Abstract

Technologically advanced states and large emerging economies increasingly use foreign investment screening mechanisms (FISM) to block inward foreign investment targeting sectors considered critical. Is the proliferation of FISM auguring an era of deglobalization, a re-assertion of national-state sovereignty over globalized economic ties, and the end of neoliberal orthodoxies of liberalized investment regimes? To answer these questions, the article draws upon geographic political economy and legal geographies. It argues that the multiplication of FISM is a response to a strategic context defined by three macrogeographic trends: (1) contemporary industrial restructuring and the salience of intellectual property-based monopolies; (2) a historic episode of centralization of capital driven by strategic mergers and acquisitions; and (3) evolving landscapes of state capitalism under conditions of intensified geoeconomic competition. Although FISM reproduce the fiction of state power as expressing the will of the sovereign nation to defend itself against foreign interference, market distortion, and technology theft, they consist of legally enshrining state authority to support national champions, and making sure they engage favorably with competitive dynamics of capital centralization, notably by conserving their monopoly over key intangible assets and strategic resources. FISM are best seen as tools that explicitly mobilize state power and coercion to aggressively (re)negotiate globalization.

Keywords

Introduction: the revenge of national security on foreign investment?

In November 2022, the German government blocked the acquisition of two domestic semiconductor companies (Elmos and ERS) by Chinese investors, on the ground that it would endanger ‘public order and security’. A week later, the UK government ordered a Chinese firm to reverse its acquisition of Newport Wafer Fab, the UK's largest microchip producer, on grounds of ‘national security’. In June 2023, the Italian government prevented the Chinese chemical giant Sinochem from nominating the Italian tyre manufacturer Pirelli's chief executive officer, despite Sinochem being Pirelli's largest shareholder since 2015. The decision was justified by the need to preserve the independence of a company said to be ‘strategically important to the nation’. In this case, the government did not block or unwind the investment, but limited the decision-making power of the investor, even years after the investment happened. These are three recent examples of foreign investment screening. This consists of public authorities blocking an inward investment deemed undesirable, subjecting its admission to requirements, or demanding divestment from a specific firm or asset on grounds of national security (Bauerle Danzman & Meunier, 2023; UNCTAD, 2019). This practice differs from statutory bans on foreign direct investment (FDI) or sectoral exclusions, insofar as it involves the discretionary use of regulatory powers to be exercised on a case-by-case basis: decisions are made based on the screening of individual transactions by relevant ministerial cabinets or specialized committees (UNCTAD, 2023: 2).

Investment screening is a practice that is codified into law and takes the form of procedural legal processes based on predetermined criteria (Bauerle Danzman & Meunier, 2023). Such criteria can diverge significantly depending on national legislations, but they typically involve a combination of the following: they can be sector-specific (e.g. does the investment target an economic sector considered ‘strategic’, ‘sensitive’, or ‘critical’?); they can be related to the type of entity conducting the investment (e.g. is the investor public or private?); or to the nature of the transaction (e.g. does the value of the transaction exceed a particular amount? Does it result in significant foreign capital participation in the targeted firm, or the acquisition of voting rights?). These criteria define the conditions under which an investment must obtain prior authorization and under which an investment screening procedure is triggered. For instance, a transaction entailing foreign ownership of over 25% in a sector considered strategic may trigger a screening process.

The practice of foreign investment screening has proliferated over the past few years. According to the United Nations Conference on Trade and Development, a total of 42 countries have adopted foreign investment screening mechanisms (FISM) and conducted investment screening for national security purposes, which is an all-time high. These countries include the USA, Canada, France, Japan, Germany, Italy, Finland, Sweden, Spain, South Africa, Mexico, the UK, China, Australia, Russia, Czechia, Israel, Latvia, Ireland, Denmark, Slovakia, Slovenia, India, the Philippines, Romania, Thailand, and Saudi Arabia (UNCTAD, 2023).

The growing adoption of FISM must be understood in the context of increasing concerns among policymakers and legislators that core firms and key assets can fall prey to what is euphemistically termed in the policy jargon ‘opportunistic investment behavior’. This refers to investors seizing crises as opportunities to acquire (or take controlling stakes in) distressed firms and underpriced assets, notably in sectors considered strategic. Furthermore, there are concerns that opportunistic investments can be controlled or influenced by foreign governments aiming to take control of key firms, assets, core technologies, or critical infrastructure. This poses risks in terms of economic sovereignty and increased vulnerability to foreign geopolitical influence. In short, there are increasing concerns among state actors that FDI can pose risks for ‘national security’ and ‘public order’.

The multiplication of FISM is a deep-seated regulatory trend which has happened under the radar of economic and political geographers, despite their interest in regulations and state regulatory activities. FISM should be of interest to the two branches of regulatory thought in geography: first, the traditions concerned with ‘real’ regulations (i.e. regulations as a set of historically and geographically specific social practices), and second, régulationist and Régulation-adjacent approaches interested in dynamics of macro-institutional change and the role of rules, norms, and conventions in organizing the social and economic relations of capitalist society (Jones, 2017; Phillips, 2022).

According to the 2022 World Investment Report ‘together, countries that conduct FDI screening account for 63% of global FDI inflows and 70% of stock (up from 52% and 67%, respectively, in 2020)’ (UNCTAD, 2022: 13). This is particularly significant insofar as FDI are a cornerstone of economic globalization, alongside international trade in goods and services, portfolio investment, and cross-border bank lending. This therefore raises several questions: is the proliferation of FISM auguring an era of reversal, or decreasing intensity, of globalization as we know it? Are FISM the harbinger of an age of ‘deglobalization’, ‘slowbalization’ (The Economist, 2019), or ‘globalization in reverse’ (Gong et al., 2022; van Meeteren and Kleibert, 2022)? Are we witnessing a protectionist backlash against open markets, and a re-assertion of national-state sovereignty over globalized economic ties? Is this signaling the end of neoliberal orthodoxies of liberalized investment regimes and norms of free capital mobility and investor protection at all costs? Does the multiplication of new legal, regulatory, and institutional mediations in the form of FISM portend the emergence of a new mode of regulation beyond neoliberalism?

At first sight, the case of FISM certainly lends itself easily to such interpretations: states are ostensibly affirming their sovereign authority to regulate the entry of foreign investors into their national territories; they seem to reprioritize public concerns (national security, public order) over private rights; and FISM appear to suggest that states are much less optimistic about the virtues of open investment environments and greater economic integration. In sum, the proliferation of FISM would seem to provide robust evidence that there is indeed a sort of Polanyian countermovement currently taking place, indicating both a trajectory of deglobalization, the rise of ‘protectionist sentiments’, a ‘return of the nation’, and states moving into a post-neoliberal direction (e.g. Gerbaudo, 2022).

However, understanding FISM in these terms would be significantly misconstruing the role that they play in ongoing processes of state restructuring, and in the form and pattern of economic globalization that is currently emerging. By better appreciating the geographic political economic drivers of FISM, their concrete workings, and the legal spatialities they produce, we can get a better understanding of how they simultaneously contribute to reconfiguring state power and economic space. My central claim is that, although FISM reproduce the fiction of state power as expressing the will and interest of the sovereign nation to defend itself against foreign interference, market distortion, and technology theft, they essentially consist of legally enshrining state authority to support national champions and other domestic firms, and making sure they engage favorably with competitive dynamics of centralization of capital, notably by conserving their monopoly over intangible assets and strategic resources. FISM are undoubtedly a marked departure from the policies of FDI liberalization that characterized the 1990s. Nevertheless, they do not constitute attempts at undoing the world created by neoliberalism. Rather, they aim at locking in a series of technological and industrial advantages accumulated under the neoliberal regime. 1

The article proceeds in five steps. The second section documents the recent trend of proliferation and tightening of FISM, and zooms in on their basic features, as well as the main sectors, transactions, and investors they cover. The third section turns to the existing literature on FISM. I focus on two influential explanations for the recent proliferation of FISM in the fields of International Relations and International Political Economy: the rise of China as a transnational investor, and the ‘weaponization of economic interdependence’. These arguments contain a kernel of truth but are incomplete. In the fourth section, I submit that developing a fuller account of the determinants of FISM requires examining three material trends rooted in uneven geographical development: (1) contemporary industrial restructuring and the salience of intellectual monopolies; (2) a historic episode of centralization of capital driven by strategic mergers and acquisitions (M&As); and (3) evolving landscapes of state capitalism under conditions of intensified geoeconomic competition. The fifth section then argues that to understand precisely what FISM do and how they produce particular dispositions of state power, we must take seriously that they are creatures of the law. Legal geographies can help us analyze the role they play in restructuring patterns of cross-border investment. The sixth section concludes and emphasizes the article's contribution to debates in economic geography and beyond on the future of globalization and neoliberalism. Throughout the article, the analysis relies upon a range of primary and secondary sources. In addition to various policy notes released by international organizations such as UNCTAD and the OECD, I draw upon the legal texts (mainly bills and statutory laws) introducing FISM in various jurisdictions, as well as two databases: the PRISM dataset which contains information about FISM deployed in 38 OECD countries between 2007 and 2022; and UNCTAD's Investment Policy Hub. 2

The multiplication and tightening of FISM

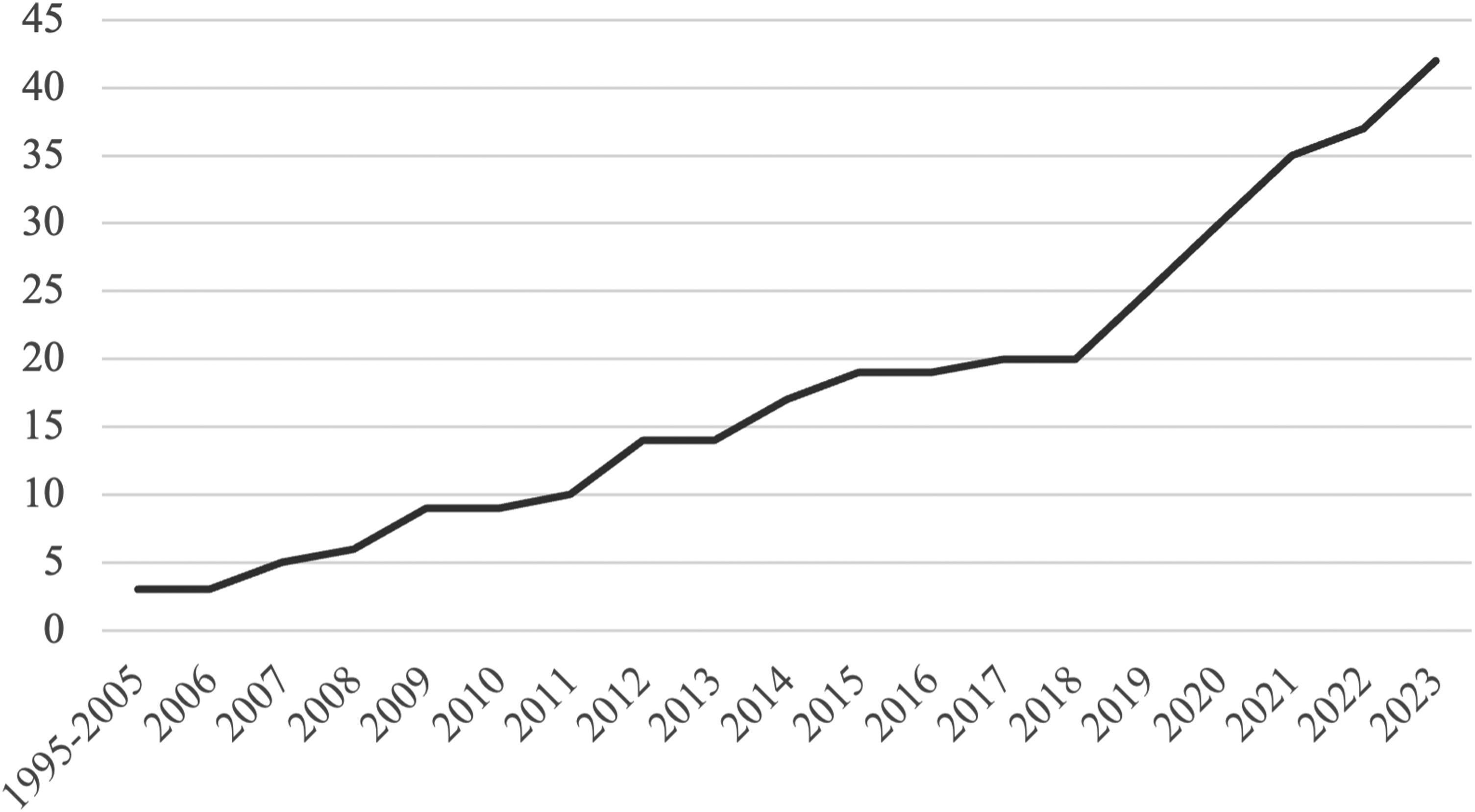

This section presents some stylized facts concerning the multiplication of FISM to the attention of economic and political geographers, setting the scene for the analysis, arguments, and theoretical contribution articulated later in the article. 2020, 2021, and 2022 have been record years for the adoption of FISM. This partly reflects the impacts of the COVID-19 pandemic and Russia's war of aggression in Ukraine, which considerably magnified concerns for national security and critical supply chains. Yet these two crisis events have only accelerated a regulatory trend that has long predated them. Starting in the mid-2000s, states have been passing legislative changes to either introduce new FISM or to considerably expand the scope covered by existing ones. By contrast, only 3 FISM were introduced between 1995 and 2005. The cumulative number of countries with FISM in place has increased from less than 3 in 2005 to more than 42 at the time of writing, as Figure 1 shows.

Number of countries with FISM (based on UNCTAD’s Investment Policy Hub).

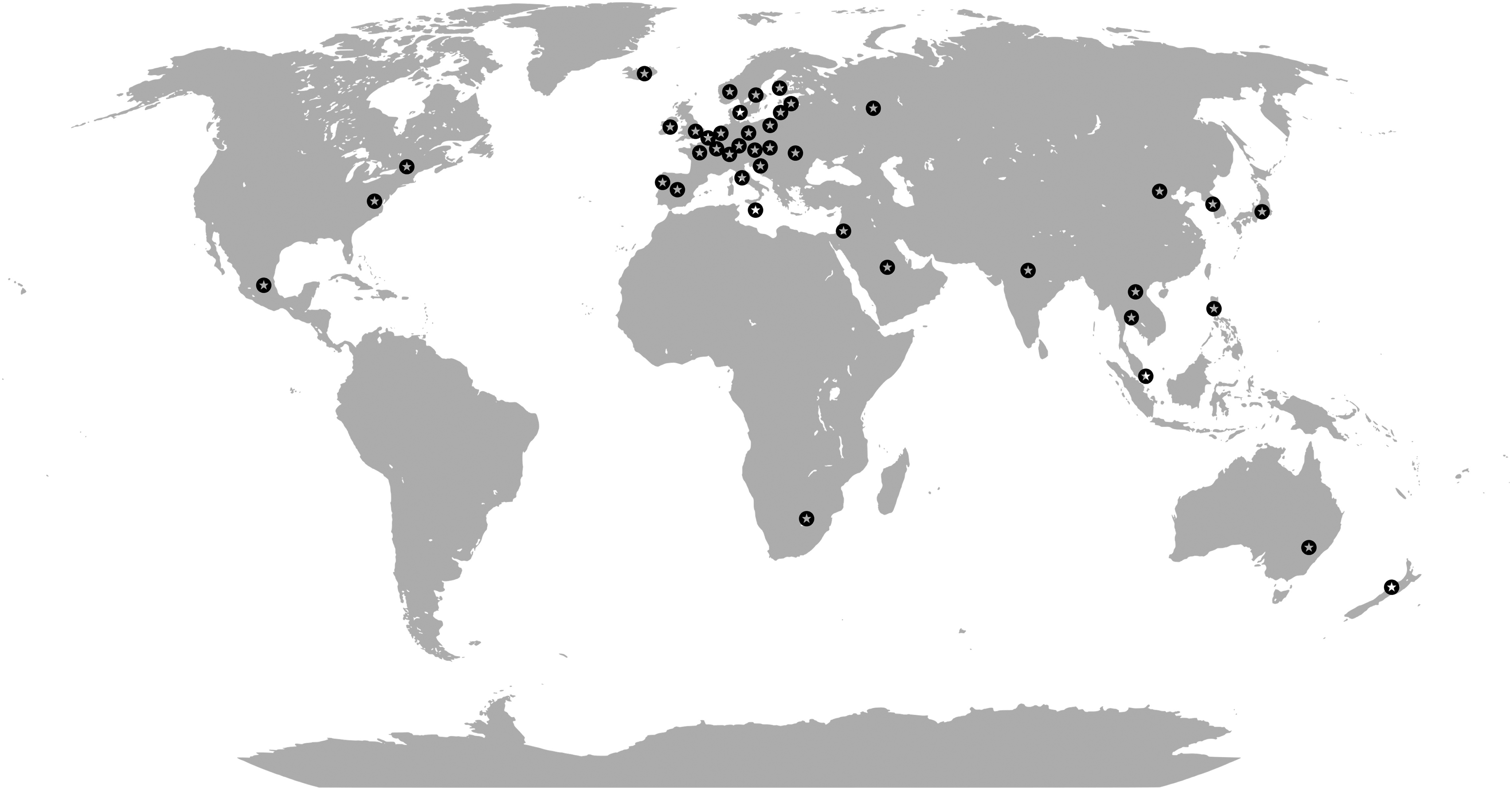

Countries with FISM are shown on Figure 2. For the most part, these are technologically advanced economies and large and powerful middle income or emerging market economies. Only one of these countries is in Latin America, and another in Africa. The conclusion will return to this important geographical fact.

Countries with FISM.

The new legislative amendments passed during this period have also greatly widened the activities and transactions falling under the purview of FISM, for instance, by lowering the threshold criteria related to the value of the transaction or the share of foreign capital participation triggering a screening process. They have also broadened the types of investors of concern. For example, FISM have often been expanded to not only target investors formally owned by foreign states, but to also include foreign corporate entities simply presumed to be associated with, or influenced by, foreign governments. Moreover, the scope of FISM has been considerably extended to cover ever more economic sectors and activities, way beyond what is traditionally considered to be a matter of national security, such as the defense and military industry. Despite a significant degree of variation across national legislations in terms of what sectors are considered to be ‘strategic’, ‘sensitive’, or ‘critical’, and therefore falling under the purview of FISM, the tendency has been to add to these sectors and to broaden the definitions of such terms. The array of sectors and activities now routinely covered by FISM is truly remarkable, and include transport and aviation, infrastructure, energy, media and telecom, financial services, food security, public health, and increasingly foundational or high technologies, such as AI, advanced robotics, semiconductors, cloud computing, 5G, advanced materials, quantum technologies, or renewable energy (see UNCTAD, 2019: 8; PRISM dataset; various national legislations).

According to UNCTAD (2019: 5), 52% of the measures adopted between 2011 and 2019 consisted in extending the scope of FISM. Fourteen percent of legislative changes extended disclosure obligations, that is the type of information that investors must disclose as part of the screening practice, often in the form of mandatory filing obligations. This can be information about ownership and management structure or scope of operations. Another 14 percent extended screening timelines, which are the timeframes during which the review takes place, and during which state authorities can render a decision on the investment. Furthermore, 10 percent of new legislation over the same period have introduced provisions allowing states to impose sanctions, under the form of financial and sometimes criminal penalties for noncompliance with obligatory filing obligations (Investment Policy Hub; UNCTAD, 2019).

The following are notable examples of recently passed legislations that combine these various dimensions. The 2018 US Foreign Investment Risk Review Modernization Act (FIRRMA) ‘expands the jurisdiction of the Committee on Foreign Investment in the United States [CFIUS] to address growing national security concerns over foreign exploitation of certain investment structures which traditionally have fallen outside of CFIUS jurisdiction. Additionally, FIRRMA modernizes CFIUS’s processes to better enable timely and effective reviews of covered transaction’. 3 The UK National Security and Investment Act, which came into force in 2022, ‘represents a major upgrade of the UK's investment screening powers’ (UK Government, 2023). The Act identifies ‘17 sensitive areas’ falling under the purview of the FISM, from computing hardware to data infrastructure and synthetic biology, and significantly expands the types of transactions covered beyond M&As, now including ‘minority investments, acquisitions of voting rights and acquisitions of assets including land and IP [intellectual property]’ (Norton Rose Fulbright, 2022: nd). In the European Union (EU), Regulation EU 2019/425, in force since 2020, established a framework for ensuring coordination, exchange of information, and greater freedom at both EU and national level to conduct foreign investment screening. With this regulation, the European Commission is actively encouraging member states to tighten their FISM. The French state amended its FISM several times over the past few years, including in 2019, 2020, 2021, 2023, and 2024. It added more sectors to the list of sensitive activities (biotechnology, renewables, public health), lowered the equity ownership threshold for scrutinizing foreign investments from outside the European Union from 25 to 10 percent, and bolstered its power to sanction in case of noncompliance (Direction Générale du Trésor, 2023). Germany's FISM, in place since 2004, has been tightened multiple times since then, notably in 2021, when the list of security-relevant sectors was extended from 11 to 27 sectors. In the sectors considered most strategic, the acquisition of 10 percent or more of the voting rights of a target company by an investor from outside the European Economic Area now triggers a screening process. Germany is preparing further amendments to their FISM. In March 2021 and October 2022, Canada tightened its FISM. It expanded the list of national security sectors to include 31 critical minerals and sensitive personal data and extended the types of foreign investors covered to include not only state-owned enterprises but also private firms ‘closely tied to, subject to influence from, or who could be compelled to comply with extrajudicial direction from foreign governments, particularly non-likeminded governments’ (Government of Canada, 2023: nd).

With more and tighter FISM currently in place across the world, there has also been a strong upward trend in the number of investment transactions screened per year. In 2022, France received 325 cases (an increase from 184 in 2018), which encompass both applications for pre-authorization on planned investment (to determine if they would have to be authorized by the French Treasury or not) and filings for in-depth analysis. As a result of pre- or formal screening procedures, 131 transactions were authorized, among which 70 (or 53 percent) were subject to specific conditions and mitigation measures (Direction Générale du Trésor, 2023). In Germany, the cases filed as part of the FISM increased from 78 in 2018 to 306 in 2021. In 2021, 14 transactions (4.5 percent of the applications) were either prohibited or side conditions were required (Bundesministerium für Wirtschaft und Klimaschutz, 2023). In the USA, CFIUS filings jumped from 97 in 2013 to 286 in 2022. Of these 286 notices, 162 led to in-depth investigations, and CFIUS adopted mitigation measures and conditions in 52 instances (or 18% of the total filings) (CFIUS, 2023).

In sum, over the past 15 years, a growing number of states have passed legislation establishing tighter and tighter FISM, often containing increasingly sophisticated and institutionalized procedures. This has considerably empowered state apparatuses to block or unwind foreign investment deemed undesirable, or to extract conditions from foreign investors. These powers are being actively used, in ways that are already shaping patterns and regulatory geographies of M&As and FDI. How to explain these developments?

A response to rising China and the weaponization of economic interdependence

Within International Relations and International Political Economy (IR/IPE), two relevant arguments have been put forward. The first one sees the profusion and tightening of FISM as a direct response to the surge of transnational investment from China. The most developed version of this argument can be found in the work of Meunier and collaborators (e.g. Meunier, 2019; Chan and Meunier, 2022; Bauerle Danzman and Meunier, 2023). She argues that new sources of FDI often stoke fears and trigger the deployment of restrictive investment policies. Consider these two historical examples: surging American FDI in France in the 1960s, and rapidly increasing FDI from OPEC countries and Japan to the USA in the 1970s–1980s, triggered negative perceptions and media representations, in turn sparking policy responses on the part of recipient countries. The recent Chinese case presents the additional peculiarity that China is perceived by many western actors as radically different from, if not incompatible with, liberal market economies (Meunier, 2019). Chinese investment is often presumed to be state-led and therefore politically risky. Consequently, notwithstanding its relatively low volume compared to more ‘traditional’ sources of investment, Chinese investment has acquired an outsized importance in public debates, gradually leading western policymakers to reevaluate the tradeoff associated with Chinese FDI: the risks they pose for national security are now largely seen to be greater than their potential benefits in terms of increasing domestic welfare. Babić and Dixon (2022) call this ‘the China effect’. These shifting perceptions and narratives about threatening Chinese investment then travel across countries and drive legislative changes and the adoption of FISM elsewhere, as shown in the case of the Nordic region (Mattlin and Rajavuori, 2023).

This argument undeniably has some traction. Many transactions blocked over the past few years indeed came from firms controlled by Chinese investors, including in the three examples mentioned in the introduction. There is much evidence of a clear shift of attitude toward Chinese investment in western economies, notably in the context of a general turn toward discourses and strategies of ‘geopolitical de-risking’. Yet there are potential objections to this argument. First, FISM have been deployed in many countries where it is much more difficult to identify a clear animosity toward Chinese investment, notably in non-western emerging economies such as South Africa and Mexico. Second, even in countries where the ‘China effect’ can be robustly documented, many governments had started using and tightening FISM before investment from China soared in the early 2010s. For instance, the French state tightened FISM in 2005, in response to an undesired takeover attempt of the national champion Danone by the American giant PepsiCo, and again in 2014, to make sure that the state would have a say in the investment deal between the American General Electric and the French firm Alstom (Lenihan, 2018: 3). Furthermore, examples of FISM being used to block investments from supposed economic allies abound. In 2017, the USA blocked an $850 million investment from a German firm (Infineon technologies AG) seeking to acquire an American firm (Wolfspeed) and its silicon carbide substrate business (a key component for semiconductors). In 2018, the USA blocked the takeover of American chipmaker Qualcomm by Singaporean firm Broadcom for national security reasons (UNCTAD, 2019: 13–14). In the same year, the Spanish government blocked the acquisition of Abertis Infraestructuras (a Spanish firm) by an Italian holding company Atlantia and forced a restructuring of the deal to make it a joint acquisition by Atlantia and Hochtief (a German subsidiary of the Spanish company Actividades de Construccion y Servicios) (UNCTAD, 2019: 15). The latest amendments to Italy's FISM gave the state authority to screen investment coming from the European Economic Area (UNCTAD, 2023). Consequently, the ‘China effect’ may not explain the whole story of FISM.

These objections should also give us pause as to the invocation of notions of ‘national security’ or ‘public order’ as motives to block investment. The literature earlier reviewed offers a useful analysis of the role of these notions in the discursive justification of investment screening, and in signaling a shift of perspective among policymakers. But it neither problematizes these notions nor does it scrutinize how they function as powerful legal categories. As discussed below, national security is not a pre-given, objective notion, which policymakers simply weigh against other criteria, such as economic welfare. It is a legal construct that codifies and enables particular forms of state intervention over investment flows. On this, the literature on the ‘China effect’ has little to say.

The second argument that the IR/IPE literature offers is that FISM epitomize a general reorientation in economic policymaking, which is driven by the increasingly networked structure of the economy. Commentators refer to this as the ‘securitization of economic policy’ (Vidigal and Schill, 2021), the emergence of a ‘geoeconomic world order’ (Babić et al., 2022), or the ‘weaponization of economic interdependence’ (Farrell and Newman, 2019). While there is some nuance between these various conceptual proposals, the essential argument is that the formation of complex globalized and interconnected networks of production, trade, finance, technology, infrastructure, and digital data spanning territorial borders has enhanced security threats. 4 These risks are heightened by technological developments (including the proliferation of dual-use technologies), the broad use of digital technologies, and the increasing reliance of governance on data management. FISM are thus understood as a defensive mechanism (alongside trade restrictions and protectionist policies) to reduce the threats, dependence, and vulnerabilities that may result from the weaponization of networks of corporate ownership and control.

This argument helpfully locates the proliferation of FISM within broader shifts in economic and political relations, technological developments, and the highly integrated structure of the world economy. It also helps explain the extension of the scope of FISM to cover sectors and activities deeply integrated in these globalized networks, such as cutting-edge tech and critical infrastructure (e.g. 5G), with the explicit aim preventing foreign actors from controlling key network nodes. Several countries have also amended their national legislations to cover economic activities involving access to sensitive personal information or capable of shaping public opinion. That said, there are also potential objections to this argument. One is that, even in the case of one of the most stringent and robust FISM (that of the USA), it is highly questionable if protection against ‘weaponized interdependence’ is the prime motive of investment screening. A leading expert on the American FISM, Bauerle Danzman (2021), warns against the abuses of this term in this case. If reducing the potential for weaponized interdependence was indeed the main objective, FISM would arguably be considerably tougher. She adds that the notion of weaponized interdependence downplays the fact that much investment screening practice takes into account market logics and commercial concerns, such as the acquisition of dominant market positions (Bauerle Danzman, 2021).

I indeed mentioned earlier several cases where FISM were used to protect national champions. Moreover, many national legislations explicitly state that decisions to block or submit inward investment to conditions can be motivated by market and economic criteria, such as maintaining technological leadership or globally competitive positions. For example, under the Investment Canada Act, the Canadian government justified including critical minerals in its FISM because of their importance for national security, but also because ‘Canada's future prosperity and global leadership in emerging low-carbon and other technology sectors requires reliable market-based access to Critical Minerals across the value chain’ (Government of Canada, 2023: nd). The South Korea Act on Prevention of Divulgence and Protection of Industrial Technology (passed in 2009 and amended in 2011 and 2017) specifically states that the FISM applies when targeted companies are in possession of ‘national core technologies’ defined as having ‘high technological and economic values in the Korean and overseas markets’ or bringing ‘high growth potential to their related industries’ (UNCTAD Investment Policy Hub). When France tightened its FISM in 2023, Finance Minister Bruno Le Maire linked the measure to the necessity to support French firms in the face of foreign competition. 5 That FISM are so often embedded in industrial strategies of technological leadership, economic competitiveness, value capture, and market dominance get somehow lost when we primarily see them as tools to protect against weaponized interdependence. Insulating strategic infrastructure, keeping control of core technology, and ensuring the integrity of domestic supply chains are commercial imperatives as much as it is a matter of national security.

To sum up, IR/IPE arguments about the ‘China effect’ and ‘weaponized interdependence’ contain a kernel of truth but only offer a partial explanation as to the political economic drivers of the recent proliferation of FISM. The remainder of this article shows that a deeper geographical engagement reveals a fuller explanation of this phenomenon and its implications for geographies of investment regulation, globalization, and neoliberalism.

Locating FISM in evolving landscapes of strategic M&As and state capitalism

Let us take a step back and start from the basics: FISM are, for the most part, about screening a particular type of financial transaction, namely takeovers and M&As. Why have policymakers increasingly felt the need to exercise control over these transactions? Takeovers and M&As are about firms buying each other out, or buying shares in other firms, either directly, or through the financial system. Put differently, they are two different modalities of what Marx (1991) calls the centralization of capital. This refers to the redistribution of ownership and control of existing capital in fewer hands. Insofar as mergers consist of distinct firms combining their operations to become a single legal entity, they are a straightforward form of capital centralization. Similarly, in acquisitions or takeovers, a firm buys or takes control of a target firm, whether the latter consents or not. This may be done without taking full ownership of the target firm, for instance, by obtaining assets, liabilities, or taking equity stakes (and often by borrowing funds from banks or leveraging the financial system). This is a more complex form of centralization which maintains a separation between ownership and control even as it recombines them, often to the benefit of the larger or more powerful firms.

As it turns out, the world economy is amid a historically unprecedented round of centralization of capital. According to figures from the Institute for Mergers, Acquisitions and Alliances, there has been a consistent (albeit fluctuating) upward trend in global M&A activity in both value and volume since the 1980s (Keenan and Wójcik, 2023). M&A activity has been particularly strong from the mid-2000s, which is precisely when states have started introducing legislative changes to deploy new and tighter FISM. Global M&As are currently at historic highs, reaching a record-breaking $5.9 trillion in transaction values in 2021. According to the consulting firm Bain and Company (2022), 47 percent of these M&As are ‘strategic’, that is, acquisitions conducted by non-financial firms in order to expand production capacities, gain access to new geographic markets and customer bases, concentrate market power, acquire new sources of raw material or strategic suppliers, or gain control of key technologies, intellectual property, intangible assets, technical skills, and operational know-how (Alami and Dixon, 2022, 2024; Keenan and Wójcik, 2023).

Why has this process of capital centralization via strategic M&As accelerated and reached historic proportions? This, largely, is a story of uneven geographical development and differential paces of industrial capital accumulation across sectors since the early 2000s. First, financialization has played a key role, insofar as ‘financialized modes of competition … have increased the attractiveness of M&As as they provide solutions to strategic and operational challenges while simultaneously capturing financial synergies, boosting short-term earnings and increasing shareholder value’ (Keenan and Wójcik, 2023: 7). Second, and relatedly, financialization has unfolded against the backdrop of industrial restructuring and transformations in firm organizational strategies. Schwartz's work is particularly insightful here (Schwartz, 2022). He argues that contemporary industrial organization has developed into a three-layer industrial structure:

A top layer of ‘intellectual monopoly capitalism’ (Durand and Milberg, 2020; Baines and Hager, 2023), where firms capture high profit volumes by monopolizing control of intangible assets, from trademarks and patents to other forms of intellectual property. Monopoly control of intangible assets is not only a source of market power and/or revenue generation (under the form of rents protected by intellectual property rights), but it also affords these firms the ability to exert control over subordinate firms and the wider division of labor along value chains, thereby empowering them to capture value produced elsewhere within the circuit of capital (Baglioni et al., 2023). Examples include Nvidia, Qualcomm, Apple, Siemens, and typically top firms in sectors with a high degree of intellectual labor, such as tech, life, and medical sciences). A second layer where firms generate profits through control over highly capital-intensive productive assets and/or the possession of tacit knowledge. Examples include Foxconn, TSMC, or top brand automakers. A third lawyer of firms focusing on labor-intensive manufacturing and service production, where profits derive largely from squeezing labor as much as possible. Examples include pharmaceutical industry contract manufacturers, automotive part suppliers, and light electronics assembly firms.

6

The key point is that strategic M&As increasingly play an essential role in the corporate profit strategies of all three layers of firms, and especially the first two (Schwartz, 2022). The first layer of firms engages in offensive acquisitions to preempt potential or nascent competitors (thus maintaining barriers to entry and preserving market power), but also to acquire strategic portfolios of patents and other intellectual property, and to prevent disruptive innovations. These strategies are particularly prevalent in the ‘big pharma’ and biotech sectors (Fernandez and Klinge, 2020). Firms in the second layer tend to acquire existing competitors to expand control over production, achieve larger economies of scale and scope, and raise the mass of capital in circulation to generate higher profits. In this layer too, competitive production and innovation processes depends more and more on collecting digital data (about labor processes, workflows, inventory fluctuations, consumer behavior, etc.) within broader production and logistical networks (Rikap and Lundvall, 2021). Firms therefore also engage in M&As in pursuit of core technologies around data and digital. Finally, firms in the third lawyer engage in M&As horizontally as well, to expand the scale and scope of their operations, and to maintain some pricing power with respect to firms in the other two layers.

Three additional factors have led to an intensification of this process of capital centralization via strategic M&As. First, the post-2008 global financial crisis world has been characterized by cheap and abundant liquidity (at least until the post-COVID-19 bout of inflation). Firms have therefore been able to leverage the financial system (both cheap credit and outsized market capitalization) to engage in strategic takeovers and M&As. Second, firms extracting raw materials and related products (food, and agro-chemicals; energy, hydrocarbons, and mining) have benefitted from the commodity super cycle (which lasted from the early 2000s to the mid-2010s), and have used these large rents to acquire competitors and secure new natural resource assets (land, energy supplies, etc.) across diverse geographies (Bowman, 2018; Clapp et al., 2021). Third, firms in the second and third tier of industrial structure have been particularly exposed to tendencies of overcapacity. The formation of global and regional divisions of labor has indeed led to an immense increase in manufacturing capacities. This has aggravated tendencies toward overcapacity across a range of industrial sectors (including agro-chemicals, shipbuilding, aluminum, steel, coal power, solar panels, etc.) and intensified global competition between industrial firms. Facing this context, industrial firms prefer to grow and sustain profitability rates by acquiring other firms than by accumulation proper (Alami and Dixon, 2022). This, however, does not decrease competition, but merely displaces it to the realm of M&As, as firms compete for limited strategic investment opportunities.

Importantly, what firms experience as intensified competition for market share and access to strategic assets and investment opportunities, nation-states experience as growing geoeconomic rivalry in the realms of international trade, investment, and technological leadership. The channels through which inter-firm competition translates into interstate geoeconomic rivalry are diverse. They can be direct (corporate lobbying by business groups or individual firms, 7 issuing industry reports and position papers, parliamentary representation, close contacts between government officials and large firms) and indirect (macroeconomic aggregates such as pressure in the balance-of-payments, data on sectoral external competitiveness, or on foreign M&As and takeovers involving domestic companies). Which is why states have been increasingly implicated in the varied processes of centralization of capital earlier described. States have offered credit subsidies, tax cuts, and other forms of strategic backing to support the transnational expansion of their national champions, and their absorption of competitors. States have also increasingly mobilized state-owned enterprises, policy banks, sovereign wealth funds, and other state-controlled corporate entities to either directly acquire strategic competitors and assets, to offer liquidity to private firms, or to act as co-investors with the private sector (Alami and Dixon, 2024). In addition, state capitalist vehicles have been used as defensive tools. Germany, for instance, has used the investment arm of its main policy bank, KfW, to co-invest in domestic firms with foreign investors. This is to prevent foreign investors from acquiring controlling stakes in domestic firms. France and Italy have used their respective strategic investment funds (Bpifrance and Cassa Depositi e Prestiti Equity) to perform similar functions.

This multifaceted involvement of state capitalist instruments in strategic M&As has resulted in a growing fusion of private/state capital, and an increasing integration of the latter into global corporate networks of ownership and control (Alami and Dixon, 2022; Babić, 2023; Haberly and Wójcik, 2017). This creates major tensions: it makes it harder to trace ultimate ownership or effective state influence on particular investment transactions, which raises suspicion that foreign actors with deep pockets may be able to swiftly capture key productive assets or intellectual property which took years and considerable expenses to develop. This explains why FISM in technologically advanced economies have been expanded to cover ever more high-value-producing activities, core technologies, and intellectual property, as well as to cover the more complex and diverse modalities of centralization earlier discussed. This also explains why FISM national legislations are geographically variegated across countries, notably in terms of their sectoral coverage: factors explaining the latter include a country's sectoral specialization and geographical position in global and regional divisions of labor, and the presence of firms in the three-layer industrial structure discussed earlier.

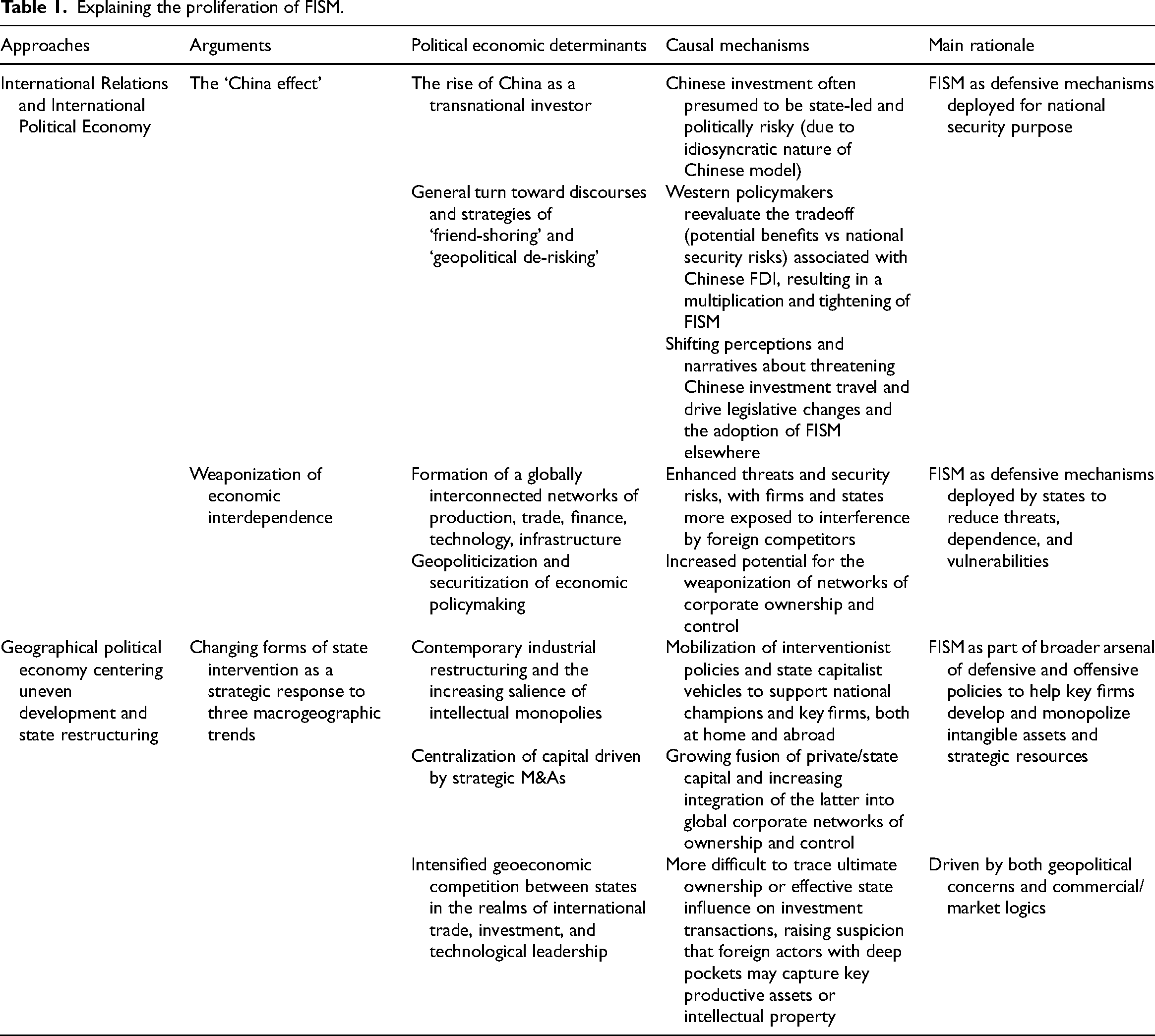

In sum, the profusion and tightening of FISM over the past 15 years are responses to a strategic context structured by three interrelated macrogeographic trends: (1) contemporary industrial restructuring and the increasing salience of intellectual monopolies; (2) a historic episode of centralization of capital driven by strategic M&As; and (3) evolving landscapes of state capitalism under conditions of intensified geoeconomic competition. To be clear, this is not to downplay the animosity that China's involvement in all three trends increasingly generates among western policymakers and state managers. Nor is it to downplay the anxieties resulting from the objective vulnerabilities inherent to the networked structure of the world economy. But none of these factors can be fully grasped without reference to these macrogeographic trends. The argument so far is summed up and contrasted to the existing literature in Table 1.

Explaining the proliferation of FISM.

Now that we have identified the geographic political economic determinants of FISM, we can turn to what is it exactly that they do, and how do they do it. FISM are introduced via legislative changes and statutory acts, and they mobilize legal notions such as sovereignty, national security, public order, national interest, and the like. They also affect cross-border capital mobility, which is itself legally codified and made possible through the law in the first place. In other words, we must take seriously that FISM are creatures of the law. As such, what sort of state power do they legally codify and give force to? With what implications for geographies of investment regulations, globalization, and neoliberalism?

Legal geographies of foreign investment screening

This section draws on conceptual insights from legal geography scholarship (Blomley, 2021; Delaney, 2015), and, particularly, on approaches that center power and political economy (Orzeck and Hae, 2020). From this perspective, law is constitutive of the operations of political and economic space, and it is intrinsic to patterns of capitalist development, crises, conflicts, and contradictions (Tzouvala, 2020; Hunter, 2021). The law plays an active role in structuring state activities and patterns of globalization (Barkan, 2011; Potts, 2020). It ‘polices the spheres of politics and the economy while mediating their interrelation’ (Barkan, 2011: 603). How the law invests the state with powers is key to understanding the nature of the intervention, its workings, its spatialities, and its impacts on globalization. In what follows, I use these conceptual resources to analyze FISM. I make three arguments: (1) scrutinizing the ways in which FISM operate as an exceptional form of law allows to understand how they fit within the legal architecture of globalization and the disposition of state power that they legally codify; (2) FISM contain strategic legal ambiguities, which afford states considerable room for maneuver to exercise power over investment transactions: (3) FISM function as boundary-making practices, which construct differentiated legal geographies of cross-border investment regulations.

FISM as exceptional forms of law

FISM operate as exceptional forms of law. They do so in the prosaic sense that states often implement FISM as temporary, ‘interim’ measures before making them permanent. France, for instance, made permanent in 2023 the tighter regulations that it had first established as emergency measures during the COVID-19 pandemic and Russia's invasion of Ukraine. Moreover, FISM operate as exceptional forms of law insofar as they directly mobilize legal exceptions, such as the clause of national security in international law. The invocation of national security allows states to legally deviate from the rights and obligations that they commit to when they enter into international trade and investment agreements, such as principles of nondiscrimination, free and fair competition, market neutrality, and investor protection (Vidigal and Schill, 2021). National security clauses are common provisions in international economic law and are key to the global architecture of trade and investment governance (e.g. in Article XXI of the World Trade Organization). They play a fundamental role in ensuring that states, under certain conditions, can exert sovereign authority over the entry of foreign investors, including in ways that temporarily and exceptionally suspend the rights and obligations that they legally agree to in the context of trade and investment agreements. As such, they function as a safety valve for the global investment regulatory regime, and the continual use of these exceptions is central to its functioning (Lang, 2019; Meyer, 2022). National security exceptions are both exceptional and permit the regular functioning of the legal regime.

Thus, the use of legal exceptions does not signal states retiring from the global investment regulatory regime and its legal architecture of rights and obligations codifying norms of free capital mobility and investor protection. What is worthy of attention in the case of FISM, however, is how they reposition the role of the exception within these norms, and under what conditions it can be mobilized. Indeed, as they become tighter, FISM carve out additional space and legal terrain for a more extensive mobilization of the national security exception, by offering more expansive criteria defining how it can be used, as well as for what purpose (more on this below). They therefore use existing legal rights and mechanisms to legally enshrine new and more extensive state prerogatives, related to the monitoring, surveillance, and potentially direct intervention in cross-border investment transactions. This affords states the ability to position themselves as obligatory passage points in transnational circuits of investment. This is not a move away from an open investment regime and globalized investment flows; this is about establishing a new disposition of state power within it. The legality of the national security exception is a cornerstone of this rearticulation of state power.

However, the more expansive FISM become, the more they stretch definitions of national security exceptions, and the more the gap between how these exceptions are interpreted in domestic and international law widens. This puts the global legal investment regime under strain. Besides, states become more exposed to legal claims that they de facto abuse such exceptions. Indeed, for national security exceptions to function as a safety valve, they must remain limited in scope. As two international lawyers put it, they must be ‘subject to conditions and limitations to ensure good faith use and prevent abuse’ (Vidigal and Schill, 2021: 112). This is so that various state and market actors accept their legality, and so that FISM remain embedded in a liberal investment regime, which must be coherent, transparent, predictable, and rules-based. Yet, notions of national security are characterized by considerable malleability, which is key to how FISM operate.

The malleability and practical ambiguity of FISM

As FISM regimes become more expansive and sophisticated, they also become more institutionalized and routinized. Most FISM legislations specify ‘explicitly the scope, coverage, rationale and conditions under which the scheme is applicable, including a procedural timeframe and an expiry period for the exercise of the blocking power by the relevant authority, as well as a clearly defined set of rights, obligations, sanctions, and remedies for the investors concerned’ (UNCTAD, 2023: 8). This is key to giving investment screening, which is an inherently political practice, a pretense of universality, rationality, and predictability. Institutional routines and procedures are necessary to portray investment screening as a formal practice that is neatly defined and contained within liberal boundaries, and itself governed by (and subject to) the depoliticizing rule of law.

Nevertheless, there is a clear tension between, on the one hand, these procedural, depoliticizing, and technocratic features, and, on the other, the remarkable malleability and fluidity of FISM. The repeated extension of the list of sectors and activities covered by FISM clearly denotes flexibility in how the legal exception of national security is operationalized. There is also considerable ambiguity across national legislations about how it is even defined or assessed. ‘Some assessment provisions are deliberately left open to interpretation … which can add to the uncertainty associated with FDI screening regimes’ (UNCTAD, 2023: 11, emphasis added). For instance, the Canadian FISM asserts that the state can intervene if ‘there are reasonable grounds to believe that the investment could be injurious to Canada's national security’ (Government of Canada, 2023: nd). It also states that security risks can be assessed on the basis of a very expansive list of criteria, such as the impact of the investment on ‘the level and nature of economic activity in Canada, including employment, resource processing … components and services produced in Canada … the effect on productivity, industrial efficiency, technological development, product innovation and product variety in Canada; the effect on competition; the compatibility with national industrial, economic and cultural policies; and the contribution to Canada's ability to compete in world markets’, and more generally, ‘the Minister is satisfied or is deemed to be satisfied that the investment is likely to be of net benefit to Canada’ (see Investment Canada Act, paragraphs 20–21).

Ambiguous definitions and operationalization of the concept of national security render FISM extremely flexible mechanisms, which affords states a wide margin of regulatory discretion. This is a case of the law offering a degree of what legal geographer Delaney calls ‘practical ambiguity’ (Delaney, 2015: 99). Although the law appears to be codifying a neatly defined and stable domain of intervention, the flexibility, fluidity, and ambiguity of notions of national security offer states considerable room for maneuver to exercise power (other examples of loosely defined legal notions which play a similar role in FISM include: ‘distortions to the smooth functioning of the economy’, ‘disruptions to public order’, ‘market distortions’, and the like). This, however, exposes states to the possibility that decisions based on loose definitions of national security could be contested by investors, and brought before an international court or arbitration tribunal. Yet several states have already declared that they would not recognize the judicial authority of said institutions in defining what is national security (Vidigal and Schill, 2021: 2014). Besides, only a fraction of FISM afford the investor a right to judicial appeal against a decision blocking a proposed transaction (UNCTAD, 2023: 13). In other words, states are explicitly hedging against dispute resolution protocols, by declaring that only they can define and unilaterally declare where and when security exceptions apply.

There are two takeaway points here. First, FISM's practical ambiguity is key to reconfiguring state power and authority to regulate strategic investment, in ways that make it broadly compatible with the legal architecture of globalization, while allowing considerable discretionary power. This marks a shift from judicialization and legalization in FDI policy to domestication, bureaucratization, and flexible uses of the law. 8 Second, and simultaneously, FISM regimes are gradually reworking (and bending) norms concerning how the security exception can be used and under what conditions it can be legitimately mobilized within this legal architecture. The strategy of leveraging practical ambiguity has been relatively successful so far, yet it is precarious and necessarily limited in terms of how far states can go, before FISM appear as plainly arbitrary, and drive an unbridgeable chasm between domestic and international interpretations of national security exceptions. This would risk collapsing their legality, and therefore the legal basis of the powers they bestow upon states. This would also risk further politicizing investment relations, which international economic law precisely aims to prevent.

To negotiate the tensions inherent in their practical ambiguity, FISM offer neat categorizations of the investors, sectors, and transactions that fall under their purview. As shown in the next sub-section, this allows maintaining the appearance that, although FISM afford wide discretionary powers to the state, those are confined within a formally delimited and legally coded perimeter of action. This ostensibly presents state power as indeed subjugated to law, and investment screening as lawful practice.

FISM as boundary-making practices

The law does not simply operate on a preexisting terrain; rather, it codifies practices by actively delimiting its domain and object of authority, and its mode of action over them. It does so by functioning as a ‘boundary-making’ practice and discourse (Barkan, 2011; Christophers, 2014; Potts, 2020). The ‘“law” draws lines, constructs insides and outsides, assigns legal meanings to lines, and attaches legal consequences to crossing them’ (Delaney, 2015: 99). It often operates as a form of what Potts (2020) walls ‘reasoning by dichotomy’: it establishes neatly separated dichotomous categories (such as foreign/domestic, public/private, and political/commercial) which are then subjected to differential legal treatment. These categorizations, and associated practices of inclusion and exclusion, are not neutral representations of political economic processes, but a form of ordering them (Barkan, 2011: 10; Delaney, 2015: 99). Boundary-making practices ground the generation of ‘legal truths’ about political economic processes: they ground particular ways of understanding, representing, and acting upon them (Christophers, 2014: 432).

The practice of investment screening codified in FISM is fundamentally an exercise in classification, conceptual recategorizations, and market ordering. It does so in several ways. First, as already extensively discussed, FISM establish a jurisdictional delineation between sectors and activities considered sensitive/strategic/critical, and those which are not. More and more sectors are included in this category on the presumption that they are particularly exposed, or prone to, ‘malicious’ foreign investment behavior (as the 2021 UK National Security and Investment Bill puts it). Their inclusion in this category grounds legal truths about risks and potential market power abuse associated with foreign takeovers and M&As in these sectors, which warrants the invocation of national security exceptions. This in turn justifies the differential treatment of these sectors: foreign investment targeting entities or assets in these sectors are regulated by a different investment regime, with enhanced state scrutiny and surveillance.

Second, FISM operate another form of delineation and boundary-making based on the nature of the investor. They establish different categorizations of investors based on their association (presumed or effective) with foreign states. Entities typically singled out are those directly controlled by foreign governments through ownership (at least 11 FISM national legislations have provisions targeting foreign state-owned entities, according to UNCTAD's Investment Policy Hub). However, more and more legislations now explicitly mention that it can be difficult to trace ultimate ownership or effective state influence due to complex chains of ownership and control. They include broader definitions of how firms can be influenced by foreign states, including via funding and subsidies (see, e.g. Regulation EU 2019/425, or the Slovakian FISM). These very broad definitions allow recategorizing a wide range of entities as belonging to this category and therefore legally falling under the purview of screening procedures. Stretching the boundaries of the category of investors considered to be potentially influenced by foreign states thus legally empowers states to exercise discretionary powers over transactions involving a remarkably wide range of actors.

Third, a similar dynamic is at play in the categorizations performed by FISM based on the type of transactions. Insofar as FISM are fundamentally about intervening in transactions that lead to a redistribution of ownership and control, it is unsurprising that they target explicitly takeovers and M&As. Nevertheless, as FISM have been tightened, the tendency has been to redefine, in a more expansive way, what counts as effective or potential control, with the effect of including a much wider set of transactions under their scope, including minority investments. Many national legislations have lowered thresholds (in terms of transaction value or in terms of foreign capital participation) supposed to indicate effective or potential control. For instance, in France, a transaction triggers the FISM when a non-European Economic Area investor crosses the 10% threshold, even if the foreign investor does not acquire controlling rights, and even if the targeted firm or asset remains technically controlled by a French entity. 9 Some FISM legislations include criteria to assess not only effective control but also ‘material influence’, commonly defined in competition law as the ability to influence the target entity's policy. Such criteria include the acquisitions of voting rights, or the presence of foreign actors on boards of directors. FISM therefore effectively recategorize a broad array of financial transactions as leading to potential foreign control and/or material influence, which subjects them to state power under the form of screening practice.

In sum, the three forms of boundary-making and jurisdictional delineation performed by FISM (based on different types of sectors/investors/transactions) allow for a powerful reclassification of vast swathes of transactions previously considered to be within the ambit of the private sphere of market activity. These demarcations produce legal truths and impose moral differences about foreign investment behavior: on the one hand, ‘benign’, desirable, commercially oriented transactions, to be governed by an open, liberal investment regime and substantive obligations of investor protection; and on the other, potentially ‘malicious’ and therefore undesirable investment, to be subject to extra-scrutiny, prior approval, disclosure requirements, filing obligations, sanctions in case of noncompliance, or mitigating measures to change the terms of the investment deal. In other words, pace the IR/IPE literature reviewed earlier, FISM are not simply about policymakers re-assessing the tradeoffs associated with FDI. Rather, FISM construct differentiated legal geographies of investment regulations, characterized by distinct regimes of investor's rights and obligations and legally sanctioned state authority. Under the pretense of weeding out malign actors, blocking adversarial foreign investment, and defending the liberal properties of markets, FISM carve out (through law) a remarkably broad domain of state intervention into the competitive dynamics of centralization of capital.

Finally, FISM produce a fourth type of categorizations based on geographic origin and/or geoeconomic groupings. By definition, FISM discriminate based on a foreign/domestic distinction. Yet many national legislations do more than that. For instance, FISM in 12 European states specifically target investors not belonging to the European Union. At least four other states specify that their FISM applies to investors not belonging to the European Economic Area, and another four to investors not belonging to the European Free Trade Association (UNCTAD, 2023: 8–9). Some governments have also started to introduce exemptions or simplified procedures for investors coming from countries belonging to specific geopolitical groupings. For example, US allies in the context of the Five Eyes intelligence alliance (Canada, Australia, the UK, New Zealand) qualify as ‘excepted foreign states’ under the new rules of the U.S. FISM, as long as they continue to demonstrate that their respective FISM are sufficiently tight to prevent them serving as ‘backdoor routes’ to the USA for potentially risky foreign investments (CFIUS, 2023).

This suggests that FISM could be increasingly deployed in the future as tools of geopolitical and geoeconomic alliances, with the objective of shaping legal geographies of investment regulations in ways that disadvantage competitors. Moreover, FISM could be used as leverage to push other states to adopt tight(er) screening regimes. This would effectively make FISM channels through which powerful states can exercise extra-territorial powers to shape the form and direction of globalization. There is already some evidence of this. In 2016, a deal between the Chinese Fujian Grand Chip company and the German chipmaker Aixtron was blocked by the USA, because Aixtron owns a subsidiary on American territory. This episode arguably played an important role in the decision to tighten FISM in Germany in 2017, demonstrating the extra-territorial implications of FISM (Chan and Meunier, 2022).

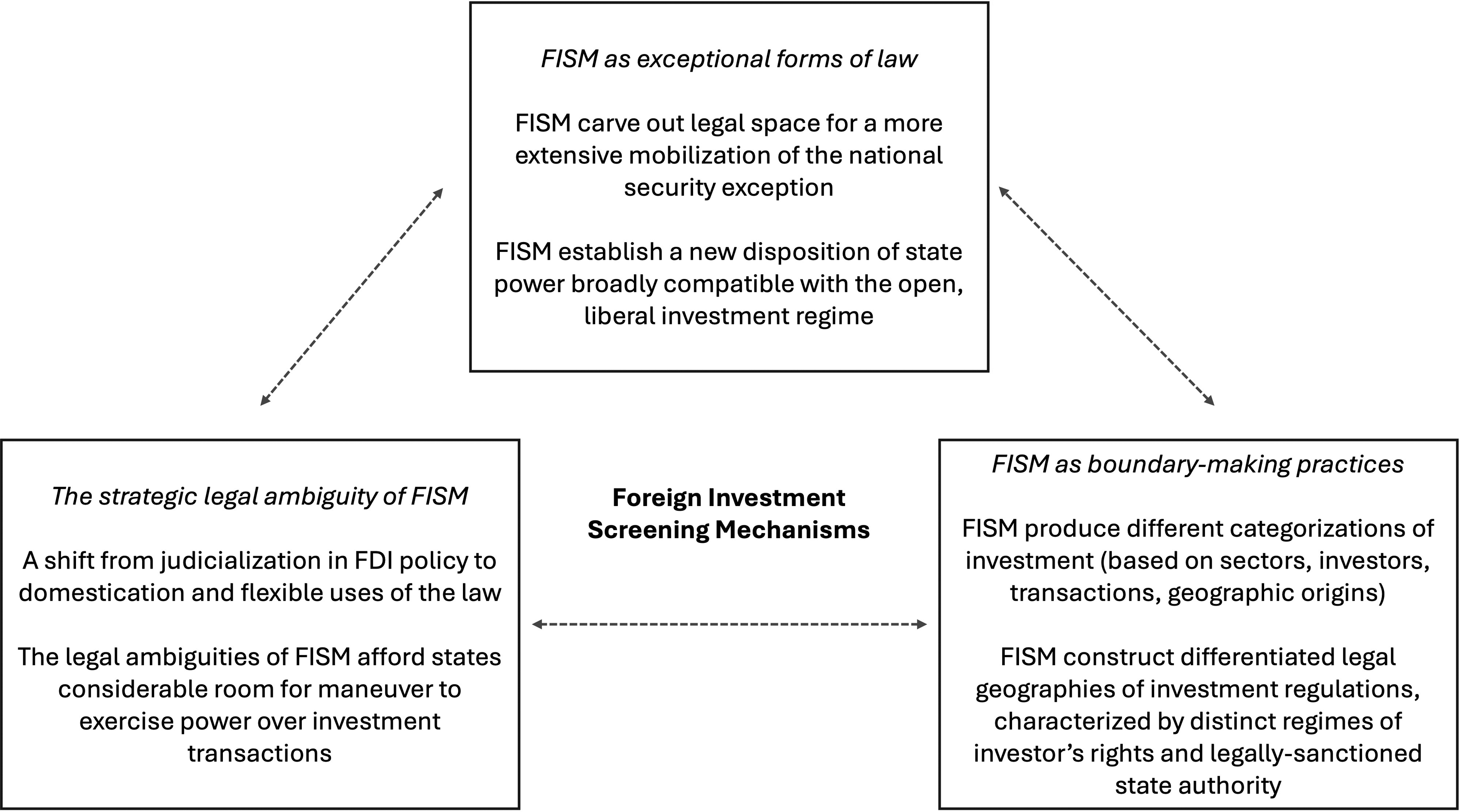

Finally, there is some evidence that FISM can be mobilized for other geostrategic purposes than to compel other states to implement similar mechanisms. They can be used as bargaining ships in the negotiation of bilateral investment deals and reciprocal market access, or, put differently, to open new geographies of outward foreign investment. FISM in Europe ‘have a tangible external economic policy justification and outlook. They empower the EU in its trade and investment negotiations with third countries to achieve, on the basis of reciprocity, better access of EU investors to third-country markets in return for limiting screening in the EU of inward FDI coming from the EU's treaty partners’ (Schill, 2019: 108). FISM strengthen ‘the EU's bargaining power in bilateral negotiations with economically powerful countries, such as the USA and particularly China, with whom the EU seeks to establish comprehensive treaty rules governing reciprocal access for, and protection of, foreign investment’ (Schill, 2019: 108). My argument on the legal geographies of FISM is summarized visually on Figure 3.

Legal geographies of FISM.

Conclusion

We can now answer the questions raised in the introduction concerning FISM and the future of (de)globalization, neoliberalism, and the remaking of the world economy. First, there are reasons not to understand the tightening and proliferation of FISM as signaling a backlash against globalization. FISM are firmly embedded in trends which have been, and continue to be, major drivers of globalization (notably, the formation of global and regional divisions of labor, global industrial restructuring, strategic corporate reorganizations, and the centralization of capital via strategic M&As). As regulatory transformations, FISM do not buck these trends; they accompany their continuous (if antagonistic) development, and politically mediate their contradictions in novel ways, under conditions of intensified geoeconomic competition. Rather than a protectionist reaction against globalized economic flows, they afford states the ability to firmly position themselves as nodes, or obligatory passage points, in transnational circuits of investment. They bolster states’ capacities to act as a vigilant figure in such circuits, surveilling and monitoring a wide range of cross-border transactions, always in the position of flexing muscle. This argument speaks to recent calls to (re-)center themes of geopolitics and risks in economic geography, insofar as geopolitical tensions and rising nationalism are ostensibly leading forces in the ongoing restructuring of economic globalization (cf. Gong et al., 2022; Yeung, 2023; Potts, 2023). The emerging couplings of geopolitics and state regulatory powers over investment flows analyzed in this article do not block global connectivity, but rather ‘modulate it and enable new forms of dis/connection’ (van Meeteren and Kleibert, 2022: 400). More precisely, although FISM reproduce the fiction of state power as expressing the will of the sovereign nation to defend itself against foreign interference, market distortion, and technology theft, they essentially consist in legally enshrining state authority to support national champions and other domestic firms, and making sure they engage favorably with competitive dynamics of centralization of capital, notably by conserving their monopoly over intangible assets and strategic resources.

Second, framings of FISM as defensive assertions of national sovereignty over globalized economic ties downplay their role in facilitating the extra-territorial expression of state power, such as when they aim to defend the competitive advantages of national champions globally, and their ability to capture value produced elsewhere in the world economy. FISM are best seen as tools to aggressively (re)negotiate globalization. Economic and political geographers increasingly pay attention to the multifaceted role of the state in reconfiguring global production networks, including by acting as promoter, regulator, investor-shareholder, and direct owner of capital (Alami and Dixon, 2024; Hess, 2021; Horner and Alford, 2019; Werner, 2021; Whiteside et al., 2023). The role of the state as investment screener develops in dialectical tension with these other roles, at times in a complementary manner (such as when FISM are functionally integrated into techno-industrial strategies), or in direct conflict (such as when FISM are deployed as a competitive response to the transnational expansion of foreign state-owned or state-supported firms). The power and salience of the law as a cornerstone of these processes of state restructuring has been underexplored so far.

Third, FISM do not signal states withdrawing from globalization, but a partial renegotiation of how such project was legally coded over the past two decades, notably the global investment regulatory regime and its legal architecture of rights and obligations. FISM are stretching norms concerning the conditions under which the national security exceptions can legitimately (and lawfully) be mobilized. While this creates real tensions in the global investment governance regime, this has so far allowed the construction of differentiated legal geographies of investment regulations, characterized by distinct regimes of investor's rights and obligations and legally sanctioned state authority. FISM contribute to the production of an extended legal space empowering states to intervene in cross-border investment transactions, bending the existing legal architecture of globalization. This lends support to Potts’ argument that global economic geographies are being reconstituted today by the increasing complexification and layering of governance arrangements, characterized by overlapping and sometimes contradictory formal and informal rules and institutions (2023: 683).

Fourth, arguments that FISM constitute a break with neoliberalism are premature, insofar as the novel disposition of state power codified by FISM does not reject norms of free capital mobility and does not break with general commitments to investor protection. The national legislations establishing FISM are at pains to re-affirm strong commitments to these legal norms. They do carve out an exceptionally broad domain of state intervention into investment relations, yet as boundary-making practices, they also work toward establishing (and policing) neat separations between the economic and the political, in characteristically neoliberal fashion. None of this is to say that ongoing changes are not significant. In my view, FISM are evidence that states are increasingly struggling to conciliate the two contradictory imperatives at the heart of what Davies calls ‘the distinctively neoliberal paradigm’ namely, ‘upholding the market as a legally-mandated universal norm of social organization, while nurturing the most innovative, competitive and powerful firms and territories’ (Davies, 2020: nd). The construction of differentiated legal geographies of investment regulation is arguably an attempt at finding new legal, institutional, and geographical mediations of these two imperatives. FISM allow leaning more heavily into the latter, while not relinquishing the former (for now, at least).

Fifth, this argument speaks to ongoing debates, among régulationists and others, on the current evolution of neoliberalism as a mode of regulation (Boyer, 2020; Durand, 2023; Jessop, 2019). According to the régulationist canon, a mode of regulation is characterized by a hierarchical articulation of institutional forms (i.e. the capital-wage labor nexus; the monetary and financial regime; the type of competition; the modalities of state intervention; the form of integration into the world economy; the regulation of cross-border trade and investment; etc.). A re-organization of these institutional forms and how they relate to each other may suggest the emergence of a new mode of regulation. In my view, the dynamics of macro-institutional change analyzed in this article do not suggest that is currently the case. Firmly anchored in the neoliberal paradigm, this reconfiguration is best seen as a mutation in response to the macrogeographic transformations in the structure of accumulation discussed earlier. This macro-institutional adaptation is not stabilizing but generating new scalar contradictions in the mode of regulation, notably between aggressively nationalist forms of neoliberalism at national and sub-national scales, and the neoliberal transnational architecture of the world economy.

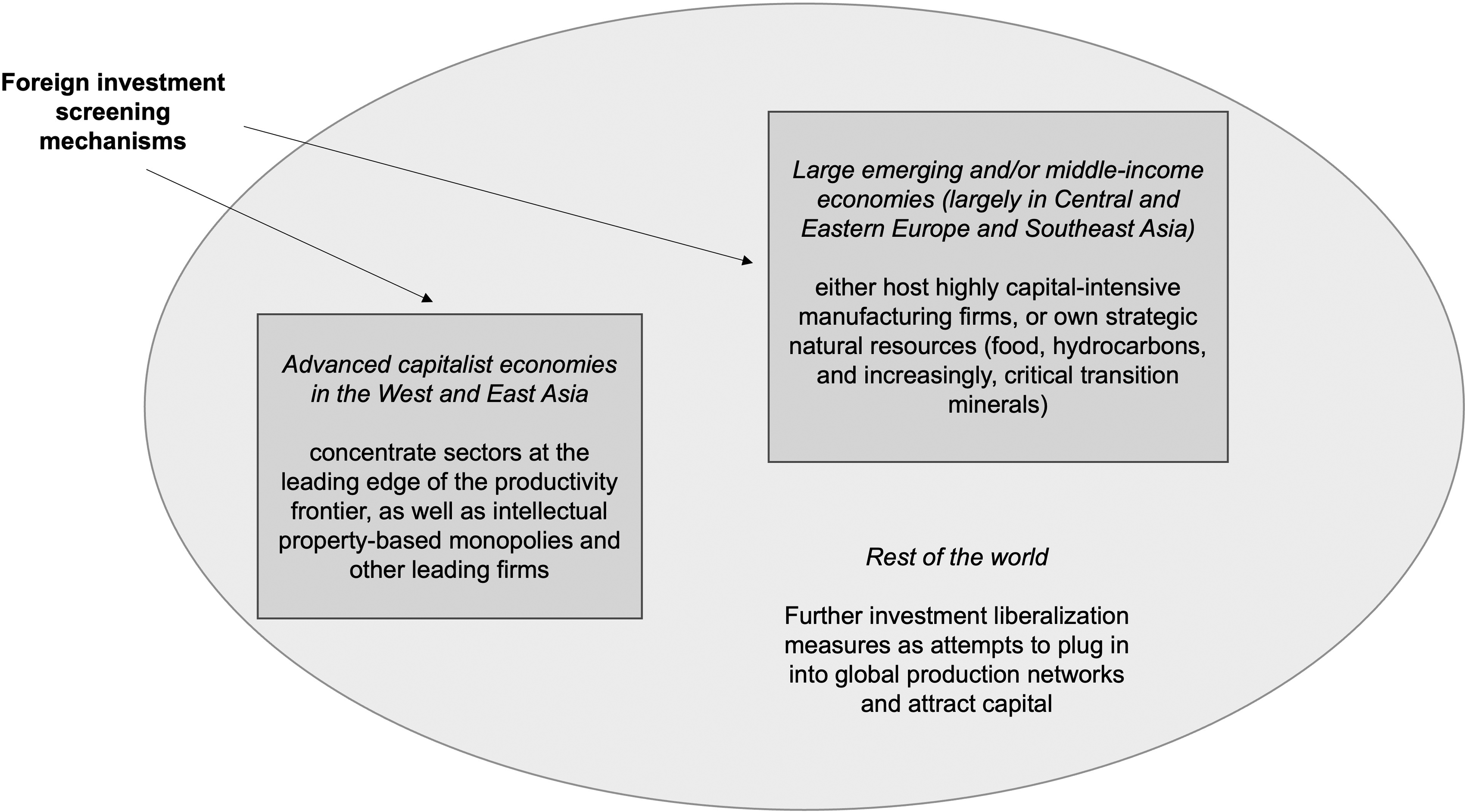

Sixth, it is worth emphasizing that only one country in Africa (South Africa) and one country in Latin America (Mexico) have implemented FISM. In most developing countries, the tendency is overwhelmingly to continue to liberalize and facilitate foreign investment (UNCTAD, 2022). 10 What we see overall is therefore not a reversal of the investment liberalization trend globally, but rather, uneven geographies and temporal rhythms of investment control and liberalization. This geographical unevenness and partially diverging patterns of regulatory reform reflect the process of industrial restructuring, and resulting three-layer corporate structure, discussed in the third section. The general picture is this: for the most part, FISM are deployed in advanced capitalist economies (in the west and East Asia) which disproportionately concentrate sectors at the leading edge of the productivity frontier, as well as intellectual monopolies and other leading firms in the first layer of global industrial structure. FISM are also established in large emerging and/or middle-income economies (largely in Central and Eastern Europe and Southeast Asia), which either host highly capital-intensive firms (in the second layer of industrial structure) or own strategic natural resources (food, hydrocarbons, and increasingly, critical transition minerals). This highly schematic picture is necessarily limited but gives a general sense of the economic geographies underpinning FISM, as shown on Figure 4. These uneven economic geographies in turn underpin and reproduce unequal political power relations between states, and the capacity of richer and more powerful economies to re-shape the rules of the global economy in ways that suit them, potentially at the expense of poorer, less powerful state actors.

Economic geographies of FISM.

In conclusion, FISM are potent mechanisms, with the potential to profoundly shape spaces of investment, competition, accumulation, and emerging geographies of globalization, all the more so that advanced capitalist states are now considering combining them with outbound investment restrictions. Future geographic research may examine their effects on, among other, corporate networks of ownership and control, patterns of technological innovation and knowledge discovery, global production networks, regional development, and extended urbanization. For this, as well as to critically engage with ongoing debates as to the future form and nature of capitalist globalization, we need creative (re)combinations of political economy, economic geography, and legal analysis.

Footnotes

Acknowledgements

An earlier version of this article was delivered as the 2023 Early Career Keynote Lecture in Economic Geography at the Annual Meeting of the American Association of Geographers in Denver, at the invitation of the AAG Economic Geography Specialty Group. It has benefited from discussions with Mikael Omstedt, Callum Ward, Gabe Eckhouse, Tim Blackwell, and Adam Dixon. Emily Rosenman, Nina Ebner, Joel Wainwright, Seth Schindler, and Ntina Tzouvala have generously offered in-depth comments on earlier drafts of this article.

Declaration of conflicting interests

The author declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by the H2020 Marie Skłodowska-Curie Actions (grant number 101024448).