Abstract

This research note aims to prompt a debate over the asset-light strategy that hotels are increasingly implementing nowadays. First, it evaluates the impact of an asset-light model on hotel firms’ returns, return volatility, and the Sharpe ratio, based on annual data from 1970 to 2018 of 65 U.S. public hotel firms. Evidence shows that going asset-light has no significant impact on companies’ returns, return volatility, and performance. Second, the study offers possible explanations behind such results and raises questions for future research.

Introduction

There is no doubt that the asset-light strategy traded its tactical attributes for a one-size-fits-all model (Blal & Bianchi, 2019; Low et al., 2015). The split between real estate and management is said to enable hotel companies to lighten their balance sheets (“The Global HOTEL Report 2018,” 2018) while mitigating companies’ operating and real estate risk (Page, 2007), expand market share (Brookes & Roper, 2012), and increase the firms’ value (Sohn et al., 2013). However, research on this subject remains incomplete (Li & Singal, 2019; Low et al., 2015), which could drive hospitality firms to choose unsuited business and ownership models, resulting in potential business downfalls. The extant literature tends to focus on the short-term financial benefits of disposing of real estate risk (Kim et al., 2019; Page, 2007; Sohn et al., 2013, 2014) and has largely ignored more strategic dimensions. This leads to the unexplored conclusion that financial and strategic objectives are substitutes, although it is recognized that strategic considerations should be preferred over short-term financial gains for companies to sustain their competitive advantage (Cooremans, 2011). In fact, apart from three studies (Blal & Bianchi, 2019; Li & Singal, 2019; Low et al., 2015), to the best of the authors’ knowledge, current literature investigates the asset-light strategy’s performance in the hotel industry either from a financial or from a strategic angle. While financial literature mostly recognizes the asset-light model as a global solution for hospitality players (“Investing in Hotel Stocks: The Benefits of Asset Backing,” 2019; Kim et al., 2019; Page, 2007; Sohn et al., 2013, 2014), most strategic papers emphasize the necessity to adapt the model considering each individual situation (Hotel Management International, 2018; Li & Singal, 2019; Perryman & Combs, 2012). This research note aims to fit this gap by, first, exploring the impact of going asset-light on hotel performances and, second, by triggering the discussion about such results. We found that asset-light strategy has no impact on hotel firms’ returns, return volatility, and the Sharpe ratio. We argue that these results might be explained by the complexity of the principal–agent constructs behind the asset-light choice and that can outweigh the advantages of going asset-light.

Data and Methodology

To explore our research question, we use longitudinal data analysis, combining cross sections and time series that have been performed on GRETL. 1 This method enabled us to evaluate asset-light strategy performance between 1970 and 2018 2 on public U.S. hotel firms. This data analysis method enhances the accuracy of econometric estimates as it involves more degrees of freedom than time-series or cross-sectional data and reduces collinearity between explanatory variables while controlling for unmeasurable and unobservable variables (e.g., cultural factors, corporate culture, and business practices; Hsiao, 2006). The panel data are unbalanced, accounting thus for companies entering the database, exiting the database, or merging. When data of a company are not available for a given year, the observation is treated as a missing value and discarded.

We retrieve data from 65 eligible firms from Thomson Reuters DataStream through sector filters “Travel & Leisure” and subsector filters “Hotels & Motels.” We retrieved the following dependent variables:

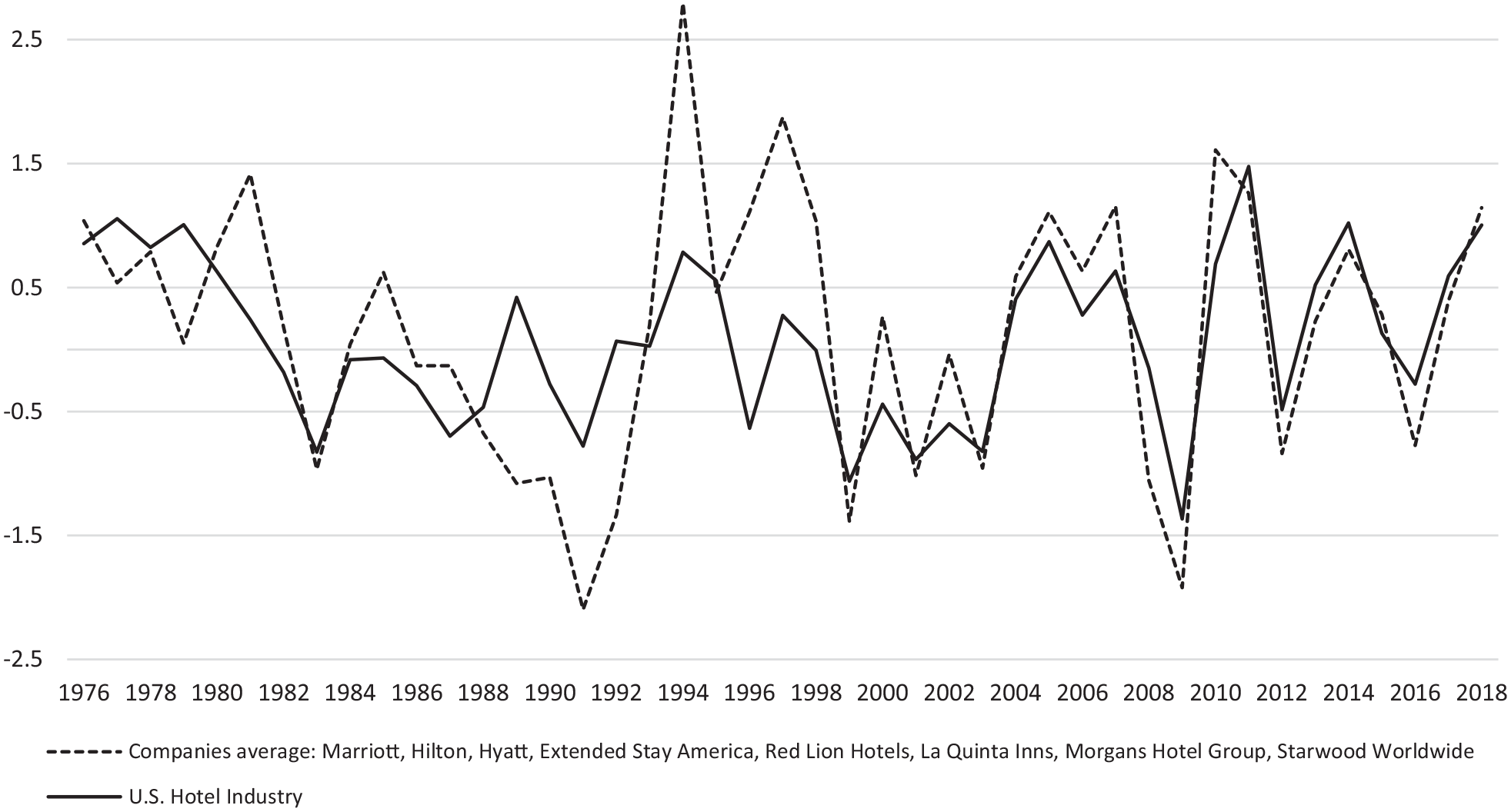

Hotel Firms’ Average Sharpe Ratio Versus U.S. Hotel Industry Average (1976–2018).

We test the impact of implementing an asset-light strategy on U.S. hotel companies’ returns, return volatility, and Sharpe ratio running the following multilinear ordinary least squares (OLS) regression:

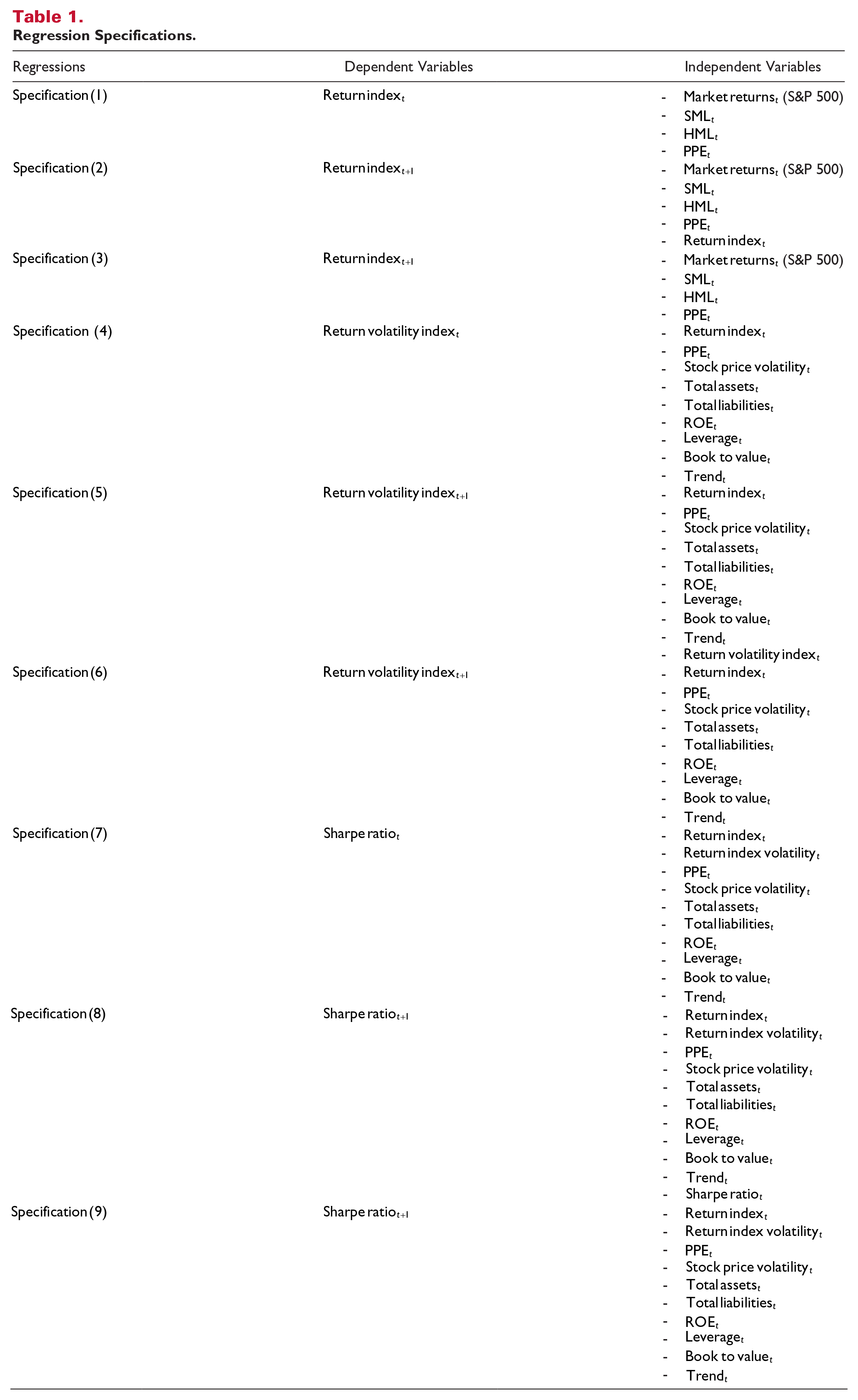

Table 1 summarizes the different specifications adopted to test the impact of asset-light strategy on returns, volatility, and the Sharpe ratio.

Regression Specifications.

The S&P 500 is a proxy for the MKT factor. The return volatility is computed as a dynamic volatility based on the change in annual returns from one year to the next. The Sharpe ratio

The authors decided whether to use a random or fixed effect based on the Hausman test results.

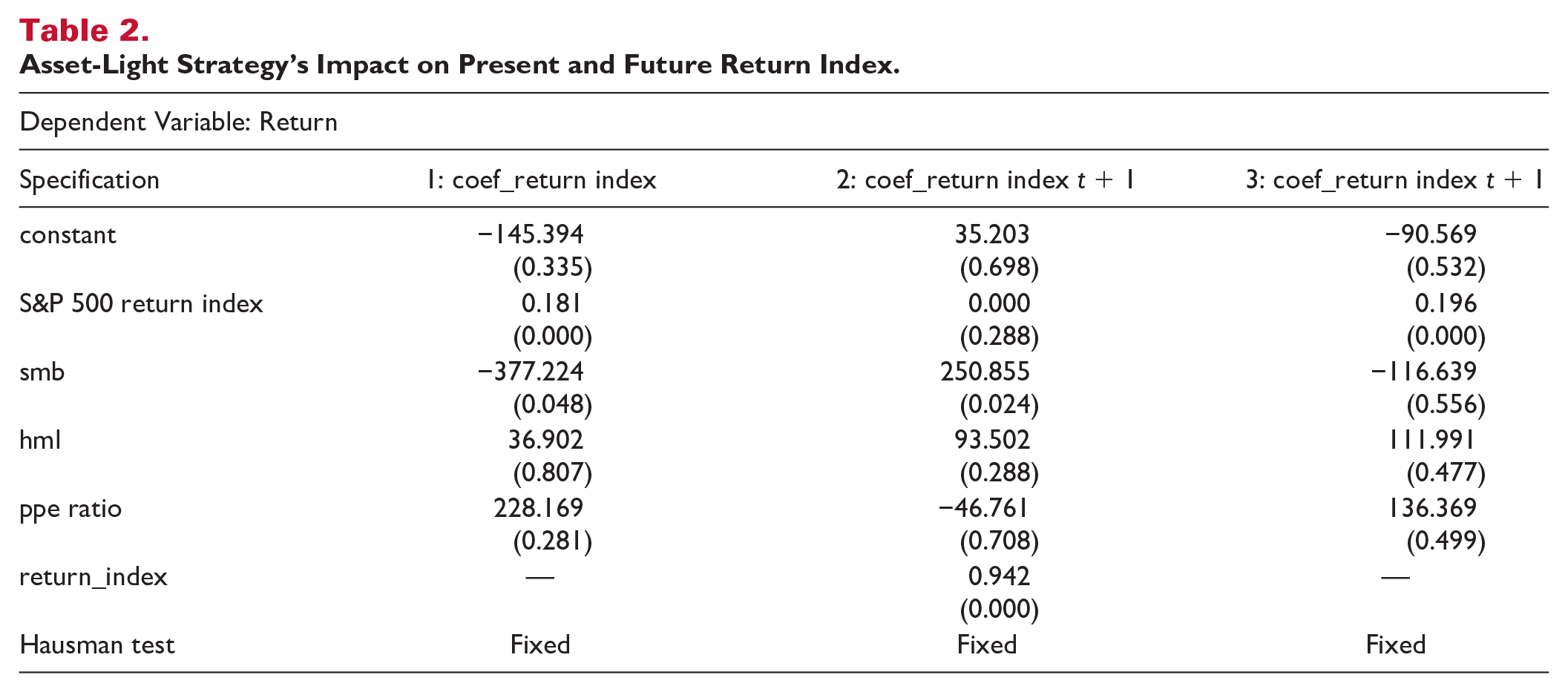

Table 2 depicts the asset-light strategy’s impact on present and future returns. Using a fixed model effect, it appears that the asset-light strategy has no significant impact on present returns. Interestingly, for the S&P 500 return index, the value is lower than 1, which implies that, in terms of the Capital Asset Pricing Model (CAPM) model, the U.S. hospitality market from 1970 to 2018 was exposed to lower risk than the market (β < 1).

Asset-Light Strategy’s Impact on Present and Future Return Index.

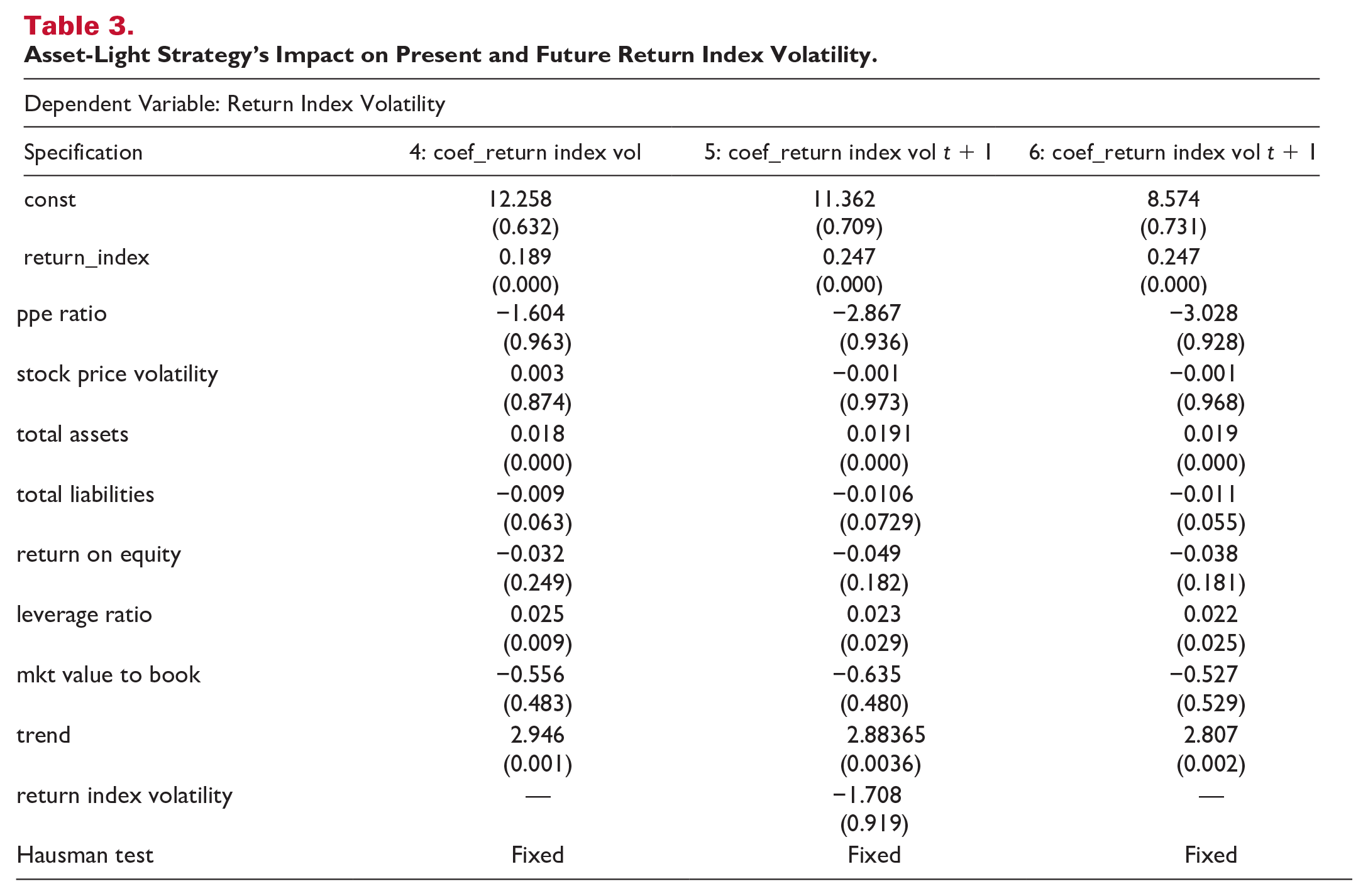

Table 3 shows that from 1970 to 2018, the asset-light strategy (PPE ratio) was neither related to present nor future return index volatility. To test the robustness of our results, we also adopted a different computation of the volatility of companies’ returns. In particular, we computed the volatility as an average of the monthly volatility. The results are consistent. Specifically, the asset-light strategy does not influence the volatility of firms’ stock returns.

Asset-Light Strategy’s Impact on Present and Future Return Index Volatility.

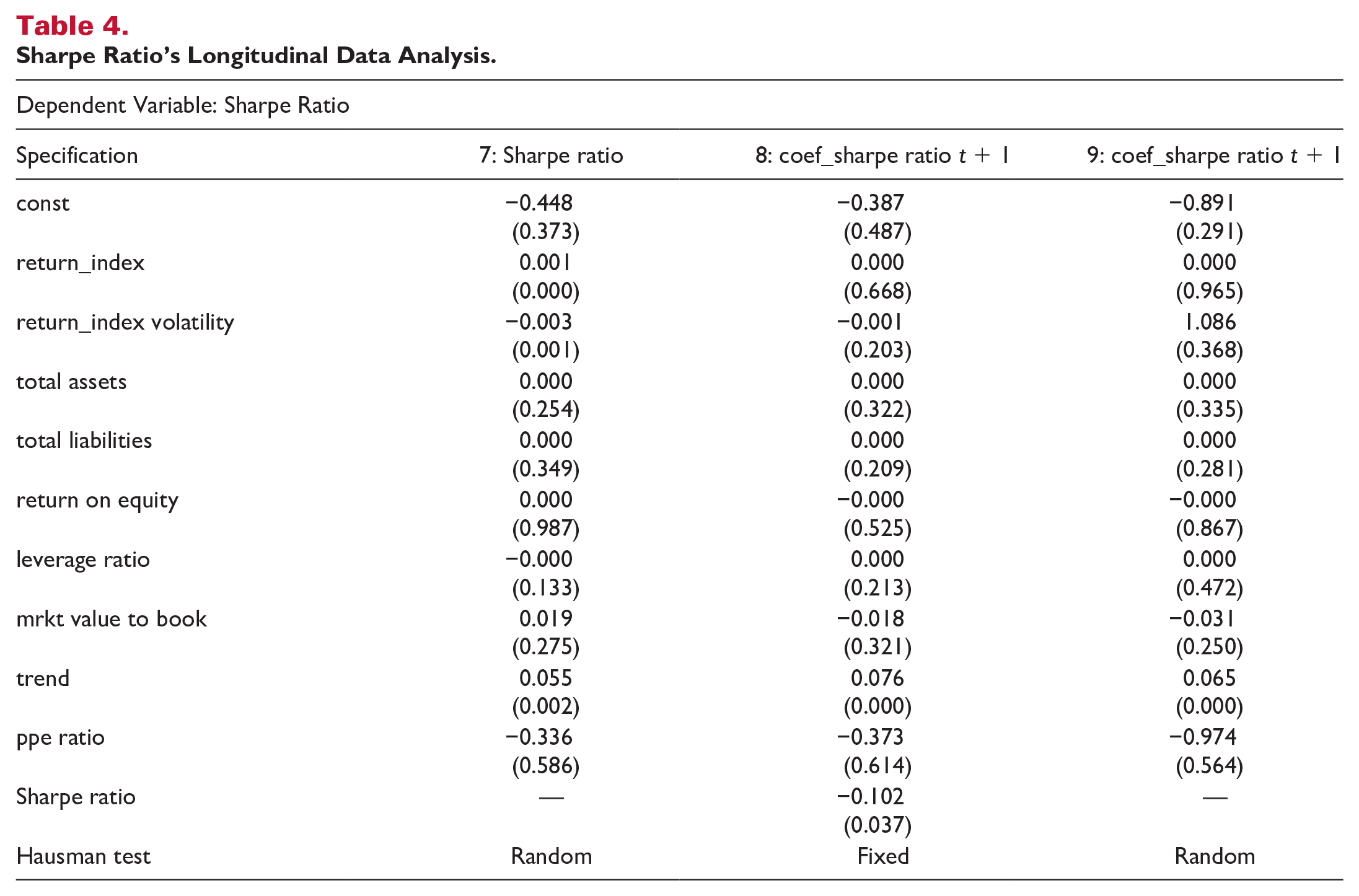

Consistent with previous findings, the asset-light strategy has no impact on U.S. hotel companies’ present and future performance (Table 4).

Sharpe Ratio’s Longitudinal Data Analysis.

Discussion

The results show that the asset-light strategy fails to constitute a generic solution for all hotel companies. In particular, results show that the asset-light strategy has no impact on the long-term performance of hotels listed on a stock exchange. We argue that such results might be explained by the transitivity costs related to the principal–agent problem that the separation between ownership and management inevitably raises.

In fact, as originally reported by Berle and Means (1932), the separation of ownership and management results in a complex ownership structure. Not every company has the means to support such complexity. For instance, franchise and management contracts are subject to agency relationships (Deroos, 2010), defined as a contract under which the principal appoints the agent to accomplish services on its behalf (Jensen & Meckling, 1976). The agency relationship management is costly and time-consuming. When it comes to communication, “franchisees are definitely on the other side of the wall” (Brookes & Roper, 2012, p. 587). Yet, one of the main franchising challenges is to avoid the type of “free riding” that arises from the agent–principal relationship (Kidwell et al., 2007). The agent (franchisee) may choose to free ride, that is, to benefit from efforts made by other outlets using the same brand by cutting inputs to increase profits (Combs et al., 2004; Perryman & Combs, 2012). For instance, a franchisee could reduce bathroom-cleaning frequency to increase profits or fail to upgrade facilities (Perryman & Combs, 2012).

High transaction costs also result in contract incompleteness: “the economic agents cannot conclude complete contracts because transaction costs are too high to specify all relevant circumstances in the contracts” (Windsperger & Dant, 2005, p. 261). This means that residual rights will not be addressed in franchise contracts (Hadfield, 1990).

In addition, it has been established that real estate holdings are associated with value creation for shareholders when properties are integral components of service performance or house strategic functions (Yu & Liow, 2009).

Finally, the argument that going asset-light strengthens competitive advantage by focusing on brand equity is controversial. In fact, capital expenditures to boost brand image might come at the expense of equity value (Turner & Guilding, 2010).

Overall, this study has enhanced the understanding of the asset-light strategy. The present findings might not only lay the foundations for academics to further investigate the asset-light model, but also uncover considerable managerial implications that could possibly influence shareholders’ willingness to invest in hospitality companies.

This research note aims to intensify the debate over the asset-light model and ownership practices in the hospitality industry (for U.S. and international companies). The authors hope that this study can set the grounds for further research exploring the plural form allocation to each ownership type.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, or publication of this article.