Abstract

This research note investigates the stock market reactions of international hospitality firms to COVID-19’s pandemic announcement by the World Health Organization. In line with the behavioral finance literature, the findings indicate that, in the short term, investors overestimated the risks underlying asset-heavy firms because of information uncertainty. Firms pursuing an asset-light (AL) strategy are associated to significantly less negative cumulative abnormal returns in the 4 days following the announcement, especially firms following an AL strategy that reduces significantly the operating leverage. However, this difference vanishes after 5 trading days, meaning that investors revised their expectations. This research note suggests that the cost structure of AL firms matters in reducing information uncertainty and sheds light on the consequences of the COVID-19 crisis on the hospitality industry. It also provides useful information to board members, financial analysts, and companies’ top managers when evaluating whether and how to pursue an AL strategy, and the potential consequences of it.

Keywords

Introduction

This research note investigates hotel and restaurant firms’ stock market reactions to the World Health Organization (WHO) announcement that the COVID-19 epidemic had officially become a pandemic. Following this announcement, lockdown restrictions started to be imposed in Europe and in North America, drastically impacting consumer demand and threatening the survival of many firms in the hospitality industry. As this exogenous shock is exceptional both in scope and severity (Ding et al., 2020; Ramelli and Wagner, 2020), it provides an interesting laboratory to investigate how firms with different characteristics responded to this shock. Song et al. (2020) document that large internationalized US restaurant firms, with more leverage, more cash flows, and less return on assets (ROA), suffered less negative stock market declines over a 5-month period. This study explicitly contributes to this literature by investigating the stock market reaction of international hospitality firms to the pandemic announcement by the WHO.

The hotel and restaurant industry is specific because of firms’ high proportion of fixed assets and reliance on consumers’ discretionary spending (Kumcu and Kaufman, 2011; Singal, 2012; Upneja and Dalbor, 1999). The pursuit of a fee-oriented asset-light (AL hereafter) strategy reduces this risk (Choi et al., 2018) and enables firms to have greater flexibility (Gim and Jang, 2019), to stabilize cash flows (Andrew et al., 2007; Dogru et al., 2020), and to grow faster without heavy investments (Sohn et al., 2013), which led many hotel and restaurant firms worldwide to develop their managed and franchise businesses in recent decades (Li and Singal, 2019). This trend deeply impacted firms’ cost structure, as companies pursuing an AL strategy benefit from franchise and management fees, without having to support the significant fixed costs of owning and/or operating a business that make them struggle with profit variability during periods of unstable demand (Graham and Harris, 1999). This relates to the concept of operating leverage (OL), a measure of operating profit’s sensitivity to variations in revenue. 1 The risks associated with high OL have been well documented in the literature (e.g. Bessembinder, 1991; He et al., 2020; Kahl et al., 2014; Novy-Marx, 2011).

Fee-based income is more stable than operating profit earned from company-owned properties, contributing to risk reduction (Sohn et al., 2014). During a period of low demand, firms with higher fixed costs suffer the most and have more uncertain future cash flows. While the operating loss of company-owned properties is transferred directly to the owner’s bottom line, operators can still get profit since the base fee is positive, as long as the hotel under management contract or franchising generates revenue (Sohn et al., 2014). While previous research has examined the role of business strategies on various outcomes (e.g. O’Neill and Xiao, 2006; Panvisavas and Taylor, 2006; Poretti and Blal, 2020; Seo and Soh, 2019; Sohn et al., 2013), their influence on information uncertainty and in turn on stock market reaction to an exogenous shock lacks similar research.

Substantial evidence in the behavioral finance literature documents how behavioral biases influence risk perception and investors’ reaction to new information (e.g. Danbolt et al., 2015; Jegadeesh and Titman, 1993; Zhang, 2006). Zhang (2006) shows that greater information uncertainty produces higher expected returns following good news and lower expected returns following bad news, where information uncertainty is defined as (p. 1) “ambiguity with respect to the implications of new information for a firm’s value.” Moreover, sentiment influences the assessment of risk, as happy investors underestimate risk, while pessimistic investors overestimate risk (Danbolt et al., 2015; Johnson and Tversky, 1983; Kaplanski et al., 2015; Loewenstein et al., 2001). The COVID-19 crisis occurred unexpectedly after one of the longest bull markets ever 2 and led to the biggest drop in investor sentiment on record. 3 Relaxing the assumption of strict investor rationality, this study posits that investors, in response to the pandemic announcement, overestimated the risks underlying firms with a high degree of OL because of the greater information uncertainty related to future cash flows. To the best of our knowledge, no prior studies have examined how the information uncertainty related to the business strategy followed by hotel and restaurant companies influences investors’ reactions to a negative exogenous shock impacting the whole industry. This research note intends to fill this gap.

Using a sample of publicly listed hotel and restaurant firms in Europe and North America and applying an event study methodology, the findings documented in this research note contribute to the literature in several ways. First, it adds to the overall understanding of the consequences of the COVID-19 crisis on the hospitality industry (Ding et al., 2020; Ramelli and Wagner, 2020; Song et al., 2020) by showing that business strategies and the underlying information uncertainty affect investor reaction. More specifically, this study explicitly contributes to Song et al. (2020) by highlighting the role of AL strategies that reduce OL (i.e. that are substantial enough to modify the cost structure of the firm) in mitigating stock market reaction. Second, it provides additional insight into the AL phenomenon and its perception by market participants. Only AL strategies that lower OL significantly reduce information uncertainty and mitigate investors’ perception of the firm’s underlying risk and ability to survive a crisis. Finally, in line with Hirshleifer (2001) and Daniel et al. (1998, 2001), it sheds light on specific situations in which investors’ psychological biases (e.g. behavioral biases related to pricing anomalies, such as underreaction to new information and overconfidence, or the overweighting of prior information due to conservative (anchoring) biases) are increased when there is more uncertainty.

Data and methodology

Sample

To build the sample, this study started with all hotel and restaurant firms available on Thomson Reuters Datastream (N = 322), from which only companies from Europe and North America were retained (N = 140). Franchise and management fees information were collected in the available annual reports and 10-k forms (N = 88). The final sample is composed of 69 companies for which stock prices as well as accounting information were available on Datastream. Of the 69 firms, 28 (41%) are from Europe 4 and 41 (59%) are from North America.

Event study

To capture the market’s reaction, this study implements an event study with the event being the COVID-19 pandemic announcement by the WHO. Event study is typically applied to estimate the stock market reaction to news announcements, in which the sign and significance of the abnormal returns following the announcements are evaluated (Graf, 2009). In line with Lee and Connolly (2010) and Gim and Jang (2020), using ordinary least-squares regressions, the parameters of the market model (model 1) were first estimated for each firm over 200 daily returns, from −210 days to −10 days before the event date:

Next, the abnormal returns are calculated by comparing each firm’s effective stock return on a given day to the expected return using the estimated parameters derived from the market model and applied to the market return. In other words, the abnormal returns are the prediction errors from the market model:

where

In a last step, cumulative abnormal returns (CARs) are computed as the sum of abnormal returns over a given event window ({−1; +t}) 6 :

Model development

To analyze the factors impacting the stock market reaction to COVID-19 pandemic announcement, the following ordinary least-squares models are used:

where

Results

Market reaction to WHO announcement

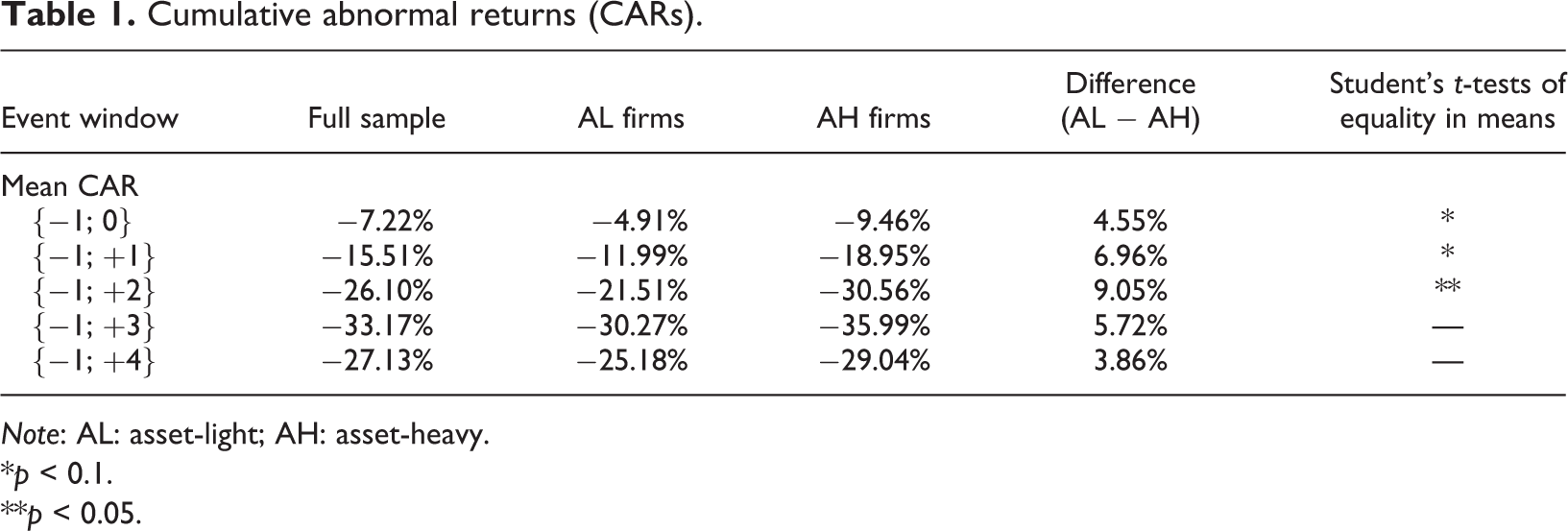

Table 1 provides descriptive statistics about mean CARs over five time windows ({−1; 0} to {−1; +4}). Regarding the full sample, it appears that mean CARs range from −7.22% for the {−1; 0} time window to −33.17% for the {−1; +3} time window. When the sample is split between AL and asset-heavy firms, results suggest that CARs are more negative for asset-heavy firms over the five time windows. Student’s t-tests indicate that the difference in mean CARs is statistically significant for three time windows out of five. Overall, these preliminary results indicate that the stock market reaction to the COVID-19 pandemic announcement significantly differed across firms following different business strategies.

Cumulative abnormal returns (CARs).

Note: AL: asset-light; AH: asset-heavy.

*p < 0.1.

**p < 0.05.

The determinants of CARs

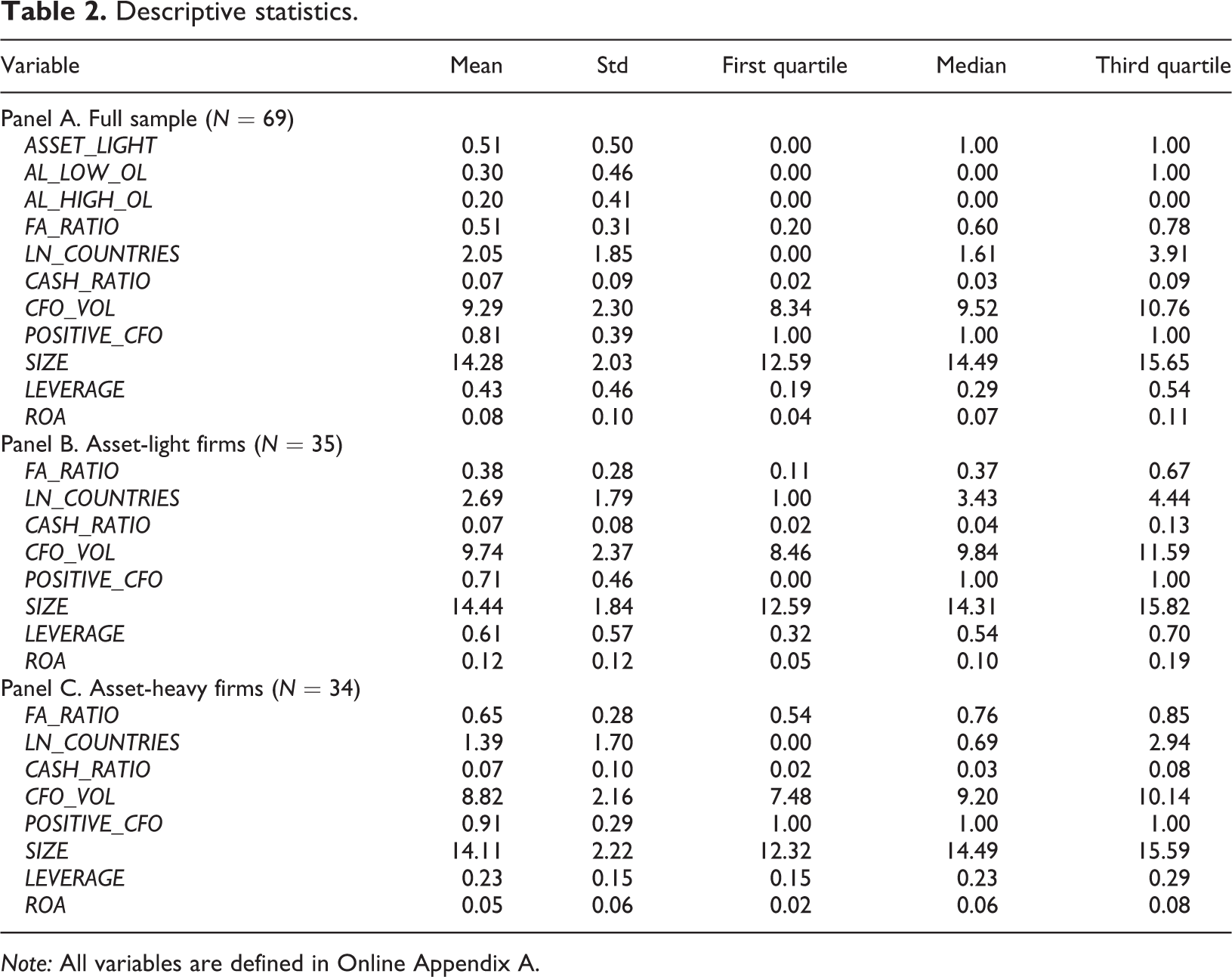

In this section, the determinants of CARs are investigated using multivariate analyses (models 4 and 5). Table 2 presents descriptive statistics of the variables used in the tests for the full sample (panel A), AL firms (panel B), and asset-heavy firms (panel C). AL firms have smaller fixed assets ratios (FA_RATIO), are more internationalized (LN_COUNTRIES), have greater cash flow volatility (CFO_VOL), disclose less frequent positive net cash flows (POSITIVE_CFO), are larger (SIZE), have more debt (LEVERAGE), and generate better economic performance (ROA).

Descriptive statistics.

Note: All variables are defined in Online Appendix A.

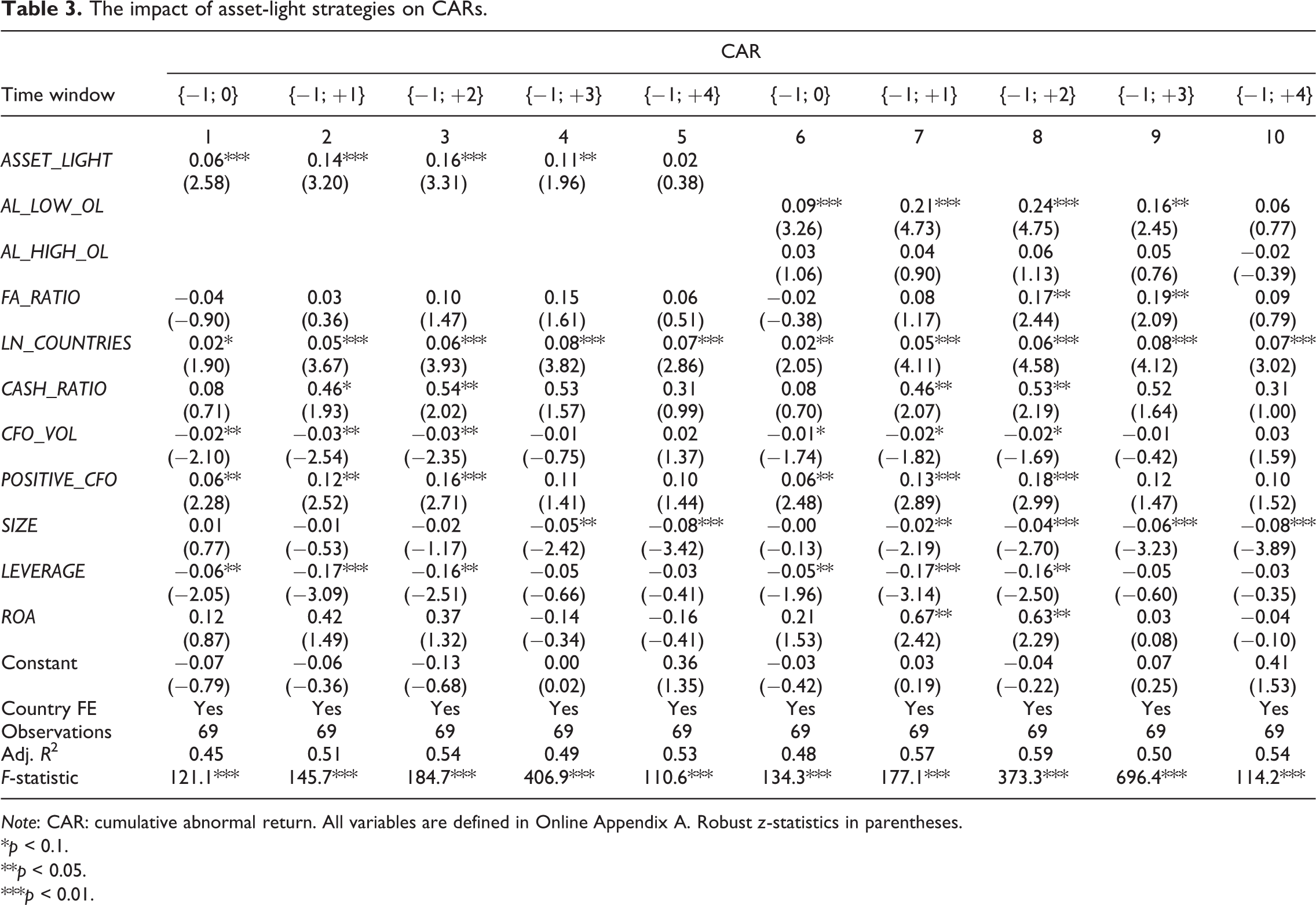

Table 3 documents the results of the analysis of the determinants of CARs using ordinary least squares regressions. In columns 1 to 4, the coefficients on ASSET_LIGHT are positive and significant (p < 0.01 in columns 1 to 3, and p < 0.05 in column 4), meaning that pursuing an AL strategy led to less negative CARs following the announcement. However, the coefficient on ASSET_LIGHT is not significant in column 5, meaning that the difference in CARs between AL and non-AL firms vanishes after 4 trading days. Next, in columns 6 to 10, we differentiate between AL firms with a high OL (AL_HIGH_OL) and low OL (AL_LOW_OL) to analyze how the cost structure of AL firms mitigated the stock market reaction to the pandemic announcement. 8 The results indicate that firms applying an AL strategy that leads to a low degree of OL are associated to less negative CARs, as documented by the positive and significant (p < 0.01 in columns 6 to 8, p < 0.05 in column 9) coefficients on AL_LOW_OL in columns 6 to 9. Again, this effect vanishes after 4 trading days as documented in column 10. In contrast, the coefficients on AL_HIGH_OL are not statistically different from zero in all columns. In line with Song et al. (2020), internationalization (LN_COUNTRIES) and positive cash flows (POSITIVE_CFO) moderate the severity of CARs, while larger firms with more cash flow volatility and more leverage suffered form more negative CARs.

The impact of asset-light strategies on CARs.

Note: CAR: cumulative abnormal return. All variables are defined in Online Appendix A. Robust z-statistics in parentheses.

*p < 0.1.

**p < 0.05.

***p < 0.01.

Overall, these results contribute to Song et al. (2020) by documenting an overreaction of investors in non-AL firms and AL firms with a high degree of OL. In other words, this study documents that abnormal returns for AL firms with low OL are less negative in the days following the pandemic announcement. However, after 4 trading days, the difference disappears as investors revised their expectations. In line with Hirshleifer (2001) and Daniel et al. (1998, 2001), psychological biases are increased when there is more uncertainty, and only an AL strategy that reduces OL leads to lower levels of information uncertainty.

Conclusion

The COVID-19 crisis provides an opportunity to investigate investors’ perception and understanding of firms pursuing AL strategies in a period of extraordinarily high uncertainty. Using a sample of hospitality firms, this research note analyses whether the stock market reaction to the pandemic announcement differs across firms with different business strategies. The findings indicate that CARs are significantly less negative for firms pursuing an AL strategy that reduces OL. This study contributes to the overall understanding of the consequences of the COVID-19 crisis on the hospitality industry. While Song et al. (2020) explain that, in the case of the COVID-19 crisis, the risk reduction role of franchising may be marginalized as damages from COVID-19 are omnipresent, we show that in the short term, AL strategies that reduce OL mitigated abnormal stock market reactions. Despite the uncertainty caused by the crisis and its consequences in the long run, we provide insight into investors’ perception of the risk underlying hospitality firms with different business models. The findings also aim to better inform executives about investors’ perception of a specific business strategy, namely the AL strategy. Finally, this study sheds light on the role played by OL for hospitality firms. These results are particularly useful to board members, hospitality financial analysts, and hotel and restaurant companies’ top managers when evaluating whether and how to pursue an AL strategy, and the potential consequences of it.

This study is not without limitations. The nature and the size of the sample potentially limits the extent to which the results can be generalized. By including country fixed effects, our models are accounting for country-specific differences. Moreover, given the range of control variables that are included in our tests, the heterogeneity underlying our sample (e.g., in terms of degree of internationalization, liquidity, profitability, size, leverage, and business volatility) should also be accounted for. Nevertheless, the sampled hospitality firms in different countries may be heterogeneous in terms of various factors such as brand equity (i.e. firm level) and government regulations on business (i.e. country level). Also, the WHO’s COVID-19 pandemic announcement may not be sufficient to fully grasp investors’ perception and response to the crisis.

Future study topic can be inspired based on the findings of this study. While the focus of this study is on the short-term stock market reaction, it might be interesting to investigate the impact of the pandemic on hospitality firms in the longer run. The COVID-19 pandemic is still in progress; therefore, future studies are advised to continue observing the situation to find further research implications. Future research may examine investors’ reaction to firms pursuing AL strategies during global economic recovery from COVID-19. Furthermore, the results of this study can be compared with other types of negative announcements. It could also be a fruitful future research topic to explore how the various country-level initiatives undertaken to limit bankruptcies and boost consumption have impacted hospitality firms’ businesses.

Supplemental material

Supplemental Material, sj-pdf-1-teu-10.1177_13548166211005198 - Asset-light strategies and stock market reactions to COVID-19’s pandemic announcement: The case of hospitality firms

Supplemental Material, sj-pdf-1-teu-10.1177_13548166211005198 for Asset-light strategies and stock market reactions to COVID-19’s pandemic announcement: The case of hospitality firms by Cédric Poretti and Cindy Yoonjoung Heo in Tourism Economics

Footnotes

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Supplemental material

Supplemental material for this article is available online.

Notes

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.