Abstract

Many financial literacy educational efforts mainly focus on teaching money management. However, money management alone does not address financial prerequisites concerning home ownership, savings or retirement planning since these issues are governed by agents outside households, namely the financial system and policy makers. This study examines students’ response to a financial literacy teaching that treats financial issues as controversial and contextually bounded to the financial and societal systems. Data consists of 36 students’ conversations during a financial literacy teaching intervention. Results show that students are capable of grasping and relating to financial concepts where association to the financial system and policy-making produce elaborate understanding. Furthermore, students that contest given financial concepts and system do not only present constructive alternate solutions for the future, but these students also seem to grasp current financial and societal systems in more advanced ways and thereby demonstrate a possible convergence between financial literacy and citizenship education.

Introduction

Since contemporary societies leave the individual responsible for choosing and defraying housing, healthcare and pensions, the ability to interact with the financial system is considered an important competence for all (Retzmann and Seeber, 2016). To meet this demand in education, the Organisation for Economic Co-operation and Development (OECD), along with many national educational frameworks and curricula seem to promote financial literacy teaching and learning that mainly focus on money management, such as income and expenditure (Bosshardt and Caltabiano, 2013; Menzies and Wood, 2012; OECD, 2018; OECD/INFE, 2015; Tisdell et al., 2013), along with a message of prudence concerning loans and mortgages (Lucey and Bates, 2012). But even though money management and the ability to calculate future expenditure and interest (cf. Lusardi, 2015; OECD, 2018) are indisputable prerequisites for managing a household, money management do not sufficiently inform individuals when dealing with welfare functions that are governed by authorities far outside the confining walls of households, namely by financial markets and policy makers. Essentially, educational intentions and financial realities show several aspects of inconsistency where educational questions and aims do not address financial issues relevant to young people.

In response, researchers have associated financial literacy with economics (Berti, 2016; Retzmann and Seeber, 2016) and different forms of citizenship education (Björklund and Sandahl, 2020; Davies, 2015; Lefrançois et al., 2017). However, research has not paid much attention to the implementation of such curricular initiatives. Yet one scarce example comes from Sweden where Björklund (2019, 2020) investigated how social studies teachers in upper secondary school perceive and realise financial literacy as a segment within social studies, which is Sweden’s primary subject for citizenship education (Sandahl, 2015). Even though the social studies syllabus invites teachers to utilise features from both economics and citizenship education when teaching financial literacy (Swedish National Agency for Education [SNAE], 2018), Björklund (2019, 2020) show that teachers still perceive the financial literacy segment as unresolved. This also resonates in content choices, teaching designs and stipulated aims. Many social studies teachers do not consider financial literacy to fit with the other content features included in social studies.

Two issues seem to illustrate the impediments of associating financial literacy with citizenship education. Many teachers have a hard time to combine financial literacy with social studies since they relate financial literacy to be a private and not a societal matter (Björklund, 2020). Furthermore, teachers tend to stress colloquial and life-skill features of financial literacy, which seems to prompt a financial literacy approach with focus on money management (Björklund, 2019).

However, a financial literacy approach that actually addresses financial and societal interrelations towards individuals and households, also poses challenges to teachers and students alike. In an earlier study, students responded to a question concerning financial liability when a changed interest rate put an individual in financially unsustainable situation (Björklund and Sandahl, 2020). Answers suggested that students are able to both problematise issues related to the current financial system as well as suggesting alternative financial solutions for the future. Students’ answers also changed the very perspectives of financial issues, from being something personal to becoming a question of banks, the financial system and political initiatives. However, every time students shifted perspective, from one financial context to another, students addressed a new learning objective which made previous understandings and perspectives precarious. These learning objectives were the financial system, political governance and the societal system. Each of these learning objectives was framed as threshold concept (Land et al., 2003), hence concepts decisive for students’ further financial understanding (Björklund and Sandahl, 2020).

This paper contributes to further elaborate a financial literacy teaching design that addresses financial issues in relation to the financial system, political governance and the societal system, hence addressing teaching and learning difficulties conveyed by social studies teachers and students alike. This is framed as a teaching intervention that explores students’ response to a financial literacy teaching that treats financial issues as controversial and relates personal finances to financial and societal intentions and possibilities.

The aim of this article is to identify and discuss principles for a financial teaching design that utilises epistemic means from citizenship education. The following research questions are addressed:

What kind of financial and systemic knowledge should be added in advancing students’ financial understanding?

How does a teaching design that treats financial issues as controversial affect students’ financial understanding and learning progression?

Financial literacy education: Origin and implementation

Financial literacy is mainly discussed on a political and curricular level which is consistent with the origin of financial literacy as school subject. Soon after the financial crises of 2007–2008, the OECD intensified their attempts to introduce financial literacy in national curricula worldwide (OECD, 2017; OECD/INFE, 2015). The OECD financial literacy approach, with focuses on money management and compliance with current political and financial order, became an important model for curricular discussions and national frameworks (Bosshardt, 2016). Many national frameworks seem to follow an approach (Bosshardt and Caltabiano, 2013; Menzies and Wood, 2012) where financial literacy education is considered a panacea to a societal problem. Concrete effects, however, are hard to identify in society (Lusardi, 2015). At the same time, the ambition to organise a financial literacy teaching that actually makes a difference in young peoples’ lives seems to be strong (Blue et al., 2014; Fernandes et al., 2014; Huston, 2010; Walstad et al., 2010). However, research suggests that financial literacy curricula fail to address financial questions which relate to students’ life-world experiences (Tisdell et al., 2013). Some researchers even question whether financial literacy is teachable to students who do not manage a household themselves (Lee, 2010).

In curricular discussions, a lack of epistemic origin is suggested to make financial literacy incomprehensible when taught as a singular subject (Remmele, 2016). The OECD approach is also criticised as being insufficient in providing the proper means for coming generations in relation to financial expectations stipulated by the OECD. Therefore, associations with other disciplines are discussed. Many argue that financial literacy should be associated with economics which would provide a broader context and prepare students to become financially informed and active citizens (Berti, 2016; Retzmann and Seeber, 2016). However, other research results suggest that merely associating financial literacy with economics does not appear to promote financial literacy learning significantly (Gill and Bhattacharya, 2019). Another strand of research stresses the political dimensions of financial literacy and point out that economic pretexts must be balanced against the intentions of economic policy. Otherwise, the individual will be left with all financial responsibility, even for matters that households cannot affect (Davies, 2015).

Against this background, citizenship education has been suggested as being able to provide the proper means for teaching financial literacy. In this field of teaching, the democratic aspects of being financially educated and able are put forward (Amagir et al., 2018) and neo-classical aims of traditional financial literacy education should be disclosed and discussed (Sonu and Marri, 2018). Several studies argue for the use of Westheimer and Kahne’s (2004) conceptions of citizenship when teaching financial literacy (Björklund and Sandahl, 2020; Khalil, 2021; Lefrançois et al., 2017; Lucey and Bates, 2012) which emphasise that financial education should support individuals’ ability to take active part in current society as well as the ability to take leadership in future financial and societal change.

As mentioned earlier, financial literacy is taught in Sweden’s upper secondary school as a segment of the compulsory course in social studies (SNAE, 2018). Social studies is the primary subject for citizenship education in Sweden, based on political science, economics, sociology and law (Sandahl, 2015). Although Swedish social studies teachers have taught financial literacy since 2011, many teachers still perceive financial literacy as something unresolved. Teaching aims in financial literacy seem clenched between practical money management and a teaching that considers financial issues as being systemic and political, and many teachers convey that they cannot fit financial literacy into social studies. In absence of consistent teaching approaches, students’ presumptive future financial needs inform teachers in content choices and instructional approaches. Thus, many different forms of financial literacy teaching exist, yet many lean towards money management (Björklund, 2019, 2020). Here, the epistemic means from citizenship education are not utilised in financial literacy teaching. Such epistemic means could invite students to different perspectives and to consider the aims of different agents which is normally understood through contextualisation (Sandahl, 2020).

In order to find a way forward for financial literacy teaching it is important to encapsulate an aspect of the collective criticism against traditional financial literacy teaching. As long as financial issues are considered mainly a private matter and financial literacy education mainly seeks answers in the context of households and individuals (Davies, 2015; OECD, 2017; Retzmann and Seeber, 2016), financial literacy will not provide sufficient means to manage personal finances since financial prerequisites, including terms and regulations, are formed and controlled elsewhere. Consequently, it appears to be important to shift financial contexts and relate personal financial aspects to the financial system and financial policy making when teaching financial literacy. At the same time, it seems to be a general concern that upper secondary students are not financially proficient to make these connections and that they first have to learn money management (OECD, 2018).

When asked, however, secondary students are aware of future financial liabilities and expectations (Ali et al., 2014). There are also indications that secondary students understand the importance of a balanced budget where expenditure cannot exceed income (Björklund and Sandahl, 2020). Therefore, it seems feasible to move forward and place the focus of financial literacy teaching in the interrelation between the individual and the financial and societal systems. In other words, to treat financial literacy as a societal issue which affects individuals and households, but at the same time treat it as a societal issue that is possible to shape.

In a previous study, Björklund and Sandahl (2020) explored students’ financial reasoning (concerning both content and contextual associations) by inviting secondary students to discuss financial liability in relation to the question of how drastically changed interest rates affect individuals. The students’ answers revealed three issues that are important to regard when devising a financial literacy teaching that utilises both students’ pre-knowledge and means of citizenship education. Firstly, the students were generally aware that there are financial structures and agents that affect household finances. Secondly, when analysed through Westheimer and Kahne’s (2004) citizenship conception, few students perceived the financial system as something that can be influenced or changed democratically. Thirdly, each step of changed financial perspective, namely the financial system, political governance and the societal system posed specific learning challenges for students when analysed as threshold concepts (Björklund and Sandahl, 2020; cf. Land et al., 2003). These results in general and the threshold concepts in particular became important when the teaching intervention for this study was designed.

Theoretical framework

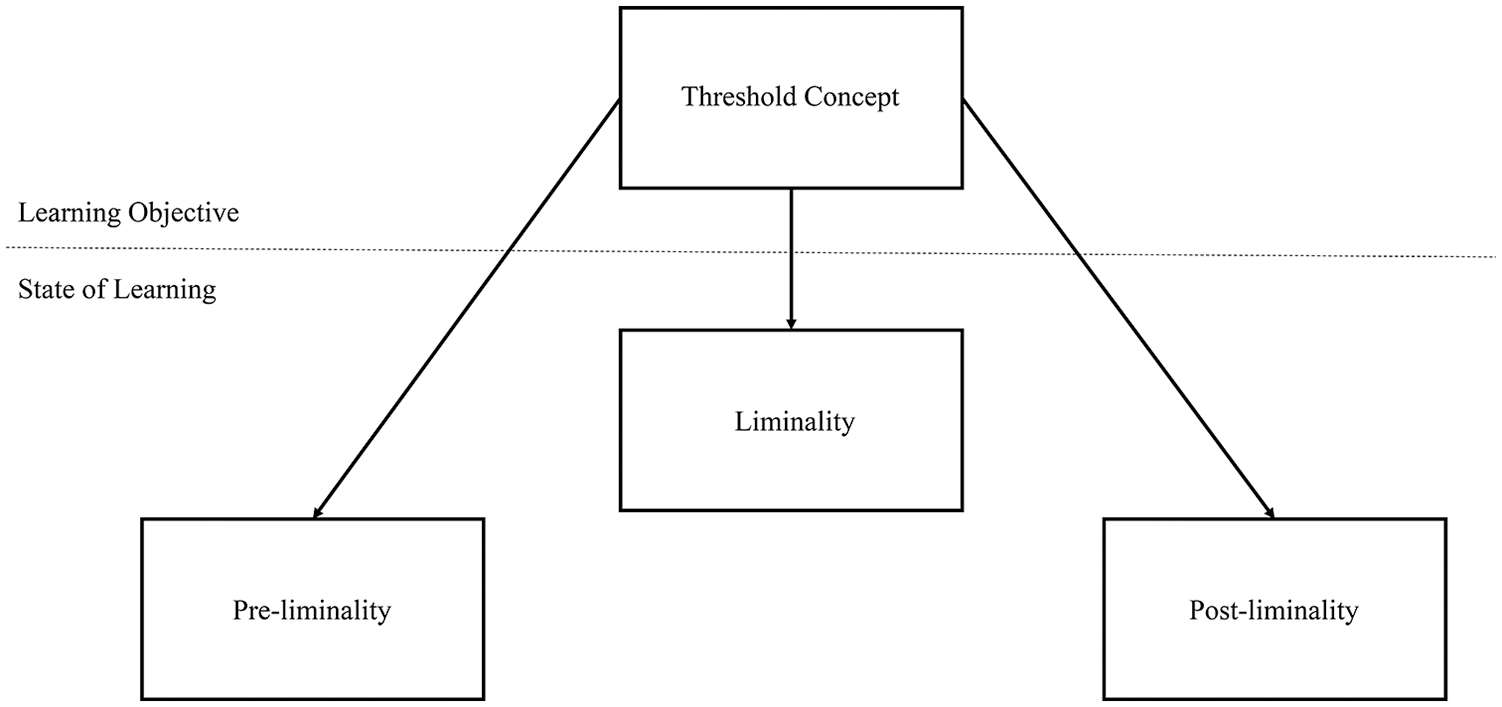

When researching students’ learning processes and identifying possibilities and impediments in relation to learning objectives, it is important utilise an instrument for analysis that focuses on learning of troublesome questions. Such questions usually concern knowledge that is conceptually difficult and counter-intuitive where presumptive answers can include different aspects. Therefore, the framework of threshold concepts (Land et al., 2003) and its construction of liminal spaces (Land et al., 2014) appear to be feasible. Threshold concepts bind a subject together and when students grasp such concepts, they are supposed to pass through a disciplinary gateway of understanding. A threshold concept has a number of generic features. A threshold concept is transformative in its capacity to significantly shift students’ perception of a subject. It is irreversible since students are unlikely to forget it. It is integrative since it exposes earlier hidden epistemic relations which can be described as an underlying game or structures that organise facts and truth claims. It is bounded with conceptual borders to other conceptual domains which constitutes an important function to contextualise and define the concept. Finally, a threshold concept often consists of troublesome learning, usually due to an inherent complexity of counter-intuitive nature. The latter means that the use of common sense to grasp the concept often mislead students’ understanding. Therefore counter-intuitive learning can be said to be troublesome in itself (Davies and Mangan, 2007; Land et al., 2003, 2014, 2016).

This turns the focus to the learning process of threshold concepts. When passing through the conceptual gateway, students commonly experience stages of doubt and uncertainty which are defined as steps of liminality (Cousin, 2006; Land et al., 2014). Traditionally, the liminal steps are presented in an order which appear to follow students’ learning in a linear and temporal fashion. The first step is a pre-liminal phase where students are instigated to encounter the troublesome piece of knowledge. This evolves into a second, reconstitutive, step which is denominated as liminal which often includes partial understandings or ‘stuck places’ where students often ‘oscillate’ between earlier understandings and new conceptual knowledge. In this process the use of ‘mimicry’ is common, where students imitate or try to grasp the concept by manifesting superficial or limited understandings. At the same time ‘heterotopia’, which consists of divergent opinions and conceptions of the topic at hand, can contribute to alternate and elaborate understandings of the threshold concept. In the third post-liminal consequential step, an understanding of a threshold concept is expressed (Cousin, 2006; Meyer and Land, 2005; Meyer et al., 2010).

However, it is important to distinguish between different forms of troublesome learning. Several studies use threshold concepts to discuss a piece of learning that has a quite distinctive and disciplinary defined nature yet is still hard to grasp for most students. Adjacent examples to this study are threshold concepts in economics such as opportunity cost (Shanahan and Meyer, 2006) or price and cost (Davies and Mangan, 2007) which constitute fundamental pieces of learning that enable students to discuss economic problems. The threshold concepts presented in Björklund and Sandahl (2020), such as political governance or the societal system, however, present an inherent troublesome nature where students need to understand different aspects of a concept that appears to vary in meaning depending on focus and context (cf. Perkins, 2006), hence no singular disciplinary solution is at hand.

In this study it is therefore important to recognise the inherent troublesome nature of the concepts that students are trying to comprehend. The liminal state also offers a number of opportunities for students to grasp different aspects and views of a troublesome concept where their understanding does not congeal or become simplified. When students remain in the liminal state, the possibility of heterotopia may occur, where presumptions and earlier understandings are questioned and previous unthinkable options are considered which not only may enable an understanding of the threshold concept itself, but also produce new solutions to old problems. Therefore, the lesson design in the classroom intervention aspired to keep the students in a liminal state during their discussions as long as possible. Thus, it is neither certain nor desirable that students’ learning follow the linear appearance from pre-liminality, via liminality to post-liminality (see Figure 1) (cf. Land et al., 2014).

Threshold concept in relation to states of liminality (cf. Land et al., 2014).

Methodology

The classroom intervention

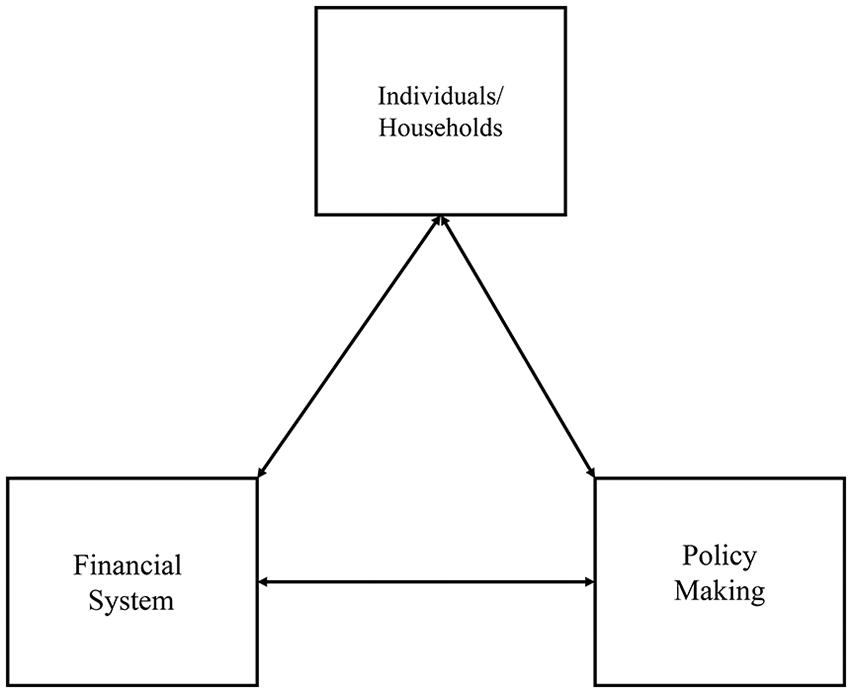

When designing the financial literacy teaching intervention, the threshold concepts: the financial system, political governance and the societal system form a backdrop when choosing design principles. Two major means, derived from citizenship education, were utilised – a shift of financial contexts and problematising financial concepts. To be able to displace financial discussions, a systemic model was used which gave financial literacy teaching a new context. Households was related to the two major structures that frame the financial system and deeply affect households’ financial liabilities and opportunities, namely the financial system, mainly presented as banks, and aspects of policy making possible to affect by democratic means (see Figure 2). However, evidence from Björklund and Sandahl (2020) suggest that this alone would probably not have been sufficient to provide students with new financial insights and perspectives.

Financial literacy teaching context.

Financial and societal systems, however functional they appear to be, also include inconsistencies which can have an adverse effect on different agents in systems. In relation to this, given financial concepts such as risk and liability, do not mean the same thing for banks as they do for individuals. Therefore, it was important to invite students to discussion and critical scrutiny which had an aim to uncover the origin and nature of existing financial and societal systemic features as well as the possibility of political and financial change.

To advance such an ambition in a teaching intervention and to utilise citizenship educational means, the Beutelsbach consensus (Christensen and Grammes, 2020; Reinhardt, 2016) seemed like a feasible organising principle. The Beutelsbach consensus is an agreement formulated in 1976 that stipulates guidelines for all social science education in Germany. The agreement consists of three basic principles. Firstly, it is prohibited to overwhelm the students with desirable opinions and hinder them to form independent views and judgements. Otherwise, education can turn into indoctrination. Secondly, controversial issues must be treated as controversial in the classroom. The teacher should never supress views or opinions and be careful when correcting students. Thirdly, students should be invited to analyse political structures to probe their own opinions against these structures. Furthermore, students should also be given the opportunity discuss how they could affect political decisions and structures (Christensen and Grammes, 2020; Reinhardt, 2016).

The intervention was designed as a segment over four lessons where two lessons lasted 60 minutes, and two lessons lasted 90 minutes. The intervention was executed in three different higher education preparatory programme classes in year 10 which included 87 participating 16-years old students. The three different classes were taught by three different teachers which were all consulted when the researchers designed the intervention. One of the researchers observed all the lessons and helped to administrate the recording of the students’ discussions. The lesson design was quite meticulous; however, it cannot be considered to be a manuscript. Therefore, variations in relation to phrasing, students’ questions and additional explanations and discussions occurred, which was essential to create a natural teaching. However, all three classes were taught the same way in relation to content, context and major questions to discuss, and therefore teaching in all three classes must be considered to be equivalent.

The first lesson started with a brief example of budgeting income and expenditure but swiftly shifted to its main issue – savings in relation to risk and revenue when buying different bank products. Students were given the opportunity to discuss merits and disadvantages with different forms of savings along with the fact that saving money also includes different degrees of risk for the individual. Examples included calculations.

The second lesson focused on income, credit, loans and mortgages which were related to short-term credits for consumption and long-term mortgages and student loans. Students were invited to discuss risks and merits with different credits, loans and mortgages. In relation to this, students also discussed that individuals have the freedom to choose to take on debts to buy different things such as consumer products and services, cars and homes. Examples included calculations of interest rates and how changed interest rates or mortgage regulations could affect household finances.

The third lesson concerned how banks earn money by producing bank products such as mutual funds, credits, loans and mortgages and how banks relate to risk, interest and revenue. Here general financial rules and regulations such as the Swedish government deposit guarantee and freedom of contract were discussed. This formed a background for discussing banks as producers and sellers of bank products and individuals as buyers and consumers of the same bank products. Sellers’ and buyers’ different terms were discussed. Small groups, which consisted of three to five students, were invited to discuss two questions which were recorded. The discussions lasted between 2 and 18 minutes where the average length was 10 minutes. The two questions discussed were:

Do you consider banks and individuals to have equal terms on the savings and credit markets?

Do you think that something should be altered in the relation between sellers and buyers on the savings and credit market?

The fourth and final lesson focused on the financial system as a whole and the different roles and prerequisites for the different agents within the system. Different perspectives on the financial system’s role and function in society were discussed, especially systemic autonomy, political regulations and the possibility to change the system by democratic means. Once again, the same groups of students as in lesson three, were invited to discuss the final questions. Discussions were once more recorded. Discussions lasted between 2 and 15 minutes where the average length was 9 minutes. The two questions discussed by students were:

What merits and disadvantages does a deregulated financial system have in a democracy?

How do you think that the financial system could be reformed?

Thus, the teaching design invited the students of relating financial issues to a financial and societal context, and to problematise financial issues in two steps. Teaching aimed at uncovering the integrative and bounded nature of the concepts presented to students, hence, to make students understand issues of sometimes counter-intuitive nature. The questions were aimed at inviting students to discuss the inherent troublesome nature of the concepts while remaining in a liminal state. Thus, it is desirable that students oscillate, yet also are confident enough to present suggestions we can denominate as heterotopia. For this study, conversations also showed different outcomes of the teaching design.

Study setup

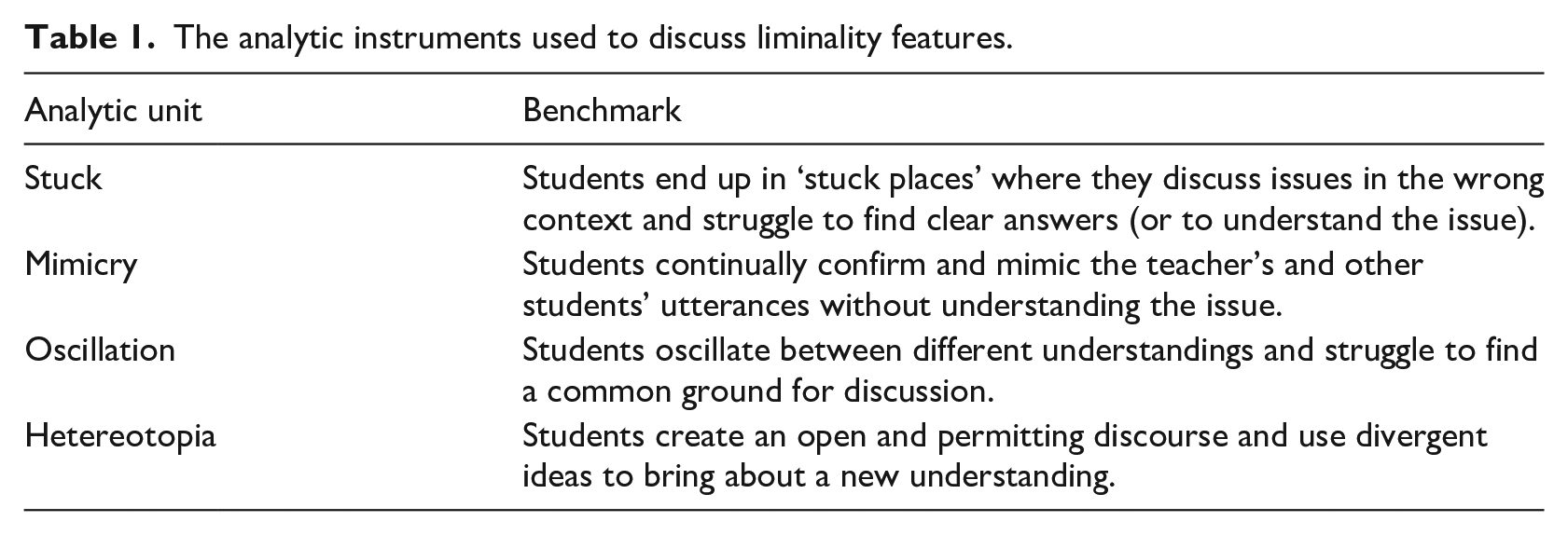

Data consists of 36 recorded student discussions from the end of lesson three and four of the intervention. All discussions were verbatim transcribed. The student discussions were later theoretically coded, using the construct of liminal spaces as an organising principle. Since every discussion was sprung by two different questions, each discussion was first divided in relation to which question it concerned. When called upon, each conversation was divided into smaller sections following the content of the conversation, hence following principles of a traditional content analysis (Krippendorff, 2004). Each part was later coded in two steps which utilised the construct of liminal spaces as an organising principle. During the first step each part of the conversations was coded as an example of pre-liminality, liminality, or post-liminality where conversations coded as liminal often lasted longer than 10 minutes and conversations coded as pre-liminal or post-liminal often were shorter than 7 minutes. During the second step, each part of the conversations was related to the different features of liminality. Thus, the features of ‘stuck’, ‘mimicry’, ‘oscillation’ and ‘heterotopia’ formed pertinent instruments of analysis. The analytic instruments are described in Table 1.

The analytic instruments used to discuss liminality features.

In the following analysis the different features of liminality were used to discover patterns in each form of liminality in relation to the different features of the threshold concept construct. In order to discuss the plausibility of these patterns they were compared with the original content analysis. Thus, the liminal features and the patterns they create in each liminal step could be compared to the discussion questions and contextual intention behind the lesson design and uncover how this troublesome learning appear before students. To emphasise the liminal stage as a desired aim with the intervention the conversations that convey pre-liminal and post-liminal understanding are presented before the conversations that exemplify liminality in the results chapter.

Since all conversations were conducted in Swedish, the conversations displayed in this paper were translated into English where underlying intentions and colloquial expressions were preserved as far as possible. Students participating in the conversations were also given pseudonyms.

Results

Pre-liminality

Students which convey pre-liminal understanding do not really grasp the underlying problem they are supposed to discuss. Instead, these students instrumentally relate to the question given to them:

Do you consider banks and individuals to have equal terms on the savings?

Well, I think that it has to be something that divides the two. . .

Yes! (laughter)

…

What was the question?

What do we believe? Ok, the question. . . Do you consider banks and individuals to have equal terms on the savings and credit markets? Do we believe it to be so?

Well. . .who knows. . .

Several groups of students seem prompted to deliver a shared answer to the question rather than discussing the problem. This obviously becomes an obstacle for further understanding. The following discussion is a representative example:

Should we deal with the next question?

Yes!

But how should we answer this question then?

Question one?

Question one!

We haven’t reached any conclusion!

That is my opinion as well.

Well, let’s say that there is a difference then!

Both examples can be referred to as mimicry in relation to the task and to the classroom situation. Students mimic features usually associated with schoolwork, such as sitting together in a group discussing a question and presenting an answer to these questions. Neither setting nor questions, however, seem to instigate these students to confront the problem presented to them.

Other student conversations engage with the stipulated problems; however, these students utilise conceptual understanding from other contexts, separate from the societal context that the questions refer to, which leads to pre-liminality. The students, however, quickly accept the conclusions which are put forward in the discussion, which impede further debate and understanding:

What merits and disadvantages does a deregulated financial system have in a democracy? What do you think?

Well, the merits are that you can earn a lot of money if. . .if so, there is no competition law or something like that. Then you can buy companies. . .

Aha!

…that try to compete you out of existence.

Precisely! Excellent! Anyone else that comes to think of any merit?

No not exactly. . .

This is also an example of mimicry, yet here related to the use of facts and context which leads the conversation in a direction which do not support any further learning. Students refer to a deregulated financial system in terms of free competition of corporations rather than to the role of financial institutes and banks in society and its effect on individuals and society. This shows the importance of understanding how a concept is bounded towards other concepts and how this affects meaning and significance in a particular context.

As referred to earlier, most students lack their own experiences of financial use and managing a household. Still, students tend to utilise their own life-worlds experiences as examples and contexts for discussing the problem. This often leads students into stuck places and represents a salient example of pre-liminality:

Well, the financial system has a few functions such as effecting payments and to convert savings to funding and to handle risk. So, what should be altered here. . .well what can you say. . .in my opinion no alteration is needed because I think that everything seems to work just fine. What do you say?

Well, I don’t know

If you want to transfer money to a friend. Does that work well?

Yes!

Perfect!

Is it?

Or. . .if you transfer money. . .Then I have to know the account number!

No Swish! (The major Swedish p2p-system for money transfers)

…

But then you don’t transfer money to someone’s account.

Yes you do!

…

Yes you do! Swish is really convenient if you know that person’s phone number, and that you can look up!

Here, the students do not use the theoretical teaching they have received over four lessons which revealed possible relations between the different agents in the financial and societal system. Instead, students utilise their own life-world experiences to discuss the problem in relation to intuitive explanations, which prevent them from approaching the problems embedded in the question. These students mimic features of understanding, yet without grasping the integrative features of the problems presented to them. Thus, a salient obstacle for students that display pre-liminal understanding seems be a lack of basic conceptual understanding. This leads them to mimic both classroom activity and conceptual pre-knowledge which also impede further oscillation towards new advanced knowledge.

Post-liminality

A common feature of the discussions categorised as examples of post-liminal understanding is that students tend to present ‘the right answer’, often in a very self-evident and direct manner. The depiction of answers as being correct and complete impede further oscillation and thwart heterotopia. A notable tendency in these discussions is to utilise common-sense explanations deriving from the assumption that the financial system is fair and natural:

Well interest, that’s a good thing because they (banks) earn money in relation to our loan.

Yes. . .

That’s a good thing because then they gain from that – they still do a job and we borrow money from them.

Yes that’s true.

…

We receive the money we don’t have.

Yes. . .that’s pretty fair and the banks can’t decide on funny interest rates because then you turn to a different bank!

Here the integrative understanding of the financial system is equated with an acceptance of an underlying epistemic logic, perhaps deriving from earlier economics studies, or from conversations at home. This integrative understanding seems to overrule any other assumptions concerning the topics that are up for discussion, for example concerning a desirable relation between individuals and banks:

I’ve been told about this since first grade.

Well, I haven’t!

It’s because my mother works at a bank.

Yes.

So I hear about these things all the time.

That gives you a head start, but to me this relation (between individuals an banks) is a bit fuzzy and I don’t really know what to think. . .We’re buying a mutual fund, from which we can profit or lose, then it’s up to the bank and that’s not really fair. So then you, perhaps could come up with some (alternate solution) . . .

But if the mutual fund is earning or losing money – that’s not the bank’s fault. It’s still your decision to buy it!

Yes exactly. . .and therefore the individual should think better so it becomes more fair, I don’t know!

…

What is unfair, do you think?

Well, I don’t think that anything regarding the relationship should change. I think its functional as it is.

Well I don’t really know about that. . .

The bank gives you advice on what to buy – what they think will thrive. But you’re still the one that has to decide what to do. So, you’re still accountable for your own choices from which you have to face the consequences!

Here the epistemic use inexorably moves the discussion into a post-liminal state where the integrative understanding is absolute and impedes any disagreements which could be used to question presumed self-evident concepts and further develop an understanding of the underlying premises of the financial system. A delicate balance becomes evident. Integrative understanding is a premise to avoid stuck places and mimicry. However, this epistemic understanding could easily turn into a systemic compliance including instrumental understanding of economic causal relations and truth claims. In similarity to the pre-liminal discussions the problem is not really discussed. Instead these discussion rush to solve the question.

Liminality

Common features of the discussions categorised as examples of liminal understandings are that students show a conceptual understanding, yet at the same time all questions are discussed as problematic and controversial, hence answers and conclusions are not considered as given and self-evident. Perhaps this can be related to an understanding of the inherent troublesome nature of the concepts used in these conversations. Hence, the balance between a conceptual understanding and problematisation also seems to occur as a result of students’ attitude of embracing divergent conceptions and opinions. However, the importance of students’ integrative conceptual understanding is an important prerequisite for all liminal conversations:

You said earlier that the banks take the biggest risks. I would say that the households take the biggest risks!

Why?

Because we are people. . .and, perhaps you shouldn’t relate anything to emotions and such, but. . .it affects families more if they lose all of their money compared to a bank which is just a corporation.

Well, yeah. . .

It’s people that get hurt and I think. . .in the relation between buyers and sellers, when we invest or buy mutual funds and such – It’s us that take the biggest risk because we invest our money. The bank, they just handle our money and pass it on to these funds. . .so it’s our money they lose. If we profit, then the bank also earns. . .

Yeah, but you have to consider the responsibility that the banks hold.

Yes!

They take. . .huge risks. . .it concerns hundreds of millions!

But at the same time, that’s their field of expertise! They don’t expose themselves to unnecessary risks. When they expose themselves to bigger risks, they also raise the prices (towards the buyers).

…

Does anyone have anything to add?

I think. . .sometimes, when you call your bank to schedule a meeting about a loan. Then they can be rude. Then you don’t know if they can be like. . .sort of manipulative and trick you into doing something you don’t want.

Yes! More clarity in the relationship between banks and households!

Yes exactly!

…

Because they act like advisers, but in reality they’re salesmen.

Yes exactly! Then I think it’s better if they give. . .clearer advise so you totally get what you get yourself into since it concerns money and well. . .it concerns the future.

If the bank became your friend.

But I don’t think that they should be your friend. They should be. . .professional and do their job but they should be transparent enough, so the buyer really understands what he gets himself into.

If the buyer would know all of this, no money would ever reach the banks.

Here, the problem is discussed using the specific concept of risk which is made possible due to an integrative understanding of this concept. The clear use of this concept also gives the discussion a direction. In relation to this, deviant, counter-intuitive, statements, such as the emotive expression concerning whether banks try to fool their costumers, can be utilised to present a new suggestion. This seems to induce a form of heterotopia that causes oscillation which, in turn, keeps the discussion in the liminal state. Conversely, it also seems that this form of heterotopia needs to be balanced against an integrative understanding of other students in the group, otherwise it can lead to a stuck place. The important and delicate balance between conceptual use, integrative understanding and heterotopic use of deviant statements is something that recurs in many of the liminal discussions.

What merits and disadvantages does a deregulated financial system have in a democracy?

It gets easier because. . .as we said earlier, the price shifts in relation to demand, and so forth.

Yes!

Disadvantages can be that it gets easier for banks to take advantage of people. . .and so on, if it’s totally deregulated. But on the other hand. . .

Like transferring money.

…if it’s too regulated, then perhaps no one wants to manage any banking.

No! In that case the government probably will govern the banking.

Yes!

…

You remove all means of competition when you make too. . .

Yes! And it’s not always a good thing when the government runs everything!

No, no! It’s probably for the best if someone else and not the government looks after money. . .

Exactly!

…

You need a little competition!

Yes, and it’s probably not a good thing if the government is in control of both money and all political decisions.

No, cause the government can. . .raise the price on loans without the knowledge. . .

Yes.

…the banks possess. Banks can also do that, but they have a greater understanding of what their customers find acceptable.

Epistemic relations, including both economic and political understanding, of the concept of regulations are utilised to discuss the problem. Yet, it is when a counter-intuitive suggestion concerning governments and banking is inferred that the discussion gain a momentum. Hence, heterotopia causing oscillation is a significant element to advance students’ understanding of financial matters in a societal perspective. The latter becomes even more evident when an integrative understanding and compliance of the financial system changes into self-evident coherence and conclusions.

Discussion

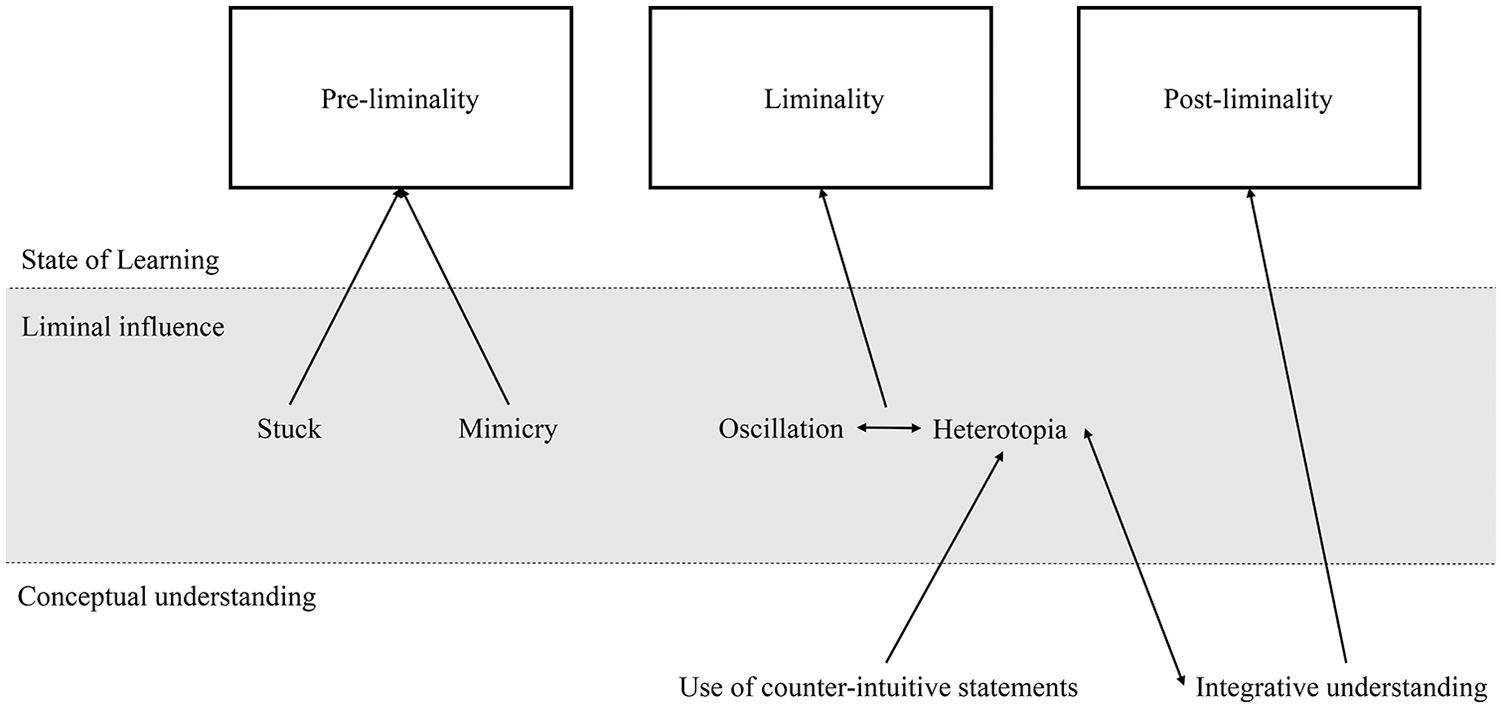

Results from this study show that students get stuck and remain in a pre-liminal state when they solely relate financial issues to their own life-worlds, that is, students’ understanding become contingent and anecdotical (cf. Björklund and Sandahl, 2020). This can, to some extent, explain students’ difficulty in noticing the relational aspects of financial matters which, in turn, lead to that generalisations and understandings of financial principles become unreachable. Perhaps the most salient feature of the pre-liminal conversations was students’ lack of understanding concerning how the concepts are bounded, especially in terms of contextual understanding. Thus, the questions students were supposed to discuss during the intervention simply became something they responded to without considering any underlying meaning or relation to the subject at hand, hence a kind of instrumental learning. Instead of discussing the problem presented to them, the questions triggered conversations where students delivered answers in line with what they think that the teacher wants.

Results also show that students that consistently comply with the current financial system and adopt an instrumental understanding, and hence assume full predictability of economics, tend to obstruct further discussion which also impedes a further understanding of financial concepts as something dependant on current and future financial and societal systems. Hence, an unbalanced use of the integrative understanding of financial concepts, such as liability or risk, is the most salient feature of the post-liminal discussions. Results in this study imply that students’ life-world experience can lead to post-liminality as well, yet here, the cited student referred to the experience deriving from a parent which must be considered something different compared to life-world examples deriving from a student’s own experiences. We believe that parents and other adults will remain an important source of financial knowledge and experience for students (OECD, 2017).

Furthermore, this study shows that it is important for students to challenge and discuss the current financial and societal order, both with an objective to understand this system as well as to acknowledge alternate future world-orders. However, the same approach seems indispensable if students should be able to relate personal financial issues to affecting factors in society. In relation to this, challenging statements, and even misconceptions, are decisive to prolong debates and allow participants to elaborate their financial understanding. Hereby, heterotopia can offer students a more complex understanding of financial concepts and relations, hence heterotopia is the most salient feature of the liminal conversations. Students’ financial literacy learning in a liminal state appear to be a result of a very delicate balance between integrative understanding, hence theoretical insights concerning the relational nature of all financial issues provided by teaching, and practical experience deriving from real-life examples, where students actually realise that financial issues concern them.

Students’ understanding in relation to liminal steps.

Keeping this delicate balance in mind, we believe that these results can inform future lesson design and teaching. However, it is important to recall the teaching challenges social studies teachers face. Many teachers consider financial issues as private and colloquial (Björklund, 2019) where they also contextualise financial literacy using the students’ current life-worlds (Björklund, 2020) which is consistent with salient curricular discussions (OECD/INFE, 2015; Tisdell et al., 2013). This approach seems to produce traditional financial literacy teaching with focus on money management along with a view of financial matters as something private (Bosshardt and Caltabiano, 2013; Menzies and Wood, 2012; OECD, 2017). Here, focus is placed on matters that do not seem to add any new knowledge for 16-year old students (Björklund and Sandahl, 2020) and do not explain the financial prerequisites that deeply affect all financial agents, including individuals.

However, due to the lack of an established epistemic foundation for financial literacy teaching (Remmele, 2016) which would function as sense-making, it is hardly surprising that teachers focus on meaning-making aspects (Sandahl, 2015; Svingby, 1986) in their financial literacy teaching. Nevertheless, we believe that two explicit measures can inform and help teachers to change their financial literacy perspective to create a balance between theoretical and practical elements in their teaching.

Relate financial literacy teaching to financial contexts and legislation

First, teaching should shift the conceptual focus of financial literacy teaching from being solely focused around money management to include concepts like financial regulations, freedom of contract and risk which seem important to emphasise if students are supposed to discuss both current and future world-orders in financial terms. At the same time, it is important to stress the interchangeability of these concepts along with the contexts they appear in. This teaching approach also stresses the differences between how personal finances function in comparison to how the economic and financial system work which also shed light on different functions and agency that different entities in the system have. Such a teaching approach can utilise epistemic means from other disciplines that social studies teachers are proficient in, such as political science and economics. Thus, the epistemic means of citizenship education can make financial literacy comprehensible for both teachers and students (cf. Remmele, 2016). These epistemic instruments also have the potential to function as sense-making for students since the underlying rationale and principles from political science and economics are used to explain financial matters (Sandahl, 2015; Svingby, 1986). Consequently, students should be invited to a financial literacy education that really has the potential to matter in their future lives. It is reasonable to consider financial matters as highly political and a democratic issue (Davies, 2015).

Teach financial issues as controversial issues

Second, teaching should actively invite students to problematise financial concepts and contexts. Hence, discussions can function as a possible method of instruction, since students need to utilise elaborated conceptual and contextual understanding; potential deficiencies in students’ understanding also become visible for teachers, who can address these issues in class. Therefore, the Beutelsbach consensus (Christensen and Grammes, 2020; Reinhardt, 2016), where students are invited to discuss different alternatives and probe their own opinions against these alternatives, seem like a feasible approach for financial literacy teaching in terms of citizenship education. The same approach also could counteract assumed indoctrinating aspects of financial literacy (Arthur, 2012; Berti, 2016; Sonu and Marri, 2018) and become a contribution to richer and fuller citizenship education (Björklund and Sandahl, 2020; Davies, 2015; Lefrançois et al., 2017).

Results from this study can also contribute to financial literacy curricular discussions. Collectively, the results further substantiate the need to contextualise financial literacy together with the financial system and political decision-making in order to produce a relevant and elaborative financial education. Concerning the means to do just that, this study concurs with several other studies regarding the need for financial literacy teaching to utilise the epistemic means from other disciplines. Here, different voices in the debate do not really contradict, but rather complement each other. For this study, the Swedish social studies subject, which can be defined as a citizenship education (Sandahl, 2015), constituted a teaching context where the students already had received basic teaching in political science and economics. Thus, this study agrees with Retzmann and Seeber (2016) and Berti (2016) regarding the importance of economic understanding when learning financial matters. Yet, in order to recognise temporal matters and propose incentives for change, political and democratic dimensions of financial and economic issues are central to emphasise in teaching since they turn financial matters into societal issues. Therefore, this study is in line with Davies (2015) and Lefrançois et al. (2017).

Conclusions

In a wider perspective, it is important to stress the fact that 16-year old students really can grasp complicated financial and societal matters (cf. Ali et al., 2014; Lee, 2010; OECD, 2017, 2018; OECD/INFE, 2015). However, very little seems to support that financial literacy should be included in any curriculum due to internal ends. Instead, the future of financial literacy teaching and learning will depend upon its presumptive societal significance. Here, citizenship education, including criticism and discussion (Khalil, 2021; Lefrançois et al., 2017), cannot only educate independent and self-sufficient individual, but also help students to grasp financial concepts and further understand financial and societal prerequisites important for their future (cf. Biesta, 2011). Even though financial issues seem to be sensitive and deeply private for many students (Appleyard and Rowlingson, 2013), financial issues are also private matters which deeply depend upon societal systems and political decisions. The self-sufficiency, that financial literacy teaching aims for, therefore is deeply dependent on the community and society outside peoples’ homes, which, in turn, is the heart and soul of citizenship education (cf. Parker, 2005; De Tocqueville, 1835/2003). Thus, financial literacy can become a welcome contribution to citizenship education. However, more research is needed especially considering feasible teaching design which utilises teachers available teaching skills from citizenship education.

Footnotes

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.