Abstract

Increasingly complex industrial services rely on outcome-based contracts (OBCs); however, there is a dearth of research in this area of growth. The present research examines the benefits, risks, and overall contract performance of OBCs when they are based on a payment for availability (aOBC) versus a payment for economic results (eOBCs) logic. We offer a conceptual model that not only takes the perspectives of both the buyer and the seller into account, but also the role of product innovativeness and market turbulence as potential moderators. Results obtained from a multi-industry survey among 259 buyers and sellers using OBCs in complex industrial services show that both buyers and sellers attach higher benefits to eOBCs as opposed to aOBCs. With regard to perceived risk and overall performance, both forms of OBCs are found to perform equally well, both from the buyer and the seller perspective. However, when technological turbulence is high, buyers perceive significantly more benefits, making eOBCs more attractive from the buyer’s perspective. In contrast, when product innovativeness is high, aOBCs emerge as the better option because of the sellers’ higher risk for eOBCs compared to aOBCs. In sum, these findings help managers to better decide which type of OBC promises to be most beneficial under the given contextual conditions.

Introduction

Outcome-based contracting has gained increasing attention in recent years, both in academia and business practice (Kim et al., 2007, 2010; Ng et al., 2013). The essence of outcome-based contracting is the buying of relevant business outcomes rather than resources (such as spare parts or repair actions) required for their provision (Ng and Nudurupati, 2010). Outcome-based contracts (hereafter OBCs) are touted for their potential to align the interests of customer and supplier firms because they compensate the supplier ‘based on the same outcome that the customer cares about (i.e., product utilization), and hence the supplier is motivated to increase product performance’ (Guajardo et al., 2012: 961).

OBCs have a longer history in certain markets, such as airline, defense, logistics, as well as health care and public services. More recently, however, a wide range of suppliers in diverse industries is experimenting with this new business model (Ng et al., 2013). This trend is due to several drivers, such as the ongoing service transition of goods-based manufacturing companies (Ostrom et al., 2010), the growing demands of customer firms that increasingly pressure their suppliers to show them value for money (Terho et al., 2012), and the ever-increasing global competition that forces supplier firms to find innovative ways of differentiating their market offer (Ulaga and Eggert, 2006).

With regard to their underlying payment models (Holmbom et al., 2014), two different forms of OBCs can be distinguished: customers either pay for availability, or they pay for economic results. When customers pay for availability, they are being charged for the operational readiness of a system (Guajardo et al., 2012; Ng et al., 2010). The most prominent example for OBCs based on availability (aOBCs) comes from the airline industry where Rolls Royce invented its ‘Power-by-the-Hour®’ offering as early as the 1980s. Rather than charging its customers for the jet engine and the time and material needed for service and repair, Rolls Royce is being paid for the number of hours that its jet engines are operating in the air. In contrast, when customers pay for economic results, the performance indicator is a monetary outcome variable, such as incremental revenues or profits. An example for OBCs based on economic results (eOBCs) is a marketing consultancy that implements a new pricing scheme at a customer firm and shares the incremental profits with them. 1 Compared to aOBCs, providers adopt responsibility for more operational tasks in eOBCs and deliver an outcome that is directly relevant to the customer’s bottom line.

All forms of OBCs are likely to have their specific benefits and risks; and despite the alignment of interest, customer and supplier firms might differ substantially in their views on the benefits and risks associated with OBCs. Typically, OBCs tend to imply a shift of risk away from the buyer toward the seller (Selviaridis and Wynstra, 2015). To date, however, empirical research has not yet provided a finer-grained view on the bright and dark sides of OBCs from both the customers’ and the suppliers’ perspective. Developing a better understanding of the benefits and risks associated with outcome-based contracting is a key factor to enhancing its effective implementation and identifying situations where it is most likely to lead to favourable results for both contracting partners.

Against this background, our aim is threefold: first, we want to shed light on the benefits, risks, and overall performance of OBCs with payments based on availability versus economic results. Identifying and selecting the right payment model is an issue of high managerial importance because it determines how the ‘value pie’ (Jap, 2001) is shared between the contracting partners; second, we differentiate between the customers’ and the suppliers’ perspective. Understanding both views, their commonalities and differences, is essential for a better understanding of OBCs, and how they are best managed; and third, our study considers two contextual boundary conditions that impact the benefits and risks of OBCs. More specifically, we investigate how product innovativeness (internal environment) and technological turbulence (external environment) moderate the generation of benefits and risks with OBCs. In sum, our research contributes an empirical, multi-contextual perspective to the extant literature on outcome-based contracting that is still dominated by conceptual and analytical research.

Literature review

As it currently stands, the insights on OBCs – and contracting for services in the more general sense – are mainly derived from conceptual and theoretical approaches (Ng and Nudurupati, 2010). In particular, a substantial body of work draws on formalized analytical models (e.g., Kim et al., 2007, 2010; Mirzahosseinian and Piplani, 2011; Roels et al., 2010). More specifically, Roels et al. (2010) show that performance-based contracts are preferable in cases in which an output is equally dependent on the input provided by the buyer and the seller. While the conceptual and theoretical approaches have provided important insights and foundations for future study, there is a dearth of empirical work providing insights on OBCs in practice.

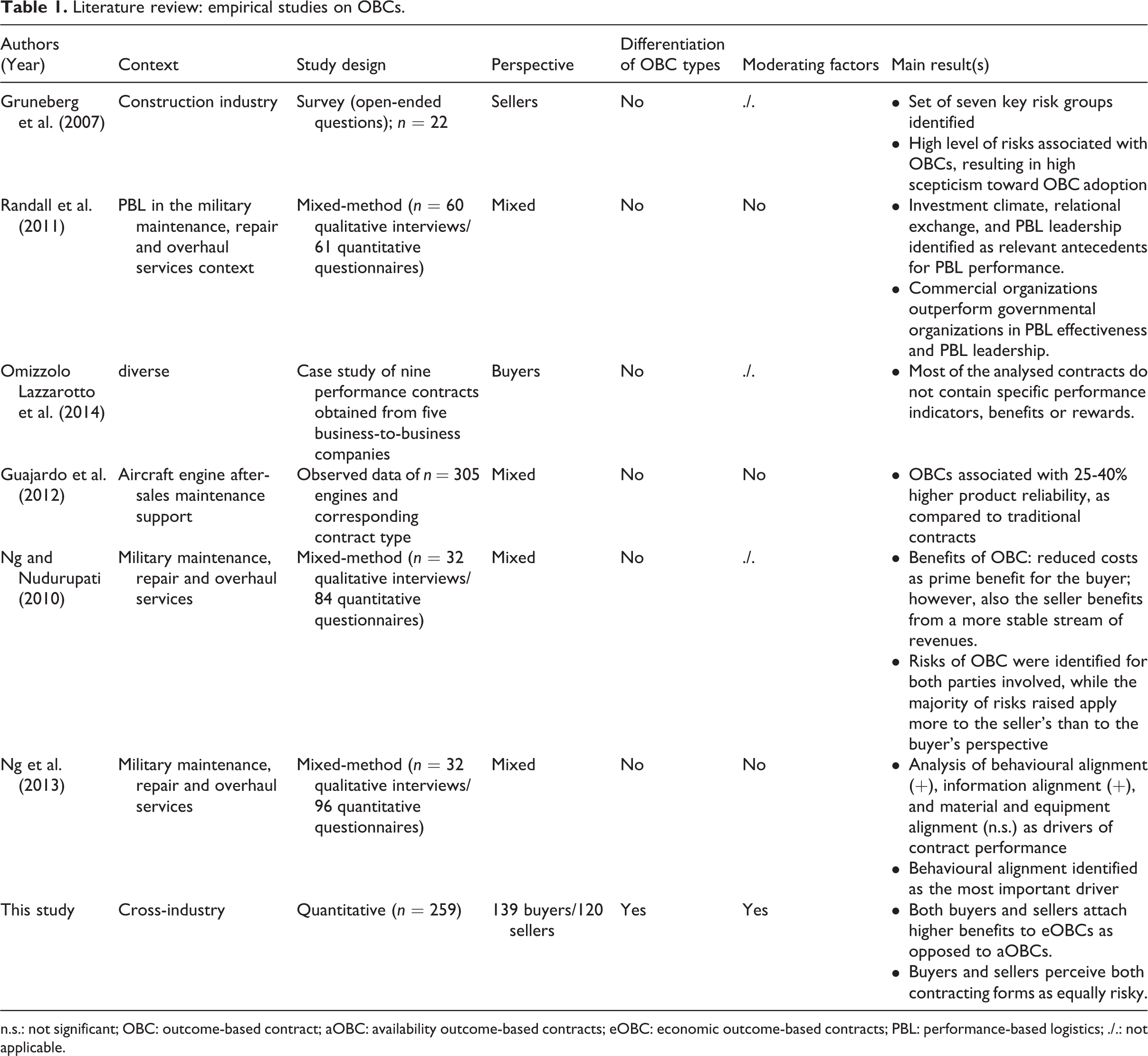

The empirical studies that exist, have investigated the effects stemming from the use of OBCs on perceived or observed outcome variables. Table 1 summarizes the state of knowledge derived from these empirical studies on OBCs.

Literature review: empirical studies on OBCs.

n.s.: not significant; OBC: outcome-based contract; aOBC: availability outcome-based contracts; eOBC: economic outcome-based contracts; PBL: performance-based logistics; ./.: not applicable.

Two empirical studies have looked at effects of OBCs in comparison to more traditional contracting forms. Specifically, Randall et al. (2011) have compared performance evaluations of 61 managers involved in outcome-based contracting in the military maintenance, repair and overhaul services context. Following their results, OBCs are superior to traditional post-production support approaches with regard to nearly all of 42 performance items assessed. Drawing on observable data of 305 Rolls-Royce aircraft engines, Guajardo et al. (2012) have shown that the use of OBCs is associated with a 25–40% increase in product reliability, as compared to after-sales services which are based on input-based contracting forms (IBCs; i.e., time and material-based contracts).

Other authors have investigated the role of contractual, relational, or other types of antecedents on performance in ‘pure’ OBC contexts; for example, Ng et al. (2013) employ a mixed-method design to investigate the role of relational assets, namely value-driven alignments – that is, the level of perceived alignment of behavioural, information-related, and material- and equipment-related processes between the two partnering firms – and partnership inputs, on OBC performance as perceived by employees delivering on the contract. Results obtained from a partial least squares regression model based on 96 questionnaires indicate that performance of OBCs is significantly impacted by behavioural and information alignment, whereas material and equipment alignment was not found to exert an effect (Ng et al., 2013). Similarly, Omizzolo Lazzarotto et al. (2014) have looked at management practices used in the context of nine OBCs implemented across five firms in different business-business (B2B) settings. Their interview findings reveal a substantial amount of variance in contract and relationship performance, and tentatively support the importance of formal and informal coordination mechanisms between partners. The latter finding is mirrored in the study by Randall et al. (2011), who – in addition to a supportive investment climate and OBC-oriented leadership – similarly emphasize the key role of relational exchange for effective OBC implementation.

Our review of empirical studies shows that the majority of empirical studies in this area draw on case study approaches or on relatively small sample sizes. To the best of our knowledge, there is only one notable exception employing a larger sample and a more robust methodology (i.e., Guajardo et al., 2012). Moreover, while OBCs are becoming relevant in a growing number of industries, empirical insights lack generalizability, given the data collected are limited to a few specific contextual settings – with the military sector playing the predominant role.

From a content perspective, there are hardly any reliable findings on OBC-related benefits and risks as being perceived from the predominant parties involved, namely buyers and sellers. Existing findings in this area are at best inconclusive. On the one hand, conceptual work suggests that OBCs are beneficial for both the buyer and the seller (for a review see Holmbom et al., 2014). On the other hand, some studies seem to reveal that the majority of risks apply more to the seller’s than to the buyer’s side (Gruneberg et al., 2007; Ng and Nudurupati, 2010). These studies, however, are either limited to the perspective of one of the two parties involved, or do not specifically disclose to which extent benefits and risks are relevant for the buyers and sellers.

Against this background, our study aims to shed light on the benefits and risks of two types of OBCs – namely eOBCs and aOBCs – as perceived by both the buyers and sellers. In addition, addressing the issue of generalizability, we investigate boundary conditions that impact the benefits and risks related to the utilization of the two OBC types.

Conceptual model and hypotheses

Model overview

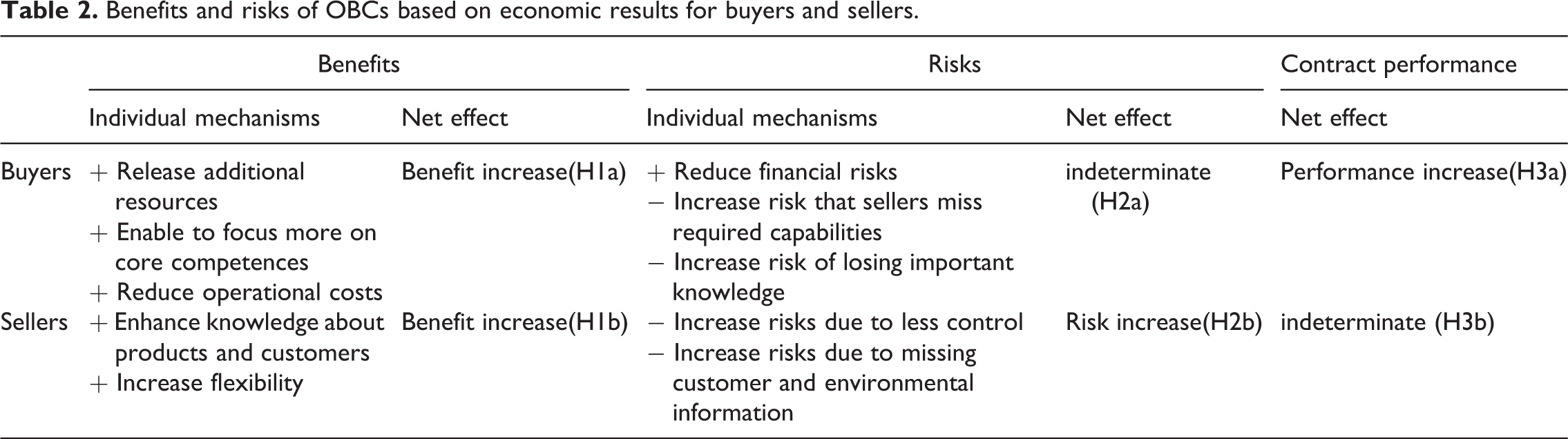

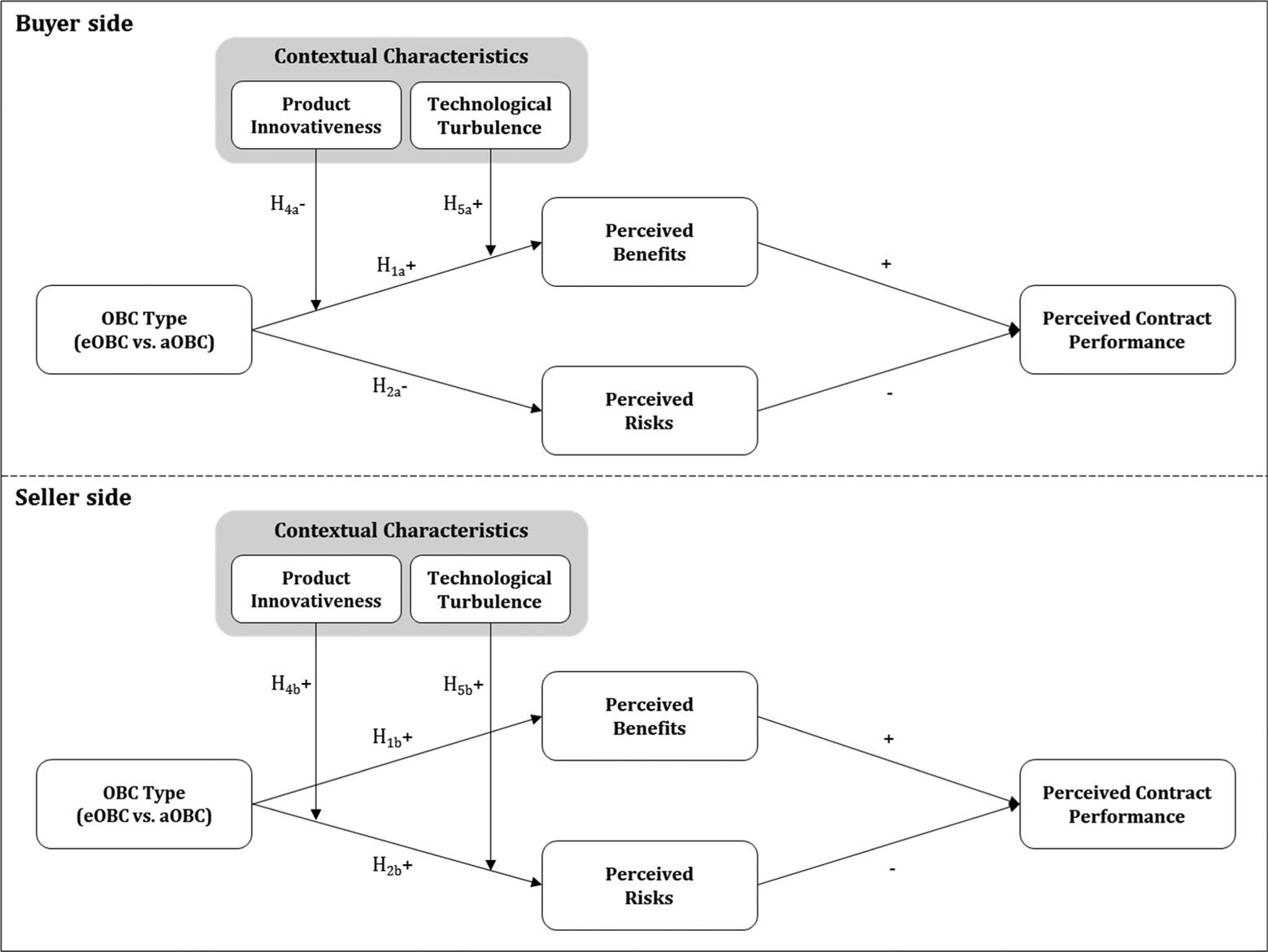

In this section, we develop our conceptual model, which captures the effect of eOBCs versus aOBCs on contract performance. To do so, we theoretically link eOBCs to buyers’ and sellers’ perceived benefits and risks as well as contract performance. Table 2 gives an overview about the different benefits and risks of eOBCs for buyers and sellers and depicts the hypothesized main effects for both parties. In a second step, we investigate the moderating impact of two environmental characteristics. Figure 1 depicts our conceptual model.

Benefits and risks of OBCs based on economic results for buyers and sellers.

Conceptual model. OBC: outcome-based contract; aOBC: availability outcome-based contracts; eOBC: economic outcome-based contracts.

Main effects of OBCs on buyers and sellers

From a theoretical perspective, performance implications resulting from the use of eOBCs versus aOBCs can be explained drawing on transaction cost (TC) theory (Coase, 1937; Williamson, 1975, 1985, 1996). Having emerged as one of the most fundamental theoretical approaches toward explaining B2B exchange relationships (Rindfleisch et al., 2010), TC theory argues that different institutional arrangements of organizing economic exchange correspond with different levels of production and transaction costs, with the latter referring to all ex ante and ex post costs related to organizing the exchange (Rindfleisch and Heide, 1997). Thereby, what makes TC theory particularly relevant to the context of this study is the emphasis on asset specificity and uncertainty as the two main characteristics of transactions, as well as the acknowledgement of the potential of opportunistic behaviour of the exchange partners.

With an eOBC, sellers take over a substantial part of buyers’ operations, that is, they not only maintain the machinery and equipment but also take over operational tasks and provide the machinery output (Hypko et al., 2010). This reduces overall production costs, as sellers – given their experience in delivering the outcome and economies of scale and leverage – will likely perform activities even more effectively and efficiently (Miller et al., 2002; for a similar argumentation in the context of outsourcing see Cheon et al., 1995). More specifically, when operating machinery or equipment for their buyers instead of just maintaining or repairing it, sellers gain in-depth knowledge about the performance of their products and their customers’ business processes (Ulaga and Reinartz, 2011); knowledge that they can use to further improve their offerings and strengthen customer relationships (Miller et al., 2002). Moreover, eOBCs provide sellers with more flexibility regarding the extent and the timing of their efforts (Holbom et al., 2014), thereby allowing them to optimize operational costs. In addition, the shift in operational responsibilities releases additional resources on the buyer’s side, allowing them to focus on their core competences (Holbom et al., 2014).

With regard to transaction costs, eOBCs as compared to aOBCs are characterized by ceteris paribus (c. p.) higher levels of asset specificity, which should in turn increase the potential of opportunistic behaviours. Using eOBCs as a governing mechanism, however, the theoretically predicted issue of increasing monitoring costs can be meaningfully addressed by defining outcomes in economic terms. In so far, a near-to-perfect alignment of incentive structures can be achieved when following eOBC as compared to aOBC logic.

In sum, we expect that buyers and sellers both attach higher benefits to eOBCs compared to aOBCs. H1a: Buyers’ perceived benefits will be higher for OBCs based on economic results compared to OBCs based on availability. H1b: Sellers’ perceived benefits will be higher for OBCs based on economic results compared to OBCs based on availability.

The effect of eOBCs (versus aOBCs) on perceived risks should be different for buyers and sellers. From a buyers’ perspective, it can – corresponding to the operational costs benefits outlined above – be argued that eOBCs should have opposing effects on perceived risks. As the seller takes over the responsibility for a larger part of the client’s value chain, eOBCs will reduce customers’ financial risks due to downtimes, overcapacity or ineffective and inefficient operation (Hypko et al., 2010). On the other hand, related to the c. p. higher level of asset specificity, eOBCs also come with the risk of losing important knowledge and becoming dependent on the seller, which is even more profound when entire operational processes are concerned (Holbom et al., 2014). In addition, eOBCs accompany the risk that sellers miss the capability to deliver the outcome, as they might lack the required knowledge regarding customers’ business processes (Hypko et al., 2010). Because of these opposing effects, we argue that buyers perceive eOBCs and aOBCs as equally risky.

In contrast, sellers might perceive higher risks when using eOBCs as opposed to aOBCs, because with eOBCs responsibility for entire customer activities is transferred from the customer to the supplier. This creates considerable risks for the supplier for three reasons: first, the outcome of the activity is heavily influenced by customer behaviours (e.g., customer utilization), which are often not controllable by the seller and subject to moral hazard (Guajardo et al., 2012); second, fulfilling results-based promises demands in-depth knowledge about customers’ business processes and not just the product itself. However, oftentimes, customers are not willing or able to share the information required to successfully perform the activity (Tuli et al., 2007); and third, with eOBCs in particular, sellers run the risk of not accurately assessing the costs involved in delivering the outcome, especially because they lack important information on economic developments (Holbom et al., 2014). Market dynamics and volatility may drive fundamental shifts in requirements and market capabilities, resulting in changes to buyer demands or expectations. Thus, we hypothesize a positive effect of eOBCs (versus aOBCs) on perceived risks for sellers. H2a: Buyers’ perceived risks will be equal for OBCs based on economic results and OBCs based on availability. H2b: Sellers’ perceived risks will be higher for OBCs based on economic results compared to OBCs based on availability.

We also assume differential effects of eOBCs (versus aOBCs) on buyers’ and sellers’ perceived contract performance. For buyers, eOBCs should have a positive effect on their perceived contract performance compared to aOBCs, mediated by their perceived benefits. Buyers can better focus on their core competences when sellers adopt more responsibilities for operational tasks and provide monetary output, thereby profiting from sellers’ economies of scale and scope. When buyers perceive eOBCs as more beneficial and equally risky compared to aOBCs, this in turn should enhance their relative performance.

In contrast, we do not assume an effect of eOBCs on contract performance for sellers. For sellers eOBCs accompany more benefits, but at the same time also involve more risks. Overall, we therefore assume that sellers perceive eOBCs and aOBCs as equally attractive. H3a: Buyers’ perceived contract performance will be higher for OBCs based on economic results compared to OBCs based on availability. This relationship is mediated by their perceived benefits. H3b: Sellers’ perceived contract performance will be equal for OBCs based on economic results and OBCs based on availability.

Moderating effects of context characteristics

Acknowledging that any economic exchange is embedded in a contextual surrounding, the description of transactions with contextual variables is at the core of TC theory. A company’s contextual situation can be characterized by both its internal (e.g., product characteristics) and external (e.g., industry characteristics) environment (Ekeledo and Sivakumar, 1998). We focus on two context factors that likely influence the outcomes of OBCs for buyers and sellers: product innovativeness (internal environment); and technical turbulence (external environment).

Product innovativeness

Product innovativeness captures the degree of newness of a seller’s overall product portfolio (Stock and Reiferscheid, 2014). From the customers’ point of view, product innovativeness might decrease sellers’ perceived ability to successfully reduce operational costs for them, preventing to capitalize on the benefits theoretically derived via the transaction cost framework to a full extent. When the underlying products are highly innovative, sellers are supposed to have less experience with deploying them in customers’ specific business processes and delivering the desired outcome. In particular, lack of experience with deploying an innovative product results in lower economies of scale and leverage that the seller can reap compared to a situation where the seller has accumulated substantial experience with an established product. This is especially true for eOBCs where the seller takes over more operational tasks compared to aOBCs. eOBCs demand not only in-depth knowledge about the product itself but also the products’ performance in the customers’ processes. Hence, we assume that product innovativeness will mitigate the perceived benefits of eOBCs for buyers. H4a: Product innovativeness negatively moderates the relationship between eOBC (versus aOBC) and buyers’ perceived benefits.

For sellers we assume higher risks for eOBCs when product innovativeness is high. When the products involved are highly innovative, eOBCs will be very complex and involve high uncertainty, thereby increasing the risks for the seller. With regard to environmental uncertainty, TC theory argues that changing environments lead to difficulties in adaptation, which in turn increases transaction costs as contractual agreements have to be amended and renegotiated (Rindfleisch and Heide, 1997). A similar mechanism can be assumed to be in place when product innovativeness is high: a high degree of product innovativeness, likewise, poses a challenge to sellers with regard to being able to effectively implement and efficiently operate complex industrial offerings. This can be explained by increasing transaction costs, related to the need for more frequent and/or more extensive customer adaptation and testing to realize economic opportunities, thereby c. p. increasing the risks for the seller. Thus: H4b: Product innovativeness positively moderates the relationship between eOBC (versus aOBC) and sellers’ perceived risks.

Technological turbulence

Technological turbulence refers to the rate of technological change in a market (Jaworski and Kohli, 1993). Markets with high technological turbulence require buyers and sellers to keep up with the changing environment by constantly developing new knowledge and competences (Stock and Zacharias, 2011). For buyers, technological turbulence should amplify the effect of eOBCs on perceived benefits. When technological turbulence is high, buyers will find it difficult to keep up with the technological developments in their non-core markets. Staying up-to-date in these markets would take up too many resources and would prevent them from focusing on their core competences. In line with the TC framework, from a buyer’s perspective it seems thus even more reasonable to outsource entire activities to suppliers, in order to minimize production costs (Cheon et al., 1995). While the TC framework furthermore suggests that externalizing activities corresponds with an increase in monitoring costs, eOBCs – via their capability to align interests of both parties involved – are assumed to provide an effective safeguard against opportunistic behaviours in which sellers might engage.

Summarizing these arguments, it is assumed that technological turbulence will reinforce the benefits associated with eOBCs as compared to aOBCs. H5a: Technological turbulence positively moderates the relationship between eOBCs (versus aOBCs) and buyer’s perceived benefits.

For sellers, technological turbulence is assumed to increase the perceived risks associated with eOBCs. When technological turbulence is high, it is more difficult to accurately assess the risks and costs involved in delivering economic results for their buyers (Hypko et al., 2010). In turn, the uncertainty about future states that characterizes turbulent industries will transfer a larger amount of risk to the supplier when using eOBCs. From a theoretical perspective, this assumption is supported by the adaptation challenge stemming from volatile environments (Rindfleisch and Heide, 1997). Similar to the case of product innovativeness, rapidly changing technological developments correspond with a need to quickly adopt one’s offerings, c. p. increasing transaction costs and enhancing perceived risks. We therefore expect that eOBCs with high technological turbulence results in higher levels of perceived risk for sellers and hypothesize: H5b: Technological turbulence positively moderates the relationship between eOBCs (versus aOBCs) and sellers’ perceived risks.

Research design and empirical results

Data collection, sample and measurement

Data collection and sample

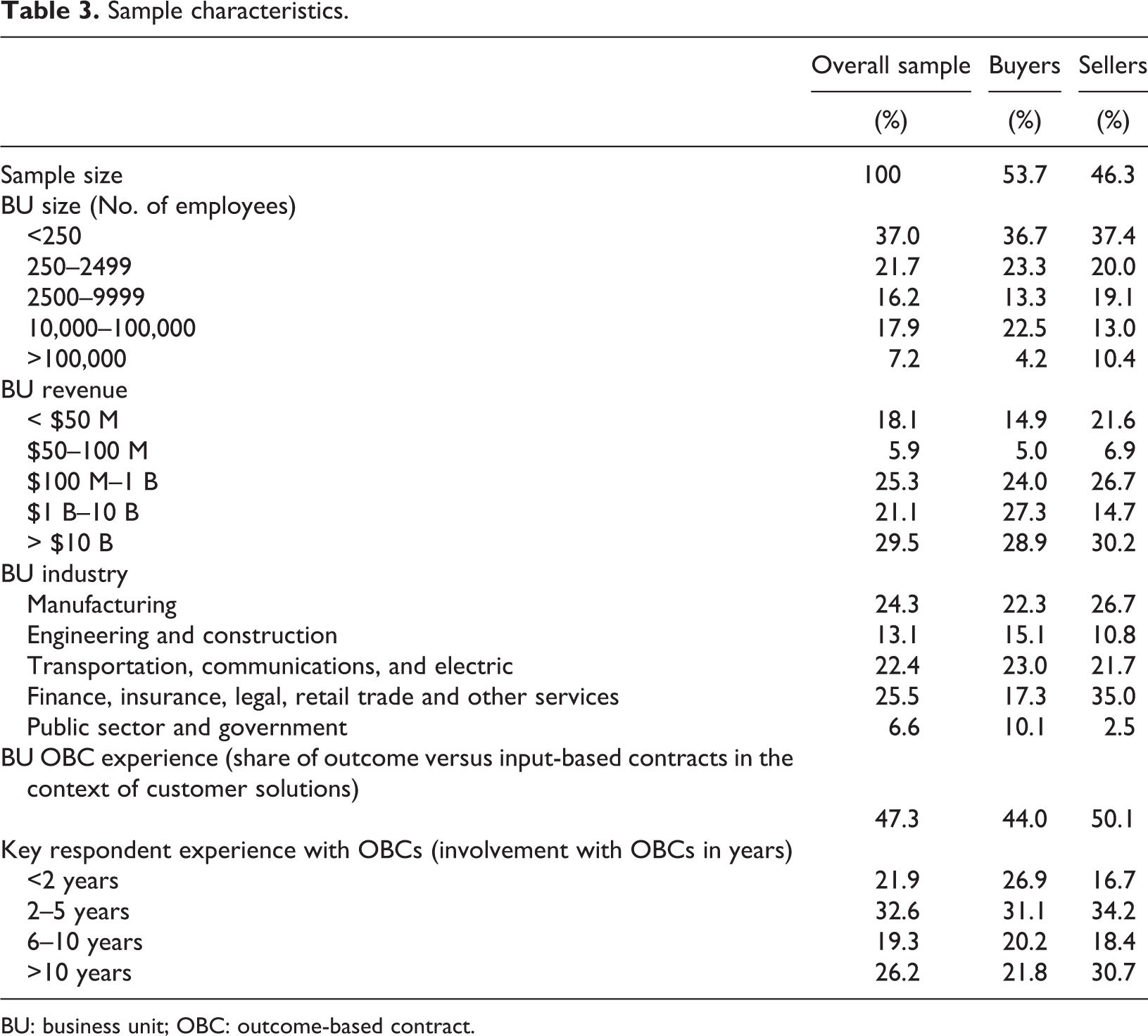

To empirically test our model we collected data by distributing a standardized online survey to the member organizations of a global, independent contracting association, the International Association for Contract and Commercial Management (IACCM). To ensure a high level of generalizability of the findings, IACCM was regarded as a particularly suitable partner due to its diverse membership base. A summary presentation of the major findings of the study was offered to respondents in order to incentivize participation. After having eliminated four cases due to inconclusive answering patterns, a total of 259 complete questionnaires were included in the analysis. The sample covers a broad range of industries, with the majority of respondents coming from manufacturing, transportation, communications and electronics, as well as finance, insurance, legal, retail trade and other services sectors (Table 3).

Sample characteristics.

BU: business unit; OBC: outcome-based contract.

Before starting the questionnaire a brief description of complex industrial services and OBCs was provided to the participants. 2 Participants were subsequently asked to indicate the perspective from which they are usually involved in outcome-based contracting activities within their organization. This not only ensured that both buyers and sellers were surveyed, but also filtered out respondents that have no knowledge or history of using OBCs. Of the 259 respondents, 139 (53.7%) answered the questionnaire from the perspective of the buyer of OBCs (i.e., the respondent was involved in sourcing industrial services from suppliers). The remaining 120 (46.3%) were involved in outcome-based contracting from the seller side (i.e., their organizations acted as providers of industrial services). Based on the perspective indicated, respondents were subsequently routed to two specific versions of the questionnaire. Those two versions took account of the particular perspective of the respondent, but were otherwise identical. Finally, participants were screened based on their firm’s share of OBCs versus IBCs to make sure that all participants have at least some experience with OBCs.

Measurement

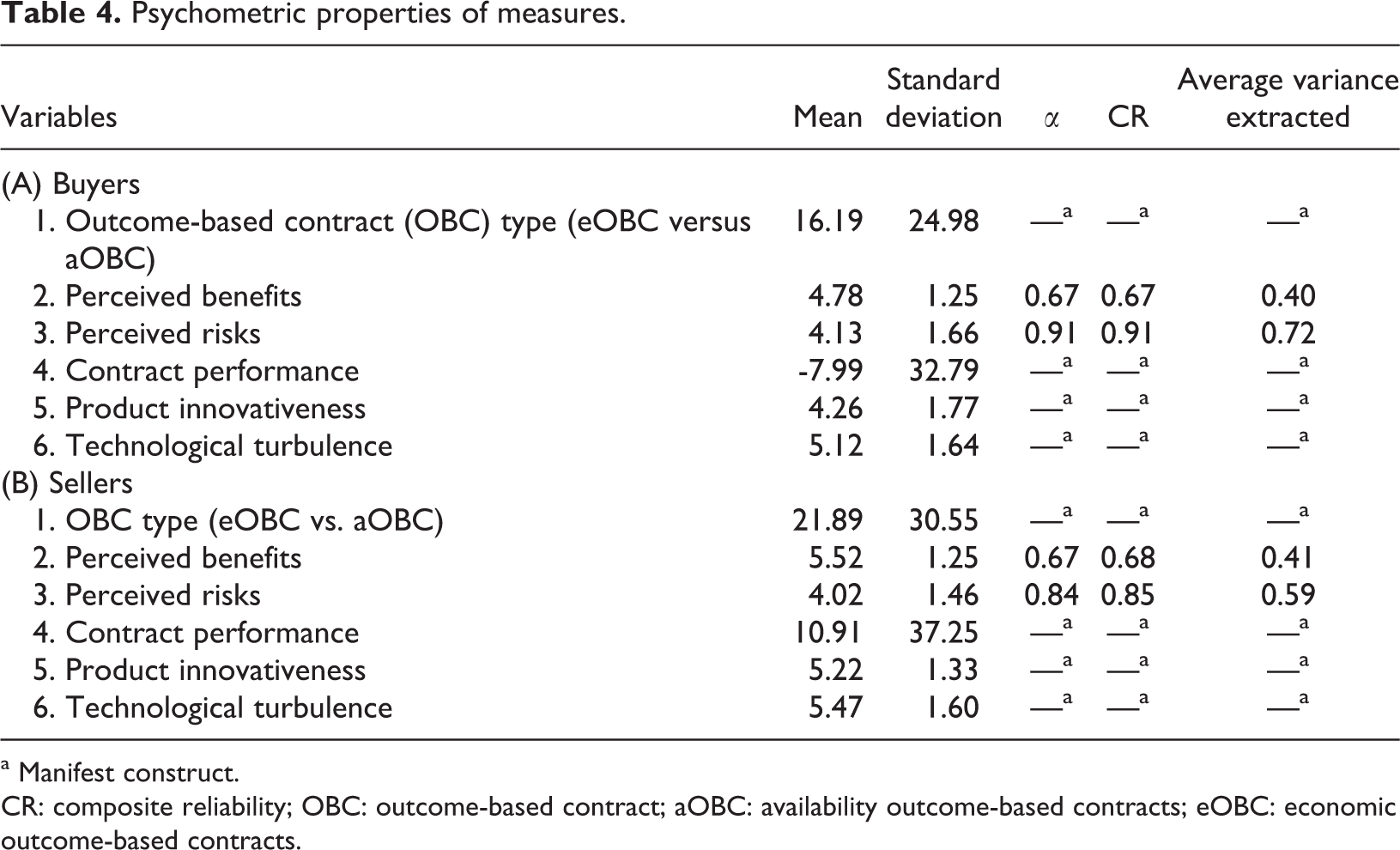

To capture OBC types, respondents were asked to characterize their business units’ portfolio of current OBC contracts with regard to different payment models by allocating percentage values to the two different payment models (i.e., OBCs based on customers’ economic results and OBCs based on availability). We utilized the relative percentage allocated to eOBCs (versus aOBCs) as our independent variable. Benefits as well as risks related to the utilization of OBCs were assessed using multi-item measures. In case of perceived benefits, this measure includes major benefit facets, for example, increased flexibility (Mirzahosseinian and Piplani, 2011), concentration on core tasks (Holbom et al., 2014; Miller et al., 2002), and cost reduction (Ng and Nudurupati, 2010). Our risk measure encompasses uncertainty, for example, due to unclear outcome, process, or costs, as well as loss of control (Ng and Nudurupati, 2010). To capture our dependent variable contract performance, respondents indicated the share of contracts with above average performance. Context characteristics were measured using single item scales for product innovativeness (‘Our products/services are highly innovative’; Homburg and Stock, 2004), and technological turbulence (‘The technology in our industry is changing rapidly’; Jaworski and Kohli, 1993). All measures were obtained using Likert scales ranging from 1 (= totally disagree) to 7 (= totally agree). Tables 3, 4, and 5 summarize sample characteristics, descriptive statistics and psychometric properties of our measures.

Psychometric properties of measures.

a Manifest construct.

CR: composite reliability; OBC: outcome-based contract; aOBC: availability outcome-based contracts; eOBC: economic outcome-based contracts.

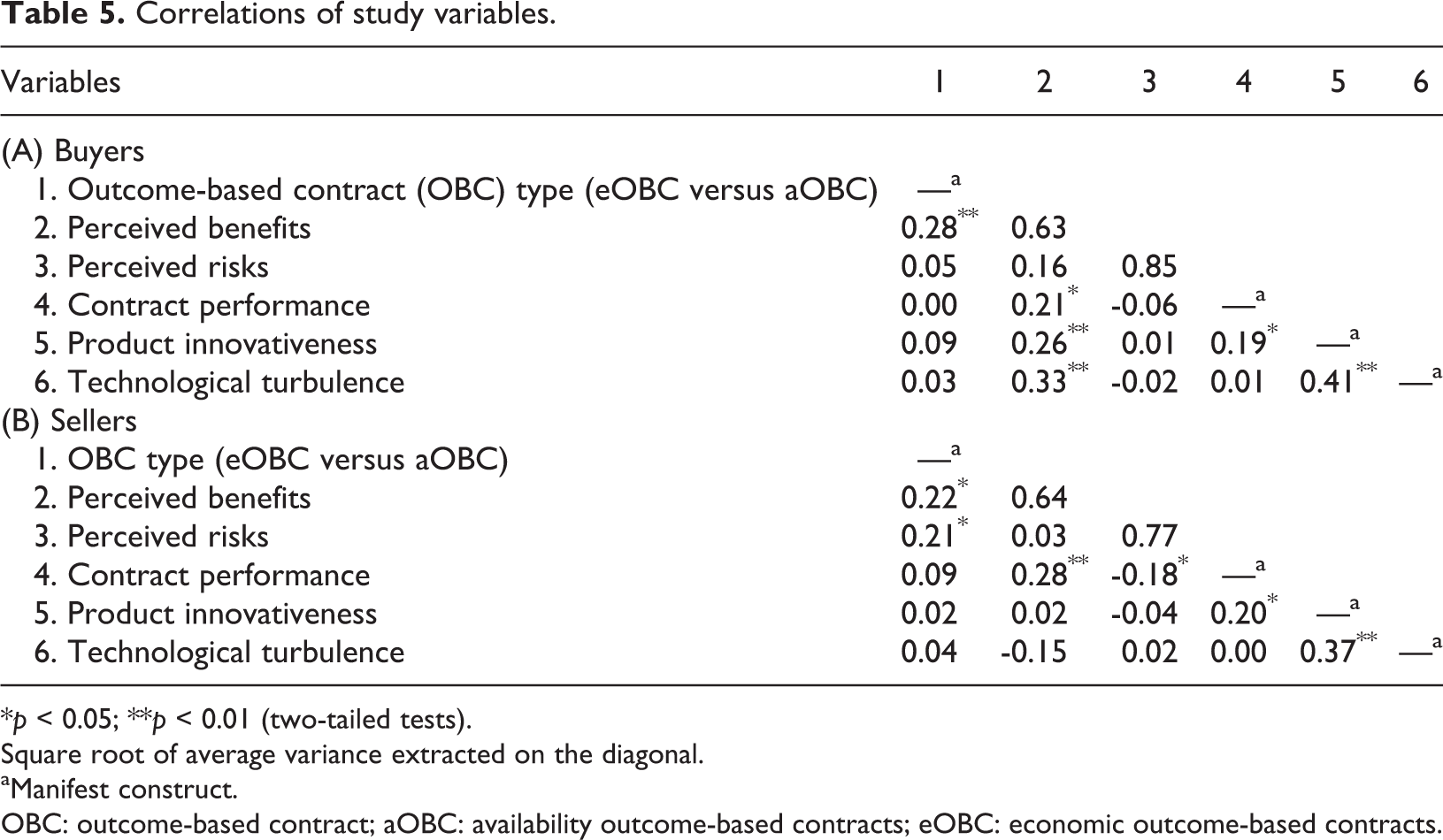

Correlations of study variables.

*p < 0.05; **p < 0.01 (two-tailed tests).

Square root of average variance extracted on the diagonal.

aManifest construct.

OBC: outcome-based contract; aOBC: availability outcome-based contracts; eOBC: economic outcome-based contracts.

Common method variance

As all measures were collected from a single source, we assessed common method variance using the Harman single factor test which is one of the most widely used techniques to address the issue of common method variance (Podsakoff et al., 2003). For this test, the researcher loads all variables into an exploratory factor analysis and determines the number of factors that emerges. ‘The basic assumption of this technique is that if a substantial amount of common method variance is present, either (a) a single factor will emerge from the factor analysis or (b) one general factor will account for the majority of the covariance among the measures’ (Podsakoff et al., 2003: 889). In our exploratory factor analysis, three factors emerged and the first factor explained less than half (27.37%) of the observed variance, indicating that common method variance poses no serious threat to our analysis. In addition, a confirmatory factor analysis with a single factor showed a very poor fit (CFI = 0.403; TLI = 0.360; RMSEA = 0.122), providing further evidence for the absence of common method variance.

Results

Main effects of OBCs on buyers and sellers

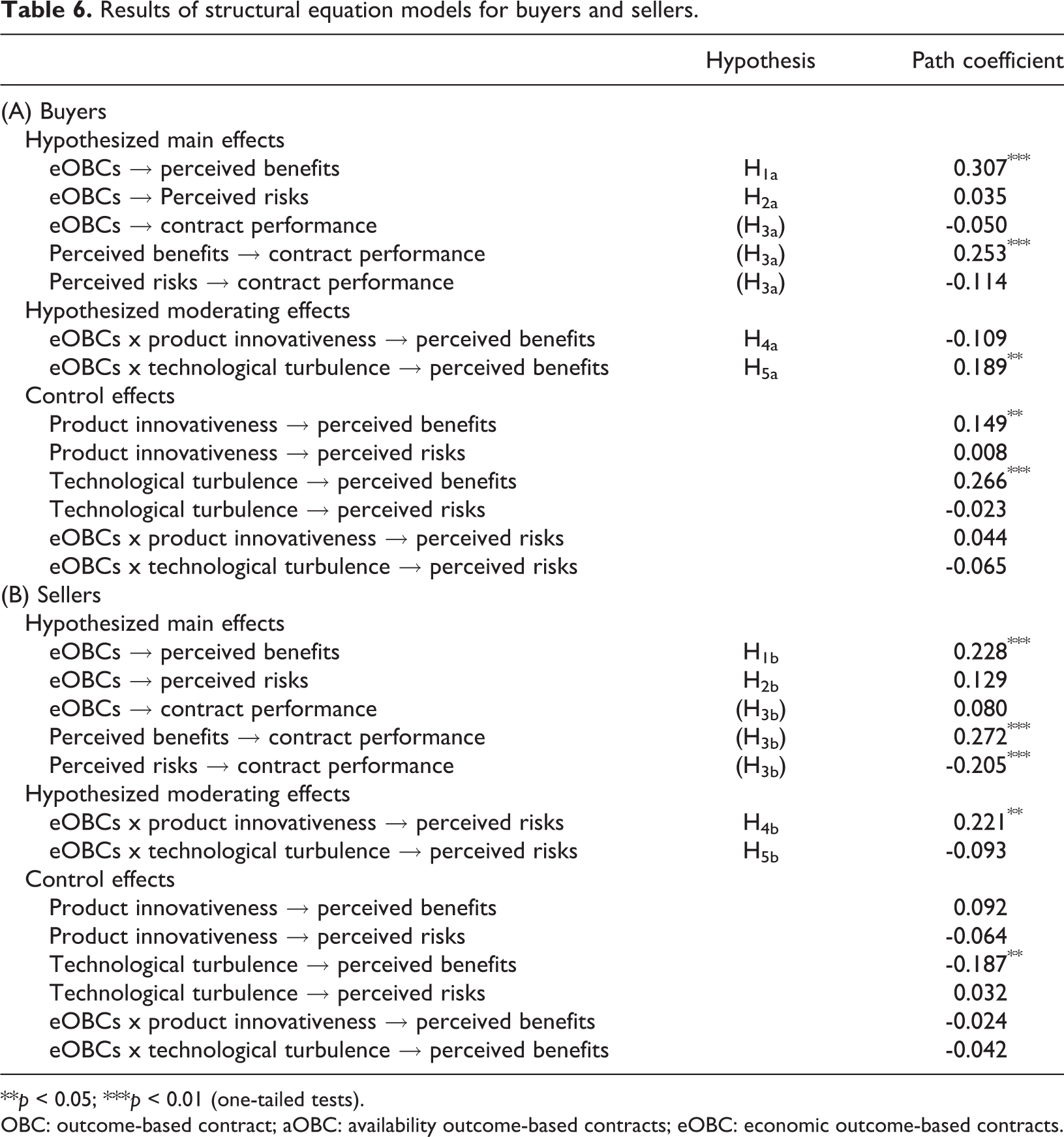

We employed structural equation modelling (SEM) using Mplus 7 (Muthén and Muthén, 1998–2012) to test our hypotheses for buyers and sellers. SEM is a popular statistical tool that has been adopted across different disciplines such as strategic management, human resource, and marketing research. Compared to more traditional regression analyses, SEM allows for the simultaneous estimation of several interconnected hypotheses representing chains of cause and effect within a single analytical framework. SEM has been found to provide more reliable and valid results than other multivariate techniques (Cheng, 2001) and it has then been advocated because it can expand the explanatory ability and statistical efficiency for model testing with a single comprehensive method (Hair et al., 2010).

Initially we analyzed the consequences of eOBCs (versus aOBCs) for buyers (see Table 6, Panel A). In line with H1a, we found a significant, positive effect of eOBCs on buyers’ perceived benefits (0.307; p < 0.01); that is, buyers perceive the contract as more beneficial when it is based on economic results than when it is based on availability. In line with H2a, we found no significant effect of eOBCs on buyers’ perceived risks (0.035; p > 0.05). Consequently, buyers attach similar risks to both, OBCs based on economic results and OBCs based on availability. We could not confirm the positive total effect of eOBCs on contract performance hypothesized in H3a (0.024; p > 0.05). Hence, on average, buyers perceive OBCs based on economic results and OBCs based on availability as performing equally well.

Results of structural equation models for buyers and sellers.

**p < 0.05; ***p < 0.01 (one-tailed tests).

OBC: outcome-based contract; aOBC: availability outcome-based contracts; eOBC: economic outcome-based contracts.

We then examined the consequences of eOBCs (versus aOBCs) for sellers (see Table 6, Panel B). In line with H1b, we can confirm the positive effect of eOBCs on perceived benefits for sellers (0.228; p < 0.01). Thus, buyers and sellers both perceive OBCs as more beneficial when they are based on economic results compared to availability. In contrast to H2b, the results do not support a positive effect of eOBCs on perceived risks (0.129; p > 0.05). Accordingly, sellers do not perceive higher risks when OBCs are based on economic results. In line with our assumption (H3b), we did not find an overall effect of eOBCs on contract performance for sellers (0.115; p > 0.05), leading us to conclude that the benefits and risks attached to eOBCs cancel each other out. Thus, overall, sellers perceive OBCs based on economic results and availability as equally attractive.

Moderating effects of context characteristics

As, on average, buyers and sellers perceive eOBCs and aOBCs as equally attractive, it seems worthwhile looking at the context characteristics that reinforce the differences between contract types. Here, we again find differential effects for buyers and sellers. For buyers, our results do not support a negative moderating effect of product innovativeness on the benefits of eOBCs (-0.109; p > 0.05), as stated in H4a. In contrast, we could confirm the positive interaction effect of technological turbulence and eOBCs on perceived benefits (0.189; p < 0.05), as hypothesized in H5a. Therefore, buyers perceive eOBCs as more beneficial compared to aOBCs when technological turbulence is high.

For sellers, we could confirm the positive moderating effect of product innovativeness on the link between eOBCs and perceived risks (0.221; p < 0.05), supporting H4b. With regard to technological turbulence, we found no moderating effect on the risk outcomes of eOBCs for sellers (-0.093; p > 0.05), thereby contrasting H5b. Thus, for sellers, eOBCs are more likely to pay off if product innovativeness is low, while the degree of technological turbulence does not make a difference to them.

Discussion

Theoretical and managerial contributions

This study makes several contributions to the academic literature and managerial practice. First, we shed light on the particular effects of OBCs from both the buyers’ and the sellers’ perspectives. Previous studies focused on one of the two exchange partners (e.g., Gruneberg et al., 2007; Omizzolo Lazzarotto et al., 2014), or have looked at OBCs from a more general perspective (e.g., Randall et al., 2011), without taking into consideration the individual views of buyers and sellers. Differentiating between the two views, thereby, seems particularly useful in light of the propositions of TC theory, suggesting different effects of the use of aOBCs versus eOBCs for buyers and sellers. Interestingly, while both OBC types were found to correspond to similar levels of overall risks and benefits, buyers and sellers do differ in their perception of OBCs under contingent conditions, as shown by the results of our moderator analysis.

Second, our study explores differences between OBC types. Although previous research acknowledges different OBC types (e.g., Holmbom et al., 2014), and practice does make extensive use of both types, researchers have not yet investigated their differential outcomes. Here, our study shows that buyers and sellers both attach higher benefits to eOBCs as opposed to aOBCs. An interesting finding relates to the levels of risk associated with an increasing use of eOBCs: here, based on the notion that OBCs tend to shift risks towards the seller, it was hypothesized that eOBCs should further reinforce this tendency (Hypko et al., 2010; Selviaridis and Wynstra, 2015). Our results, however, suggest that sellers do on average not perceive eOBCs as more risky in comparison to aOBCs. In so far, increasing responsibilities for more operational tasks and higher levels of asset specificity associated with eOBCs seem to not necessarily come at the costs of increasing levels of risks for sellers, but are merely associated with higher perceived benefits – at least from the perspective of an ‘average’ seller.

In sum, as indicated by the non-significant total effects of eOBCs versus aOBCs, both forms of OBCs were found to perform equally well, both from the buyer and the seller perspective. However, once we consider context characteristics, one of the two contract forms emerges as being superior to the other, which leads us to the third contribution of this study.

Finally, we consider two important context characteristics that impact the effectiveness of OBCs, that is, product innovativeness and technological turbulence. When technological turbulence is high, buyers perceive significantly more benefits, making eOBCs more attractive from the buyer’s perspective. Given that the hypothesized corresponding risk-increasing effect from the seller’s perspective (H5b) was found to be non-existent, these findings suggest that eOBCs should be chosen as the preferred option in technologically turbulent markets. It thus seems that sellers can most effectively capitalize on their comparably better capabilities with regard to operating the systems and services they provide in highly turbulent markets. In contrast, when product innovativeness is high, aOBCs emerge as the better option. Here, while no differences with regard to perceived benefits from the buyer’s perspective were found, sellers associate higher risks with eOBCs as compared to aOBCs. A reason for this might be that in case of highly innovative products, sellers’ internal capabilities are yet on the rise, as they themselves might still learn and experiment with ways of increasing operational efficiencies of their innovative offerings.

From a theoretical angle, both product innovativeness and technological turbulence can be assumed to contribute to volatility, bringing about the need for re-arrangements and adaptation of existing contractual terms (Rindfleisch and Heide, 1997). The results of the empirical analysis show that both factors have fundamentally different impacts on the benefits and risks perceived by each of the contractual partners. In particular, advantages of the use of a particular contractual arrangement for one exchange partner do not necessarily lead to disadvantages for the other one. With regard to generally advancing TC theory arguments, this highlights our study’s contribution with regard to the recently formulated need for ‘fine tuning this important theory to meet B2B’s new contextual realities’ (Rindfleisch et al., 2010: 212).

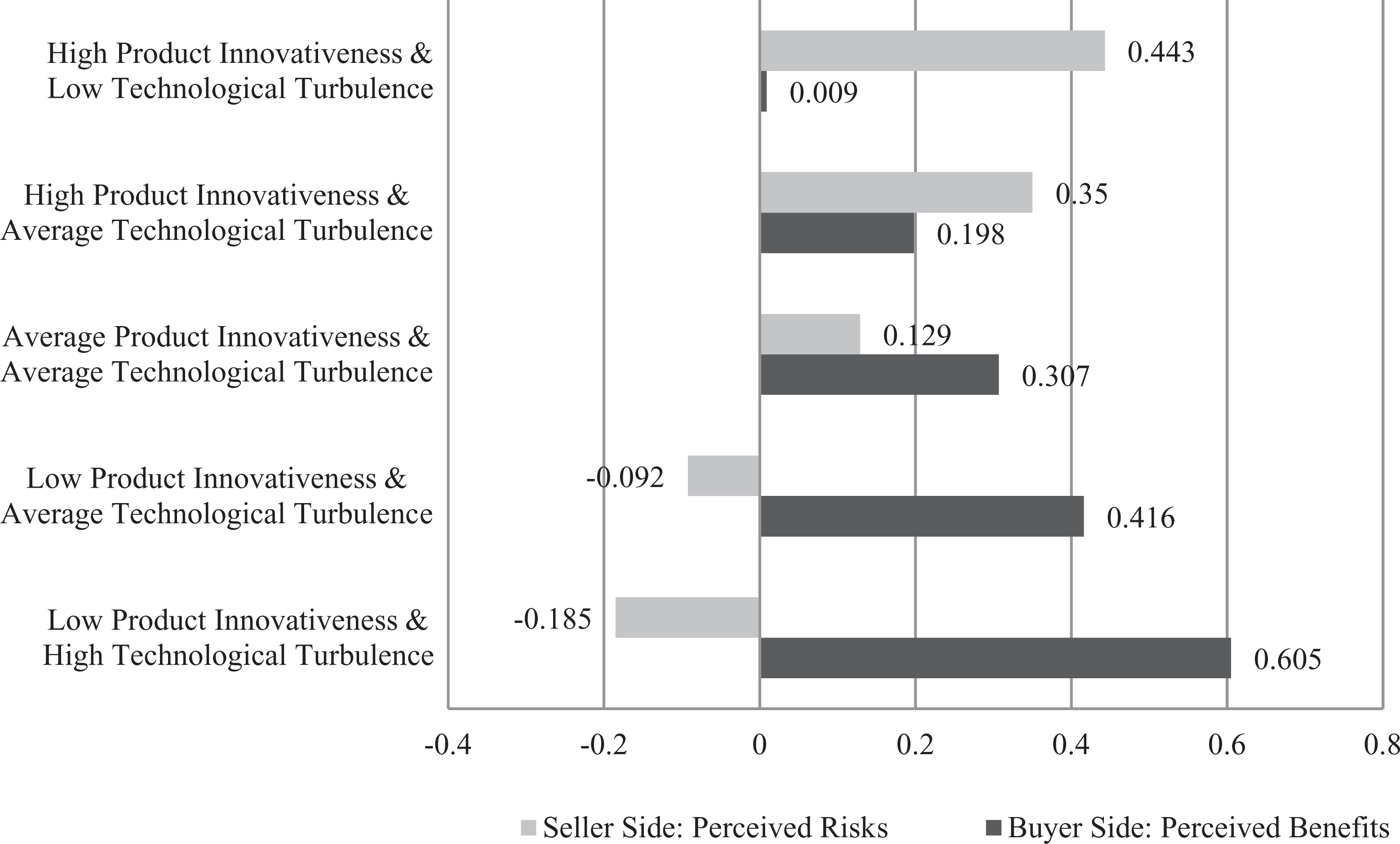

With regard to management practice in the context of outcome-based contracting, the findings of this study help managers to better decide which type of OBC promises to be most beneficial under the given contextual conditions. To illustrate the role of product innovativeness and technological turbulence as environmental conditions, Figure 2 provides an analysis of the total effect of the use of eOBC versus aOBC contracts with regard to buyers’ perceived benefits and seller’s perceived risks as a function of both context characteristics. It is shown that under conditions of high levels of product innovativeness and low technological turbulence, the use of eOBCs considerably increases risk as perceived by sellers. At the same time, such environments are also the comparatively worse ones with regard to buyer’s perceived benefits. In turn, when product innovativeness is low and technological turbulence is high, buyers associate the highest benefits with the use of eOBCs, and seller’s perceived risks are least as well. In so far, eOBCs should be the preferred option when contractual arrangements regarding established and well-understood products are made in highly turbulent environments. Here, the net benefit of shifting comparatively higher levels of responsibility to sellers is highest.

Total effects of outcome-based contracts type on benefits and risks as a function of product innovativeness and technological turbulence.

Limitations and research directions

We qualify our findings by pointing out some limitations in our research design, but also hope we offer fruitful avenues for future research. First, we used the overall business unit-level and the corresponding OBC portfolio as our unit of analysis. In doing so, our study provides a first glimpse into the average effect of OBC usage on buyers and sellers. While we considered both buyers and sellers, we did not survey buyers and sellers working together on specific contracts, which – in light of the sensitivity of the research context and related data –can be considered a very difficult endeavour. Nevertheless, studying individual OBCs could further enrich our findings and probe into the robustness of our results. In particular, investigating individual OBCs would enable us to better understand the mechanisms via which OBCs determine contract performance and influence the overall relationship between sellers and buyers.

Second, we relied on self-reported measures to capture contract performance. Although subjective performance measures ensure comparability across different types of companies and situations, they also bear the risk of measurement error (e.g., due to overstatements). Thus, objective measures should increase validity of findings of future studies. In the context of this study, overall performance could be measured with the same performance indicators specified in the OBC agreement, as long as these are used and generally comparable across different industries and individual contracts. In case of eOBCs, cost-savings or another monetary-based performance indicator may be used. In case of aOBCs, measures of product performance such as product reliability (as used by Guajardo et al., 2012 in the context of aircraft engine after-sales maintenance support) or service levels may be utilized. Thereby, with regard to the use of objective performance indicators, it has to be acknowledged that OBCs may be generally challenging in terms of current data collection systems – for example, to report availability or to monitor economic outcomes. Indeed, there have been a number of high-profile cases where the absence of necessary monitoring systems and associated contract management skills have resulted in major performance shortfalls and multi-million claims against suppliers for overcharging (NAO, 2014). Obtaining data from multiple respondents might be advantageous to determine the stability of our results. In this context, a dyadic study design in which an individual contract is looked at from the buyers’ as well as the sellers’ perspective would be useful.

Third, to account for the suitability of OBCs in specific context situations, we considered two context characteristics – one internal (i.e., product innovativeness) and one external (i.e., technological turbulence). Yet, we can think of other contingencies, such as relationship strength between buyer and seller and information technology, which might also impact the effectiveness of OBCs. For example, OBCs demand more intense dialogue and a readiness to be more open and collaborative. This represents a very real contrast from the traditional approach to contract negotiations, which tends to focus on risk allocation (IACCM, 2014). The practical implications of OBCs therefore appear to demand a greater readiness by personnel within both the buyer and the seller firm to cooperate and share information, not only at inception but throughout performance of their relationship. This may represent a significant cultural shift by one or both parties. A useful measurement approach to account for such effects, a composite perceptual measure reflecting qualitative (such as trust, satisfaction and commitment) and quantitative aspects of relationship strength (duration and frequency) as proposed by Dagger et al. (2009) is suggested.

To summarize, while OBCs have the potential to deliver benefit, it is clear that organizations need to understand and adjust their internal attitudes and capabilities in order to ensure these benefits are realized. By analyzing the moderating role of these organizational characteristics, researchers could further enhance our understanding of outcome-based contracting.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.