Abstract

Financial education has been criticised for its limited effect on behaviour. To explore ways of improving behaviour in managing personal finances, interpretive methodology and an intervention were used in five financial education courses in Estonia. It was hypothesised that applying behavioural insights into the design of financial education helps the participants to improve their financial behaviours. The intervention employed goal setting, partitioning, commitment to achieving the goal, feedback, deadlines, peer pressure and advice. These five case studies reveal that promotional goals are more motivating than prevention oriented goals, peer effects can be utilised only in homogeneous groups and that partitioning needs to be incentivised. The results provide support for the hypothesis; furthermore, positive changes in behaviour were noted also 6 months after the end of the course. However, the intervention and its elements would benefit from further testing.

Keywords

Introduction

Financial literacy is a life skill necessary for improving the financial well-being of the individual, the household and society at large. In more than 50 countries, national strategies for financial education have been launched (OECD, 2015). Yet, there is not much evidence of successful interventions for improving behaviour in managing personal finances for the longer term (Atkinson et al., 2015). Financial education programmes have been found to improve knowledge (Kaiser and Menkhoff, 2017) but to have a ‘positive but modest’ (De Meza et al., 2008; Miller et al., 2015) impact on behaviour, if any at all (Atkinson et al., 2015; Fernandes et al., 2014; Mandell and Klein, 2009). Therefore, more effective tools are needed for improving behaviours and increasing financial well-being.

It may be that individuals lack confidence and motivation instead of knowledge. The importance of these is highlighted in the definition of financial literacy used in the Programme for International Student Assessment (PISA) test: Financial literacy is knowledge and understanding of financial concepts and risks, and the skills, motivation and confidence to apply such knowledge and understanding in order to make effective decisions across a range of financial contexts, to improve the financial well-being of individuals and society, and to enable participation in economic life. (OECD, 2013: 144)

Another possible explanation for the disparity between knowledge and actual behaviour are the heuristics and biases described by behavioural scientists (Benartzi and Thaler, 2007; Ranyard and Ferreira, 2017; Thaler and Sunstein, 2009). Procrastination, overconfidence and optimism (De Meza et al., 2008; Kahneman and Riepe, 1998; O’Donoghue and Rabin, 1999) may be the reasons for a lack of long-term planning in personal finances, rather than a lack of knowledge. Furthermore, Newall and Parker (2018) find negative correlation between financial knowledge and investment behaviour. Willis (2008) believes that ‘people are financially illiterate not because they are stupid, but because they have better things to do with their time’ (p. 202).

In order to find ways to increase the effectiveness of financial education, I used interpretive case study research in five groups as part of a financial education programme. The interpretive approach is arguably better than positivistic methodology for understanding consumers’ financial behaviours (McGregor and Murnane, 2010). Instead of objectively observable causes of behaviour, understanding of participants’ world is sought for. Participants’ worlds were observed, and an intervention was tested in groups of students and adult learners in Estonia. Here the gap between knowledge and behaviour has been found to be the largest. In international comparison, Estonian students and adults rank third in the world in financial knowledge but are among the bottom ten in behaviour (OECD, 2014b, 2016).

The intervention included goal setting, commitment to the goal, partitioning, deadlines, feedback, peer pressure and advice. Each of these has been found to have positive impact on managing personal finances (Ashraf et al., 2006; Carpena et al., 2017; Ferreira, 2011; Hilgert et al., 2003; O’Donoghue and Rabin, 1998; Thaler and Sunstein, 2009), but the full set has not been included in the design of a financial education programme before. The outcomes of the intervention were measured at the end of the course, and the longer term changes in behaviour were assessed in follow-up surveys.

In the next section, literature on the effectiveness of financial education and applying behavioural insights into it are briefly analysed. Next, methodology and methods, samples and results of the five case studies are explained. The article concludes with a discussion of the results and explanation of the limitations of the study.

Financial education and sound behaviour in managing personal finances

Understanding the basics of finance is required to make sound choices among a great variety of financial services. Both traditional and ‘new’ financial services, such as peer-to-peer lending, allow substantial financial decisions to be made over the Internet without any human interaction. On one hand, this improves financial inclusion. On the other hand, this may lead to harmful decisions due to a lack of understanding of what is being purchased.

The relation between knowledge and behaviour is complicated. High level of financial knowledge can be the reason for prudent behaviour in managing personal finances, but it can also be the other way around – knowledge can be acquired in the process of making sound financial decisions (Hilgert et al., 2003; Monticone, 2010; Riitsalu, 2018). It is supported by the findings of Happ et al. (2018); in their study, ‘personal experience’ was frequently named to be the main source of financial knowledge. Fernandes et al. (2014) state in their meta-analysis of relevant literature that researchers ‘have drawn sharply different conclusions about the effects of financial literacy and financial education’ (p. 1862). Therefore, the dominating approach to improving financial literacy – by provision of knowledge with the expectation of it leading to sound behaviours – may be misleading. However, financial knowledge has been found to correlate with saving and investing behaviour (Guiso and Jappelli, 2008; Lusardi et al., 2017; Lusardi and Mitchell, 2007; Van Rooij et al., 2011). Hilgert et al. (2003) find knowledge about credit, saving and investment to be correlated with better credit management, saving and investment practices, respectively, but they also note it is not enough to prove the causality or the causality may be reversed.

There is a growing body of research on the limited effects of financial education (Altman, 2012; Atkinson et al., 2015; Fernandes et al., 2014; Willis, 2008). It has been found to be effective in certain groups and on influencing certain behaviours (Bernheim and Garrett, 2003; Clark et al., 2017; Lusardi, 2004; Lusardi and Mitchell, 2007; O’Prey and Shephard, 2014), but it is not universally useful for improving the management of personal finances. Brief one-time financial education courses have limited effect on financial behaviours, if any at all (Lusardi and Mitchell, 2007), unless action has to be taken as part of the course (Clark et al., 2017). Miller et al. (2015) find controversial evidence of the effects of improved financial knowledge on behaviours in their analysis of 188 papers and state that ‘financial education can impact some financial behaviours, including savings and record keeping’ (p. 26). They did not find any significant effects of the delivery methods, types or length of financial education programmes. Kaiser and Menkhoff (2017) argue in their analysis of 115 studies that financial education significantly improves financial behaviours ‘but it is crucial in which way financial education is implemented’ (p. 2). Amagir et al. (2018) conclude in their recent review of financial education research that there is a ‘shift from a traditional subject-matter-based approach to a skills-based approach, in which the student learns the skills by doing, as opposed to the “chalk and talk” model in which the student is often passive’ (p. 71). This study is a clear evidence of such a shift.

The perfect financial education programme is yet to be designed. Mandell and Klein (2009) show in their study that an ‘excellent personal finance course’ does not significantly influence the behaviour of high school students (p. 21). De Meza et al. (2008) verify that ‘financial education is not likely to have major lasting effects on knowledge and especially on behaviour. Psychology may be the main driver of what people actually do’ (p. 2). Fernandes et al. (2014) find that ‘the partial effects of financial literacy diminish dramatically when one controls for psychological traits that have been omitted in prior research’ (p. 1861). Farrell et al. (2016) show that self-efficacy can have more effect on saving behaviour than financial knowledge. Pinjisakikool (2017) reveals that people with internal locus of control tend to be on higher financial literacy level. Therefore, it may be that the individual characteristics explain financial behaviours more than their knowledge of relevant topics. As suggested by Carpena et al. (2017), financial education programmes need to be personalised for having significant behavioural outcomes.

These findings emphasise the need for finding effective tools for improving the design of financial education initiatives. Drexler et al. (2014) tested different ways of providing financial education in randomised controlled trials and found that the effectiveness depends largely on how the financial education programme is designed. Simpler training concentrating on basic rules of thumb proved to be better than the more traditional financial education course covering the conditions of financial services in greater depth. Similarly, Kaiser and Menkhoff (2018) find that teaching methods have strong impact on the behavioural outcomes. In their study, courses that employed active learning were found to have positive effects, in contrast to traditional lecturing. Peeters et al. (2018) emphasise the need to incorporate practical exercises in financial education training for practicing the newly acquired skills. Amagir et al. (2018) recommend to use ‘experiential learning’ for increasing the effectiveness of financial education. In this study, an intervention is tested as a possible tool for improving the behavioural outcomes of financial education.

Behavioural insights applied to financial education

Research on economic psychology and behavioural economics provides tools that have been found to have a positive impact on behaviour. As Altman (2012) says, the bounded rationality approach is better for improving financial decision-making than the conventional approach to increasing financial literacy. In recent years, numerous randomised controlled trials have been conducted to improve spending, saving and debt behaviours. For example, in the United States, text messages asking to make a saving decision prior to tax return doubled the saving rate compared to the control group (Center for Advanced Hindsight, 2018). In Europe, pop-up warnings and framing proved useful for decreasing unnecessary online purchases (Meccariello and Näsgarde, 2018). However, these behaviour changes tend to be minor, often merely a few percentage points increase, and such interventions may have little long-term effects. Such nudges have been criticised for small impact and questionable generalisability, but their ratio of impact to cost is often more favourable than of traditional interventions (Benartzi et al., 2017).

Goal setting (Carpena et al., 2017), partitioning (Van Raaij, 2016), deadlines, commitment (Ashraf et al., 2006) and reminders (Karlan et al., 2010) have been used for improving saving behaviour. Carpena et al. (2017) found class-room based financial education to improve attitudes and awareness, but to have no impact on behaviour. Similarly to this study, they tested adding goal-setting treatment to the financial education programme and found it to lead to improved behavioural outcomes. Those who had set a goal as part of the financial education programme, were 6.3% more likely to save in a bank than those who had attended the course without the goal-setting treatment. However, they found such improvements only in simple short-term behaviours, and highlighted the importance of personalisation of financial education and counselling. In this study, goal setting is combined with advice from peers as a form of personalised financial counselling.

Higgins (1998) distinguishes between promotional and prevention goals – two separate systems of self-regulation. Promotional goals are used in approach strategies, such as saving for buying a new digital device; prevention goals are set for avoiding negative future scenarios, such as falling into debt or losing one’s home (Zhou and Pham, 2004). Vlaev and Elliott (2017) suggest using ‘evaluation and goal setting’ as a motivational technique for improving financial behaviours (p. 197). They describe its three steps; setting a personally relevant goal, imagining the positive outcome of achieving that, and identifying the most critical obstacles in achieving it.

Peer effects are useful in promoting financial literacy (Bursztyn et al., 2014; Yoong, 2010), and talking about money matters in the family has a positive relation with financial literacy in the PISA test (Riitsalu and Põder, 2016). Personal relevance, social norms and peer effects have positive impacts on sound behaviours (Dolan et al., 2012; Ferreira, 2011; Peeters et al., 2018). All of these tools were included in the design of the intervention analysed in this study; these have not been combined into one intervention for improving financial behaviours before. The design of the intervention is explained in the following sections.

Methodology and methods

The large gap between knowledge and behaviour observed in Estonia (OECD, 2016) shows that financial education programmes need to be designed more carefully to have influence on actual behaviour, instead of improving knowledge only. I hypothesised that applying behavioural insights into financial education helps to bridge that gap.

For being able to change behaviours, deeper understanding of individuals’ worlds is needed. According to McGregor and Murnane (2010), interpretive approach enables to understand consumer financial behaviour better than positivist methodology. The first intends to understand these behaviours, the last ‘aspires to causal explanation’ (Lutz, 1989). I decided to use interpretive approach, as it aims to understand what is happening, how people feel in that situation, how these feelings came to be and how these meanings affect their lives (McGregor and Murnane, 2010). The small groups of participants enabled to observe their meanings over several months, and the discussions allowed to understand their behaviour better than positive methodology would have permitted.

In the interpretive approach, the researcher’s interpretations ‘play a key role’ (Andrade, 2009: 43). I have designed, delivered and analysed the results of each of the cases, hence have been in the centre of the study. In positivist approach, such subjectivism would be seen as a major limitation of the study, but in interpretive research, the inquirer is in the role of a ‘passionate participant’ (Klein and Myers, 1999), rather than an ‘objective mirror’ (Guba and Lincoln, 1994).

A case study method was adopted to conduct this exploratory study. Five case studies consisted of a financial education course and an intervention combined with pre- and post-assessment. Prior to teaching the course and conducting the experiment, participants’ financial knowledge and behaviours were assessed. The intervention used behavioural insights and consisted of goal setting, commitment, partitioning, deadlines, feedback, peer pressure and advice. For increasing internal validity of the study, the intervention was carried out as uniformly as possible in all five cases. I gave the instructions in the beginning of the course, and the list of possible goals was similar in all groups. In the last two cases, the duration of the course was shorter; therefore, some of the mechanisms of the intervention could not be employed in full. The behavioural outcomes of the interventions were assessed in the end of the course and a follow-up survey was conducted for measuring longer term changes.

I have used quantitative and qualitative methods for collecting and analysing the data. The pre-assessment used a questionnaire, the results of it were analysed quantitatively. During the course, observation and interviews were used for understanding the participants’ experiences, attitudes and progress towards the goal. In the end of the financial education programme, achievement of the goals was calculated using content analysis of participants’ reports, and quantitative analysis of the follow-up survey data. The more detailed explanation of the intervention and assessment methods is provided in the description of each of the cases.

Consent to use the data anonymously has been received from the participants. As the samples were relatively small, reflecting any personal details of the sources of the quotes would have endangered their anonymity; therefore, no details are provided. The main disadvantage of these interpretive case studies is that the results have limited external validity. As participants were self-selected, they may be more aware of their behavioural hurdles than an average consumer is, and it was not possible to randomly assign some of them into a control group. The reasons for that are explained in the last section of the article. However, the aim of the research was to explore the applicability of behavioural insights into the design of financial education course, rather than to prove the effectiveness of this particular intervention or to ensure the generalisability of the results.

Sample, data and results

The first three cases were conducted with university students, the fourth with commuters, and the fifth group consisted of early-career entrepreneurs. In all five cases, pre- and post-assessment was used, combined with an intervention. All stages of the study, including the follow-up survey, were completed by 98 individuals, roughly half of the total number of participants of the five financial education courses. Although the sample is small compared to most of the published studies, a hundred students out of a million Estonians (the population of Estonia is 1.3 million) is not less than a thousand students of three hundred million Americans (the population of the United States of America is 327 million, United States Census Bureau, 2018).

The first three case studies are based on a financial education course consisting of seven lectures over 4 months. In the first lecture, the participants’ knowledge, attitudes (see Appendix 2 of Supplementary material) and behaviour were measured. In the next class, an assignment was given to them; its outcomes were measured at the end of the course, and a follow-up survey was conducted 6 months later. The fourth case used a one-time financial education course for adult learners and a follow-up survey conducted 5 weeks later. The last case is based on a programme for early-stage entrepreneurs, consisting of two training sessions over 3 weeks. These groups enabled testing the approach in financial education courses with varying length and for different target groups.

Cases 1, 2 and 3: Financial education course at the University of Tartu in 2014, 2015 and 2017

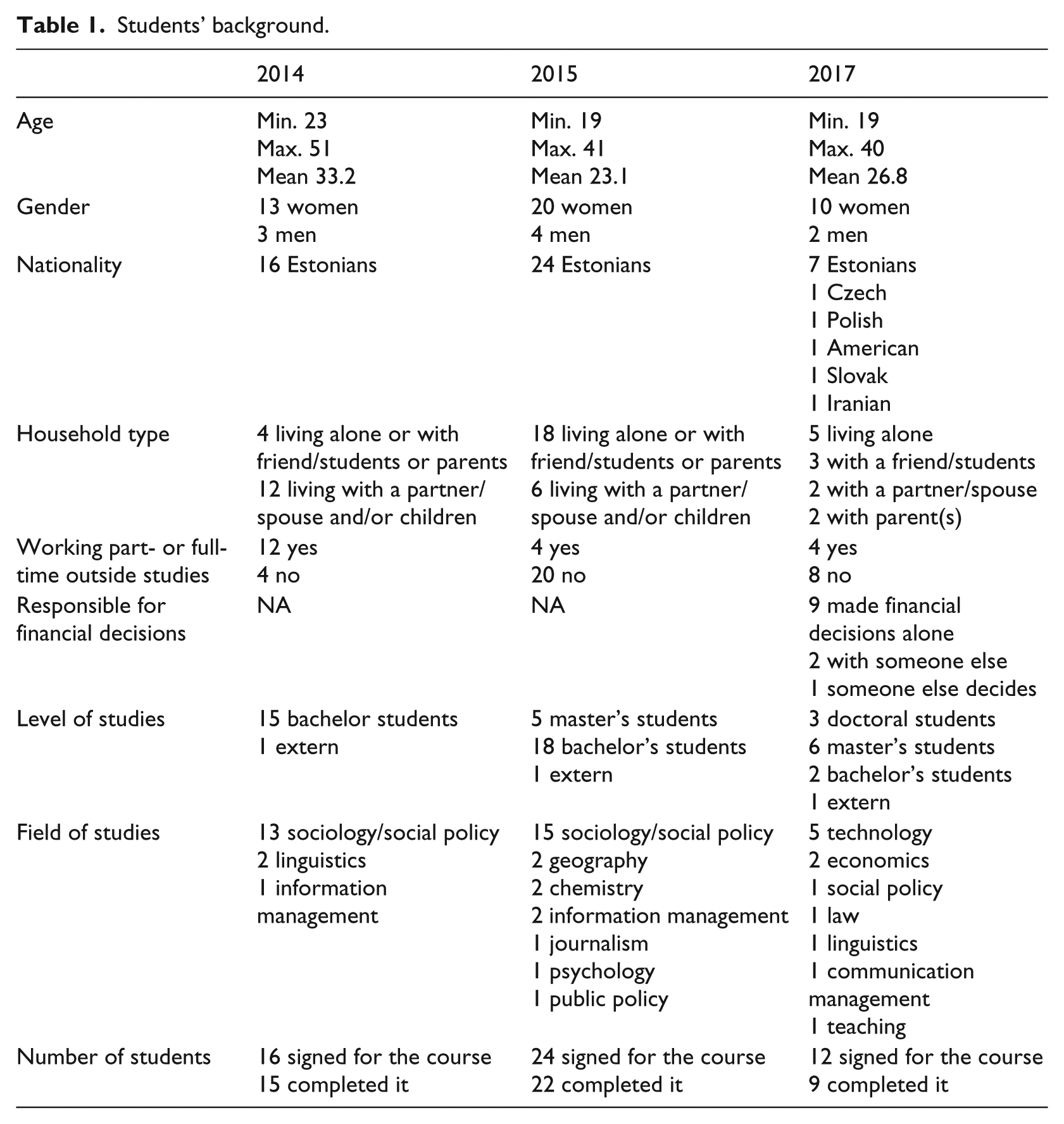

I have designed and taught a Financial Education course in the Institute of Social Studies at the University of Tartu. In autumn 2014 and 2015, it was taught in Estonian, while in spring 2017, it was taught in English, and leaned more towards behavioural economics than in previous years. The topics ranged from budgeting and planning, saving and investing, insurance and pensions, to avoiding debt and fraud. It was an elective course in all 3 years, available to students from all fields and levels of study. The participants differed considerably from group to group, as can be seen from Table 1. In the first year, most were working outside their studies and had a family. In the second year, most were full-time students, younger and mostly financially dependent on their parents. In the third year, it was an international group with a more diverse background. In the first and second year, the majority was bachelor’s students of sociology or social policy, whereas in the final year, the majority was on master’s level or higher and studying technology disciplines or economics (see Table 1 for a more detailed overview).

Students’ background.

In the first lecture, a quantitative survey was carried out to map students’ knowledge, attitudes and behaviour using the OECD financial literacy measurement toolkit (OECD, 2014a). Test results showed that students attending the course had relatively good financial knowledge compared with the Estonian population (see Appendix 1 of Supplementary material), but they did not plan their finances for the longer term, nor did they save or invest. Therefore, instead of focusing on the provision of financial knowledge, the course had to address attitudinal and behavioural issues. For that reason, an intervention was designed using the ‘behavioural economics lens’ (Altman, 2012).

The intervention

In the second lecture, the students were asked to choose a measurable goal in their personal or household finances. It had to be personally relevant and achievable within 7 weeks. The principles of goal setting were explained to them, but they were free to set their own goal. To commit to achieving it, they were asked to hand in the promise in writing. This was a dilemma for me as it was evident that some of these goals were not motivational and were rather unlikely to be achieved. On one hand, for improving the financial well-being of the student, I should have interfered. On the other hand, to help students learn about the factors affecting their behaviour in managing personal finances and choosing effective goals, interfering had to be avoided. Therefore, I did not suggest any changes, but at the end of the course and the assignment, explained the possible reasons for failure. However, to limit the range of difficulty of the goals, sample goals were suggested in the lecture.

The next step was to divide students into small groups. There, each student explained the chosen goals, reasons for not behaving in the desired way so far and the rationale for choosing this particular goal. The task for the group was to advise each member on achieving the goal and to find information from both practical and academic sources to support their arguments. The hidden agenda of requiring such teamwork was to use commitment, peer pressure and advice as tools for overcoming biases hindering sound behaviour. For a 7-week period, the group had to meet outside the lectures on a regular basis to advise each other and report on the progress they had made. I set deadlines for these meetings and reminded of them in the lectures. In 2014 and 2015, the assignment was incentivised by assigning a grade. In 2017, the assignment was not graded. In the first year, the students wrote and presented their team report. It had to cover the following topics: description and justification of the goals; explanation why these had not been achieved before the intervention; advice given by the team members; progress in achieving the goals and explanation of reasons for not achieving (if relevant); conclusion and protocols of team meetings. In the last year, progress towards goals was discussed individually in every lecture, and they filled out a questionnaire at the end of the course. The questionnaire covered the same issues as the written report, except for the protocols.

Results

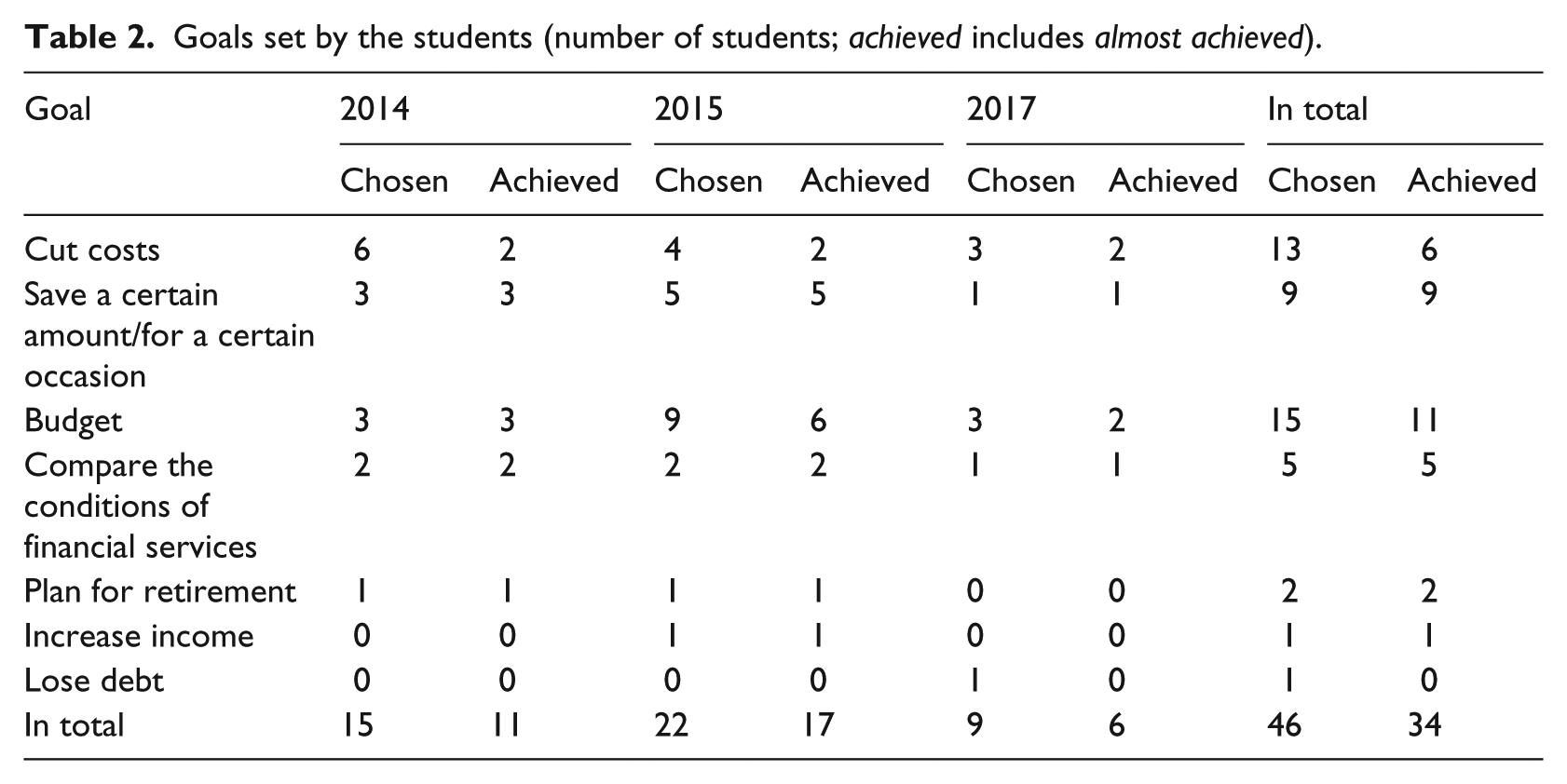

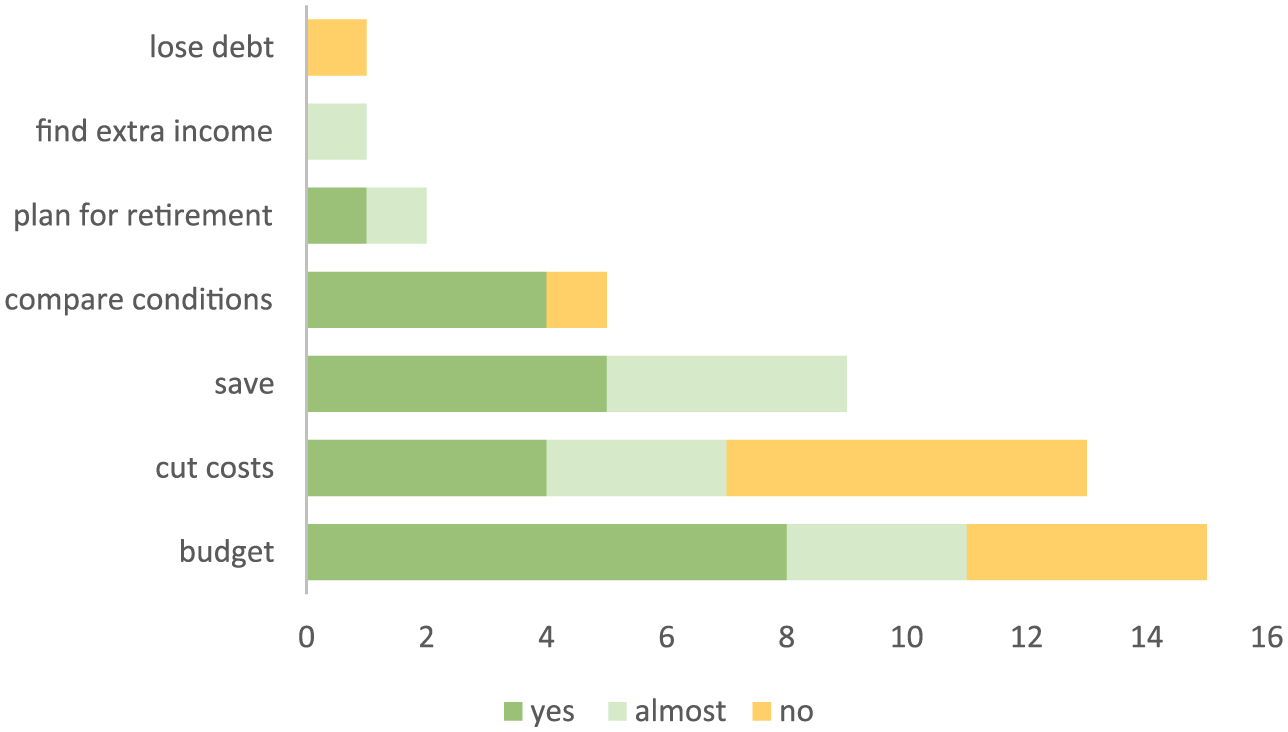

Based on the reports, discussions and the questionnaire, I analysed the results of the intervention. In 2014, 11 of 15 achieved their goal in full or to some extent; in 2015, 17 of 22 succeeded. In the last group, two-thirds achieved their goal at least to some extent (see Table 2). Those who failed to achieve their goal had chosen to cut costs or to start budgeting (see Figure 1). Both are relatively abstract and not especially rewarding goals. None of the students who decided to save for something relevant and tangible had failed.

Goals set by the students (number of students; achieved includes almost achieved).

Achievement of the goal by its type (number of students).

The main reasons for not behaving in the desired way before the intervention were reported to be being attracted to spend money rather than save, having to cover unexpected costs, the lack of motivation and the strength of habits. Merely one student said it was due to the complexity of financial services.

In all groups, students were asked to explain what had hindered them from working for these financial goals before the intervention and which had been the major obstacles they faced during this assignment. The main obstacles were said to be the lack of time and unexpected costs. As one student said, ‘life just happened’. However, they did note it may have been self-rationalisation, rather than objective reasoning, as expressed by one of them, seemed that I don’t have the time but in fact it is possible to find time if you have motivation.

All the students had changed their behaviour for the short term to some extent, and many believed they could continue behaving differently after the end of the project as well. A few quotes to illustrate their feedback: the task taught me it is possible to save even though I didn’t achieve the goal of actually keeping a budget, I am now more aware of my spending and can control my expenses better.

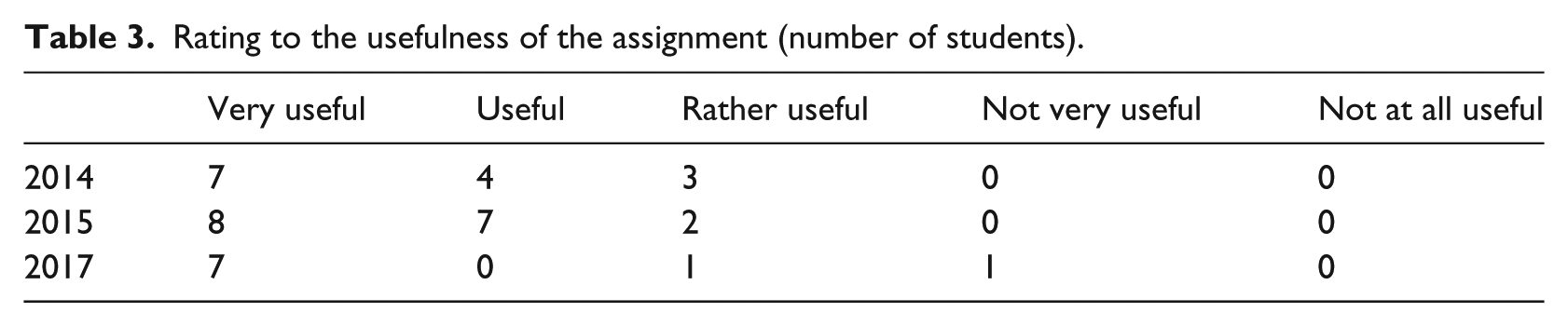

At the end of the course, students were asked to rate the usefulness of the assignment. More than half found the assignment very useful, 11of 40 rated it as useful, no one considered it not useful at all (see Table 3).

Rating to the usefulness of the assignment (number of students).

Besides raising awareness and acknowledging the reasons for their less than sound financial behaviours, majority of them started learning from their peers as illustrated by a quote from one of them: I have always thought I cannot save because my income is too small. After hearing a fellow student talk about how she saves from her even smaller income I started to think, maybe I do have some unused resources? Maybe it is just a small thing that I need to change that will help to improve my financial situation?

In addition, the negative effects of social norms were noted: When I was analysing the conditions of my credit cards I realised I had taken two of them only to prove my social status. There was a time when credit cards seemed to be a token of high status and the cards offered by the bank seemed like a good opportunity to allow myself costs I couldn’t have afforded at the moment. … I have been aware of the costs and fees but have just ignored it.

The only student who found the assignment to be of rather little use explained, if people had the personal determination and skills to achieve their goal, it can be helpful. But I feel that this assignment can be done on your own time since the topics covered in class were not really needed to work on the goal.

This student had chosen as a goal ‘to find a suitable credit card to apply for when she returns to her home country’. She had compared the conditions of many providers, but did not have a high enough income to qualify for one. Although credit cards were explained in class, the conditions and requirements vary in countries; therefore, the coverage may not have been sufficiently detailed for her needs. It brought me back to the dilemma of whether to interfere in the goal-setting stage or not. If the goals are too simple, for example, to set a budget, it is challenging to provide relevant knowledge on a suitable academic level, especially for doctoral students.

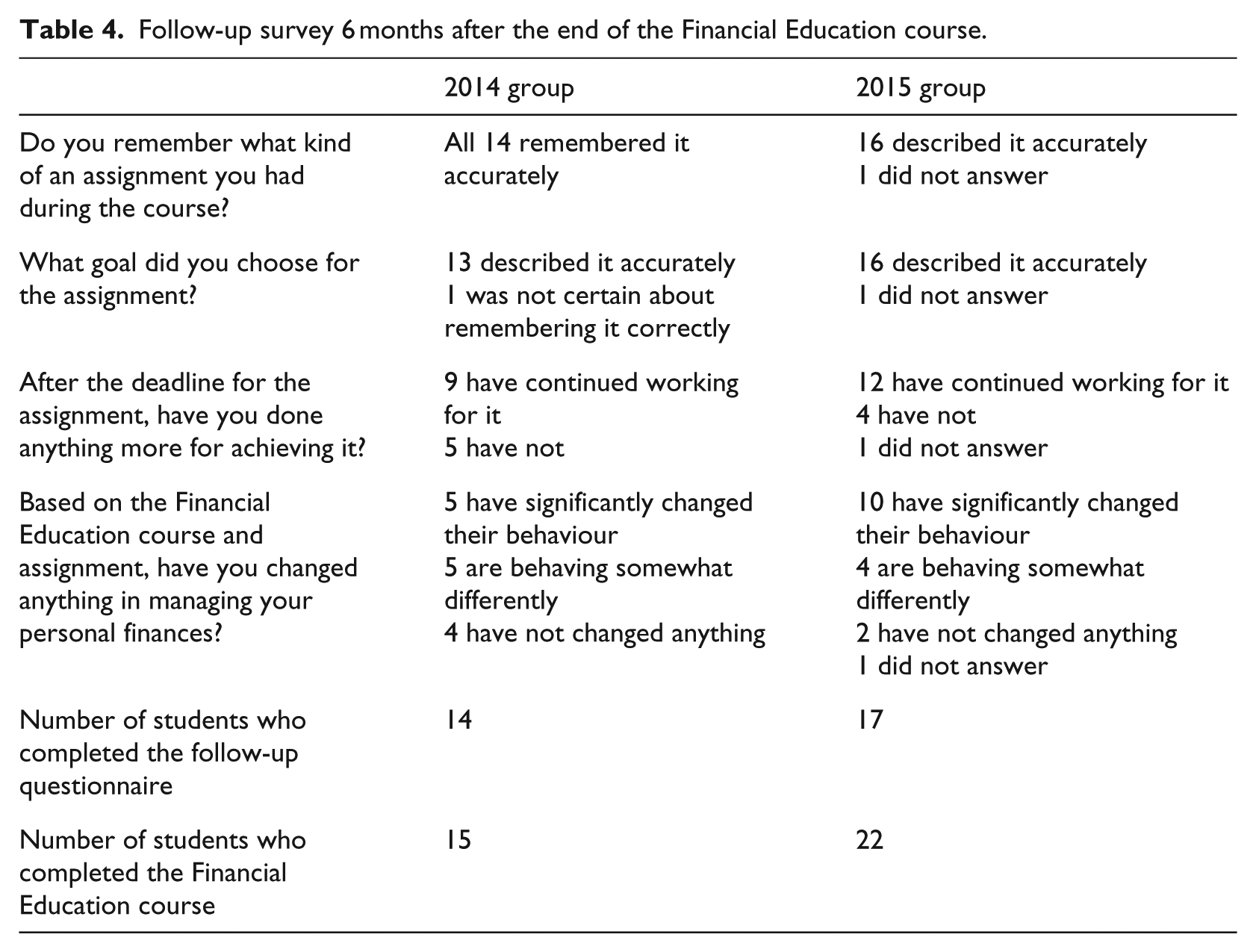

To measure the long-term changes in behaviour, 6 months after the end of the Financial Education course, the participants received an e-mail asking them to fill out an online questionnaire (Table 4). In the first group, 14 of 15 responded, 13 accurately remembered the goal they had chosen, and 9 said they were behaving differently because of the intervention. In the second group, 17 of 22 responded to the online survey, 16 accurately remembered the goal they had chosen, and 12 said they had changed their behaviour because of the intervention.

Follow-up survey 6 months after the end of the Financial Education course.

The follow-up questionnaire also asked for feedback to the contents, methods and format of the course. This was intended for improving the design of the next courses and to avoid disparities such as the one quoted earlier. In both groups, nearly half would have liked to learn more about investing. This was surprising, as investing is very rare in Estonia, and in class, these topics seemed to interest the audience the least. In the next years, more attention was dedicated to investment services, and a guest lecturer from Nasdaq OMX was invited to explain the basics of the stock market. To the question ‘which topics should have been covered less’, more than half replied that all topics were covered in sufficient depth considering the length and scope of the Financial Education course.

Case 4: Financial education for commuters

More than 1% of the Estonian population commutes to work in Finland (Telve, 2015). The majority of these commuters are men without tertiary education. It is one of the strategic aims of the Estonian Lifelong Learning Strategy to persuade them to continue their studies, and they are seen as one of the vulnerable groups (Ministry of Education and Research, 2014). To help them in taking the first step, a financial education course was provided to them in the location most convenient for them – on the ferry travelling from Estonia to Finland. In designing the programme, secondary data were used, gathered by both the Ministry of Education and Research and the ferry line. Both institutions were consulted before finalising the programme.

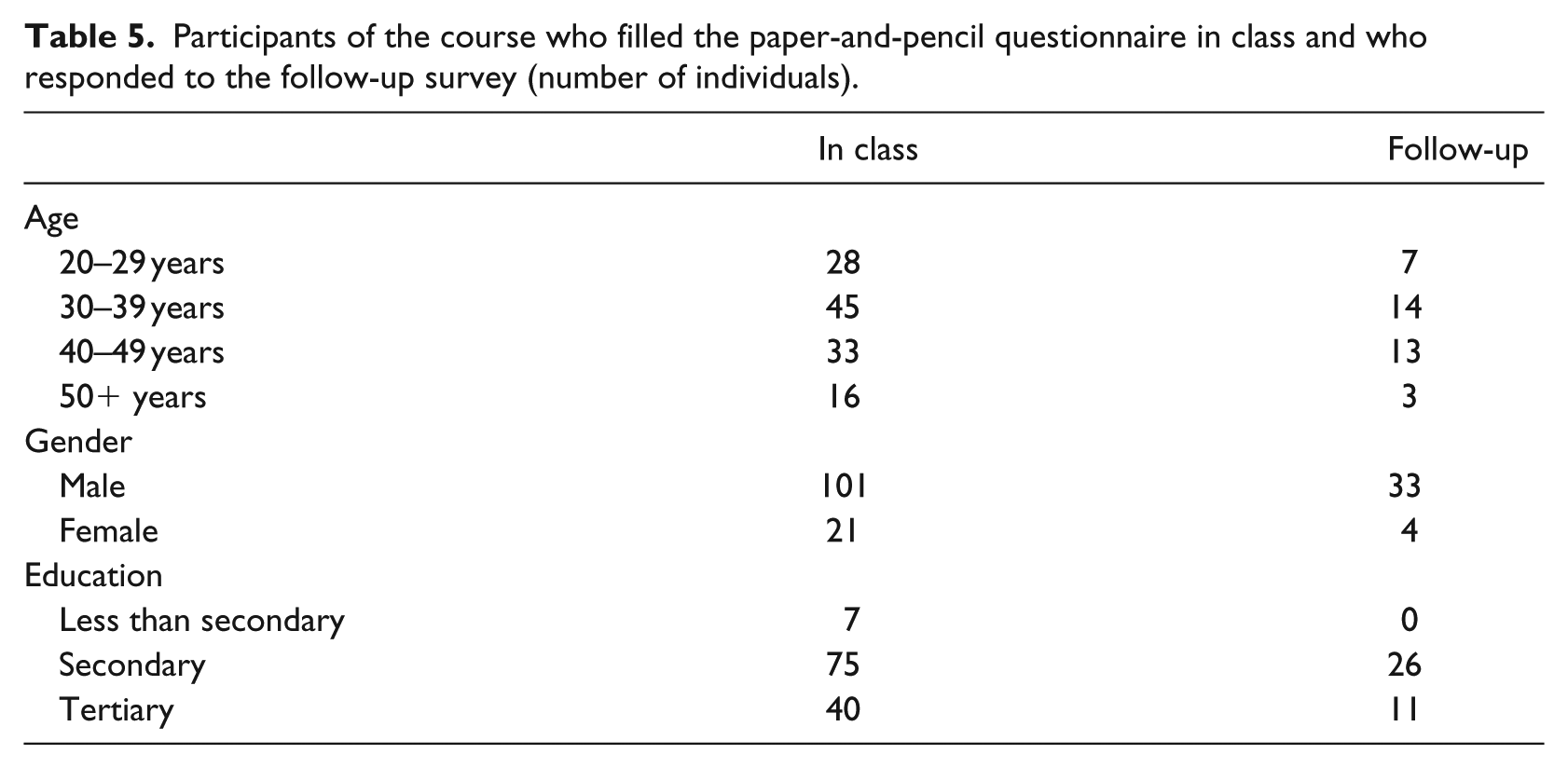

From February to May 2015, weekly financial education lectures were provided free of charge, with a total of 17 meetings on seven topics involving more than 150 participants. They were mostly men aged 30–49 and with secondary education (see Table 5). After the introduction, the participants were asked to fill out a paper-and-pencil questionnaire. It was not mandatory, and therefore, there are missing data for more than 30 participants. The aim of the survey was to map their interests and current financial behaviours.

Participants of the course who filled the paper-and-pencil questionnaire in class and who responded to the follow-up survey (number of individuals).

The paper-and-pencil survey results revealed that commuters are financially more secured than the average population. Two-thirds could cover their expenditures in case of income loss for more than 3 months without borrowing or moving home. This is double the Estonian national average (Saar Poll 2015). Furthermore, 17% had invested in financial instruments, nearly five times more than the average population. As one of the participants said, The biggest risk is not to take any risks

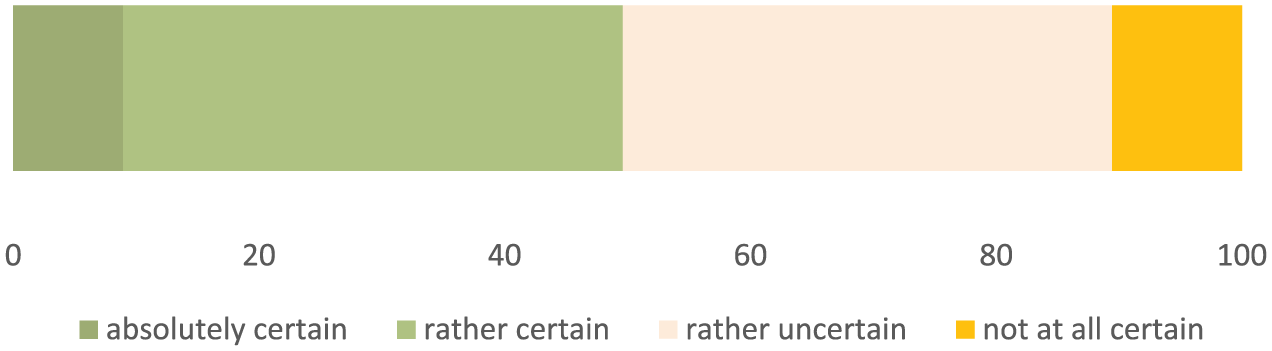

However, half of them were not confident in having planned their finances sufficiently for the longer term (see Figure 2).

Certainty in having planned personal finances sufficiently for the longer term (n = 123).

Despite thorough background analysis and consultation with the Ministry and the ferry line prior to the course, their high level of financial literacy was unexpected. In fact, they are not the vulnerable group in Estonia. Quite the contrary, these are the few who do engage in long-term planning and saving, unlike the secondary data from educational surveys and ferry line customer data suggested. In hindsight, it is easy to understand how living such an uncomfortable life is a prudent financial decision.

Based on these findings, the contents of the Financial Education course were shifted from prevention topics, such as keeping track and avoiding debt, to more promotional subjects, such as investment services for the beginner and intermediate level. The participants learned from each other’s experiences in investing money and using various tools for that, while the discussion was led by the lecturer to provide objective knowledge.

The intervention

As part of the training, the commuters received a card where they had to choose a measurable and personally relevant goal. On the card, there were seven options to choose from, with blank fields to be filled by the participant. For example: To save for …………….. / name of the purchase / by the ……………. / date / ………………. euros.

The card in Estonian, compiled by me and designed by the ferry line, is in Appendix 3 of Supplementary material. Its aim was to have the participants choose goals of similar difficulty.

The groups were too heterogeneous and the training too short for dividing them into teams. Instead, the goals and possible obstacles were discussed in class. After 5 weeks from training, they received an invitation by e-mail to participate in the online follow-up survey. They were informed about the follow-up in class when they received the card.

Results

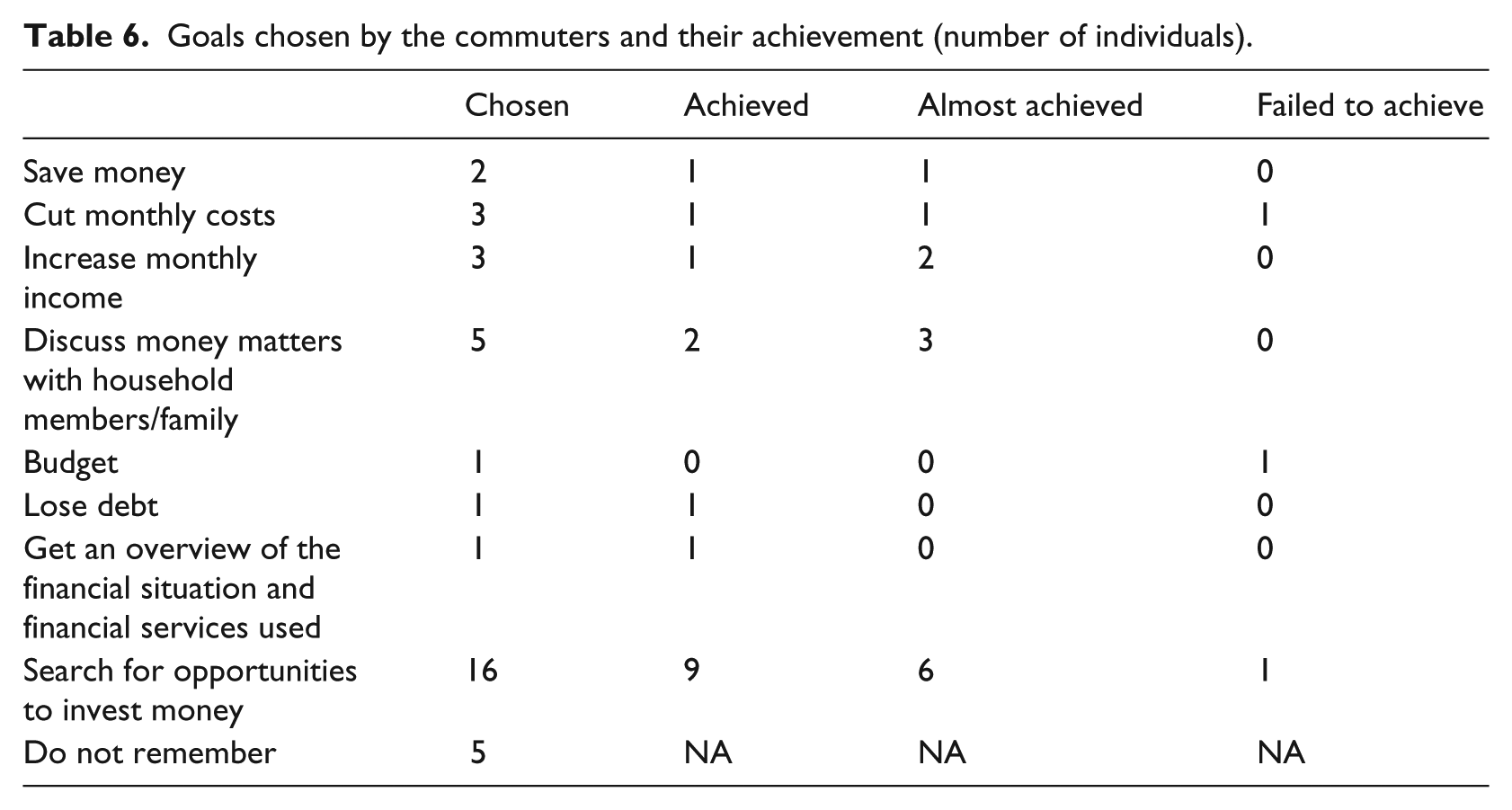

A total of 38 participants responded to the follow-up, 5 of the 38 did not remember the goal they had chosen, 29 had achieved it to at least some extent. Most had decided to search for suitable ways for investing their money (see Table 6) and only one had failed to achieve that. This can be interpreted as a promotional goal. As discussed in the cases of students, these are more motivating than prevention goals (such as cutting monthly costs).

Goals chosen by the commuters and their achievement (number of individuals).

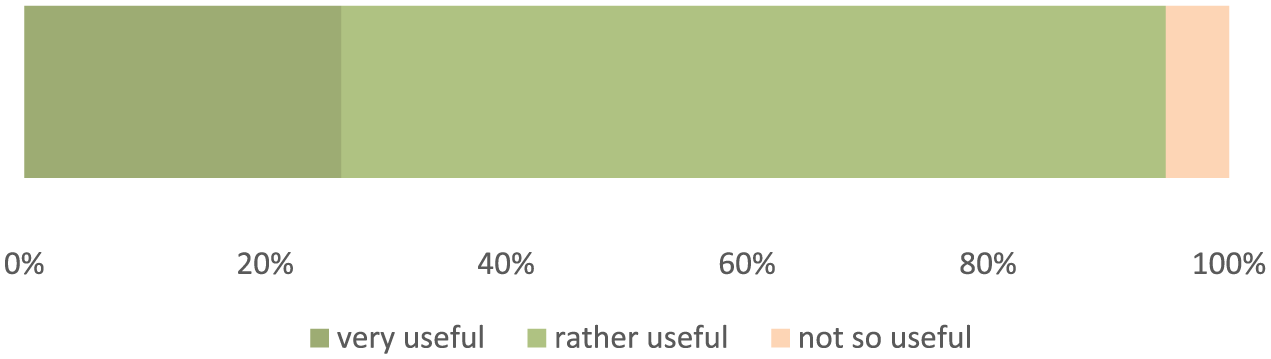

The self-reported reasons for failure were unexpected costs and the lack of time, just as reported by the university students. Most of the respondents rated the training as rather useful or very useful (see Figure 3). None found it to be not useful.

Usefulness of the financial education course for managing personal finances.

Learning from people with similar background and deciding to work for a personally relevant goal as part of the training improved the outcomes of the course. However, as roughly only a third of the participants filled the follow-up survey, these results must be treated with care.

Seven of 38 said it is hard to decide whether they have changed anything in their personal finances because of the course. To illustrate the feedback of that minority, two quotes from their comments in the survey, You can’t change your money matters in a second. It is more of a long-term issue At the moment I have not made any major changes, but I have searched for different options for investing money and I am planning to try investing in the nearest future

Case 5: Financial education for early-stage entrepreneurs

From October 2016 until December 2017, a 2-day financial education course was provided to early-stage entrepreneurs. They attended the financial education course as part of a training module for starting their own business, funded by the Unemployment Insurance Fund. On the first day, in a 6-hour academic training, they were invited to analyse their short- and long-term plans in various exercises, to acknowledge the importance of consciously managing their personal finances in their career stage and become aware of behavioural biases. The second day focussed on comparing financial services, especially savings and investment products. The participants were aged 25–49; 11 women and 12 men.

The intervention

On the first day, they were asked to choose a personally relevant goal that is achievable in 3 weeks’ time. It had to be written down and handed to the lecturer. Next, they were divided into pairs and asked to explain the goal they have chosen, reasons that have stopped them from behaving in the desired way so far, and advise each other in achieving their goals. Finally, they divided the goal into smaller steps and filled in a detailed action plan for the next 3 weeks. The translated form of the action plan is in Appendix 4 of Supplementary material. They were asked to exchange contacts and to remind each other of the plan every week. The aim of the intervention was to help the early-stage entrepreneurs to acknowledge the importance of managing their personal finances effectively and to nudge them towards taking the first step immediately. Just as in the previous case studies, the mechanisms it used were commitment, measurable and personally relevant goals, partitioning, deadlines, reminders, peer pressure and advice.

After 3 weeks, on the second day of the Financial Education course, their progress was measured via a paper-and-pencil survey. It was handed out at the beginning of the class and filled in individually. Later, their experiences were discussed in class. The measurement took place in advance, to avoid any influences from the in-class discussion.

Results

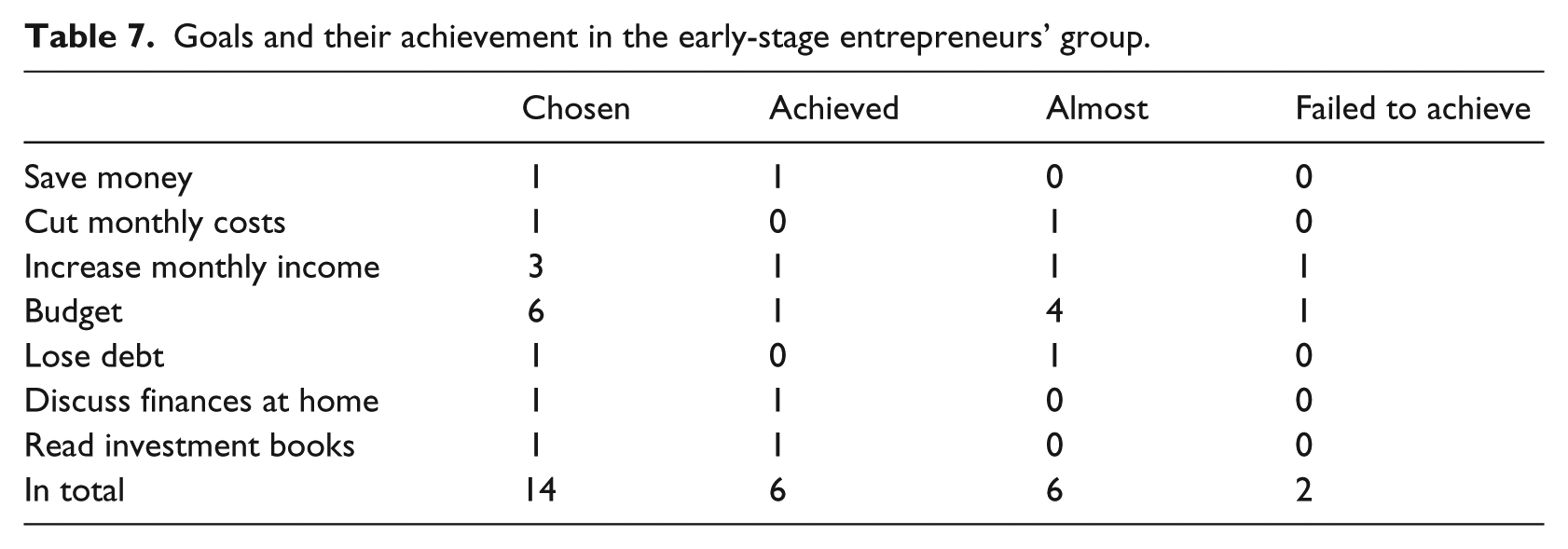

The full course has been completed by 14 early-stage entrepreneurs, 12 of 14 achieved their goal in full or to some extent, and merely three say that they have not changed anything in their financial behaviour (Table 7). The sample is too small for analysing which types of goals are more motivating than others.

Goals and their achievement in the early-stage entrepreneurs’ group.

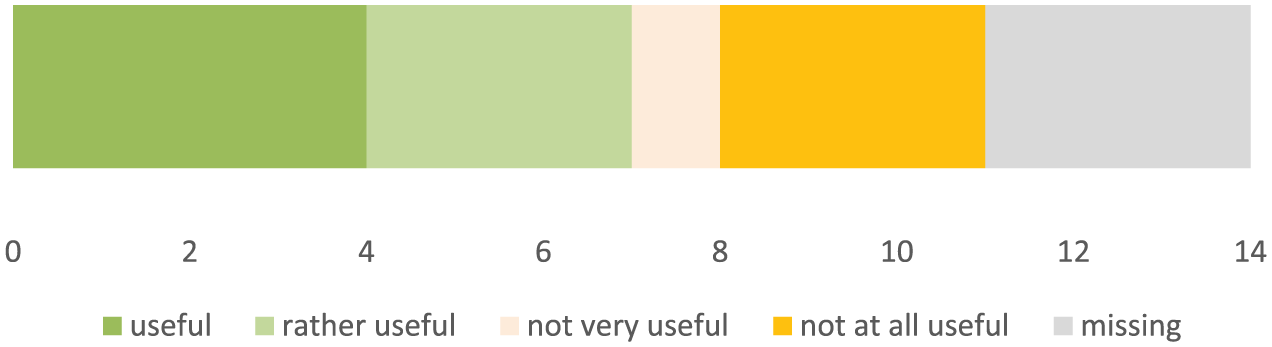

Peer advice has not been used in this group. Merely half found it useful, while no one rated it as very useful (see Figure 4).

Rating of the advice and help from team member in working towards the goal.

This happened due to the lack of communication. As the participants were not acquainted with each other, majority had not contacted the team member outside the class. One of them explains, we did exchange phone numbers in class, but neither of us made the call

Therefore, partitioning has had rather little effect, as only a few have reminded the peer of the deadlines or advised regarding achieving the sub-goals. The majority had ignored the deadlines as admitted in these quotes: In reality, I did not really pay attention to the deadlines the sub-goals were good in principle, but in practice they were not used, unfortunately

This highlights the need for carefully selecting homogeneous group members for making use of peer advice. Strangers will not talk about their personal finances outside the class, at least not without being incentivised to do so.

Those few who did communicate between classes, rated the advice and deadlines as very useful: it [peer advice] disciplines, keeps me on the course sub-goals are of great help in not giving up on achieving the larger goal

Discussion

The results support the hypothesis that behavioural insights, such as goal setting, deadlines and commitment, applied to financial education help to improve financial behaviours. A total of 75 of 98 participants achieved their goal in full or to some extent, and more than half reported that they behave differently after the end of the course because of the intervention.

The first key finding is that promotional goals are more motivating than prevention goals. In individualist cultures, such as Estonia, people are found to be more promotion-focused (Pham and Higgins, 2005). However, in the three student group cases, less than a quarter chose a promotional goal such as saving for a certain purchase or increasing income. This can be explained by several factors. First, individuals are loss averse (Kahneman and Tversky, 1979), at least twice as sensitive to losses as they are pleased with gains. Therefore, the participants may have been more motivated to choose to avoid losses than to set promotional financial goals. Second, it is easier to say ‘I should spend less’ than to decide on a concrete and achievable promotional goal (Ariely and Kreisler, 2017). Third, it might be a domain-specific effect. Cho et al. (2014) studied the role of regulatory focus in saving behaviour in the United States. There 63 per cent of the respondents had chosen a prevention-orientated saving goal as their primary financial goal. Fourth, prevention-orientated individuals are more prone to the status quo bias (Chernev, 2004), the tendency to keep things the way they are instead of making any changes. The latter implies that the students who chose to cut costs may be more prevention-orientated; it would explain why less than half of them succeeded in changing their behaviour.

In this study, the regulatory focus of the participants (i.e. whether they are more promotion or prevention-orientated individuals by their personality traits) was not measured. In future research, it should be included in the analysis of the effectiveness of prevention and promotion-focused financial goals. The regulatory fit has been proven effective for improving health behaviours (Sherman et al., 2006), but to give mixed results in saving behaviour (Cho et al., 2014). In this study, promotional goals were substantially more motivating than the prevention ones – none of the students who had chosen to achieve rather than avoid something in their finances failed to achieve it. This brings us back to the dilemma of interfering in the goal-setting stage. Emphasising the effectiveness of promotional, salient, tangible and measurable goals may have improved the outcomes of the course for the whole group. On the other hand, learning from personal experience, including failures and about one’s own attitudinal and behavioural obstacles, may be more useful for the longer term.

The second key finding is that for utilising peer effects, the participants of the financial education course need to be fairly homogeneous and have relatively close-group relationships and regular meetings. The intervention received positive responses from the participants in all cases; the majority rated it as a useful tool for improving their financial behaviours. However, in one-time or two-day training, peer pressure and advice did not prove as useful as in the longer financial education course, indicating the need to carefully select the participants and highlighting the limited effects of short financial education courses.

This poses a challenge for the designers of such programmes. Understanding the needs and values of the participants prior to the course requires more data than the basic socio-economic factors can provide. As shown in the fourth study, even thorough analysis of secondary data and consultation with the stakeholders may prove insufficient for understanding the financial situation of the participants. The group considered to be in a vulnerable state turned out to be the more advanced instead. Furthermore, as financial education courses are mostly voluntary, self-selected sample does not enable the creation of homogeneous groups.

In the first two groups of students, the participants were rather homogeneous. As they were in a similar life stage (the first group had to manage their time and money for their work and family, the second group was more dependent on their parents), it was easier to learn from each other. In the third year, the group was more heterogeneous. This limited the extent of peer effects. For example, two women from different continents and with 21 years of age difference had problems in their teamwork. One of them writes, The advisor was very helpful until I started to ignore her e-mails. I had already failed and did not want to face this fact. … At first I asked her about it [her goal]. But she pretty soon had it achieved and I did not have a further role.

In the fourth, the commuter case, the group was more heterogeneous and the one-time meeting did not allow for exploitation of peer effects. However, they did learn from their peers, especially regarding investment services.

The third key finding is that partitioning works only if the reminders of the sub-goals are well-designed or incentivised. In the student cases, regular reminders were provided by the lecturer. These were rated as useful by the participants. The pre-filled multiple choice cards used in the fourth case served as a commitment device for the participants and helped to measure the outcomes of the course. If it is not possible to have several meetings of the same group nor divide them into smaller teams, such a card is a useful tool for improving and evaluating the outcomes of the brief course. In the fifth case, sub-goals were set and contacts exchanged for deadline reminders, but merely a few acted upon them between the meetings.

Financial education tends to be seen as something other people need, not me. Often, people say, it is those who earn significantly less or more than them, or those who have less or more education, that need financial education. This is illustrated by a quote from an international student: very good training, especially for people who have problems with planning and controlling spending.

The reasons for that can be optimism and overconfidence, as De Meza et al. (2008) stated, noting that ‘optimism is a prime cause of financial incapability’ (p. 50). It is human to think that things will somehow be sorted out in the future and no negative scenarios can happen to me, only to others. However, these biases can harm long-term financial well-being, especially as people in more vulnerable situation may not self-select into financial education programmes.

Making changes in personal finances requires understanding from the other household members. Many students wrote about problems with working for the goal due to unexpected costs related to children’s schools or friends’ events. A student from the third group had chosen to cut costs with her partner and save a certain amount of money on a joint account. She wrote in her report, soon I realised that completing the goal is complicated as I do not have the sole responsibility and we have not clearly agreed on what we can spend this money on, and what not.

Therefore, household agreement is needed. Finances tend to be a sensitive subject, and not many households discuss these issues regularly. A student from the first group had called a family meeting for the assignment and the outcome was that they managed to plan a holiday together. So far, it had not been talked about nor prioritised, and therefore they did not think they would be able to find the time and money for travelling together. The effectiveness of talking about money matters among family or peers was noted as a useful change by several students: although talking about personal finances is uncomfortable, it is an eye-opening experience, as it makes one think how to save wisely. … Each team member learned something new from the advice of others.

Changes in personal finances also affect other behaviours. Several students improved their health behaviours as well: they started cooking at home, eating more healthily and walking or cycling more than before. This confirms the findings of improved behaviours in one domain also having positive behavioural outcomes in other domains (Cappelen et al., 2017). Therefore, sound financial behaviour does not only improve financial well-being but also well-being on a broader scale.

Assessment of financial knowledge and behaviour throughout the financial education courses is vital for improving behavioural outcomes. In the first three cases, it helped me to design the course and the participants to acknowledge their attitudinal obstacles. In the fourth case, timely measurement enabled changes to the contents of the course to match the adult learners’ actual needs. In the fifth case, assessment brought out the shortcomings of the design of the intervention in heterogeneous groups.

Limitations

The main limitations of the study are the self-selection of the participants and the analysis of self-reported data. However, financial education is more likely to succeed in creating behaviour change in ‘teachable moments’ (Kaiser and Menkhoff, 2017; Lusardi, 2009) and specific ‘life events’ (Amagir et al., 2018). It can be assumed that the participants chose to attend because of being in an opportune life stage; therefore, they were more aware of their hurdles than students of a mandatory course would have been. The samples of the cases could have been larger for enabling deeper analysis; the same problem many studies on the effectiveness of financial education in college suffer from (Amagir et al., 2018). However, that would have set limitations to the amount and extent of measurement tools employed. There is no standard or rule for the ideal number of cases, but according to Eisenhardt (1989), five is sufficient: ‘a number between 4 and 10 cases usually works well’ (p. 537).

The last shortcoming is the lack of a control group. Again, the same problem has been faced by most of the researchers of the effectiveness of financial education (Amagir et al., 2018). It would not have been fair to assign some of the voluntary participants of a financial education course to a control group, the same problem the researchers of consumer education ‘have long wrestled with’ (Willis, 2009: 440). Provision of financial knowledge and skills without intending to improve the financial behaviours of a group of voluntary participants would have been unfair. Even if I would have overcome this dilemma and randomised half of the group into a standard financial education programme without the assessments and intervention, despite the evidence of such an approach to be less effective (Drexler et al., 2014) and having to provide at least some of the course in parallel, the treatment and control group would have been too small and too diverse for meaningful conclusions. Furthermore, members of the treatment and control group would have talked about their experiences during the course, leading to spill-over effects and contamination of the data (Edovald and Firpo, 2016).

An alternative would have been to provide the standard approach in 1 year and conduct the intervention in another. This would have not given a reliable comparison, as the groups of students are rather diverse also across years as presented in Table 1. For the same reason, providing the intervention in some groups of commuters or early-career entrepreneurs and not in others would not have given a sufficient comparison either. The third option would have been to conduct the intervention as part of some other subject’s course. However, those who self-select into a financial education course are already more aware of their finances. Even if all the elements (including the assessments, discussions, commitment, reminders, peer advice etc.) could have somehow been incorporated into the programme of another subject, the groups would still not have been sufficiently homogeneous. Spencer et al. (2015) conclude in their analysis of research on the effectiveness of financial education that correlational studies using control groups are not applicable for the providers of voluntary financial education courses.

Conclusion

Financial education is becoming increasingly important for improving financial well-being in all life stages. Yet, there is limited evidence of its effectiveness for achieving actual behaviour change. Furthermore, there is evidence that good knowledge of financial matters does not necessarily translate into sound behaviours. For increasing the effectiveness of financial education, an intervention was designed and tested in five case studies. The findings support the hypothesis that behavioural outcomes can be improved by financial education programmes that use behavioural insights into their design. Furthermore, changed behaviour can be seen also in the longer term. However, these programmes have more influence if they consist of regular repeated meetings instead of brief sessions, and are run for a homogeneous group. In all five cases, promotional goals were found to be more motivating that prevention goals. Therefore, promotional goals set as part of the training, commitment to achieving them by the deadline, partitioning and peer advice are a relatively cheap tool for the promoters of financial education. The intervention would benefit from further testing as the sample of each case was rather small and self-selected.

Supplemental Material

supp. – Supplemental material for Goals, commitment and peer effects as tools for improving the behavioural outcomes of financial education

Supplemental material, supp. for Goals, commitment and peer effects as tools for improving the behavioural outcomes of financial education by Leonore Riitsalu in Citizenship, Social and Economics Education

Footnotes

Acknowledgements

The author is grateful to Liam Delaney for his guidance in the early stage of the study, to Katri Kerem for her help throughout the process and to Philip Newall, Tim Kaiser and W. Fred van Raaij in the final stage. She would like to thank Heli Lehtsaar-Karma for helping to conduct the two last cases and Adele Atkinson for her feedback. The whole study could not have been possible without Rein Murakas taking the risk of giving the responsibility of designing a new course to a novice in academia. The author would also like to thank the participants in the conferences Research in Behavioural Finance (2016 in Amsterdam) and Leveraging Behavioural Insights (2017 in Tel Aviv) for their feedback and suggestions.

Declaration of conflicting interests

The author(s) declared the following potential conflicts of interest with respect to the research, authorship, and/or publication of this article: The author was working for the University of Tartu as explained in the paper, and as a consultant for the OECD at the time of writing the paper.

Funding

The author(s) received no financial support for the research, authorship and/or publication of this article.

Supplemental material

Supplemental material for this article is available online.

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.