Abstract

The use of glucagon, in conjunction with insulin, in a dual chamber pump (artificial pancreas, AP) is a working goal for multiple companies and researchers. However, capital investment to create, operate, and maintain facilities with sufficient scale to produce enough glucagon to treat millions of patients, at a level of profit that makes it feasible, will be substantial. It can be assumed that the marketplace will expect the daily cost of glucagon (to the consumer) to be similar to the daily cost of insulin. After one subtracts wholesaler and pharmacy markup, there may be very few dollars remaining for the drug company to cover profit, capital expenditures, marketing, burden, and other costs. Without the potential for adequate margins, manufacturers may not be willing to take the risk. Assuming that the projections discussed in this article are in the right ballpark, advance planning for the supply for glucagon needs to start today and not wait for the AP to come to market.

The use of glucagon, in conjunction with insulin, in a dual chamber pump (artificial pancreas or AP) is a working goal for multiple companies and researchers. The concept is, with the use of hardware, sensors, and software, to meter the infusion of insulin and glucagon to mimic a normal profile in a person with diabetes. In this article, I address some of the challenges associated with the use of glucagon with regard to manufacturing, supply, and marketing. I believe that many of these issues have not been fully appreciated to date.

Though there is variation among different subjects and among different bihormonal algorithms, research suggests that the amount of glucagon needed per day in an adult with type 1 diabetes using an AP can range as high as 0.5-1.0 mg.1-3 The pump chamber housing glucagon will probably need to hold 3 to perhaps 5 days of medication. The required drug maintenance temperatures are likely to range from that at the skin surface to the local external environment (100°F or more). In contrast to the lyophilization/reconstitution approach, much of the recent glucagon research has focused on developing a stable liquid that will maintain potency and physical characteristics without line obstruction.

There are certain assumptions that need to be made regarding the supply of glucagon for an AP. Our belief is that few of these have been previously addressed.

Assumptions

The marketplace will expect the daily cost of glucagon (to the consumer) to be similar to the daily cost of insulin.

An AP will ultimately be used by millions of persons with diabetes.

Synthetic and recombinant glucagon are clinically equivalent.

Supply

Currently, in the United States, glucagon is approved only in recombinant form and marketed only by Eli Lilly and Novo Nordisk. Each uses a proprietary manufacturing process (E. coli and yeast, respectively), and currently neither company will sell to a third party for remarketing. Synthetic glucagon is not yet approved by the FDA (though it is in Japan).

To market glucagon in the United States, any new market entrant would need to either (1) develop its own recombinant process and build facilities to support this endeavor (~US$10+ million for a base facility [operating costs not included] with expansion and scaling at additional cost, to be determined) or (2) purchase or produce synthetic glucagon. Both of these approaches will require extensive regulatory work to gain FDA approval, including an animal toxicology study and a human study (eg, a single-dose human crossover study with a comparator). To these requirements must be added the development of a manufacturing/packaging process for either liquid or lyophilized glucagon (~US$3-5 million), which may well require 1-2 years of development time (likely longer if pursuing a stable liquid glucagon).

Synthetic glucagon can currently be produced in batch sizes up to 0.5 kilograms, requiring a time frame of 2-4 months per batch (assume 3 months). If demand grows and volumes are large, recombinant glucagon may offer a lower cost of goods than synthetic glucagon. Synthetic peptide manufacturers note that scaling is limited and thus price reductions may not be significant at larger volumes. The expectation is the need for recombinant production.

There are those who would suggest that the development of improved delivery systems for glucagon in the severe hypoglycemia (SH) treatment space (either through better lyophilized/reconstituted systems or stable liquid glucagon) will expand the market sufficiently to drive down prices. Examination of the SH opportunity (which is outside the scope of this article) would likely show that although there is an increased opportunity (which could lead to slightly lower glucagon raw material costs), the scale is may be insufficient to appreciably affect the price of glucagon in the AP.

User Market

Let us now evaluate the market. The potential market for an AP is all people with type 1 diabetes and the population of type 2 patients who use insulin. To identify the segment of the type 2 population that has difficulty with maintaining tight control, we can further narrow the type 2 insulin users to those who have been on insulin for at least 7-10 years. With these criteria in mind, what do we arrive at in the way of a potential target population for use of an AP?

There are currently ~1.2 million patients with type 1 diabetes in the United States (growing by approximately 35-50 000 per year). Approximately 30% of individuals with type 2 diabetes are using insulin, which yields a population (currently) of ~4.5 million. Assuming that 25% of these patients have been on insulin for ~10 years yields ~1.125 million. In a published article 4 the authors noted that treatment with insulin for >10 years is an important predictor of increased risk of SH in type 2 diabetes. They went on to note that people with type 2 diabetes become insulin deficient, their frequency of SH approaches that experienced by people with type 1 diabetes. (These are approximations for illustration purposes only.) This yields a total of ~2.3 million potential AP users. If the penetration rate started at 10% in year 1 and took 10 years to reach a maximum of 70% of the defined universe (for this exercise), the number of AP users in year 1 and year 10 respectively would be 230 000 patients and 1.61 million patients. As mentioned, current studies suggest that the daily use of glucagon could range from 0.5 mg to 1.0 mg. At the end of year 1, the daily consumption of glucagon would be 115- 230 grams/day. In year 10, the daily consumption would be 800-1600 grams. At a rate of 115 grams/day in year 1, 42 kg would be consumed (low end) and 84 kg on the high end. Annual consumption in year 10 would be 292-584 kg.

There is no current or planned capacity to meet this demand. As already noted, current synthetic maximal batch sizes max at about ½ kg and require approximately 3 months to produce. As noted, at the end of year 1, a 0.5 kg batch would last for only 2-3 days. To meet anticipated demand, it will be necessary to define usage patterns, understand the need for resources, and determine near-term and long-term capital investment.

Costs

Since recombinant glucagon is not currently available for purchase in the United States (for remarketing), synthetic glucagon would be the only recourse for companies other than Eli Lilly and Novo Nordisk (unless they chose to build their own recombinant facility). Currently, the best prices available for GMP glucagon, in raw form, range from $3.50 to $4.50 per mg ($3500-4500 per gram).

Raw glucagon needs to be formulated. This may involve adding excipients, stabilizers, and agents to increase speed of reconstitution (in the lyophilized case) or to maintain viability. These additives may also add challenges regarding toxicity, may require solvents that are not well-suited for a human drug, or raise other concerns. In addition, it will be important to understand whether packaging will be needed to minimize exposure to light and to understand other elements of the final product. Even if all safety and regulatory issues are successfully dealt with, there remain substantial costs to optimization of additives, formulation, and package development.

Packaging may be simple (a vial) or a more complicated and expensive (a prefilled syringe or pen device). If the product has temperature stability challenges and requires cold storage and transport, the costs will rise substantially.

Let’s take a snapshot of some the potential costs (a list obviously based on estimates):

Raw glucagon: $3.50-4.50/mg

Formulation and packaging: $1.50-2.50/unit

Marketing costs: ?

Overhead and profit: ? (given the capital outlay and risk, a significant markup may be required)

Warehousing and distribution: 7%

Retailer markup: 25%

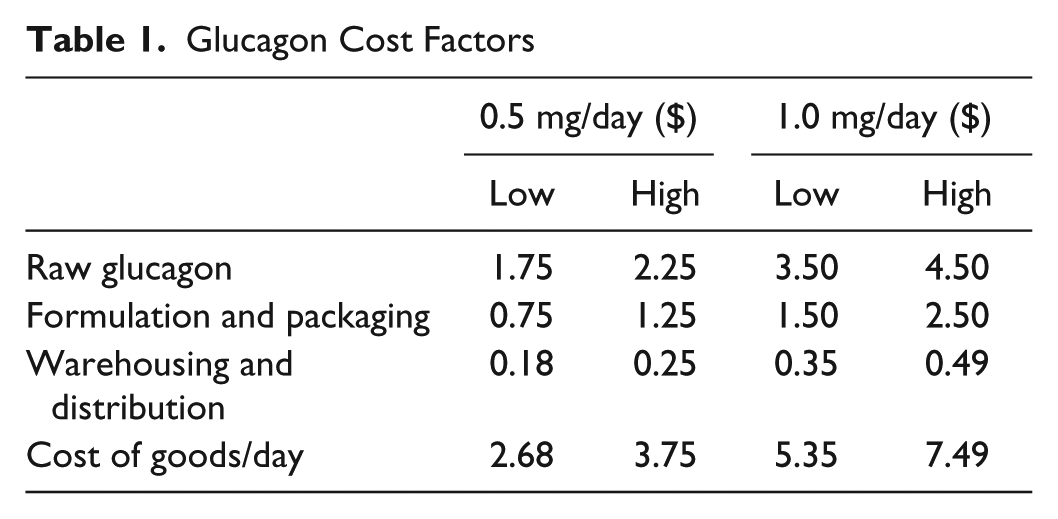

Using the lowest known estimated costs from the list above, the cost per day (excluding any manufacturer profit, return on investment, marketing costs, and overhead burden) is shown in Table 1.

Glucagon Cost Factors

It should also be noted that non-US North American costs for glucagon are 25-30% of those for the United States. If single-payer governments will reimburse only the existing glucagon price(s), given the daily/annual projected usage, it is highly unlikely that the AP could include glucagon or that it would be reimbursed at a sufficient rate to make it financially viable unless there was a major price decline.

FDA Approval

Whether recombinant or synthetic glucagon is used, it is an open question as to whether the FDA will require studies to show that the continual daily administration of exogenous glucagon will lead to antibody formation or other complications. If the glucagon formulation contains any other agents, they may also need to be studied to determine the impact (if any) of chronic long-term administration. Should such studies be required, the development cost and time requirements could further impact the cost of glucagon supply and further compound the issues being discussed.

Marketplace

Let’s look at the insulin and glucagon costs apart from the AP pump, sensor(s) and software. Assume that insulin cost for a 1000 unit vial today is ~$220 (retail). Assuming an average daily dose of 50 units the daily cost of the insulin alone would be ~$11. If the market expected that the glucagon (at retail) cost should be equal to the insulin we can calculate the pricing and cost structure, as follows: Assume a glucagon retail cost of $11/day. Assume a pharmacy markup of 25%, which means the cost from the wholesaler needs to be $8.80. Assuming the wholesaler markup is ~7% means that the wholesaler needs to purchase the drug from the manufacturer for $8.22. If the basic cost of goods costs are $2.68-7.49, that leaves $0.73-5.54/mg to cover profit, capital expenditures, marketing, burden, and other costs (depending on the dosage).

Given the projected volume of glucagon, there would be considerable capital expense to ramp up and continue expansion to meet the potential demand for glucagon. This would also mean that the daily cost of insulin and glucagon would be approximately $22/day or roughly $8000/year. Especially in regions outside of the United States, these numbers represent a major challenge. Inside the United States, the payers may well expect research that shows the combination reduces hospital admissions, emergency transport, and related service costs.

Conclusions

To be financially viable, the cost of raw glucagon will need to be substantially lower than current market prices ($1000/g or less).

Developers of proprietary liquid formulations have an expectation that the drug would command a premium price. Given the challenges raised in this article, that assumption needs to be carefully reviewed.

Whether glucagon is available in a liquid form ready for transfer to an AP or lyophilized and reconstituted just prior to transfer to the AP, the overriding issues are supply and cost.

Capital investment to create, operate, and maintain facilities with sufficient scale to produce enough glucagon to treat millions of patients, at a level of profit that makes it feasible and desirable, is going to be substantial. Without the potential for adequate margins, manufacturers may not be willing to take the risk.

Glucagon production and supply would be mission critical if the AP were to be successfully introduced, and would leave no margin for supply error.

Assuming these projections are in the right ballpark, advance planning for the supply for glucagon needs to start today and not wait for the AP to come to market.

Have researchers and manufacturers considered these and other factors relating to the inclusion of glucagon in an AP? The challenges are multifactorial and should be carefully weighed now to allow for the necessary planning and effort(s) to include glucagon in an AP.

Recommendations

Define whether there will be insulin only pumps and/or an insulin/glucagon AP. Projections for both (if they are to exist) with quantity and uptake estimates by year.

Establish the payer community willingness to support the concept and define reasonable and acceptable reimbursement rates since this will define the return for the risk and investment.

Footnotes

Abbreviations

AP, artificial pancreas; FDA, US Food and Drug Administration; GMP, good manufacturing practices; SH, severe hypoglycemia.

Declaration of Conflicting Interests

The author(s) declared the following potential conflicts of interest with respect to the research, authorship, and/or publication of this article: Dick Rylander, Jr is an employee and stockholder of Enject, Inc.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.