Abstract

The Lodging Shared Economy (LSE) is made up of a complex web of parties which enables guests to stay at a host’s home either with the host at home or away from the property. Many hosts utilize an LSE Online Platform (LSEOP) company such as Airbnb or Vacation Rentals by Owner (VRBO) to rent out a host’s property to a guest and receive payments from the guest including sales and lodging taxes, and they also remit payments to hosts and government agencies. Governmental agencies receive taxes from LSEOPs and distribute taxes to appropriate government accounts. The governmental agencies also enact laws and legislation to govern the activities of guests, hosts, and LSEOPs. This complex process serves the interests of each party involved but at times these diverse interests interfere with another party’s concerns resulting in conflicts, lawsuits, and public policy. This article addresses only regulations within the United States. Using a content analysis design, it provides a summary of LSE regulations for each state, thus allowing comparisons in determining highly taxed versus lesser taxed properties and highly regulated environments versus laissez-faire destinations. Although LSE companies typically transact the financial aspects of the stay, hosts are ultimately responsible for complying with other public policy regulations such as parking, noise, trash, and traffic laws. This study analyzed the most recent court cases among LSEOPs and government entities that illustrate some of the push and pull of public policy decisions on short-term rentals across the United States.

Introduction

The LSE is best represented by companies like Airbnb and VRBO, which provide a platform for host to rent rooms and properties across the globe and are known as online marketplace distribution channels. VRBO and Airbnb emerged as companies in 1995 and 2007, respectively; therefore, the issues related to regulating their short-term rental (STR) guest activities represent a relatively recent occurrence. These LSEOP companies provide a service by virtually introducing hosts to guests for a limited number of nights, with a maximum number of possible nights determined many times by local policy regulations.

Hosts benefit by having their properties marketed professionally without the annoyance of having to personally maintain a website for their own rental or deal with any of the other details managed by LSEOP Internet sites. In addition, LSEOP companies perform reservation and financial transactions so that hosts do not need to deal with those aspects of each transaction. Similarly, potential guests enjoy the convenience of exploring potential vacation housing based on images and descriptions of the property on one website—without having to search individual host websites—one-stop shopping. Although Airbnb and VRBO are worldwide and must comply with rules and regulations from each host country, this study focused on the diverse variety of local taxation and lodging regulations within the United States. The current public policy regarding the regulations governing LSEs and the collection of taxes with regard to LSE commerce appears to be inconsistent both between the states and even within the different municipalities inside the states. This lack of consistency can create policy implementation challenges among LSE operators and may create a situation where their operations are in violation of one or more local and/or state regulations. This appears to be in stark contrast to current regulation and taxation policies for the hotel industry. This disparity in public policy enforcement creates a potential for public safety issues (e.g., sanitation and security) and a competitive disadvantage for hotels who are considered to be held to a higher standard by state governments both in regulation enforcement and in tax collections.

As part of the financial transaction, hosts are ultimately responsible for paying taxes associated with state and local taxes, lodging taxes, and other miscellaneous fees. In some cases, LSEOP companies collect and remit these taxes and fees in many jurisdictions where required. This prevents hosts from collecting fees from guests and remitting them to government agencies, which is a great convenience for LSE hosts. However, hosts are responsible for complying with public policy regulations for their given municipality such as parking, noise, trash, and traffic laws. In addition, hosts are responsible for understanding the legality of renting space on their property, especially if their property is part of a homeowner’s association or other contractual arrangement (e.g., resort or apartment complex). In fact, many municipal governments require a 24–7 point of contact to address these concerns in real time.

Many stakeholders with diverse motivations are involved with guests enjoying host properties which affect STR public policies. Guests want to enjoy their LSE experience at a reasonable price while hosts (both amateur and professional) and LSEOP companies want to increase revenues from those guests. Municipalities wish to not only increase tax revenues but also conversely ensure guests do not cause problems in the host neighborhoods such as noise or parking. Neighbors do not want to be inconvenienced by guests’ noise, parking, or traffic issues.

Finally, hotels want a level playing field including the imposition of hotel taxation for LSE properties with the claims that LSE properties perform the function of a hotel and compete with hotels but are not required to pay hotel or bed taxes in many municipalities (Leshinsky & Schatz, 2018). In addition, some city planners fear that LSE patronage will lead to gentrification, resulting in housing values escalating to the point where residents can no longer afford to live in these neighborhoods overrun by LSE guests (Dudás et al., 2017; Gurran et al., 2018). Balancing these various objectives has led to many legal battles and the creation of many regulations specific to STRs. Many popular vacation spot municipalities have been more proactive in creating rules and regulations to protect their constituencies, while other municipalities are still on a learning curve for instituting appropriate hotel taxation and rental regulations.

An example of a lack of understanding or refusal to obey existing regulations includes a couple in Denver, Colorado who was arrested for renting out a secondary residence because the local laws required hosts live in their domiciles to lawfully rent them (McCann, 2019; “What Regulations Apply to my City?” n.d.). Other jurisdictions have instituted severe fines such as in El Segundo, CA, where the “program has a two-strike policy. A first violation generates a $2,500 fine; a second violation is a $5,000 fine and leads to the short-term home share permit will be revoked” (El Segundo City, n.d., p. 1). These regulations stand in contrast to other jurisdictions who are not as punitive in nature. This patchwork of regulations ranging from the very prescriptive to the laissez-faire leads to confusion among the stakeholders, and it is crucial for LSE hosts to know and keep abreast of all rules and regulations that pertain to their rental property.

Some LSEOP companies have been accused of not collecting hotel taxes until local municipalities require them to do so. According to their website, Airbnb claims to be following taxing rules and regulations in the areas it provides rentals (“Responsible Hosting in the United States,” n.d.), but there are questions on whether their compliance is comprehensive or merely agreeing to comply in specific municipalities only when they are found in defiance of collecting local taxes, with a “catch me if you can” approach. This tactic places the burden of proof on municipalities to prove and pursue wrongdoing, which requires public resources to find and issue fines and warnings to hosts.

Martineau (2019) reported that a Palm Beach, Florida tax collector had been trying to collect taxes for more than 5 years and many lawsuits; however, Airbnb’s public policy head, Chris Lehane, reportedly said to a gathering of mayors, “Read my Lips: We want to pay taxes.” (p. 1). Anne Gannon, Palm Beach County Tax Collector’s reply was, “All we want them to do is pay their taxes” (Martineau, 2019, p. 1). Kaplan and Nadler (2015) claim Airbnb works diligently with taxing officials to lawfully pay required STR taxes. Crommelin et al. (2018) suggest that Airbnb has much information at its disposal that it could share to help build public policy that accommodates all involved parties, but they (Airbnb) are apparently not willing to do so, citing confidentiality as their justification. Leshinsky and Schatz (2018) suggest an alternative method might be to have a collaborative and cooperative approach between municipalities, the host, and the LSEOP company to not only address these violations but also do so without using public funds.

This study also analyzed the impact politics play in various rental offerings in different municipalities. Specifically, this study reviewed if certain states or regions have more or fewer policies than others for rental hosts. Policy differences were shown to exist even within the same state. For example, Airbnb lists 43 distinct sets of regulations for different cities and taxing municipalities within California (“Responsible Hosting in the United States,” n.d.).

LSE Industry

The LSE allows homeowners to rent their domiciles using LSEOP companies as intermediaries to make money, while at the same time, offering STRs to guests at either a less expensive price or offering a different experience to guests than might be available at a hotel (Kreeger, 2020). Barnes and Mattsson (2016) found that low price was the major reason guests chose an LSE property over a hotel room. Airbnb was founded in 2008 and by 2012 and claimed 141,000 rooms rented on New Year’s Eve of that same year—a sum of rooms representing almost 50% more rooms than those contained on the Las Vegas strip (Geron, 2012). VRBO preceded Airbnb and was founded in 2007 to rent out a condominium in Breckenridge, Colorado. It has grown from this one listing 25 years ago to more than two million listings today (“A History of Vrbo Timeline: 25 Years of Bringing Families Together,” 2022).

Literature Review

This study explored methods and regulations used across the nation to achieve a compromise between the positive taxes generated by LSE rentals and neighbor frustrations generated by guests as mentioned by Binzer (2017). Focused on a stricter regulatory environment, Smigiel (2020) presented a case for more stringent regulations and accountability for LSEOP companies to ensure a better balance among tax revenue collection, host revenue generation, and satisfactory guest utilization. Although many hosts rent their current home and do not have a choice of where they can offer rentals, fee-based companies such as AirDNA assist hosts to identify the best and worst cities to conduct STRs of their properties based on five criteria to maximize profitability for hosts (Shatford, 2016). There are other companies that assist hosts in assessing the viability of offering an LSE property for rent including Avalara, which is a company that specializes in managing and consulting lodging taxes (“Industry Solutions: Short-Term Rental,” n.d.).

The state of Arizona is a good example of a compromise between the desire to attract the tax dollars from short-term lodging rentals and the necessity of protecting residents from excessive noise and traffic from additional LSE guests in each neighborhood. Arizona’s Senate Bill 1350 was passed in 2016, which prevented jurisdictions from banning LSE lodging opportunities (SB 1350, 2016). In 2021, Arizona House Bill 2672 was passed to provide protections for LSE neighbors to help regulate misuse of these properties (HB 2672, 2019). Gurran et al. (2018) make the case using Coase’s theory saying that, “if property rights were able to be clearly defined, and able to be properly defended, individuals and even groups would be able to negotiate or bargain with each other to compensate those affected by a particular activity” (p. 404), which would limit the involvement and resource use by jurisdictions.

Arkansas Maumelle’s City Council Attorney Melissa Krebs noted the need to address noise complaints as well as special parties and stated, “We have seen on social media houses being rented out for parties where they are charging money for entry” (Simpson, 2021, p. 1). There was also a discussion of LSE properties being used for weddings. As a result, many municipalities have added regulations that prohibit parties, gatherings, and weddings because of noise and parking issues. An example is Las Vegas which states, “Other commercial events that are typically held at banquet facilities, such as weddings, parties, and receptions, are prohibited at short-term rentals” (Las Vegas: Rule, 2022, p. 1). It appears that the more experience a municipality has with LSE guests, the more rules and regulations it creates to protect itself and neighbors surrounding the LSE property.

Regulations and Terms

One issue facing hosts of LSE rentals is the lack of universal taxation methodologies or rules and regulations. This increases the complexity of managing several properties in different municipalities and underscores the importance of LSE hosts remaining aware of new rules and regulations to ensure compliance and in many municipalities, to avoid fines and penalties. In addition to new rules and regulations, there can also be specific terms used differently in different municipalities. One such example is the Santa Cruz County Planning Department (n.d.) in California, which defines the following three rental property types as follows, A Hosted Rental is a short-term rental (less than 30 days) of one or two bedrooms in a home, where the property owner will stay on site during the rental. A Hosted Rental is different from a Vacation Rental which is a short-term rental of an Entire House. A Hosted Rental is also different from a Bed and Breakfast which is a hosted short-term rental of three to five rooms (p. 1).

Another regulatory concept is an Accessory Dwelling Unit, which is what many refer to as a mother-in-law residence, which is a separate structure that is independent from the primary structure on the property. Certain states such as California have diverse and wildly different regulations based on jurisdiction, such as the town of La Mirada, California which does not allow any LSE rentals within its jurisdictional boundaries, whereas the city of Orange which is just a few miles away allows STRs with regulations that are different than many other jurisdictions in the state of California. Therefore, it behooves the LSE host to understand and comply with the regulations of their STR.

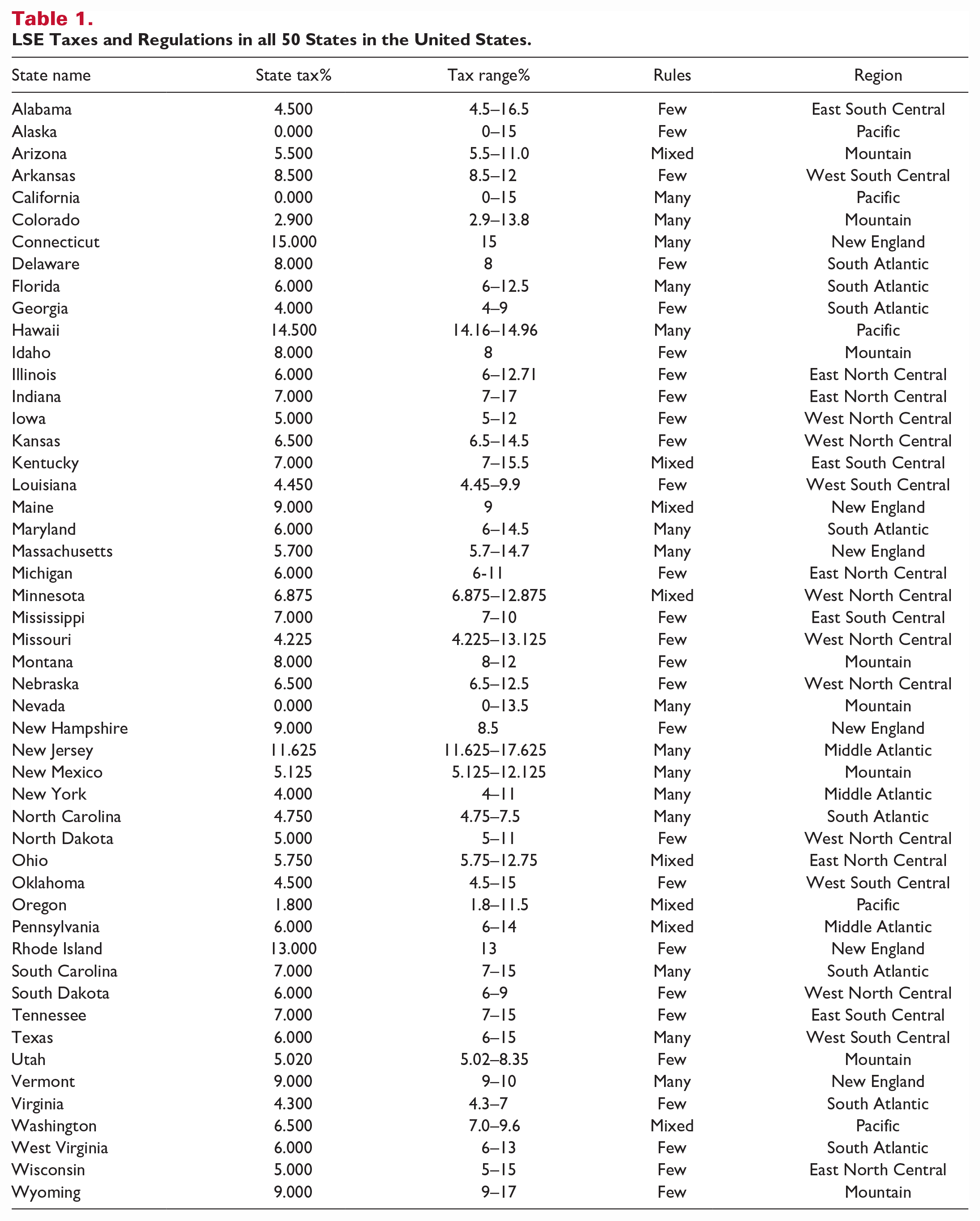

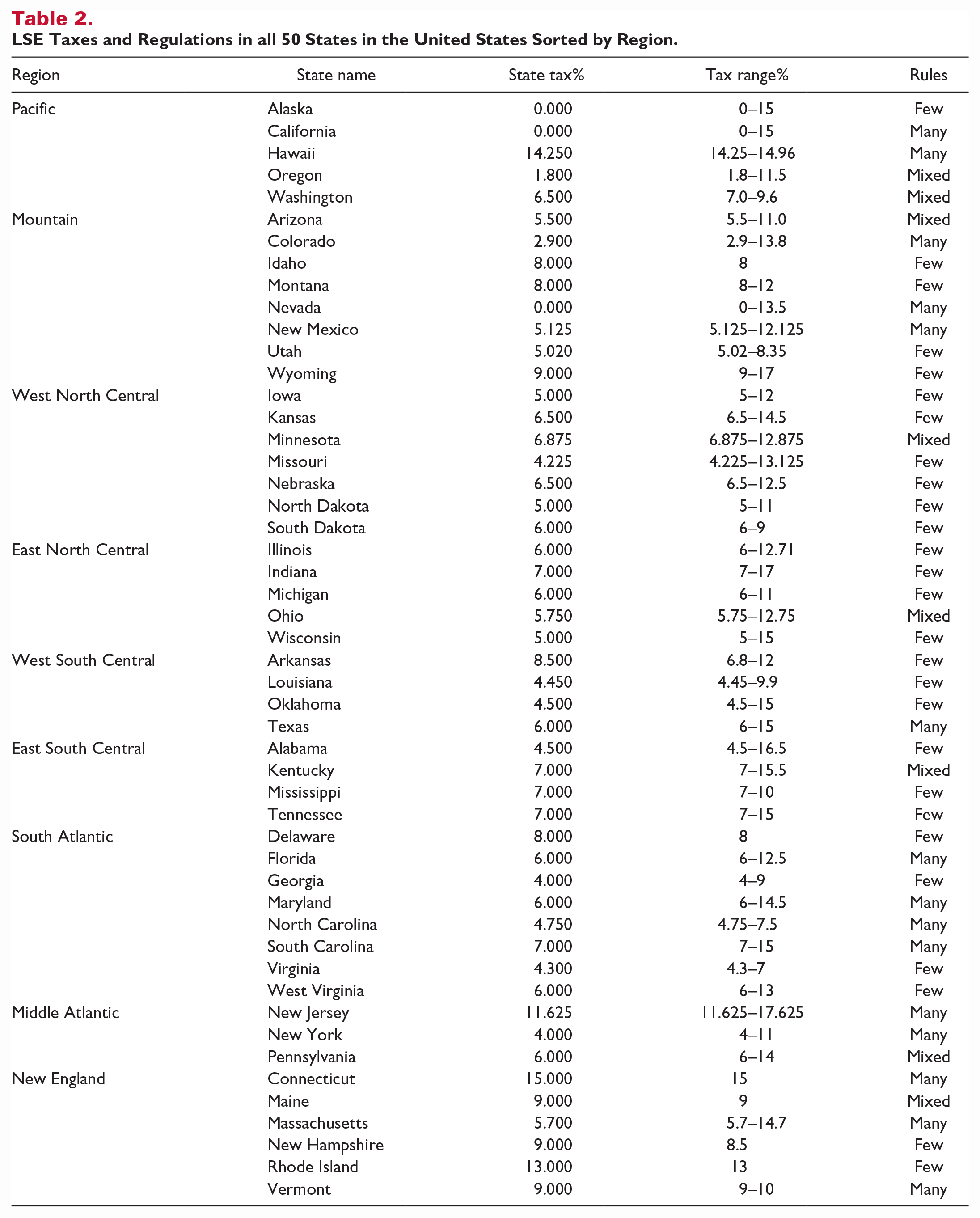

Table 1 contains attributes for each state in the union including: the name, state tax rate for LSE rentals, a range of tax rates available within the state, a level of regulations (Few, Mixed, or Many), and U.S. region. The sources for these data from both Table 1 and Table 2 were collected from diverse locations and websites including Airbnb (“What Regulations Apply to my City?” n.d.), Avalara taxes (“Industry Solutions: Short-Term Rental,” n.d.), the U.S. Census Bureau (2013), and World Population Review (2022) websites. Many of these attributes appear in the maps below.

LSE Taxes and Regulations in all 50 States in the United States.

LSE Taxes and Regulations in all 50 States in the United States Sorted by Region.

LSE Policies: Public Policy Perspective

As mentioned above, there are various goals of the different players involved with STRs and the parties who create the public policy for a given municipality or state include city, county, and state officials as well as state congressmen and senators. Their overarching goal is to ensure all residents’ rights are protected as well as to bring in taxing revenues and ensure tourism/bed taxes are paid fairly by all engaging in accommodation rentals. Sometimes, those who set public policy are at odds with each other such as legislation that seeks to prohibit all STRs from a given municipality such as is currently done in cities including La Mirada, CA and Irvine, CA (Rules: La Mirada, CA, 2022; “Short Term Rentals: Irvine,” n.d.).

Alternatively, there are efforts to forbid prohibiting STR activity in states including Arizona, Illinois, and Tennessee (Martineau, 2019; SB 1350, 2016; Zalewski, 2019) to ensure that municipalities within a given state do not have the power to prohibit STRs within their jurisdiction. However, even if these municipalities are prevented from prohibiting STRs, they still can pass legislation and regulations that protect neighbors of STR properties. There is an abundance of these types of regulations across the country that seeks to protect neighbors of STR hosts.

Another public policy focus is to prevent LSE rentals from escalating housing prices and rents to unaffordable levels through gentrification. According to Lee (2016), Los Angeles has avoided outright bans on STRs due to LSEOP companies such as Airbnb who have lobbied in L.A. Specifically, “Airbnb spent $100,000 in 2014 alone to lobby Los Angeles officials” (p. 252) to not ban their services. However, Lee (2016) credits part of the gentrification issues in Los Angeles to LSE rentals since it takes from the housing market units in which residents used to live and instead rents these units to guests. In addition, LSE rentals exacerbate a phenomenon called “hotelization,” which Lee defines as those units that can be rented for less than a hotel room but more than the “residential market or rent-controlled rent” price tag (p. 230). Referring to Los Angeles residents, Lee (2016) mentioned that “Even an outright ban on STRs would be better for low-income residents than the unregulated status quo. Airbnb must become a responsible partner and facilitate, not hinder, the goals of affordable housing advocates.” (p. 251). Gentrification is a serious concern that will continue to attract much attention in the STR community.

Challenges With the LSE Policies: Owners’ Perspective

LSE hosts want to have an uneventful stay and as a result make a reasonable profit from housing guests in their homes or rental properties. They do not want to encounter what one host found 10 days after the guests had left, which was his oven on the highest setting, the air conditioning unit turned on full blast with windows opened (Bad behavior! 2018). This guest behavior is not what most hosts experience, but it is always a possibility. Hosts rely on LSEOPs to vet guests to avoid damage to the host property. Essentially what hosts want is to make an honest profit and provide a good experience for their guests.

Owners (hosts) also want to obey the laws and not be fined or assessed for back taxes. One Airbnb owner stated, “I have this underlying fear . . . that I am breaking a law that I don’t really know about” (Martineau, 2019). As with most businesspersons, hosts merely want to make an honest profit and not find out later the LSEOP “broker” they were using was not doing business in the most ethical manner and now are required to decrease their profits to repair damage done by the LSEOP company. Furthermore, hosts want a governmental set of regulations that do not stifle their ability to rent their properties.

Challenges With the LSE Policies: Consumers’ Perspective

LSE guests want an honest deal from their STR stay. Many are looking for an inexpensive place to stay while others seek memorable experiences but regardless, all guests seek a stay free from harm of all kinds. Guests expect physical safety as well as for their full selves, including not having images or video capture them while occupying the unit, as a couple encountered in Longboat Key, Florida. The guests noticed a camera in their room and contacted the police, who confiscated the equipment and charged the host with “video voyeurism.” Airbnb has zero tolerance for hosts spying on their guests and will terminate their STR contract with the host and report them to the police (Brown, 2017). These types of negative experiences can spoil the LSE experience for guests.

U.S. Regions

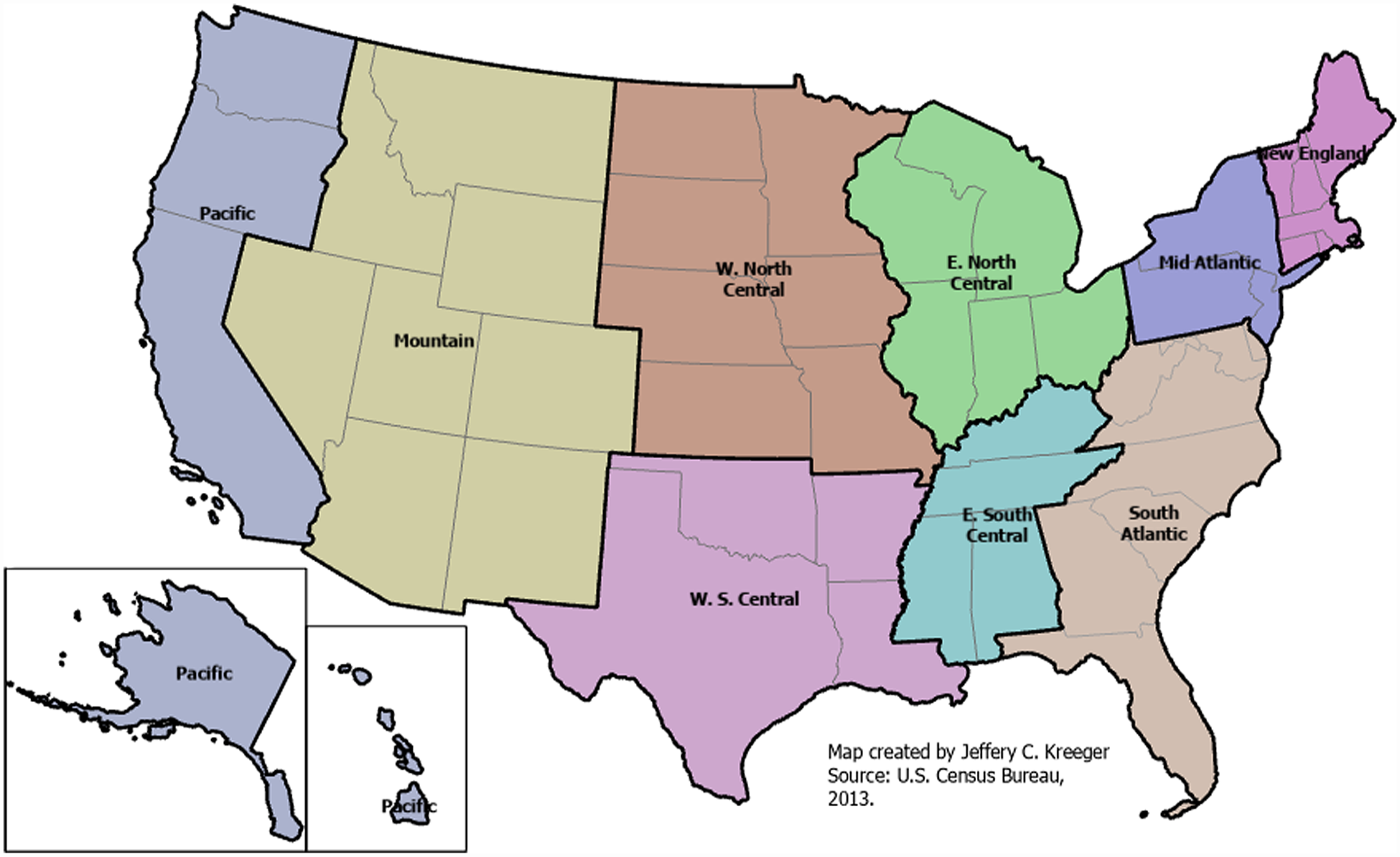

Figure 1 illustrates the nine U.S. regions. These divisions were established by the Census Bureau and include the following (from west to east): Pacific, Mountain, West North Central, East North Central, West South Central, East South Central, South Atlantic, Mid Atlantic, and New England (U.S. Census Bureau, 2013). These nine regions were introduced in the decennial census in 1910 except for Alaska and Hawaii (“Regions and Divisions,” 2021).

U.S. Regions—(U.S. Census Bureau, 2013).

Pacific Region

The Pacific U.S. Region incorporates the three west coast states of California, Oregon, Washington as well as Alaska, and Hawaii. These five states have STR taxes that range from 0% in Alaska to 15% within a city in California. The number of unique rules and taxing areas in each state is high in California and Hawaii. They are moderate in Oregon and Washington, and there are only a few within Alaska. California and Hawaii both enjoy a substantial amount of tourism visitation with Alaska and Washington bringing in a fair number of tourists as well. Airbnb was formed in this region in San Francisco and since then, the state of California has developed more than 43 municipal taxation and regulation regions within the large state, making it the state within the United States with the largest number of different municipality regulations for running an LSE rental: Florida comes in second with 12 unique municipality regulations.

The sheer size of California, which is over 10% larger in landmass than the country of Japan (Mapfight Website, n.d.), contributes to the vast number of different municipality regulations. While California’s landmass is only 5% (1/20th) the size of the total contiguous U.S. landmass (Mapfight Website, n.d.), nonetheless it encompasses a substantial percentage of the unique regulation entities in the U.S. rules and regulations can also restrict STR operations. California has created more rules and regulations and various taxing rates for LSE rentals throughout its state than any other. California’s state Senate Bill 1049 imposes penalties for noise violations to control noise within neighborhoods with LSE renters. These penalties can be assessed for up to US$1,500 for the first offense up to US$5,000 for third and other offenses within a calendar year.

Mountain Region

The Mountain Region incorporates Arizona, Colorado, Idaho, Montana, Nevada, New Mexico, Utah, and Wyoming. These eight states have STR taxes that range from 0% in Nevada to 17% within a city in Wyoming. The number of unique rules and taxing areas in each state is high in Colorado, Nevada, and New Mexico. They are moderate in Arizona, and there are only a few within Idaho, Montana, Utah, and Wyoming. The state of Arizona has experienced diverse bills from the senate and house which address both sides of STR regulation issues—those in favor of prohibiting the banning of STRs and those which protect neighbors from rental guest abuses. Senate Bill 1350 was passed to encourage short-term lodging rentals and prohibit bans against STRs, whereas HB 2672 (2019) was passed to establish regulations against misuse from rentals including the following: Limiting or prohibiting the use of a vacation rental or STR for the purposes of housing sex offenders; operating or maintaining a sober living home; selling illegal drugs, liquor control or pornography, obscenity, nude or topless dancing and other adult-oriented businesses. (p. 1). To reduce parties in rentals, HB 2672 (2019) limits the number of people who can be in residence to “not more than two adults per sleeping room plus two adults” (p. 1). Additional bill sections detail how devices need to be added to monitor noise on the premises along with a three-strike policy on noise violations.

The state of Colorado currently has eight jurisdictions with diverse, specific regulations. Notably, VRBO had its genesis in 1995 in the Denver metropolitan city of Aurora, where its founder created VRBO to rent his Breckenridge ski resort condominium. However, the simplicity of VRBO’s beginnings has developed into a complex set of regulations that vary from state to state and from municipality to municipality. For example, as mentioned above, a Denver couple was charged with running an illegal STR scheme because they did not reside at the residence they rented out (McCann, 2019), because the “Denver Municipal Code requires the owner or lessor of a STR to live at the location being rented as their primary residence” (p. 30). In addition, some Colorado “cities (e.g., Vail and Steamboat Springs) have an additional marketing district tax” (State Lodging Tax Center, n.d., p. 1.), which can vary from 1.4% to 4.0% and hotel taxes are assessed up to 10.75% in the city and county of Denver, with the city of Wheatridge coming in as the second highest Colorado percentage at 10.0% (“Occupancy Tax Collection and Remittance by Airbnb in Colorado,” n.d.).

The state of Nevada is a mixed bag of tax rates that range from 0% to 13.5% but the Silver State also has some municipalities that are very restrictive including Henderson, which seeks to protect neighborhood interests by providing a 28-page ordinance (Ordinance no. 3736, 2020) which requires hosts to install and operate a porch camera to capture activity on the host’s property as well as the requirement to constantly monitor noise levels on and around the property—from LSE guests (noise monitoring also required for North Las Vegas). Other different regulations in Nevada include distances from other structures/neighbors. Alternatively, there are no specific regulations for LSE innkeepers in the state of Wyoming although the state relies heavily on existing regulations written for traditional bed and breakfasts. In 2021, the city of Cheyenne identified about 260 STRs (Austin, 2021) and anticipated more during Cheyenne Frontier Days at the end of July – it is the largest rodeo in the United States. Wyoming’s strategy is to focus future regulations on limiting guest sizes (to eliminate parties) using the definition of a family unit as a limiting factor.

West North Central Region

The West North Central Region incorporates the states of Iowa, Kansas, Minnesota, Missouri, Nebraska, North Dakota, and South Dakota. These seven states have STR taxes that range from 5% in Iowa and North Dakota to 14.5% within a city in Kansas. The number of unique rules and taxing areas in each state is few except for Minnesota, which is moderate. Other than Minnesota; all states in this region have few regulations below the state level indicating that STR regulations have not yet been specified at lower geographic levels. Prior to the Super Bowl in 2018, Minneapolis’ (the “big game’s” host city) City Council approved two ordinances for STRs regarding host licensing with the city of Minneapolis. Essentially, if a host lives at the property and rents out a room while the host is also on site, the license fee is free; however, if the host lives at the property but leaves the premises during a guest’s stay, the host needs a US$46 license fee. If the host does not live at the property, their license fee can range from US$70 to US$350 (“Minneapolis Approves Two Airbnb Regulation Ordinances,” 2017). Furthermore, Kansas City recently established regulations for STR hosts and guests including application and license fee as well as a requirement to announce and get permission from adjacent neighbors (New Airbnb Regulations, 2018).

East North Central Region

The East North Central Region incorporates the states of Illinois, Indiana, Michigan, Ohio, and Wisconsin. These five states have STR taxes that range from 5% in Wisconsin to 17% within a city in Indiana. The number of unique rules and taxing areas in each state is few except for Ohio, which is moderate. The states in this region have STR taxes that range from 5% in Wisconsin to 17% in Indiana with a County Innkeeper’s Tax, which in itself can be as high as 10%. The number and complexity of regulations vary greatly within this region from Chicago to more rural counties. Like Arizona’s legislation that prevented jurisdictions from prohibiting STRs, the state of Illinois created House Bill 2919 that prohibits outlawing STRs (Zalewski, 2019); however, this legislation does not prohibit the creation of complex regulations and rules for STRs. The largest city in this region is Chicago, Illinois, which regulates hosts based on a 44-page document that specifically address the defined four categories of STRs: Shared housing unit, bed and breakfast, vacation rental, or an actual hotel (Rules: Chicago, IL, 2022).

West South Central Region

The West South Central Region incorporates the states of Arkansas, Louisiana, Oklahoma, and Texas. These four states have STR taxes ranging from 4.45% in Louisiana to 15% within a city in either Oklahoma or Texas. The number of unique rules and taxing areas in each state is few except for Texas, which has many. Recently, the Fifth District Court struck down as unconstitutional that prohibited out-of-state hosts to rent STRs in the city of New Orleans. (McGill, 2022). This ruling indicates that where local authorities and homeowners attempted to restrict who can operate STRs, the courts sent a message that restrictions must meet certain criteria and not overreach. This court case along with a requirement that STR host obtain operator permits indicate that the residents of New Orleans view STRs as businesses that need greater regulations and restrictions.

Within Texas, the cities of Austin, Galveston, and San Antonio require business permits for STRs to operate. The city of Houston classifies STRs as lodging establishments and regulates them under the Hotel and Motel Ordinance. This appears to hold STRs to the same standard as hotels and motels of the city and is considered to be more restrictive than the other three municipalities that only require business permits.

Oklahoma City is the only municipality within the state of Oklahoma that provides any regulation regarding STRs and has a unique “Home Sharing License” that requires a special exception if the rental is not the host’s primary residence. Another unique aspect of this restriction is that if the guest stays more than 30 days, the Home Sharing License is no longer needed, which in effect, redefines STRs as 30 days or less.

East South Central Region

The East South Central Region incorporates the states of Alabama, Kentucky, Mississippi, and Tennessee. These eight states have STR taxes that range from 4.5% to 16.5%, both of which are within the state of Alabama. There are few unique rules and taxing areas in each state except for Kentucky, which is moderate. Alabama and Mississippi appear to have no state or municipal laws or ordinances currently regulating STRs within their states. Nashville is currently the only municipality within the state of Tennessee that regulates STRs and requires the host to obtain a permit to operate. Zoning regulations within Nashville’s Metropolitan Code also restrict where an STR can operate according to which special district they occupy.

Within the state of Kentucky, Louisville requires both registrations as an STR and is restricted through standards set by the Louisville Metro Board of Zoning Adjustment. Lexington has similar measures to Louisville but takes the extra step of requiring all STRs to obtain a Certificate of Occupancy issued through the Division of Planning and Zoning. Tennessee’s General Assembly passed the Short-Term Rental Unit Act in 2018 which among other things, prohibits cities from banning STRs (Martineau, 2019).

South Atlantic Region

The South Atlantic Region incorporates the states of Delaware, Florida, Georgia, Maryland, North Carolina, South Carolina, Virginia, and West Virginia. These eight states have STR taxes that range from 4% in Georgia to 15% within a city in South Carolina. The number of unique rules and taxing areas in each state is either many (Florida, Maryland, North and South Carolina) or few (Delaware, Georgia, Virginia, and West Virginia). Both North and South Carolina present interesting examples of states where specific municipalities appear to be heavily regulated and taxed (e.g., Asheville NC, Wilmington NC, and Charleston, SC) while other parts of the states have no regulations on the books or procedures in place to enforce/collect accommodation taxes. It is apparent that municipalities that are seen as high-traffic tourism destinations are the ones that focus on both regulation and local accommodation taxation efforts, whereas cities that see little to no tourism activity do not place much emphasis on these efforts. Maryland also falls into this same category with their concentrated effort being within the counties near Baltimore and Washington D.C.

With more tourism destinations throughout the state than most, Florida appears to be the leader in this area of a greater statewide effort to control and tax LSE operations. The state of Florida requires that all vacation rentals within the state be licensed through the Department of Business and Professional Regulation. In addition, the state of Florida requires LSEOPs to collect and pay both state and local taxes in the booking process bypassing the host which appears to be far more effective and efficient. This statewide strategy to collect all applicable taxes while leaving much of the specific regulations up to the local municipalities appears to work well and should be considered a “best practices” example for other states to follow.

Currently, the state of Delaware does not have legislation that taxes LSE bookings. Other than those regulations, there has been little additional legislation specifically targeting the LSE. One exception is a case in Sussex County in Delaware, where MacArthur (2017) writes about how an Airbnb host was denied permission to lease out her property as a STR. Hosts are ultimately responsible for remitting a lodging tax, but these taxes apply only to guests who stay less than 5 consecutive months. Virginia, West Virginia, and Georgia are similar to Delaware with only Arlington County, VA and Atlanta, GA having any regulations regarding STRs.

Middle Atlantic Region

The Middle Atlantic Region incorporates the states of New Jersey, New York, and Pennsylvania. These three states have STR taxes that range from 4% in some New York State locations to 14.625% in New Jersey’s Bergen and Hudson Counties. The number of unique rules and taxing areas is high in New Jersey and New York and moderate in Pennsylvania. The largest city in this region is New York City (NYC) with a population of more than eight million. NYC was one of the first cities from which Airbnb offered rentals, but there have also been several battles through the years in this huge, metropolitan city. NYC Mayor Bill de Blasio sought out illegal STR hosts and was successful in gaining six figure awards from Airbnb hosts who rented out a whole home for less than 30 days, which is illegal in NYC (White, 2021). Furthermore, NYC recently created a law that requires STR companies to share hosts’ personal information with the city (Blecharczyk, 2020). The state of New York is a good example of a state with a diverse population. Although NYC makes up most of the state, there are other parts of the state where regulation applies and perhaps more interestingly, different regulations than might be necessary outside of NYC. In fact, additional County Hotel Room Occupancy Taxes can be assessed and range from 2% (Delaware County) to 7% (Onondaga County) depending upon in which county the host property rests. Perhaps, this difference is illustrated through a comparison of rules needed within NYC and those for tourists visiting Niagara Falls near Buffalo, New York’s second largest city—NYC has far more regulations than Buffalo.

Philadelphia is the second largest city in the region, with a population more than 1-1/2 million. Like many other cities, the city of brotherly love updated its rules and regulations to be more responsive to the unique challenges offered by STRs (Rules: Philadelphia, PA, 2022). Although most of the state of New Jersey welcomes STR business, the township of East Hanover, New Jersey passed an ordinance making it illegal to offer STRs for any time period shorter than a 176-night stay (Rules: East Hanover, NJ, 2022).

New England Region

The New England Region incorporates the states of Connecticut, Maine, Massachusetts, New Hampshire, Rhode Island, and Vermont. New England represents a mixed bag of regulatory municipalities and has state tax rates from 5.7% in Massachusetts to 15% in Connecticut. What is interesting about Massachusetts is that within the state they have a large range of tax rates within the state ranging from 5.7% to 10.7% (“What Regulations Apply to my City?” n.d.). The number of rules assessed in each state also varies from a few (New Hampshire and Rhode Island) to many (Connecticut, Massachusetts, and Vermont) and Maine, which has a moderate number of cities with different rules and regulations. Like other states, Connecticut did not have special regulations that pertained to the LSE until legislators created a special notice in 2019 to include LSE properties in the 15% Room Occupancy Tax, which has historically been assessed on hotels, motels, and bed and breakfast properties (Pinho, 2016; State of Connecticut—Department of Revenue Services, 2019). Furthermore, this same change in regulations appears to be aimed at the LSEOP companies since it includes a criterion of retail sales greater than US$250,000.

Summary of Major STR Lawsuits

There have been numerous lawsuits related to STRs, but one of the most pivotal decisions was made by the U.S. Supreme Court in South Dakota v. Wayfair, which set up the framework for retailers to make online intermediaries (like LSEOPs) be responsible for paying taxes for retailers (Bologna, 2020). This landmark case provided the momentum for other states to follow and institute similar requirements for LSEOPs to collect and pay taxes for STR hosts. Other states continued the momentum of requiring LSEOP companies to collect and remit taxes. These states include California’s SB 1072, Georgia’s HB 448, Illinois’ SB 3386, West Virginia’s SB 163, and Wisconsin’s AB 683 (Bologna, 2020). These states’ efforts created a tsunami that LSEOPs have had to accept and take over those collection and remittal responsibilities. These cases established LSEOPs as the official collectors of taxes for hosts except where otherwise mentioned by state regulations.

Government agencies appreciate the shift of collecting taxes from individual hosts to the few LSEOPs because in theory, it makes collections and audits easier; however, many government officials, including Wisconsin Rep. Joel Kitchens (R), are skeptical. He states, “I don’t believe those platforms are actually collecting [taxes]. They claim they will get it to us, but I’m very skeptical” (Bologna, 2020, p. 1). Bologna (2020) further reports that Ulrik Binzer, CEO of Host Compliance LLC, stated: The STR industry is a large business worth more than US$30 billion a year. The average lodging tax rate is in the 8% range across the country. So there should be total collections in the billions of dollars, but I don’t think that’s actually happening (p. 1). To illustrate his point, Ulrik Binzer mentions how Tennessee was receiving about US$1 million in collections, but after Binzer implemented “a series of short-term rental compliance and enforcement strategies” (p. 1.), the state began collecting US$9 million. These suspicions have led to audits and lawsuits by government agencies against the LSEOP companies.

State and local governments have sued LSEOPs they suspected of not collecting and/or remitting taxes; however, even before going after LSEOP companies, NYC’s de Blasio administration sued two NYC landlords in 2017 to 2018 who rented some portion of their leases as STRs. In these two unprecedented lawsuits, NYC and the landlords settled for a total of US$1.2 million. This was perhaps a wakeup call for LSEOP companies and received the attention of other government agencies, who also began to sue more feverishly for taxes not paid (White, 2021).

Further lawsuits have been waged against out-of-state investors in an attempt by lawmakers to decrease neighborhood gentrification. While officials in New Orleans were trying to prevent further rising housing costs due to out-of-town investors, the Fifth District Court struck down as unconstitutional that prohibited out-of-state hosts to rent STRs in the city of New Orleans. (McGill, 2022). The judge who struck down the New Orleans law “noted a California decision upholding the city of Santa Monica’s requirement that someone lives at a short-term rental full time, ‘but that person did not need to be the owner of the property,’ so out-of-state owners weren’t excluded” (McGill, 2022, p. 1). This reference was to Santa Monica, California where they passed a bill that there had to be someone at the home of a rental, but the person did not need to be the owner. It could instead be a hired employee which prevented the law from prohibiting out-of-town hosts.

The results of this patchwork of various regulations from state to state or varied regulations within the municipalities within a state lead to an unnecessary burden for all stakeholders involved in the LSE. This leads to an environment where operators unknowingly are in violation of regulations. This could also cause confusion among the regulatory authorities allowing dishonest operators to take advantage of selective enforcement of both regulatory and taxation efforts. The results of these conditions could cause harm to the traveling public who choose to engage in commerce with the LSE and might not enjoy the same level of protection that are present when booking a hotel for overnight stays. This lack of consistent regulations throughout the United States presents a threat to public safety and creates an environment of uncertainty as to what policies should be in place to present this. In addition, weak efforts to enforce the proper taxation of LSEs create an unfair disadvantage for the hotel industry where taxation efforts are consistently enforced throughout the United States and create an unfair playing field.

Methodology

This study utilized content analysis design to provide a comparative summary of LSE regulations for each state to facilitate comparisons among states to determine highly regulated environments versus laissez-faire destinations. Content analysis is a valid qualitative methodology within the field of hospitality and tourism management research and has seen an increase in usage to determine the existence of concepts or themes within a collected body of literature (Kim & So, 2022; Mody et al., 2021). Attributes about each state were collected from various sources to capture tax impacts and regulatory impacts on each state in the union and are presented in Table 1. Snyder (2019) synthesized practical guidelines from various studies on the subject to stress the importance of a comprehensive and rigorous review that considers diverse viewpoints. While this study is not a literature review, per se, the authors have considered not only the pro-LSE perspective, but also the regulators’ perspectives. What is not included in this article is a very large spreadsheet that is an expansion of Table 1 and includes rows of data for each county, city, town, or other municipal jurisdiction that has a vested interest in protecting residents and tax revenues. This expanded table was created using a similarly rigorous approach as mentioned by Snyder (2019) in her article. This expanded table can be obtained from the authors upon request, as its size is beyond the scope of the current article guidelines.

The sources for these data were collected from diverse locations and websites including Airbnb (“What Regulations Apply to my City?” n.d.), Avalara taxes (“Industry Solutions: Short-Term Rental,” n.d.), the U.S. Census Bureau (2013), and World Population Review (2022) websites. Although many of the categorizations for the states were not delineated precisely, Table 1 shows each of the 50 states with assessed state-level taxes (“Industry Solutions: Short-Term Rental,” n.d.) on LSE rentals as well as the range of taxes within each state including local taxes (“What Regulations Apply to my City?” n.d.). While care was taken to accurately calculate and portray these ranges, there was a potential for error in calculating tax ranges for any given state.

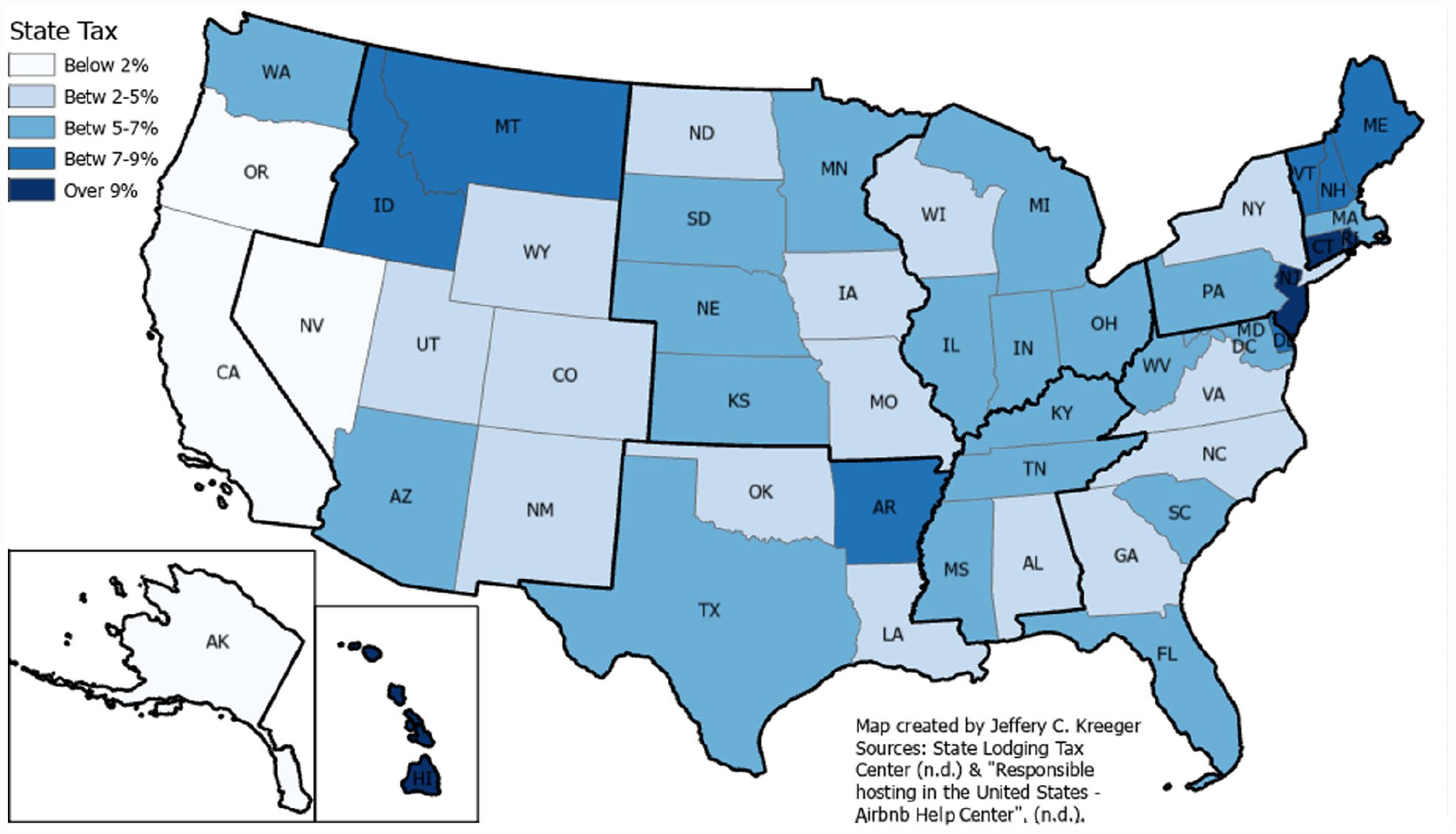

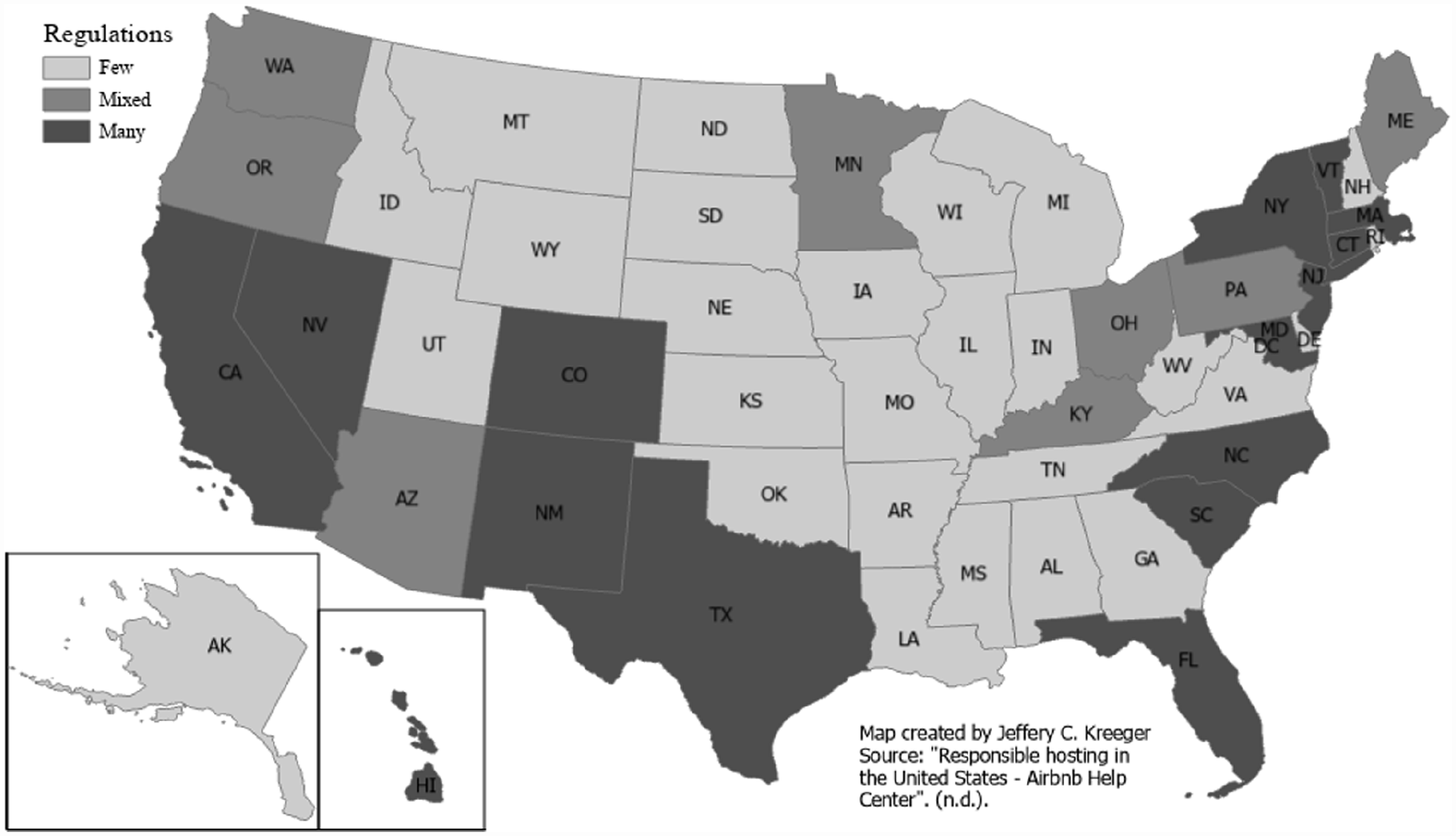

Figure 2 shows only state taxes assigned to STRs by state within each regional boundary. These taxes were compiled using the Airbnb website and the Avalara state taxing page (“Occupancy Tax Collection and Remittance by Airbnb in Colorado,” n.d.; State Lodging Tax Center, n.d.). Figure 3 illustrates a qualitative assessment of the rules and regulations required by each state. This attribute field called “Rules” was populated by two data analysts who separately and independently assigned one of three labels (Few, Mixed, or Many) to each state using the following altered criteria (see below) to determine which label to assign. These two sets of results from the data analysts were then compared with each other and discussed using the original set of rules. There were 13 states with discrepancies: Illinois, Kentucky, Louisiana, Minnesota, Missouri, Nebraska, New York, Ohio, Oklahoma, Oregon, Tennessee, Washington, and Wisconsin. After some discussion about these states, a criterion was deleted from the list of criteria which addressed tax rate ranges. Because this attribute of “rules” was meant to deal with rules and regulations, the taxation criterion was removed, thereby making the creation of this category more objective—and removing all discrepancies between the two data analysts.

State Taxes for Short-Term Rentals.

State Level of Regulations for Short-Term Rental.

This three-level categorization was determined as follows. One label was used to assess the STR regulatory environment in each state, which is less than ideal to represent a whole state’s environment. Three categories were created to represent a state’s overall regulatory environment toward LSE rentals: Few, Mixed, and Many. A challenge was assessing a generalization for a whole state that portrays the regulatory environment for each state. This “Rules” category attempted to do that. States in Airbnb’s website (“What Regulations Apply to my City?” n.d.) were analyzed based on the following methodology. A state with a “Few” category label had either zero cities or counties within the list of rules and URLs, which indicates there are limited rules and regulations below the state level. States with the “Mixed” categorization include a state with two or three cities or counties where there are separate and distinct taxes and rules and regulations among the municipalities. The “Many” category indicates there are specific tax rates and/or rules pertaining to four or more cities and/or counties.

Discussion

This study found vast differences among states’ regulations for short-term lodging rentals, which underscores the need for hosts to fully understand the regulations for their properties to avoid penalties and fines. In short, there appear to be no consistent regulations among states or even by the municipalities among those states. It was observed that states which had a wider variety of regulations among the municipalities tended to be larger states with several large population centers (e.g., California, Texas, and Florida). The highly regulated states that did not fall into this category tended to be states that have multiple popular vacation destinations (e.g., North Carolina, South Carolina, and Vermont).

Because municipalities do not have the resources to adequately police LSE rental activities, perhaps a better model is for municipalities to work closely with the STR companies to ensure regulations are being properly followed (Leshinsky & Schatz, 2018).

A further result of this lack of guidance through proper regulation is the confusion over when and how STR operators should be paying accommodation taxes. In some municipalities, the service provider (e.g., Airbnb and VRBO) will collect said accommodation taxes from the guest and pay them accordingly. Where the service provider does not collect accommodation taxes, the host is responsible for tracking, collecting, and paying these taxes. In a statement on Airbnb’s website, the service provider states: We automatically collect and pay occupancy taxes on behalf of hosts whenever a guest pays for a booking in specific jurisdictions. Hosts may need to manually collect occupancy taxes in other jurisdictions and in certain listed jurisdictions where Airbnb does not collect all applicable occupancy taxes. (“What Regulations Apply to my City?” n.d.).

These inconsistent accommodation tax collection policies lead to the question of whether hosts of STRs that are not assisted by accommodation service providers are collecting and paying their appropriate taxes. As many of these operators are amateur innkeepers who lack the proper training, it is likely that when not monitored and left to their own initiative, accommodation taxes are not being properly being paid. Where accommodation taxes are not being collected from LSE STRs, hotel operators assert that this is not a level playing field as they try to compete for the same guest. These hotel operators argue that guest will take the total cost of accommodations into consideration when making their selection and that the added burden to collect accommodation taxes weighs against them in the “value equation.”

An additional consideration that traditional hotel operators claim works against them is that the business regulations and inspections they are subjected to protect guests from harm through unsafe or unhygienic practices. Most professional hoteliers invest heavily in their housekeeping and maintenance departments to satisfy these regulations and pass regular inspections. This results in a clean, healthy, and safe environment all of which benefit the traveler, which in turn promotes societal benefits like economic prosperity through safe travels. While some of these types of cleaning/health regulations appeared in a few municipalities, they were vastly missing from most STR regulations.

Conversely, the lack of regulations and inspections for amateur LSE innkeepers can create an atmosphere of unprofessional management with no incentives or punishments for failing to maintain proper cleaning or safety standards. Consequentially as many LSEs compete against traditional hotels with a lower price, fewer dollars are collected to be spent on housekeeping and maintenance upkeep. Without proper oversight, a case can be made that LSE STRs may at some point harm the travel industry as stories emerge about the problems guests and neighbors encounter with amateur innkeepers unprepared or unwilling to manage their operations in a professional and safe manner.

An even greater concern beyond the unprofessional management of STRs is the presence of bad actors within the LSE community. Several documented cases (Allen, 2022; Sheikh, 2022; Sperling, 2022) have surfaced where LSE hosts have placed hidden cameras within the accommodations and secretly taped guests in what they believed to be their private environment. Most of the LSEOPs such as Airbnb and VRBO have strict policies against secret camera filming violations, but these measures are punitive in nature whereas they deal with the problem after the host has been caught violating the policy as opposed to preventive measures. While these privacy violations appear to be extremely rare and it is believed that the vast majority of amateur innkeepers do not engage in this illegal behavior, such cases garner a tremendous amount of attention from the media as it tends to be sensational in nature and in turn gives the travel industry negative press which in turn could discourage travel. In contrast, professionally operated hotels by their nature have policies in place that are preventive in nature to protect a guest’s safety and privacy. Such measures include background checks, rigid key control standards, multiple daily inspections of guest rooms, and onsite loss prevention/security staff.

Conclusions

Implications

The implications of this study suggest that there is very little consistency in both the regulation and accommodation tax collection enforcement across the United States. This leads to confusion and disagreements among host, guest, and government regulatory/taxing authorities. With regard to the states and municipalities where no STR regulations exist, there is frustration and confusion over how, when, and where these businesses can operate. Observing the inconsistent or lack of regulations regarding STRs within the United States provides an environment of confusion and frustration for amateur innkeepers who wish to open and operate these accommodations. A lack of guidance through regulations also increases frustration among other interested parties such as potential guests and residents within the neighborhoods that house STRs.

Recent newspaper articles (Bell, 2022; Hamed, 2019) describe conflicts that arise between operators of STR accommodations and their neighbors. Where regulatory agencies do not provide rules, local homeowners associations look to fill in this gap with amendments to their neighborhood regulations which leads to disagreements and legal challenges (Ruch, 2022; Stetson, 2022). These recent conflicts indicate that the move to regulate STRs is driven primarily by residential neighborhood homeowner associations who are concerned with Not In My Backyard (NIMBY) quality of life concerns such as parking availability and disturbances and neighborhood peace issues. There seems to be a lack of legislation to be driven by consumer protection concerns or a lack of proper accommodation tax enforcement.

With lax or no oversight from government regulatory agencies regarding consumer protection, STR guests do not benefit from the same level of protection as guests who patronize hotels which are highly regulated. Several recent newspaper stories have documented incidents where STR guests have been scammed or placed in unsafe and unhygienic environments. Hotels, while not immune to these environmental concerns, are far more regulated through government inspections and quality control efforts through hotel companies. The authors assert that as more unethical or unsafe incidents continue to increase from a lack of consistent regulations for STR stays, state governments should consider focusing on instituting regulations that provide similar levels of protection that hotel guests enjoy. It is recommended that either new legislation efforts be guided by ‘best practices’ of existing effective regulations from around the country or that existing business regulations be expanded to include STR businesses.

Where accommodation taxes are not enforced or collected by STR properties, hoteliers believe that this is not a level playing field of competition when they compete for the same guests seeking accommodations. When taxes for STRs are not collected, compared with hotel accommodations which are mandatory, guests will take this total cost into consideration and often choose the less expensive option. This perceived inequity of taxation enforcement is further amplified when considering that many times these accommodation tax funds are used to promote the destination through convention and visitor bureau advertising campaigns. This free-rider effect (Lundtorp, 2003) produces an environment where STRs benefit from destination advertising and promotion without having to pay for it and where the local hotels are left with the task of collecting the correct taxes.

This disparity in the lack of accommodation tax collection between STRs and hotels should be immediately addressed in the spirit of fair competition in the free market. The vast majority of municipalities within the United States could benefit from a new source of revenue from STR collection efforts. It is also recommended that this additional tax revenue be used to fund inspections and similar oversights that exist within the hotel industry. As there has been a proven track record of having the online lodging service providers collect the accommodation taxes as part of the booking process, it is recommended that states and municipalities focus on this as a remedy to increase collections.

In conclusion, the explosion of online lodging service providers and the business they produce has been a boon to the U.S. economy in recent years. Online lodging has also satisfied the demand for travelers to experience a lodging product that differs from a traditional hotel stay. As with many business models that grow exponentially, there appears to be a lag in proper consumer protection regulations and a consistent method to fairly collect taxes and fees. It is believed that the growth in STR demand is going to continue and efforts to accurately regulate these businesses will properly protect the guests who place an inordinate amount of trust in the host. This effort to regulate this portion of the lodging industry also benefits the host as it provides guidance and legitimacy for their operation.

This study represents a call to action for both state and municipalities to begin efforts to coordinate the state and municipal laws for greater standardization and minimization of policy conflicts regarding LSEs. As previously mentioned, the regulation and taxation public policy regarding the hotel industry have been successful throughout the United States and could serve as a model that could be extended to LSEs.

In addition, associations such as the National Association of Counties and the National League of Cities in the United States aim to guide public policy for the common good. Although there has been some effort by these organizations to provide guidance through opinion articles (Binzer, n.d.), a greater effort should be made through active participation in conferences and advisement committees that could create standard public policy verbiage regarding LSEs.

An additional step in helping to pass consistent and meaningful regulations would be for LSE operators to be cooperative partners in the process. The authors recommend a stronger partnership between national, state, and local governmental regulatory agencies and LSE operator associations. This could be accomplished by approaching associations representing LSE operators such as Association of Lodging Professionals (ALP) and requesting to negotiate and contribute input in crafting meaningful regulations that benefit both consumers and operators.

Limitations

This study has involved gaining and interpreting data from many governmental and other sources and, therefore, is subject to misinterpretations and errors; however, any inaccuracies are unintentional. Also, this article should not be relied upon for offering a STR personally; instead, a lawyer should be consulted for specific details and legal advice. While both authors are PhDs, they are not lawyers. The authors randomly sampled several of the stricter jurisdictions on LSE websites and found properties offered that apparently do not comply with the respective regulations. This is an area for future research. Another area for further research includes a more rigorous analysis of the correlation between rules and regulations mandated by municipalities and their political bent. Even though seven out of nine regions appeared to have a strong, positive relationship between the level of regulations and political majority in each state, these relationships are based on aggregated state data and could perhaps be more applicable at a city or local level. Another limitation is that this study is a comparative analysis from a regional and state perspective and sought to give a broad-brush narrative regarding LSE issues; however, there is a plethora of information about the conflicting pursuits of goals among hosts, LSEOPs, and governmental entities at a more localized level such as city, town, or municipality. There are many diverse interests below the state-level awaiting exploration.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, or publication of this article.