Abstract

Objectives:

This article aimed to discuss the emergence of medical device sector in China from a sectoral innovation system perspective, to explore the drivers and barriers to the successful building of an innovation system of medical devices, and to highlight the policy implications and suggestions for sustainable innovation of medical devices.

Methods:

A theoretical framework of sectoral systems of innovation was applied in the analysis of data, and materials were collected from multiple sources with particular attention paid to the evolutionary phases, structure, and function of the innovation system.

Results:

The evolution of medical device sector in China could be divided into four phases: initialization (1960s–1970s); exploration (1980s); steady growth (1990s); and rapid growth (since 2000). Through analyzing the innovation system’s structural components of technology, actors, and networking, as well as institutions, this study indicated that the government policy decision was the most important driver that affected the virtuous cycle of the Chinese medical device innovation system, followed by market demand and entrepreneurial activities. However, barriers against the innovation cycle such as knowledge base development and diffusion, legitimacy, and resource mobilization still remained.

Conclusion:

In its endeavor to build an innovation system, the Chinese medical device sector had made some progress in meeting the local medical demands and improving its industrial competence. Although a Chinese innovation system for medical devices was initiated under the guidance of the government, knowledge advancement and diffusion had become the main challenges for the sustainability of innovation in this sector. The future development depends on China’s effort and ability to establish education and health research systems specific to medical devices.

Introduction

The development of medical device sector in China has attracted much attention from around the world due to the nation’s huge market and rising research and development (R&D) capabilities.1,2 The sales of medical devices in China totaled no more than CNY 14.5 billion in 2000, but increased to CNY 308 billion in 2015. Since 2013, China has been ranked as the second-largest medical device market in the world after the United States.3,4 The global consumption proportion of medicine to medical devices was 1:0.7 in 2014, while for developed countries, it had reached 1:1.02. However, it was only 1:0.19 for that of China, which indicates its vast market potential for medical devices. 4

With the demands for medical devices growing among patients in recent years, this industrial sector is becoming increasingly important to the Chinese government. 5 Three domestic clusters of this sector have rapidly emerged, namely, (1) the Beijing-Tianjin Bohai Rim region (R&D cluster); (2) the Yangtze River Delta region (manufacturing cluster); and (3) the Pearl River Delta region (manufacturing cluster of electronic components). These industry clusters have been boosting competitive conditions for developing medical devices, such as basic science research, innovative industrial design, good manufacturing capability, convenient transportation, concentration of universities and high-level hospitals, and a mature financing system. 6

Medical device, by definition, is any instrument, apparatus, implement, machine, appliance, implant, in vitro reagent or calibrator, software, material, or other similar or related article. Physicians use them for diagnosis, prevention, monitoring, treatment or alleviation of disease, or compensation for an injury, also for investigation, replacement, modification, and support of the anatomy or of a physiological process as well as life-supporting or sustaining, control of conception, disinfection of medical device, and provision of information for medical purposes through in vitro examination of specimens derived from the human body. 7 Medical device sector is widely recognized as a high-technology industry because of its multidisciplinary, knowledge demanding, and capital-intensive features, which reflects a country’s technology and manufacturing readiness level.3,8 While the Chinese medical device sector has made rapid progress, how to acquire significant technological and market breakthroughs are still the major challenges ahead.

At present, the acquisition of some high-end medical devices for China’s hospitals still depends on imports. Domestic exports are mainly medical consumables that do not hold core technologies. On one hand, some leading local enterprises, standing out from niche markets, have made advancement in R&D, manufacturing, and marketing; on the other hand, most Chinese small- and middle-sized enterprises (SMEs) are still concentrating on producing generic products of medical devices. 9 Facing the surging demand from the domestic patients, the Chinese medical device sector calls for a more specific inquiry and well-established management. However, current literature lacks a systematic exploration on the situation of medical device sector in China.

Against this backdrop, this study aimed to discuss the emergence of medical device sector in China from a sectoral innovation system perspective, to explore the drivers and barriers to the successful building of an innovation system of medical devices, and to highlight the policy implications and suggestions for sustainable innovation of medical devices. The findings are expected to not only contribute to medical device innovation in China but also provide reference to innovators of medical devices in other countries.

Theoretical framework

In this study, the framework of sectoral innovation system is adopted to account for the medical device sector innovation in China. Conceptually defined, a sectoral innovation system is “a set of specific uses products and series of agents that carry out lots of market and non-market interactions for specific product in creation, production and sale.” 10 Compared with other innovation system frameworks such as those operated on national, regional, or technological domains, the framework of sectoral innovation system is more applicable for this study because sectoral innovation system functions better in identifying sector boundaries and structure; exploring participating agents and their interactions within learning, innovation and application contexts; and observing the influence of supply and demand, even the impact of institution and policy involved on the sector innovation. Also, combined with evolutionary theory and a dynamic view of sectors, the framework of sectoral innovation system can be useful in analyzing the specific impact factors in the innovation performance and the dynamic evolution of an industry.10–12

The application of sectoral innovation system framework usually comprises two parts. The first part is a structural analysis of a sectoral innovation system, which aims at clarifying the three building blocks of a sectoral innovation system, including knowledge and technologies, actors and networks, and institutions (see Table 1). All these three building blocks are indispensable and need to be clearly understood as essential components. 12

Definitions of three building blocks of a sectoral innovation system.

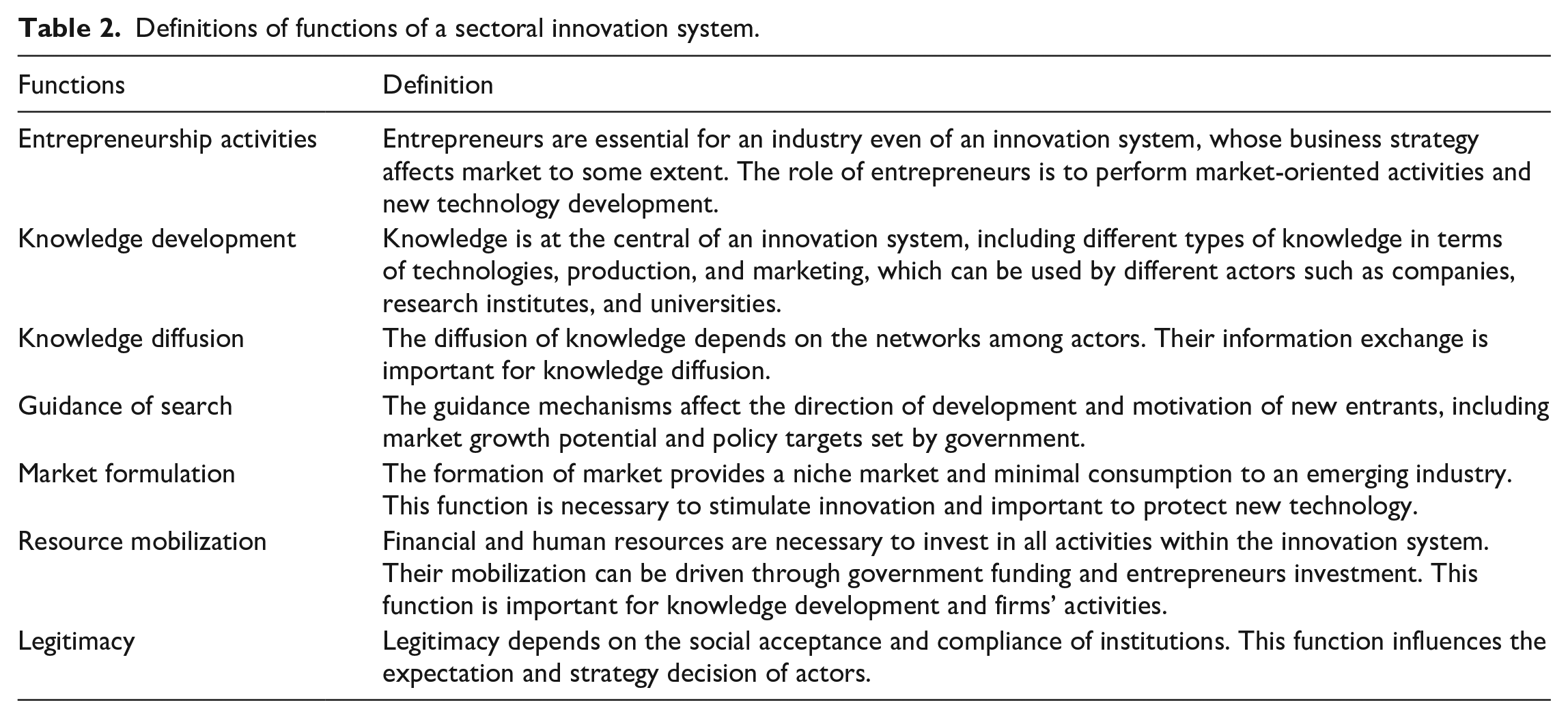

The second part is a functional analysis of a sectoral innovation system, which is based on the structural analysis made in the first part to measure dynamic performance in the sector. A functional analysis model is composed of seven functions: entrepreneurship activities, knowledge development, knowledge diffusion, guidance of search, market formulation, resource mobilization, and legitimacy (see Table 2).13–15 Through assessing the operational performance and external economic effects produced among these seven functions, a sector innovation system can be estimated in terms of virtuous circle or vicious circle, which provides a basis for exploring the drivers and barriers of a sectoral innovation system and making policy suggestions about how to improve sectoral innovation system.

Definitions of functions of a sectoral innovation system.

Recent years saw the framework of sectoral innovation system being widely applied to studies of different fields, such as the automotive sector in Thailand, 16 the animal monitoring technologies in Germany, 17 and solar innovation system in United Arab Emirates. 18 Furthermore, it has also been applied in the field of medicine such as the sector of tradition Chinese medical health food in China, 19 pharmaceutical industry in Taiwan, 20 biopharmaceutical sector in China, 21 and the antidepressants in traditional Chinese medicine. 22 As medical device sector is multidisciplinary and diversified in essence and largely contingent on changes of technology as well as policy, the framework of sectoral innovation system that emphasizes the dynamic development of an industry is deemed to be appropriate for studying the sectoral innovation.

Methods

Research design

This study applied a qualitative case study by identifying the medical device sector in China as a whole case.23,24

Data collection

Data and materials were collected from multiple sources. First, official data and policy documents were collected from the China Food and Drug Administration (CFDA) and the General Administration of Customs. Second, data about global and Chinese patent application of medical devices were extracted from Wanfang Database through International Patent Classification to each category (IPC A61B, A61C, A61F, A61G, A61H, A61J, A61M, and A61N) during 1999–2015. Third, academic publications on medical devices in China were searched and downloaded from China National Knowledge Infrastructure (CNKI) database, Web of Science, and ScienceDirect. For the fourth batch of data, materials about the leading firms and their networking partners were obtained through searching official websites of firms and relevant industrial newspapers and reports.

Furthermore, the fifth data were mainly elicited from five key informant interviews conducted separately with two government officials and three industrial practitioners. All the five interviewees were purposively selected and approached through personal introduction before the formal interviews. The two government officials were policymakers who directly participated in designing innovation policies for medical device sector in China. The three industrial practitioners had worked in the medical device sector for more than 10 years. In consideration of their experiences and expertise, they were able to provide detailed and insightful information about medical device innovation in China. The qualitative interviews were implemented in a face-to-face way at the workplace by following an interview guide (see Supplemental File 1). The fourth and fifth authors, as experienced university researchers, conducted the interviewees. All the interviews lasted about 1 h and were taped, which were transformed into the transcript of Word after the interviewees.

Regarding data saturation, the researchers took efforts in two ways. First, with qualitative information input from both government and industry, qualitative data saturation was reached. Second, through collecting qualitative and quantitative data and materials from different sources as described above, it was intended to ensure that all the data and materials would conform and complement each other to reflect the exact structure and functions of the medical device innovation system in China.

Statistical analyses

For the data about patent applications and academic publications, descriptive statistical analysis was conducted to generate their trends by using software of SPSS for Windows.

Data analysis

All the data collected were correlated and analyzed by applying the framework of sectoral innovation system. First, an evolutionary history of the Chinese medical device sector was designated into four stages according to the innovative characteristics of main medical device products. Second, structural analysis of innovation system was carried out by categorizing all the qualitative and quantitative data into the three building blocks of innovation system as knowledge and technologies, actors and networks, and institutions. Third, functional analysis of innovation system was conducted based on the results of structural analysis to demonstrate the interactional relationships of seven functions. All the data analysis was conducted by the fourth and fifth author.

With the results from the three types of data analysis above, the inducement mechanisms (drivers) and blocking mechanisms (barriers) of the medical device innovation system in China were explored through discussion, which led to specific policy-making suggestions for sustainable development of the sector.

Results

Development phases of medical devices in China

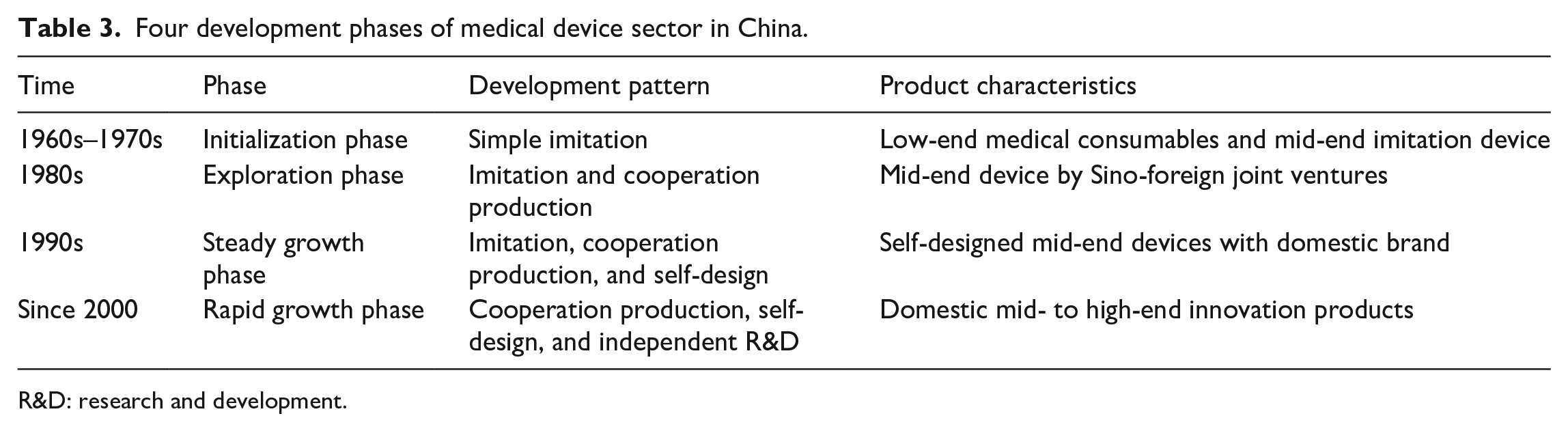

Based on the development pattern and product characteristics, the evolution of the medical device sector in China since 1960s can be divided into four phases (see Table 3).

Four development phases of medical device sector in China.

R&D: research and development.

1960s: initialization phase

Upon the establishment of the People’s Republic of China in 1949, the whole nation was found in possession of no industrial capabilities to supply itself with medical devices to meet the urgent demands from a huge population of patients. Since the early 1960s, simple imitation production had been adopted by the Chinese medical device firms that were funded and run by the government. Most of the local firms produced low-tech medical consumables, while some leading firms started up with imitating mid-end imported devices like diagnostic X-ray and electrocardiogram machines. This kind of development pattern allowed local firms to invest less capital and techniques. Therefore, it could satisfy the urgent market demand to a certain extent and organize technical teams in a short period, which was crucial for the Chinese medical device sector that cried out for capital and technology at the time.

1980s: exploration phase

Since China’s reform and opening up in the 1980s and entry into the World Intellectual Property Organization (WIPO), the development pattern of medical device sector had gradually changed from simple imitation to cooperation production. A lot of subsidiaries of multinational companies (MNCs) were set up in China due to the increasing domestic market demand. Local firms tried to establish joint ventures with foreign investors to conduct cooperation production as a shortcut to obtain the advanced technology. Through cooperation production, a large number of mid-end device products were released to the market. However, the purpose of developing innovation products was not fulfilled because MNCs still monopolized the key technologies of imported devices. Most joint ventures were virtually low-cost assembly factories.

1990s: steady growth phase

In this phase, the Chinese medical device sector underwent some rapid changes due to the government’s stress on intellectual property rights. Besides cooperation production, local firms started to implement self-design strategy, which was to exploit existing technologies to improve a medical device’s function and outward appearance, though without being able to change its core components. Furthermore, domestic brands were gradually cultivated to support the market with mid-end products through self-design. Nevertheless, only a small number of large-scale firms could afford to develop self-designed products as it required more investment and risk-taking than what was for imitation products. Above all, local firms still had huge hurdles to overcome before the core technologies of high-tech medical devices were acquired.

Since 2000: rapid growth phase

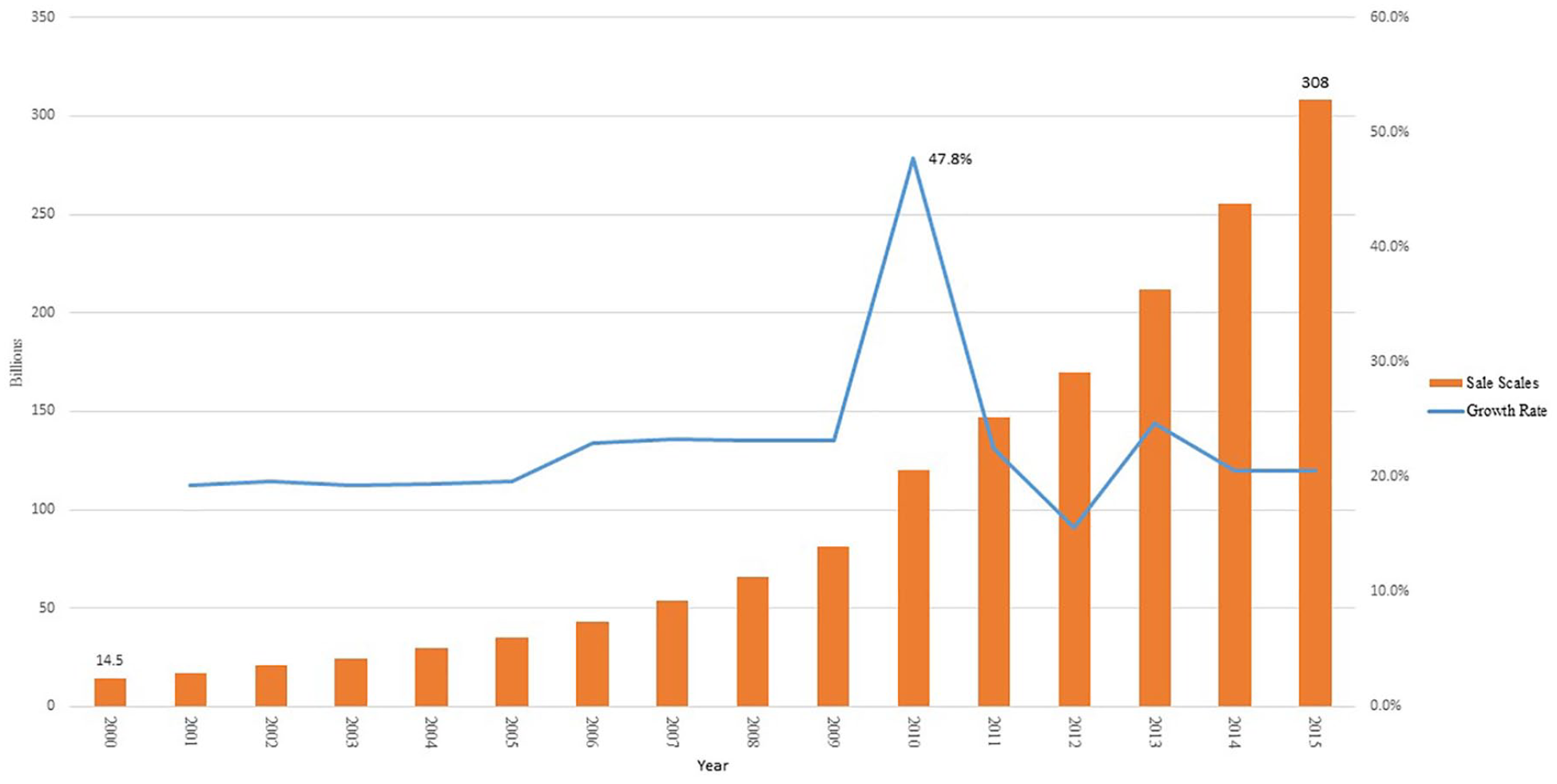

Since entering the 21st century, the sales of medical devices have revved up at an annual growth rate of 40% (see Figure 1). Especially with the introduction of China’s new medical reform planning in 2009, the capital investment in health care system increased sharply, which significantly stimulated the consumption of medical devices. Owing to the favorable policies from the government, independent innovation of medical devices has been actively endorsed. A number of universities began to establish education programs specific to medical devices. Some of them founded scientific research centers with affiliated firms specializing in varieties of medical devices to reinforce the connection between manufacturing and research institutions and accelerate technology transfer. At the same time, brands were promoted for domestic mid- to high-end medical devices, such as patient monitoring device, medical imaging device, laboratory equipment, and interventional products. Moreover, local firms began to invest in homecare devices and wearable medical devices to compete with MNCs.

The sale scales of medical device in China (2000–2015).

Structural analysis of medical device innovation system in China

Evolution of technology for medical devices in China

Considering patent being a significant indictor reflecting technology development both in China and across the globe, patent applications for medical devices were analyzed to trace the technological evolution of medical devices in China.

With regard to global patent applications related to medical devices, there were a total of 1,678,339 applications between 1999 and 2014, increasing at an annual growth rate of 3.77% (see Figure 2). The quantity proportion of patent applications in the United States, Japan, and China changed dramatically in this period. The number of patent applications from China markedly increased since 2009 and resulted in a sharp leap from 6.7% in 1999 to 55.3% in 2014.

The global patent applications of medical device (1999–2014).

As for Chinese patent applications related to medical devices, the number of applications also increased dramatically during this period from 1999 to 2015, which climbed 10 times higher (see Figure 3). However, the proportion of inventions to be patented in the total of the applications was about 30%, most of which were of utility models. On the other hand, the proportion of the applications with a foreign business address significantly decreased since 2006, suggesting the major factor of domestic applicants in the overall growth of the period.

Chinese patent application in medical device (1999–2015).

Within all the global patent applications, most of the items were under the category A61B (diagnosis, surgery, and identification), which accounted for up to 36% of the total, followed by A61F (implantable medical device) and A61M (interventional medical device). It served as an evidence that A61B, A61F, and A61M were the three major areas of medical device R&D across the world (see Figure 4).

The global patent application in IPC classification.

In the Chinese case, these three categories of patent applications were also indicative of the most active R&D fields (see Figure 5), meaning that China was moving in the same direction therein with the global R&D.

China patent application in IPC classification.

Actors of medical devices in China

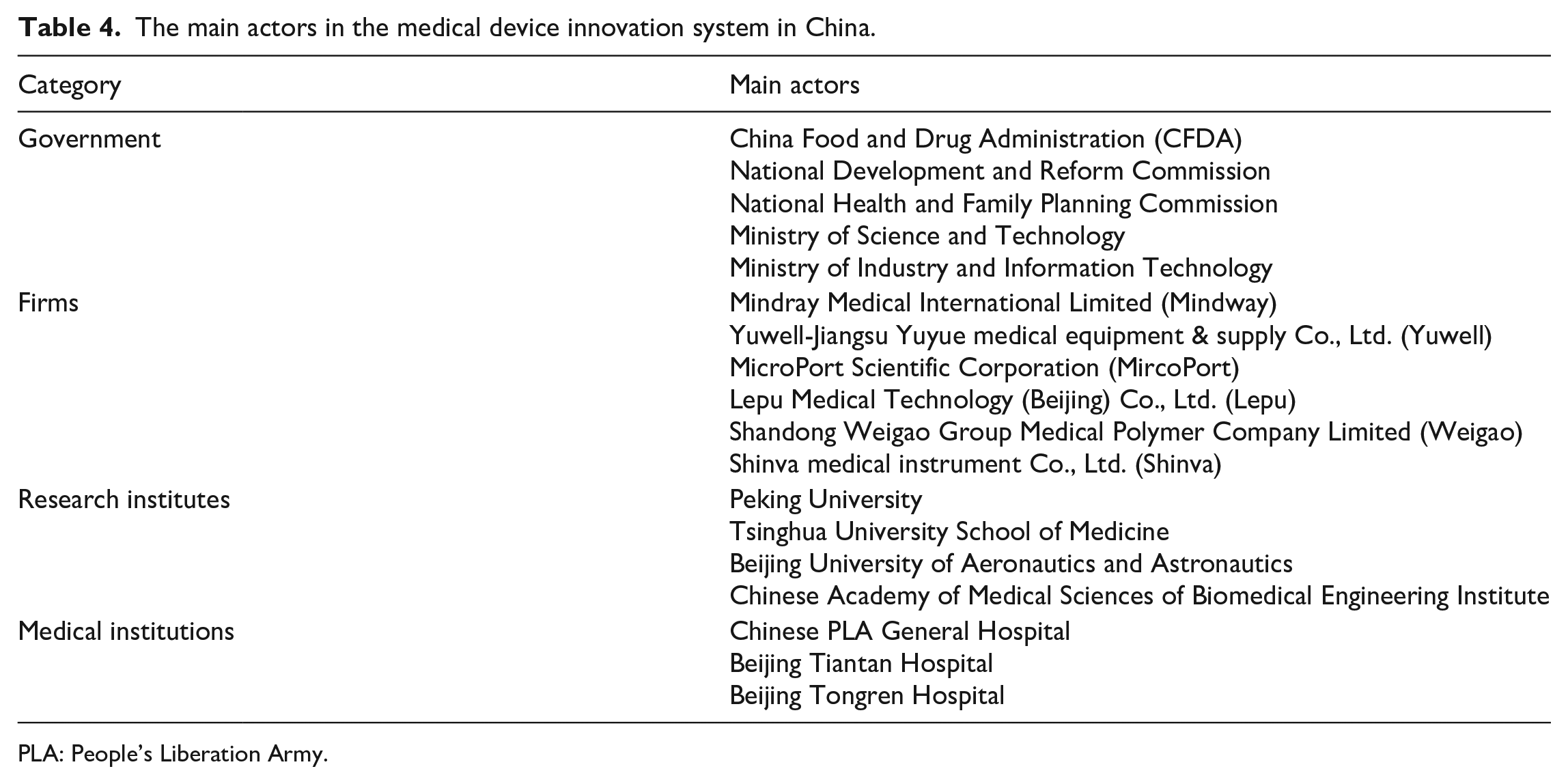

As summarized in Table 4, the main actors in the Chinese medical device innovation system included the government, firms, research institutes, and medical institutions.

The main actors in the medical device innovation system in China.

PLA: People’s Liberation Army.

Among all the actors, firms had played a leading role in shaping the innovation system of medical devices in China. The National Medical Products Administration (NMPA, previously known as the China Food and Drug Administration) focused mainly on regulating the registration of medical devices but paid less attention to product innovation. Research institutes had just begun to conduct exploratory research and experiment on commercializing their scientific findings. Despite being the major users of medical devices, medical institutions were so unduly overloaded with their daily routine that they were not up to leading the medical device innovation. Consequently, medical device firms had become the core actors in establishing the medical device innovation system in China.

The medical device sector in China was mainly composed of SMEs. These SMEs, being mostly private businesses, mainly focused on producing generic products and competing for price and marketing in geographically small areas because they usually did not have capability to distribute their own products to other regions and compete with the local producers that produced similar products. Generally, they were also not able to organize innovation activities. However, as summarized in Table 4, some leading firms had taken creative actions to climb upon the value chain. Their activities were gradually changing the industrial structure leading to a new innovation system of medical devices in China.

We have summed up the product area, target market, R&D strategy, and marketing strategy of the six leading medical device firms into Table 5. A shown by the results, these leading firms were similar in terms of the R&D and marketing strategies adopted although they focused on different product areas, which was explained in more detail below.

A summary of leading medical device firms in China.

R&D: research and development; M&A: merge and acquisition.

With regard to their R&D strategies, these firms set up independent R&D departments and entered into the target market of new products through strategic merge and acquisition (M&A). The leading firms all emphasized self-innovation. For example, Lepu and MicroPort that succeeded in substituting the import in the implant device market, and Mindway that competed with MNCs in mid- to high-end device all put about 10% annual turnover in R&D. In particular, innovation on product iteration was important for medical device companies to keep the competitiveness of their products. Considering the relatively low profit of medical device in China, such kind of R&D investment was a significant investment for medical device companies in China. Furthermore, innovative techniques were transferred by these firms to enrich their product lines to expand sales. Besides, these firms widely used M&A as the most critical strategy to make a quick push into a new market. For example, in 2011, Mindway acquired Datascope to become one of the three major brands of life information monitoring in the world. MicroPort acquired Wright Medical OrthoRecon in 2013 to enter the orthopedic market. To introduce the cardiology specialist products to China, Lepu carried out a series of M&A activities, such as the acquisition of Winmedic and Star to enter the market for cardiac treatment devices, and the acquisition of Shaanxi Qinming for cardiac pacemaker market. Through their successful M&A, these firms showed rapid growth and built new product lines with less R&D resource investment. Moreover, the Chinese firms began to internationalize their business and brand names through the acquisitions of foreign companies.

As their marketing strategies, the leading firms all emphasized the importance of cultivating their own branding and establishing productive marketing channels. Due to the fact that the sales channels in China were fragmented and difficult to maintain, strong management of branding and marketing was deemed essential to enable a local firm to stand out and compete with MNCs. For example, Yuwell reinforced its competence as a leader in the homecare device market by its successful marketing strategy. Its brand building laid a good foundation for sales. It was the first company that received the “Chinese Famous Brand” award in the industry because of its brand products such as Yuwell sphygmomanometer and Yuwell wheelchair. The brand name Yuwell won an award for “Chinese Famous Trademark” in 2007 as well. To open up and keep a strong hold on marketing channels, Yuwell offered a wide variety of products for a factory outlet price to its agencies, which ensured that they significantly boosted sales and increased profits. Besides establishing marketing channels on their own, these leading firms also used M&A strategy to expand their marketing network quickly. For example, Shinva acquired Vastec Medical Ltd. in 2013 to take over its marketing network in more than 20 cities in China, moving the Shinva products into the target markets apace.

In summary, the leading firms tended to select and concentrate on certain product areas. To develop their product lines and improve the technical product contents, not only did they invest in R&D by themselves but also apply M&A to obtain innovation capability as quick measures. Moreover, they gained higher profits from the channels bonding the powerful domestic sales markets and networks together. In the process, their brand was uplifted as a result of combining technological innovation and marketing channel management.

Networks among actors

Before 2000, the network of actors of the medical innovation system hardly took form in China. At the start of the new century, with the domestic demands rising and China’s health system reform deepening, the government began to initiate cooperations among firms, universities, research institutes, and medical institutions to improve the innovation capacity of domestic medical devices. It was anticipated that the Chinese medical device firms, by making use of the technological strengths of research institutes, could shorten the R&D process and accelerate the industrialization of innovative medical device products. Furthermore, it was also expected that the cooperation between firms and medical institutions would benefit the clinical trials in hospitals to ensure the academic promotion and clinical applications.

In 2009, the Ministry of Science and Technology of China organized the institutions in the medical device domain into the China Strategic Alliance of Medical Device Innovation, a sectoral alliance at the national level. Driven by this front, different types of networks were established. For regional networks, provincial and city-level alliances emerged, such as the Chengdu Strategic Alliance of Medical Device Innovation and the Guangdong Strategic Alliance of Medical Device Innovation. For specialized medical areas, there was, for instance, the Eye and Optical Strategic Alliance of Medical Device Innovation, formed by Eye Optical Research Institute of Wenzhou Medical University, Peking University, 66 Vision Tech Co., Ltd, Beijing Tongren Hospital, and Zhejiang Institute of Medical Device Testing. The Minimally Invasive Interventional and Implanted Strategic Alliance of Medical Devices Innovation was established as a result of the cooperation of various medical institutions, including MicroPort Scientific Corporation, Ruijin Hospital of Shanghai JiaoTong University, School of Medicine of University of Shanghai of Science and Technology, and Changhai Hospital of Second Military Medical University. For cooperative laboratories and research centers, hosted by Tsinghua University, the National Engineering Laboratory for Neuromodulation was cofounded by Beijing Pins Medical Co., Ltd. and Beijing Tiantan Hospital. Furthermore, the Ministry of Science and Technology approved and supported the plans for Mindray to build the National Engineering Research Center for Diagnostic Instruments and that for Lepu to build the National Engineering Research Center for Heart Disease Explants Intervention of Medical Instruments and Equipment.

However, the overall progress of networking among firms, universities, research institutes, and medical institutions remained in the initial phase as yet. Many problems, such as a lack of correct product positioning for cooperation projects, R&D without considering the clinical application, and inadequate intellectual property protection among cooperators, still hindered the networking effect of the Chinese medical innovation system.

Institutions for medical devices in China

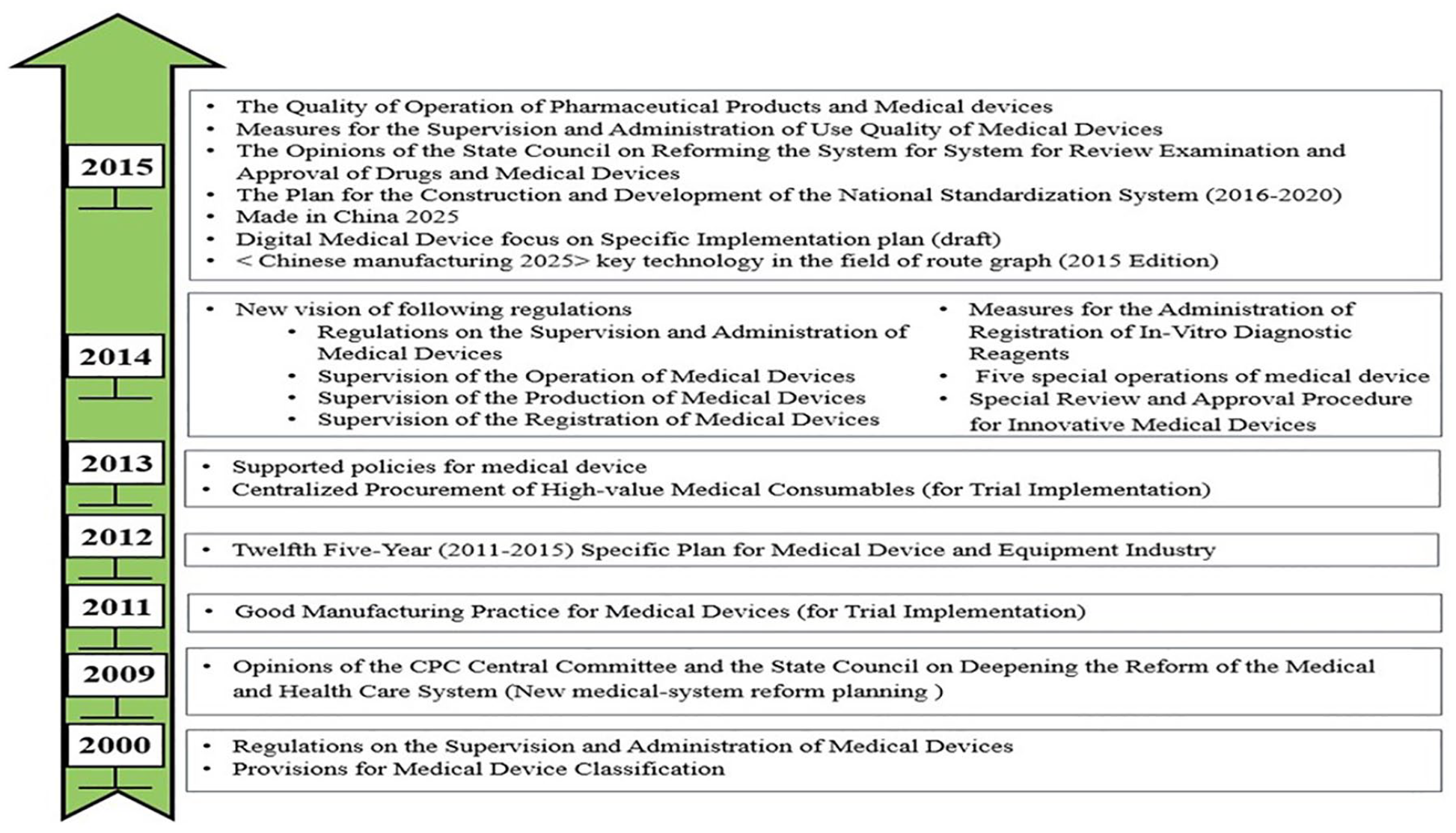

Since China’s reform and opening up in 1978, the main policies of the government concerning medical devices had evolved from supervising the safety of medical devices to supporting the sectoral industrial innovation. In the 1980s, because of the rapid development of medical device market, a large number of high-risk products from domestic and foreign firms were sold without supervision. Therefore, the central government authorized the CFDA in 1994 as a special management department to monitor and regulate the sales of medical devices made either in China or by foreign manufacturers. The primary efforts of the CFDA in the 1990s were to set up the basic supervision infrastructure to control the risk of medical devices in the market.

Since the turn of the century, the policy started to lean toward more normative supervision. The Regulations on the Supervision and Administration of Medical Devices (RSAMD) was issued by the State Council in 2000, signaling that China had ushered in the legalization of supervision and administration for medical devices. Following the launch of the new health system reform planning in 2009, a revised version of RSAMD was released in 2014, which imposed systematic, stricter risk supervision on medical devices, for example, enforcing a new risk classification for managing medical devices and making compulsory registration for all items in Class I category. All the documents for product registration to be submitted and the designated registration departments were clearly listed in the new version of RSAMD. Moreover, the registration procedure was amended to such that the manufacturing license of a product being registered could be provided after the registration to reduce any extra cost incurred. On the other hand, the new RSAMD of the regulations strengthened the quality management system of manufacturing enterprises, added a registration system of medical device re-evaluation, detailed on the recall system for monitoring and reporting the adverse events of medical device usage, and adjusted the range and variety of punishment. As well, a system for incoming inspection and records was set up to strengthen the monitoring of sales. Also added to the new RSAMD was the setup of mechanisms for examining innovation medical devices and giving emergency approval.

Besides, the new health system reform planning and the 12th Five-Year Plan provided immediate support for upgrading the Chinese medical device sector. Moreover, priority registration was given to innovative medical device that owned core technology invention patent and significant clinical efficacy with the issue of the two official documents, namely, the Special Review and Approval Procedure for Innovative Medical Devices in 2014 and the Reform on the Drug and Device Approval System in 2015. Furthermore, the 13th Five-Year Plan listed high-performance medical devices as a key development field that would receive continuous support of national policies. The evolution of policies pertaining to medical devices in China is indicated by Figure 6.

Evolution of medical device policies in China (2000–2015).

Functional analysis of medical device industry in China

Base on the results of the structural analysis of the Chinese innovation system of medical devices, the functional performance of the system is summarized as shown in Table 6.

Drivers and barriers affecting the functions of the medical device innovation system in China.

R&D: research and development; M&A: merge and acquisition; RSAMD: Regulations on the Supervision and Administration of Medical Devices; SMEs: small- and middle-sized enterprises; MNCs: multinational companies.

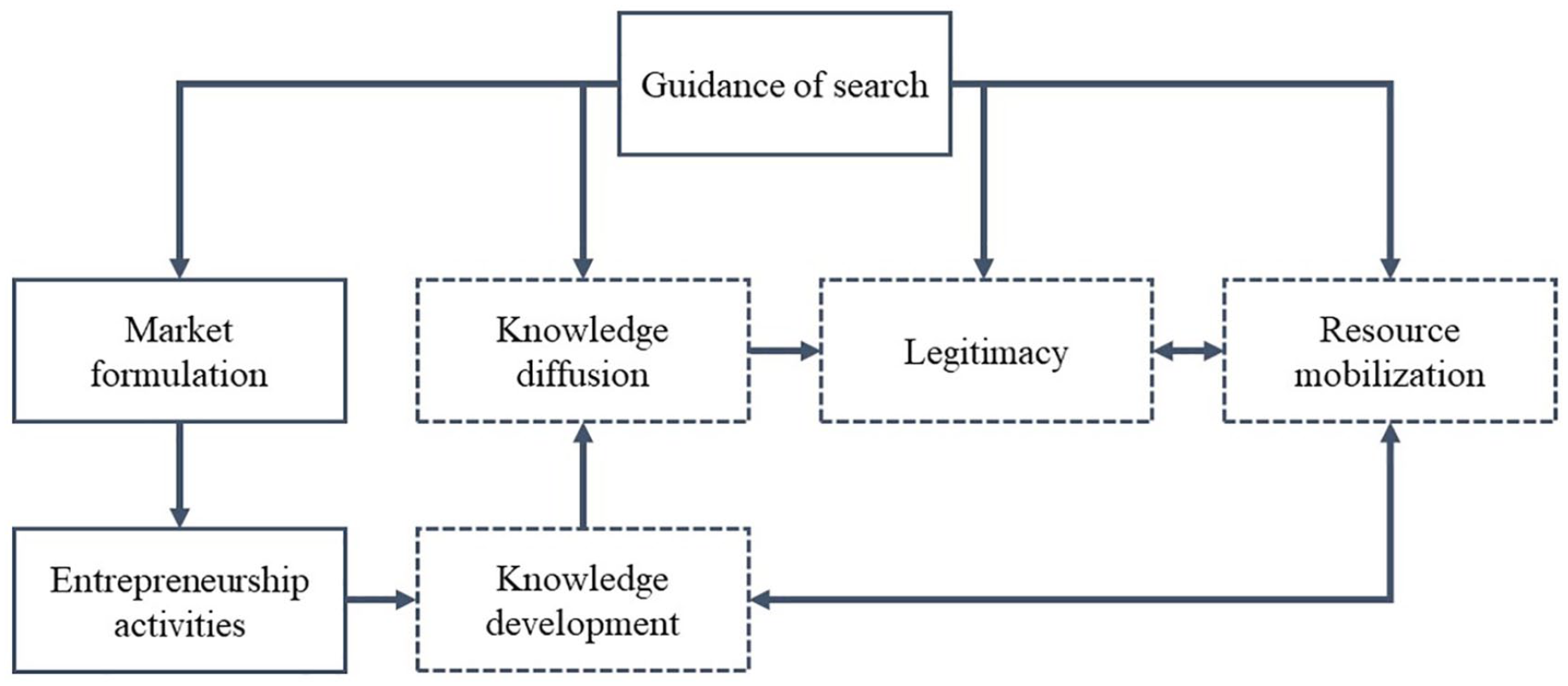

In practice, various functions of innovation systems interacted with each other in the course of the evolution, which led the industry to a virtuous cycle (see Figure 7). The virtuous cycle of the innovation system functions started with guidance of search. The explicit search direction of medical device industry was laid down by the Chinese government. Then, other major factors, such as market formulation, knowledge diffusion, legitimacy, and resource mobilization, were motivated by the policy guidance of the government. After the Chinese medical device market was set up, entrepreneurial activities were undertaken by entrepreneurs in various fields of medical devices. Then, the medical device technologies were developed and diffused through the networks and cooperation. The rapid diffusion and development of knowledge enhanced the legitimacy of medical devices, including the acceptance level of the customer and the attention of policymakers, which in turn stimulated the mobilization of resources, including finance and human resources. The knowledge development was improved with resource mobilization at the same time to form a virtuous cycle of the innovation system of medical devices in China.

The virtuous cycle within an innovation system of medical device in China.

Discussion

According to the structural and functional analysis above, in this section, we will discuss the drivers and barriers of the Chinese medical device innovation system and highlight the policy implications and strategic suggestions for sustainable innovation of the sector.

Drivers and barriers

The evolution of the Chinese medical device sector in the past decades has established the foundation for development without losing its orientation. The main priority has been given to guidance of search and market formulation for pursuing the sector development, which pushed forward the entrepreneurship activities. In recent years, there has been an enormous demand for medical devices in China due to a number of contributing factors, including growing public concern over the aging population, general awareness of the importance of healthy living and innovative medical options, as well as the launching of the new health system reform planning, which was to enhance and upgrade the national medical infrastructure.1–3,25,26 Moreover, the government has attached great importance to the development of the sector through a series of policies in support of the firm’s innovation and the local innovative products. Our research findings also indicate that firms are the more active player than the government. Some of the leading firms being active in the R&D and marketing network establishment are gradually upgrading the international competitiveness of domestic devices.27,28 Thus, the function performance modules of guidance of search, market formulation, and entrepreneurship activities have turned out to operate better than the others. 29

While a positive mechanism of circulation has been developed for the innovation system, the Chinese medical device sector still faces the challenges of competing with MNCs in the high-end lines. The functional analysis of the medical device innovation system explored the existence of the barriers that blocked the smooth run of the innovation circle. Relatively speaking, the medical device sector in China is still found immature to some extent in terms of weak knowledge development, slack network cooperation (knowledge diffusion), inefficient mobilization of resources (resource mobilization), and the low acceptance level for high-end domestic products (legitimacy). 29 Actually, a sound knowledge base is always the core of high-tech industry and also the most challenging goal to accomplish. China lagged behind the world’s developed countries in starting up the medical device sector by about half a century, which caused a significant gap between its knowledge base and the MNCs’, such as that of General Electric Company and of Philips. 30 Moreover, loose network cooperation between actors resulted in insufficient technology transfer and commercialization. It was also difficult to carry out clinical trials because of the weak networking between medical device firms and medical institutions. 31 In addition, due to the limited financial resources, the local innovative SMEs were often acquired by MNCs, and local talents were attracted to MNCs as well.5,32,33 At the same time, medical devices of well-known MNC’s brands were still the first choice for local customers, especially in the case of hospital preference. The local actors were yet to put in more effort and resources to improve the R&D and marketing capacity for the sustainable development of medical devices and boost consumer’s confidence in domestic brands.

Managerial and policy-making suggestions

Based on the discussion above, some policy implications and strategic suggestions for sustainable innovation of medical devices can be drawn as follows. First, it is deemed essential to improve knowledge development and diffusion, as well as the implementation of science and technology funding programs, to enhance knowledge accumulation and realize the integration of academics and industry and accelerate the industrialization of R&D achievements. 34 Second, for the legitimacy of domestically made medical devices, the government must encourage public hospitals to purchase those devices based on cost-effectiveness evaluation. It is also needed to execute the quality control standards of medical devices strictly to speed up the improving of the image for the home-made brands to enhance credibility and thus consumers’ confidence. 35 Third, for resource mobilization, increasing financial support such as tax incentives by the government should motivate firms to strengthen the R&D activities and the product innovation. To improve the shortage of human resources for medical device innovation, the government may consider the setup of a special category scholarship to encourage innovation and create opportunities for multidisciplinary exchanges of ideas in this field. On the other hand, enlistment of student candidates to join in a reserve pool of researchers for this sector and providing them with internship opportunities in domestic enterprises has been proved to be one of the effective measures to fill the talent gap.36–38

Fourth, regulatory policy for breakthrough products of medical device is also warranted. Some regulatory agencies, such as the Food and Drug Administration in the United States, have established particular regulatory pathways for breakthrough products to facilitate market access of medical devices. Such kind of institutional design is suggested to be founded in China to promote the innovation of medical devices. Fifth, joint efforts to enhance transparency in knowledge base of medical device should be encouraged. Better availability of pre-clinical, clinical, and after-marketing results in published literature would be helpful to develop consistent standards for medical device, which can benefit knowledge development and diffusion of medical device in the long run. Sixth, the idea of total product lifecycle should be integrated with innovation systems to manage the innovation of medical device. As medical device mostly follows a way of evolutionary innovation, the lifecycle of medical device needs to be systematically considered by industrial practitioners when planning innovation projects for medical device products.

Research limitation and future research

There are a number of limitations in this study. First, in our research, we had difficulty in collecting fully comprehensive data, especially those concerning knowledge base information due to the multidisciplinary nature of the medical device sector. Future studies can focus on a specific aspect of knowledge base, like academic publication, patent, and clinical trials, to generate more profound findings of the knowledge base evolution of medical service. Second, this article has offered only an overview of the medical device industry in China from sectoral innovation system perspective and identified the drivers and barriers in the system through functional analysis. Future studies are warranted to examine the innovation systems of subsegments of medical device sector to provide better insights into different subsegments of medical device innovation and to better inform innovators specialized in designated areas of the medical device sector. Third, this article mainly focused on local medical device companies. Future studies can explore the deeper interactions between local medical device companies and international companies for R&D of medical device products. In particular, the design of the government policies that encourage and support international cooperation should be further explored. Fourth, medical device technologies such as self-powered medical information sensors have emerged and commercialized for market in recent years.39–41 Future studies on these cutting-edge medical devices from an innovation system perspective are needed to enrich our understanding of the unknown part of the medical device sector.

Conclusion

Through its endeavor to build an innovation system, the Chinese medical device sector has made some progress toward satisfying the domestic medical demands and improving its industrial competence. In the course of the system building, the government guidance on how to take the strategic initiative coupled with its across-the-board support played a decisive role. However, knowledge development and diffusion is posing severe challenges to the sustainability of this innovation system. More effort and judicious use of resources available are needed for the medical device industry in China to achieve speedy development on a sound education and health research basis that is forged in the service of this sector.

Supplemental Material

Supplementary_file_1_-_interview_guide – Supplemental material for Building an innovation system of medical devices in China: Drivers, barriers, and strategies for sustainability

Supplemental material, Supplementary_file_1_-_interview_guide for Building an innovation system of medical devices in China: Drivers, barriers, and strategies for sustainability by Sok Teng Cheong, Jian Li, Carolina Oi Lam Ung, Daisheng Tang and Hao Hu in SAGE Open Medicine

Footnotes

Acknowledgements

The authors acknowledge all the participants in research material collection. Also, we appreciate the valuable comments from the reviewers and the editor, which helped to improve the whole manuscript.

Consent for publication

Written consent was obtained.

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Ethical approval and informed consent

Ethical approval for this study was obtained from the University of Macau (MYRG160(Y1L2)-ICMS11-HH), and written informed consent was obtained from all subjects before the study.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This research was funded by the University of Macau (File no. MYRG160(Y1L2)-ICMS11-HH).

Supplemental material

Supplemental material for this article is available online.

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.