Abstract

Financial inclusion is high on the agenda for governments as well as for organizations such as the World Bank. Research has pointed out that Muslims worldwide are less included in the formal financial system than non-Muslims, but there is no knowledge about the extent to which religious norms (most importantly the ban on interest on money) lead to financial exclusion among Muslims in the West. In this article I approach the issue of financial exclusion and inclusion through three interrelated questions that will be answered with data collected in Norway 2015 and 2016. The questions are: (a) To what extent do Muslims see conventional banking as a problem in their own lives? (b) Do level of education, age, national background or level of religiosity predict demand for Islamic banking? (c) Is demand for Islamic banking changing? This article is a first step in what should be a broader research program to find out whether and how religious norms cause financial exclusion of Muslims in the West.

Introduction

Financial inclusion is high on the agenda for some governments as well as for organizations such as the World Bank. Muslims worldwide are less included in the formal financial system than non-Muslims (Demirguc-Kunt et al., 2013; Financial Services Authority, 2000). For instance, a study of 29 000 people in 29 countries found that Muslims are less likely to have bank accounts than non-Muslims, partly for religious reasons and partly because of discrimination (Beck and Brown, 2011). There is no knowledge about the extent to which religious norms—most importantly the ban on interest on money—lead to financial exclusion among Muslims in the West. In the research literature about European Islam, the issue of Muslims’ perception of finance and economic matters is hardly mentioned. An authoritative 2012 review article about research on Islam in the West did not mention the topic at all (Voas and Fleischmann, 2012).

The financial inclusion of Muslims in Western societies is a precondition for the political empowerment and full participation of this growing religious minority and it is, therefore, an issue of political importance. If financial products that comply with Islamic values could be one element in such inclusion, it will be necessary to ask whether regulatory adjustments need to be made in order to create a level playing field for potential suppliers in this market. The issue of the potential roles of Islamic finance in the inclusion of Muslims in the West touches on core themes in political research, such as integration, participation, and trust in institutions. At the same time, this is about Islam in global politics because the concern with finance and economics shown by Muslim intellectuals from the 1960s and the proliferation of Islamic banks from the 1970s may be understood as an element in a global revival of Islam (Kepel, 2003: 75–80; Pal, 1999). In research about the historical emergence of Islamic finance it is common to see the trend as an element in a process of Islamization taking place across the world and affecting Muslim communities in the West (Saeed, 2014).

Research questions

I ask three interrelated questions that will be answered with data collected in Norway during 2015 and 2016. The data include: a survey of just over 700 Muslims; 10 interviews; and three focus groups. The questions are as follows.

To what extent do Muslims see conventional banking as a problem in their own lives?

Do level of education, age, national background or level of religiosity predict demand for Islamic banking?

Is demand for Islamic banking changing?

This article is a first step in what should be a broader and more ambitious research program to find out whether and how religious norms cause financial exclusion of Muslims in the West. I have chosen to focus on Muslims in Norway in order to get a better grasp of how religious norms impact Muslims’ thinking about finance. This was convenient because of my own extensive contacts in Norway. It is also a relevant population because Norwegian Muslims are a highly diverse group in terms of ethnicity, length of stay, reason for migration, and degree of religious commitment. As in most Western countries there is no Islamic banking alternative in Norway, which means that anybody who shuns the services of conventional banks will be financially excluded.

Brief historical background

There are two opposing strands in the modern Islamic debate about finance. The core of the disagreement is the Quranic ban on riba, translated in the widest sense as “interest” (Thomas, 2006). On the one hand, there are the modernists who want to adjust an Islamic perspective on economics to the modern world. They are of the opinion that riba in the Quran refers only to a particular kind of usurious interest on loans taken by moneylenders in pre-Islamic Arabia. On the other hand, there are the traditionalists who cast the net wider and insist that riba in the Quran covers all kinds of interest on money, which makes most types of conventional banking practices prohibited. The most important traditionalist was the Indian writer Maulana Maududi (1903–1979). He was keen to show that profit from trade was encouraged by the Quran, but that profit derived from lending money was prohibited (Maududi, 1969: 165). Islamic banking in its current forms started in the 1960s. In 1963, an interest-free bank was started in Egypt, but it was closed down by the authorities in 1967 (Visser, 2013: 119). From the early 1970s several Islamic banks were established in the Middle East. This development coincided with the political turmoil in the wake of the energy-crisis and the oil embargo of 1973 and the new crisis following the Iranian Revolution of January 1978–February 1979. This led to new wealth and growing self-confidence in parts of the Islamic world, particularly in Saudi Arabia.

Muslims in Norway

In 2017 there are 148,000 members of Muslim organizations (mosques) in Norway, which is around 2.8% of the Norwegian population (Statistisk Sentralbyrå, 2017). Many of these organizations are organized in the umbrella organization Islamic Council of Norway, which works to promote the interests of members and create understanding for Islam in Norway (http://www.irn.no/om-irn/). In addition to members of religious organizations there are Muslims outside these organizations. Depending on how one defines “Muslim” the total population is around 200,000 or just under 4% of the population (Statistisk Sentralbyrå, 2017). The oldest Muslim groups in terms of national background are immigrants (and their children and grandchildren) from Pakistan, Turkey, and Morocco who came as migrant laborers in the 1960s and early 1970s. In the 1980s there was substantial immigration of refugees from Iran. 55% of Iranians in Norway said in 2016 that they do not belong to any religion reflecting their rejection of the political Islam of Iran after 1979. Among Muslims from all other countries attachment to Islam is far stronger, with Somalis and Pakistanis showing the strongest identification with the religion in which they were brought up (Rapporter, 2017/13: 85–87). From the 1990s, Muslim immigration has been dominated by refugees, first from the Balkans with Bosnia as an important country of origin and later from Somalia, Iraq, Syria, and Afghanistan. In terms of research, it is challenging to take a good sample from this diverse population (Rapporter, 2017/13: 25–28). In research about Muslims in Denmark it has been recognized that many persons of Muslim background—and of Muslim faith or practice—are not members of religious organizations and that it is important to use research methods that reach Muslims who are non-organized (Jeldtoft, 2011; Kühle, 2011). However, as I mentioned above 148,000 out of roughly 200,000 Muslims in Norway are in fact members of mosques. The percentage in Denmark is far lower and my best guess is that this is a consequence of public funding mechanisms creating different incentives. Therefore, the caution against relying on networks in mosques to recruit respondents may be right for Denmark but not for Norway.

The survey

The development of a survey questionnaire that would be as relevant as possible to the target group was done by the author together with a reference group of 12 Muslims in Oslo. In the reference group both men and women were represented and there was diversity in terms of age and professional background. Drafts of the questionnaire were tested and revised. The questionnaire was made available in Norwegian, English, Arabic, and Urdu. Between September 2015 and April 2016, we collected 707 responses to the survey. We employed two strategies for reaching respondents. Firstly, a research assistant collected paper questionnaires face-to-face from persons who identified as Muslims. He visited five different cities in Norway and collected responses from several types of organizations, including mosques and student organizations. These responses were collected from persons who were present when the research assistant visited the organizations. This type of convenience sampling is clearly vulnerable to selection bias and cannot give a sample that is representative of the Muslim population. However, by targeting religious and non-religious organizations and various national backgrounds we created a sample that was as good as it could be given our resources.

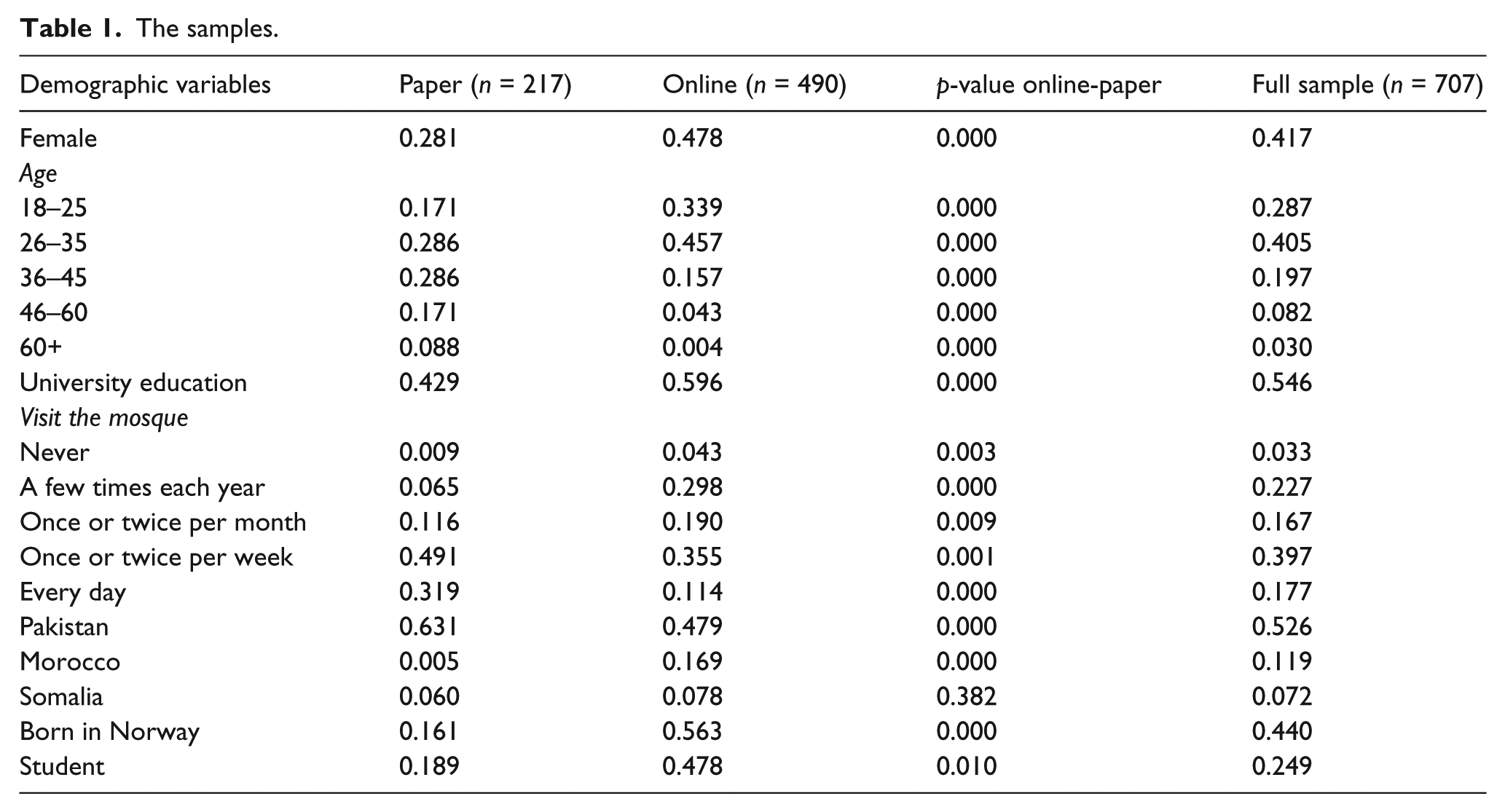

Secondly, with assistance from the University of Oslo we created an online questionnaire that was sent out through personal networks. The online questionnaire could only be filled out once for each e-mail address, but the invitation to participate with the link to the questionnaire could be forwarded to others by anybody who received it. These two approaches in effect created two different samples with 217 responses on paper and 490 responses online. As we see from the p-values in Table 1 the two samples were drawn from different groups of Muslims in Norway. The online sample has a more equal distribution of men and women, while men dominate in the paper sample. In Table 1 we list key demographic variables of the two samples: paper; and online.

The samples.

To assess the effect of sampling, I first ran a logistic regression, with sample as dependent variable. This analysis underlines the conclusion drawn by comparing sample means, and shows that apart from gender, being a student, and coming from Pakistan, all demographic variables are significantly different in the two samples, even when controlling for other demographic variables. This shows that oversampling from a specific demographic group cannot explain the sample differences.

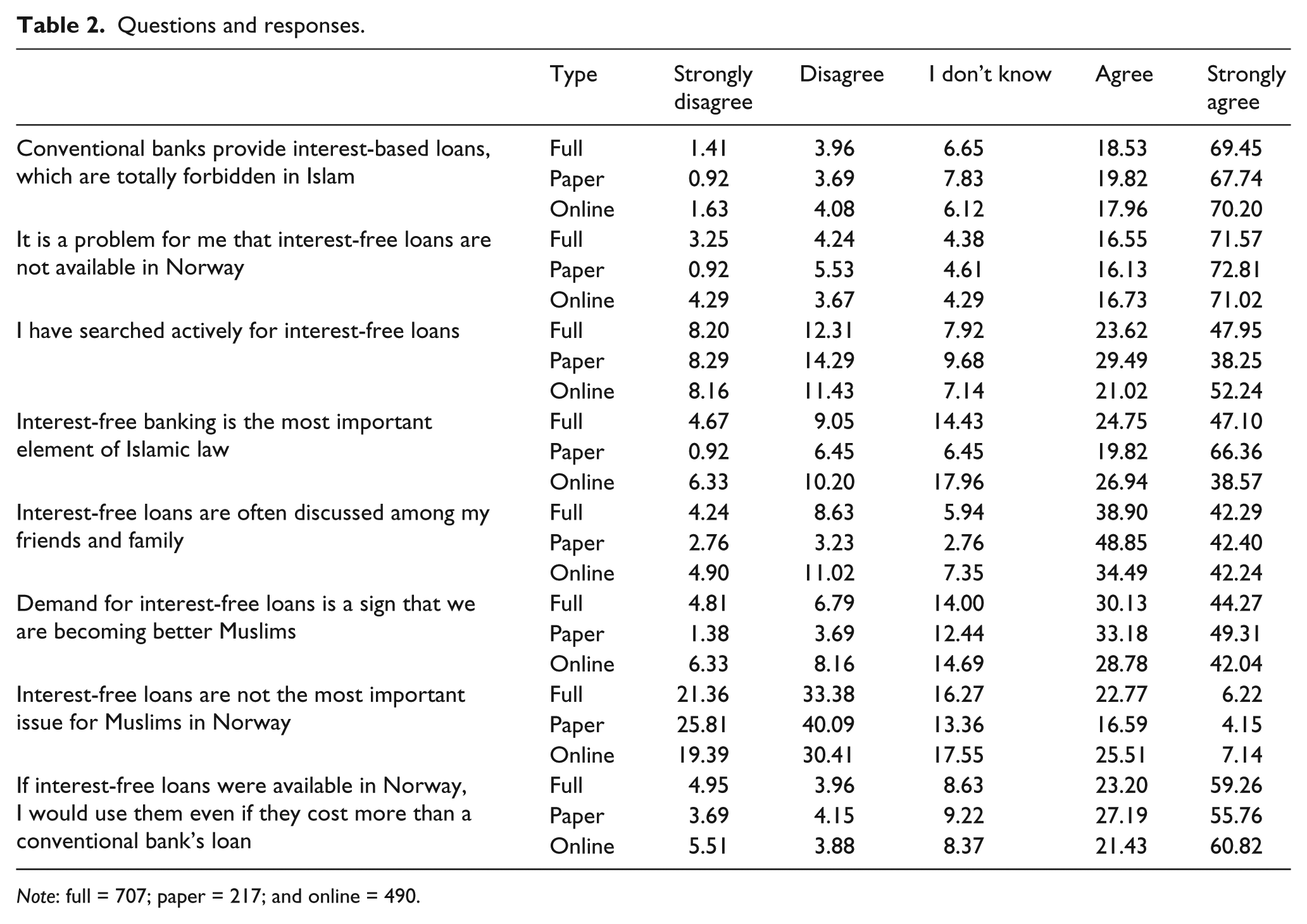

I assessed whether the respondents gave systematically different answers in the two samples, when controlling for demographic variables that could plausibly explain differences in the answers. In Table 2 we list responses to eight statements about interest-free loans. We presented all 707 respondents with statements on a five-point Likert-scale from strongly agree to strongly disagree. In the column called type we list the sample from which the answers are taken. Full means that we look at both samples combined, paper means that we look at the responses to the paper survey in isolation, while online means responses from the online survey in isolation. We can see that the two samples on the whole do not diverge dramatically in their general attitudes to interest-free and conventional loans.

Questions and responses.

Note: full = 707; paper = 217; and online = 490.

A difference between the two samples can be seen in the responses to the statement “I have searched actively for interest-free loans” to the effect that 52.24% in the online sample strongly agree while 38.25% of the paper sample strongly agree. However, if we add up those who either strongly agree or agree to this statement we see that the difference is far smaller with 67.74% in the paper survey and 73.26% in the online sample. Also, very similar numbers disagree or strongly disagree. The other statement where there seems to be a difference between the two samples is “Interest-free banking is the most important element of Islamic law.” In the paper sample 86.18% either agree or strongly agree to the statement, while in the online sample 65.51% do the same. Conversely, a higher percentage in the online sample disagrees with the statement and 17.96% say they do not know, which could mean that they simply do not think much about Islamic law. There would be several ways to interpret this difference.

For several variables, the respondents answer systematically different, even when controlling for demographics, at a 5% significance level. Furthermore, other variables are close to attaining statistical significance. This indicates that sampling strategy matters a lot for which conclusions we draw when studying Muslims in the West. Future studies could calculate effects from different sampling strategies to address robustness concerns. However, the limited size of my paper sample gives little statistical power when splitting the samples. Therefore, I focus on the combined sample when looking at substantial relationships.

Q1: To what extent do Muslims see conventional banking as a problem in their own lives?

As a first approach to the issue of potential financial exclusion as a result of religious norms the first four statements in our questionnaire address the issue of how Muslims think and feel about conventional bank loans, that is, loans with interest. From the responses to these four statements we see that a very large percentage of our sample(s) see conventional banking as forbidden according to their religion. Almost 90% agree or strongly agree with the statement that conventional banks provide interest-based loans, which are totally forbidden in Islam. The same percentage agree or strongly agree that it is a problem for them personally that interest-free loans are not available in Norway. Statement four is an attempt to find out how Norwegian Muslims think about Islamic banking in legal terms. There is a difference between our two samples on this point with 66.36% of the respondents in the paper sample and 38.57% in the online saying they strongly agree with the statement “Interest-free banking is the most important element of Islamic law.” I believe this illustrates that the issue of finance is of real importance to many Muslims in Norway and that the lack of a Sharia-compliant banking alternative is perceived as a real challenge. The difference between the two samples in the responses to the fourth statement could perhaps be due to less overall interest in Islamic law in the online sample, but this is impossible to say with certainty. All in all, the responses to the first four statements indicate that conventional banking—and a lack of an Islamic option—is a more serious challenge to the economic integration of Muslims in Norway than anybody has imagined, in research or in politics. Financial exclusion would easily translate into forms of socio-economic disadvantage, for instance lower rates of homeownership. Data from Western countries show that Muslims have a lower degree of homeownership than non-Muslims (Engebrigtsen and Farstad, 2004: 26; Maurer, 2005; Tameme, 2009, especially Chapter 6).

We may compare these results with data from the qualitative elements of the project. I carried out 10 long interviews and three focus groups. Seven of my interviewees were positive to Islamic banking and felt that they personally would benefit if these services were established in Norway. A 43-year old man said: “I have many friends who have sold their houses and are now waiting to take an Islamic loan to buy a new house.” I have encountered this type of experience numerous times also outside formal interview situations when talking to Muslims in Norway about finance. It would be surprising if we would not find some comparable patterns in other European societies since the Norwegian Muslim population and their political and economic context are not fundamentally different from those found in neighboring countries. Seen together there is little doubt that in our samples there is a real sense in which Muslims feel it is a problem that they have to use conventional banks if they want to take a mortgage.

Q2: Do level of education, age, national background or level of religiosity predict demand for Islamic banking?

I looked at how the responses to our questions correlated with age, education, with the frequency of mosque visits, and with two types of national background, Somalia and Pakistan. We focused on these national backgrounds because they are the most numerous in our samples and in public statistics of immigrant groups with a Muslim background in Norway.

Age, level of education, and national background had little effect on how respondents replied to the statements in our survey. However, the effect of frequency of visits to the mosque had a clear effect. We placed those who visit the mosque every day and those who visit the mosque once or twice per week on the category “Often visit the mosque,” and we placed those who say they never visit the mosque and those who say they visit the mosque a few times per year in the category “Seldom visit the mosque.” In Figure 1 we see that those who visit the mosque often tend to agree more strongly to most of the statements except for the statement where the value is reversed, i.e. “interest-free loans are not the most important issue for Muslims.”

Responses and frequency of mosque visits.

The trend among those who seldom visit the mosque is even clearer. This group tends to disagree far more than the average with all statements. It is tempting to take the frequency of visits to the mosque as a proxy for religiosity. Good measurements of religiosity need to include a variable about individual religiosity, such as praying alone or belief in God. Visits to the mosque is an expression of the degree to which an individual takes part in public religion. Mosques serve other functions as well—social or educational purposes, for instance—but it would not be unreasonable to say that we have found what is likely to be a correlation between strength of religiosity and interest in Islamic banking.

Q3: Is demand for Islamic banking changing?

During my background work to this research, I talked to a large number of Norwegian Muslims of varying ages and national backgrounds and I was often told that the awareness about Islamic economics as an important focus for personal piety and religiosity had become more important over the past 8–10 years. Some would point to a survey carried out by the Norwegian bank DNB in 2007. The bank interviewed 200 customers with Muslim names about their potential interest in Islamic financial products. In the survey 57% found it very interesting and 21% somewhat interesting to become a customer if a bank was certified according to the principles of Islamic banking.

My research did not contain any longitudinal element and we have no historical data about our subject matter to compare present data with. Therefore, it is not possible to say anything certain about change. However, we can use some of the qualitative data collected to say something about how Muslims perceive the question of change. A 70-year old man related an experience of slowly coming to realize the importance of religion in economic matters: He said: “It was not normal to take a loan from a bank at that time. We got some money from parents perhaps. We expected to go back to Pakistan. But later we realized that we would stay on in Norway. Then we looked around and there was no Islamic alternative. Then we became more established. We had time to think about Islam. In the early time we had no time because work took all our time.”

This quote sums up a life-story that is common among the Muslims who arrived in Norway from the late 1960s till 1975 when the country imposed a ban on labour immigration (Tjelmeland and Brochmann, 2003). In this period Pakistanis, Turks, and Moroccans established themselves as guest-workers in Norway. Most of them came alone and planned on staying for a limited time. They worked hard and had relatively little to do with religion. However, after a while many realized they wanted to stay and they established families. With family life greater religious needs necessarily emerged, the need for life-cycle rituals, for instance (Vogt, 2008). Both individual interviews and discussions in focus groups gave an impression that Muslims themselves believed that the awareness of Islamic economics had grown over the past decade, and that demand for new financial products had increased accordingly.

Discussion and future research

The social and economic inclusion of Muslims in the West presupposes full financial inclusion, but neither researchers nor policy-makers know anything about the extent to which Islamic norms make Muslims shun conventional financial services. There is hardly any research about the demand for Islamic financial products in the West (but see Dar, 2004; Tameme, 2009). Muslims in our samples felt that using conventional banking is wrong and that the lack of an Islamic alternative is a real problem in their own lives. There is a real possibility that religious norms against conventional banking cause financial exclusion, although our research did not specifically look at actual use of conventional banks. In this article, we have mapped elements of a religious mentality that might cause financial exclusion. If future research uncovers that religious norms do in fact cause financial exclusion, this would raise the question about what to do with this. Financial exclusion on religious grounds should generate debate about possible ways to deal with the problem.

We found that the only socio-demographic variable that had a clear relationship to demand was frequency of visits to the mosque. Contrary to what we expected, younger and higher educated Muslims did not seem to have greater demand for Islamic banking. We cannot say much about change over time, but among the Muslims who were interviewed in this project there was a tendency to see Islamic economics as a topic that had emerged as an important marker of personal piety and religious identity over the past decade.

I said that this article is a first step in what should be a broader and more ambitious research program. In August 2017, I initiated a three-year, collaborative research project supported by the Research Council of Norway that aims to fill more of the knowledge gaps by collecting data from four European countries: Norway; Denmark; Sweden; and Finland (see: https://www.prio.org/Projects/Project/?x=1776, for more information).

Footnotes

Acknowledgements

I would like to thank Mian Tayyib and Erlend Langørgen for excellent research assistance. I also thank Mr Fazal Hadi of the Islamic Cultural Centre, Oslo, Professor Mehmet Asutay of Durham University and Professor Muhammed Azeem Qureshi of Oslo Metropolitan University for their help and comments.

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: The research for this article was funded by Finansmarkedsfondet.

Carnegie Corporation of New York Grant

This publication was made possible (in part) by a grant from Carnegie Corporation of New York. The statements made and views expressed are solely the responsibility of the author.