singular kind of governance system that aims to avoid free cash flow problems while fostering managerial risk-free behaviour. Most strategic decisions are taken before the project begins, leaving day-to-day or tactical decisions to project firm managers, who are not invited to decide on growth via reinvestment opportunities. This is not problematic since project assets have limited lives. However, this governance system ensures the return of free cash flow to investors and thus takes control over reinvestment decisions away from managers. This alignment effect takes place at the level of both managerial and capital providers’ incentives.

From a managerial perspective, this work contains several interesting insights, mainly for the vendor’s commercial action. As noted above, the implicit governance system limits managerial discretion. The buying firm has an incentive to maintain the status quo regarding their suppliers and technology. Since avoiding disruption is a key motivation, incumbent suppliers have a solid and sustained commercial advantage over newcomers. Therefore, incumbent suppliers are able to focus on the integrity of their margins, and newcomers should limit marketing and sales efforts designed to acquire new customers. The evidence suggests that in the context of project finance, the project firm has an incentive to maintain its portfolio of suppliers. This situation will only change if the firm is highly displeased with a supplier. When this occurs, newcomers are given an opportunity to intervene. This opportunity should not be wasted. A clear understanding of the legal and contractual framework helps the supplier to address the potential customer, and customer reference marketing may be a helpful tool in this regard. Customer references allow for the identification of other relevant customers and explain how the supplier was able to guarantee free cash flow continuity from the project firm to its destinations. Positioning customer cash flow continuity as the primary criterion in capital equipment decision-making is a way to make explicit the vendor’s commitment to the buyer’s key concerns.

Last, the use of only one side of the dyad in this empirical research implies certain methodological constraints. Hence a suggestion for further research is to expand the empirical unit of analysis from the potential customer to the entire triadic network and to include all of the established dyadic relationships. Moreover, limitations also stem from the adopted research method: the case study. Because this method cannot ground empirical generalization, it cannot ground claims to statistical significance. In this sense, another suggestion for further research is to adopt quantitative methods as an additional form of research.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.