Abstract

Objective:

2014 marked a rising public commitment to universal health coverage in Vietnam to eliminate the financial burden for patients, but there are lots of hindrances. It is evident that patients met difficulties to validate their insurances, so health insurance does not significantly address out-of-pocket payments issues. Furthermore, the unequal geographical distribution of hospitals in Vietnam has created an inequality between non-residing patients and residing patients; the former usually pay more. This calls into question how the validity of healthcare insurance and patient’s residence could be related to patient’s financial status and their satisfaction with health insurance.

Methods:

Bayesian regression models are employed to analyze a data set of 1042 inpatients in hospitals of all levels in Northern Vietnam.

Result:

The results show that living in the same region as the hospital and having valid insurance is negatively correlated with the impoverishing risk. Regarding patients’ satisfaction with health insurance, it is negatively correlated with having a residence in the same region as the hospital but positively correlated with higher socioeconomic status and insurance validity. Finally, on average, the satisfaction of patients who have already recovered from the illness and those who quit early is lower than that of patients who needed follow-up in medical care or stop in the middle.

Conclusion:

This article suggests that policymakers consider addressing the unequal geographical distribution of hospitals and healthcare quality to help patients avoid going to hospitals outside their regions, which may generate a financial burden for patients and lower their satisfaction with health insurance.

Introduction

Having valid insurance in Vietnam is extremely important when receiving healthcare. In 2013, a Vietnamese was in an emergency state, and the total cost of treatment was more than 100 million VND. 1 Since the hospital’s insurance department told his wife that his treatment would be covered by insurance, she borrowed money using their house as collateral, reassuring that the money reimbursed by the insurance would help her pay the debt. However, the district’s insurance agency where they lived refused to pay for the treatment because that particular treatment in that hospital is not covered by insurance, while it is in some other hospital. Since the health insurance was recognized as invalid, the patient did not have their treatment covered by insurance, and their family was facing a risk of falling into destitution.

This is just one story among thousands of patients whose treatments are not paid by insurance. In 2016, out-of-pocket (OOP) payment accounted for 41% of the national aggregated health spending, while nearly 76 million people (approximately 81% of the population) had already had insurance in the same year. 2 In 2002 and 2010, 3.4% and 2.5% of the population became impoverished in Vietnam due to OOP payments for health care. 3 This calls into question whether having invalid health insurance could alleviate the impoverishment of a patient and which factors could adversely affect patients’ financial situation.

There has been an unequal geographical distribution of hospitals in Vietnam for a long time, 4 and this encourages patients to seek healthcare and treatment in hospitals even without valid insurance. Currently, the geographical distribution of hospitals in Vietnam seems to favor affluent and densely populated areas. High-quality healthcare facilities and medical staffs concentrate in urban areas, whereas provincial hospitals in rural areas often lack advanced facilities and human resources. Apart from the difference in quality between urban and rural areas, healthcare provision is drastically different between levels of hospitals. The public hospital system in Vietnam is divided into three levels: district hospitals (684 units), provincial hospitals (419 units), and central/national hospitals (47 units). 5

In comparison with medical facilities of lower levels, high-level hospitals provide more healthcare services, especially those requiring high technical skills. Still, most of them are located in municipal cities (e.g. Hanoi, Ho Chi Minh City, and Can Tho). Due to this quality gap and the skepticism about treatment in the commune and provincial hospitals, central hospitals in metropolitan cities are usually overcrowded with patients and out of bed for inpatients, even though they could be well treated in local facilities. The concern over the quality of local medical facilities and the quality gap between high-level and low-level facilities encourage people to travel to cities for the best treatment. However, travel costs and accommodation can be a financial burden and are not covered by insurance.

Given the imbalanced geographical distribution of medical centers and the quality gap of healthcare service across the country, the law on health insurance had been gatekeeping people from having treatment in the hospital they want with valid insurance. The government restricted the primary facilities people could register their insurance at. For many, they could only register the district/commune medical centers located near their place of residence as their primary facilities. If they want to use health insurance to cover their expense in provincial or national hospitals, a referral from the medical staff of the primary facilities must be obtained and sent to the hospitals where the patient is transferred to. Otherwise, bypassing lower-level hospitals for higher quality service could financially hurt people. 6 Exceptions exist for certain groups (e.g. students and poor and near-poor people); they could register provincial or national hospitals as their primary medical facilities.

Due to this regime, many inpatients could not have their health expenses covered by insurance when receiving treatment in provincial or national hospitals. Some inpatients do not have their expenses covered by insurance due to the lack of knowledge about the procedure to transfer hospitals, having treatment that is regulated to be not covered by insurance (especially ones requiring high technical skills) and other reasons. The expense for healthcare and treatment in national hospitals could severely hurt their financial health.

The uneven distribution of hospitals in Vietnam might be a bumper on the road to fulfilling the government’s ambition to cover 100% of the population. Patients who travel far to have a treatment that is not covered by insurance could feel dissatisfied with health insurance, even though their health problems have been well treated. Even people who went to local hospitals near their homes would not be satisfied with the health insurance because those hospitals might not be the ones they want. They go to the primary facilities that they registered for the sake of financial health. In these situations, patients’ satisfaction is influenced by the validity of their insurance and whether they live near the hospital. Even though these factors should be considered when evaluating satisfaction regarding healthcare insurance, they have been ignored.

When many governments worldwide are trying to achieve universal healthcare coverage, the factors affecting patients’ financial status and their satisfaction with the health insurance should be of great concern. Research into health insurance in Vietnam has assessed the catastrophic health expenditure or OOP payment,7,8 the impact of insurance to reduce financial burden, 9 and household vulnerability to healthcare cost.10,11 Research also assessed the financial protection of health insurance regarding the level of healthcare providers 12 and the financial burden associated with residence. 13 Nevertheless, no research has assessed how the validity of health insurance and residence on financial distress and patients’ satisfaction with health insurance. However, it is necessary to answer this question because it is not the fact of having insurance. Still, the fact that health insurance is valid to the healthcare providers helps patients reduce financial burden significantly. The association between residence and satisfaction with health insurance is also yet examined even when going to hospitals far from residence might generate cost which is not covered by insurance. With a data set of 1042 inpatients in Vietnam, this article evaluates the impact of healthcare insurance on patient’s financial status and how patient’s residences could have an economic effect due to the unequal distribution of healthcare and hospitals. Although this model has been examined by Vuong 14 with the frequentist approach and Ho et al. 15 with the Bayesian approach, there are several reasons to re-examine this relationship. The former research has only been interpreted with a subset of 330 observations. Hence, this article employs a bigger data set using the Bayesian model built but interpreted in Ho et al. 15 and tested whether patient satisfaction regarding health insurance is affected by residence.

Literature review

Health insurance in Vietnam

Health insurance was introduced in Vietnam in 1993 to alleviate the financial burden for ill households. Since then, the enrollment rate only improved significantly, especially after the law of health insurance in 2008, which was implemented from the beginning of 2009. At the time of 2016, there are two main schemes of health insurance: compulsory health insurance and voluntary health insurance. The former is Vietnamese with employment contracts of at least 3 months, civil servants, the disabled, veterans, and other groups regulated by the government. Voluntary health insurance covers those without compulsory health insurance (self-employed person, workers in informal sectors, etc.). The latter only appeared after the law amendment in 2003.16–18 In addition to these schemes, there are two special schemes: one for the poor and children under 6 years old. The social health insurance enrollment rate increased substantially over the years. In 2008, the social health insurance program only covered around 41% of the population.11,19 The number was 58.3% in 2009, 66.8% in 2012, and 89.3% at the end of 2019. 20 However, the voluntary insurance enrollment rate remained low at the time of this research. 21

The financial protection of health insurance and patient’s satisfaction with health insurance

At the time of this research, patients would have a substantial amount of healthcare and treatment expenses covered by insurance if their healthcare insurance is valid to the healthcare providers and if healthcare insurance covers the type of treatment. The two criteria are simple, but there are several obstacles to fulfill both.

During the period covered in this study, there are public and private healthcare service providers in Vietnam. Still, healthcare insurance does not cover checkups and treatment costs in most private institutions.22,23 Studies found a strong substitution effect from private medical facilities to public ones.23,24 Regarding public hospitals in Vietnam, they are classified into four levels: commune level, district level, provincial, and central levels. Except for some special groups (such as students or poor people), many people could only register at commune or district level facilities. The list of facilities available for registration is restricted based on the insured’s residence and working place.25–27 Suppose the insured goes to the medical facilities where insurance is registered. In that case, at least 80% of medical checkup and treatment expenses for one visit will be covered, and the covered expense could be more generous for groups such as the poor or soldiers.

Meanwhile, expenses at an unregistered hospital would not be covered by insurance unless the patient is transferred according to a reference letter of medical staff from the registered facilities, as regulated in Circular on transfer between medical facilities issued in 2014. 28 Without a reference, the insurance will be recognized as invalid, and the medical bills will not be fully covered, increasing OOP payment significantly. In the case of the insured using healthcare service in a central hospital without valid insurance, only up to 40% of the checkup and treatment expense will be covered in the case of inpatients. Outpatients will have to pay the cost by themselves. Despite being sensitive to medical costs, 29 many patients go to hospitals where their insurance is not registered, mostly because of the unequal geographical distribution of hospitals in Vietnam and the skeptics about healthcare service in hospitals of lower levels. In central hospitals, the rate of patients whose insurance was registered elsewhere reached 75% during the 2008–2009 period. 30 Even when patients could be treated well in lower-level hospitals, they would rather receive treatment in higher-level hospitals. For example, 90% of patients in the Outpatient Department of the Vietnam National Children’s Hospital (a central hospital in Hanoi) could be treated in lower-level facilities. 30

The validity of the insurance also depends on the type of healthcare service and treatment. The government restricts medical checkups, technologically advanced treatments, and medicine covered by health insurance. As of 2016, the list of 177 technologically advanced treatments covered by insurance is regulated in the government’s “Decision No. 36/2005/QD-BYT,” which includes several cancer treatments, transplants, and certain treatments for kidney and heart. In 2014, the government issued Circular No. 40/2014/TT-BYT on the list of medicines covered by insurance, such as medicines for chronic kidney failure treatment and undernutrition. However, the procedure to receive payments by insurance is complicated, and many patients faced the risk of impoverishment due to information asymmetry. The medical expense of patients, who received technologically advanced treatments at the hospital where they registered their insurance, would not be covered by insurance if the Ministry of Health had yet approved that hospital to provide such treatments and allowed these treatments to be covered by health insurance. 1 Patients have reported to pay a fortune for healthcare and have to cope with poverty when learning that their insurance will not cover their expenses at the registered hospital. 1

The unequal distribution of hospitals, the complicated procedure to transfer hospitals, and the difficulties to validate one’s healthcare expense to be covered by insurance brought in a situation where patients could not have their expenses covered while owning insurance. Such complications, even when having valid insurance, upsets many patients and could hurt them financially.

When the previously reviewed documents suggest that the financial benefits of healthcare insurance in Vietnam vary depending on the situation, we also find a mixed result about the financial effect of health insurance in Vietnam and worldwide. Vuong 14 suggests that two out of three uninsured and non-resident inpatients in Vietnam will be impoverished due to medical costs. He also stresses the high risk of destitution that uninsured patients face upon the occurrence of hospitalization. Health insurance also contributes to the decreasing frequency and amount of debts for healthcare. 31 Meanwhile, the economic effect of health insurance was found to vary across different schemes. 32 In detail, while the voluntary scheme reduced OOP payment significantly and the health insurance programs reduced the aggregate OOP payment, the heavily subsidized health insurance schemes (for the poor and near-poor people) did not decrease the amount of OOP payment. In a study of insurance programs across the world, Lofgren et al., 33 reviewing 8755 abstracts and 118 articles about public health insurance in low- and middle-income countries, find a mixed effect of increasing insurance coverage, even though it tends to improve financial protection and health condition as well as access to health services.

Patient’s residence, its effect on patient’s financial situation, and satisfaction with healthcare insurance

As mentioned, hospitals and health facilities are unequally distributed in Vietnam. Many patients went to unregistered hospitals located in urban areas for checkups and treatment. This potentially generates more costs other than the expense for healthcare services. According to Nguyen, 13 patients treated at the hospitals were paid an average of 28 million VND (US$1208) in total costs, and the non-resident patients will have to pay approximately 1.36 million VND (US$59) higher for the relatives who accompany him or her to the hospital than the resident patients do. Going to hospitals outside the region of residence also generates travel costs for patients and his or her companion, even when patients are transferred to hospitals with valid insurance. Even though insurance covers the expense of moving the patient and medical checkup before transference at the registered hospital according to Circular No. 14/2014/TT-BYT and the Law on Health Insurance in 2008, insurance does not include the insurance travel cost of the companions. Revisiting hospitals far from the place of residence is also inconvenient and costly. In China, Liu et al. 34 show that 88.4% of the respondents prefer primary health institutions (village clinics and township hospitals) since revisits are more convenient when they live closer to the hospital. Fiestas Navarrete et al. 35 observe geographically distributed effects on medical access and OOP payment reduction: the nearer to the hospital one lives, the less the financial risk is. In general, the literature suggests a negative relationship between going to a hospital far from residence with a financial burden.

According to Circular No. 40/2015/TT-BYT, most insured groups must register their insurance at commune or district medical facilities near their residence or workplace, except when the commune or district lacks facilities or the insured belongs to special groups. When healthcare quality varies across regions, this restricts patients from registering insurance at the hospital they want. According to the insurance regulation, patients’ dissatisfaction with the procedure to transfer to reputable hospitals has been reported for several years.36–38 Medical staff in higher-level hospitals also met difficulties to transfer patients to lower-level hospitals when patients could be treated well in lower-level facilities. This is because many patients and their families were skeptical about the quality of lower-level hospitals near their place of residence. This hints at a difference in satisfaction level with healthcare insurance when patients are treated in different hospitals assigned according to their residence, even when the treatment outcome is the same.

Research questions

Since having invalid health insurance and going to hospitals in other regions imposed certain financial burdens, understanding the patients’ financial burden needs to examine the correlation of patients’ post-treatment financial situation with patients’ residences and the validity of their insurance.

RQ1. Is the patients’ financial status after treatment associated with their residence and the validity of health insurance?

Furthermore, the factors which could influence patients’ satisfaction with health insurance should be examined. This article examines four potential factors (treatment outcome, socioeconomic status, residence, and the validity of their insurance) based on the literature. First, patient’s opinions about health insurance could change due to patients’ socioeconomic status. As Thuong et al. 32 suggested, the financial effect of health insurance in Vietnam varies across schemes. The heavily subsidized programs (for the poor, near-poor, and disadvantaged groups) do not reduce the OOP payment. This might adversely affect the attitudes of these groups toward health insurance. Socioeconomic status also increases willingness to pay for health insurance, 33 associated with higher patients satisfaction. 39 Second, the patient’s residence could determine the hospital where the patient could register their insurance. This will not be a matter if the quality of healthcare service is equal across regions. When it is not, residence-based insurance limits patients’ ability to register insurance in regions where healthcare quality is better. Third, for the sake of maximizing the financial protection of the insurance, patients might forgo the chance of having better treatment outcomes and vice versa. Hence, treatment outcome and the validity of health insurance might influence their satisfaction with the insurance. For these reasons, this article seeks to answer the following question:

RQ2. Are patients’ satisfaction with their health insurance associated with treatment outcome, their socioeconomic status, residence, and the validity of their insurance?

Method and material

Material

The current analysis employs a data set of 1042 records of inpatients in hospitals across 19 out of 25 provinces and cities in Northern Vietnam, described by Ho et al. 15 An early subset of the data set was deposited in Vuong and Nguyen 40 and used for analysis.41,42 The data set, collected from August 2014 to March 2016 by a collaboration between hospital personnel and a research firm in Hanoi, contains information regarding patients’ demographic traits, socioeconomic status, views about the treatment service, and medical cost.

The interviewees are inpatients who were randomly chosen from records in hospitals in the Northern area from all levels: district level (An Lao District General Hospital, Nong Cong District General Hospital, etc.), provincial level (Hai Duong Province General Hospital, Hai Phong Hospital of Obstetrics and Gynecology, Thanh Nhan Hospital, Viet-Tiep Hospital, etc.), and central level (Viet Duc Hospital, Bach Mai Hospital, Central Tropical Diseases Hospital, etc.). Interviewers approached interviewees individually and explained ethical standards and the issues related to sensitive data such as personal income, the amount of “thank-you” money before asking questions. Because the data set tackles some sensitive information, it sometimes took several weeks to persuade a patient to participate. The first survey round was conducted from 10 August 2014, until the first week of February 2015, the response rate is 40%, and the number of qualified answers is 330. The survey was continued until March 2016. The final total number of qualified answers is 1042 responses. Previous research papers analyzed the subset of 330 observations. 14 Thus, this article can be considered a much-needed replication study that used the final data set of 1042 observations and the Bayesian statistical approach to answering the two research questions mentioned earlier.

This survey met the ethical standards of the Interna-tional Committee of Medical Journal Editors (ICMJE) Recommendations, the World Medical Association (WMA) Declaration of Helsinki, and Decision 460/QD-BYT by the Vietnamese Ministry of Health. The survey was approved by DHVP Research Consultancy Ethical Board. Since it concerns sensitive information about patients’ behaviors during medical treatment, their financial status, and expenditures other than hospital fees, the investigators had to gradually approach the patients and/or their families to learn about the information of interest.

Bayesian model

In previous studies such as Vuong, 14 the traditional frequentist approach was employed to investigate the effect of residency and insurance coverage on the financial situation of 330 patients. However, this approach faces the problem of multicollinearity that leads to biased estimates because a patient’s residence-based insurance type might encourage patients to choose the registered hospital near their residence for the sake of financial protection. In other words, the purpose of having valid insurance to minimize financial burden might increase the chance that patients choose a nearby hospital. Furthermore, the predictors might be endogenously determined by unobserved variables (e.g. the availability of hospitals near the residence).

Our solution to these issues is to use the Bayesian method with uninformative prior. In addition, the Markov Chain Monte Carlo (MCMC) simulation techniques are employed to assess the health of the model. The simulation uses four Markov chains, each containing 5000 iterations with 2000 chains for warmup. According to Assaf and Tsionas, 43 the Bayesian method based on MCMC can be used to check and mitigate multicollinearity with an unobserved common factor. This method may also mitigate collinearity problems by representing the relationship in a more realistic way. 44 The Gelman shrink factor plots are provided to diagnose the posterior coefficients.

The Bayesian method is also chosen for some additional advantages. The Bayes rule offers a formal approach to incorporate existing knowledge, known as priors, with new data. 45 Compared with the traditional method using p-value, which has various limitations,46,47 the Bayesian analysis allows us to use data to check the model’s robustness. 48

Variable

To answer our research question regarding the relationship of patients’ socioeconomic status, residency, insurance validity, and their satisfaction with health insurance, the following variables are used (see Table 1).

List of variables used for model construction.

Table 2 presented the descriptive statistics of the used variables.

Descriptive statistics of variables used for model construction.

Result

The effect of insurance and residence of patient’s financial burden

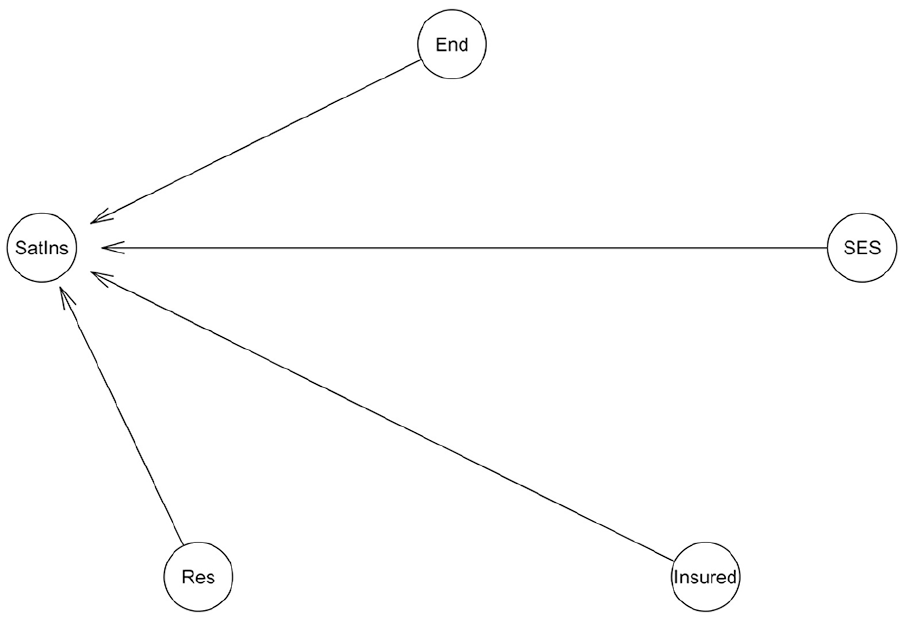

The purpose of Model 1 is to examine the relationship of health insurance and residence with patients’ financial status. This logical network of Model 1 is visualized in Figure 1. The arrow shows the effect of a variable on the likelihood of the occurrence of another variable.

Residency–Insurance model.

To estimate the posterior coefficients of the model, we employed a Bayesian MCMC simulation with 4 Markov chains, 1000 warmup iterations, and 5000 iterations. We also run a diagnosis of the convergence. The trace plots (Figure 2) of the posterior coefficients show that all chains are stationary and well converged. Furthermore, the value of the indicators, effective sample size (n_eff > 1000), and the Gelman shrink factor (Rhat = 1), signals that the model is healthy.

Trace plots of Residency–Insurance model’s posterior coefficients.

The Gelman shrink factor plots are provided in Figure 3. They show that the shrink factor reduces to 1.0 quite quickly during the warmup, which complies with the standards of MCMC simulation. The mean value of the potential scale reduction factor is 97.5%, and we also have the multivariate potential scale reduction.

Gelman shrink factor plots of Residency–Insurance model.

The MCMC algorithm produces samples that are autocorrelated, not independent. The Markov property will be violated if the mixing process is slow due to too high or too low acceptance rate. Autocorrelation functions are performed to check whether autocorrelation is eliminated after certain finite steps. Autocorrelation graphs in Figure 4 show that autocorrelation reduces to 0 during the process. Furthermore, all of ESS (effective sample sizes) exceed 1000.

Autocorrelation graphs of Residency–Insurance model.

The result of Model 1 is summarized in Table 3. Answer to RQ1, both living in the same region with the hospital and having valid insurance are negatively correlated with the financial burden. The gap between b_res and b_insured suggests that living in the same region as the hospital has a stronger negative effect on financial burden than insurance.

Result of the Residency–Insurance model.

SD: standard deviation.

All coefficients have the distribution which satisfies the technical requirements with Highest Posterior Distribution Intervals (HPDIs) at 89% (see Figure 5).

The distribution of coefficients for the Residency–Insurance model (with HDPI at 89%).

Socioeconomic status, insurance, residence, and patient’s satisfaction regarding health insurance

As a multilevel model with varying intercept allows us to distinguish the relationship of patient’s satisfaction regarding health insurance with residency, socioeconomic status, and insurance of the patients given each value of the treatment result, we construct a multilevel Bayesian network, as shown in Figure 6.

SES–Res–Ins model.

The MCMC simulation was performed with four chains, each with 5000 iterations with 2000 chains for warmup. Figure 7 shows the Hamiltonian MCMC technical validations for the model, which shows no divergent chains. This indicates that our model has good convergence.

The Hamiltonian Markov chain Monte Carlo (MCMC) technical validations for the SES–Res–Ins model.

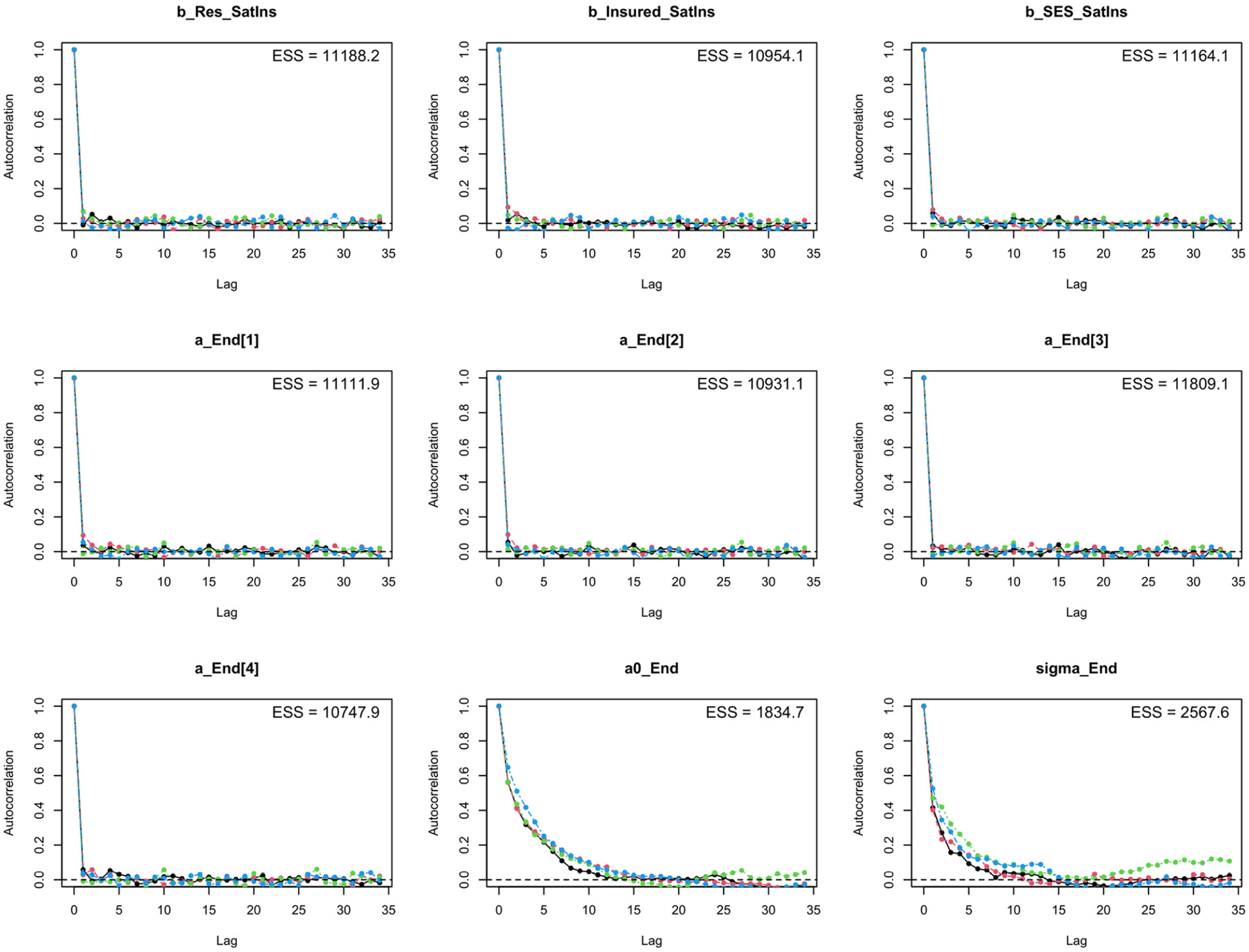

The Gelman shrink factor plots show that the shrink factor reduces quickly to 1, and the mean value of the potential scale reduction factor is 97.5% (Figure 8). Autocorrelation graphs in Figure 9 show that autocorrelation is eliminated after certain finite steps. All of the effective sample sizes are above 1000.

The Gelman shrink factor plots of SES–Res–Ins model.

Autocorrelation graphs of SES–Res–Ins model.

The result of the Bayesian model is shown in Table 4. Since n_eff is above 1000 and Rhat is around 1, the model is reliable. Finding the answers for RQ3, the model suggests that patients with better socioeconomic status are more likely to have a higher level of satisfaction with health insurance. Patient satisfaction with health insurance is also negatively correlated with living in the same region with the hospital (b_Res_SatIns = −0.08) but positively correlated with having valid insurance (b_Insured_SatIns = 1.91). On average, patients who need follow-up treatment (B) and stopped in the middle (C) are more likely to be satisfied with the insurance than patients who quit early (D) and recovered (A), but the difference is small.

Result of the SES–Res–Ins model.

SD: standard deviation.

Figure 10 provides the interval distribution of the posterior coefficients of the SES–Res–Ins model.

Interval distribution of the posterior coefficients of the SES–Res–Ins model.

Discussion

Consistent with Vuong, 14 our result shows that having valid insurance and going to a hospital in the same region is negatively correlated with the financial burden imposed by medical payment. As we further investigate patients’ satisfaction levels across different socioeconomic backgrounds, the result suggests an inequality of benefits from health insurance among patients from high, middle, and low socioeconomic backgrounds. Besides, the level of satisfaction with health insurance is negatively associated with the patients’ socioeconomic status, residence but it is positively correlated with having valid health insurance. In contrast to our expectation, on average, patients who are total cured tend to be the least satisfied with health insurance, while those who quit in the middle of the process or need follow-up have the highest satisfaction level. However, the difference is minimal.

Insurance, financial distress, and patients’ satisfaction with health insurance

The burden alleviation effect of having valid insurance might contribute to the fact that health insurance is compulsory for most Vietnamese citizens and covers most essential treatment. For example, according to Article 21 of the Vietnam Law on Health Insurance in 2008, the insurers paid some of the following care: medical examination and treatment, pregnancy checkup and birth-giving, and transferal cost from district hospitals to higher-level ones. According to Decision No. 36/2005/QD-BYT, health insurance also covered highly technical treatment, including certain types of cancer treatment or transplants. Having valid insurance is positively associated with patient’s satisfaction level regarding health insurance, which is perhaps the result of the negative correlation between having valid health insurance and financial burden for patients.

However, insurance coverage is the highest only when patients stay in the hospital where their insurance is valid. This is emphasized in Law No. 46/2014/QH13 amending the Law on Health Insurance (which came to effect at the beginning of 2015), which states that the coverage of healthcare costs of patients who do not go to the hospital in accordance with their insurance will substantially be reduced. The higher-level the hospital a patient goes to without valid insurance, the higher the reduction of insurance coverage is. If patients bypass the village hospital for the district, provincial or national ones (which are usually further from their residence) without any referral, the additional cost is generated by traveling and the lack of insurance coverage. 6 Furthermore, during the process where patients verify whether their insurance is valid for the treatment, information asymmetry also increases the risk of going to hospitals without valid health insurance; hence, open, transparent, and quality information is needed.49–51

This article also found that different socioeconomic groups might have a different average level of satisfaction with health insurance. According to the finding of Thuong et al., 32 the subsidized insurance schemes (for the disadvantaged groups) did not reduce the amount of OOP payments. This limited financial effect explains why inpatients from low socioeconomic backgrounds are more likely to be dissatisfied with health insurance. However, the reasons behind this result should be further investigated because the level of public insurance benefit varies among the insured groups, favoring the disadvantaged groups. According to Law No. 46/2014/QH13 amending the Law on Health Insurance, people with a pension, relatives of ones contributed to the Revolution (“người có công với Cách Mạng”). Low-income families will be covered for 95% of their health examination and treatment, while it is only 80% for others.

Residence, financial distress, and patients’ satisfaction with health insurance

The findings of this article support those of Nguyen 13 and Fiestas Navarrete et al. 35 While Nguyen 13 found non-residing patients pay more than non-residing ones, we found it is more likely for the non-residing inpatients to fall into poverty than residing inpatients. The inequality in access to healthcare due to the unequal distribution of hospitals in Vietnam is attributable to this result. Central hospitals such as Viet Duc Hospital and Bach Mai Hospital in Vietnam are well-known for their quality of healthcare services and the high concentration of highly technical staff. Since they are usually overcrowded, out of bed for inpatients or inpatients sharing beds in these hospitals are common. However, these hospitals are often located in municipal cities, especially Hanoi. When high-quality hospitals are concentrated in cities where the living standard and income are much higher, non-resident inpatients from other regions might find the more burden to cover payments not covered by insurance, such as cost for companions.

Non-resident inpatients are also more likely to be dissatisfied with health insurance. Apart from financial reasons, inconvenience might lead to a lower level of satisfaction. As Roh et al. 52 mentioned, patients prefer going to hospitals near their houses because revisits will be much more convenient. Furthermore, when there is residence-based insurance in Vietnam, the residence might add more burden to hospitals in other regions. Inpatients with residence-based insurance might have difficulties obtaining valid insurance when transferring hospital because it requires a referral of medical staff from the hospital where the insurance is registered. When the registered hospitals at the commune or district level are capable of giving treatment, the patients will not be allowed to transfer to the hospitals they want unless they are willing to forgo the insurance benefits.

Meanwhile, receiving treatment with valid residence-based insurance in lower-level hospitals might not be a satisfactory experience for patients due to the skeptics about the quality of treatment. Healthcare in lower-level hospitals is not as good as that in higher-level hospitals. However, this point needs further check with a more comprehensive data set that categorized patients based on their insurance type.

Limitations

We fully acknowledge the limitations of this study. 53 According to one of the results, going to hospitals in other regions is positively correlated with financial burden and negatively correlated with health insurance. This might hint about the burden of obtaining valid insurance when transferring hospitals to other regions, which undermines patient satisfaction even though healthcare insurance alleviates financial burden. However, future research needs to examine this point since the data set used in this article does not provide any information regarding transferring hospitals or the troubles of obtaining valid insurance.

Furthermore, countries differ in the capacity and quality of the healthcare system and the design of insurance policies, so the results of this article should be cautiously applied. The data set used in this article is acquired from inpatients in hospitals in Northern Vietnam. When the diversity of cultures in Vietnam across regions might result in different practices and behaviors,54,55 the result might differ when including data of outpatients and hospitals from other regions. Still, our result could be a useful reference for policymakers who wish to reduce the healthcare disparities and access to healthcare. Finally, we fully acknowledge the limitation of this data set due to the nature of convenient sampling and the fact that this data set only covers inpatients in Northern Vietnam. It might not represent the whole situation of other regions in Vietnam when each region could have its practice and attitudes toward healthcare. As such, the result should be carefully used and interpreted with this geographical limitation of the data set.

Conclusion

Using Bayesian statistics with a data set of 1042 observations, we found that the proximity of patients’ residences and their validity of health insurance are negatively correlated with their financial status after treatment. Regarding the satisfaction with the health insurance, while the proximity of patients’ residences is negatively correlated with the satisfaction, the validity of the health insurance shows a positive association with patients’ satisfaction. A better socioeconomic status was also found to be associated with higher satisfaction. In the time of increasing commitment to universal health coverage on a global scale, this study provides further insights into how insurance in Vietnam reduces the risk of poverty. However, the unequal geographical distribution of quality of healthcare and hospitals is a still notable hindrance for patients, especially non-resident ones, to have quality healthcare without carrying more financial burden. This article also provides a hint about the impoverishment risk of patients who have residence-based insurance and seek healthcare elsewhere since they might meet difficulties to validate their insurance and pay for the cost of going to hospitals outside the region of residence.

Footnotes

Acknowledgements

The authors thank friends and colleagues who have provided assistance and support for this research: Nghiem Phu Kien Cuong (Viet Duc Hospital, Hanoi), Dam Thu Ha, Vuong Ha My, Vuong Thu Trang (Vuong & Associates), Ho Manh Tung, Nguyen To Hong Kong, and Le Tam Tri (Centre for Interdisciplinary Social Research, Phenikaa University). The authors are also indebted to hundreds of patients and their family members for their willingness to answer deep and often time-consuming interview questions; without their information, this study would not be possible.

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Ethical approval

This survey met the ethical standards of the International Committee of Medical Journal Editors (ICMJE) Recommendations, the World Medical Association (WMA) Declaration of Helsinki, and Decision 460/QD-BYT by the Vietnamese Ministry of Health. The survey was approved by the DHVP Research Consultancy Ethical Board.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Informed consent

Written informed consent was obtained from all subjects before the study.

Data availability

The data set is deposited in a data article: https://doi.org/10.3390/data4020057, and OSF: ![]() and DOI: 10.3390/data4020057.

and DOI: 10.3390/data4020057.