Abstract

Acquiring financial literacy presents many unique challenges for young adults with disabilities. Although financial literacy can and should be taught throughout the lifespan, this review examines the curriculum accessible to students with high incidence disabilities who are 14–21 years old, when they are planning for transition from secondary school to the workforce/higher education. This review examines five examples of promising financial literacy curriculum: Financial Fitness for Life, Practical Money Skills, Finance in the Classroom, Money Talks 4 Teens, and Money Smart for Young Adults. The curricula are compared for their application of universal design and culturally responsive curriculum principles. Completed rubrics will be presented to evaluate those curricula based on standards-based financial literacy concepts particularly relevant to youth with special needs, principles of universal design, and culturally responsive curriculum.

What good resources are readily available for teaching financial literacy to young adults with special needs? How do those resources compare when it comes to universal design and cultural responsiveness? This article will answer those questions about five examples of promising financial literacy curriculum from the United States: Financial Fitness for Life (Gellman and Laux, 2011), Practical Money Skills (Visa, 2000-2016), Finance in the Classroom (Utah State Board of Education, n.d.), Money Talks 4 Teens (University of California Cooperative Extension, 2008), and Money Smart for Young Adults (Federal Deposit Insurance Corporation (FDIC), 2011). Completed rubrics will be presented to evaluate those curricula based on standards-based financial literacy concepts particularly relevant to youth with special needs, principles of universal design, and culturally responsive curriculum.

Although there are many health impairments and different special needs, we focused our review of curriculum for students with the four most common categories among special education services: those who have specific learning disabilities (LD), speech and language impairments (SLI), intellectual disabilities (ID), and emotional and behavioral disabilities (EBD; Minarik and Lintner, 2016). These four disabilities make up over 75% of students receiving special education services in the United States (Minarik and Lintner, 2016). Students with disabilities are generally taught alongside their non-disabled peers in public schools in the United States. Teachers expect to integrate students who have special needs into their “regular” classes while attending to the unique learning needs identified in Individual Educational Plans (IEPs). In the United States, under federal special education law (IDEA, 2004), all students identified with a qualifying disability are entitled to an Individual Education Plan (IEP). For students aged 16–21, the IEP focuses on preparation for life after high school and includes an assessment process identifying priority academic and life skill goals for a student with a disability. The IEP also addresses specific skills and goals necessary for a student’s successful transition from school to adulthood. Thus, the transition portion of the IEP should be addressing employment, education, independent living skills, and other goals for students with special needs.

We did not examine the curriculum specifically for its applicability to lower incidence disabilities such as visual or hearing impairment. Although financial literacy can and should be taught throughout the lifespan, this review examines curriculum and instruction for secondary students with high incidence disabilities who are of transition-age: 14–21 years old by federal definition (IDEA, 2004). As youth face transition plans (required as part of a student’s IEP), this time for financial education is non-negotiable.

In the United States, acquiring financial literacy presents many unique challenges for young adults with disabilities (Gargia-Iriarte et al., 2007; Harnett, 2006; Lehmann et al., 2000 Lombe et al., 2008; Mittapalli et al., 2009). Some will rely on government benefits, others will have families who control their purse strings. Many will face discrimination. Minorities and lower income families are overrepresented in special education, making culturally responsive instruction all the more important. Thus, finding an excellent curriculum to teach young adults with special needs financial literacy is imperative.

An underlying (perhaps false) assumption within the field of financial literacy education is that all individuals face an equal playing field, and if provided specific information, all are enabled and competent to carry out financial choices (Pinto and Coulson, 2011). The belief that all students experience the same financial life and opportunities overlooks the dissimilar situations and conditions that affect the personal finances of many youth (Pinto and Coulson, 2011; Roithmayr, 2014). Financial education for students with disabilities from a social justice viewpoint is “concerned with equity in all aspects of social and economic life and cultural recognition” (Pinto and Chan, 2010: 61). Financial literacy curriculum, at its best, should address systematic injustices and barriers to financial literacy for students with disabilities. Teachers are encouraged to supplement and adapt any financial literacy curriculum that they choose to meet the individual needs and context of their students. Typically, teachers using financial literacy curriculum in the United States would receive training on the concepts as well as curriculum during their teacher preparation programs at the college level.

This article will recommend five different curricula that show promise for educating students with disabilities. While there are numerous other Internet-based financial literacy curricula, these four were recommended by Caniglia and Courtney (2013). The printed curriculum is the best available for financial literacy instruction, published by the premier organization for teachers of economics: The Council for Economic Education. All the curricula discussed in this review will be evaluated on their conceptual integrity, applicability to all learners, and cultural relevance. Each of the curricula has advantages and disadvantages. The rubric can be applied to other curricula for the sake of comparison.

Important conceptual content for youth with disabilities

The slim volume National Standards for Financial Literacy (Council for Economic Education (CEE), 2013) recommends key concepts, topics, and benchmarking progressions for financial literacy. These voluntary recommended standards are meant to guide states in their development of financial literacy benchmarks for K-12 students across the United States. Many states have based their standards on these recommendations. The standards include fundamental concepts and skills that all students should learn for basic financial literacy. The following concepts seem most relevant to youth with special needs: earning income, budgeting, saving, banking, and insuring. So, those concepts were the ones we examined and evaluated most closely in the curriculum reviewed. The two main concepts (which were included in the national standards) that we omitted from our review of curriculum were credit and financial investing. Credit is a more general topic in financial literacy which can be addressed with many different online activities and resources. Financial investing is a more advanced topic which we assumed would come after all the other concepts were learned. We thought that earning income, budgeting, saving, banking, and insuring were the more fundamental concepts which must be addressed immediately in ways that are specific to youth with special needs. As mentioned previously, using principles of universal design that incorporate adaptations and accommodations into instruction increase access to the curriculum materials for students with disabilities. These five concepts all provide contexts for students to develop personal goals, engage in decision-making, participate in problem-solving, and take actions that will serve their best interests. They are crucial to transition planning as students prepare for adulthood (Wehmeyer et al., 2012).

In evaluating the conceptual content of the curricula, we used the criteria not present, evident, or strongly evident in order to judge the quality of the curricula’s conceptual breadth and depth. If the concept was not included in any easily accessible way, we coded it as not present. If the concept was included in some way, it was coded as present. Strong evidence of the conceptual focus meant that the curriculum included examples, scaffolding, and multiple strategies for teaching the concept.

Earning income

Earning income is fundamental to financial literacy. Generally, financial literacy curriculum promotes paid employment. Employment is a key area of emphasis for most youth with disabilities as not only does paid work give individuals with disabilities opportunities for integration into the community, but it is the basis for budgeting, saving, banking, and insuring. Low employment expectations, and confusing government programs with conflicting eligibility criteria have prevented many young people with disabilities from making successful transitions from school to employment (National Collaborative on Workforce and Disability, 2012). All financial literacy curriculum for students with special needs should introduce and reinforce the importance of earning income. As many transition-age students demonstrate a lack of financial skills, IEPs may include specific annual goals targeting acquisition of financial skills. When financial literacy curriculum encourages students to think about potential careers and practice job seeking skills, we rated it highly in teaching the concept of earning income.

Budgeting

Assuming that youth with special needs will have some income, they need to understand that they need a spending and saving plan (budget). Budgeting is a skill that can be incorporated into IEPs. Tom Nerney, of the Center for Self-Determination, explains that a highly personalized individual budget [is] integrated within a student- and family-directed Individual Education Program (IEP). The youth with a disability or disabilities and his or her family get together with supportive people in their community to develop a vision for the youth’s future. This vision becomes the basis for an implementation plan and budget for achieving the goals. This implementation plan and budget are then incorporated into the IEP to reflect the transition plans (Mittapalli, 2015: 110).

Not only should budgeting be defined, but an excellent financial literacy curriculum should offer students practice in making a budget and considering ways of changing the budget to meet different goals and circumstances. When the curriculum included videos about budgets and interactive worksheets for practicing budget development, we rated it highly for teaching the concept of budgeting.

Saving

Saving for emergency expenses like a car repair or medical bill strains many American budgets (Bell, 2015; Board of Governors of the Federal Reserve System, 2015). Especially for students with disabilities managing government benefits, accumulating savings and assets is a challenge (Mittapalli et al., 2009). One strategy that promotes asset accumulation is the Individual Development Account (IDA; Leydorf and Kaplan, 2001; Lombe et al., 2008). IDAs allow lower income families and persons with disabilities who receive financial assistance, such as Supplemental Security Income (SSI), to save a portion of their earned income without losing benefits. These savings must be earmarked for specific purposes such as education (Assets for Independence (AFI), 2016; Center for Self-Determination (CSD), 2005). Financial literacy instruction should introduce students with disabilities to savings options such as IDAs.

Saving is an area in which there is a documented need for improved financial literacy for youth with disabilities. Parents in one study reported that the large majority (84%) of youth with disabilities receives an allowance or other personal spending money, yet only 45% have a savings account (Cameto et al., 2004). When the curricula included interactive compound interest calculators and savings goal-setting activities, we rated it highly for its conceptual integrity for teaching savings.

Banking

Because youth with disabilities are more likely to be in families that use alternative banking services (like prepaid debit cards or payday loan establishments), financial literacy curriculum should introduce youth to the benefits and accessibility of banks and credit unions (FDIC, 2014). Fees are generally lower at banks and credit unions than at check-cashing and payday loan establishments. Not only do teachers need specific resources to teach about banks to youth with disabilities, they must also have the local contextual knowledge to share with students about which financial institutions will be accessible to them (Johnson and Sherraden, 2007). The financial literacy curriculum should introduce how to use check registers and debit cards. While some students with disabilities may have personal agents (either a family member, guardian, or appointed agent) who act on their behalf in terms of making purchases, banking, or other financial transactions, most students with disabilities can learn to make purchases or bank with the use of debit cards, prepaid credit cards, or electronic banking (Mittapalli et al., 2009). Curricula that specifically taught students how to write checks, understand ATMs, and evaluate the benefits of different banking establishments were rated highly for this concept.

Insuring

Students with disabilities need to understand the importance of insuring their health, place of residence, and vehicle (if applicable). While earning income allows more flexibility in budgeting and saving, it also offers the opportunity for different kinds of health and life insurance. Students transitioning to independence need to know the relative merits of Medicaid, the Health Insurance Exchange of the Affordable Medical Care Act, and private insurance.

As many youth with disabilities may come from families with fewer resources, the need to have insurance seems contraindicated. However, having insurance, especially health insurance, provides an individual with autonomy and opportunities for choice-making in terms of selecting healthcare and healthcare providers. In addition, insurance can be viewed as a part of asset management and can promote an individual’s financial independence by protecting personal assets such as a car or against liability claims. If a curriculum helped students understand the meaning and importance of different kinds of insurance, as well as evaluate the merits of insurance, we rated it highly.

Universal design for learning

Universal Design for Learning (UDL) provides a framework that allows students with differing learning styles to access the curriculum and instruction (CAST, 2011; Fowler et al., 2014). UDL permits a diverse spectrum of learners to access the material successfully by providing a range of strategies for learning the same content. Although all learners can benefit from UDL strategies, UDL is especially important for special educators to consider when evaluating the curriculum. By adapting a UDL framework, teachers can meet the diverse learning needs of all students through varying teaching methods and assessment techniques.

As defined by the Higher Education Opportunity Act (2008), Universal Design for Learning (UDL): (a) provides flexibility in the ways information is presented, in the ways students respond or demonstrate knowledge and skills, and in the ways students are engaged; and (b) reduces barriers in instruction, provides appropriate accommodations, supports, and challenges, and maintains high achievement expectations for all students, including students with disabilities and students who are limited English proficient. [20 U.S.C. 1003 (a) (24) (A and B)

UDL principles build on cognitive neuroscience related to learning and include (a) recognition systems that distinguish patterns and items, (b) strategic systems conveying information on how to perform actions, and (c) affective systems that establish what is essential and offer incentive for learning (CAST, 2011; National Center on Universal Design for Learning (NCUDL), 2014). The Center for Applied Special Technology (CAST), has interpreted those neuroscience principles to mean that the UDL curriculum should include multiple means of representation, multiple means of expression, and multiple means of engagement (National Collaborative on Workforce and Disability for Youth (NCWD), 2012; Rose and Meyer, 2006). These core principles are fundamental to a high-quality curriculum for all subject areas; how they apply to the financial literacy curriculum will be explained in the following sections.

Multiple means of representation

Students vary in how they perceive and comprehend the curriculum presented to them. The more diverse formats and modalities included in the curriculum, the more likely that all students will understand the curriculum (Courey et al., 2013). For example, if teaching how to earn income, the learner could access information through a variety of modalities such as sound, enlarged text, pictures, or graphs. Earning income could be presented via a field trip to different job sites, listening to diverse employment stories, or by interviewing a guest in the classroom. Utilizing video, pictures, and audio all are multiple means of representing a concept to accommodate diverse learning needs. Determining which means of representation would provide the best access to the information would rely on individual student learning characteristics. Students should not just read about financial literacy or hear about it, they should see multiple examples of the concept modeled in myriad ways.

Multiple means of expression

A curriculum that includes multiple means of expression provides students with different avenues to convey their knowledge. This UDL principle suggests that an excellent curriculum would allow students to create posters, oral presentations, brochures, or letters. Besides typical paper and pencil tests or essays, students could demonstrate knowledge about budgets by designing a budget, creating a budget online using a template or interactive simulation, conducting an interview, or by developing a video to teach others how to budget. These are all examples of multiple means of expression that go beyond completing worksheets or multiple-choice tests. Adaptations would be based on learner characteristics. The curriculum should provide a variety of ways for students to demonstrate their mastery of financial literacy concepts.

Multiple means of engagement

In a UDL approach, engagement refers to capturing students’ interests and promoting their desire to learn via authentic and purposeful content. The goal is to promote learning through more authentic, relevant instructional examples that encourage students’ active participation (Courey et al., 2013; NCUDL, 2014). The curriculum should activate learners’ interests and motivation using diverse and creative methods. It should provide different instructional choices that connect to student interests or that encourage peer collaboration. In contrast to typical options such as only reading articles or finishing worksheets, an engaging curriculum should alter the physical environment by including such options as classroom simulations or inviting business and financial service providers to an informational interview session. For example, students could acquire information about saving by playing interactive savings games online, choosing pictures representing savings goals, or working collaboratively with other students on developing savings plans.

Culturally responsive curriculum

Many have written about the importance of culturally responsive instruction and even provided rubrics to evaluate culturally responsive teaching (Abdal-Haqq, 1994; Banks, 1997; Gay, 2002, 2010; Lucas and Villegas, 2013; Villegas and Lucas, 2002, 2007). Few provide concrete examples of a culturally responsive curriculum; more common are descriptions of instruction. We focus in this article on the curriculum, the written and visual materials provided to teachers to guide their instruction, of financial literacy. After defining culturally responsive curriculum, we offer examples of what the culturally responsive curriculum might look like in the field of financial literacy education for youth with disabilities.

Given the persistent issue of the disproportionate enrollment of culturally and linguistically diverse (CLD) students in special education, a culturally responsive curriculum is especially relevant (Hosp and Reschly, 2004; U.S. Department of Education, 2015). National reports document four decades of overrepresentation of Latino, American Indian, and African American students in categories such as learning disabilities, cognitive disabilities, and emotional/behavioral disabilities (Hosp and Reschly, 2004; U.S. Department of Education, 2015). To address the disproportionate presence of CLD students within special education, the curriculum design should reflect and respond to the unique facets of culture and community.

The culturally responsive curriculum should identify the differences between the school and the student’s cultural background, and as the nature of the term “responsiveness” suggests, attend to distinctive cultural backgrounds by actively addressing those needs, and adjusting instruction in response to such needs (Espinosa, 2005; Klump and McNeir, 2005). In essence, the culturally responsive curriculum explicitly bridges the gap between a student’s home and the community culture. This means that the curriculum would incorporate information relevant to the student’s family and community in the content presented (Villegas and Lucas, 2002). The financial literacy curriculum that is culturally responsive would include content on home insurance as well as renter’s insurance and validate that renting a home is sometimes a better choice than buying a home. When working with budgets, the culturally responsive curriculum might include different examples of family structures in creating budgets. The more the curriculum provides avenues and supports for students to share with others in their class about their family and community values related to finances, the more culturally responsive we would rate it.

The curriculum should create a learning environment steeped in connections to students’ cultural contexts (Belgarde et al., 2002). Basing their description of the culturally responsive curriculum largely on Abdal-Haqq (1994), Klug and Whitfield (2003) stated, “Curriculum that is culturally responsive capitalizes on students’ cultural backgrounds rather than attempting to override or negate them” (p. 151). The culturally responsive curriculum should depict multiple views of reality, everyday life examples that are connected to students’ experiences within their family, culture, language, and community (Villegas and Lucas, 2002, 2007). For example, when teaching the concept of saving, the culturally responsive curriculum might suggest that saving for a quincenera (celebration of a young women’s 15th birthday) or a visit to the extended family in another country would be examples of savings goals. Students with emotional and behavior disabilities may benefit from explicit curricular resources teaching ideas of delayed gratification and persistence in meeting their savings goals, and stories of diverse figures who have demonstrated those skills should be included in the culturally responsive curriculum.

Furthermore, the culturally responsive curriculum can be viewed as a person-centered approach to pedagogy (Pewewardy and Hammer, 2003) that, as described by (Belgarde, Mitchell, and Arquero, 2002) “generally validates the cultures and languages of students and allows them to become co-constructors of knowledge in the school setting” (p. 43). Content and materials should acknowledge and embrace who students are and where they come from. For example, the curriculum should be presented in multiple languages. It should reflect different cultures and incorporate students’ personal stories and experiences as they learn about financial literacy. The culturally responsive curriculum encourages CLD students to discover who they are, as opposed to being forced into the mainstream curricular dialogue. It should encourage students to develop self-awareness. Fundamentally, the culturally responsive curriculum focuses on authentic content that is student-centered and reflective of the student’s actual life (Chion-Kenney, 1994). When students have the opportunity to create their own savings profile and identify personal savings goals, it would be an example of the person-centered culturally responsive curriculum. A curriculum that included interview guides for students to use in talking with their families about insurance goals would be a culturally responsive curriculum. Similarly, a curriculum that provided structures for students to collect and share family stories about earning income or saving money would also be more culturally responsive.

The culturally responsive curriculum recognizes students’ need to encounter connections among themselves, the topics, and the instruction that is presented within the classroom (Montgomery, 2001). Culturally diverse examples of different occupations that provide income should be affirmed in the culturally responsive curriculum. Migrant labor, manufacturing, and entrepreneurship should all be acknowledged and affirmed. Reasons for earning income, such as helping with family expenses, paying for a trip to an amusement park, or buying fashionable shoes, would all be culturally responsive examples which might be included in the curriculum.

The culturally responsive curriculum should help students achieve higher order knowledge and skills (Gay, 2010; Klump and McNeir, 2005; Pewewardy and Hammer, 2003). That means the curriculum must scaffold content and resources so that students can proceed through the materials regardless of their starting point. Scaffolding is good for all learners, but especially CLD students and youth with disabilities (Villegas and Lucas, 2002). Students need scaffolds to develop critical thinking skills to make complex decisions. Examples of scaffolds that might be found in the culturally responsive curriculum would be graphic organizers to help learners organize their ideas, sequenced directions for varying levels of challenging tasks, and providing multiple options to students for discovering concepts or applying skills. Youth with special needs deserve a curriculum that includes more supports than just fill-in-the blank worksheets. An example of a financial literacy topic that requires critical thinking and scaffolding for CLD students is choosing health insurance. This life skill takes practice and guidance in order for youth to eventually be able to complete this task independently. Navigating the Healthcare Exchange requires the ability to compare and contrast, and students would benefit from graphic organizers to help with this task.

Selective review of financial literacy curriculum for students with special needs

Five specific promising curricula that are web-based and/or easily available to teachers and students were reviewed. Notes about each curriculum are included in Tables 1 to 5. These curricula were selected based on principles of universal design (CAST, 2011) and the recommendations of Caniglia and Courtney (2013). The curricula are further discussed in Henning and Johnston-Rodriguez (2018).

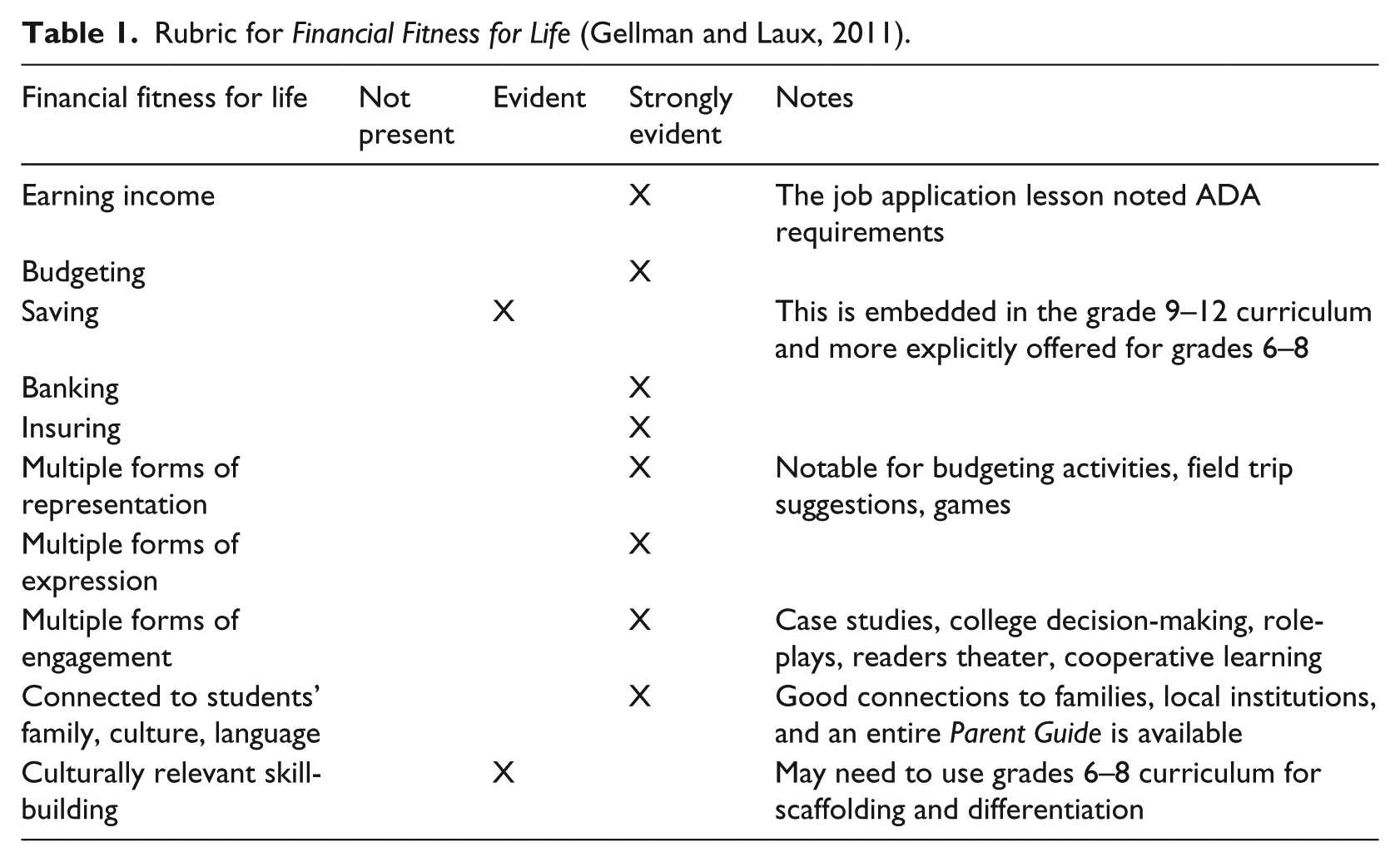

Rubric for Financial Fitness for Life (Gellman and Laux, 2011).

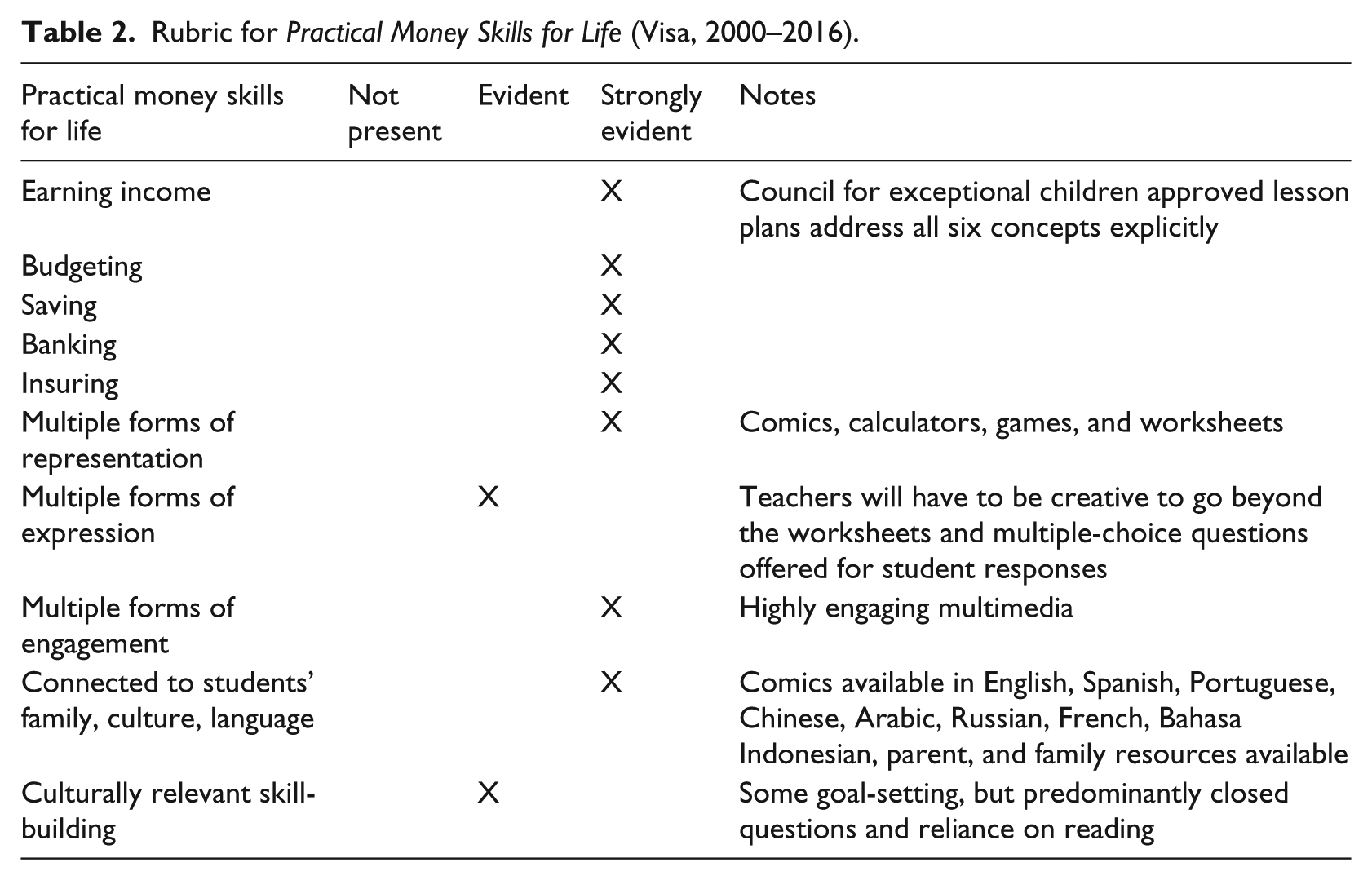

Rubric for Practical Money Skills for Life (Visa, 2000–2016).

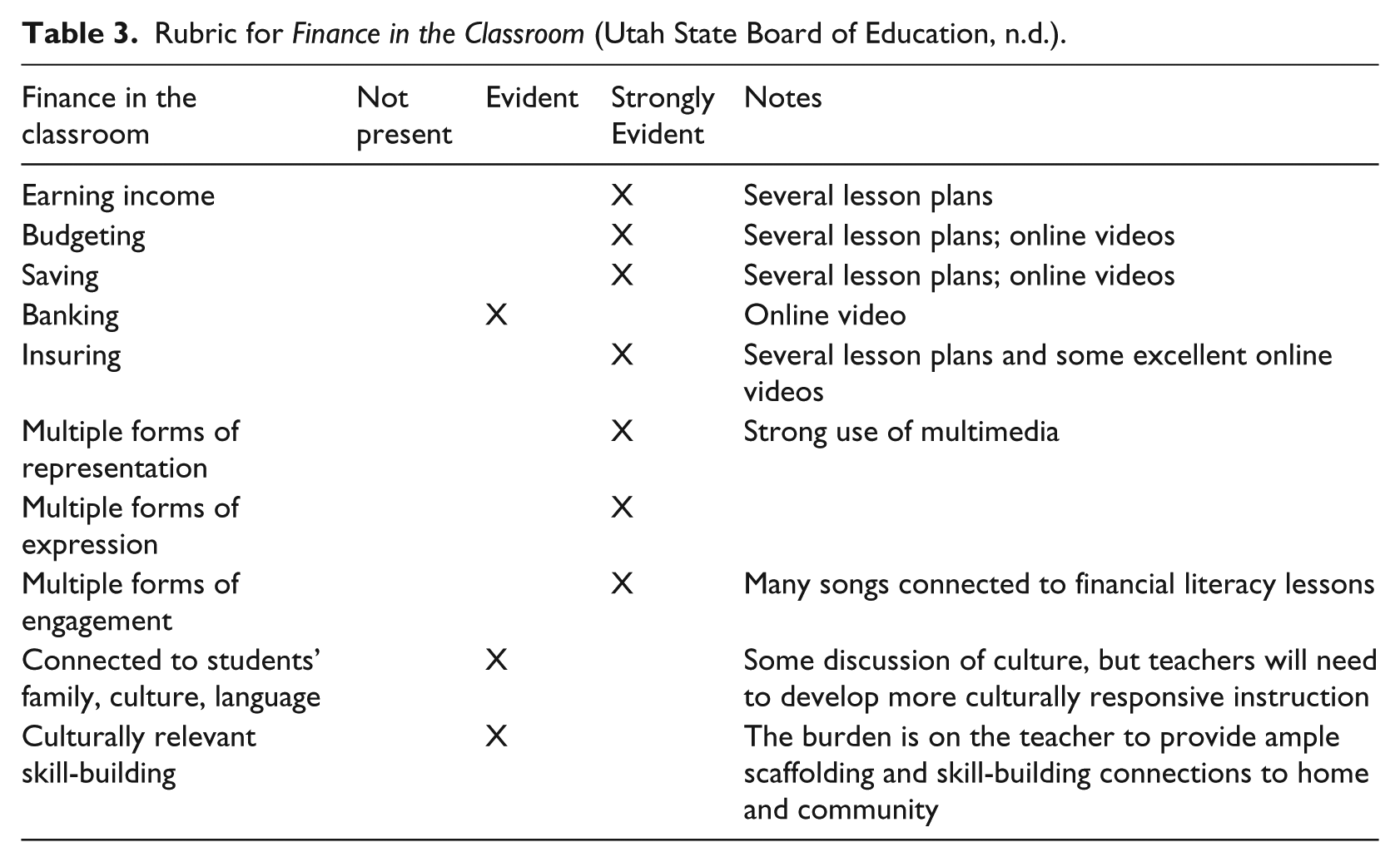

Rubric for Finance in the Classroom (Utah State Board of Education, n.d.).

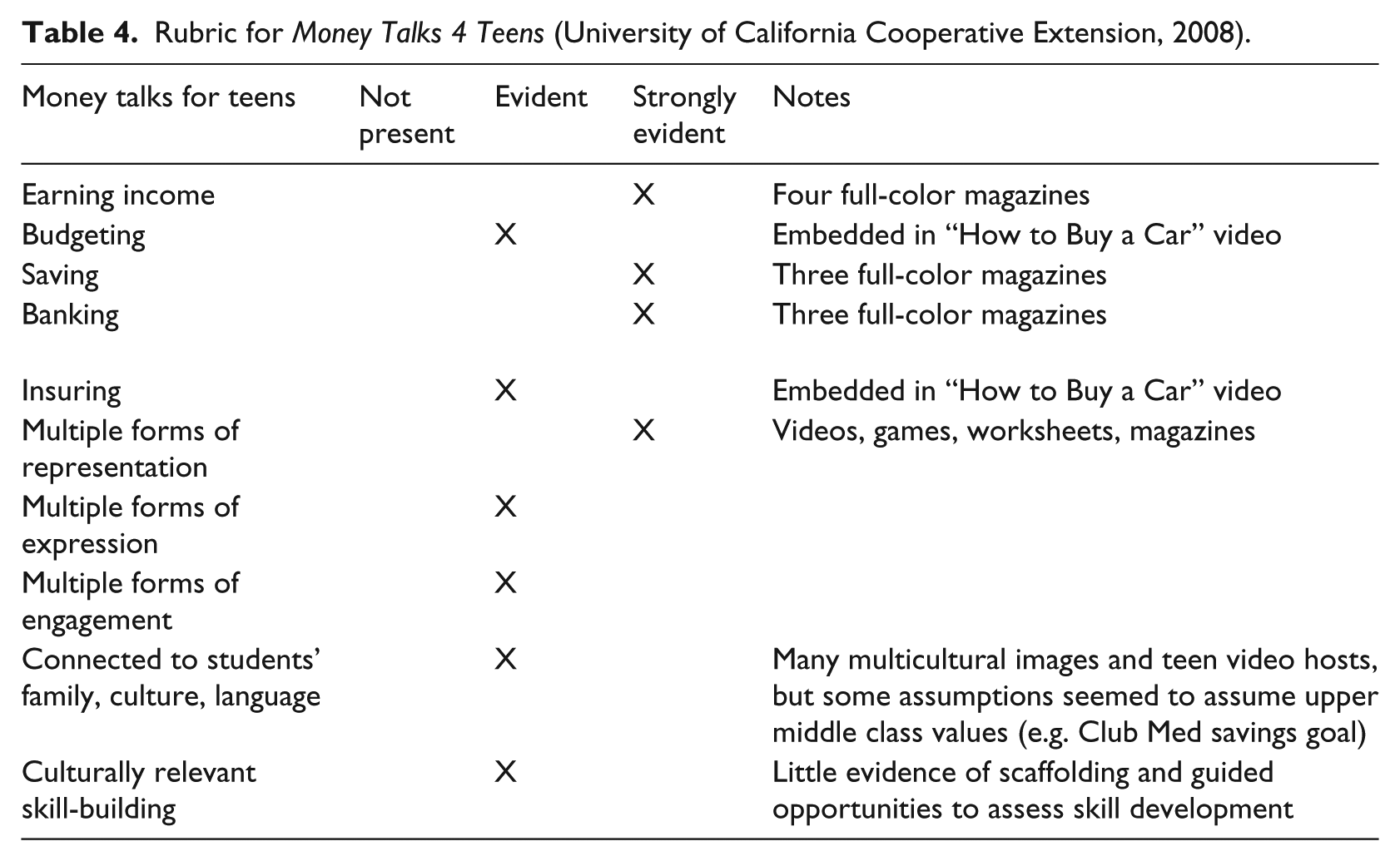

Rubric for Money Talks 4 Teens (University of California Cooperative Extension, 2008).

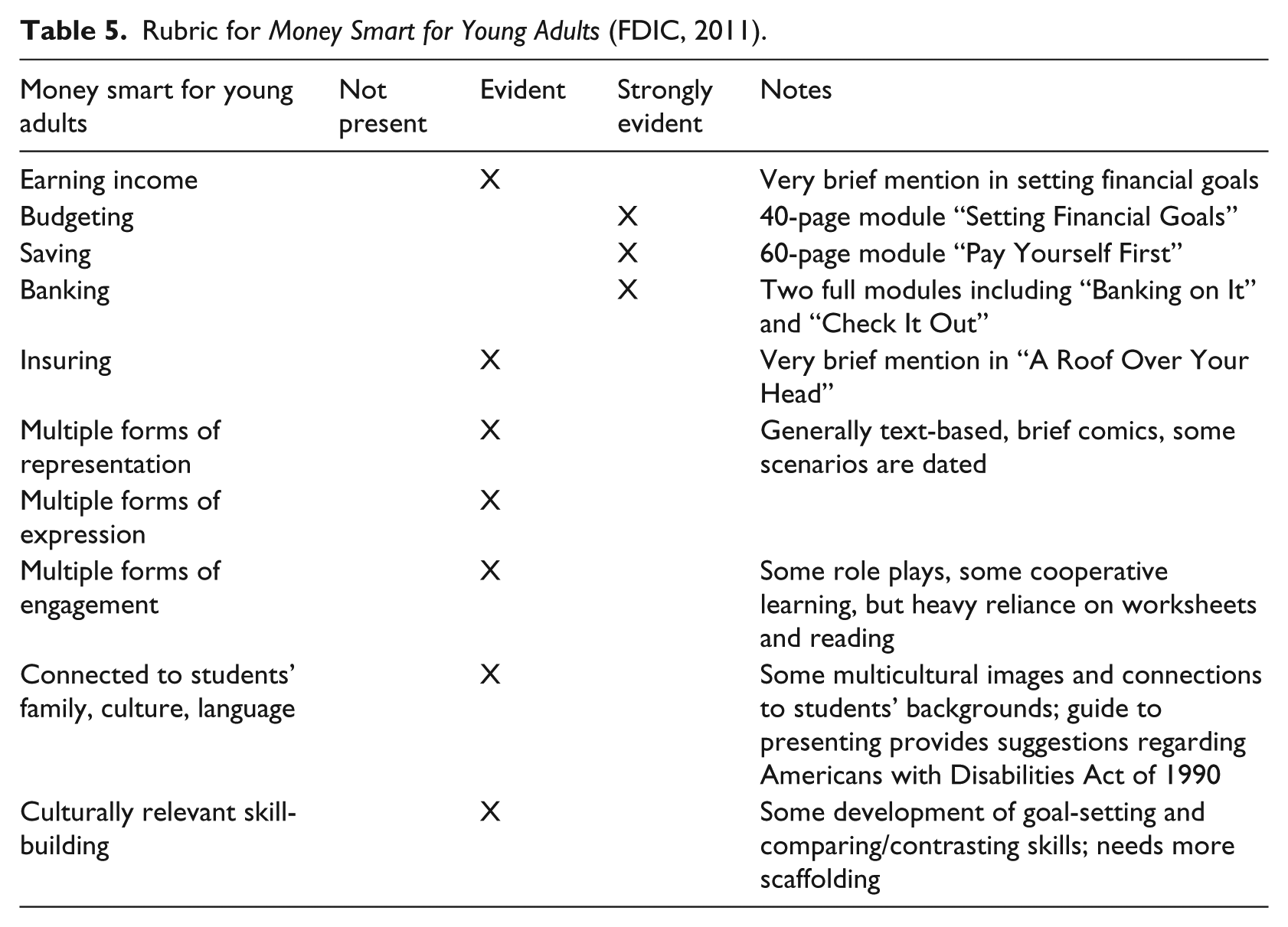

Rubric for Money Smart for Young Adults (FDIC, 2011).

An Associate Professor of Social Studies Education, who specializes in economic curriculum and instruction and an Associate Professor of Special Education, who specializes in transition planning and systematic instruction completed rubrics to evaluate each curriculum. After independently reviewing each curriculum, the two curriculum evaluators triangulated their rubric results and discussed any inconsistencies in their evaluations. Their evaluations of the curriculum matched between 60% and 90% when comparing their rubrics. Discussion to triangulate their evaluations revealed that the economic educator had a more critical approach to evaluating the conceptual focus of the curriculum while the special educator had a more critical focus in evaluating the UDL aspects of the curriculum. This is a strength of the research design.

The first five criteria of the rubrics evaluate the conceptual content of each curriculum. The next three criteria of the rubrics evaluate aspects of the curriculum from a universal design perspective. The last two criteria of the rubrics hone in on elements of a culturally responsive curriculum.

Each of the curricula will be analyzed, in turn, in the following section. We present the curriculum in ranked order for how we evaluated it overall for its usefulness to educators and youth with special needs. The curriculum which we rated most highly, overall, is Financial Fitness for Life (Gellman and Laux, 2011).

Financial Fitness for Life (Council for Economic Education)

One of the best things about Financial Fitness for Life (Gellman and Laux, 2011) is that there are teacher and student workbooks at the K-2, 3–5, 6–8, and 9–12 grade levels. All of the materials cover the same financial literacy concepts, but they are differentiated for each grade span. This allows teachers to select from the 6–8 activities for some groups of students and then use the 9–12 student workbook for other groups of students. Reading levels and conceptual difficulty are already adjusted among the different workbooks for students. The lesson plans and activities included in this curricula were perceived as the most-developed and easiest to implement for special education teachers. Titles of lessons make the conceptual focus evident.

Financial Fitness for Life (Gellman and Laux, 2011) is notable for its integration of the best practices in pedagogy and content knowledge. The hands-on lessons, games, cooperative learning activities, role-plays, readers’ theater, and handouts offer numerous ways to access financial literacy content and skills and adapt to individual learner needs. Of all the curriculum reviewed, the content of this curriculum is probably the most aligned with professional economists’ thinking about financial literacy knowledge. Plus, an extensive network of state (US) councils for economic education and centers for economic education (within most states) offer professional development workshops to teachers wishing to learn more about how to use these materials.

The only two areas on the rubric that did not receive the highest marks for this curriculum were the concept of saving and the inclusion of culturally relevant skill-building. Saving was embedded in two of the grade 9–12 lessons, but it was not taught as explicitly as might be expected for learners with special needs. Teachers could turn to the grade band 6–8 curriculum for savings lessons, but not all teachers would know this or have access to the different grade-level materials. While there were a variety of skill-building activities for most of the concepts, these were not always presented in a sequential manner that built on diverse cultural background knowledge.

Unlike the rest of the curriculum reviewed in this article, the Financial Fitness for Life (Gellman and Laux, 2011) materials are not available entirely at no cost to all. Teachers may be able to receive the student workbook, teacher guide, and a flash drive with all the materials if they register for a professional development workshop offered by the Council for Economic Education (CEE) or one of the state or regional centers of economic education affiliated with the CEE. All of the visuals from the teachers’ guides for Financial Fitness for Life are available at no cost on the CEE website (http://councilforeconed.org/resource/financial-fitness-for-life-grades-9-12/). Otherwise, these materials can be purchased from the online store at the CEE website (http://store.councilforeconed.org/t/categories/financial-fitness-for-life/s/ascend_by_name). Student workbooks cost US$14.95, teacher guides cost US$33.95, and a full package of materials for teachers (including a flash drive) costs US$93.95.

Table 1 summarizes the evaluation of Financial Fitness for Life (Gellman and Laux, 2011). Notes of particular importance are included for some of the criteria.

Practical money skills (http://www.practicalmoneyskills.com/)

This is the most engaging multimedia curriculum reviewed (Visa, 2000–2016). Visa provides a curriculum portal full of excellent resources that are very accessible to youth with disabilities. Comic books in full color that quickly download or project on screens can be read in seven different languages. Avengers Saving the Day teaches banking and budgeting through a story featuring familiar superheroes such as Spider-Man, Iron Man, Black Widow, and Thor. The Guardian of the Galaxy comic, created in 2016, is highly engaging while teaching key concepts of earning income, saving, and budgeting. More knowledgeable teachers will want to avoid the activity on the last page of the comic book asking students to distinguish between wants and needs. Gallagher and Hodges (2010) have an excellent article explaining why economists do not recognize the concept of “needs” and instead focus on prioritizing choices among different “wants.”

Financial Football and Financial Soccer are both online games within the Practical Money Skills portal which challenge students to answer multiple-choice questions (at differentiated skill levels) in order to move down the playing field. Realistic graphics, music, and National Football League (NFL) and FIFA (Federation International of Association Football) logos make the games fun. Lesson plans, modules, and downloads or CDs of the games allow teachers to customize their students’ experience.

A search of this website for “special needs” will glean many useful articles for families and teachers, including spotlights on innovative educators who are using this portal to teach young adults with disabilities. An entire section of the website (https://www.practicalmoneyskills.com/foreducators/lesson_plans/special.php) is devoted to lesson plans that are approved by the Council for Exceptional Children, the major professional organization for special educators in the United States, targeted for young adults with learning disabilities. Although the website was created by Visa, it does not appear to be biased toward credit usage, and the corporate sponsorship may be what allowed funding for such engaging graphics and games. This curriculum is most notable for its multiple means of representation and engagement. Students who love comic books or online games will find this curriculum compelling. Teachers will have to create some of their own scaffolding in order to take their students from “fun” games to applying their understanding of the knowledge they learn on this website.

Table 2 summarizes the evaluation of Practical Money Skills for Life (Visa, 2000–2016). Notes of particular relevance to this curriculum’s components are included for some of the criteria.

Finance in the Classroom (Utah State Board of Education) (http://financeintheclassroom.org/)

The teacher resources on this website are notable for short book reviews, online videos, songs, PowerPoints, lesson plans, and reviews of financial apps. Some of the videos are accessed more easily by Utah educators, but many are freely available online. This website is fairly easy to navigate and includes many lesson plans and activities for K-12 students. Lesson plans are correlated to standards in social studies, language arts, or mathematics. Parent resources are also included. The curriculum includes a plethora of multimedia options and a variety of means of representation and student engagement. Student resources include a huge number of online calculators (to calculate insurance, investments, benefits, retirement, and savings goals). The printables under student resources may be especially applicable to students with special needs. Budgeting, cheap dates, and many worksheets related to earning income are relevant to youth transition plans. Teachers may need to supplement with more culturally diverse examples and scaffolding depending on individual student learning needs and cultural background.

This website provides fewer scripted lesson plans than some of the other curriculum reviewed. But, for a teacher looking for multiple means of representing a concept, especially using songs, phone apps, or videos, this is a great resource. Table 3 summarizes the evaluation of Finance in the Classroom. Notes of particular importance are included for most of the criteria.

Money talks for teens (http://moneytalks4teens.ucanr.edu/index.cfm)

The Money Talks for Teens (University of California Cooperative Extension, 2008) website provides links to pdfs for teen guides, which are magazine-like newsletters that can be used to teach about budgeting, banking, credit, and working. Short videos featuring multicultural young adults present engaging overviews of how to buy car or save money to make dreams come true (University of California Cooperative Extension, 2008). But the “How to Buy a Car” video suggests relying upon parents to get cheaper insurance rates, perhaps unrealistic for some students. The “Making Your Dreams Come True” video suggests goals like going to Club Med or Hawaii, which might be out of reach for many populations. The games offered on this website are less glitzy than Practical Money Skills offerings, but the online games offer a good place to start for students needing to learn some of the more rudimentary skills of how to select an ATM (automated teller machine) or make healthy inexpensive grocery store purchases within a budget. An online Jeopardy game reviews banking. An Expense Station game allows players to create a budget considering many realistic expense choices. Students can choose to play the game with the status of single parent with a child, which includes variables like receiving welfare, food stamps, earned income credit, and a child care subsidy while taking GED (General education development) classes. Teachers seeking different means of representation and some engaging activities specifically targeted to low-income families will find this website worth accessing.

The “Related Links” tab for teachers and teens has resources targeted especially to Californians, although some links are broken. This portal does not include many resources for encouraging multiple means of assessing students’ knowledge, other than online game playing and some worksheets included with the magazines. The burden will be on teachers to create lessons around some of the helpful resources that are assembled here.

Table 4 summarizes the evaluation of Money Talks 4 Teens. Details are included for many of the criteria.

Money smart for young adults (https://catalog.fdic.gov/store/youth)

A participant guide and teacher guide are scripted, making it easy to teach directly about topics such as using a check book, protecting against identity theft, and selecting a bank (FDIC, 2011). The concepts of budgeting, saving, and banking are taught very explicitly in modules that contain so much current material that teachers can pick and choose from the resources to best serve their students. Multiple-choice assessments, PowerPoint slides, role-plays, and other activities are included in this curriculum. Worksheets to compare banks and practice using a check register are notable. IDAs are mentioned in the “For Further Information” section of several modules, and they are explained briefly in the “Pay Yourself First” module. The module “A Roof Over Your Head” explores the details of home buying versus renting. Teachers may find the level of detail in some of the modules (such as “Borrowing Basics”) to be more than necessary for the students in their classes. Some of the scenarios which can be completed online look a little dated in their graphics.

The saving module makes the error of referring (like some of the Visa materials) to needs versus wants. Again, informed teachers know that economics is more about making choices among wants than about the unclear and often culturally biased definition of a need. Teachers wanting plenty of scripted instruction, as well as cooperative learning activities and different multiple-choice assessments will appreciate this curriculum. The pretests and posttests for each module are notable.

This curriculum can be ordered at no cost as a CD or downloaded from the Internet. There are eight different modules, including ones that focus on banking, checking, saving, and borrowing. Downloading the modules takes a bit of time (setting up an account, unzipping multiple files), but if the CD is ordered (arriving in about a week), it is easy to open all the materials.

Table 5 summarizes the evaluation of Money Smart for Young Adults (FDIC, 2011). Notes explicate some of the criteria on the rubric.

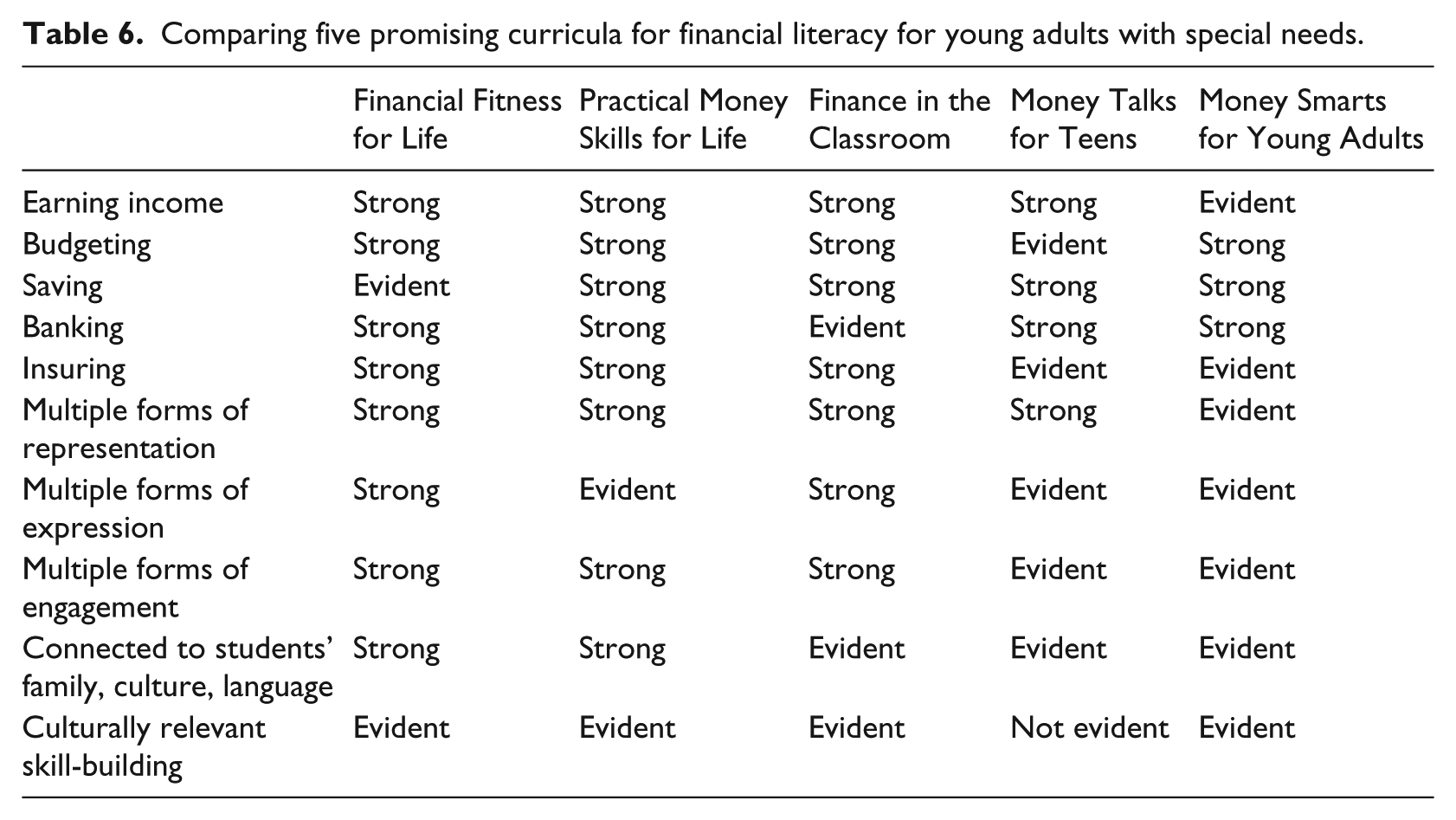

A comparison of all five curricula

Each of the curriculum reviewed includes helpful resources we would recommend to financial literacy educators. Table 6 summarizes how the curricula compare. The curriculum is presented in the order of the greatest number of strengths, which also reflects our holistic evaluation of the curriculum. As the summative table shows, all the curricula could be enhanced by more attention to culturally relevant skill-building.

Comparing five promising curricula for financial literacy for young adults with special needs.

Financial Fitness for Life (Gellman and Laux, 2011) is the strongest, overall, for its attention to universal design in its well-developed lesson plans. Practical Money Skills (Visa, 2000-2016) is most noteworthy for its explicit coverage of key concepts in financial literacy. Finance in the Classroom (Utah State Board of Education, n.d.) also scored very well in its attention to universal design. Teachers looking specifically for full-color free resources to distribute to their teens on earning income, saving, and banking will find Money Talks for Teens (University of California Cooperative Extension, 2008) most useful. Teachers wanting well-developed modules with pre- and posttest assessments for budgeting, saving, and baking, may favor Money Smart for Young Adults (FDIC, 2011). Because most of these resources are available at no cost, teachers can combine resources from multiple financial literacy curricula in order to tailor their curriculum to the needs of their own students.

Conclusion

All financial literacy curricula have some limitations (Willis, 2008). Teachers need to be aware of the cultural relevance, accuracy of content, and how current the materials are. Each of the curricula reviewed in this article offer some culturally responsive materials combined with some excellent content relevant to youth with special needs. The materials reviewed provide strong resources for an individualized approach for financial education for students with disabilities, based on current economic and sociocultural factors. Given the risks that students with special needs have when it comes to achieving financial independence, the curricula reviewed go a long way toward meeting transitional goals and IEP planning. Because most of the materials are freely available online, teachers can pick and choose from the various resources to meet the needs of their classes.

We encourage more educators of students with special needs to review these curricula, as well as others that are available to teach financial literacy. We have found no other rubric that specifically reviews financial literacy curriculum for its strength in meeting both UDL and Culturally Relevant Curriculum goals. We shared this rubric for classroom teachers, banking professionals, and special educators to use as a starting point. Future researchers may refine this rubric to better match their understanding of the requirements for a financial literacy curriculum for students with special needs in their own contexts. Those with different experience and expertise may also rate the same curriculum differently. Future research would be especially helpful on how the financial literacy curriculum meets the needs of students with low incidence disabilities. We invite others to join efforts to improve the financial literacy resources for youth with special needs.

Footnotes

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.