Abstract

This study examines the capabilities of in-service secondary school teachers to provide financial education. Data were gathered from online surveys, which were spread among 300 teachers in the Flemish region of Belgium. We distinguish between perceived and actual capabilities. Our results reveal that only one third of teachers consider themselves sufficiently competent to provide financial education. Actual capabilities are assessed using a broad measure of financial literacy, which takes into account teachers’ financial knowledge, financial behaviour and financial attitudes. Our results indicate that only approximately half of teachers score sufficiently on financial knowledge and only a third attains the preferred minimum score for financial attitudes. In addition, our heterogeneity analysis shows differences in scores related to teacher characteristics such as gender, teaching discipline and teaching experience. The large share of teachers not reaching the threshold indicating adequate capabilities for providing financial education raises concern, as teacher quality is an important factor contributing to the effectiveness of financial education. Teacher professional development can play a crucial role here.

Keywords

Introduction

The ability to make well-informed financial decisions is a critical twenty-first century life skill. Due to changes in, for example, retirement provision, and the growing complexity of financial markets and products, individuals are becoming increasingly responsible for their own financial well-being (Aprea et al., 2016). These trends, combined with insights demonstrating significant room for improvement regarding the financial literacy of both adults and youth around the world (Organisation for Economic Co-operation and Development (OECD), 2016a, 2017), have led governmental bodies to develop policies aiming to raise financial literacy levels (OECD, 2016a). Most of these focus on integrating financial education in school curricula (Fox et al., 2005). 1

As interest in financial education programmes increases, so does the amount of studies discussing the effectiveness of these programmes (e.g. Asarta et al., 2014; Batty et al., 2015; Fan and Chatterjee, 2018; Xiao and O’Neill, 2016). A majority of these studies focus on evaluating student outcomes (McCormick, 2009; Sasser and Grimes, 2010). In contrast, little is known on the capabilities of the teachers participating in these programmes. However, the literature provides evidence that teacher quality plays a central role in student performance (e.g. Stronge et al., 2011) and influences student learning to a larger extent than any other objective school variable (Goldhaber, 2002; Hanushek, 2011). So despite the recognition that well-trained teachers are considered as crucial for the effectiveness of financial education (Consumer Financial Protection Bureau, 2013; Totenhagen et al., 2015; Van Campenhout et al., 2017), there is only limited evidence available on teachers’ financial literacy.

In this article, we examine whether in-service secondary school teachers are sufficiently financially literate to provide financial education. To this end, we spread online surveys among a sample of 300 teachers in Flanders, the Dutch-speaking region of Belgium. While previous research focuses either on measuring teachers’ self-perceived competences to teach financial topics (Sawatzki and Sullivan, 2017; Way and Holden, 2009) or exclusively measures teachers’ financial knowledge (Otter, 2010), we follow De Moor and Verschetze (2017) in taking a more comprehensive approach by additionally assessing teachers’ financial behaviour and attitudes. In addition, we assess which teacher characteristics influence financial literacy, and to what extent teachers perceive themselves competent to provide financial education. While De Moor and Verschetze (2017) focus on pre-service teachers (i.e. students in teacher education), we examine the financial literacy of in-service teachers. As Flanders is reforming the educational system and introducing the obligation for schools to provide financial education, it is particularly relevant to investigate whether current teachers are sufficiently financially literate, or whether professional development would be required.

Literature review

Financial literacy

Along with the increased interest in financial literacy, a multitude of definitions have been proposed. Both Remund (2010) and Huston (2010) reviewed the literature to establish common ground regarding the conceptualisation and operationalization of financial literacy. Huston (2010) concluded that, in correspondence with general literacy, financial literacy has two main dimensions: understanding (financial knowledge) and application (the appropriate use of this knowledge).

Remund (2010) evaluated different definitions used in the literature and reveals that these dimensions of understanding and application can be further categorised as follows: (a) knowledge of financial concepts, (b) the ability to communicate about these concepts, (c) the ability to manage personal finances, (d) the skills to make well-informed financial choices and (e) the confidence to plan for future financial needs. The definition developed by Programme for International Student Assessment (PISA), which is often referred to, largely reflects these five categories: Financial literacy refers to the knowledge and understanding of financial concepts and risks, and the skills, motivation and confidence to apply such knowledge and understanding in order to make effective decisions across a range of financial contexts, to improve the financial well-being of individuals and society, and to enable participation in economic life. (OECD, 2017: 50)

The fact that equating financial literacy with financial knowledge is insufficient, is also reflected in the operationalization used in recent OECD studies (e.g. OECD, 2016b). In these studies, financial literacy levels are not only assessed by items measuring financial knowledge but also by items examining financial behaviour and attitudes. This allows to determine whether a participant has a sufficient understanding of financial topics, and if this understanding consequently results in appropriate application.

The importance of financial education for young people

Many strategies striving to enhance the population’s financial literacy focus on educating youth. A major benefit of integrating financial education in school curricula is the potential to reach all students. Irrespective of their socioeconomic background, students get equal opportunities to develop financially desirable behaviour (Van Campenhout et al., 2017). Reviewing the literature on financial literacy sheds light on why financial education could be beneficial for youth in both the short- and the long-term.

The current generation of youth increasingly faces complex financial decisions, tasks and responsibilities, such as managing student loans and credit card debts (Lusardi et al., 2010). As financial mistakes at a young age may snowball into larger problems later in life, the provision of financial education at school may be a strategy to prevent youth from making these mistakes (Lusardi et al., 2010). This is confirmed by several studies demonstrating that financial education has a positive impact on financial knowledge and behaviour, even years later. Brown et al. (2016) reveal that financial literacy training at high school reduces the likelihood of having debts a decade later. This is a promising finding, especially when considering that outstanding debts are the greatest financial concern during early adulthood (Brown et al., 2016). Peng et al. (2007) examine the long-term effect of financial education on investment knowledge. Results indicate that alumni who followed a personal finance course have higher levels of investment knowledge. Finally, Xiao and O’Neill (2016) show that individuals who received financial education, scored higher on financial literacy and are more likely to demonstrate desirable financial behaviour, such as saving.

The role of teachers in financial education

High quality teachers are considered to be a prerequisite for effective financial education, and a variety of factors have been shown to contribute to this quality. First, teachers need to feel confident about their capability to provide financial education, as teacher efficacy in general has been shown to have a positive effect on aspects such as teachers’ instructional behaviour and student achievement (Haynes and Chinadle, 2007; Tschannen-Moran and Woolfolk Hoy, 2001). Second, teachers must be sufficiently financially literate themselves to provide their students with high quality financial education (De Moor and Verschetze, 2017). Finally, it seems plausible that factors such as teaching discipline and years of teaching experience may influence teachers’ (perceived) competences regarding the provision of financial education (Way and Holden, 2009).

A few studies examined teachers’ attitudes towards, and beliefs about, financial education (e.g. De Moor and Verschetze, 2017; Neill et al., 2014; Otter, 2010; Sawatzki and Sullivan, 2017; Way and Holden, 2009). While almost all teachers in these studies acknowledge the importance of financial literacy at school, only a selection consider themselves capable to teach financial topics. Sawatzki and Sullivan (2017) assess the self-perceived competences of Australian primary school teachers and show that while more than 75% consider themselves financially literate, only 50% feel confident to provide financial education. Way and Holden (2009) reveal that on average, 61% of the K-12 teachers in the United States consider themselves capable to teach financial matters. This percentage drops to 47% when more technical aspects such as risk management or insurance are concerned.

While Sawatzki and Sullivan (2017) and Way and Holden (2009) rely on measures of self-perceived competence, other researchers test teachers’ financial literacy in an objective manner. Otter (2010) reveals an average knowledge score of 37.5% on a personal finance questionnaire, indicating that teachers lack the subject matter knowledge that is required for providing financial education. Furthermore, Loibl (2008) shows that irrespective of teaching discipline (business education, family and consumer sciences, social studies or science), teachers’ average knowledge test score is lower than 50%. The approach of De Moor and Verschetze (2017) to test the financial literacy of (pre-service) teachers is innovative in two ways. First, they go beyond measuring financial knowledge by additionally examining teachers’ financial behaviour and attitudes. They argue that teachers’ adequate financial behaviour and attitudes are essential to set an example for students. Second, the authors introduce a minimum level of financial literacy that teachers should reach, that is, a particular threshold to be considered capable to provide financial education. This implies that a distinction could be made between being financially literate and being sufficiently financial literate to teach financial topics. Their results indicate that only 16% of the pre-service teachers reach the threshold of 75%.

To our knowledge, the comprehensive approach of De Moor and Verschetze (2017) has not yet been used to examine in-service teachers. This study aims to fill this gap in the literature by spreading an online survey measuring financial knowledge, behaviour and attitudes among in-service teachers in Flanders. In addition, we examine to what extent teacher characteristics influence these financial literacy scores and ask teachers to indicate their self-perceived competence to provide financial education.

Based on the discussion above, we aim to answer the following research questions:

RQ1. Do in-service secondary school teachers feel competent to teach students about financial topics?

RQ2. Are in-service secondary school teachers sufficiently financially literate to be capable to provide financial education? Which teacher characteristics influence teachers’ financial literacy levels?

Method

Research context

In this study, we focus on in-service secondary teachers in Flanders, the Dutch-speaking region of Belgium. Students in the Flemish secondary education system are usually between 12 and 18 years old and follow one out of three tracks: general secondary education, technical secondary education or vocational secondary education. The six secondary school years are divided into three stages, each lasting 2 years.

In general, secondary education students attend broad, non-specific courses which prepare them for higher education. Technical secondary education combines general education with more technical subjects. After technical secondary education, the students may practice a profession or attend a university college. This track also includes practical training. In vocational secondary education, the focus lies on learning a profession.

The research context of Flanders is of particular interest, as from school year 2019–2020 onwards, the educational system will be reformed. In particular, schools are then obliged to ensure that students eventually master a set of basic competences – among which financial literacy – that allow them to fully participate in society (Ministerie van Onderwijs en Vorming, 2017). Since no specific requirements related to financial literacy were included in the curriculum before this educational reform, the majority of current in-service secondary school teachers have not received training to provide financial education. Therefore, we assess whether in-service teachers in Flanders are capable to teach their students about financial topics or whether some form of professional development would be required.

Sample

Data for this study were collected via an online survey. The survey gathers information related to teachers’ profiles (e.g. years of teaching experience and discipline) and their capabilities to provide financial education. We initially distributed 1615 surveys, of which 490 were returned. The 300 surveys without any missing data were eventually included in the study. All in-service secondary school teachers could participate, independent of aspects such as teaching discipline. We apply sampling weights to the data to ensure our sample is representative in terms of teacher- and school-specific characteristics in Flanders.

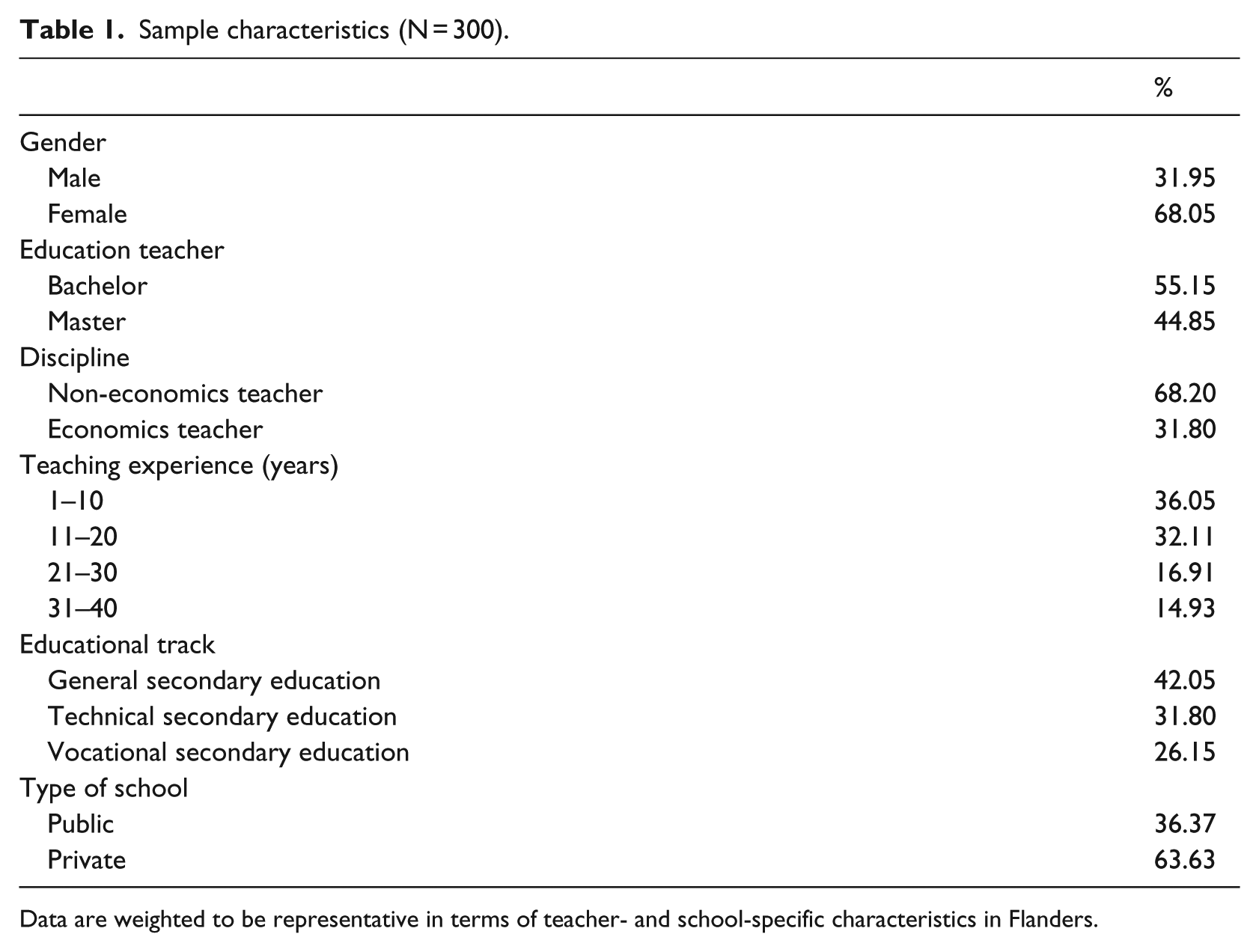

Table 1 reports the sample characteristics. Our weighted sample contained more female (68.05%) than male teachers (31.95%). Most of the teachers in our sample have a Bachelor degree (55.15%) as the highest attained level of education, the remainder a Master degree (44.85%). Since teaching discipline may influence a teacher’s financial literacy level, we made a distinction between economics (31.80%) and non-economics teachers (68.20%). The years of teaching experience may play a role in whether a teacher feels confident to teach financial topics. The majority of teachers in our sample have less than 20 years of experience (68.16%), the remainder has 21–30 years (16.91%) or 31–40 years of experience (14.93%). Teachers were also asked to indicate in which educational track they usually teach: general secondary education (42.05%), technical secondary education (31.80%) or vocational secondary education (26.15%). Finally, we asked teachers whether they work in a public (36.37%) or a private school (63.63%).

Sample characteristics (N = 300).

Data are weighted to be representative in terms of teacher- and school-specific characteristics in Flanders.

Measurements

We measure teachers’ perceived competence by asking them to respond to the question: ‘How competent do you consider yourself in providing financial education?’. Responses were indicated on a 5-point Likert-type scale ranging from 1 = totally incompetent to 5 = very competent. Teachers’ actual competence to provide financial education is captured by measuring their personal financial literacy level. To measure financial literacy, we follow the approach of the OECD (2015), which defines financial literacy as a combination of financial knowledge, financial behaviour and financial attitudes. 2 Financial knowledge is measured through nine questions covering the following themes: simple and compound interest, inflation, time-value of money, stocks, bonds, investment products, risk and return, and the relation between bond prices and interest rates. The questions originate from OECD (2015), Lusardi and Mitchell (2011) and Van Rooij et al. (2012). Every correct answer is attributed a value of one. The final score is measured as the number of correct responses to the financial knowledge questions, rescaled to 100.

Financial behaviour is measured through questions that examine how teachers deal with money in their daily lives. Four behavioural items were included considering a purchase, paying bills on time, responsible budget behaviour and shopping around before making a financial decision. The questions assessing the financial behaviour of teachers are derived from the survey of the OECD (2015) toolkit for measuring financial literacy. The response to every item is scored with a one if it reflects desirable financial behaviour, and with a zero otherwise. The financial behaviour score is measured as the sum of the number of desirable financial behaviours, rescaled to 100.

Teachers’ financial attitudes are evaluated using three statements which measure teachers’ beliefs regarding planning, saving for the future and spending. The statements are designed to capture attitudes towards the long-term, and answered using a 5-point Likert-type scale. The statements are derived from the OECD (2015). The financial attitude score is measured as the average sum of the values for the three statements, rescaled to 100.

Analysis

To determine whether or not an individual teacher is capable of providing financial education, we consult his or her scores on all financial literacy domains (financial knowledge, financial behaviour and financial attitudes). To get an overview of the financial literacy in the full sample, we compute the mean score of all teachers for each domain. In addition, we examine the scores among subsamples of teachers, created on the basis of teacher and school characteristics. In correspondence with De Moor and Verschetze (2017), we calculate the proportion of teachers scoring above the 75% (sufficient score) and 85% (excellent score) thresholds. To test whether the means of subsamples are significantly different from each other, we use a one-way analysis of variance (ANOVA) analysis. In addition, we run ordinary least squares (OLS) regression analyses to determine which teacher and school characteristics are correlated with scores on each of the financial literacy domains.

Results

Teachers’ perceived capabilities to provide financial education

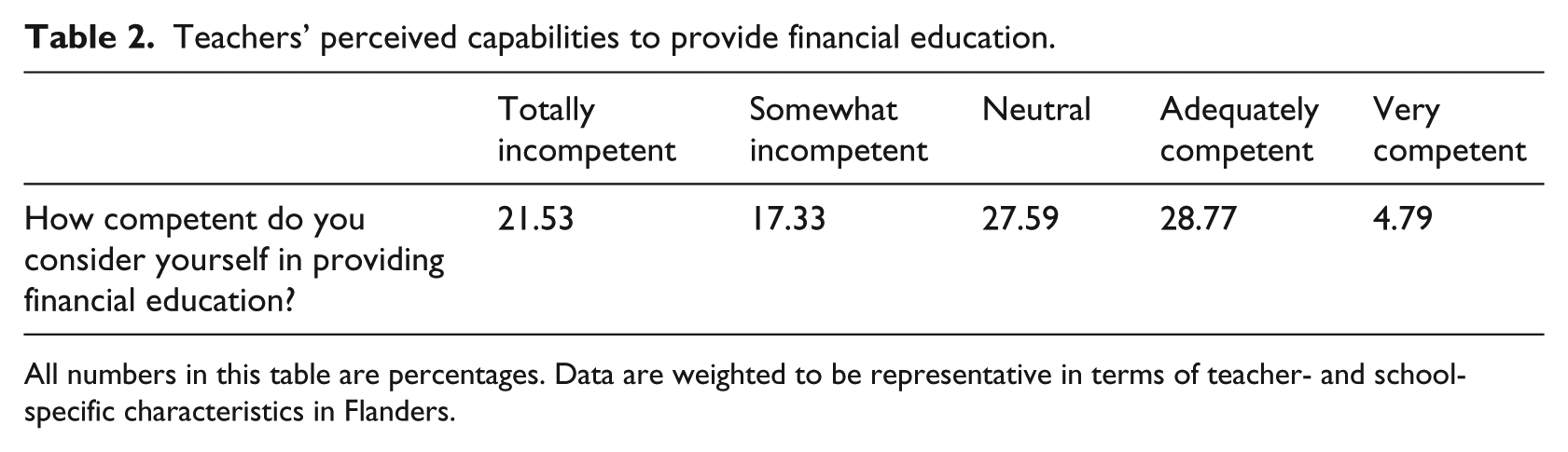

As previous studies argued that teachers’ effectiveness in providing financial education may be influenced by their perceived capability to teach financial topics (e.g. Way and Holden, 2009), we start our results section with some descriptive statistics on how teachers perceive their capability to provide financial education. Table 2 reports that only 34% of the teachers consider themselves competent enough to provide financial education.

Teachers’ perceived capabilities to provide financial education.

All numbers in this table are percentages. Data are weighted to be representative in terms of teacher- and school-specific characteristics in Flanders.

Teachers’ actual capabilities to provide financial education

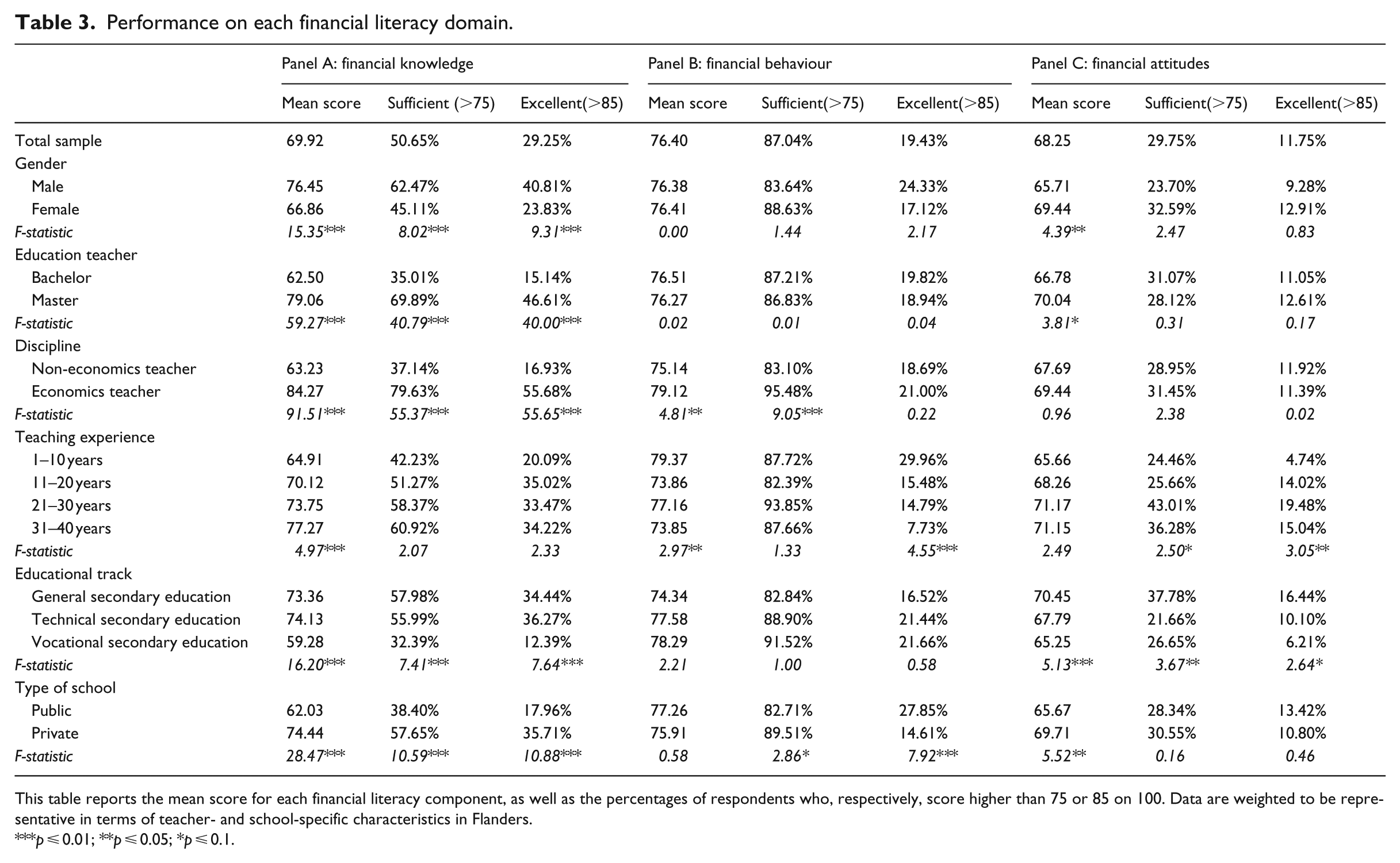

As the next step in our analysis, we investigate whether teachers score sufficiently high on financial knowledge, financial behaviour and financial attitudes to be considered capable to provide financial education. The results are presented in Table 3. Panel A reports the results on financial knowledge, Panel B those on financial behaviour and panel C those on financial attitudes. The first column of each panel presents the full sample’s average score, the second and third column present the percentage shares of respondents scoring higher than the 75% and 85% thresholds, respectively. These thresholds indicate whether a teacher has sufficient or an excellent score on financial knowledge, financial behaviour and financial attitudes. In accordance with De Moor and Verschetze (2017), we consider the 75% threshold as the minimum level for being able to teach financial topics.

Performance on each financial literacy domain.

This table reports the mean score for each financial literacy component, as well as the percentages of respondents who, respectively, score higher than 75 or 85 on 100. Data are weighted to be representative in terms of teacher- and school-specific characteristics in Flanders.

p ⩽ 0.01; **p ⩽ 0.05; *p ⩽ 0.1.

The average score of the participating teachers is approximately 70% on financial knowledge, 76% on financial behaviour and 68% on financial attitudes. This implies that the average teacher scores less than the minimum level for two out of the three financial literacy domains. In contrast to financial behaviour for which 87% of the teachers score sufficiently, only 51% of the teachers score sufficiently on financial knowledge and only 30% on financial attitudes. In addition, only a minority of teachers have excellent scores on financial knowledge (29%), financial behaviour (19%) and financial attitudes (12%).

The next rows in Table 3 report teachers’ financial literacy scores split by teachers’ gender, educational background, teaching discipline, teaching experience, educational track and type of school. We use the F-statistic from the ANOVA to test whether the differences between the subgroups are significant. The results indicate that males tend to have higher financial knowledge scores than females. The reverse is true for financial attitudes, where women tend to outperform men. The highest attained level of education significantly impacts the financial knowledge score but does not influence financial behaviour or financial attitudes. Considering teaching disciplines, we observe that on average, teachers whose main subject is related to economics score higher on financial knowledge than those who teach other subjects. The effect of discipline on financial behaviour is less outspoken, and for financial attitudes, the difference between economics and non-economics teachers is not significant. Despite the fact that economics teachers tend to perform better, the share of those with an excellent score is still relatively small: 56% of the teachers score excellent on financial knowledge, 21% on financial behaviour and 11% on financial attitudes. Teaching experience also seems to have a positive effect on financial knowledge. For the two other financial literacy components, the relation is less clear-cut. We further notice a difference between the average financial knowledge score of teachers in general or technical education and those teaching in vocational education. The last group of teachers scored significantly lower than the other two groups. Regarding the type of school, we observe that teachers in private schools have higher average scores on financial knowledge and financial attitudes than teachers in public schools.

Teachers’ characteristics influencing financial literacy

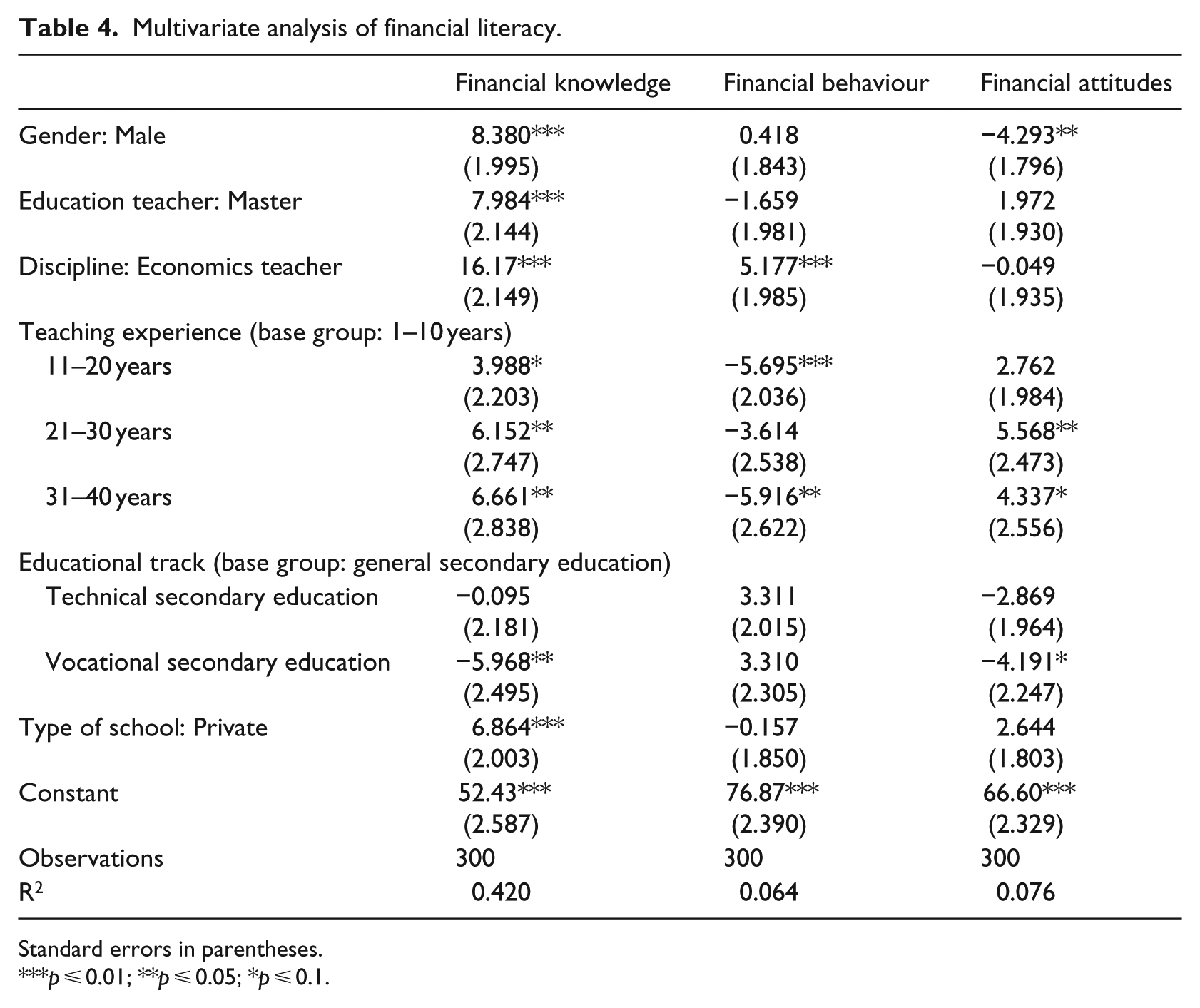

Finally, we examine whether the influence of the teacher (and school) characteristics on the three financial literacy scores remains significant after simultaneously controlling for all other variables. Table 4 therefore presents the results of the OLS regressions with the scores on each financial literacy component as the outcome variables, and gender, educational background, discipline, teaching experience, educational track, and type of school as the predictors. 3 We find that gender differences are only statistically significant in the knowledge and attitudes components: compared with their female colleagues, male teachers score, on average, 8.38 points more on knowledge and 4.29 points less on attitudes. With regard to the educational level of teachers, findings indicate that, ceteris paribus, a Master degree results in a knowledge score that is 7.98 points higher. Regarding the disciplines of teachers, we find that economics teachers score, on average, 16.17 points higher on knowledge than non-economics teachers. Moreover, being an economics teacher has a positive influence on financial behaviour: economics teachers score, ceteris paribus, 5.18 points higher than non-economics teachers. With respect to years of teaching experience, we notice that the knowledge score tends to increase with experience upto 30 years. For financial behaviour, we find some evidence that the least experienced teachers have the highest scores. The financial attitude score is highest for teachers having 21 to 30 years of experience. We also find that teachers in vocational education, on average, score significantly lower than teachers whose main teaching responsibilities are situated in general secondary education (5.97 points lower on knowledge and 4.19 on financial attitudes). Finally, we observe some differences in teachers’ financial knowledge according to school type. Teachers working in private schools seem to be more financial knowledgeable compared with those active in public education (6.86 points higher).

Multivariate analysis of financial literacy.

Standard errors in parentheses.

p ⩽ 0.01; **p ⩽ 0.05; *p ⩽ 0.1.

Discussion and conclusion

In this article, we examine whether in-service secondary school teachers in Flanders are well prepared to provide financial education. Our results reveal that only approximately one third of the teachers perceive themselves competent enough to provide financial education. Considering their actual capabilities, we notice that approximately half of the teachers reach the minimum threshold that indicates sufficient financial knowledge for providing financial education, and that only one third show the financial attitudes considered as adequate. Flemish teachers have more favourable scores in the domain of financial behaviour, with almost 4 out of 5 teachers reaching the preferred minimum. The results additionally indicate heterogeneous effects. In particular, the financial knowledge score tends to be higher for teachers who are male, are higher educated, have more teaching experience and work on private schools. Teacher characteristics seem to be less influential in the financial behaviour and financial attitudes domain. Most important to note is that economics teachers generally perform better on financial behaviour and that female teachers tend to score better on financial attitudes.

With financial education gradually becoming part of school curricula worldwide, it is problematic that teachers’ perceived and actual competences to provide financial education are lacking. Since teacher quality is one of the most important determinants of effective financial education (e.g. Van Campenhout et al., 2017), incapable teachers reduce the likelihood that financial education programmes become successful. Therefore, our conclusion implies a need for teacher professional development (TPD). The aim of TPD initiatives is to positively impact the quality of teachers such that their teaching practices are changed and student learning is enhanced (Collinson et al., 2009; Desimone, 2009).

Previous studies demonstrate the feasibility of TPD within the financial literacy context. Many teachers seem to be willing to engage in TPD initiatives (Neill et al., 2014; Sawatzki and Sullivan, 2017). Furthermore, even short initiatives can have a positive impact on student performance, which implies cost effectiveness (Swinton et al., 2007). However, while a significant number of studies evaluating financial education programmes integrate some form of TPD (e.g. Asarta et al., 2014; Batty et al., 2015), these studies rarely assess its impact separately. As a result, it remains unclear how TPD initiatives should be shaped to optimise its potentially beneficial effects (Compen et al., 2019). Considering that financial education is often integrated in school curricula nationwide (OECD, 2016a), future research is particularly recommended to evaluate TPD forms that allow for large-scale implementation, such as online TPD (Dede et al., 2009).

A few limitations of our study are noteworthy. First, as the participating teachers responded to an open call, our sample is unlikely to be free from selection bias. Potentially, mainly teachers with a particular interest in financial education filled in the survey. As a result, we are unable to claim that our sample is representative for the entire teacher population in Flanders. Second, while the survey results provide us with relevant insights regarding the financial literacy levels of teachers, it would have been informative to gain a deeper understanding of the exact needs of teachers that should be fulfilled to become and feel capable to teach about financial topics. A suggestion for future research is therefore to collect qualitative data that could be useful when designing TPD.

Footnotes

Appendix 1

Appendix 2

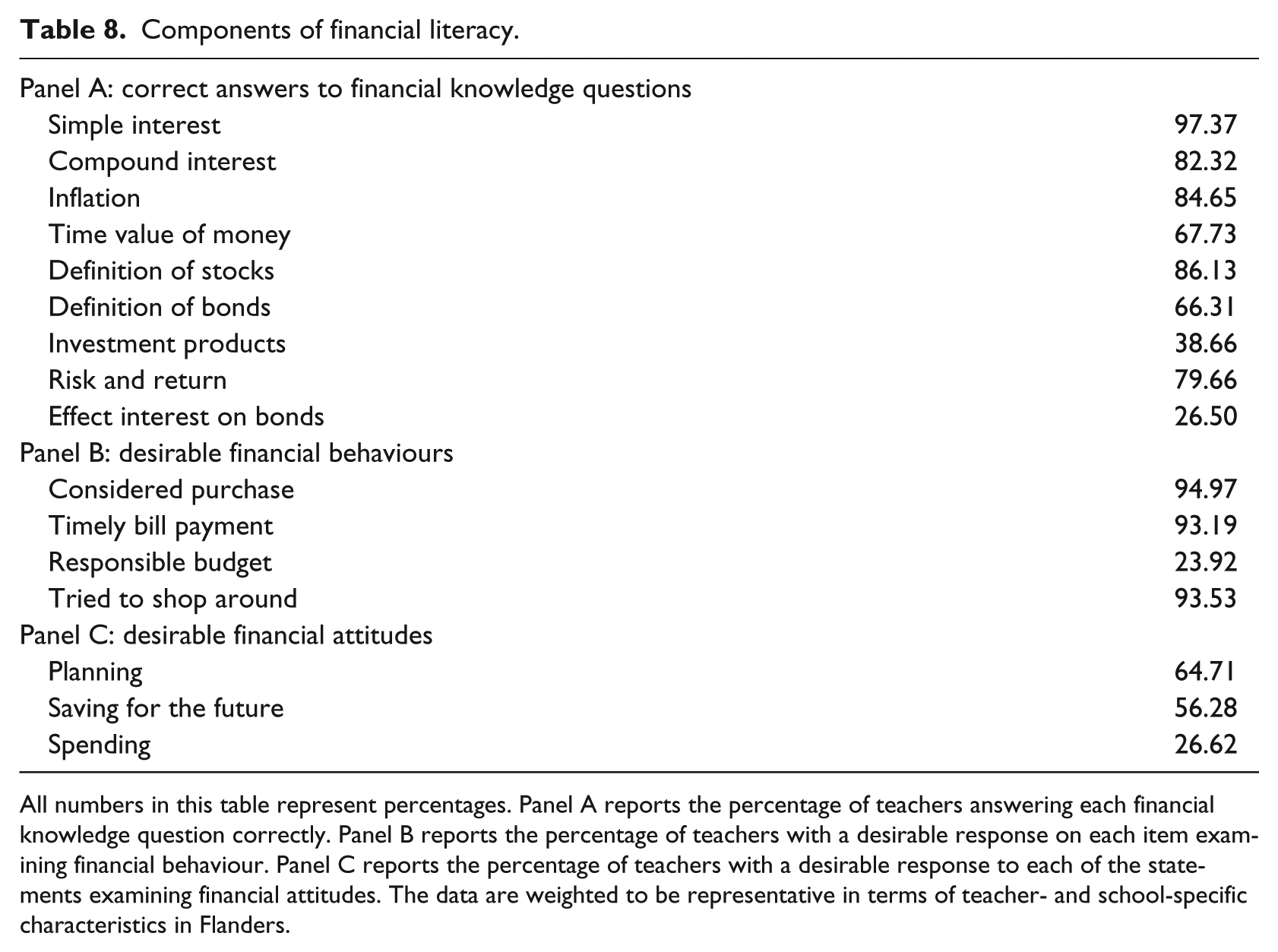

Components of financial literacy.

| Panel A: correct answers to financial knowledge questions | |

| Simple interest | 97.37 |

| Compound interest | 82.32 |

| Inflation | 84.65 |

| Time value of money | 67.73 |

| Definition of stocks | 86.13 |

| Definition of bonds | 66.31 |

| Investment products | 38.66 |

| Risk and return | 79.66 |

| Effect interest on bonds | 26.50 |

| Panel B: desirable financial behaviours | |

| Considered purchase | 94.97 |

| Timely bill payment | 93.19 |

| Responsible budget | 23.92 |

| Tried to shop around | 93.53 |

| Panel C: desirable financial attitudes | |

| Planning | 64.71 |

| Saving for the future | 56.28 |

| Spending | 26.62 |

All numbers in this table represent percentages. Panel A reports the percentage of teachers answering each financial knowledge question correctly. Panel B reports the percentage of teachers with a desirable response on each item examining financial behaviour. Panel C reports the percentage of teachers with a desirable response to each of the statements examining financial attitudes. The data are weighted to be representative in terms of teacher- and school-specific characteristics in Flanders.

Acknowledgements

The authors would like to thank Evelyn Bijnens and Geert Van Campenhout for their help to contact the participants and proofreading the survey. For insightful comments and suggestions, we thank Vanessa Naegels.

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by Wikifin.be, the financial literacy programme of the Financial Services and Markets Authority (FSMA) and by the Research Foundation Flanders (FWO) through the programme ‘Financial Literacy @ School’ (Grant no: S000617N).