Abstract

As Big Data, the Internet of Things and insurance collide, so too, do the best and the worst of our futures. Insurance is summoned as an example of the interference in our private lives that is already underway everywhere. In this paper, we pause to reflect on this argument. Can changes in the way insurance measures the value of behaviour really serve as an example of the individual and social harms of datafication? How do we know? Insurance is a mathematical relationship staged between individuals and groups, between risk and uncertainty, between distribution and assessment, between the value of sharing and the sharing of value. We use the case study of Discovery International, owner of Vitality, the market leading brand in behavioural insurance to consider how behaviour is being branded and how the brand behaves.

This article is a part of special theme on The Personalization of Insurance. To see a full list of all articles in this special theme, please click here:https://journals.sagepub.com/page/bds/collections/personalizationofinsurance

The important point is to make them click, that they talk about it […] We have to catch people, by the coupons, by their friends who have points. (Generali Vitality IV #1, 2017)

Introduction

How do you get people to talk about insurance, how do you get them to publicly share their experience of it and why would you want to? For most of its customers insurance is a dull necessity not the sort of thing they are eager to have a conversation about. Besides Wallace Stevens, the poet and underwriter for Hartford Accident and Indemnity Company, few have been intrigued by the way the technical geometry of insurance is orchestrated around the metaphysical dramas that drive sales. Insurance is the best-known mechanism for compensating loss, a product engineered to restore value, a promise that the world can be set right again even in the face of illness and death. This much may be gleaned from centuries of marketing, advertising and branding. It is harder to surface the way this is part and parcel of the technical and commercial practices of insurance. Generali Vitality want their policyholders to talk, to share, precisely because their product depends on maintaining a connection between how the company values risk and how its customers value insurance.

Getting to grips with how this connection works is hard because despite insurance’s social importance and sentimental resonance, its techniques are arcane. It is well understood that technically, insurance concerns the classification and distribution of risk, but precisely how this is done is a highly niche form of expertise. There is some general awareness that insurers employ what, following Mackenzie (2011), might be called ‘canonical mechanisms’ that is, sets of knowledge generating arrangements that facilitate actuarial calculations of risk, which are in turn factored into the premium charged to consumers. Beyond this, a fog surrounds precisely how insurers measure and cost risk and how this is translated into the products and prices offered to individual consumers. This fog has become appreciably thicker with the arrival of new techniques, data sources, products and market entrants. These innovation surges have triggered attention from outside the sector – especially to products incorporating telematics and health-tracking – but little clarity about how insurance product innovations work in practice.

Our paper is part of a move to remedy this by delving deeper into the case of the most controversial insurance product innovation – behaviour-based, or interactive, health and life insurance. We focus on Vitality, a brand wholly owned by the South African financial services group Discovery Limited. Vitality is delivered as a branded program, to individuals and employer groups, through a network of equity, partnership and franchise arrangements giving Vitality a presence in 19 countries and in the region of 17.8 million customers (Discovery, 2018). Discovery was founded in 1992 and has focused on incorporating incentive-based health promotion from the start. The company owns the best-known brand in the field and has elaborated a system of value-based practices and a socio-economic philosophy to support it. The ‘Shared-Value Insurance’ model was developed in collaboration with academic specialists in strategy, management and behavioural economics (Porter and Kramer, 2001; Porter, Kramer and Sesia, 2014). The model both underpins the general principles of interactive incentive-based insurance and drives specific product features, including the exhortation to customers to ‘share.’

We begin with a brief outline of the methods we used to investigate Vitality’s business model. From there we move on to identify how public concern about the prospects of discrimination, exclusion and surveillance, centre around the use of personalisation strategies, individual-level data and individual pricing. These are grim prospects, but their necessary debate has been hampered by a recursive hype cycle between consultancy reports, journalism and academic analyses that confuse, and are confused by, the different categories of insurance, its idiomatic languages and the byzantine regulatory and commercial contexts it operates in. Health and life insurance are parastatal industries. They operate in the spaces between supranational, national, federal, state, jurisdictional regulation and policy on the one hand and between consumer, employer and capital markets on the other. Despite this, critical discussions seldom differentiate between categories like life, health and even motor, between individual and employer markets or between different regulatory contexts. These distinctions are inextricably related to how and why behavioural data is used, shared and valued in insurance. Added to this the vocabulary used to describe insurance, particularly its emerging forms, is varied, imprecise and unsettled. This allows attention to be diverted to the most visible Internet of Things (IoT)-based innovations and inhibits a more empirical, granular analysis of how insurance is changing and what the implications of that might be.

Our two main empirical sections attempt a correction by explaining how the Vitality program works and how it is sold in double-facing markets – both direct to consumer or ‘B2C,’ and direct to group/employer, known as ‘B2B.’ Establishing a space between these two markets helps to expose two distinct but overlapping senses in which Vitality’s program and products can be understood as much as branding behaviour as personalised risk assessment. In the first section, BEHAVIOUR Branding, we describe how central individual behaviour tracking is to the Vitality brand. In the second section, BRANDING Behaviour, we focus on how Discovery’s corporate efforts to protect and maintain the Vitality brand are shaped by the regulatory and competitive contexts it trades in. In these two sections we aim to establish a distinction between the different health and life insurance markets and the distinct roles behavioural data sharing plays within them. In both markets, behavioural data creates value for the company but not necessarily because it provides a more accurate ‘canonical mechanism’ for the actuarial calculation of individual level risk.

Methods and materials

Our aim is to investigate how behaviour-based insurance is conducted at an industry level or ‘in the wild.’ To do so, we combine a variety of sources including regulatory documents, grey literature, corporate websites, consultancy blogs and primary interviews with industry and regulatory professionals. The documents from regulatory agencies, including the Financial Conduct Authority (FCA) in the UK and the European Union regulator, the European Insurance and Occupational Pensions Authority (EIOPA), provide aggregated data on the uses of various kinds of individual-level data in risk modelling and pricing practices across the sector. These insights allow us to contextualise the uses of self-tracking IoT-based data and inform our argument that, despite its visibility, self-tracking data is of marginal importance in the health and life insurance sector. Regulatory documents reveal concerns about how some individual level data acts as a component of price, but it is not self-tracking data. We combine analysis of these documents with evidence collected from interviews with 12 professionals employed by insurance or data regulators, and insurance national federations, including EIOPA, the Directorate-General for Financial Stability (DG FISMA) at the European Commission, and the Commission Nationale de L’Informatique et des Libertés (CNIL) in France, the authors of a European Economic and Social Committee opinion (EESC, 2017) and executives of the Fédération Française de L’assurance (FFA).

In order to assess the concrete modalities and technical practices of behaviour-based insurance, we conducted 22 interviews with professionals employed by European insurance and mutual insurance companies. 1 Eleven of these interviews were with employees of Vitality and Generali in positions ranging from product design, marketing and program implementation which allowed us to track the various steps of the product from conception, selling, implementation to follow up. The interviews were combined with documentary analysis of grey literature, published reports; corporate, partner, group/employer and consumer facing websites; blogs and other online sources to provide our case study. We focused primarily on Vitality branded products sold in France, the US and the UK to give an insight into how the way they are branded and employ behavioural self-tracking schemes varies in accordance with local regulation and health care policy.

Disentangling persons, data and pricing

John Hancock’s announcement in September 2018 that it would no longer underwrite traditional life insurance and instead offer only its Vitality branded interactive health tracking policies broke through the usual disinterest in insurance stories to earn coverage in, among others, The New York Times, The Washington Post, Forbes, CNBC and the BBC. Behaviour-based programs in the health, life and motor sectors have turned insurance into clickable media content and drawn attention from a range of commentators and scholars interested in the individual and social harms digitalisation and datafication can do through surveillance of individual-level and/or ‘behavioural’ data. The use of new, and visibly material, devices like black box telematics, wearables and apps has prompted concern that insurance is becoming a world of ‘real-time rate hikes and financial penalties’ (Zuboff, 2019: 215; see also Krüger and Ní Bhroin, 2020; Lupton, 2016; O’Neil, 2016; Schüll, 2016).

This prospect seems plausible given the affordances of tracking devices and the data they gather. The question we raise is whether we currently know enough about insurance, and behavioural insurance specifically, to assess it. In critical discussions insurance is usually cast in a supporting role, as one of many examples of the datafied, platform-based surveillance and quantification of individuals (see Tanninen, 2020, this issue). Journalistic 2 and academic accounts rely heavily on consultancy reports with titles like Disruption in the Insurance Industry: here comes the Internet of Things (IBM Institute 2017; see also AT Kearney, 2014; McKinsey, 2019, 2016), which outline prospective futures. There is a recursive loop that runs from these reports to news articles to academic texts back to news articles that all feeds into a hype cycle. A whole economy, as Pollock and Williams, have shown, springs from industry analysis: ‘you know what is coming next: because you are making it come next’ (2016: 3). Analysts’ reports are suggestive, but they have an interest in identifying what is coming next and are not a reliable source on empirical practice in an arcane field.

The tendency to use consultancy reports as a primary source may be understandable given the unobtrusive and under-researched character of insurance but it hampers publicly framed discussion of the issues raised by behaviour-based products. In consequence characterisations of the present and future of behavioural underwriting, such as that offered in Zuboff’s (2019) analysis of surveillance capitalism, seem clearer and more inevitable than they are. In her account, insurers are using behavioural underwriting as a means of reducing their risk through machine processes that are designed to modify behaviour by triggering financial penalties. In this, she reiterates three main issues– the role of personalisation, the use of individual health data and the emergence of individual pricing – also raised in earlier work by Lupton (2016), Neff and Nafus (2016), O’Neil (2016) and Schüll (2016). These three issues are implicated in behaviour-based products but there is a lack of clarity about what each issue means in practice, about whether they necessarily relate to one another and how. It does not necessarily follow, for example, that personalisation means personalised pricing, that the use of individual data means IoT-derived health data or when it does it that that impacts price. In what remains of this section, we attempt to define more carefully how personalisation, individual data and pricing may be understood in insurance practice.

First, personalisation. Personalisation conveys a sense of both an offer made at the level of the individual and of ‘constant intimate surveillance’ of the same individual. It is bound up with the emergence and ongoing refinement of transactional history based offer and recommender systems by supermarket loyalty schemes, online retailers and digital streaming sites (Knox et al., 2010; Moor and Lury, 2018; Seaver, 2015; Vargha, 2011) and it is an inherently paradoxical concept. In combining the idea of an offer for the person, made out of their (transactional) history, personalisation appears to be all about the person as a distinct and unique individual. As a commercial process however, personalisation involves extracting and combining multiple data points into a dynamic series of re-contextualised recommendations and offers. As Seaver characterises it: Personalized recommender systems were once pitched as a fine-grained improvement on coarse demographic targeting … the new generation of contextual recommenders appeals to the partible person: your likes, and maybe even your identity, may vary according to the situations you find yourself in. Given these trends in recommender research and development, we are in for a future where data mining concerns itself increasingly with the determination of context, drawing on a range of signals to personalize more precisely than the unified ‘person.’ (2015: 1103).

Behavioural insurance fits with the notion of a ‘tracking-intensive world’ in which the person can be sliced, divided and treated as data (Schüll, 2016: 327). Data, Cheney-Lippold (2017) remarks, is mobilised in technology discourse as a way of expressing the human condition directly and used by companies with obligation to tell us how they make ‘us.’ This fuels dread – and fascination – with commercial surveillance that is evident in responses to behavioural insurance, of the ‘endless trapdoors ahead: data inaccuracies, intentional gaming, constant intimate surveillance 24/7.’ 3 The challenge in resisting incursion into the private territory of human experience is to avoid promoting the conceit that datafied personalisation can see deeper than it can.

Self-tracking devices promise a peculiarly intimate way of seeing the person, a deep body periscope. Where a traditional insurance assessment may use body-mass-index calculations or ask questions about fitness, risky habits and occupations, self-tracking data seems to offer an almost unmediated assessment. The devices are themselves very visible, their incorporation into insurance a tangible sign that individual, behavioural data is being used. The problem is first, in the hop, skip and jump from the incorporation of self-tracking devices to the use of the data they gather for real-time risk assessment and pricing and second, in the way this diverts attention from the role being played by other forms of individual data. The visibility of wearables begs comparison with more established black box, telematic motor insurance schemes. Since both track forms of movement using black boxed algorithmic devices and/or smartphone apps it is easy to treat them as having broadly comparable affordances for insurance. Although they remain a relatively small proportion of the market, telematic motor insurance schemes do track driving for specific risks and the data they gather triggers penalties, bonuses and informs price (Meyers, 2018; Meyers and Van Hoyweghen, 2018, 2020). This makes motor telematics something of an outlier in price personalisation, as Moor and Lury (2018: 507) note, few cases feature ‘the kind of transparency about the linking of price to personhood that is present (at least to some degree) in ‘black box’ insurance policies for young drivers.’ It is not at all clear that anything equivalent is likely in the health and life sectors given the categorical differences between health and driving as risk objects and the very different regulatory restrictions that apply.

While public attention has focused primarily on health tracking data, all sorts of other individual-level data have quietly begun to be used in insurance pricing. In 2019 the European Union regulator, EIOPA, conducted a thematic review of how Big Data analytics were being used across insurance sectors (See Figure 1). Their review emphasised the increasing role played by ‘alternate’ or ‘external’ data, a category which includes but is certainly not limited to, telematic and wearable data. Traditional data includes demographic, exposure (e.g. type of vehicle, value of contents) and, to a lesser extent, behavioural (e.g. smoking, drinking, distance) data. External data includes a wide range of data – for example IoT data, online data and financial data – that are called ‘external’ because they are not modelled as actuarial risk factors. As in all Big Data epistemologies, external data analysis is based on correlation and its capacity to expose strange connections – owners of orange cars make fewer insurance claims, regular dentist visits are a reasonable proxy for high credit scores – without the need to identify a causal mechanism.

EIOPA internal and external data sources.

The use of external data was also a target of the UK’s Financial Conduct Authority (FCA) 2019 investigation into insurance pricing practices. The FCA noted that firms use between 50 and 400 factors in their pricing models. Among these, a growing number have no identified, causal connection to actuarially modelled risk. Thus, for example, the price offered may be influenced by individual level data on online purchase histories (including what, when, where and by what means items are purchased); social media, internet or mobile activity; geographic location tracking; the condition or type of device, operating systems and applications used to access the internet; and specific patterns of website behaviour. Regulators in Europe, the UK and the US all recognise that these data can produce unfair and discriminatory outcomes that contravene statutory limitations on discrimination and exceed the permitted actuarial exceptions for discrimination, for example on the grounds of age.

4

In the US, insurance is regulated primarily at state level, with some legal protections including the prohibition of discrimination on the grounds of pre-existing conditions, effective at federal level (McFall, 2019). New York’s state insurance regulator advised insurers in 2019 of their statutory obligations to ensure data sources are not based in any way on ‘race, color, creed, national origin, status as a victim of domestic violence, past lawful travel or sexual orientation.’ They accordingly cautioned insurers against using: external data sources, algorithms or predictive models in underwriting or rating unless the insurer has determined that the processes do not collect or utilize prohibited criteria and that the use of the external data sources, algorithms or predictive models are not unfairly discriminatory. The insurer must establish that the external data sources, algorithms or predictive models are based on sound actuarial principles with a valid explanation or rationale for any claimed correlation or causal connection. (New York State Department of Financial Services, 2019)

Insurance prices emerge somewhere in the collision between actuarial risk and non-risk factors. Figure 2 describes something of the range of insurance price components. Under expected claims cost are the actuarial rating factors used to calculate risk. That includes individual behavioural data, like smoking and drinking, but does not generally include behavioural data derived from IoT devices. EIOPA’s review collected feedback from 222 insurers across 28 jurisdictions. Of these around 20 health insurance firms said they were using data from wearable devices and mobile phone apps but primarily for product development, sales and distribution.

The components of price (FCA, 2019).

The other area where individual behavioural data has a major effect on price falls under expenses, especially the costs of acquisition. Historically advertising, promotion and sales would be the major costs, (c.f. McFall, 2014) but this has changed with the move to online purchasing. In the online environment discounting for new customers and price optimisation strategies are a substantial part of the cost to acquire. Optimising price to entice new customers creates acquisition costs that are borne by all customers. The result is that the most brand loyal customers subsidise the cost of the newest, least brand loyal and most price sensitive customers. The individual behavioural data with the most significant impact on price is the data used to assess propensity to buy.

This still accounts for a relatively small part of price. Another detail usually missed in the behavioural data debate is that underwriting is not the primary source of insurance profit. The provision of additional services such as premium finance has become increasingly significant in recent years (FCA, 2019) but as far back as the nineteenth century a substantial part of insurance profit has been derived from investment income (Ericson et al., 2000; McFall, 2014). Research by Van der Heide (2019) has delved further into insurers’ investment practices and revealed how substantially the way insurers evaluate the economic worth of their contracts has changed since the 1970s. Van der Heide’s analysis traces how the privatisation or ‘individualisation’ of risk and responsibility that underpinned the rolling back of welfare provision from the 1980s (Baker and Simon, 2002; O’Malley, 1996) was also instantiated in concrete insurance practices and arrangements. In traditional life insurance, he explains, policyholder benefits were related to investment income, but risk was borne by the company as a whole, not by individual policyholders. The emergence of unit-linked insurance, which dominated the life sector by 2010, tied policyholder benefits directly to financial market performance. The result is that insurance contracts have become more like other investment and financial instruments (c.f. Christophers et al., 2018) in which the cost of financial risk is charged directly to the individual. From this perspective it is not so much the personalisation of risk but its individualisation that has had the most impact on pricing.

In the two sections that follow, we give an overview of how Vitality operates in ‘double-facing markets’ that present ‘B2C’ an offer to individual consumers and/or a ‘B2B’ offer to business/groups/employers. In the first section, BEHAVIOUR branding, we argue that behaviour is Vitality’s central brand value and trace its role, particularly in the B2C market. In the next section, BRANDING behaviour, we document how developing and protecting this brand value has informed Discovery’s corporate strategy and its B2B offer.

BEHAVIOUR branding: The Vitality program

As the market leader Vitality provides important insight into the implementation of self-tracking programs in health and life insurance. Discovery Limited is a South African financial services group, focused primarily on insurance. The company was founded in 1992 by Adrian Gore in a national context composed of an underfunded, public health care system and expensive private provision (Porter, Kramer and Sesia, 2014). By the end of the decade Discovery was the largest health insurer in South Africa, had embarked on an international expansion programme and had launched Vitality. Vitality was conceived as a health promotion program designed around a system of financial and non-financial incentives and rewards. It was based on the proposition that healthier behaviour would lower rates of health care consumption allowing the insurer to lower the price of cover and finance rewards (Gore, 2018).

Vitality soon became Discovery’s main product and the centrepiece of the company’s international expansion in the early 2000s. It was implemented in the UK in 2004 through a joint venture with Prudential Assurance, once the UK’s largest insurance company with a long track record in group health and pensions. The scheme was marketed under the umbrella of PruHealth as a ‘unique way of rewarding you for actively looking after your health throughout the year’ (French and Kneale, 2009: 1041). This predated the proliferation of self-tracking devices and apps in the 2010s. Initially, Vitality points were awarded for activities including participating in a smoking cessation programme, visiting a gym, shopping for fresh fruit and vegetables, completing regular health screens, and demonstrating improvements in BMI and blood pressure (French and Kneale, 2009). The novelty of the scheme was complemented by promotional devices like the ‘help yourself’ to an orange or a tennis ball bus-stop in Figure 3.

PruHealth bus-stop campaign, JC Decaux.

The joint venture with Prudential ended in 2014. Discovery now operates the Vitality scheme through the subsidiary brand names Vitality Health Insurance, Vitality Life Insurance and Vitality Invest alongside a network of partnership arrangements. In the last decade Discovery has reached around 17.8 million customers in 19 countries through arrangements including a 2010 equity partnership with Ping An in China; a 2013 partnership with AIA operating in Australia, Sri Lanka, Taiwan, Thailand, South-Korea, Hong Kong, Singapore, Malaysia, Vietnam and Philippines; partnerships in the US initially with Humana then through a 2016 partnership with John Hancock; a 2016 partnership with Generali operational in France, Germany and Austria; a 2016 arrangement with Manulife Canada and most recently a 2018 partnership with Sumitomo Life in Japan.

There is a lot of variation in the Vitality offer across these settings – in some it is health insurance, in some life, in others both; it may be sold direct to consumers, to employers, or both. In the US, John Hancock sells Vitality branded life policies direct to individuals through a partnership arrangement while Discovery’s US subsidiary, Vitality Group, sells health insurance direct to employers and through brokers; Vitality UK sells health insurance direct to employers, and both health and life insurance direct to individuals; in France the Generali–Vitality partnership sells only to employers.

Despite the variety of product and distribution mechanisms, the central brand value is always behaviour. The program has a common core around three main phases that are customised locally: behavioural assessment, improvement and reward. In France, Generali–Vitality expresses the core reflectively – ‘se connaître, s’améliorer, profiter’ Know yourself; Improve yourself; Enjoy. 5 In the UK, this is rendered as ‘Understand your health, Get healthier, Be rewarded’ while the US has it as Assess, Improve, Track, Reward. 6 The first step centres on completing health checks and reviews. These include standard health assessments including BMI, waist-hip ratio, blood pressure, cholesterol and blood sugar combined with the Vitality Health Review of individual nutrition and wellness habits, vaccinations, dental and cancer screenings. Vitality points are awarded for completing each of these actions. On the basis of these reviews, customers are advised of their ‘Vitality age’ presented as a ‘scientific calculation that assesses the impact of your lifestyle on your health.’ 7

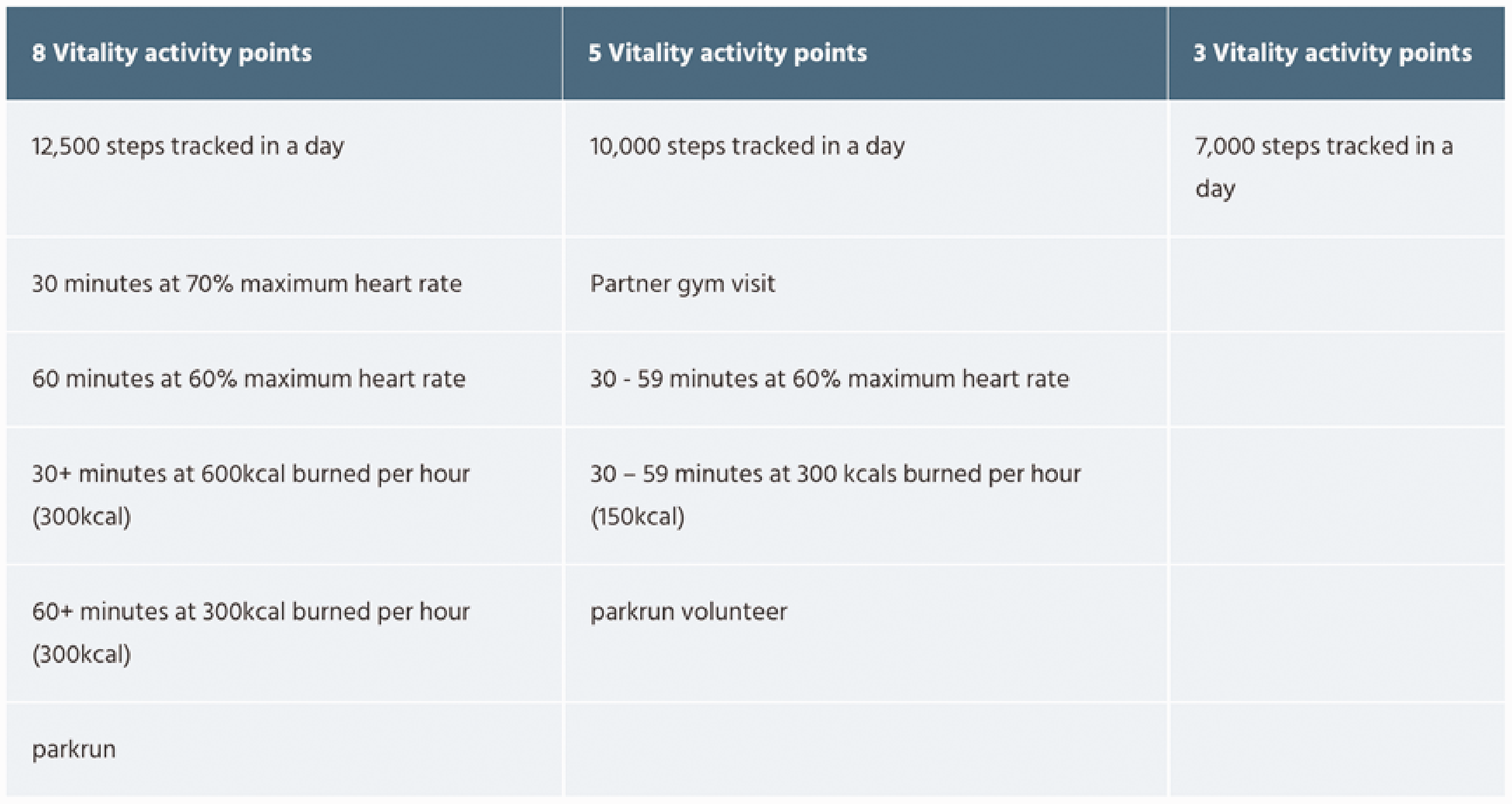

To access program rewards, members have to accumulate points to obtain one of four or five status positions variously labelled as blue, bronze, silver, gold, platinum, diamond, etc. Completing reviews and checks earns initial points, but the core of the program is Improve your health. This is where sharing behavioural data starts to acquire value. Members can still earn points from activities like going to the gym by reporting proof online. Increasingly though, the focus is on the accumulation of points by self-tracking variables such as blood pressure, blood sugar, weight, heart rate and especially physical activity using wearable devices, smartphones and apps. To accommodate different sorts of activity, the program defines a valid workout according to criteria including duration, heart rate, calories burnt, step counts and average speed (see Figure 4).

Vitality points for activity tracking. 14

By earning points, Vitality members improve their status and unlock rewards that again, vary locally. In the majority of territories, the rewards are discounts on sports goods, groceries, hotels, cinemas, Starbucks, Amazon and the flagship reward, a heavily discounted Apple Watch. The most controversial rewards are premium rebates. Rebates, expressed in the UK Vitality program as ‘the more points you earn, the higher your Vitality status, the bigger the rewards and the lower your premium can be,’ are a core part of the offer in British, South African and North American contexts. 8 They are notably absent in other many territories.

This absence appears rooted in both regulatory prohibitions and market resistance. In France, for example, the use of individual tariffs in health insurance is explicitly prohibited under the Loi Évin enacted in 1989 while in Germany premium discounts or paybacks are possible but the regulatory structure of the private insurance market prohibits regular, dynamic, behaviour-based risk-rating (Arentz and Rehm, 2016). In the US, some companies trading in individual markets offer rewards but not premium discounts as this would contravene Obamacare regulations prohibiting price discrimination on the grounds of pre-existing conditions (McFall, 2019). The situation is more complicated in group health, where employers can negotiate premium discounts for introducing self-tracking but even then it is a group not an individual discount that is at stake. It is worth noting too that even where premium discounts are not explicitly prohibited by law, regulations governing, for example, cross-subsidy between high and low risk members, can limit insurers’ economic incentive for adopting them. Social and political resistance is a significant impediment especially in territories with social insurance-based universal healthcare. It is probably not incidental that the Vitality program features premium discounts in the US and South Africa, countries without universal healthcare systems, and in the UK where the National Health Service (NHS) is tax not insurance funded and private health insurance is, at around ten per cent, comparatively rare.

Market resistance, in a cautious and reputation sensitive industry, is a related impediment. In France, Generali–Vitality declined to launch the product in direct to consumer markets and packaged it to employer markets as a social responsibility solution to mitigate reputational damage (Generali Vitality IV #2, 2018). Major insurers have not taken the view that self-tracking data can price individual health risk more accurately (EIOPA, 2019; McCrea and Farrell, 2018). Even if they did come to believe in individual risk modelling it is still uncertain that any efficiency gains would offset the associated infrastructural expenses and reputational costs (c.f. Swedloff, 2015).

If there is no clear margin in individual risk modelling it raises the question of why Vitality places such emphasis on individual behaviour. One answer to this lies in the importance of cultivating market or brand attachment in insurance (Cochoy et al., 2016). Historically, companies have invested heavily in promotional marketing to overcome disinterest and resistance. Initially this usually involved some combination of ‘explaining’ their technical approach to risk and exploiting sentiment, especially fear and shame. In the twentieth century, beginning with the ‘man from the Prudential’ (McFall, 2011, 2014), this involved cultivating a specific brand identity. Most insurers have struggled with this: brand loyalty, recognition and differentiation are all low in a sector that is heavily reliant on price competition where there is annual renewal and customer inertia where there isn’t. There is then some competitive advantage to having a distinctive set of attributes to build a brand identity around. Making behaviour a central brand value sets Vitality apart. It is interesting too that Vitality has chosen internationally renowned brands including Starbucks, Amazon and Apple as reward partners. Apple is widely reckoned the world’s most valuable brand and its customers are loyal to the point of fandom. In partnering with Apple to offer a discounted Apple Watch, Vitality might expect to accrue some benefits by association but there is more at stake. The capacity to provoke a particular version of healthy behaviour is as much at the core of the Apple Watch as it is of Vitality.

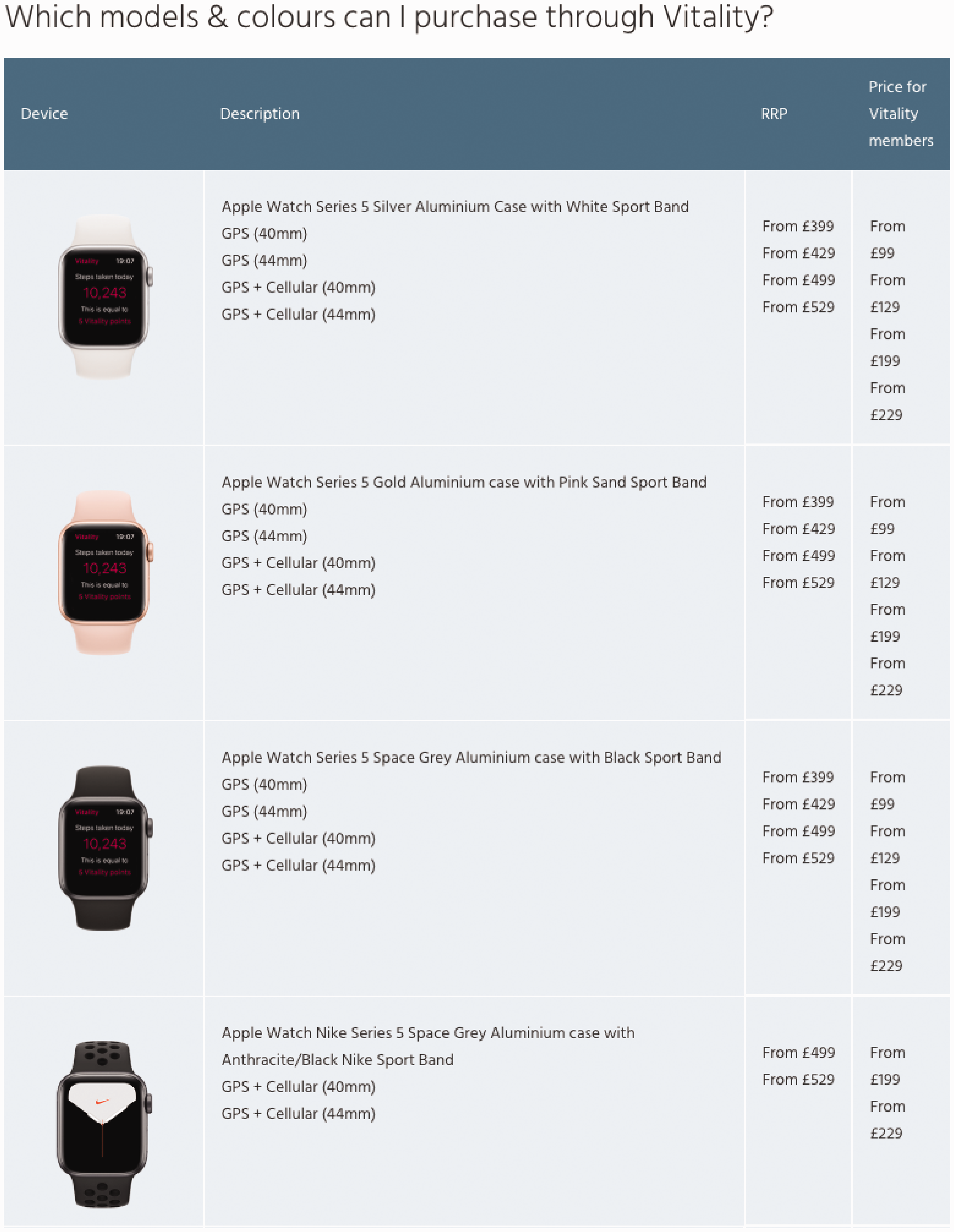

Consider the detailed terms of Vitality’s 2019 Apple Watch Series 5 offer to individual markets in the UK shown in Figure 5. The right-hand columns contrast the RRP with the Vitality price and reveal a potential saving of around £300. This saving can be achieved by members who accumulate 160 points per month over 24 months. The scale slides down in four phases to members who accumulate less than 40 points and will pay the full RRP by direct debit. 9

Vitality Apple Watch Series 5 offer. 15

Vitality points are a behavioural currency. They can be earned through activity and exchanged for goods discounted in line with a dynamic exchange rate. To earn enough Vitality currency to pay for the watch in full you need 160 activity points per month. This averages out at roughly 5.33 points per day which can be earned by taking just over 10000 steps, 30–59 exercise minutes at 60% maximum heart rate, or a parkrun, etc. To meet monthly targets, every month, demands active behaviour in excess of WHO guidelines but failing to do so increases the cost of goods exchanged.

Wearable devices do not determine behaviour, wearers play around with them, forget them and discard them (Neff and Nafus, 2016; Tanninen, 2020). The Apple Watch can claim to be ‘stickier’ than its competitors having acquired 55% of the smartwatch market by 2019. 10 It is a socio-technical attaching device that is fairly successful at seducing and capturing or ‘captating’ its users and algorithmically gaming them into closing activity circles with an ambient interface wrapped in Apple packaging (Callon, 2016; Cochoy et al., 2016). It fits Vitality perfectly not only because of the Apple brand allure but because it is the best available means for provoking the kind of behaviour the company has a proprietary stake in.

BRANDING behaviour: Discovery’s business model

In February 2015, the South African newspaper Business Day published an unremarkable looking story about Discovery. Discovery has partnered with a major US life insurer to launch products developed on the Vitality model in April. The US insurer, which Discovery has not yet named, will launch a suite of products similar to those of Discovery Life in SA. […] Discovery said it had ended its partnership with US health insurance partner for Vitality, Humana. “Humana will continue with Vitality as we built it with them but change its name.” said Mr Gore. (Jones, 2015) It’s at the heart of their intellectual capital, it’s what they sell […] it’s their exclusive right, there are no other programs, so that is something they really don’t want to share […] The product is 90% theirs, the actuarial heart of the product, it’s them, our part was more about marketing. (Generali Vitality IV #3, 2018 our translation)

Annual reports and published corporate histories locate Gore’s idea for Vitality in the plural contexts of South African health care, his experience as an actuary working in product development and his reading of behavioural economics. The Harvard case study produced by Michael Porter, Mark Kramer and Aldo Sesia reports: In late 1997, Gore launched Vitality to the broker community. Built on the principles of behavioural economics, Vitality encouraged sustained behavior change by offering individuals a combination of knowledge tools (information about health), access to wellness partners (e.g., fitness clubs), and financial incentives that increased proportionally as members engaged with the program. In accord with South African law, Vitality was offered separately from Discovery Health’s medical schemes for a monthly fee that covered the cost of the program. Membership was voluntary, but only members of a Discovery medical scheme could join Vitality. (Porter, Kramer and Sesia, 2014: 4)

The theoretical claim that people can be gently nudged away from chronic, preventable, lifestyle-related disease toward better, healthier behaviour rooted in behavioural economics is the practical basis of the Vitality program. This is combined with Michael Porter’s value-chain theory to create the two main characteristics of Discovery’s shared-value model. The first is that corporate social responsibility (CSR) cannot transform relationships between corporate finance, government, global societies and individual people, these relationships have to be completely remodelled. The second is that nudging individuals, businesses and institutions to ‘share’ value will help achieve that transformation.

The word ‘share’ here is doing a lot of work. It invokes, first, centrist, liberally paternalist politics and a new socio-political ‘insurantial imaginary’ mobilised through behavioural underwriting. It is an almost poetic paradox that Francois Ewald – the intellectual architect of Foucauldian approaches to socialised insurance, welfare solidarity and risk – has endorsed this new datafied imaginary (Ewald, 1986, 2012; Ewald and Thourot, 2013). Second, it invokes sharing individual health data. Finally, it invokes sharing in the social media vernacular.

These last two forms of sharing are integral to the Vitality brand, but they have been difficult to accomplish in practice. One element of the John Hancock story that gets lost in translation is that their move to underwriting only interactive life policies means they sell only products that have this feature. This is akin to Apple bundling its proprietary apps in every IoS device. The features are there, but the company cannot force its customers to use them. We do not know the percentage of John Hancock’s customers that are active users of the Vitality program. In the Generali Vitality version, the interactive feature is opt-in for all members but only 20% activate it (Vitality IV#4 2019). This statistic makes it that bit harder for agents and brokers to close the sale.

Insurance sales agents have long been taught that sales cannot be closed by reason alone. As Prudential Assurance once informed its agents through the words of Oliver Wendell Holmes ‘reason may be the lever but sentiment is the fulcrum and the place to stand on if you want to move the world.’ In a datafied environment the lever may be better described as ‘technique,’ meaning an assembly of practice, expertise and technology. At the point of sale in Generali Vitality this lever has to connect with ‘subjectivity, there are emotions, sometimes it’s no longer rational, we completely take off’ (Vitality IV#4 2019, our translation). The phrase we have translated as ‘take off’ is ‘on décolle.’ There is no easy equivalent in English, but it means to have a head in the sky, perhaps to soar. The sales trick is in orchestrating reason and sentiment, keeping both balls in the air.

Provoking individual customers/members to share self-tracking health data on social media is another element of Vitality’s branding behaviour. This is meant to allow the labour of promotion to be distributed (shared) between the company and its customers and ‘increase customer engagement and the number of interactions between the insurer and insured’ (Krüger and Ní Bhroin, 2020: 100). Generali Vitality’s customers have not developed the kind of attachment to the brand that might prompt posting their experience on social media. People often say to us ‘well well, again, something for the bosses, they always find new things to try to make us more productive.’ (Generali Vitality IV #4, 2019 our translation)

Closing remarks

[H]ow do these needs for production and consumption – for sale and purchase – which have just been mutually satisfied by a trade concluded thanks to conversation arise? Most often, thanks again to conversations, which had spread the idea of a new product to buy or to produce from one interlocutor to another, and, along with this idea, had spread trust in the qualities of the product or in its forthcoming output, and finally the desire to consume it or to manufacture it. If the public never conversed, the spreading of merchandise would almost always be a waste of time and the hundred thousand advertising trumpets would sound in vain. (Tarde in Latour and Lepinay, 2009: 49)

To demonstrate this, we used a case study of Vitality, the longest established and best-known brand in the field of behaviour-based or interactive insurance. Vitality are known for promoting wearable based self-tracking through a system of incentives and rewards, notably the offer of a heavily discounted Apple Watch. This scheme, and its prominent incorporation of wearable devices, has been widely read as a sign that health and life insurance is going the way of telematics schemes in vehicle insurance, to individualise premia based on tracked behaviour. We suggest that such an outcome is much easier to accomplish in theory than it is in practice. Risk pricing in insurance is an arcane technical practice conducted in a highly regulated and competitive market context. Even if self-tracking data was to be modelled as a pricing factor it is not clear that there would be sufficient incentive for insurers to use it given the regulatory environment, infrastructural expenses and reputational costs of doing so. There are also reasons to be sceptical about the clinical and actuarial reliability of self-tracking data and the devices and apps used to gather it. Insurance industry actors don’t know how to risk assess the health of individual human beings – they know how to risk assess aggregates, groups, collectives, pools, populations.

Given these impediments what value does behavioural self-tracking have for companies like Discovery? We suggest the answer to this lies in the inextricable connections between risk pricing as a technical practice and the commercial organisation of the sentimental appeal insurance makes to its customers. It is as one nineteenth century writer put it ‘the judgement with which lives are selected, and the premiums improved at interest’ (Porter, 1996: 102), not just the rates at which risk are priced, that determines an insurance office’s success. The Vitality program should be understood in the context of Discovery’s broader corporate and commercial judgement. It provides a means of reaching – or selecting – the type of customers the company wants to insure and nudging them to behave in ways that lower their costs to the company. Through Vitality, Discovery Inc. have made a brand out of behaviour in ways that can be traced in the corporate history of their own branding behaviour and their attempts to protect their intellectual property. The value of sharing lies in maintaining, through the Vitality brand, a lively exchange, a conversation, that maintains the connection between how the company values risk and how its customers value insurance.

Footnotes

Acknowledgements

The paper found its way to publication through the collective and solidaristic chat among a group of insurance scholars especially Ine Van Hoyweghen, Gert Meyers, Arjen van der Heide, Maiju Tanninen, Rick Swedloff, Jim Davey and all the contributors to this themed issue. We are particularly grateful to the three anonymous referees for their help in refining our excitable arguments.

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.