Abstract

In recent years, the financial education of young adults has gained importance in Germany; however, very few valid test instruments to assess the knowledge and understanding of personal finance are suitable for use in Germany. In this article, we describe results of a survey in which experts in Germany in areas related to personal finance judged the relevance of the items of the American Council of Economic Education’s Test of Financial Literacy for use in Germany. Overall, they found the German version of the Test of Financial Literacy to be a valid instrument for assessing the knowledge and understanding of personal finance of young adults in Germany. Also, we conducted cognitive interviews with young adults in Germany to identify the sources of their knowledge of personal finance. Most of the participants claimed they gained a significant amount but not the majority of their knowledge and understanding of personal finance through formal school education. We conclude that personal finance should be addressed more thoroughly at secondary schools in Germany

Keywords

Relevance and research questions 1

For many years, the Government of Germany has financially taken care of its elderly people. For example, the current public pension system in Germany is based on what is referred to as the intergenerational contract, according to which the working population pays for social security and thereby guarantees the financial security of the retired population. With an aging society, however, the effectiveness and fairness of the intergenerational contract model need to be questioned as the working generations eventually may not be able to manage the financial burden of the older generations. In the current public debate, it becomes apparent that people living in Germany need to take more personal responsibility for their financial security in old age. However, now there are many more financial products available to individuals, indicating that over the past several years financial decision-making has become increasingly complex. Young adults who have graduated from secondary school and are beginning higher education studies have to make many important financial decisions for the first time in their lives (e.g. how to pay for their tuition and accommodation).

One way the Government of Germany could help individuals take initiative and make sound decisions regarding retirement savings to ensure financial topics are addressed more intensively at secondary school. However, some scholars in the field of financial education do not agree with this solution and have cogently argued that championing personal responsibility and developing financial knowledge as solutions to increased financial risk and responsibility is problematic. 2 The transfer of financial risk and responsibility to individuals is a political decision which will benefit some and disadvantage others. Some scholars criticize that teaching disadvantaged groups how to save better and invest (money they do not have) will not result in less financial risk. For example, the answer to the question as to how to secure retirement for all may be public provision. These valid arguments show the importance of political decisions on the financial well-being of people. Nevertheless, governments currently can contribute to better financial decision-making by helping their people develop financial knowledge.

Unfortunately, there are very few valid instruments for assessing the knowledge and understanding of personal finance of this age group in Germany. In this article an adaptation of the American Test of Financial Literacy (TFL; Walstad and Rebeck, 2017; TFL-G: German version of TFL; Förster et al., 2017) was used for assessing the knowledge and understanding of personal finance for this target group. When adapting the TFL for use in Germany, content-related validation was essential to ensure that the original American content was relevant for test-takers in Germany. Researchers quite rightly have pointed out that knowledge of personal finance is a construct shaped by culture (Schuhen and Schürkmann, 2014: 9).

3

Thus, the adaptation of the TFL for use in Germany involved translating the items into German, modifying the content of the items to reflect German culture, and ensuring the items were financially relevant for young adults in Germany. This elaborate validation process should allow accurate conclusions to be drawn from the test results and inferences to be made regarding the knowledge of personal finance of young adults in Germany. In the internationally established Standards for Educational and Psychological Testing (AERA et al., 2014), five categories are defined: test content, response processes, internal structure, relations to other variables, and consequences of testing. Test content must be analyzed to determine how accurately the test represents the theoretical construct. One way to do this is to ask experts to evaluate how the test content relates to the content of the respective field of study. To determine whether the items on the TFL-G truly assess the knowledge that young adults in Germany need to be able to make sound financial decisions, experts in related areas were asked to judge the suitability of the set of items of the TFL-G (AERA et al., 2014: 12):

4

According to expert ratings, how relevant are the items on the TFL-G for young adults in Germany? (Question 1)

If the experts agree that the test instrument is suitable for assessing the knowledge of personal finance of young adults in Germany, we are interested in identifying the source of young adults’ financial knowledge, which they needed to be able to respond correctly to the items on the test instrument (see evidence of validation based on response processes, AERA et al., 2014: 15). Currently, little is known about whether the knowledge and understanding needed to respond correctly to items concerning financial decision-making is taught sufficiently at school or whether it is acquired elsewhere. Personal finance is not taught systematically as part of the school curricula in Germany (Kaminski and Friebel, 2012: 45; Retzmann and Seeber, 2016: 9). We analyzed some school curricula in Germany and found that in the regular schools only some finance-related topics were addressed (Happ and Förster, 2017), whereas, in schools specializing in business (Wirtschaftsgymnasium), topics related to business and economics were given much more attention. Furthermore, Germany is well known for its dual vocational education program.

5

Analysis of the curricula of vocational schools revealed that more weight was given to financial content than in both of the aforementioned types of school. During cognitive interviews, we asked students whether they felt that they received in-depth education in financial matters at school or whether they acquired their financial knowledge from other sources to determine whether there is a gap between the official curriculum and what actually is taught at school. Cognitive interviews were conducted to answer the following question: Do young adults in Germany acquire the financial knowledge needed to respond correctly to the items on the TFL-G mainly at school or elsewhere? (Question 2)

In the section “The Test of Financial Literacy,” we review the various studies, conducted in Germany, of financial literacy and the underlying constructs and tests used therein, and we present the content of the TFL-G. In the section “Results of the expert interviews concerning relevance of items on the TFL-G,” we examine results from the interviews with experts and data from an online survey completed by these experts to answer our first research question. In the section “Sources of knowledge of personal finance,” we present the procedure and results of the cognitive interviews we conducted with test-takers upon learning from the experts that the TFL-G covers important content of financial knowledge. Finally, in the section “Implications and limitations,” we discuss the results and new issues to be investigated in further studies.

The Test of Financial Literacy

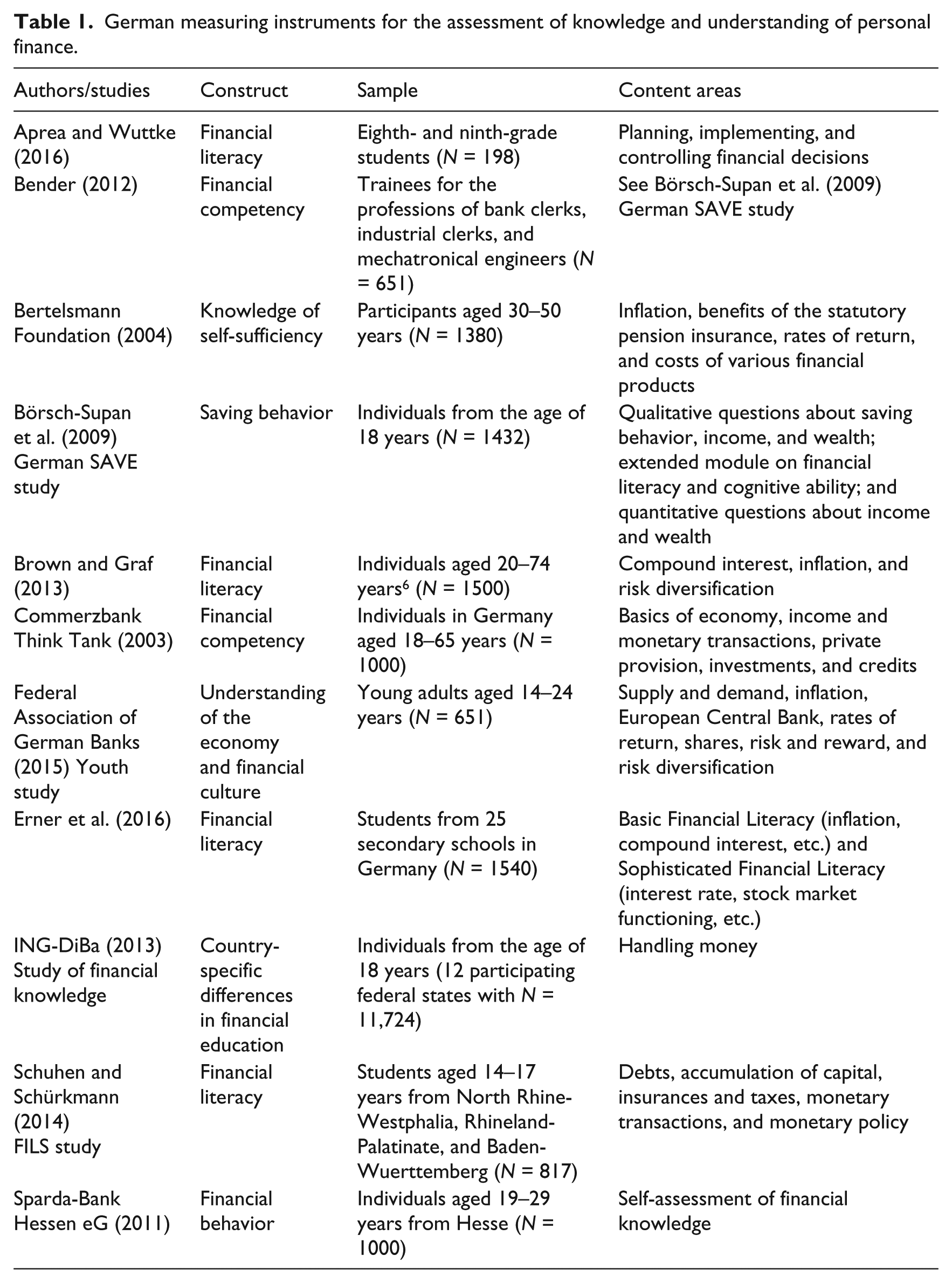

Table 1 shows that diverse approaches to the conceptualization of the construct of financial literacy can be found in the literature (Schuhen and Schürkmann, 2014). Focus in this article is on the cognitive component of financial literacy, that is, on knowledge and understanding of personal finance (Förster et al., 2017; Walstad and Rebeck, 2017).

German measuring instruments for the assessment of knowledge and understanding of personal finance.

In only a few studies were knowledge and understanding of personal finance explored holistically. Moreover, it becomes evident that in addition to using test instruments, self-assessments were used to determine respondents’ level of financial knowledge. It can be criticized that, in the aforementioned studies conducted by large banking institutes (Commerzbank Think Tank, 2003; ING-DiBa, 2013; Sparda-Bank Hessen eG, 2011), quality criteria and aspects of validity (see AERA et al., 2014) were not disclosed. Also the banking institutes focus mainly on content areas dealing with financial products, limiting the content for the assessment of knowledge of personal finance on the whole. Ostensibly, there are very few validated instruments suitable for measuring the financial knowledge of young adults. Erner et al. (2016) developed a measuring instrument and administered it to tenth-grade students. The instrument was an adaptation of Lusardi and Mitchell’s (2009) instrument, and it was further adjusted to include content from Mandell’s (2008) instrument and the instrument used in the Programme for International Student Assessment (PISA) study 2012. Erner et al. (2016) followed a procedure comparable to those of Börsch-Supan et al. (2009) and Brown and Graf (2013), who also took the American Health and Retirement Study (HRS) (Lusardi and Mitchell, 2009) as a basis for their test development. We chose to administer the TFL-G to measure young adults’ financial literacy in Germany because it covers the essential finance-related content.

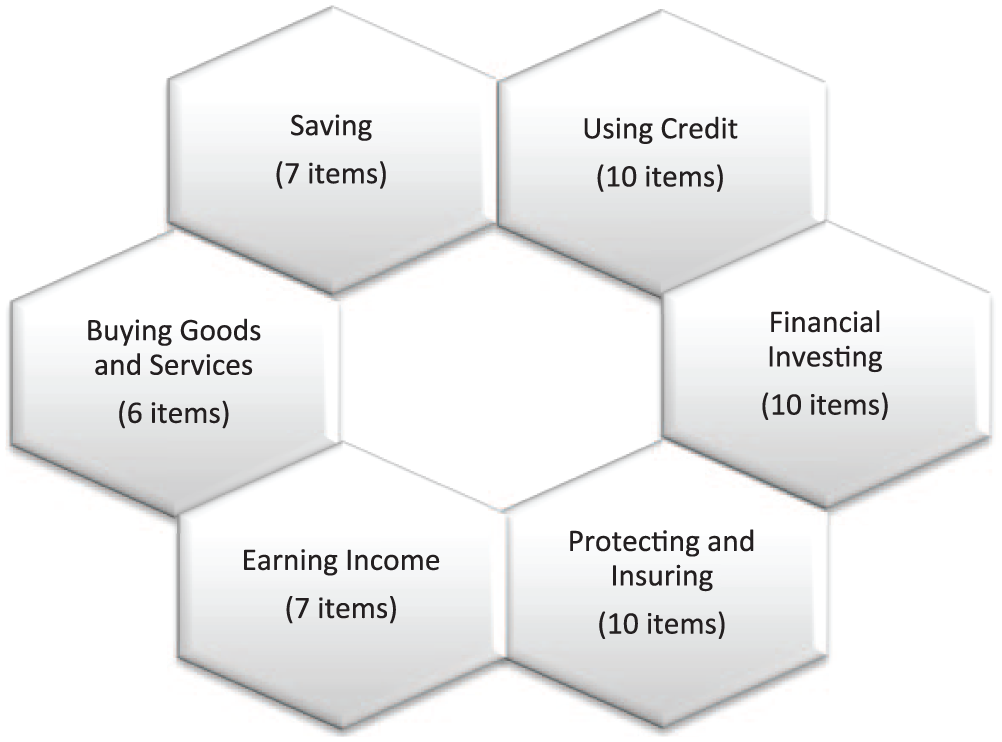

The original English version of the TFL was developed by the Council for Economic Education (CEE) to enable teachers to determine their students’ knowledge and understanding of personal finance (Walstad and Rebeck, 2016: iii). The TFL was designed for eleventh- and twelfth-graders, and its content is in line with the CEE’s (2013) National Standards for Financial Literacy. These standards define benchmarks for the following six areas (see Figure 1):

Content areas of the TFL with the number of items in the pretest.

The items on the TFL are in multiple-choice format, whereby after a short description of a situation, the respondent must choose the one correct answer from four alternatives presented (Walstad and Rebeck, 2017). In its first application in 2015, the TFL consisted of 50 items. These items were made available to the researchers in Mainz (Germany) (Förster et al., 2017). 7 To answer the two research questions in this study, it is crucial that the content covered in the six areas be clarified. In the following, according to the CEE’s standards, a concise description is given:

1. Earning income

Various sources of income exist (salary or wages, pension, capital gain, etc.), however, for most people the majority of income comes from salaries or wages. In this case, the level of income is determined by the market value of their work, and this is dependent on individual factors of the employee, for example, job skills, education, and work experience. 8 In this content, area costs and benefits of traineeships and the effect of taxes on income are discussed.

2. Buying goods and services

People can buy goods and services but with specific restrictions, for example, their income. Thus, when making a purchase, they have to choose between various goods and services and consider costs. A good basis for making purchase decisions can be created through the collection of information, adequate planning, and budgeting. Protection of consumers exists through various institutions (e.g. consumer advice centers) and laws.

3. Saving

People may choose to set aside earned income to increase their benefits in the future, for example, to be able to afford more expensive goods. Over the course of a lifetime, there are different options for saving. People choose different ways to save depending on their individual savings goals and the amount of income they have to spare. The value of savings is influenced in part by the duration of an investment, interest rates, and inflation.

4. Using credit

Taking out a loan allows the borrower to buy goods and services today and pay for them in the future in installments that include interest and amortization fees. Thereby, the interest due is the price the borrower pays for the funds provided. Based on the borrower’s credit history and the expected creditworthiness, lenders decide whether to approve or deny a loan. The interest rates can vary from borrower to borrower. Borrowers with a lower default risk get a lower interest rate than borrowers with a higher default risk.

5. Financial investing

A financial investment is the investment of money in financial assets to increase future wealth. The decision to invest is based on various criteria, for example, risks and expected rates of return. Higher rates of return often are accompanied by greater risks. Through diversification of risks into different assets, the risk of an investment can be reduced.

6. Protecting and insuring

People make choices about the protection of their income, health, and assets to protect themselves from loss. It lies at their own discretion to accept risks, reduce them, or transfer them to others. The function of a liable third party can, for example, be assumed by an insurance company, which covers various risks for a fee paid in advance. The insurance company’s fee for such protection is influenced by the consumer’s lifestyle and behavior.

Results of the expert interviews concerning relevance of items on the TFL-G

Selection of experts and interview procedure

To evaluate the relevance of the items on the TFL for young adults in Germany (Question 1), a survey was conducted with field-related experts in Germany who determined the relationship between the content of the TFL-G and the construct (knowledge and understanding of personal finance) (AERA et al., 2014: 14). In the development of the original TFL, experts in the United States contributed to the development of the test instrument; however, they gave little indication as to whether the items on the test corresponded with school curricula in the United States. During our interviews, the experts in Germany analyzed the content of the translated and adapted German version of the test instrument. 9 When selecting experts, we chose those who were qualified to evaluate the validity of the content of the measurement instrument, meaning they had sufficient professional experience (see Meuser and Nagel, 2009; Welch et al., 2002) and daily contact with young adults, which enabled them to provide important insight concerning the appropriateness of the test items for assessing the knowledge of personal finance of young adults. We conducted interviews with 10 experts in various field-related professions: 3 from the private banking sector and the central bank of Germany, 2 student liaison officers for social and financial issues, 1 consumer advice center worker, 1 representative from an insurance company, 1 debt counselor, and 2 teachers (see Förster et al., 2017: 126; Rothweiler, 2016: 35–38). To be able to conduct an analysis of the content validity of the items on the TFL-G, partly standardized, guideline-based interviews (Fowler and Mangione, 1990) were conducted with experts who then completed an online questionnaire.

1. Expert interviews:

Expert interviews are considered an effective way to gather expert knowledge (Meuser and Nagel, 2009: 17). Guidelines were prepared for, and followed by, interviewers. First, experts were asked which content areas they would describe as important for financial literacy in order to ascertain the experts’ concepts of knowledge and understanding of personal finance which are not biased by our concept. Second, the graphic of the six content areas covered on the TFL-G (see Figure 1) was presented to the experts for them to visualize the construct in this study. The experts were asked which of the content areas they would expect to be important. An overview of the content of the items in the single-content areas was given to the interviewer in case the experts had questions about the content areas. This overview was to be consulted only when necessary because the aim of the interviews was to hear the experts’ subjective opinions about the relevance of the items, and supported answers were to be avoided. The interviews were audio-recorded and transcribed using the software program MAXQDA (Gibbs, 2007). Afterward, the interview transcripts were coded in MAXQDA according to a coding scheme (Bauer, 2009). Transcribed passages from the interviews whose content could not be captured in the scheme served as a database for the extension of the coding scheme via a qualitative summarizing content analysis. After coding, the interviews were evaluated through the frequency of individual answers.

2. Online questionnaire:

Following the interviews, experts completed an online questionnaire which allowed them to provide more in-depth analysis of the test instrument at the single item level. The evaluation involved the frequency of content provided in their answers. Due to time constraints, the experts worked on only a few content areas on the online questionnaire. Experts could determine the relevance and specify the level of difficulty of single items in various content areas on the TFL-G. Some questions were standardized with fixed answer categories to allow comparability of the answers and were open-ended to allow the experts to elaborate on how the items could be improved (Lumsden, 2007).

Selected results of the expert interviews

When asked about their understanding of the construct, the experts revealed – as expected – different views according to their profession (Förster et al., 2017: 126). In line with findings in the literature, understanding of the term of knowledge of personal finance varied (Remund, 2010). The experts from the banking sector emphasized a perspective on financial products and managing them. 10 In contrast, the representative from the consumer advice center stressed the rights and awareness of consumers (e.g. in case of a guarantee claim). The different point of views – according to professional background – also is reflected in responses to questions on the online questionnaire. From the responses given during the interviews and on the online questionnaire, it appears that the experts’ understanding of knowledge of personal finance was influenced by their occupational field.

When confronted with the concept of knowledge of personal finance in this study and in the TFL-G, the experts generally agreed with the concept. The single-content areas were, in most of the cases, evaluated as being highly important for young adults by the experts whose profession was closest to the relevant area. So, the level of importance of the content area using credit was evaluated as “very high” by the representatives from the banking sector and by the social counselors for students, whereas the teachers and the representative from the insurance company considered the level of importance of this content area as being “rather high.” 11 The experts came to the conclusion – independent from their professions – that the content areas earning income and buying goods and services had a “high” level of importance. Overall, all content areas were rated by the experts as having at least a “rather high” level of importance, confirming the relevance of the content areas for our sample (see research Question 1). In addition to determining the relevance of the single items in the individual content areas for the 17- to 25-year-olds, the experts rated, on the online questionnaire, the relevance of the items for adults in general regardless of their age. The relevance of the items for both young adults and adults in general did not differ much between the content areas buying goods and services and earning income (both evaluated as “high”). In the areas saving, financial investing, and protecting and insuring, the relevance of the items for adults in general was rated as greater than for young adults, although the items were already rated as having a “rather high” level of importance for young adults. This is not surprising because young adults are starting to earn money and so questions concerning how to invest or save money are beginning to emerge. When financing their first own residence, they have to inquire about insurances such as personal liability insurance, which often had been arranged and paid for previously by their parents.

During the interviews experts were able to elaborate on young adults’ typical misconceptions surrounding the concept of knowledge of personal finance. Such misconceptions serve as starting points for financial education and need to be identified and addressed to help young adults develop their knowledge of personal finance (see section “Implications and limitations”). The difference between gross and net salary often is not understood correctly (content area earning income). In addition, 6 of the 10 experts mentioned that young adults often make mistakes when judging the risk–return relationship of an investment (content area saving). Thereby, within the statements of the experts, it becomes evident – independent of the content area – that young adults lack long-term planning skills needed for making important financial decisions. The experts reported that young adults prefer taking advice from family members and friends to having a sound knowledge base themselves. The extent to which this impression can be supported by the results of the cognitive interviews is outlined in the section “Sources of knowledge of personal finance.”

Sources of knowledge of personal finance

Interview procedure, items, and respondents

We conducted interviews using the think aloud method with young adults to gain insight into the sources of their knowledge of personal finance (see Question 2) (for details regarding the think aloud method, see Van Someren et al., 1994; for cognitive interviews, see Given, 2008). The realization of the cognitive interviews with young adults using the think aloud method was suitable because the respondents’ cognitive (thinking) processes were revealed (Van Someren et al., 1994). First, the respondents were asked to solve one item on the TFL-G and speak out loud at each step of their thinking process. 12 After solving the item, the respondents then explained where they believed they had gained the knowledge needed to answer the item. These statements were used to filter out categories for sources of knowledge.

For the cognitive interviews, two items from each of the six content areas of the TFL-G were selected for the respondents to answer. The decision to have the respondents answer just two items was made so as to minimize the level of stress for the respondents during cognitive interviews. The cognitive interviews lasted approximately 40–45 minutes each because it is difficult for respondents to maintain attention and concentration over a longer period of time. The selection of items for the cognitive interviews was based on item difficulty, item total correlation, and variance in the single items. A sample was drawn at the beginning of the Winter term 2015/2016 and Summer term 2016 consisting of 1108 respondents aged 17–25 years (Förster et al., 2017). The items chosen for the cognitive interviews were those of average difficulty (0.40–0.70), with a high corrected item-total correlation (>0.3), and a high level of item variance (>0.2) (Rüspeler, 2016: 26–27). 13 Items with these features are, from a test–theoretical point of view, quite representative for the test and therefore suitable for cognitive interviews. The respondents were selected with the help of a qualitative sampling plan (Marshall and Rossman, 2016). Young adults with the following characteristics, as identified through data gathered during the test measurement, were randomly selected:

One male and one female with A vocational training program completed, but no economics class attended in high school; An economics class attended in high school, but no vocational training program completed; Neither a vocational training program completed, nor an economics class attended in high school.

The gender of the young adults has been found in both national (German) (Erner et al., 2016) and international (Atkinson and Messy, 2012) studies to play an important role in the acquisition of knowledge of personal finance. Accordingly, we took this into consideration when selecting the respondents, and we decided to have one male and one female with each of the further characteristics. The respondents were selected according to the formal education they had obtained (see Förster et al., 2017). On the pretest in the Winter term 2015/2016 and Summer term 2016, the respondents were asked whether they had completed a vocational training program and/or had attended a major economics course at secondary school. Respondents for the cognitive interviews could be selected against this background.

Sources of knowledge of personal finance

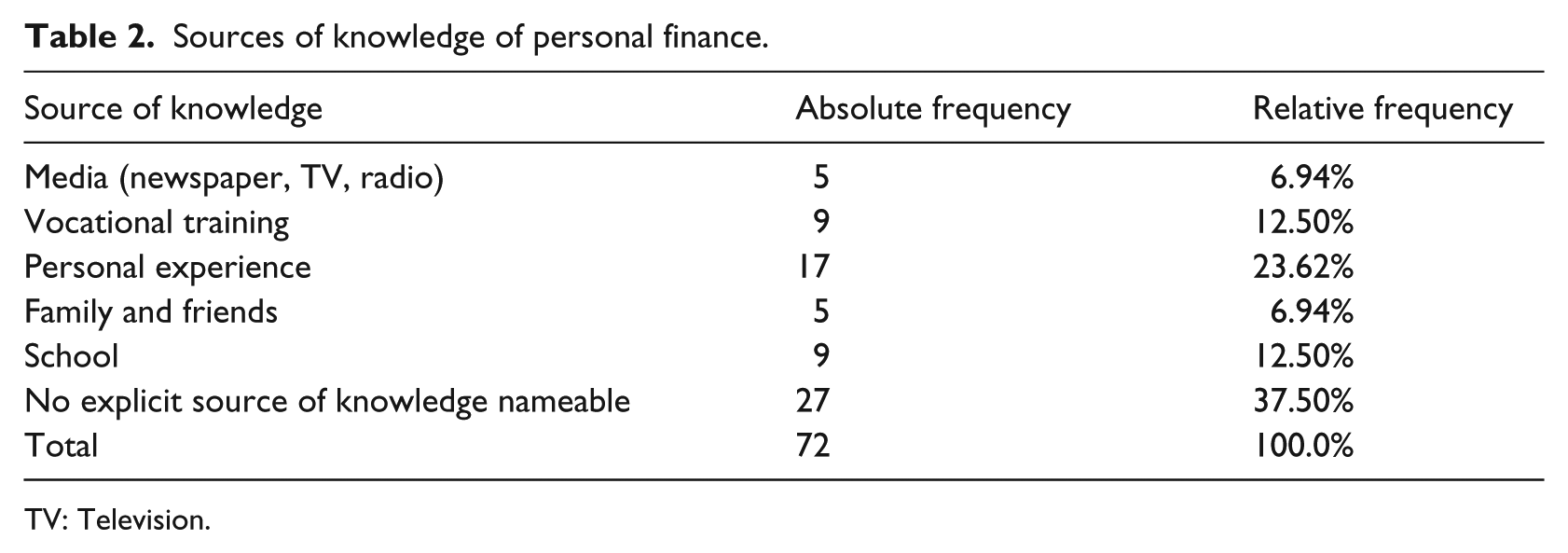

The thought processes spoken out loud by the respondents were audio-recorded and then transcribed to obtain a basic transcription (Given, 2008: 470–471). A basic transcription allows identification of the sources of knowledge from the respondents’ statements and to sort the sources into categories. The categories were created inductively from the data of the basic transcriptions (Du Bois, 1991: 75–81). While coding the categories, it became increasingly obvious which sources of knowledge had been named by the respondents. Our coding procedure shall be illustrated through the following example. A respondent said, “[…] from where I have the knowledge newspaper […].” Accordingly, we established the category media. Additional statements such as, “[…] in TV you always see these great advertisements […]” were then added to this category. Other statements such as, “[…] yes a little bit from previous experience when going to a bank […]” could be assigned to the category personal experience. On the basis of the respondents’ statements during the cognitive interviews, the following six sources of knowledge of personal finance were distinguished (see Table 2):

Sources of knowledge of personal finance.

TV: Television.

Personal experience was by far the most frequently named source of knowledge when answering the items on the TFL-G. The second-most frequently named sources were vocational training and school, which had the same frequency. The categories media and family and friends were the least frequently named sources of knowledge. These absolute frequencies are somewhat distorted since only two respondents had completed a vocational training program and four of the respondents had never had the opportunity to gain knowledge of personal finance by participating in such a program. Therefore, the particular advantage of having obtained vocational training is apparent (see Happ and Förster, 2017).

Yet, the high frequency of statements in which the respondents claimed they could not specify how they had gained the knowledge needed to answer various items correctly on the TFL-G is striking (37.5%). Exemplary statements are “[…] just thought about it […]” or “[…] just logically reflected […].” This category contains mostly statements in which the respondents claimed to deduce answers to the items using logical thinking. Moreover, in this category, statements can be found in which the respondents claimed to have been unsure about the answer and simply guessed the answer.

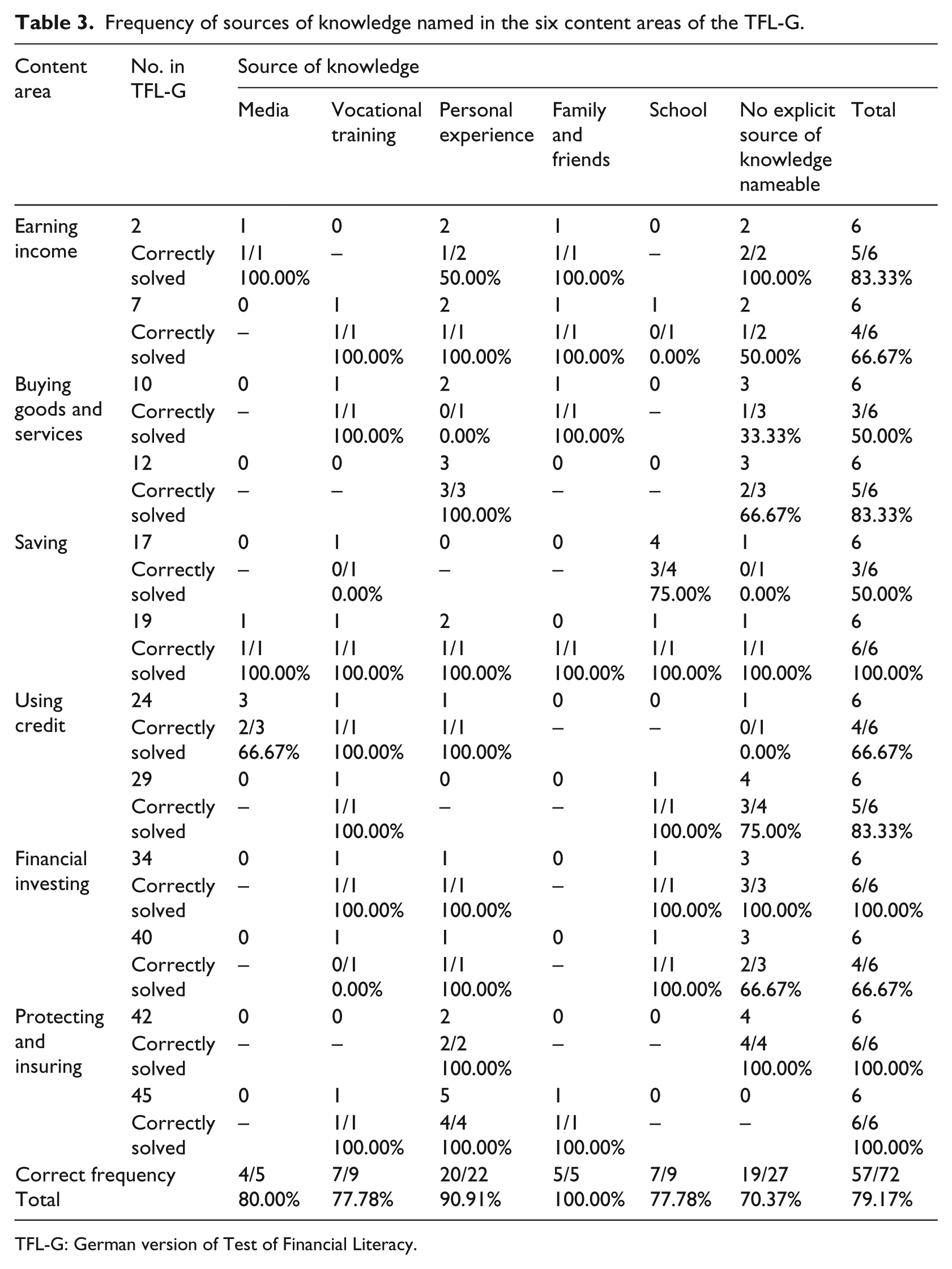

Table 3 gives an overview of the frequency with which the sources of knowledge needed to answer items in each content area on the TFL-G were named. It also shows whether the source of knowledge led to the correct answer to the item.

Vocational training

Frequency of sources of knowledge named in the six content areas of the TFL-G.

TFL-G: German version of Test of Financial Literacy.

It is not surprising that the majority of statements (two-thirds) from the source vocational training reflect the core business of banks (saving, financial investing, and using credit). One respondent had completed a vocational training program as a bank clerk. The other respondent had completed a vocational training as an industrial clerk. Furthermore, it is in line with expectations that not more statements from the category vocational training belonged to the content areas earning income and buying goods and services. Although the young adults earned their first income during their vocational training program and thus had a larger disposable income, these aspects were not sorted into the category vocational training but rather were classified as personal experience. The frequency of a correct answer in the category vocational training was 77.78%, meaning that nearly 80% of the students who acquired (or thought they had acquired) their knowledge during vocational training responded to the items correctly.

2. School

Of the nine statements from the source school, four came from the content area saving. In these cases, the respondents were asked to perform a calculation of an interest rate (including compound interest calculations) for a savings deposit. This item can be solved with strong mathematical skills, which is supported at school. In 77.78% of the statements did school as a source of knowledge of personal finance lead to correct answers to items on the TFL-G.

3. Personal experience

It is striking that personal experience was relatively seldom named as the source of knowledge needed to answer items about saving, using credit and financial investing. This could be because these three content areas are not relevant for young adults at the beginning of their studies. 14 No respondent reported having taken out a student loan, which might have been reflected in responses to items in the area using credit. On the contrary, personal experience often was mentioned as the source of knowledge needed to answer items in the area protecting and insuring. Dealing with insurance was a relevant topic for the respondents, which also was reflected in the fact that most of them had car insurance. Knowledge of earning income and buying goods and services were most relevant for the respondents’ daily actions and manifested in personal experience. We found that the use of knowledge of personal finance acquired through personal experience led to a correct answer in 90.91% of the cases.

4. Family and friends

In the five statements of the source family and friends, no unique allocation into one of the content areas can be made. However, it is noteworthy that in all cases the use of knowledge acquired from family and friends led to the correct answer to items on the TFL-G. This supports the results of previous research that the importance of the home environment as a significant source of knowledge of personal finance should not be underestimated (Lusardi et al., 2010; OECD 2014: 84–90). 15

5. Media

It is evident that three of five codings of the source media belonged to item number 24 (What does a credit bureau do?) from the content area using credit. The media played an important role in understanding the financial topics, debts, and credit bureau according to the experts, whereby a direct link to television (TV) was made. In four of five cases, the use of information from media was accompanied by a correct answer.

6. No explicit source of knowledge nameable

In 27 cases, the respondents could not name a specific source of their knowledge. The content area saving is, with only two instances, underrepresented compared to the other areas.

Implications and limitations

Regarding the first research question, through interviews with experts and analysis of their responses on an online questionnaire, the relevance of the items on the TFL-G for young adults in Germany was supported. The experts in Germany rated the relevance of the content areas covered on the test as being good. However, expert ratings can be questionable in how far their judgments are influenced by social desirability. We tried to moderate this effect using methodological triangulation and employed the online questionnaire, which followed the personal interview, however, this distorting effect cannot be completely avoided.

The results from the cognitive interviews with test-takers (Question 2) highlight that school is not such a significant source of knowledge as one might hope. In only 9 of 72 responses was school mentioned as the primary source of financial knowledge. These findings support the argument that more financial education should be offered at school. Most of the young adults in Germany visit a regular secondary school; very few choose a vocational education program or a vocational secondary school specializing in business and economics. The results of this study support the demand for greater inclusion of financial content in school subjects in Germany (Aprea and Wuttke, 2016). However, teacher education in Germany does not train teachers of regular secondary school in financial issues systematically. So, the question arises as to how teachers can teach their students about financial issues if they might not possess the knowledge themselves.

The results indicate that personal experience is important for acquiring knowledge of personal finance. Ultimately, this source not only was named most often as the source of knowledge needed to respond correctly to items on the TFL-G, but in 90.91% of the cases, it led to correct responses to items on the test. These results are in accordance with those of a number of studies in which daily life experiences were found to have a significant effect on knowledge of personal finance (Cameron et al., 2014; Marcolin and Abraham, 2006; Reifner, 2006). For financial education, this could suggest that teachers use learning situations which are highly relevant to the daily life of young adults. For example, simulation games might be appropriate because students experience results of their financial behavior in a controlled environment.

One limitation of this study is that the expert interviews (N = 10) and cognitive interviews with young adults (N = 6) were conducted with small samples. 16 It is advisable to conduct studies of larger samples to gain more representative results. However, these two methods (expert interviews and cognitive interviews) represent only part of the validation process of the TFL-G. As mentioned earlier, a sample of approximately 1108 students in different study programs were assessed using a paper–pencil version of the TFL-G (for results see Förster et al., 2017). Results of the qualitative analysis in this article and the quantitative analysis in Förster et al. (2017) both indicate that the TFL-G is a valid instrument for assessing young adults’ knowledge and understanding of personal finance in Germany (AERA et al., 2014). The results presented in this article also shed some light on the important sources of students’ financial knowledge and understanding. It should be borne in mind that knowledge and understanding of financial issues may not suffice to handle financial situations effectively. Non-cognitive facets such as attitude and motivation may be needed by consumers to make responsible and informed financial decisions. Those non-cognitive aspects of financial decision-making are not covered in our article or on the TFL but should be fostered in financial education.

Moreover, in a follow-up study an international perspective can be taken and cross-national comparisons of test results can be made. While saving is considered really important in Germany and in the United States, for example, people tend to spend and/or invest more. We do not know precisely from where such differing behaviors stem. Using more in-depth interviews or large-scale assessments would allow investigation into the behavior of subpopulations (e.g. gender, race, socioeconomic status) within and among countries.

Footnotes

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.