Abstract

This article aims at finding the relationship between households’ personality traits and their financial literacy level. The data in this research are from the household survey which can represent the population in Dutch. Using the Big Five personality traits and economic locus of control – extraversion, agreeableness, conscientiousness, emotional stability, intellect, internal locus of control, and external locus of control – I have found that those people whose personality traits are intellect and internal locus of control tend to have higher level of financial literacy than those with other personality traits.

Financial literacy has been established as a factor that affects household’s financial behavior. Financially literate people make financial decisions that benefit their own and their families’ financial well-being (Hilgert et al., 2003). In contrast, less financially literate people do not plan for retirement (Hilgert et al., 2003; Lusardi and Mitchell, 2007), struggle with debt problems (Lusardi and Tufano, 2015), lose investing opportunities by participating less in the stock market (Van Rooij et al., 2011), and hold poorly diversified portfolios (Calvet et al., 2007).

A clear link between financial literacy and financial behavior has been demonstrated, but few studies have examined the factors that explain financial literacy. In general, scholars relate financial literacy with demographic variables. For instance, Lusardi et al. (2010) find that young adults are the group that faces a critical financial literacy deficiency issue as only 27% of this demographic know about inflation and basic financial knowledge. Worthington (2006) finds that financial literacy can change through age and will peak at between 50 and 60 years of age. Gender is also a factor, as women tend to be less financially literate than men (Chen and Volpe, 1998; Lusardi et al., 2010; Worthington, 2006).

As the root of financial literacy differences has been less explored, this research proposes that personality traits can affect financial literacy among households. Researchers find that personality traits significantly predict behaviors in educational and academic performance domain. They also discover that personality traits account for high percentage compared to other variables in the models for predicting academic achievements (Chamorro-Premuzic and Furnham, 2003; Chamorro-Premuzic et al., 2008; Duff et al., 2004). O’Connor and Paunonen (2007) and Furnham et al. (2003) find that in their study personality traits are even stronger than cognitive ability in forecasting academic performance. This research forms hypotheses according to the established link between personality traits and academic performance, and applies it in the financial literacy domain with the aim to find an explanation for differences in financial literacy levels among individuals by proposing personality traits as a potential determinant.

Big Five personality traits and locus of control

Big Five personality traits consist of extraversion, agreeableness, conscientiousness, emotional stability, and intellect (openness to experience). In general, each personality trait in the Big Five has its own characteristics and values. For instance, as reviewed by Roccas et al. (2002), those who are extraverts tend to be sociable, talkative, assertive, and active. Extraverts also participate in excitements and challenges for pleasures. Agreeableness is associated with good-natured, compliant, modest, gentle, and cooperative. Agreeable persons tend to follow norms and conformity values, and care for people around them. Conscientiousness is related to being careful, thorough, responsible, and organized. Those who score high on conscientiousness are likely to pursue motivational goals and achievements. Emotional stability is associated with being calm, poised, and emotionally stable. Finally, intellect is related to being intellectual, imaginative, sensitive, and open-minded.

Locus of control (LOC) has two dimensions: internal and external LOC. In general, internal LOC is described as personal efficacy, self-belief, an action-oriented perspective, and taking responsibility for the consequences of one’s own actions. In contrast, external LOC is correlated to a belief in fate, luck, and chance (Hoffman et al., 2000; Lefcourt, 1976). Since Rotter’s LOC scale is considered broad and may not be specific in some contexts, with similar theoretical definition of LOC, researchers have developed their own LOC scales to use specifically in each area, such as Work LOC, LOC for Adults, Multidimensional Health Locus of Control.

Related previous research

Why personality traits, specifically “the big five” and “locus of control (LOC),” can be potential determinants of financial literacy? As reviewed, the Big Five contains five personality traits, including extraversion, agreeableness, conscientiousness, emotional stability, and intellect (openness to experience), while LOC contains two dimensions, including internal and external LOC. These two models have been used to predict behavior across domains, but remain less explored in the area of financial literacy. I hypothesize that the effect of personality traits on academic learning should be similar to the effect of personality traits on financial knowledge learning (financial literacy). Perry and Morris (2005) state that one of the formal sources from which everyone can gain financial literacy are high school, courses, training, and seminars. If people perform well academically, it may imply that they should have been equipped with more financial literacy. Mandell and Klein (2007) also find that being motivated and having a goal of achieving success in the future, such as earning a higher salary, are related to higher financial literacy levels. I expect that people with a motivated personality will gain higher financial literacy.

Personality research has found that conscientiousness from the Big Five and the internal LOC dimension from the LOC model are consistently related to higher educational ability. Numerous studies, as reviewed by O’Connor and Paunonen (2007) and Noftle and Robins (2007), have identified a positive relation between conscientiousness and targeted variables, especially scholastic achievement in school and university, such as grade point average (GPA), course grades, exam grades, and thesis research grades. Conscientiousness’ facets are full of competence (efficient), dutifulness (not careless), achievement striving (thorough), and self-discipline (not lazy). With the fine quality of these facets, previous studies have found that those who are conscientious have a positive attitude toward their academic intelligence, such as believing that their intelligence can be expanded throughout life, while less conscientious people feel that intelligence is stable (Furnham et al., 2003). Additionally, as reviewed by Komarraju et al. (2009), conscientious people have high motivation to achieve success and clearly have a negative relationship to avoidance motivation. For internal LOC, numerous studies have found that it has a positive relation to academic achievement (see Stipek, 1980 for review). Internals tend to stay motivated, alert, and information-seeking–oriented in order to have better opportunities in life (Judge and Bono, 2001). When they have difficulties, they deal with the obstacle by focusing on the problem and stimulating the skills necessary to ameliorate the bad situation (Arslan et al., 2009). As both formal education and financial literacy could be one of the keys to achieving success in life, I expect to find a positive relation between financial literacy and these two success-achieving personality traits: conscientiousness and internal LOC dimension.

Other than motivation, in terms of efficiency in gaining financial knowledge, previous studies have also found that conscientious people have a particular proficiency that could facilitate their financial learning. For example, Heaven and Ciarrochi (2012) show that conscientious students perform well in the subject areas of math and science. Additionally, as mentioned before, some of the formal sources from which everyone can gain financial literacy are high school, courses, training, and seminars. Since conscientiousness is positively related to good performance in these formal education systems, it may imply that conscientious people could have also gained more financial knowledge when they are in school.

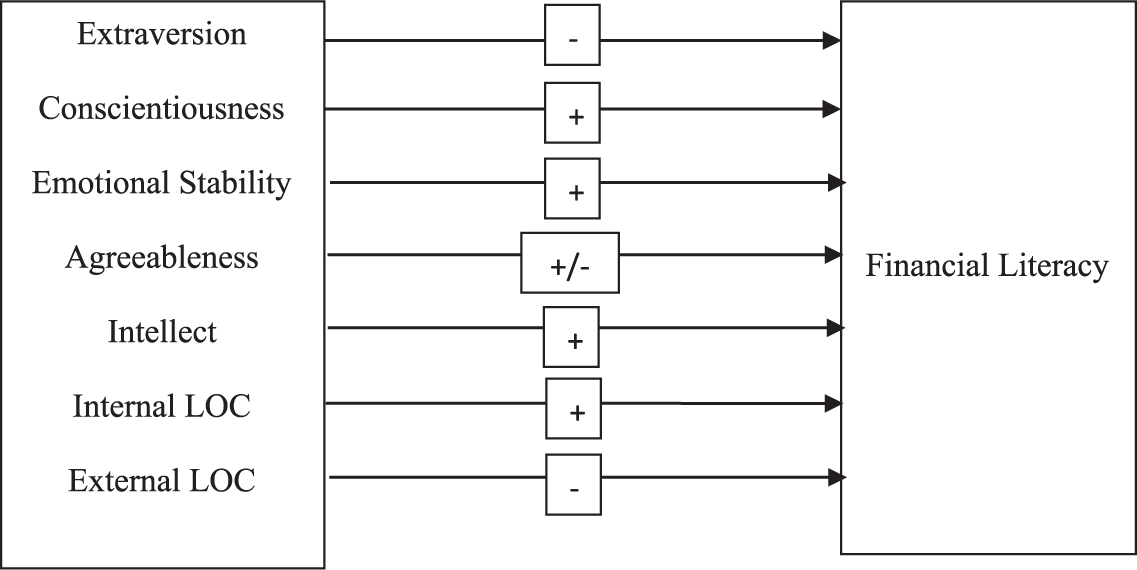

Even though conscientiousness and internal LOC have been most related to education and are expected to be most related to financial literacy, the rest of the Big Five traits and the external LOC dimension should also be discussed. Intellect (Openness), extraversion, emotional stability, and agreeableness have been significant factors for predicting academic performance, but the findings have so far been mixed and inconsistent. Intellect is positively related to intelligence which may facilitate academic achievement. Emotional stability, which is related to less stress and anxiety, could indirectly facilitate learning, which is in contrast to those who are neurotic and have to deal with debilitating effects such as stress during academic evaluation periods. Differently, extraversion is negatively related to academic performance because the socializing behavior of extraverts results in less time spent on study. Agreeableness could be considered the most inconsistent factor for academic performance because it can provide significant effects in both ways (positive and negative relations) (O’Connor and Paunonen, 2007). External LOC is related to a belief in fate, luck, and chance, not personal efficacy, which is opposite to the internal dimension and should provide a negative relation with financial literacy. All the hypotheses are presented in Figure 1.

Hypotheses.

Methodology and data

The hypotheses will be tested through a linear regression model (ordinary least squares (OLS)) as shown below. The dependent variable is financial literacy. The independent variables are personality traits and control variables including demographic information, education, and status in the household

where FinLit is a financial literacy measure, EXTRAV is extraversion, AGREEABLE is agreeableness, CONSCI is conscientiousness, INTELLECT is intellect, EMOTION is emotional stability, INTERNAL is internal LOC, EXTERNAL is external LOC, AGE is age, INCOME is income, GENDER is gender, MIDED is middle education level, HIED is high education level, MAINWAGE is a main wage earner in the house, and HOH is being head of the household.

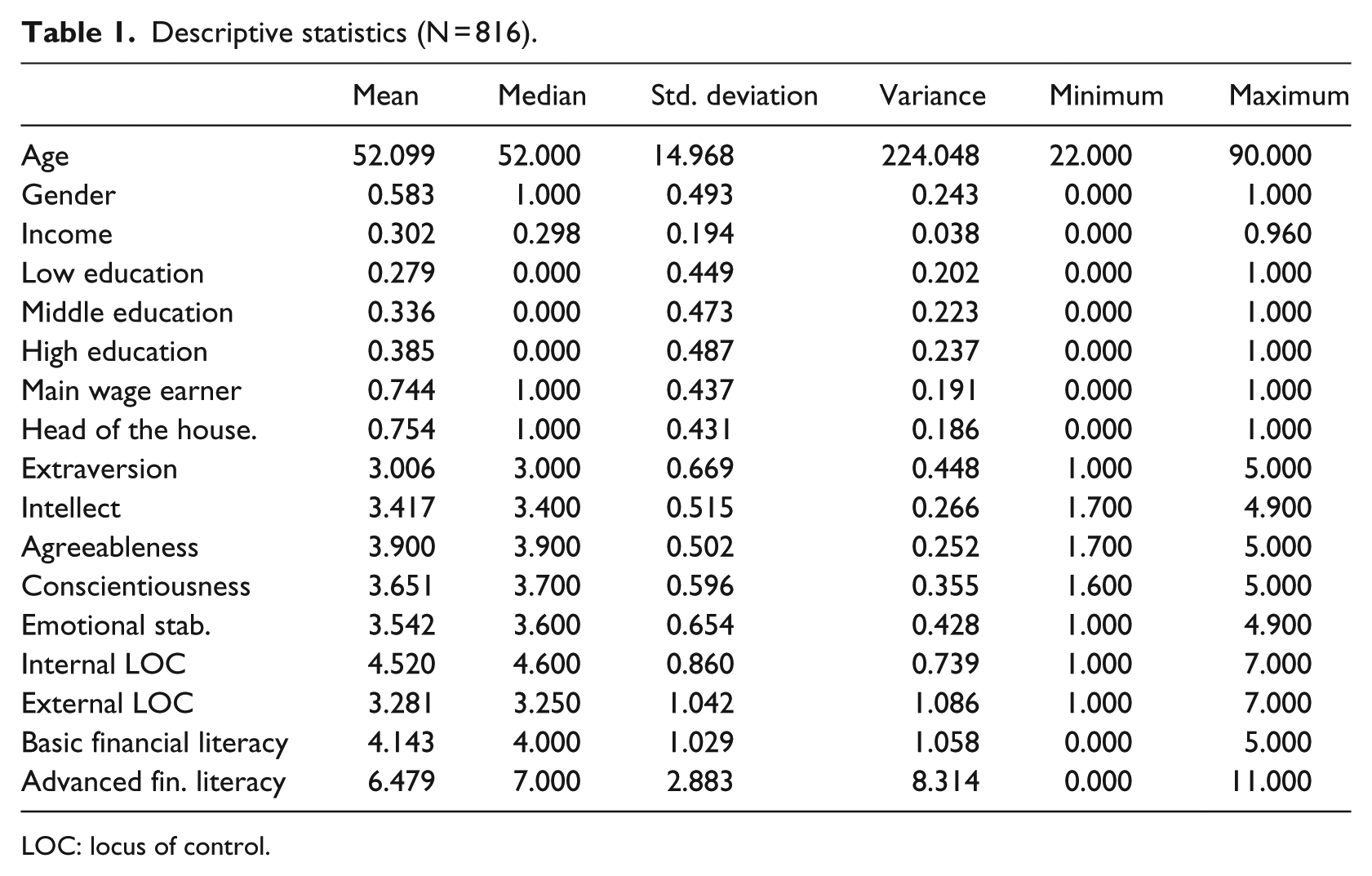

The data in this study are from the DNB Household Survey (Tilburg, The Netherlands), formerly known as the CentER Savings Survey. Every year since 1993, the survey has collected information on Dutch households including age, gender, and income. It also includes psychological and economic data that could impact the financial behavior of the households. In this article, the data are from the 13th wave collected in the year 2005 during January to August. The total sample size is 816 and the composition of the DNB Household Survey is representative for the Dutch population.

Personality traits

For the Big Five personality traits, the DNB Household Survey uses the Goldberg’s 50-item personality scale. Each set of 10 items measures one personality trait of the Big Five including extraversion, agreeableness, conscientiousness, emotional stability, and intellect. The participants will score each item from 1 to 5. For instance, one of the 10 items measuring extraversion states that “I am the life of the party.” The participants then choose a preferred answer from 1 (very inaccurate), 2 (moderately inaccurate), 3 (neither accurate nor inaccurate), 4 (moderately accurate), to 5 (very accurate). The personality score for each trait is calculated by summing every score for the 10 items representing the trait, divided by 10. The reliability analysis has been performed. The Cronbach’s alpha is as follows: extraversion α = 0.854, agreeableness α = 0.808, conscientiousness α = 0.782, emotional stability α = 0.849, and intellect α = 0.753.

For LOC, the DNB Household Survey includes the “economic locus of control” scale created by Furnham, which is considered a more specific model for economic and financial decisions than the original model. According to Fouarge et al. (2013), there are four dimensions of economic LOC, including internal, chance, denial, and powerful dimensions. The DNB Household Survey includes two of the dimensions that are compatible with the hypotheses: first, the internal dimension, described as “the belief that one determines one’s own economic fate”: and second, the chance dimension, which could be considered as a split of the external dimension as situations depend on external control, described as “the belief that chance determines one’s own economic fate.” The scale requires the participants to answer on a 7-point scale ranging from “disagree completely” to “agree completely.” Each of two LOC variables is calculated as the sum of the score from each item, divided by the number of items. The reliability analysis also has been performed. Cronbach’s alpha is as follows: the internal dimension α = 0.699, and the external dimension α = 0.670. The details of the Big Five and the economic LOC scales are presented in Appendices 1 and 2.

Financial literacy

As reviewed by Hung et al. (2009), financial literacy measures have been widely used in the form of multiple choice items. The measures can examine the participants’ financial knowledge whether by self-assessment or actual performance test. The financial domains in the questions can vary from savings, investment, debt, to numeracy.

The DNB Household Survey provides two additional modules to measure basic and advanced financial literacy. These two modules were created by Van Rooij et al. (2011) in the year 2005. Basic and advanced financial literacy measures are created by factor analysis from financial questions. The participants who answer the question correctly receive 1 point, while those who answer the question incorrectly or choose to answer “Do not know” or “Refusal” receive no point for that question. The sum of the points becomes the basic and advanced financial literacy scores. Basic financial literacy is aimed to measure the financial knowledge covering interest rates, interest compounding, inflation, discounting, and nominal versus real values. Advanced financial literacy covers more complicated topics such as the difference among financial instruments, the stock market, risk diversification, and bonds and interest rates. The complete set of these financial questions are shown in Appendix 3.

Control variables

Personal information is included as control variables. To control for gender, I add a gender dummy variable which is defined as 1 for men and 0 for women. For education, the survey provides nine levels of education that the participants have completed. I group these nine levels into three dummy variables: “low education” (including those who have special education, kindergarten or primary education, pre-vocational education “VMBO,” other sort of education or training, and no formal education), “middle level education” (including those who have pre-university education “HAVO”/“VWO” and senior vocational training or training through the apprentice system “MBO”), and “high level education” (including those who have completed vocational college “HBO” and university education “WO”). For age, I calculate the age of participants as the year of the survey minus the year of birth.

For income, I use the variable total gross income divided by 100,000, so that when it is included in the regressions, its beta will not be too small since some dependent variables are limited in range, for instance, financial risk tolerance which is in the range of 1 to 7 only. The income variable has many outliers and the data is not normally distributed. I modify it by winsorizing the data at 99%.

I include additional control dummy variables which represent the status of the members in the household. The participants respond to the question with an answer of either “yes = 1” or “no = 0.” First, regarding the head of the household status, the participants answer either “yes” for being the head of the household or “no” for being another family member. Second, to identify the main wage earner, the participants answer either “yes” if they are the main wage earner or “no” if they are not the main wage earner in the household.

Table 1 shows descriptive statistics for all the variables used in this study. The age of the participants ranges from 22 to 90 years. The average age is around 52 years. The proportion of male is higher than female as the number of male participants is 58.3%. For education level, the major proportion is 38.5% which is the participants who have high education. The percentages of main wage earner and head of the households are both about 74.4% and 75.5%, respectively. For personality trait variables, the Big Five and LOC, the answers have been spread from the minimum score to the maximum score such as extraversion, internal LOC, and external LOC. For basic and advanced financial literacy, the scores also have been spread from those who cannot answer any question to those who answer correctly all the questions. The average score of the basic financial literacy is 4.143, while the average score of the advanced financial literacy is 6.479.

Descriptive statistics (N = 816).

LOC: locus of control.

Results

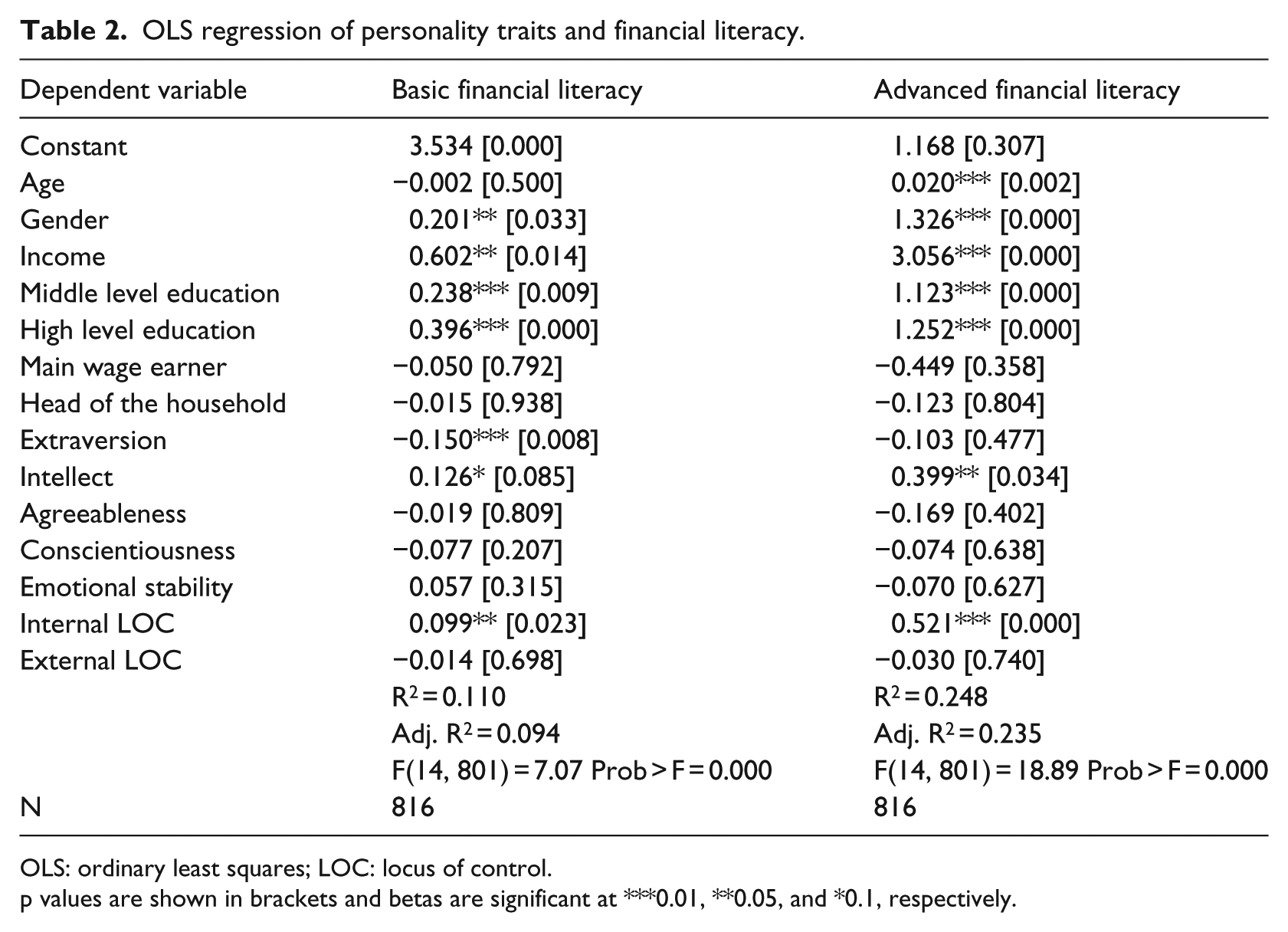

First of all, I observe the correlation between the two financial literacy variables to ensure that they are converging to each other by showing a positive correlation. I find that the correlation between the basic and advanced financial literacy measures is positive (0.388) and significant. This positive correlation indicates that the measures of two financial literacy levels are robust.

Table 2 reports the results responding to the hypotheses. For basic financial literacy in column 1, every significant personality trait follows the hypotheses including extraversion and internal LOC. Extraversion has a negative, while intellect and internal LOC have a positive relation with basic financial literacy. In column 2, advanced financial literacy is the dependent variable. The two significant personality traits are intellect and internal LOC, having positive relations with advanced financial literacy. Intellect and internal LOC are also consistent variables since they are significant in both columns of basic and advanced financial literacy.

OLS regression of personality traits and financial literacy.

OLS: ordinary least squares; LOC: locus of control.

p values are shown in brackets and betas are significant at ***0.01, **0.05, and *0.1, respectively.

The negative relation to financial literacy of extraversion and the positive relation to financial literacy of intellect follow what have been researched in the academic performance area as reviewed. Scholars have found that extraverts tend not to perform well academically, while intellects perform better in the same contexts. Extraversion tends to have a negative relation, while in contrast, intellect has a positive relation to various educational variables, such as GPA and exams (O’Connor and Paunonen, 2007). Extraversion is known for excitement seeking and socializing. Their extravert characteristics can become a burden for learning process since these habits may distract them from study and preparation. For intellect, other than the association with intelligence that can facilitate learning and academic performance, it has also been found that intellect people have significant relation to engagement motivation or the motivation to improve themselves (Komarraju and Karau, 2005). This motivation can indirectly drive them to learn financial literacy since financial knowledge can boost and improve their financial performance.

Internal LOC, which is positively related to financial literacy, also follows the findings in academic performance research where they have found the positive relation as reviewed. Not only the educational domain that LOC has been studied, the two dimensions of LOC have strong relation to financial behavior, for instance, those who have high score on external dimension are positively associated with bad credit rating (Perry, 2008), less savings, and poor budgeting (Perry and Morris, 2005). With the results in this study, it can help indicating the root of poor financial behavior among the externals (the opposite dimension of internal LOC) that these external people may have low financial literacy level.

Other than these anticipated findings according to the hypotheses, there is one issue that contradicts what I had expected: the case of conscientiousness. Conscientiousness has proved to be a strong factor in academic performance, but when it comes to financial literacy conscientiousness seems not to have much of an effect as the significance is not visible. One possible assumption is that when measuring academic performance such as GPA, it includes every course other than finance, those who have high GPA may perform well in other courses such as arts or science which can also result in satisfactory GPA. However, this unexpected result should not be ignored as it has formed a new challenge for researchers in education area about the difference between financial literacy and education in school.

For other variables in the model, only gender, income, and education have steady significant effect in all of the columns. Male and higher income are positively related to the basic, and advanced financial literacy. Middle and high education also have a positive relation to basic and advanced financial literacy. Age is only positively significant in the advanced financial literacy column.

Conclusion

Using data from the DNB Household Survey (a population survey in the Netherlands), this article aims to find the relationships between personality traits and financial literacy. Financial literacy affects individuals’ financial behavior; however, the determinants of financial literacy have been less investigated. It is important to know the source of financial literacy, because this information can help improve the financial well-being of people.

I mainly hypothesize that personality traits from the Big Five and LOC model can be potential sources of variation of financial literacy among people. Personality traits have been related to various kinds of behavior including academic performance and learning. I expect that the effect of personality traits in the domain of academic performance should be similar to the effect in the domain of financial literacy, as both are related to knowledge and learning ability. Conscientiousness and internal LOC have been found to be most related to academic performance, while the rest of the personality traits have provided mixed results. For the findings, the two personality traits that have constantly significant impact on financial literacy of individuals are intellect and internal LOC.

This article not only shows that personality traits are one of the determinants of financial literacy differences among people but also provides direction for future research. Since “intellect” and “internal locus of control” are positively related to financial literacy, future research can investigate that which factors can play role in affecting changes of intellect and internal LOC in people. Another future discussion could also be the relation between conscientiousness and financial literacy. As stated earlier, conscientiousness from the Big Five model was expected to be the personality trait most related to financial literacy as it is strongly related to academic learning and performance. However, it unexpectedly shows an insignificant impact in the domain of financial literacy. Intellect and conscientiousness can have some differences in terms of knowledge gaining and learning performance.

Footnotes

Appendix 1

Appendix 2

Economic locus of control (LOC) scale requires the participants to answer on a 7-point scale ranging from “disagree completely” to “agree completely.” The description of both internal and external economic LOC is as follows.

Appendix 3

The financial literacy measure in this study was created by Van Rooij et al. (2011).

All the basic financial literacy questions were originally created by Van Rooij and her team, whereas the questions in advanced financial literacy have been taken from other sources as listed below:

For basic financial literacy, there are five questions that the participants must answer:

For advanced financial literacy, there are 11 questions that the participants must answer:

Acknowledgements

The author would like to thank DNB Household Survey for providing the data. The author would also like to thank CentERdata, Institute for data collection and research for the data provision and support.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by the Thailand Research Fund through the Royal Golden Jubilee PhD Program (grant no. PHD/0304/2552).