Abstract

Financial citizenship is crucial in our modern world. Financial citizenship is underpinned by the education of future generations so that they can understand both their local and global economies to make the best financial decisions concerning their lives. This paper discusses financial literacy, how it relates to individual citizens, and how it correlates with social, political and business spheres. According to current financial capability models, every individual’s financial well-being can be boosted by developing their financial knowledge and competency, which will improve their motivations and confidence. Societal constructs significantly create financial socialization, which increases our accessibility and engagements with institutions, businesses, political systems and society as a whole. Being educated about the details required for financial literacy is every human being’s right. Citizens have been characterized as being personally responsible, participatory or justice oriented; each person’s specific perspective can impact their financial lives, which supports the importance of the current concept of financial citizenship. Boosting global education about economic citizenship will help to reduce poverty, create more sustainable economic environments, and improve social outcomes and the life satisfaction of the world population. These concepts will be explored and discussed in this paper.

Keywords

Introduction and background

Since the 1970s, inequalities in disposable income have been on a steady rise within the member countries of the Organization for Economic Co-Operation and Development (OECD). Inequalities in disposable income has become an important issue and has received the focus of political, social, and economic national policies (OECD, 2015). Cross country evidence shows that the financial knowledge of individuals positively affects their financial inclusion and is a key determinant of wealth and economic inequality. Individuals with financial knowledge are more likely to invest wisely than those without it, creating a gap between the financially literate and the financially illiterate, leading to wealth inequality. (Grohmann et al., 2018; Lusardi et al., 2017).

The correlation between financial literacy and financial performance as it pertains to individual outcomes has been the subject of numerous studies since the turn of the millennium. The mainstream hypothesis is that low financial literacy levels among individuals result in suboptimal economic and financial utility choices (Lucey and Bates, 2012). These financial mistakes are reportedly widespread, particularly among young generations, and lead to adverse effects for individual and social economic welfare. Lusardi and Mitchell (2014) and Lucey and Bates (2012) gathered empirical global evidence regarding the correlation between financial literacy and financial outcomes. Their findings showed that low levels of financial literacy correlate with high debt accumulation, high interest rate borrowing, adverse refinancing choices and mortgage defaults. On the other hand, high levels of financial knowledge are strongly linked to several sound short-term financial behaviors such as budgeting personal expenses and credit card payments. Research has also demonstrated that financial literacy is positively correlated with long-term sound financial behaviors such as retirement planning, savings and wealth accumulation, investment diversification, and clarity in setting personal financial goals.

Considering the correlations between financial literacy, various economic behaviors and outcomes in the long and short terms, it is alarming to see additional evidence that most American high school and college students fail financial literacy courses (Lusardi and Mitchell, 2014). This evidence highlights how young people are particularly prone to making adverse financial decisions that affect their own economic welfare. However, despite the strong correlations, a direct causal relationship between financial literacy and financial behavior and the resulting outcomes is still pending. Hilgert et al. (2003) showed that previous financial experience (including mistakes) is the most important source of financial literacy for households. Due to such endogeneities, Lucey and Bates (2012) suspected upward bias in the magnitude of financial literacy that affects financial behavior and outcomes, and recommended testing randomized interventions to effectively identify the causal effects. Similarly, Lusardi and Mitchell (2014) called for further experimental studies to better understand the direction of causality between financial literacy and economic outcomes for individuals.

From a meta-analysis of a total of 126 impact evaluation studies, financial education was documented to significantly affect the financial behavior of an individual. It was also noted that financial education has an impact on financial literacy as well. However, it was noted that financial education was more relevant in high income populations compared to low and middle income populations. From the randomized experiments, it was also evident that some financial behaviors such as handling debts would be more challenging to influence, making financial education and literacy less effective for such a behavior (Kaiser and Menkhoff, 2017)

Similarly, a meta – analysis conducted on financial education in schools shows a positive correlation between financial education and financial knowledge; this is reflective of the education experiences in other fields. Financial education also impacts financial behavior, though it is less significant. It is evident from this literature that financial knowledge has a positive impact on both the knowledge and behavior of individuals (Carpena et al., 2019).

A field experiment was conducted in India to establish the relationship between financial education and financial outcomes based on attitudes, cognition and behavior. The main objective of the experiment was to explore the barriers that prevent the translation of the financial knowledge acquired and the actual implementation of what has been learnt through financial education programs. Secondly, the study explored what interventions were effective in translating the knowledge gained into meaningful outcomes. The findings of the experiment indicate that financial education had a positive impact on attitudes and financial awareness but the impact was less significant for long term financial behavior. The delivery mode of the financial education programs can be tailored to suit individual needs and hence help in individual goal setting and behavioral change as opposed to a classroom-type of delivery (Carpena et al., 2019). For successful financial education programs that will lead to a change in financial behavior, the delivery mode of the content is documented to be important for the successful implementation of the programs.

In a follow up field experimental study in India by Carpena and Zia (2018), several financial education treatment options were explored to establish the relationship between financial education and financial behavior. Three dimensions were assessed, which were financial awareness, numeracy skills and the attitude towards individual finances. Out of the three dimensions, attitude and awareness played major roles in making financial decisions while numeracy skills did not have any major impact on the outcomes within the households that participated in the experiment. Based on these findings, it is clear that emphasis should be placed on people’s attitudes and their financial awareness as opposed to how good they are numerically.

Financial citizenship concerns the ability of an individual to access financial services and products in adequate measures. For an individual to make sound decisions on the available products and services, financial literacy is fundamental. Financial literacy influences retirement planning, wealth accumulation and savings. Financial literacy also determines one’s participation in the stock market. In addition, financial literacy education has been noted to promote equality, civic responsibility and engagement. Equality among citizens is paramount and financial literacy helps to promote this through making them more financially aware and driving them to making informed decisions in their choices of financial products and services (Arthur, 2012).

Current conceptions focus on the personal responsibility of being financially literate; hence, being financially successful and improving the financial numeracy of a person should result in better financial well-being. The field has evolved into a more contextual approach called “financial capability,” which focuses on the individual and the existing state and social institutions that financially influence an individual. The models of financial capability theorize that the financial well-being of an individual can be enhanced by developing their financial knowledge, financial skills and competencies, financial motivation and confidence, and financial socialization. When introduced at an early age, financial socialization relates well with financial learning, financial attitude and an eventual change in financial behavior (Shim et al., 2010).

Since the financial and economic systems are social constructs, it is important to assess the whole ecosystem of these constructs to understand how it affects the financial well-being of young people. The overarching framework of social constructs in modern societies is democratic citizenship. Thus, to understand, criticize and evolve the financial social construct and the well-being of individuals, we must first understand the idea of democratic citizenship.

Aim and disposition

The aim of this paper is to understand financial citizenship as an umbrella concept for financial literacy and financial capability and to identify models and variables that can represent and measure financial citizenship. This paper reviews and develops a conceptual understanding of financial citizenship and evaluates existing financial citizenship models that can be used for further research and policy making that supports building effective financial well-being programs for societies and individuals.

The paper begins by focusing on the socioeconomic importance of financial literacy and shows the relationship between financial well-being and a healthy democracy. Next, the paper will investigate the realm of “financial literate citizens” and what literacy elements are needed for good financial citizenship. The focus then turns to models of “financial citizenship” by evaluating their realms, variables, and structures, and suggests possible ways to use them in further research.

Objectives

The objectives of this paper are the following:

Discuss the relationship between financial literacy and economic well-being and show why financial citizenship is more inclusive and effective for economic well-being;

Understand the concept of financial citizenship and argue that it provides a more comprehensive and effective framework than financial literacy at addressing the goal of individual financial well-being; and

Evaluate the current models of financial citizenship.

The relationship between financial well-being and democracy

A crucial element of building a democratic society is ensuring that all members have the power to influence the social structures, processes and outcomes. Unlike corporatocracy or oligarchy in which social ideas, processes and outcomes are associated with the control of (financial) resources, social democracy promotes the participation of people in the design and decision making of social constructs and acts as a deterrent for social oppression through power and money (Lucey and Bates, 2012; Sleeter, 2008).

The research on financial literacy and capability (addressed in the previous sections) has established that financial decisions have significant impacts on the socioeconomic well-being of individuals and families through the building blocks of a democratic society. Furthermore, financial decisions have a significant sociopolitical impact, as demonstrated by numerous austerity measures across the world, public unrest and demonstrations, and government toppling, such as in Greece, Spain, Iceland, and more. This sociopolitical impact shows that educating young people on financial literacy should also be motivated by democratic principles and “good citizenship.” Other motivators for the provision of financial education include the following: valence, which is described as an individual’s perception of or importance given to the expected outcome; instrumentality, which looks at performance and its reward; and expectancy, which is the expectation of certain outcomes attached to financial education (Mandell and Klein, 2007). The importance of this is amplified by the fact that political systems change slower than financial markets. It is critical for a functional democracy to equip citizens with an understanding of financial citizenship and tools so they can adequately react to financial crises and design socioeconomic structures to avoid or solve financial problems (Remmele and Seeber, 2012).

Austerity measures were introduced after the great recession of 2007 and they were mainly implemented in Europe. Some of these measures included a reduction in employment, leading to an increase in unemployment rates across European countries such as in Latvia, Spain and Lithuania, which recorded the highest unemployment rates of 14, 12, and 13 percent, respectively. Other austerity measures include increasing taxation and reducing social spending. These measures were put in place in an effort to move towards economic recovery (Stuckler et al., 2017).

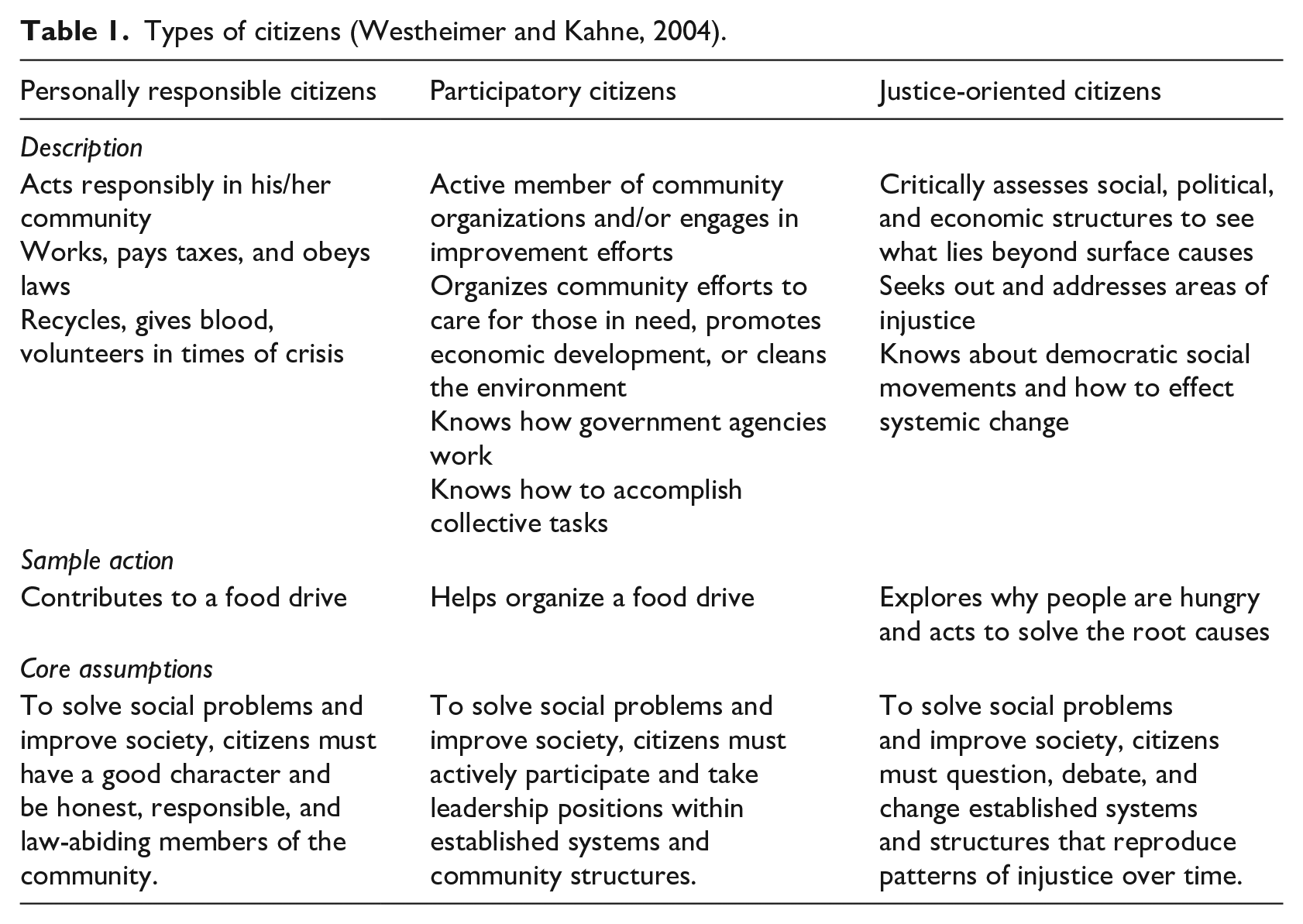

Arguably, the building blocks of a “good” democratic society are “good” citizens who are characterized by being capable of making independent arbitrary choices and acting as their own agents rather than merely being represented by political alternatives that carry predetermined socioeconomic consequences. The way young people understand a democratic society and how they interact with it as a citizen is influenced by the education they receive. Westheimer and Kahne (2004) reviewed numerous educational theories and practices for democratic citizenship and concluded that there are three conceptions of citizenship, each of which serves a particular set of roles and political implications in a society. These three conceptions are the following: i) personally responsible citizenship, ii) participatory citizenship, and iii) justice oriented citizenship. This is shown in Table 1.

Types of citizens (Westheimer and Kahne, 2004).

Justice-oriented citizens

Typically, left political oriented researchers have greater appreciation for the importance of developing critical and proactive citizenship that aims to achieve a more just and equitable society through structural changes. On the other hand, conservative oriented researchers typically consider that societal problems are a result of defects in personal characters and behaviors (Sterling et al., 2019). The aim for social justice and change, however, does not necessarily imply adopting a particular political orientation. For example, decreasing poverty is typically a claimed goal for all political parties. Instead, the focus of educating young people about citizenship should be developing their abilities to understand and activate collective change strategies that promote justice and equality in society by addressing the root causes and not the symptoms of society’s problems. Young people who become justice-oriented citizens know how to understand and influence the interplay of social, economic, and political forces. As Westheimer and Kahne (2004) put it, “if participatory citizens are organizing the food drive and personally responsible citizens are donating food, justice-oriented citizens are asking why people are hungry and acting on what they discover.” Such citizenship education would likely not stop at teaching young people how to stay out of debt and save better, but would also include teaching them about social movements and how to affect change in economic and political systems. Such systemic changes almost always involve high stakes and thus would most likely be resisted by groups in society that benefit from maintaining the status quo of socioeconomic structures. Justice-oriented citizens will have “commitment to critical and structural social analysis, to making the personal political, and to collective responsibility for action” (Westheimer and Kahne, 2004). Maitles (2001), while in China, also observed a similar aspect while attending a culture and democracy conference. While the Chinese government was keen to have young people participate in decision – making processes, the contrary was happening in Britain, where young people were described as being alienated, apathetic and not interested in politics. Single issue (such as political parties advocating for only one major public issue, which is usually controversial), social, political, and environmental components constitute citizenship, especially civic, social, and political, but this cannot be complete without economic or financial citizenship (Maitles, 2001).

Empirical evidence concludes that educating young people to be justice-oriented actually makes a considerable difference in their world view and they will consider themselves as independent agents for social change. Westheimer and Kahne (2004) conducted an experiment with US school students to measure the impact of educating them about social justice versus educating them only about public responsibility. They conducted a 2 year study of programs (educational) aimed at promoting democracy within the United States. A total of ten programs were studied over the 2 year period. A mixed methods approach where both qualitative and quantitative data were collected was utilized. The data collection included surveys, observations, interviews and documentation from program staff. The results from the study show that students who are educated to become participatory, personally responsible citizens develop a greater interest in helping others (e.g. donating) and community development (e.g. organizing charities). On the other hand, students who are educated to become justice-oriented citizens develop a higher interest and motivation in understanding the root causes of economic inequality and political systems as the route for socioeconomic change.

Given how financial injustice issues impact sociopolitical landscapes, such as the cases in Greece, Spain, Iceland, and other countries, it is logical to conclude that democracy and citizenship are closely interlinked with the financial and economic systems in a society. For example, in Greece, there was a prolonged recession, which was believed to be as a result of austerity measures taken and not directly linked to the global financial crunch. As a result, social exclusion, poverty rates and unemployment rates skyrocketed, affecting a majority of the population. With such issues affecting the Greek population, they experienced less cohesion, further affecting other spheres, including the democracy within Greece (Papanastasiou and Papatheodorou, 2018). However, contrary to this logic, educating young people on financial literacy is considered to be the personal responsibility of the consumer-citizen (Davies, 2015; Kling, 2010). Mandell and Klein (2007) surveyed the answers from young people on the question, “Which of the following do you feel is the greatest cause of serious financial difficulty in families?” The multiple choice answers given and their ratios were the following: a) bad luck, such as unexpected illness or job loss (8.6%); b) insufficient savings (9.4%); c) buying too much on credit (28.9%); d) not following a financial plan (28.9%); and e) not being able to earn enough money (24.0%). The conclusion was that young adults think that families experience financial problems due to their own mistaken financial behavior, which would have been a sound conclusion, except that the question that asked about why financial problems exist was incorrect. The question that was asked limited the choice of answers to personal responsibility or luck and did not offer a choice signifying that governing social and market structures could be a probable reason for financial difficulties within families.

The almost-global tendency to frame the issue of financial difficulties as an individual consumer-citizen behavior has been partially cemented by several studies and promotions from international organizations such as the OECD and World Bank. In addition, numerous researchers have found it more convenient (and less expensive) to borrow ready-made survey questions as assessment tools for financial literacy and its impact on young people (Davies, 2015), which likely represents a case of familiarity bias in research. It is worth mentioning, however, that one growing organization (Child and Youth Finance (CYFI), a nongovernmental organization) has introduced a counter institutional approach by researching youth financial difficulties as a citizenship issue (Cohen et al., 2013; CYFI, 2012).

Thus far, we have established that the purpose of financial literacy should be to develop young people’s abilities to become critical and proactive citizens regarding their financial status so they can tackle the financial problems of their societies at the source. We have also demonstrated that most of the current assessment tools fail to serve that purpose, but instead try to test or establish the idea that financial well-being (or the lack thereof) is a result of the personal responsibility of the consumer-citizen. The assessment tools for financial literacy have mainly been self – administered questionnaires, including pre and post assessments, which were administered mostly online but on paper as well. In a study conducted in Latvia on the suitability of tools used for the assessment of financial literacy among young people, three aspects were examined: the importance and understandability of the questions and the simplicity of the wording used in the assessment tools. From the study, it emerged that the questionnaire (assessment tools) may not be generalized globally; therefore, there is a need to customize what is most suitable for a given population to improve the reliability of the information collected (Ciemleja et al., 2014). The natural question to ask then is how we can establish an assessment/measurement model for financial literacy as a vehicle for citizenship. What are the measurable variables that we can use to understand if young adults understand financial citizenship? Before trying to define measurable variables for financial citizenship, the following section will first address a very important question: what does financial literacy for democratic citizenship involve?

What does financial literacy for democratic citizenship involve?

Using an analogy from the healthcare nutrition field, it is evident that “financial literacy” definitions assume that a person can become healthy by knowing about nutritional facts and numbers, while “financial capability” theorizes that a person can stay healthy by learning about good nutrition habits, how to practice them with confidence, and being aware of the nutritional patterns of surrounding social institutions (family and food markets). Nevertheless, what about the environment within which the food is grown? Does the ecosystem provide the necessary nutrients for everyone or only to some and not others? Are the nutrients provided by the environment polluted or healthy? Can everyone access the good nutrients they need for a healthy life? If not, why does the ecosystem act the way it does? Similarly, for young people to become “financially literate” citizens, they need more than knowledge of bonds, stocks and interest rates. To improve their well-being and that of their community, young people need to first understand the socioeconomic and political setup of their micro world, assess whether that setup serves their well-being, and understand what is keeping them from achieving financial well-being, just as they would understand what is preventing some people from accessing healthy food (Arthur, 2012; Cohen et al., 2013).

The essence of financial literacy for democracy should focus on the “problematization of financial insecurity” instead of technical solutions for what is being advocated for by other researchers and international organizations as an apolitical individual financial risk and responsibility problem (Arthur, 2016; Lusardi and Mitchell, 2014). While an understanding of personal financial management is still required, a holistic, ethical and evolutionary response to the above-mentioned problematization should endorse a critical financial literacy mindset that enables young people to tackle financial, social, and economic systems so they recognize that their economic and financial reality is a political construct, which they can choose to inherit or change (Arthur, 2016; OECD, 2012). In such approaches (problematization of financial insecurity), young people would understand the implications of one’s financial well-being within political systems that promote economic growth over individual security. They would also be able to understand that better solutions for financial difficulties could and should be pursued beyond what the current markets and laws consider possible. One important aspect is to provide age-appropriate opportunities for young people to understand the different impacts of individual versus collective policies for crucial social goods and services, such as healthcare, education, employment, retirement, food, transportation, energy, housing, and, importantly, finance (Arthur, 2016). “Without attention to such issues of equity, financial literacy education is reduced to replicating (the existing growing) inequities, and contributes to the continued marginalization of already vulnerable populations” (Pinto and Coulson, 2011).

Elements of financial literacy for democratic citizenship

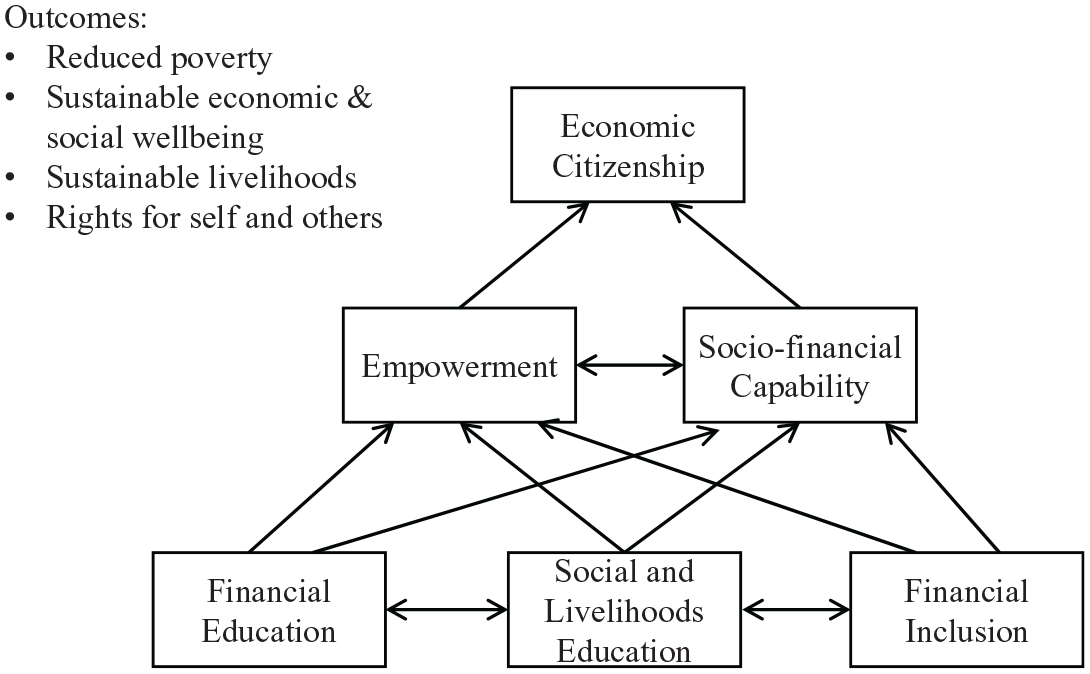

Financial literacy that aims to contribute to a democratic citizenship should enable young people to acquire the perspective of citizens, not only consumers, regarding their financial life careers. In this way, young people can understand and assess the institutional actions and legislations in a market-based system. This capability judgment goes beyond the ability to choose from alternative individual choices to the ability to evaluate political decisions and form clear ideas about the required changes to financial laws and institutions, and ultimately to the ability to mobilize such changes (Remmele and Seeber, 2012). CYFI has established a theoretical model for financial literacy that aims to educate young people on how to reduce poverty, promote sustainable socioeconomic well-being and livelihoods, and empower self and collective rights. The model is shown in Figure 1.

CYFI’s theory of change (CYFI, 2012).

At the base of the model is the goal to improve social and financial skills education, but these are not enough. According to the model, both sociofinancial capability and empowerment are needed to achieve economic citizenship. Sociofinancial capability and empowerment are acts of civil action that aim to design and implement institutions and regulations that ensure economic justice and equity (Cohen et al., 2013; CYFI, 2012).

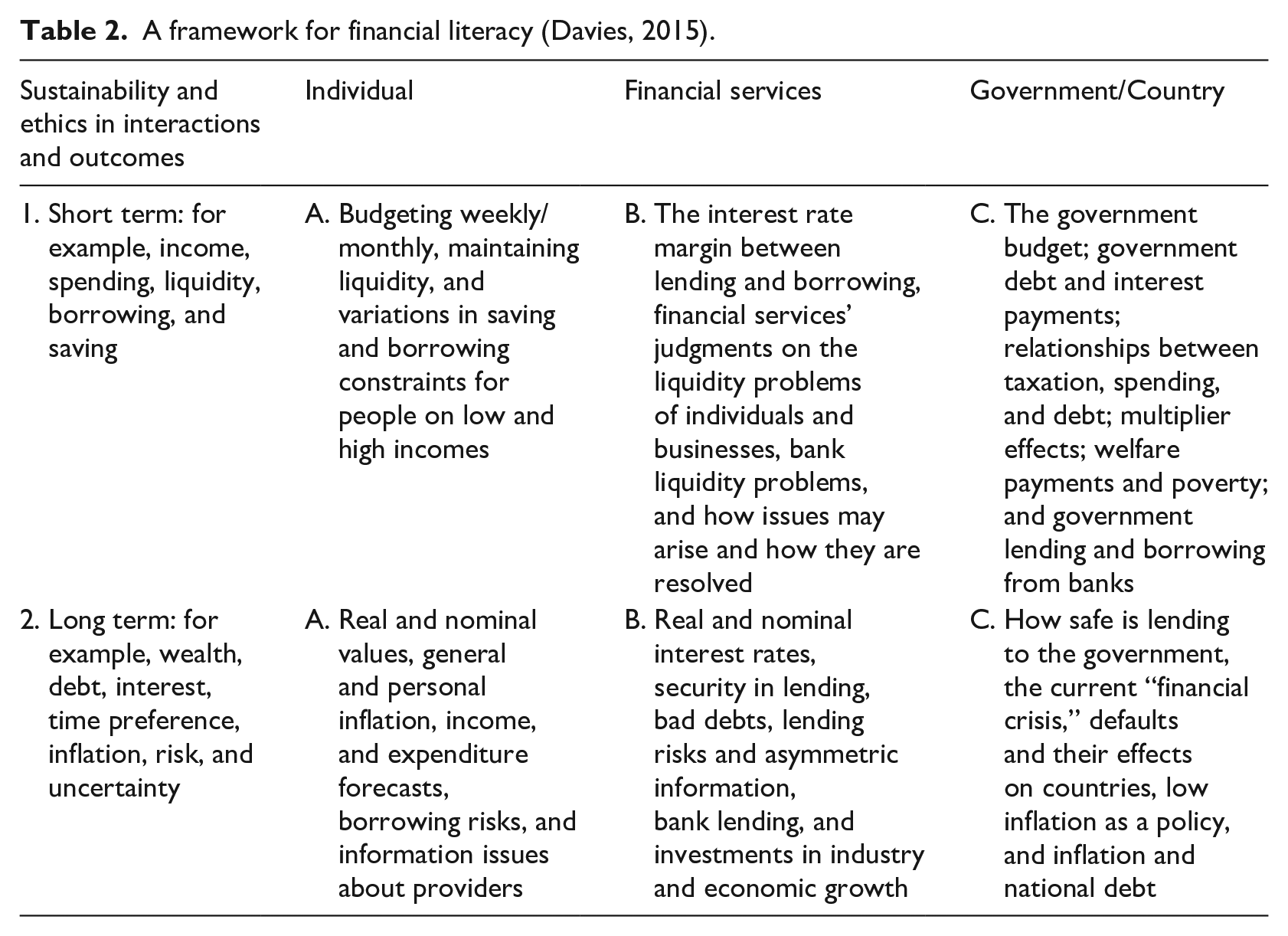

According to Davies (2015), another pillar of democracy is to educate the median voter at a young age to understand the critical financial regulations and incentives that influence governmental and financial institutions, which would automatically signal to both governments and markets that “demos” are indeed in “-kratia,” thus balancing initiatives and powers in financial markets. Davies (2015) develops an integrative framework for financial literacy with the goal of helping young people to understand their financial life from two perspectives: (1) the time frame of financial decisions: short-term vs. long-term; and (2) the impact circle of the financial decision: individual, financial institutions, and government/society. This is shown in Table 2. The aim of Davies’ model is to train young adults to understand the holistic picture of the financial decisions taken by different parties and their various implications on all parties through different time frames. The model includes elements that propel individuals towards economic citizenship. Financial literacy is aimed at enhancing the knowledge of individuals towards proper financial management and understanding the policies, regulations and availability of various financial products and services. Broadly, financial literacy is aimed at supporting individuals at managing their finances and preparing them for entrepreneurship. Without financial education and capability, young people will find it difficult to enter the labor market, either as entrepreneurs or employees.

A framework for financial literacy (Davies, 2015).

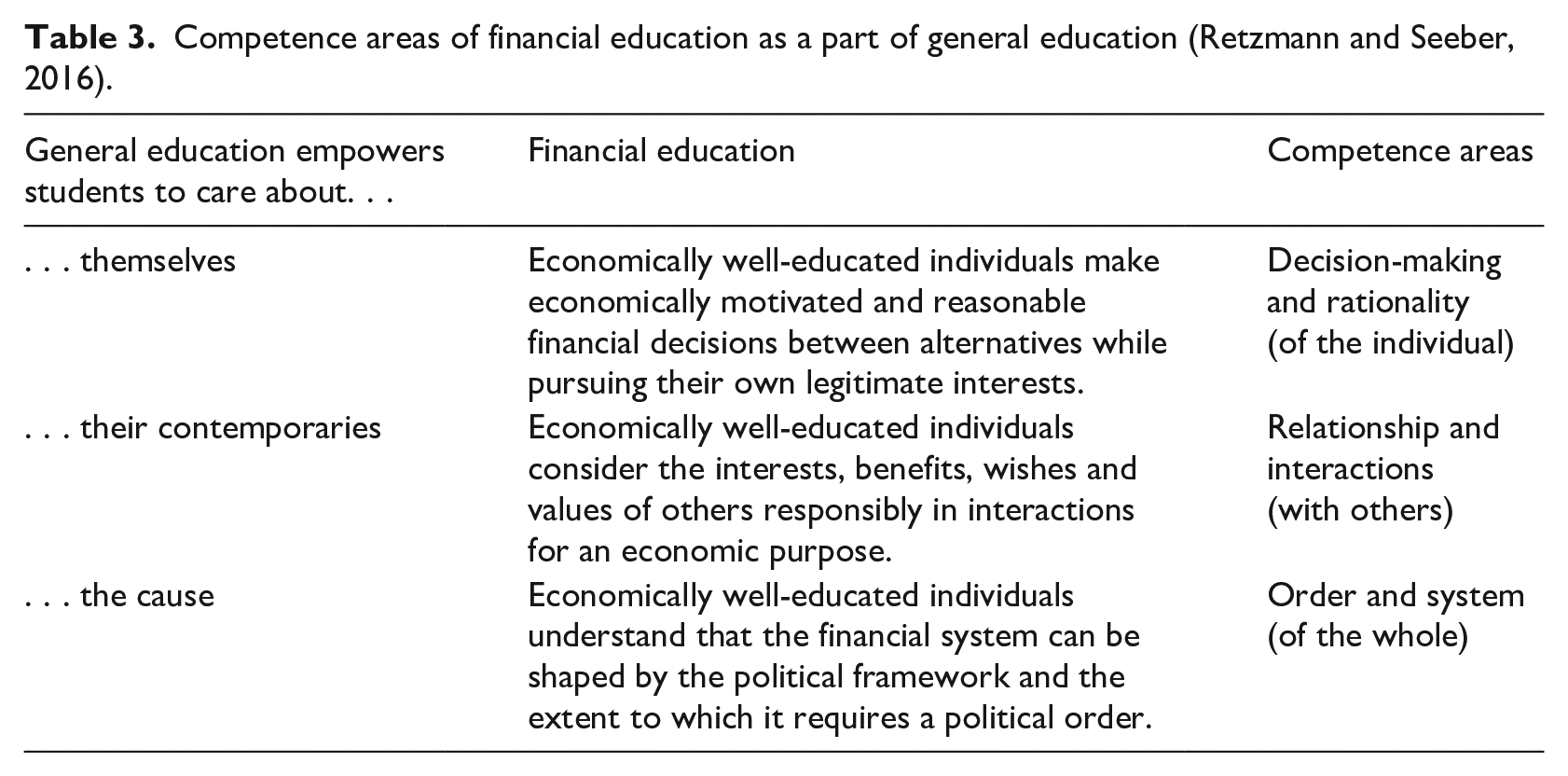

Retzmann and Seeber (2016) conceptualize an enhanced understanding of financial literacy education for citizenship, which is closely connected to a competence model for economic education that is the subject of widespread discussion in Germany and has influenced school curricula in the recent past. The model is comprised of three areas of development for economic competence, each of which is identified by three competences that one should possess to meet fundamental requirements in “economically shaped” life situations. Like many emerging studies, Retzmann and Seeber (2016) emphasize the inclusion of social impacts from financial transactions and crucial elements of financial markets and economic orders in addition to national and international financial systems.

Competence model for financial citizenship

In their model, Retzmann and Seeber (2016) focus on including declarative and practical financial education for young people, in addition to their ability to make informed and justified judgments about the entire socioeconomic system of a society. The intent of the model is to lead students to become autonomous in their personal decisions and develop domain-specific capabilities and social responsibility. The three main criteria of the model according to Retzmann and Seeber (2016) are the following:

The stated competence goals are developed on the basis of an internal capability attributed to the student,

The stated competence goals are domain-specific, and

The model distinguishes three different areas of financial competence that correspond to guiding principles valid for general education (Retzmann and Seeber, 2016).

The model defines financial competence as “the sum of an individual’s cognitive judgment, decision-making and planning abilities, their practical and technical skills for implementing decisions and plans including the use of electronic media, and their motivational, volitional and social disposition with regard to liquid funds (cash or bank money), recent and future income, and material and nonmaterial assets for themselves, as a trustee for other people, and as a social or political representative for the general public, in efficiently and responsibly generating and implementing such assets to achieve the best possible effect on the short, medium and/or long-term well-being of the people concerned.” The model identifies a “financially literate” citizen as “a person who is willing and able to judge, decide and act autonomously (self-governing), appropriately and responsibly in accordance with these transferable competences in financially shaped life situations.” As a result, it is expected that individuals who are financially literate and competent will participate more in economic policy discussions, make better choices regarding available financial services and products and invest wisely in the economies of their countries, especially those who choose to become entrepreneurs. This, in the long run, will promote financial and economic citizenship at an early age, leading to eventual cohesion and economic growth in their countries. The following Tables 3–6 describe the financial citizenship competence model of Retzmann and Seeber (2016).

Competence areas of financial education as a part of general education (Retzmann and Seeber, 2016).

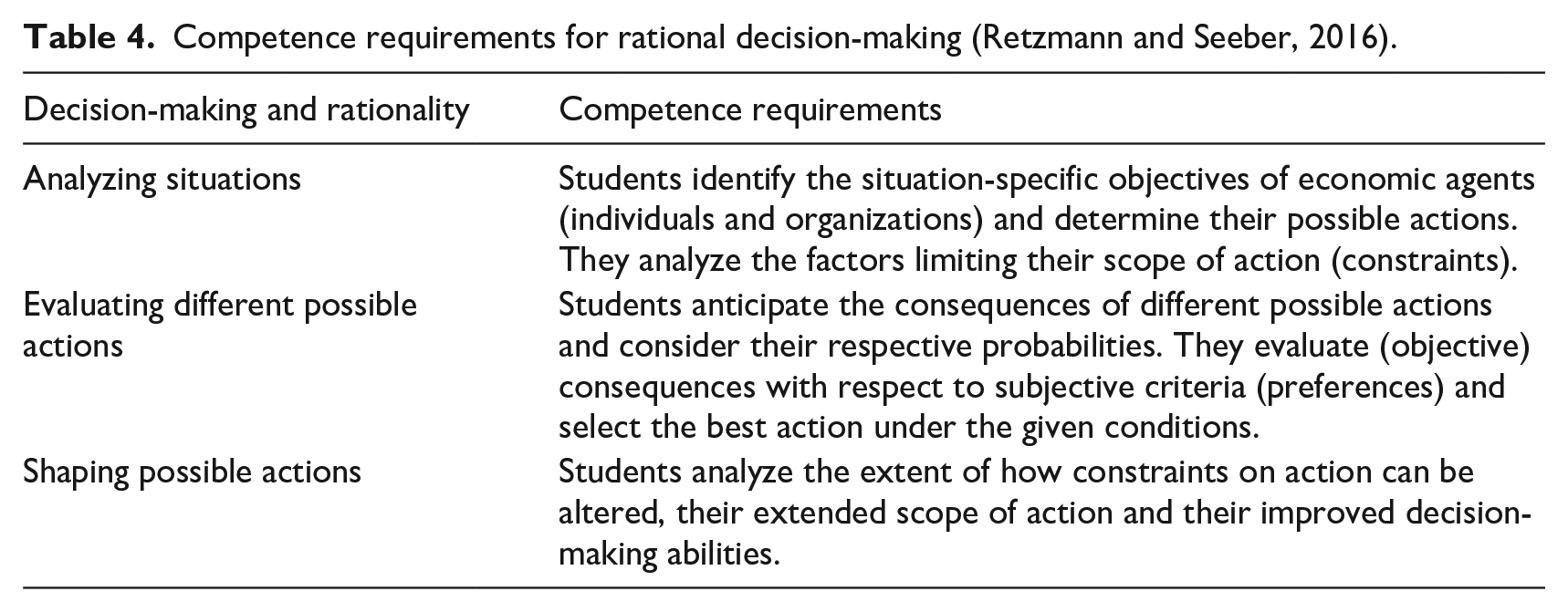

Competence requirements for rational decision-making (Retzmann and Seeber, 2016).

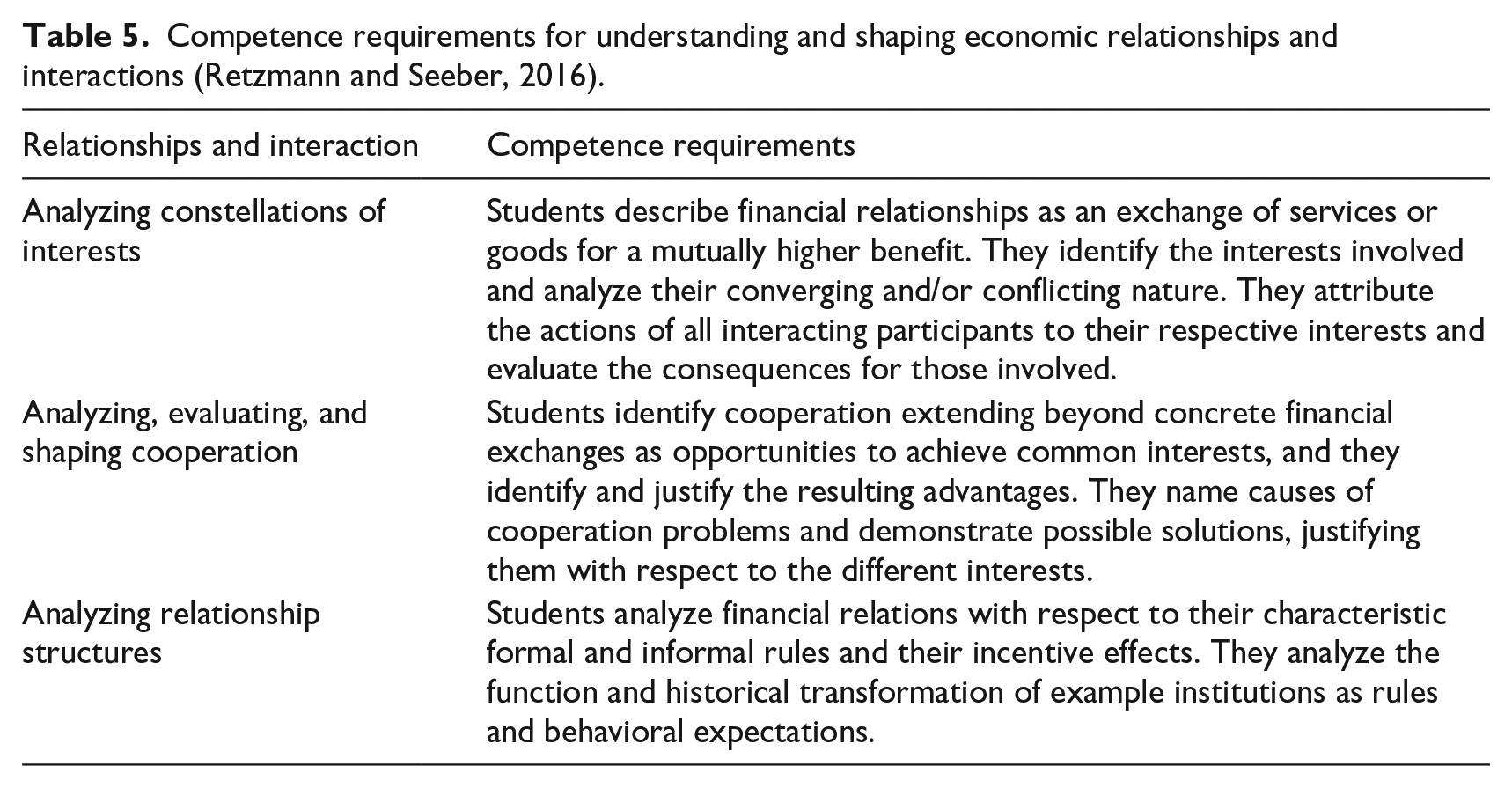

Competence requirements for understanding and shaping economic relationships and interactions (Retzmann and Seeber, 2016).

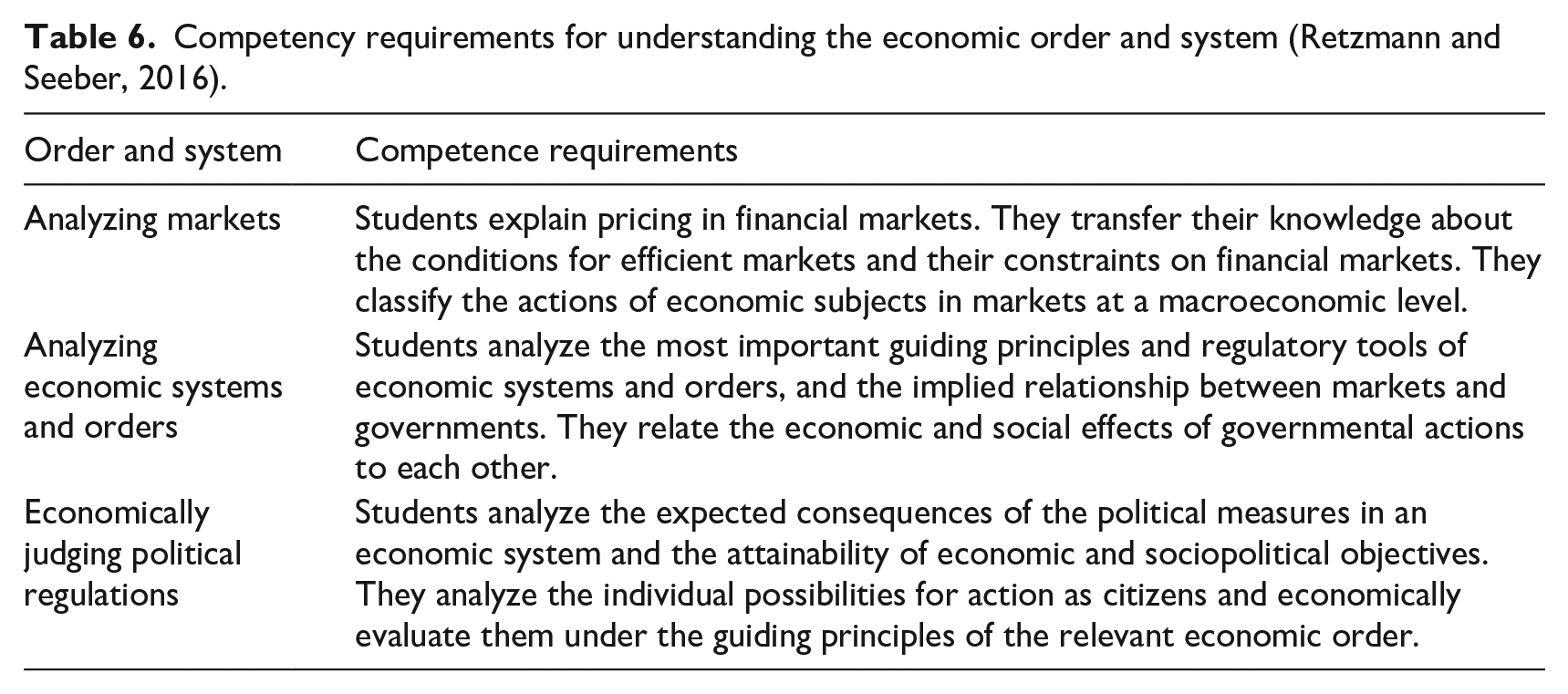

Competency requirements for understanding the economic order and system (Retzmann and Seeber, 2016).

Discussion

In summary, this paper has detailed the conceptual relationship between financial well-being, financial literacy, and financial citizenship. The idea of financial citizenship promotes the participation of people in their own economic well-being and social constructs and acts as a deterrent for social oppression through power and money (Lucey and Bates, 2012; Sleeter, 2008). Therefore, we found that it is important for young people to be educated about financial literacy and financial capabilities to sustain their own decision-making abilities, therefore promoting financial citizenship, which makes it critical for a functional democracy to have citizens who are equipped with financial citizenship understanding and tools so they can react to financial crises and design socioeconomic structures where financial problems can be avoided or treated at their source (Remmele and Seeber, 2012).

Financial citizenship entails governance and stewardship of the economy, regardless of one’s status in the society. Citizens are required to take responsibility for their financial decisions. Two components of financial citizenship emerge and are described as follows: a) citizens have the opportunity to participate in shaping how the financial system works, and b) resources are available to individuals and households to enable them to make financially responsible decisions. One major principle of financial citizenship is for citizens to have access to financial education so that they can participate in making decisions as opposed to merely giving information on available products and services. Through this principle, it is evident that financial education, literacy and competence form a major pillar in making a financial citizen. As mentioned above, the best way of enabling this to happen is by introducing financial education at an early age to promote financial literacy and competence for sound decision making (Berry and Serra, 2012).

Educating young people about this not only teaches them how to attain better individual economic well-being, but they will also learn about social movements and how to bring economic and political change. Empirical evidence concludes that educating young people to focus on being justice-oriented citizens promotes social change that can expand beyond the economic realm. Although studies in the past (such as those by the OECD and World Bank) have framed their results on financial difficulties as an individual-consumer citizen behavior issue, other more recent studies (such as those by the CYFI) have introduced the idea of the financial difficulties of young people being more of a citizenship issue. Therefore, the focus of economic well-being as a whole can be considered to be a democratic citizenship issue and should include social justice issues as well.

Financial literacy for democratic citizenship involves several factors. In order for young people to improve their economic well-being, they must first gain an understanding of the socioeconomic and political aspects of their community. Then, they need to analyze and understand the reasons that prevent them from achieving economic well-being. When viewed in this way, they have a choice to inherit or change their circumstances instead of feeling bound to existing political constructs (Arthur, 2016; OECD, 2012).

Finally, we are able to apply a theoretical model as an integrative framework for financial literacy with the goal of helping young people understand their financial options and essentially integrate them into society as well-functioning and responsible economic contributors. The theoretical model proposed by Davies (2015) focuses on two perspectives in an attempt to introduce young people to a holistic view of financial decision-making. The first perspective is on short-term versus long-term financial decision-making; and the second involves the impact that this decision will have on individuals, financial institutions, and government/society.

This is supported by Retzmann and Seeber’s (2016) competence model for financial citizenship that encourages students to develop specific capabilities in combination with social responsibility. The three main ideas of the model are the following: 1) competence goals developed according to internal capabilities determined by the student, 2) domain specific goals, and 3) three different areas of financial competence that correspond to the guiding principles valid for general education (Retzmann and Seeber, 2016).

In conclusion, financial citizenship concepts that aim to contribute to a healthy democratic society should enable young people to acquire the citizenship perspective, in addition to a rational consumer perspective, regarding their financial lives. In addition, financial citizenship is intended to reduce instances of financial exclusion within any society with the long run aim of economic equality by virtue of being better able to make sound financial decisions and participate equally in forming the policies and regulations affecting their society.

Footnotes

Declaration of conflicting interests

The author declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: The author received financial support for the research from Swedbank’s Foundation for Scientific Research.