Abstract

The racial wealth gap in the United States remains a persistent issue; white individuals possess six times more wealth than Black individuals. Leading scholars and public figures have pointed to slavery and post-slavery discrimination as root cause factors and called for reparations. Yet the institutionalization of race-neutral ideologies in policies and practices hinders a reparative approach to closing the racial wealth gap. This study models the use of algorithmic methods in the service of reparations to Black Americans in the domain of housing, where most American wealth is built. We examine a hypothetical scenario for measuring the effectiveness of race-conscious Special Purpose Credit Programs (SPCPs) in reducing the housing racial wealth gap compared to race-neutral SPCPs. We use a predictive model to show that race-conscious, people-based lending programs, if they were nationally available, would be two to three times more effective in closing the racial housing wealth gap than other, existing forms of SPCPs. In doing so, we also demonstrate the potential for using algorithms and computational methods to support outcomes aligned with movements for reparations, another possible meaning for the emerging discourse on “algorithmic reparations.”

This article is a part of special theme on Algorithmic Reparation. To see a full list of all articles in this special theme, please click here: https://journals.sagepub.com/page/bds/collections/Algorithmic%20Reparation?pbEditor=true

Introduction

The racial wealth gap between white and Black individuals in the United States is persistent, with data from the 2019 Survey of Consumer Finance (SCF) indicating that white individuals possess six times more wealth than Black individuals (Derenoncourt et al., 2022). This gap is a result of centuries of discriminatory policies and practices, beginning with transatlantic slavery and the conquest of America (Park, 2016), and continuing through Jim Crow laws, residential segregation (Massey and Denton, 2003), and discriminatory mortgage lending practices (Immergluck, 2004; Rothstein, 2018), commonly referred to as redlining (Winling and Michney, 2021), among others. In the process of outlawing these policies and practices, the US legal structure institutionalized what scholars have called “race-neutral ideology,” the idea that race and racism should never be used as a factor in designing laws and policies (Bonilla-Silva, 2018).

The utilization of such race-neutral ideology in policies and practices has been a significant contributor to the persistent racial wealth gap in the United States. For example, the Community Reinvestment Act of 1977 (CRA) was enacted to encourage depository institutions to expand credit to historically redlined neighborhoods. However, the statute itself did not include race-conscious language and instead relied on criteria for expanding credit to low-to-moderate income (LMI) neighborhoods. Even with the most recent Interagency Notice of Proposed Rulemaking to revise the CRA in 2022, this tendency remains unchanged (FRS et al., 2022). The new CRA rule requires banks to assess where and how they provide credit to LMI neighborhoods and borrowers, regardless of where their branches are located. This race-neutral approach to credit expansion has been met with criticism. Many housing researchers and advocates have pointed out that the LMI-based policy of the CRA has failed to reduce the racial homeownership and wealth gaps (Blower et al., 2021; Rinde, 2022). To address the problem, community groups and policymakers have advocated for the expansion of Special Purpose Credit Programs (SPCPs) (Reynolds et al., 2022). SPCPs are designed to expand credit exclusively to historically minoritized groups or people under the Equal Credit Opportunity Act of 1974 (ECOA). However, just how effective SPCPs are in reducing the racial homeownership and wealth gap is dependent on who they serve and whether their eligibility criteria take a race-neutral or a race-conscious approach.

The objective of this study is to examine the effectiveness of race-conscious lending programs in reducing the racial wealth gap in comparison to race-neutral lending programs, particularly SPCPs. Our research question is: If our primary goal is to reduce the racial wealth gap, is a race-neutral or a race-conscious approach more effective? Using algorithmic methods, we evaluate the potential impact of race-conscious and race-neutral lending programs by analyzing a hypothetical scenario in which previously denied borrowers are granted mortgage loans through such programs. We find that race-conscious lending programs show significantly more potential for reducing the racial housing wealth gap than race-neutral programs, thus this study calls for race-conscious policies and practices as a reparative approach to building wealth for Black Americans. Our goal is to inform policy in line with the original objective of the CRA, which was to address discriminatory redlining practices. Ultimately, we aim to exhibit how algorithms and computational methods can be employed to bolster the outcomes of reparations movements, thus contributing to the discourse around “algorithmic reparations” (Davis et al., 2021).

Mortgage lending discrimination: segregation, redlining, subprime lending

Housing is one of the main drivers for accumulating wealth in the United States, and making credit available is one of the main mechanisms for increasing the chances of such wealth accumulation (Immergluck, 2004). Credit and financial markets are shaped by market interests (Akhigbe and Whyte, 2004), but historically, publicly sanctioned policies have effectively provided access to credit to middle- and upper-income white Americans but have limited such opportunities to people of color and to Black Americans in particular (Squires, 1994). For instance, when the Federal Housing Administration (FHA) started to expand its influence on the housing market in the 1930s, it implicitly used the racist framework that the Home Owners Loan Corporation (HOLC) had constructed in the 1930s (Michney, 2022). Their infamous “redlining” maps were made for spreading and normalizing a racially stratified framework for measuring the risks of granting a mortgage (Michney, 2022; Winling and Michney, 2021). Neighborhoods inhabited primarily by people of color and/or ethnic minorities were consistently ranked with a D grade (“hazardous”) and were colored red on the HOLC maps (hence the moniker “redlining”). Although the HOLC did not use the maps to deny loans to communities of color, it is believed that the implicit message conveyed by the maps, in conjunction with the influence of racist conventions on federal governments and local real estate brokers, constituted the primary driving force behind redlining practices (Michney, 2022).

The Civil Rights Movement and the Fair Housing Act of 1968 were significant achievements in the effort to end the widespread practice of racial discrimination in housing. However, although these developments helped to reduce racial segregation and promote fair access to housing opportunities for all, they did not completely eradicate housing discrimination. Rather, new types of racial discrimination emerged. For instance, starting from the middle of the 1990s, the practice of “subprime lending” emerged and shifted mortgage lending practices. Subprime lenders aggressively targeted segregated communities of color with higher interest rates, higher fees, and less favorable terms compared to traditional, prime mortgage loans (Havard, 2005; Hwang et al., 2015; Steil et al., 2018). Subprime mortgage loans were a result of both market and government factors, including the secondary mortgage market and federal policies like tax breaks and preemption of high-interest loans (Immergluck, 2004; Van Order, 1997). Subprime lending practices were one of the main drivers of the 2008 foreclosure crisis (Faber, 2018; Newman and Schafran, 2013; Rugh et al., 2015; Rugh and Massey, 2010), thus reducing wealth accumulated by homeowners of color and enlarging the racial homeownership and wealth gap to where it stood before the Fair Housing Act was enacted.

Reparations and reparative approaches in policy

There is a long history of scholarship and civil society organizing around the term reparations in a variety of different contexts and responding to a variety of different harms, including slavery, genocide, and civil war, among others. Reparations have been understood as the acknowledgment of past wrongs and finding ways of giving “an entitlement for wrongs done” (Aiyetoro and Davis, 2010: 763). In this paper, we build on this public dialogue as well as existing scholarship on reparations to envision how shifting mortgage lending practices may contribute to reparations for Black Americans. Reparations for slavery and post-slavery racial discrimination have been a long-standing demand from Black Americans, and the Black Lives Matter movement revitalized this historic conversation and thrust it into a more public debate (Darity and Mullen, 2020; Hannah-Jones, 2020; Kelley, 2003). Scholars assert that the concept of reparations goes beyond individual compensation and should be seen as a forward-looking, future-oriented process (Táíwò, 2022) aimed at eliminating systemic racism, promoting social justice, and improving the lives of Black Americans. This perspective aligns with the views of the National Coalition of Blacks for Reparations in America (N’COBRA), which advocated for the establishment of autonomous Black institutions through reparations (Aiyetoro and Davis, 2010). As such, we agree with Kelley's (2003) claims that the focus of reparations proposals should be directed toward promoting a political economy that prioritizes collective needs.

Immediately after the abolition of slavery, there was a reparation plan approved by President Lincoln called “40 acres and a mule.” The plan was to provide land and a means of transportation for all freed people. However, the proposal was never enacted; President Andrew Johnson reversed the order and the lands were returned to white Confederate landowners. Plans during the period of Reconstruction focused more on putting freed people on low-wage labor, another kind of exploitation (Du Bois, 1935; Stanley, 1998), although many freed people claimed ownership of the land they worked (Franke, 2019). Even after the long history of expropriation, extraction, and discrimination including slavery, Jim Crow, segregation, and racist housing policy, and despite persistent demands for restitution and restoration from civil society (Coates, 2014), there have been no federal-level reparation policies for Black Americans. Even the proposals of studying reparations for Black Americans, called H.R. 40, have not passed beyond the House of Representatives.

The notion of the United States reckoning with itself would shed light on what a “reparative approach” would look like. In the monumental essay by Ta-Nehisi Coates, reparations “would mean a revolution of the American consciousness, a reconciling of our self-image as the great democratizer with the facts of our history” (Coates, 2014). Such a reckoning requires being truly honest about US society and history. This could be challenging for a nation that frames itself as the epitome of democracy and liberty and that considers that its racial conditions have been improved. Practically, the reparative approach demands deep historical analysis and understanding of current racial disparities not as a given, but as the result of historical and structural conditions. The fact is that the United States has centered racial subjugation and upheld de facto white supremacy (Bonds and Inwood, 2016) and as a result, it constitutes a racialized social system (Omi and Winant, 2015). Race-neutral policies have played no small part in upholding this system.

A reparative approach would mean explicitly taking race into consideration when examining socioeconomic disparities. For instance, President Johnson's Kerner Commission and speech in the middle of the Civil Rights Movement was a recognition that Black poverty is different from white poverty because of its roots in the exploitation of the Black population through slavery as well as the discriminatory structural conditions that persisted following abolition (Coates, 2014). In contrast, race-neutral ideology, often called “colorblind racial ideology” (Omi and Winant, 2015: 217), was formulated after the Civil Rights Movement through various tactics including “code words” –seemingly race-neutral concepts such as “get tough on crime” (Omi and Winant, 2015: 218) which employed racist themes through coded language.

The ideology of “reverse discrimination” appropriates the concepts of fairness that were articulated in the Civil Rights Movement (Omi and Winant, 2015). For instance, affirmative action, which performs preferential treatment based on historic oppression, is constructed as “unfair” and therefore an attack on innocent white people. To be “fair,” in terms of reverse discrimination, such race-conscious policies should be eliminated. The ideology of reverse discrimination has been so powerful that it has theoretically and practically impeded the initiation and formulation of any reparations for Black Americans. Legal doctrine has supported such ideology with the assumption that access to rights, power, and equity has been equally distributed historically, given that reparative policies “de-privilege whiteness and seek to remove the legal protection of the existing hierarchy spawned by race oppression” (Harris, 1993: 1779). Harris (1993) claims that such property interests in whiteness reduce the objectives of affirmative action to an individual level, compensatory arguments – for instance, the extent to which white people's rights are as “equally” protected as Black people's rights, thereby effectively turning the focus away from the core questions of distributive justice (Harris, 1993).

In contrast to compensatory arguments, distributive justice claims that individuals or groups cannot rightfully claim the benefits that they would not have been awarded under fair conditions (Fiscus, 1996). We argue that it is imperative for reparative programs to be situated in distributive justice and the counterfactual – this means envisioning and designing policy toward a society without slavery, without post-slavery racial discrimination, and without its persistent and lingering disparities. Figure 1 illustrates a scenario with such a counterfactual in mind in which the current wealth distribution between Black and white people would be equal. As seen in the figure, there is a portion of white wealth that cannot be rightfully claimed by white people and should not be protected by policy because it was stolen and expropriated through exclusionary practices. By centering distributive justice as an objective of reparative policies, we can reorient the reparative policy debate from the legal protection of “innocent” individual white people to redressing the intergenerational structural harms enacted by chattel slavery; then we can ask and measure the counterfactual: in the absence of racial oppression, what would be the present-day distribution of wealth between Black people and white people?

This graph poses a counterfactual: In the absence of chattel slavery and racial oppression, what would be the present-day distribution of wealth for Black people and white people?

Expanding access to credit and Special Purpose Credit Programs (SPCPs) as housing reparations

Following the Civil Rights Movement, the Community Reinvestment Act (1977) was designed to enforce depository institutions to meet the credit needs of the community and to address redlining practices. Specifically, the CRA requires assessing how banks grant mortgages and small business loans to LMI neighborhoods, how active banks’ investment is in communities, and how basic bank services operate in communities. Many studies show that the CRA has effectively worked for serving the credit needs of lower-income communities (Bostic and Robinson, 2003; Joint Center for Housing Studies, 2002). The CRA is often mentioned as “regulation from below” (McCluskey, 1983: 57) because when community groups demand to create CRA agreements with banks, they gain negotiation power to meet the credit needs of the community in the process.

The CRA has been in place for several decades. However, its most recent revisions took place in 2005. Given the drastic shifts in the financial landscape, including the growing use of online banking, there is now a call for significant updates to the CRA. In 2022, regulators proposed new rules to revise the CRA in order to adapt to contemporary lending practices, including online banking (Federal Reserve System et al., 2022). Under the revised rules, banks would be required to assess their credit provision to LMI neighborhoods and borrowers, regardless of where their branches are located. Additionally, regulators encouraged banks to create more credit expansion programs. However, the revised rules lack race-conscious language, instead focusing on LMI communities and individuals. While designing credit expansion programs and assessing them through income criteria may overlap with race, it does not align with the original goal of the CRA to provide access to credit to historically marginalized groups. Community groups have criticized race-neutral lending programs as not effectively reducing the racial wealth gap (Rinde, 2022; Silver, 2019). This shows how efforts to address racial injustices are still hindered by white supremacy – race-neutral programs, even in their attempts to reduce disparities, still have the effect of exacerbating racial stratification.

SPCPs show potential as a step toward reparative lending programs. SPCPs were created as a result of the ECOA and are legally allowed by this statute. One key aspect that sets SPCPs apart from other similar programs is that they may specifically and legally use race-conscious approaches to lending. The ECOA prohibits discrimination based on protected characteristics such as race, gender, religion, and national origin, among others, but it also states that it is not unlawful for for-profit organizations to extend credit offered pursuant to a special purpose credit program in order “to meet special social needs” or for non-profit organizations to design a “credit assistance program” for an “economically disadvantaged class of persons” (CFR Part 1002, 2023). This means that Congress provided a space for lenders to design credit expansion programs that have the explicit goal of “increasing access to the credit market by persons previously foreclosed from it.” We argue that the ability to design exclusive lending programs aligns with a reparative approach. However, even with the most recent revisions to the CRA, it remains challenging to adopt a race-conscious approach due to the persistence of colorblind norms and practices. Therefore, it is important to measure the consequences of race-neutral and race-conscious lending programs and consider their implications when advocating for reparative lending programs.

Algorithmic reparation

Recently, the field of algorithmic fairness and ethics in computing has been a focus of computer science, as well as other disciplines including law, policy, and social sciences, to understand how we can prevent algorithms from reinforcing inequalities and social sorting (Mann and Matzner, 2019; Starke et al., 2022). Scholars have outlined how algorithms may accelerate, exacerbate, and extend existing forces of oppression (Benjamin, 2019; D’Ignazio and Klein, 2020; Eubanks, 2018; Umoja Noble, 2018). However, there has been a concerted debate about whether such metrics are reflective of addressing systemic inequalities because they fail to address the root causes of the same (Green, 2022; Keswani and Celis, 2022). Thus, the algorithmic fairness discourse may be limited because in many cases, machine learning algorithms utilize the data at the point of creating the algorithm without considering the historical context in which the input data were generated (So et al., 2022). This can lead to machine learning models that “learn” to reinforce disparities that were created by seemingly race-neutral markers as objective truths, thereby legitimizing different treatments (Benjamin, 2019; Browne, 2010; Gerdon et al., 2022). Examples of this process in the domain of housing include the use of seemingly race-neutral variables, particularly risk-based pricing algorithms, such as security deposits in the rental market (Hatch, 2017), and mortgage insurance in mortgage loans (Deng and Gabriel, 2006). Through race-neutral ideology, algorithms tend to contribute to imposing unequal treatment on people of color through disinvestment, displacement, and other forms of housing discrimination (Desmond, 2012; Rosen et al., 2021).

The emerging field of algorithmic reparations aims to address such issues of algorithmic fairness and discrimination by developing new methods that consider the structural conditions of oppression and inequality. This is in line with work that advocates for moving away from the narrow idea of “bias” toward a more robust conceptual, computational, and historical modeling of “power” in algorithms and machine learning (D’Ignazio and Klein, 2020; Miceli et al., 2022). Davis et al. (2021) suggest that a reparative approach using algorithms can contribute to redressing past harms by utilizing the principles of intersectionality and reparations. This approach not only addresses past injustices but also looks toward the future by channeling resources to overcome existing inequities and work toward justice. How might this be operationalized? So et al. (2022) propose two empirical steps such as using causal inference and the method of “algorithmic recourse” (Karimi et al., 2021; Ustun et al., 2019) to identify historical harms and estimate the amount of money needed for housing reparations. These two steps help to determine past injustices through counterfactual analysis and design interventions (Barabas et al., 2018) to alter algorithmic decisions. In effect, these methods leverage reparative algorithms to redress algorithmic harms. The use of these methods is grounded in a theoretical shift – instead of conceiving of fairness as the absence of, or expunging of, racial classification from computational systems (race-neutral) we move toward an antisubordination approach, which contends that equal citizenship is not possible under the current social structure and requires the dismantling of racial stratification precisely by examining and attending to its racist effects (race-conscious) (Keswani and Celis, 2022).

The emerging field of algorithmic reparations calls for a deeper examination of the historical and broader societal implications of technology and data, as well as a rejection of colorblind, race-neutral ideologies. Yet questions remain. How can algorithmic processes be used to uphold the rights of marginalized groups and envision alternative futures? How can current computational methods contribute to policy design and scholarly discourse about reparations? How might they play a role in social movements for reparations for Black Americans?

In the following section, we present our case study as a preliminary step to addressing such questions. Our position is that one potential meaning of “algorithmic reparation” is the use of algorithms to make a potential reparative future visible and possible – to provide a vision around which to gather, discuss, and deliberate, in community, to be able to assess if this is the future we desire. Put differently, a reparative policy proposal generated by an algorithmic process is not a “solution” but rather a starting point for democratic dialogue, and would reveal the need for further rectification, requiring iterations for better processes. Through these processes, we aim to explore the potential of designing reparative approaches and providing estimates for reparative lending programs that prioritize the elimination of the racial housing wealth gap. In so doing, we model how algorithmic processes may be used for reparations: including (1) exposing inequality, (2) proposing a counterfactual future, and (3) providing an algorithmic operationalization for how we might arrive at that future.

Case study: race-neutral vs race-conscious SPCPs

Our case study examines and compares the impact of race-neutral SPCPs and race-conscious SPCPs. Most of the existing SPCPs operate as down payment grants. We focus particularly on evaluating their effectiveness about reducing the racial wealth gap between Black Americans and white Americans, as well as how they should be designed to fulfill that potential.

First, we compare the impact of race-conscious approaches to race-neutral approaches in SPCP, and second, we examine how much white wealth is accumulated through race-neutral approaches, thereby decreasing the chance of converging the racial wealth gap. We find that for SPCPs to reduce the racial housing wealth gap, and contribute to a reparative policy approach, they must be intentionally race-conscious to be practically more effective.

Table 1 shows the four potential types of SPCPs categorized by race neutrality and the scale of eligibility. All these types of SPCPs already exist at some scale, and we give examples of the programs that meet these criteria (Choi et al., 2022; National Fair Housing Alliance and Mortgage Bankers Association, 2023; Reynolds et al., 2022). An SPCP is categorized as race-neutral and place-based if it targets people in LMI neighborhoods. An SPCP is categorized as race-neutral and people-based if it targets LMI people. In contrast, An SPCP is categorized as race-conscious and place-based if it targets racially minoritized neighborhoods. An SPCP is categorized as race-conscious and people-based if it targets racially minoritized people. Using these categories, we examine the impact of each type of SPCP in terms of how much it would contribute to gaining home assets, and how much it would contribute to reducing the racial wealth gap between Black and white Americans as a result. While SPCPs currently operate at different geographic scales, and are not available in all regions, our case study evaluates their hypothetical impact assuming their nationwide availability. Overall, the primary research goals of this case study are the following:

To investigate the differences in impact between race-neutral and race-conscious SPCPs and how the scale of eligibility for each type of program affects this impact. To determine the extent to which race-neutral and race-conscious SPCPs could be effective in reducing the racial housing wealth gap if they were available nationwide.

Types of special purpose credit programs (SPCP) by type.

Data and methods

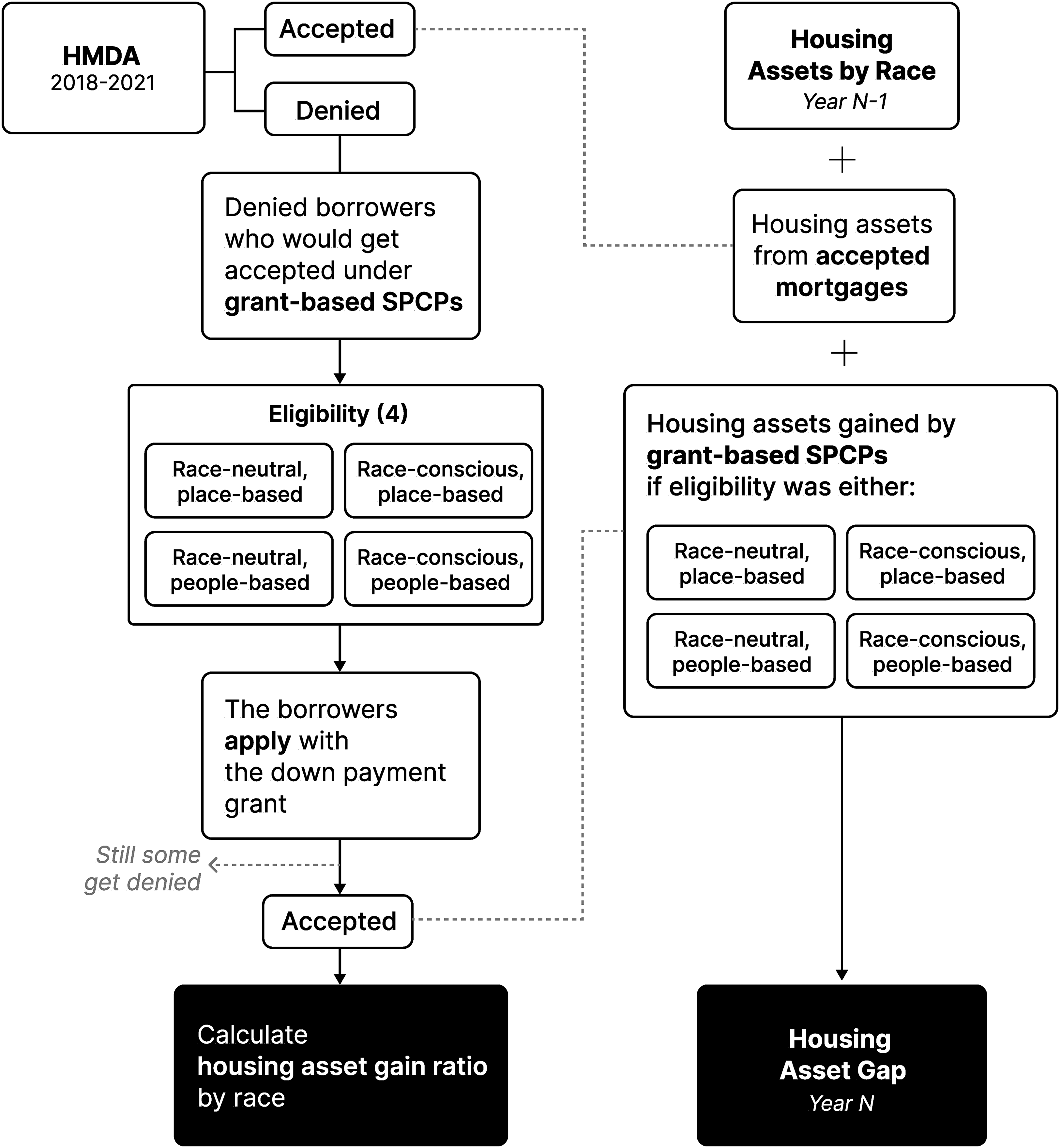

This case study represents a simulation – modeling a future policy scenario and evaluating its potential outcomes and impacts according to specific metrics of success – in our case: the potential for the policy to reduce the racial housing wealth gap. As Figure 2 details, it aims to estimate the potential increase in housing assets for historically denied borrowers if they were (1) eligible for and accepted for mortgages through SPCPs and (2) if SPCPs were available nationwide. The use of simulation to measure the impact of policies or interventions has been adopted in the urban science literature (Kondor et al., 2020; So et al., 2022; Vazifeh et al., 2018). To measure this impact by racial group, the study utilizes data from the Home Mortgage Disclosure Act (HMDA) for the years 2018–2021 as well as the 2019 Survey of Consumer Finances (SCF) data, which surveyed people in 2018. The HMDA data have all the mortgage lending decisions by lending institutions from 2018 to 2021, and the SCF data surveyed income, assets, and debts of US households. The study uses the SCF data to calculate the existing housing asset gap between Black and white households. Using four years of HMDA data, the study then estimates the hypothetical impact of each category of SPCP on housing assets, if that type of program was available nationwide to previously denied borrowers. In the analysis of the HMDA data, the study only considered mortgage loan applications for conventional or FHA loans that were first-lien, for home purchases, and for non-business purposes. Descriptive statistics about the HMDA and SCF data can be found in the appendices.

Case study design to measure housing asset gain ratio by race and housing asset gap changes potentially induced by SPCPs with different eligibility criteria.

This case study investigates the impact of grant-based SPCPs on housing asset gains by racial group and how each type of program contributes to reducing the racial housing asset gap. It algorithmically estimates the lending outcomes for borrowers who had previously been denied a loan but reconsiders them with updated conditions, i.e., reconsidering the borrower with the original characteristics plus the addition of the grant toward the down payment. To do this, we first created gradient-boosting tree-based ML models using the LightGBM package in Python and data from the HMDA for each year between 2018 and 2021. We used gradient-boosting algorithms rather than linear models (such as logistic regression) due to their intrinsic capacity to adeptly capture intricate non-linear associations between features and the target variable. Moreover, gradient-boosting algorithms inherently incorporate regularization mechanisms by managing the depth and quantity of trees within the ensemble. This built-in regularization facilitates the mitigation of overfitting concerns. The test data yielded an accuracy range of 81%–86% for the models. These models were used to predict the outcomes for all records, which were classified into three categories: accepted with a prime loan; accepted with a subprime loan (i.e., annual percentage rate is 1.5 percentage points or more than average prime offer rate); or denied. Then, among borrowers who were predicted to be denied, we modified the loan amount and loan-to-value ratio to reflect the impact of down payment assistance and re-predicted their lending outcomes. If a borrower was then accepted by the algorithm, we added the property value as a housing asset gain. We measured the impact of ranges of down payment grants from $5000 to $50,000 because those are what the existing grant-based programs usually give.

Then, we evaluated the four types of SPCPs against this model. The first scenario is a race-neutral, place-based program, in which individuals are eligible if they reside in a low-income neighborhood, typically defined as an area with a median income below 80% of the metropolitan area median income. The second scenario is a race-neutral, people-based program, in which individuals are eligible if their household income is less than 80% of the metropolitan area median income. The third scenario is a race-conscious, place-based program, in which eligibility is determined by the majority racial makeup of the neighborhood, specifically Black-majority neighborhoods. Lastly, the fourth scenario is a race-conscious, people-based program, in which only Black individuals are eligible. We compared the white/total housing asset gain ratio. Then, we calculate the housing asset gap changes with the housing asset gain from SPCPs with four different eligibility criteria using the 2019 SCF data, which have the housing asset data of 2018 by racial group. In this calculation, we do not incorporate the amount owed from mortgages because we cannot assume how borrowers from SPCPs pay mortgages over time (therefore “asset” gap). Also, we do not include non-housing assets (e.g., stocks and bonds) because we cannot estimate multi-year changes in the total housing gap using the HMDA data. The equation of the housing asset gap in the year N is the following:

Limitations

The analysis presented in this scenario has several limitations and aspects to be considered. Firstly, the assumption that SPCPs are available and widely accessible allows for the evaluation of the relative impact based on eligibility criteria. Such an assumption would require nationwide availability of SPCPs because as things currently stand, each SPCP is limited in terms of budget and geographical coverage. Secondly, the data used in the analysis pertain to previously rejected borrowers, meaning that the study cannot capture the individuals who were unable to apply for mortgage loans. Thus, this result can be considered as the minimum impact of the intervention and should be understood to estimate the relative impact difference by SPCPs with different eligibility criteria. Thirdly, regarding the racial housing asset gap calculation, it does not consider the potential return on investment (ROI) rate by racial group, which was found in a prior study to be 3.7% lower for Black homeowners compared to white homeowners, mostly due to foreclosures and short sales (Kermani and Wong, 2021). If this difference were included, the racial housing asset gap would continue to diverge regardless of the type of SPCP, although the rate of divergence would vary depending on the type. Finally, while the closing of the racial housing asset gap through housing asset gains is considered a means of evaluating the effectiveness of different reparative strategies, it must be acknowledged that measuring potential housing asset gains is only one way of approximating the closing of the racial wealth gap. The non-housing racial wealth gap, which incorporates bonds or stocks, is even wider (Derenoncourt et al., 2022), and therefore even if the racial housing wealth gap were fully closed, other wealth gaps would still need to be addressed. Also, the absence of credit scores from the HMDA data may affect the accuracy of the models. However, we do not believe it will affect the relative difference in SPCPs because SPCPs cannot affect credit scores. Lastly, the calculation of the racial housing asset gap does not consider interracial transactions and all-cash home-buying because of the unavailability of data. Adding these variations might cause some fluctuation in the baseline gap, but it would not affect the comparison of the effectiveness of four SPCPs with different eligibility criteria.

Results

Figure 3 shows the ratio of white housing asset gain expected from four different SPCPs. The results depicted in both the prime and subprime charts indicate that race-conscious SPCPs contribute relatively more toward Black people's accumulation of housing assets compared to race-neutral SPCPs. Race-conscious, people-based SPCPs are specifically designed for Black people, resulting in 100% of the housing assets being gained by Black people. The data indicate that race-conscious, place-based SPCPs (people in Black-majority neighborhoods are eligible) predominantly contribute to the accumulation of Black people's housing assets (93% on average), while race-neutral SPCPs contribute to a lesser extent (47% in people-based, 63% in place-based). It is noteworthy that, except for race-conscious, people-based SPCPs, white people still accumulate some amount of housing assets, thus hindering the convergence of the racial housing wealth gap. Overall, this illustrates how ineffective the existing race-neutral SPCPs are if we are evaluating them as reparative lending programs. Indeed, only the race-conscious, people-based SPCPs would be truly reparative lending programs. This fact is somewhat ironic given that SPCPs were conceived to address racial inequalities and yet many of them end up contributing substantially to white wealth. This is not to say white people should never get mortgages, but rather that it is debatable whether they should receive any mortgages through the few programs, like SPCPs, that specifically exist to address historic and ongoing racial inequalities. Put differently, in the context of creating reparative lending programs, if race-neutral SPCPs contribute to accumulating white wealth, then such SPCPs are, in effect, addressing different injustices, such as class inequality or poverty, rather than racial inequality and housing reparations for Black Americans (Fiscus, 1996).

Comparison of housing asset gain by race and four types of SPCPs. The distribution shows the changes by the grant amount ($5000–$50,000). The x-axis represents how many white housing assets are added from each SPCP. We adjusted housing asset gains by the number of households by race. The charts show that race-conscious SPCPs are more likely to contribute to the accumulation of housing assets for Black people when compared to race-neutral SPCPs. Race-neutral SPCPs that target low-income individuals result in the least accumulation of housing assets for Black people.

Additionally, the results of the case study suggest that as the amount of down payment grants provided by SPCPs increases, their effectiveness reaches a saturation point (as seen in Figure 4). This may be because, under a grant structure where borrowers need to apply using the grant, providing down payment assistance alone may not be sufficient to grant mortgages to previously denied borrowers. Other factors, such as credit scores, employment history, and high debt-to-income ratio, also play a role in the denial of mortgages. This result may suggest a public and private support structure to lead SPCP grants to prime mortgages because, on average, 25.4% of the loans granted through these programs are subprime, which is a significant portion. Given that previous studies have shown that subprime loans are more likely to lead to foreclosure than the individual borrower's financial conditions (Ding et al., 2011), even if these down payment grants make it possible to initiate a mortgage loan, the chances of achieving long-term home equity stability may be questionable in these cases, thereby demanding a support structure for the homeowners with mortgages.

Total home asset gain of race-conscious, people-based SPCPs by year. The X-axis represents the grant amount of the SPCP (up to $50K) and the Y-axis represents the total housing asset gain. The concave downward curves indicate that increasing grant amounts does not linearly lead to increasing assets for Black borrowers.

Figure 5 shows how four different SPCPs would contribute to reducing the racial housing asset gap between Black and white people. It shows that even though all the SPCPs would contribute to reducing the racial housing asset gap, understandably, the race-conscious, people-based SPCPs outperform other SPCPs. On average, race-conscious, people-based SPCPs reduce the racial housing asset gap about 2.1 times more than race-neutral, people-based SPCPs and around 3.3 times more than race-conscious, place-based SPCPs and race-neutral, place-based SPCPs. Interestingly, race-neutral, people-based SPCPs are more effective than race-conscious, place-based SPCPs when it comes to reducing the racial housing asset gap. This could be due to the limited number of Black mortgage applicants from Black-majority neighborhoods and the exclusion of Black applicants from outside these areas. Conversely, race-neutral, people-based SPCPs, which allow for low-income individuals to apply, have a higher number of Black applicants and are thus more effective than race-conscious, place-based SPCPs. This may indicate that income disparity is correlated with race, such that race-neutral people-based SPCPs end up covering more Black borrowers than people who live in Black-majority neighborhoods. This finding highlights the superiority of people-based SPCPs over place-based SPCPs in the design of race-conscious SPCPs (Reynolds et al., 2022) and offers a deeper insight into the interplay of racial groups, class, and neighborhoods in the context of housing.

Racial housing asset gap changes by different types of SPCPs. Types that are lower on the vertical axis are decreasing the racial housing asset gap more than types that are higher. The height of the colored box relates to the changes in the racial housing asset gap incurred by grant amount ($5000–$50,000). All charts show that race-conscious, people-based SPCPs are more effective compared to the other types of SPCPs.

Overall, the results suggest that the recent revisions of the CRA which encourage investments in race-neutral terms, and the proposed race-neutral SPCPs bolster white wealth, sometimes at higher rates than Black wealth, except when the SPCP explicitly employs a race-conscious approach. Drawing from a reparative policy approach to the history of slavery and post-slavery racial discrimination, then one of the central objectives of the CRA and of SPCPs must necessarily be to reduce the racial wealth gap. These results show that only a race-conscious approach to SPCPs shows promise in achieving that goal.

Discussion and conclusion

Race-conscious vs race-neutral policies

The findings of the case study indicate that SPCPs have the potential to serve as a form of housing reparations, and that they may contribute to reducing the racial housing wealth gap. However, it is important to note that different approaches to implementing SPCPs have varying levels of effectiveness. Specifically, race-neutral approaches end up increasing white housing assets, sometimes at higher rates than Black housing assets in people-based SPCPs, leading us to assert that they are not actually race-neutral. These findings show how race-neutral policies and practices are, in fact, racialized (Williams, 2020). Also, race-conscious, place-based approaches are less effective than race-conscious, people-based approaches in terms of converging the housing asset gap. Because of this, race-conscious, people-based SPCPs were found to be more successful overall. Finally, the study found that, except for race-conscious, people-based SPCPs, all of the SPCPs examined in the study contribute to an increase in white wealth. We do not argue that white people should never increase their wealth, only that the majority of mortgage and lending programs outside of SPCPs already serve to increase white wealth. The question arises as to why policymakers and lenders continue to use race-neutral language and implement race-neutral policies when the goal is to extend credit to historically marginalized groups. The implications of this case study include potential considerations for the design and implementation of race-conscious housing-based reparations programs.

The use of colorblind and race-neutral approaches in policy and lending practices is problematic as it contributes to the hoarding of white wealth and dilutes efforts to truly redress historical injustices (Underhill et al., 2018). We argue that the reason for this is rooted in colorblind racism and the fear of litigation, including legal disputes over “reverse racism.” This colorblind ideology makes legal doctrines believe that “granting advantages to one group necessarily disadvantages another” (Liptak, 2022: 5) without conditioning that those disadvantages originally come from a long history of discrimination. Put differently, colorblind ideology is the result of not fully acknowledging (i.e., not being honest about) the history of the United States and its perpetuation of racial disparities. For example, even though the CRA was created with the core objective of redressing redlining practices and advancing racial equity, the original legislation did not include race-conscious language. Such a race-neutral framework fails to consider the historical injustices and inherently unfair financial structures that have perpetuated racial disparities, particularly in terms of housing and wealth accumulation. Without a reparative framework, achieving racial equity and closing the racial wealth gap will remain out of reach. This case study empirically quantifies how the implementation of colorblind, race-neutral programs serves to maintain the status quo of white supremacy, even when those policies are nominally aimed at addressing long standing racial inequalities. To counteract the issue of race-neutral policies and practices and to advocate for race-conscious policies and practices that expand credit access to Black people, it is important to consider that the benefits that Black people receive through reparative programs are based on the idea of what would be fair under different circumstances (i.e., had racial oppression not existed in the United States) and that the aggregated wealth currently held by the dominant racial group, white people, is not, in fact, theirs to claim as it was secured and sustained through centuries of bondage, exploitation, and discrimination (Fiscus, 1996). Without putting this at the center of conversations about fair housing, policymakers risk being distracted by the colorblind and race-neutral ideology, and therefore risk keeping in place the race-neutral programs that are not only ineffective in reducing racial disparities but may be exacerbating them.

Policy implications for race-conscious mortgage lending

We argue that a race-conscious approach is needed in the design, implementation, and assessment of mortgage lending policies. Without this, the effectiveness of the policy will be decreased, and the programs may end up exacerbating the racial wealth gap. One issue with grant-based SPCPs is that borrowers still need to apply for a mortgage, which can create barriers for individuals with spotty traditional credit histories. Prior reports suggest that alternative sources of data for estimating borrower creditworthiness are needed to achieve the theoretical and practical objectives of SPCPs (Wu, 2021), in particular because it has been demonstrated that credit scores are not reliable measures of creditworthiness for Black people, among others.

When considering the practical implementation of SPCPs, financial institutions have expressed concerns that race-conscious SPCPs might violate the Fair Housing Act (FHA), and if it may not, what the requirements would be. In response to these concerns, federal agencies have endorsed the development of SPCPs to “specified classes of persons” (FRB et al., 2022: 1), and have assured that HUD explicitly notes that it does not violate the FHA (HUD, 2021). Furthermore, the National Fair Housing Alliance and the Mortgage Bankers Association (2023) created a toolkit to assist lenders in crafting SPCPs and navigating the complexities of meeting SPCP requirements and conducting thorough data analysis. Within the toolkit, a procedural guideline is presented for identifying community needs, which depends on recognizing the challenges that borrowers face, such as insufficient savings or high debt-to-income ratios.

When implemented, this study shows that even race-conscious SPCPs in minority-majority neighborhoods could be less effective than people-based, race-conscious SPCPs, and therefore contribute to white wealth hoarding. However, given that budgets are inherently constrained in real-world scenarios, careful considerations must be made regarding the allocation of resources for race-conscious, people-based lending programs. We argue that the priority should be assigned to Black-majority neighborhoods. The rationale is rooted in the importance to rectify the longstanding history of housing exclusion that Black communities have experienced over centuries. But, still, if financial institutions want to create place-based SPCPs, i.e., people living in Black-majority neighborhoods are eligible, we argue that reparative lending programs should be with people-based parameters (e.g., race conscious). This approach would be more effective in reducing the wealth gap and promoting racial equity.

The effectiveness of SPCPs as reparative lending programs could be – and is being – further enhanced through additional support from governments. For example, government-sponsored enterprises (GSEs) such as Fannie Mae and Freddie Mac recently outlined plans to purchase mortgages that receive grants from SPCPs, which would enable lenders to expand SPCPs without having to worry about loan risk (Fannie Mae, 2022; Freddie Mac, 2022). In their plans, they endorsed local SPCPs and launched their own SPCPs to infuse liquidity into local lenders, thereby enabling them to accommodate a greater number of mortgages facilitated by SPCPs. Considering that the approval of a mortgage loan significantly hinges on the underwriting judgments made by GSEs, the provision of support at the GSE level would serve as a response to the uncertainties prevailing in the housing market, including escalating home values and the necessity for adaptable borrower terms. Furthermore, the assessment and enforcement of the CRA should be explicitly race-conscious to measure how credit expansion, including SPCPs, contributes to reducing the racial wealth gap and investing in neighborhoods of color. With such enforcement, banks operating race-conscious SPCPs could be incentivized by the CRA. It is important to recognize the role of banks as public institutions and to keep in mind that the CRA's core objective is to redress racially discriminatory lending policies. Other ways the government could support SPCPs include providing funding to state or local financial institutions for home repairs, which would increase Black owners’ home equity over time, prevent short sales in times of financial need, and increase access to sustainable homeownership as a result. For reparative lending programs, it is important to consider not just the initiation of mortgages, but also their maintenance and stability.

Lastly, there is the potential for legal challenges to arise against SPCPs, given the historical resistance toward race-conscious programs, as evidenced by instances like Students for Fair Admissions v. Harvard. In response, we argue that it is imperative to actively cultivate public discourse concerning the rationale underlying the development of reparative policies and programs. Reparative programs are not handouts for special interest groups. Rather, they are a form of institutional truth-telling about past harms, and an institutional commitment to engage in rectification. As Justice Ketanji Brown Jackson writes in her dissent, “[t]he only way out of this morass – for all of us – is to stare at racial disparity unblinkingly, and then do what evidence and experts tell us is required to level the playing field and march forward together, collectively striving to achieve true equality for all Americans” (Students of Fair Admissions v. Harvard, 2023: 26). Fostering collective understanding of, first, uncensored history, and second, the visionary potential of reparations, will contribute to the cultivation of political momentum aimed at effectively formulating reparative policies and programs.

Algorithmic reparations

Finally, this case study has methodological implications for understanding the potential of algorithmic reparations. We used algorithms in the form of a predictive model that can help evaluate the reparative potential of different types and configurations of SPCPs toward reducing and eliminating the racial housing wealth gap. It demonstrates how algorithms, simulations, and data analysis can counter institutional power and push back against colorblind ideologies that ignore histories of oppression. This is especially important in a racialized social system that perpetuates de facto white supremacy (Omi and Winant, 2015). The case study shows that even when racist intent is not present, de facto white supremacy still hoards resources and limits opportunities for closing the racial wealth gap. The use of race-neutral ideologies perpetuates lending practices that favor white people and additionally undermines concepts of justice and fairness established in the Civil Rights Movement. In this sense, algorithmic reparations can be understood as a form of resistance to colorblindness by quantifying how racial disparities are perpetuated by supposedly race-neutral policies. Additionally, we advance the idea that algorithmic reparations might mean employing the imaginative, speculative potential of computation by using it to envision alternative futures without oppression and operationalizing ways to achieve them through policy, organizing and/or narrative change. Through mapping alternative futures, instigating dialogue, and developing narratives that envision co-liberation for all of us harmed by racial stratification, these methodologies can propose a way forward in addressing racial disparities and achieving racial justice (Collins, 2002; Táíwò, 2022).

Lastly, we see the potential reparative function of SPCPs as part of a constellation of reparations for Black Americans, not as the “only” form and not as any kind of “fix.” Housing, through its association with the land, can significantly contribute to building wealth for Black people, with intergenerational effects and the basis for creating their own vision (Boggs, 2016). But we also acknowledge that property should not be the only domain for reparations. Other paths include building autonomous Black institutions to create environments for self-determination (Kelley, 2003) or accessing land and home through anti-capitalistic means such as collective home ownership and limited equity cooperatives (Roy, 2017). These provide new visions for institutions, property, and collective ownership. Furthermore, ongoing efforts in legal, social, and political reforms are necessary to address institutional structures that perpetuate colorblind, race-neutral ideologies. Algorithmic reparations can mobilize anti-racist epistemologies and methodologies to expose historical inequalities and propose alternative reparative interventions.

Supplemental Material

sj-docx-1-bds-10.1177_20539517231210272 - Supplemental material for Race-neutral vs race-conscious: Using algorithmic methods to evaluate the reparative potential of housing programs

Supplemental material, sj-docx-1-bds-10.1177_20539517231210272 for Race-neutral vs race-conscious: Using algorithmic methods to evaluate the reparative potential of housing programs by Wonyoung So and Catherine D’Ignazio in Big Data & Society

Footnotes

Acknowledgements

The authors are grateful for the feedback and support from the housing vertical in the Initiative on Combating Systemic Racism at the Institute for Data, Systems, and Society (IDSS) at MIT.

Declaration of conflicting interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by the MIT-IBM Watson AI Lab (grant number N/A).

Supplemental material

Supplemental material for this article is available online.

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.