Abstract

The clean energy transition has entered the policy discourse and government agenda of the Caspian oil-producing countries of Azerbaijan and Kazakhstan. Both countries have set a target to increase the share of renewable energy sources (RES) in total energy production by 2030. This article presents a comparative analysis of Azerbaijan and Kazakhstan in their paths to a low-carbon sources of energy covering the status of RES, renewable energy targets, and the role of government policy schemes in promoting renewable energy (RE) deployment. The study shows that despite some commonalities in the initial conditions (such as Soviet-era legacies of fossil-fuel-based infrastructure, a high degree of dependence on oil and gas rents, and dominance of state-owned enterprises), Kazakhstan adopted a more targeted regulatory framework and more elaborate policy schemes with regards to renewables than Azerbaijan did. In the latter case, the introduction of relevant renewable legislation has been significantly delayed or implemented only partially. As a result, Kazakhstan has performed relatively more successfully on advancing non-conventional renewable energy targets: non-hydro renewable sources accounted for 3% of total electricity generated in Kazakhstan and made up only 1% of electricity produced in Azerbaijan (as of 2020). This article highlights the following factors that stand out in explaining these variable outcomes: the degree of economic liberalization, quality of governance of the oil and gas sector, regulatory frameworks, and policy support schemes.

Introduction

In tackling climate change, many countries are gradually shifting away from fossil fuels towards renewable energy sources (RES) (such as solar, wind, biomass, and hydro) and green technologies (Markard, 2018). This process dubbed a “clean energy transition” and exemplified by, for example, Germany’s Energiewende has been variously described as “a gradual, prolonged affair” (Smil, 2019, 70), a “messy” process (Bordoff and O’Sullivan, 2022), or an “uneven” restructuring of energy systems (Guliyev, 2022). While most oil and mineral-rich countries in post-Soviet Eurasia have taken steps to increase the share of RES in their respective energy mixes, there still remains a significant gap between government pledges and actual implementation of concrete low-carbon energy policies (Karatayev et al., 2021; Laldjebaev et al., 2021; Shadrina, 2020).

The governments of Azerbaijan and Kazakhstan—two major oil-producing countries in post-communist Eurasia—have set ambitious renewable energy (RE) targets to expand the deployment of renewables in electricity generation in the coming decades. Kazakhstan aims to increase the share of RES to 15% by 2030 (Satubaldina, 2021), while Azerbaijan set to reach an even more ambitious goal. The government aims to reach its target of 30% renewable energy by 2030 (Mammadli, 2022; Ministry of Energy of Azerbaijan, 2020b). To meet their respective renewable energy goals, both countries have adopted legal and regulatory frameworks and introduced a range of policy support schemes.

Using an in-depth analysis of Azerbaijan and Kazakhstan, this article examines the effectiveness of adopted policy support mechanisms and progress made so far with regards to policy promotion of non-hydro renewables in these two countries. This study examines opportunities as well as barriers and gaps in implementing renewable policies and evaluates performance regarding the adoption and implementation of relevant legislative and regulatory frameworks. The aim of the article is to examine how differential country-specific conditions can help explain the variance in the extent of “targetedness” of regulatory frameworks and level of elaboration of policy schemes which in turn account for better or worse results. The analysis shows that Kazakhstan was an earlier adopter of renewable energy and championed a more targeted regulatory framework and more elaborate policy schemes than the government in Azerbaijan did. Compared to Kazakhstan, renewable energy legislation was adopted later in Azerbaijan. The question arises: Why more targeted and elaborate renewable policies in one case and not the other?

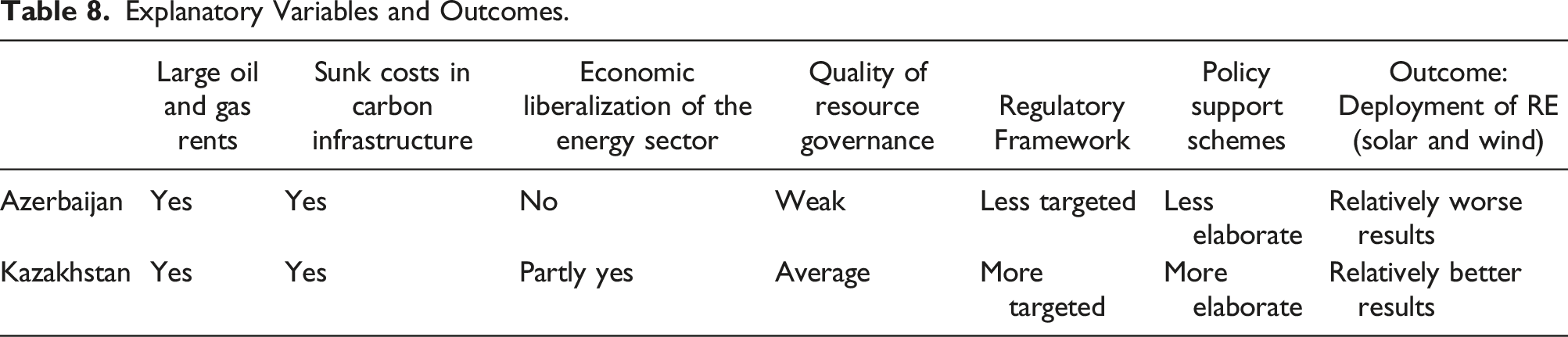

While the findings are tentative, the study shows that more targeted regulatory frameworks and elaborate policy schemes, such as those adopted by Kazakhstan, seem to yield better results. Creating a favorable enabling environment for private renewable companies—the policy pursued by Kazakhstan—appears to be more effective and efficient in promoting renewable energy than excessive state intervention and weak private firm participation, the policy stance favored by the government of Azerbaijan. Kazakhstan’s more targeted renewable policies reflect higher degree of economic liberalization pursued by Nazarbayev’s government including in the energy sector and relatively better management of its oil and gas sector.

Alongside excessive state intervention, quality of governance remains a key barrier to attracting much-needed capital to renewables expansion. While in both Azerbaijan and Kazakhstan, weaker accountability and oversight mechanisms in policy implementation raise the risks of corruption, Kazakhstan’s relatively more liberalized economy enabled the government to introduce a more targeted regulatory framework and more elaborate policy schemes which in turn fostered a relatively faster deployment of RES. It remains to be seen how the January 2022 unrest with death toll of 227 people in Kazakhstan (Bartlett & Bissenov, 2022) will affect foreign investments into the country’s renewable projects.

This study contributes to the existing research on the drivers of renewable energy transitions in mineral- and petroleum-rich countries (Abdmouleh et al., 2015; Ahmadov and Van Der Borg, 2019) and determinants of renewable policy outcomes (e.g., Marques and Fuinhas, 2012; Polzin et al., 2019). While there has been a proliferation of research on energy transitions (see, for example, Geels et al., 2017; IRENA, 2019a; Scholten, 2018; Victor et al., 2019), there is not enough understanding of which type of targeted policy support produces successful policy outcomes in low-carbon transitions. Understanding the link between policy support instruments and performance on decarbonization remains obscure, and much of the existing literature often focuses on the Global North (Del Río and Mir-Artigues, 2014).

The article is organized as follows. The next section provides a literature review with a special focus on policy support instruments in renewable development. This is followed by a description of methodology followed by two country case studies. Each country chapter starts with a summary of that country’s energy mix, renewables potential, renewable energy targets as well as its legal and regulatory frameworks and an analysis of political-economic barriers to harnessing their solar, wind and other renewable energy assets. Next, the study presents results of the analysis and discussion. The conclusion summarizes key policy implications.

Literature Review: Renewable Energy Support Policies

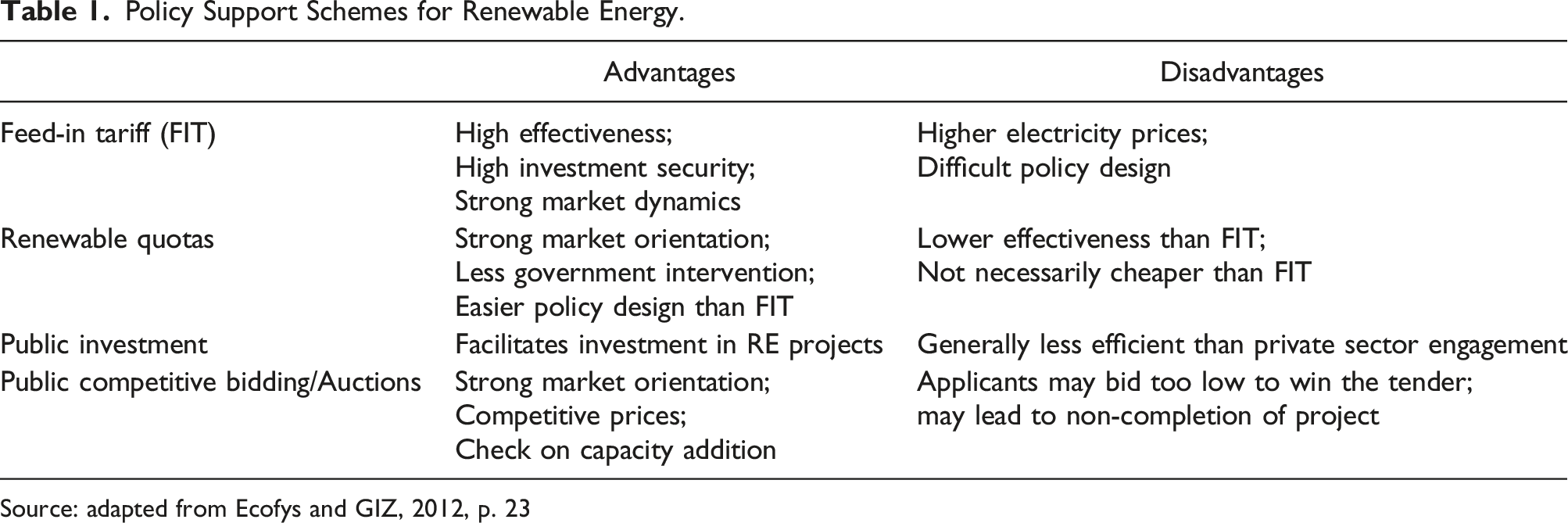

In seeking to reduce carbon emissions and promoting RES, countries across the globe adopted a range of policy support schemes. The key issue essentially revolves around the classic political economy question of whether market competition or the state should be the primary driving force. Which RE support schemes are favored ultimately depends on country-specific macro-political-economic frameworks and often some mix of state-market mechanisms is chosen. For example, following its (neo)liberal capitalist model, the UK prioritizes market-based mechanisms, whereas France has pursued the policy of state dirigisme with a greater role of the state (Green and Yatchew, 2012). A policy mix approach has advocated the adoption of a variety of policy instruments (Rosenow et al., 2017). Profitability of renewable projects has been contingent on public subsidies to renewable electricity producers provided through various policy support instruments (Mazzucato and Semieniuk, 2017, 35).

While there are existing studies providing overviews for Central Asia (Laldjebaev et al., 2021; Shadrina, 2020) and post-Soviet Eurasia, there has been scant attention paid to the role of policy support schemes and their relative performance to date. Different policy instruments can be employed ranging from the establishment of regulatory rules to the introduction of various fiscal stimuli (through subsidies and tax exemptions) to public investments (Green and Yatchew, 2012). Given that renewables are high-cost technologies and considering the continued relevance of Soviet legacies, governments across the post-Soviet space appear to play a leading role in steering the introduction of renewables-related infrastructure through various policy support schemes for RES.

Feed-in tariffs (FITs), auctions for power purchase agreements (PPAs) and renewable portfolio standards (RPSs) are the most commonly used policy support instruments (Polzin et al., 2019), with feed-in systems being the most widely spread and competitive bidding gaining more traction (Ecofys and GIZ, 2012; Schallenberg-Rodriguez, 2017).

As a policy instrument, Feed-in Tariff (FIT) schemes have become popular across Europe as a tool of mitigation of financial risk due to high upfront costs of renewable projects and has three essential elements: a renewable energy producer’s access to the grid to sell electricity (purchase obligation), guaranteed purchase at a certain price (i.e., fixed tariff) which is typically above market prices, and for a specified period of time (long payment duration) (Jacobs, 2014). A feed-in-tariff is based on the guaranteed payment of a fixed, minimum price for kilowatt-hour (kWh) of energy produced from RES (Couture and Gagnon, 2010).

Public financing schemes including public investments, loans, grants, and subsidies are employed in many countries and are viewed as particularly suitable in promoting RES in the initial stage of technology development. It particularly fits countries with weak private sectors and substandard financial markets where businesses lack sufficient capacity to invest in risky enterprises (Painuly and Wohlgemuth, 2021, 558). This also applies to post-Soviet countries many of which exhibit the co-existence of market mechanisms with strong role played by the state, known as state capitalism. Public investment is another form of RE support whereby the state provides direct funding to RE projects. Direct public investment is generally viewed as less efficient than a competitive market structure and its applicability thus needs to be limited to the early stages of RE deployment (Ecofys and GIZ, 2012).

Renewable quotas, also known as renewable portfolio standards, are the minimum share of RE in the electricity mix of power utilities. For example, renewable quotas are used extensively in China where provinces and municipalities are mandated to produce a fixed share of energy from RES (Wan and Tong, 2018).

Policy Support Schemes for Renewable Energy.

Source: adapted from Ecofys and GIZ, 2012, p. 23

Alongside the policy support schemes discussed above, governments can also stimulate renewables development by attracting foreign direct investments which are seen as a catalyst to clean energy transitions by providing much-needed financial and technological resources (Knutsson and Ibarlucea Flores, 2022). The presence of climate mitigation policies are found to be one of the key drivers for attracting FDI in renewable energy projects. By offering a guaranteed, above the market price for RE-sourced electricity, FITs are positively linked to private investment in RES (Azhgaliyeva et al., 2023).

A related strand of literature has been concerned with identifying factors favoring the deployment of renewable energy sources in mineral- and petroleum-rich countries (e.g., Abdmouleh et al., 2015; Malik, et al., 2019). A switch from fossil-fuel-based energy systems to renewable ones is associated with large economic costs which pose a financial burden for less developed countries. Many oil-producing states have developed strong vested interests around fossil fuel industries and will resist economic diversification that a transition away from fossil fuels would entail (Ahmadov and Van Der Borg, 2019). A putative renewable energy transition thus will be undermined by the rent-seeking incentives that oil and gas revenues tend to generate. In other words, for governments in developing countries “forgoing petroleum rents for uncertain prospects of developing renewable energy production can be economically and politically costly for incumbent political leaders” (Ahmadov and Van Der Borg, 2019, 362–363). In many countries that historically rely on fossil fuels, policy action to support RE is exacerbated by the path-dependent processes of “carbon lock-in” whereby fossil-fuel-based techno-institutional systems “can create pervasive market, policy, and organizational failures toward the adoption of [climate] mitigating policies and technologies” (Uhruh, 2000, 828).

The political resource curse literature contends that negative effects of a resource windfall are conditioned on—or amplified by—the quality of a countrysinstitutions. Good institutions—such as strong checks and balances, accountability, and democracy—are thought to “neutralize” the resource curse (Mehlum et al., 2006). Previous studies show that better governance quality—notably, bureaucratic competence and regulatory capacity—increase the chances of RE deployment (Cadoret and Padovano, 2016).

To summarize, current research suggests that high economic costs associated with renewable expansion, large oil and gas rents, high sunk costs in existing fossil fuel-based infrastructure, and vested interests in the fossil-fuel energy sector (dominated by state-owned enterprises) are likely to impede the deployment of RES. While countries with better-quality of governance institutions (especially in the natural resource sector), less dependence on petroleum rents, a relatively more liberalized market (and energy sector), and more elaborate and targeted policy support schemes are more likely to support the development of renewable energy.

Methods

Research Design

The study adopts a comparative case study design (Bennett, 2004) where the purpose is to provide detailed examination of individual cases in order to identify causal links between the independent and dependent variables. In this method, the researcher selects the cases to be examined and compared and offers an in-depth dive into each case paying particular attention to the interaction between variables within country-specific contexts. Case selection follows the most-similar systems design (MSSD)—also known as the method of “controlled comparison.” In the MSSD research design, chosen cases are similar in all respects except for one or several independent variables variation on which is purported to explain different outcomes, that is, variation on the dependent variable (George and Bennett, 2005, 81).

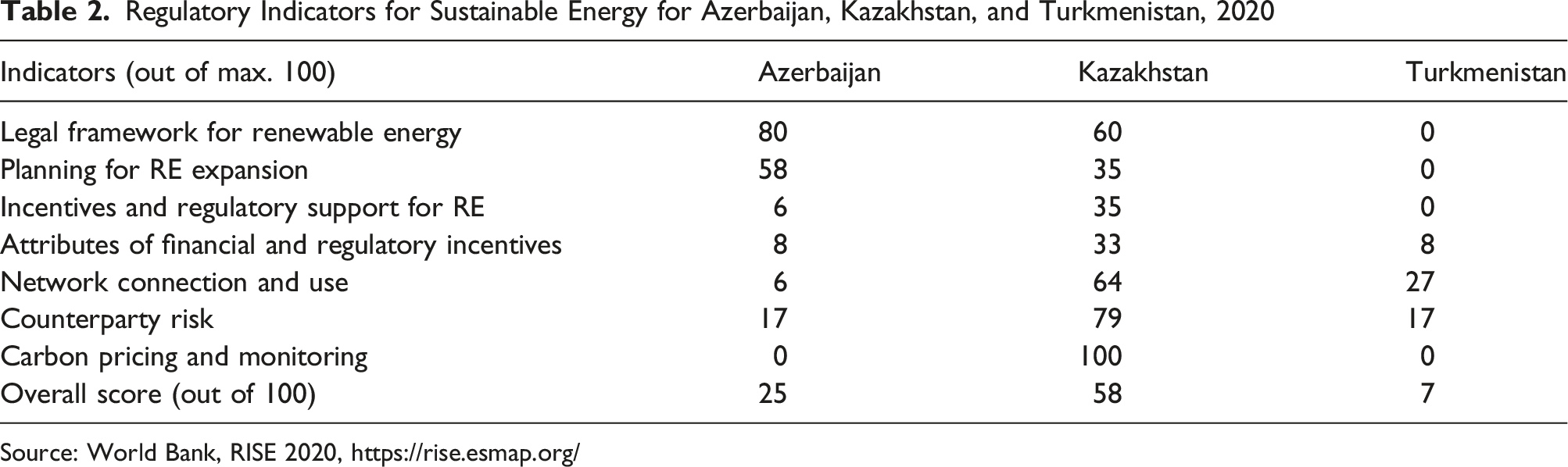

Regulatory Indicators for Sustainable Energy for Azerbaijan, Kazakhstan, and Turkmenistan, 2020

Source: World Bank, RISE 2020, https://rise.esmap.org/

Turkmenistan, another hydrocarbon-rich country with comparable characteristics would be a potential candidate case for inclusion but was left out because the country relies entirely on oil and gas in electricity production and does not have any solar or wind projects. Its overall score on the World Bank’s Renewable Energy sub-component of the 2020 RISE index is 7 (see Table 2).

Data Sources

Data on various energy and climate policies was gathered from official websites of relevant government bodies and agencies. The study also relies on existing studies on renewable policies and reports produced by international agencies such as the International Energy Agency (IEA), International Renewable Energy Agency (IRENA), and Natural Resource Governance Institute (NRGI). Additional sources for evaluating policies were drawn from a survey of country experts conducted within the framework of the joint Publish What You Pay (PWYP) and Eurasia Hub study entitled “Monitoring Energy Transitions in Eurasia (Azerbaijan, Kazakhstan, Kyrgyzstan, and Ukraine): Analysis and Policy Implications” (Guliyev, 2022). In addition, media reports and relevant statistics were used to compile information on national energy mixes and legislative acts with regards to renewable energy policy.

Case Study: Azerbaijan

As a traditional producer of oil and natural gas, Azerbaijan has abundant—albeit gradually shrinking—hydrocarbon reserves to tap into to meet its energy supply needs. Its entire energy supply and electricity generation system is built around domestically sourced and relatively affordable sources of natural gas and oil (but no coal). In Azerbaijan, as in other oil-rich countries with legacy fossil fuel infrastructure (such as gas-fired power plants), there is a weak demand for a radical shift to low-carbon sources.

In addition, state domination of the national energy market and its incomplete liberalization implies high barriers to the entry for potential RE private companies. For example, there is a total of 57 thermal power plants operating in Azerbaijan, and 50 of them are state-owned. The electricity sector is dominated by two vertically integrated companies, Azerenerji (generation and transmission) and Azerishiq (distribution) (Energy Charter, 2020). Excessive political centralization and the dominant role played by state monopolies are seen as key obstacles to developing renewable-sourced electricity generation capacity in Azerbaijan (Ahmadov, 2021).

With respect to the legislative framework, it took a long time for the government to adopt a separate law on renewables. The draft law on RES that had been long in the making was finally adopted in May 2021 (Law of the Republic of Azerbaijan, 2021), and it is yet to be seen how effectively it will be implemented. If the government is to meet its 30% renewable target by 2030 a more robust government action is needed to accelerate the deployment of renewables. The regulatory structure tasked with the promotion of RES—the Agency for Renewable Energy Sources under the Ministry of Energy [MoE]—is viewed as insufficiently empowered to change the status quo or to have a meaningful say in setting the energy transition agenda.

For a traditional fossil fuel producers like Azerbaijan, there appears to be no sense of urgency to shift to renewables. While the government took some initial steps to acquire clean energy technology, such as solar panels and wind turbines, to tap into its considerable RES potential, there has been a considerable lag in adopting an appropriate legislative framework. Similarly, the status and jurisdiction of the regulatory body for RE has underwent frequent changes indicating policy inconsistency and uncertainty. A great deal of instability in the policy environment, top-down decision making without civil society engagement, and lags in introducing relevant legislation have delayed the effective deployment of renewables.

Although there is more talk of RES now than a decade ago, the energy transition has not yet become a policy priority on the government’s agenda. The main obstacle to a successful energy transition is the existing energy management system dominated by state-owned companies. Unlike countries with a relatively liberalized market economy where private RE companies act as the driving force for a low-carbon transition, Azerbaijan with its state capitalist system (Guliyev, 2020a) lacks institutionalized private sector mechanisms needed to attract capital and technological innovation into domestic RE development.

Background

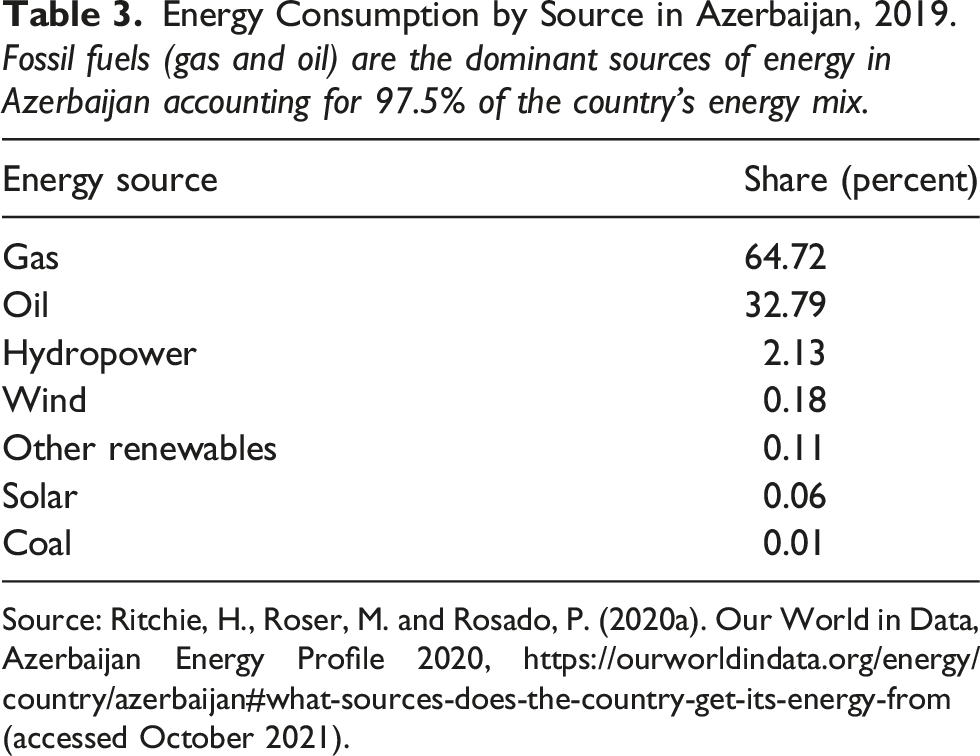

Energy Consumption by Source in Azerbaijan, 2019. Fossil fuels (gas and oil) are the dominant sources of energy in Azerbaijan accounting for 97.5% of the country’s energy mix.

Source: Ritchie, H., Roser, M. and Rosado, P. (2020a). Our World in Data, Azerbaijan Energy Profile 2020, https://ourworldindata.org/energy/country/azerbaijan#what-sources-does-the-country-get-its-energy-from (accessed October 2021).

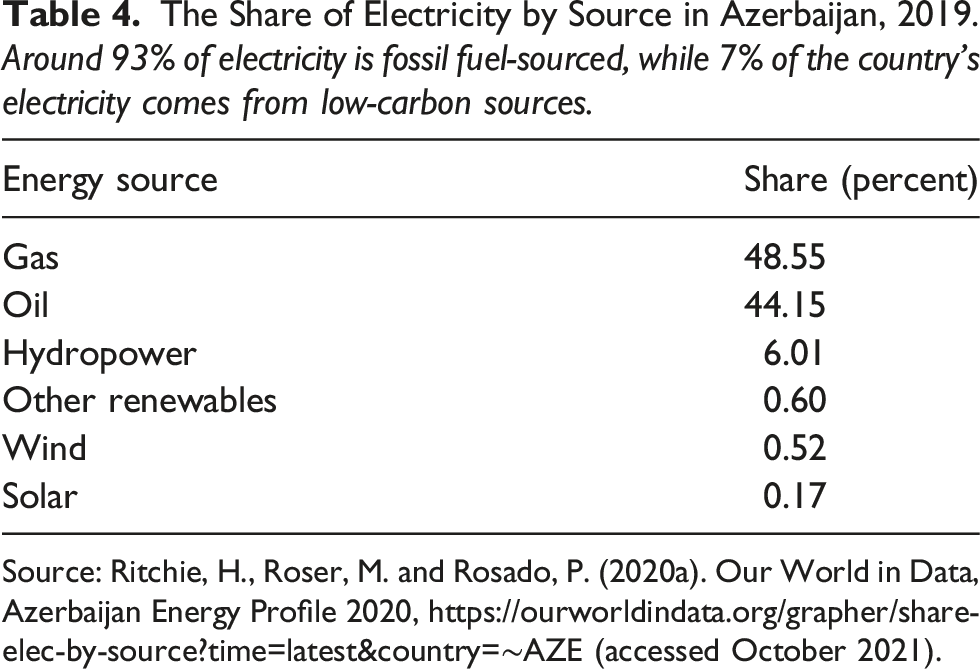

The Share of Electricity by Source in Azerbaijan, 2019. Around 93% of electricity is fossil fuel-sourced, while 7% of the country’s electricity comes from low-carbon sources.

Source: Ritchie, H., Roser, M. and Rosado, P. (2020a). Our World in Data, Azerbaijan Energy Profile 2020, https://ourworldindata.org/grapher/share-elec-by-source?time=latest&country=∼AZE (accessed October 2021).

The government has made strides to acquire RE technology reflected in the Presidential Order No. 1209 dated 29 May 2019 on the “Acceleration of Reforms in the Energy Sector” and the Order of the President of the Republic of Azerbaijan No. 1673 dated 5 December 2019 on the “Implementation of Pilot Projects in the Field of Use of Renewable Energy Sources.” In January 2020, agreements on the first pilot projects in renewable energy were signed with Saudi Arabia’s ACWA Power and Abu Dhabi’s state-owned renewable company Masdar (Ministry of Energy, 2020a). The first agreement (with ACWA) is for the construction of a 240 MW wind plant, and the second one (with Masdar) is a plan to build of a 230 MW solar power plant worth US $200 million in the Garadagh district, located 60 km south of Baku. Electricity generated at the plant will be purchased by Azerenerji OJSC which will also provide Masdar with access to the electricity transmission grid. Groundwork for a new onshore 240 MW wind farm in Khizi-Absheron developed by Saudi Arabia’s ACWA Power was laid out on January 14, 2022. The cost of the project is estimated at US$ 300 million (Ministry of Energy, 2022).

These contracts with ACWA and Masdar are foreign direct investment (FDI). Baku sees these RE projects as an opportunity to attract FDI to the domestic economy and as a way to diversify the economy following a number of exogenous shocks with adverse effects in 2008 and then again in 2015–2016 (Ahmadov, 2011; Caucasus Analytical Digest, 2016). FDI inflows have dropped in recent years and some energy multinationals divested from Azerbaijani energy projects (Guliyev, 2019). Azerbaijan has seen its oil production falling, and depletion of hydrocarbon resources poses risks to fiscal stability and sustainable development of the nation. The Shah Deniz-2 gas field development project was launched in 2018 and with the construction of the Southern Gas Corridor (SGC), Azeri gas is now supplied to Turkey and Europe. By increasing the share of renewable energy production, the government seeks to deploy renewable electricity for domestic energy consumption to ramp up its export of gas to Europe via SGC as gas exports generate higher government revenues.

In Azerbaijan, as of 2017 the total installed renewable power capacity amounted to 1267 MW (hydro: 1132 MW, solar: 35 MW, wind: 62 MW, and biomass: 38 MW) (IRENA, 2019b, 18). Largest RE projects are Azerishiq-owned 50 MW Yeni Yashma wind farm in Khizi (north of Baku) commissioned in 2018 and a 22 MW solar power plant in Nakhchivan (Yusifov, 2018).

Renewable Energy Targets

Azerbaijan joined the UNFCCC in 1995 and ratified the Kyoto Protocol in 2000 (IEA, 2021). In October 2016, Azerbaijan ratified the Paris Agreement and pledged to reduce its greenhous gas (GHG) emissions by 35% by 2030 compared to the 1990 base-year level (NDC Azerbaijan, 2017). At the 2021 United Nations Climate Change Conference (referred to as COP26), Azerbaijan announced its goal to reduce GHG emissions by 40% by 2050 and to create a “zero-emission zone in the liberated territories in Karabakh” (Azerbaijan COP26 Statement, 2021).

To achieve this goal, the government set a target to increase the share of renewables in electricity production to 30% by 2030. Works are under way to commission power plants based on RES with a capacity of 440 MW in 2020–2022, 460 MW in 2023–2025, and 600 MW in 2026–2030 (Ministry of Energy, 2020b). The government’s “green energy zone” plan for reclaimed territories in Karabakh include the development of green agriculture, construction of smart cities and the rehabilitation of large areas of forests (Azerbaijan COP26 Statement, 2021).

While the NDC outlines mitigation measures including, among others, the “development of legislative acts and regulatory documents,” there is no comprehensive national climate action plan or strategy outlining concrete steps to achieve the specified quantitative targets, neither the NDC targets seem to be mandatory (IEA., 2021). Azerbaijan has not adopted a net-zero target and associated timeline to meet it.

Legal and Regulatory Framework

This section outlines some of the key legal acts governing renewable energy development in Azerbaijan. An important first step was the adoption of the State Program on the Use of Alternative and Renewable Energy Sources in the Republic of Azerbaijan approved by Presidential Order No. 462, dated 21 October 2004. In 2011, Presidential Decree No. 1958 “Concerning the Development of the State Strategy for the Use of Alternative and Renewable Energy Sources in the Republic of Azerbaijan for 2012–2020” was approved by the president with the aim to produce the “State Strategy on the Use of Alternative and Renewable Energy for the 2012–2020 period” (Nasibov, 2021). In 2016, President Ilham Aliyev signed a decree to approve “Strategic Road Maps for the National Economy and Main Economic Sectors”, which outlined the short-, medium-, and long-term goals for the development of the economy and eleven key sectors including the priorities for the development of the renewable energy sector (Farajullayeva, 2019).

Until spring 2021, Azerbaijan did not have separate laws on renewable energy or energy efficiency (Bayramov, 2021; IRENA, 2019b). Following Presidential Decree No. 1209 of 29 May 2019 “On the Acceleration of the Reforms in the Energy Sector of the Republic of Azerbaijan,” the development of the draft law on “Use of Renewable Energy Sources in Power Generation” was initiated (IRENA, 2019a). The law was finally approved in 2021.

Azerbaijan is still developing a feed-in tariffs [FIT] framework viewed as a key policy tool at the initial stages of RE development. It lags behind on the introduction of auctions for RES procurement. Auctions are introduced as RE market matures to allow for the procurement of RES at market-based prices (IRENA, 2019b).

Moreover, Azerbaijan lacks a specific regulatory framework for the development of RES except for purchase tariffs for RE-generated electricity (Energy Charter, 2020). Much of activity in developing RE-related legislative and regulatory framework is carried out in cooperation with donor organizations: with EBRD on implementation of RE auctions and with the Asian Development Bank (ADB) on the construction of the first floating solar photovoltaic (PV) plant (Energy Charter, 2020).

The Presidential Decree No. 182 of 2009 established the State Agency on Alternative and Renewable Energy Sources (SAARES) as part of the Ministry for Industry and Energy. The Agency commenced operating in 2010 (IEA, 2021). In 2012, SAARES was abolished, and the State Company on Alternative and Renewable Energy Sources was established on its basis. The status of the Agency was altered several times. In September 2020, the Decree No. 1159 of President of Azerbaijan established the Azerbaijan Renewable Energy Agency under the Ministry of Energy, and the Charter of the Agency was approved. The Agency is in charge of “the arrangement and regulation of activities in the field of renewable energy sources and their efficient use in Azerbaijan and is involved in the implementation of state policy” (Ministry of Energy of Azerbaijan, n.d.).

Analysis and Policy Implications

While the legislative mechanism provides a policy and legislative framework for RE development, it is uncertain whether the inauguration of the relevant framework will be enough to meet the ambitious climate mitigation and renewable energy transition targets the government set out to achieve. The existing system of governing RE is excessively hierarchical and centralized with the state playing a leading role (Ahmadov, 2021). Ideally, the state should set the rules of the game and monitor compliance with those rules without interfering in the game itself or trying to influence the outcome. Best-practices in RE development shows that a successful decentralized RES model is predicated on the existence of small private producers operating in various segments of the RE market.

The Azerbaijani energy sector is dominated by a few vertically integrated state-owned monopolies, notably Azerenerji and Azerishiq. State control of energy generation, distribution and delivery is seen as inimical to the establishment of favorable business environment for the deployment of RES. Most investments in RES in Azerbaijan have to date been dominated by the state and international donors (Aydin, 2020). Recent renewable contracts with Masdar and ACWA Power reflect this dominant approach to renewable support schemes in Azerbaijan in which state/public investment plays a key role and attracts FDI from Gulf-based companies to finance renewable energy production. Despite recent changes, state-owned enterprises (SOEs) are still omnipotent with vested interest in the existing fossil fuel-based system to persist, and weak market liberalization makes Azerbaijan’s power sector less attractive to foreign investment. Unless they manage to adapt, the SOEs with high stakes in the oil sector stand to lose from a future shift to low-carbon sources.

With an overall score of 47 (out of 100), Azerbaijan demonstrated a relatively weak performance on the Resource Governance Index (RGI) published in 2017 due to weak oversight mechanisms over oil revenue expenditures and government restrictions on civil society organizations (NRGI, 2017).

Case Study: Kazakhstan

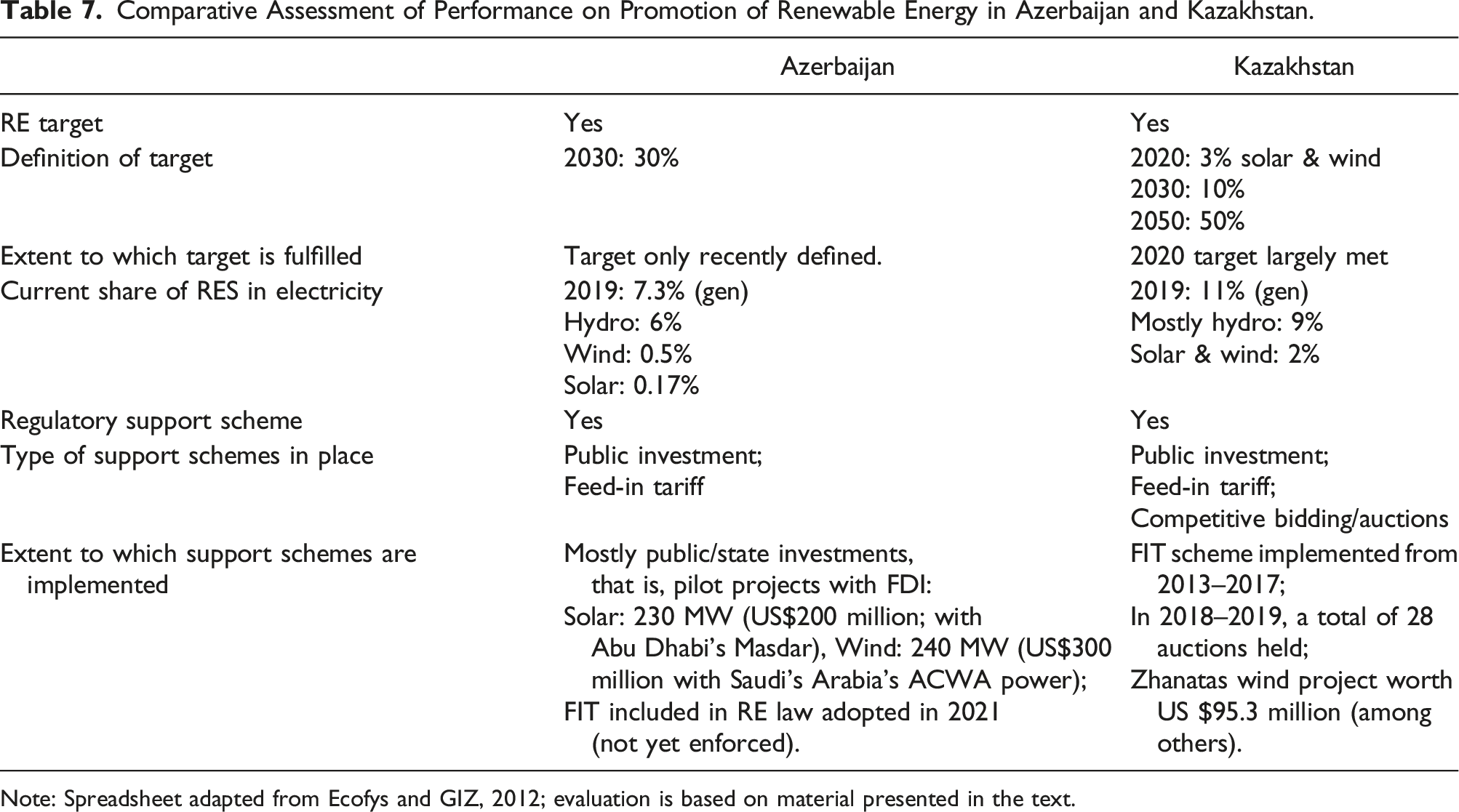

Kazakhstan is a large fossil fuel-producing country where oil and gas together account for 35% of GDP and 75% of total export (EY, 2021). Despite being a major oil and gas producer, Kazakhstan has made great strides in developing renewable projects. It has certainly been a leading country in adopting an appropriate legislative and policy framework with regards to the development of renewables among traditionally oil-producing countries in the former Soviet space. It was among the first to adopt the auction scheme for the sale of renewables and 28 such auctions were held in the years 2018–2019.

The Kazakhstani authorities have set ambitious targets to increase the share of solar and wind energy in total electricity to 3% by 2020, 10% by 2030, and 50% by 2050. The government has managed to meet the 3% target, and work is under way to meet the other targets too.

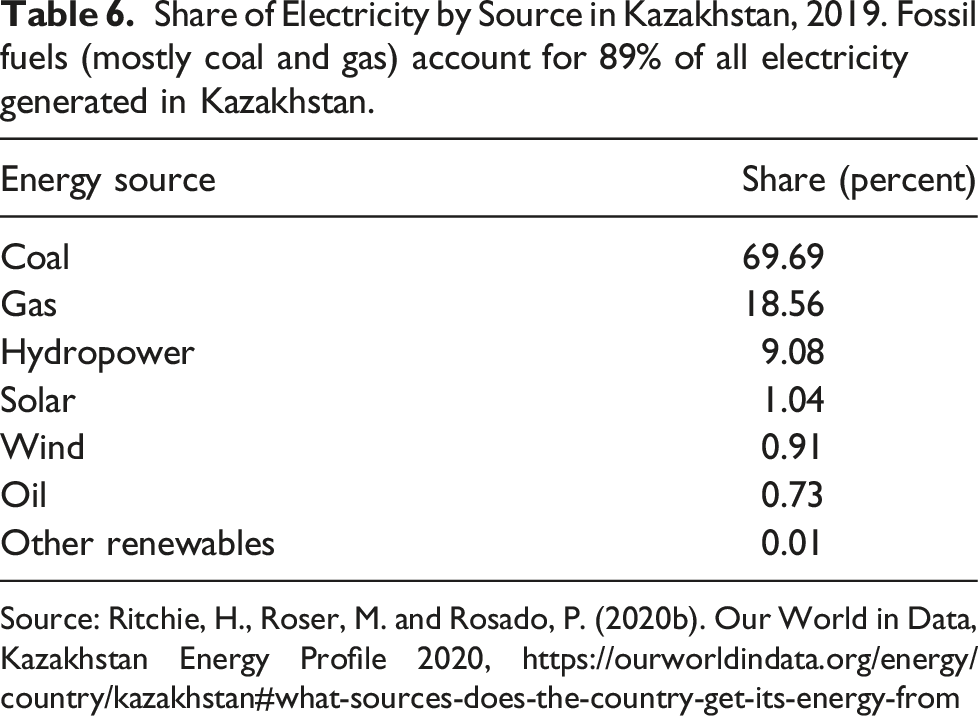

Despite its elaborate policy and legislative framework, however, the deployment of renewables has been slow (Mouraviev, 2021), and some experts doubt that RE policies are implemented effectively enough to meet the 2030 and 2050 targets. Fossil fuels (mostly coal and natural gas) still account for some 89% of all electricity generated in Kazakhstan.

There are a number of shortcomings in the existing RES legislative and policy framework in Kazakhstan. First, one area of improvement is a lack of clear rules governing the process of acquiring and getting access to land for renewable energy projects (Karatayev et al., 2021).

Second, the policy instability reflected in frequent changes in the RE policy framework and oversight institutions introduces an element of unpredictability in the policymaking environment. Such policy instability and a lag between the adoption and implementation of renewable policies are linked with increased level of risk (or its perception) for foreign companies willing to invest in Kazakhstan’s renewables sector (Laldjebaev et al., 2021).

Finally, Kazakhstan’s reputation for low accountability, weak rule of law and high perception of corruption makes its energy market less attractive for potential foreign investors and increases the risks of investment. This ultimately delays the expansion of renewables and can slow down the speed of RE development, which might ultimately jeopardize the government’s plans to meet said RE and climate change targets (Karatayev and Clarke, 2016). Unless the government improves transparency and accountability including by closer engagement with civil society, current polices alone are likely to be insufficient to lead to a more extensive adoption and utilization of renewables.

Background

Kazakhstan is a major producer and exporter of fossil fuels (oil, natural gas, and coal). It is the world’s 9th largest producer of coal, the 17th producer of crude oil, and 24th for natural gas (IEA, 2020). The country’s total oil reserves are estimated at 30 billion barrels, and it holds 2.3 trillion m3 in proven gas reserves (BP, 2021).

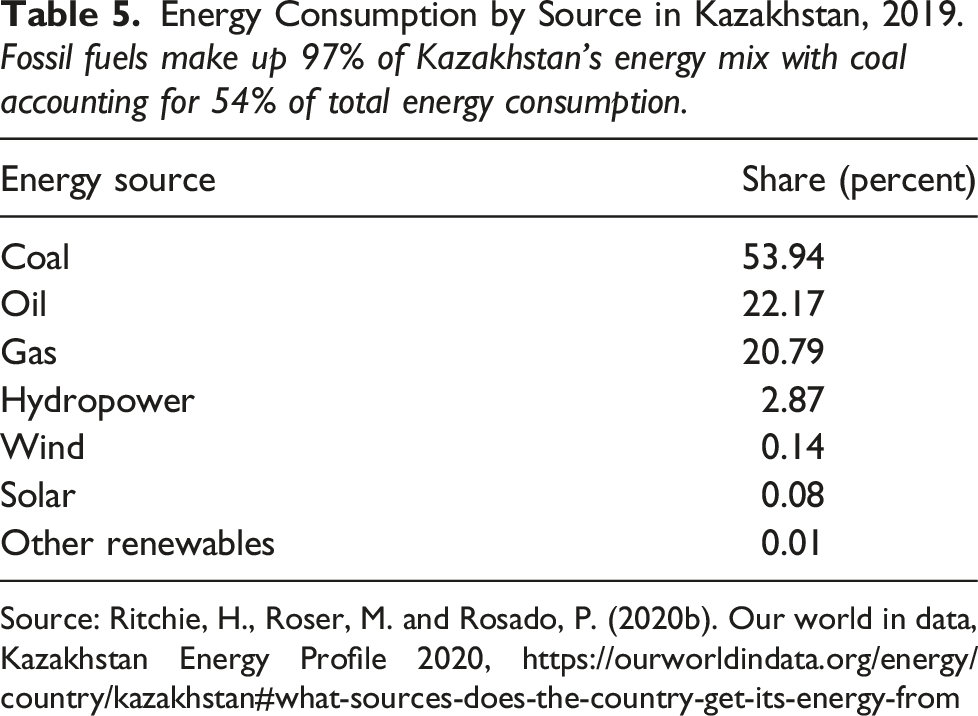

Energy Consumption by Source in Kazakhstan, 2019. Fossil fuels make up 97% of Kazakhstan’s energy mix with coal accounting for 54% of total energy consumption.

Source: Ritchie, H., Roser, M. and Rosado, P. (2020b). Our world in data, Kazakhstan Energy Profile 2020, https://ourworldindata.org/energy/country/kazakhstan#what-sources-does-the-country-get-its-energy-from

Share of Electricity by Source in Kazakhstan, 2019. Fossil fuels (mostly coal and gas) account for 89% of all electricity generated in Kazakhstan.

Source: Ritchie, H., Roser, M. and Rosado, P. (2020b). Our World in Data, Kazakhstan Energy Profile 2020, https://ourworldindata.org/energy/country/kazakhstan#what-sources-does-the-country-get-its-energy-from

In the 1990s, Kazakhstan implemented economic liberalization reform to attract Western investors into Kazakhstan’s oil and mineral sectors. As a result, Kazakhstan privatized its oil and gas sector by selling state-owned enterprises to foreign investors (Luong and Weinthal, 2001) and was “considerably more aggressive in its implementation of the privatization programme than its counterparts in Azerbaijan and Kyrgyzstan” (Ahmadov, 2011, 123).

Renewable Energy Targets

Under the Kyoto Protocol, Kazakhstan has committed voluntarily to reduce carbon dioxide emissions. Kazakhstan’s commitment under the Paris Agreement—which it ratified in 2016—targets a 15–25% reduction in greenhouse gas (GHG) emissions by 2030 compared to the 1990 level (Kazakhstan NDC, 2016).

In 2013, Kazakhstan adopted the “Green Economy Concept” which sets renewable and low-carbon energy (electricity) generation targets for solar and wind at 3% by 2020, 10% by 2030, and 50% by 2050 (ADB, 2020, Kazakhstan, 2013). The authorities announced in May 2021 that the 3% target had been met in 2020, and President Tokayev instructed the government to increase the share of renewables to 15% by 2030 (Satubaldina, 2021). While this official renewable energy target is supported by the government’s action plan, it remains legally non-binding (World Bank RISE, 2020).

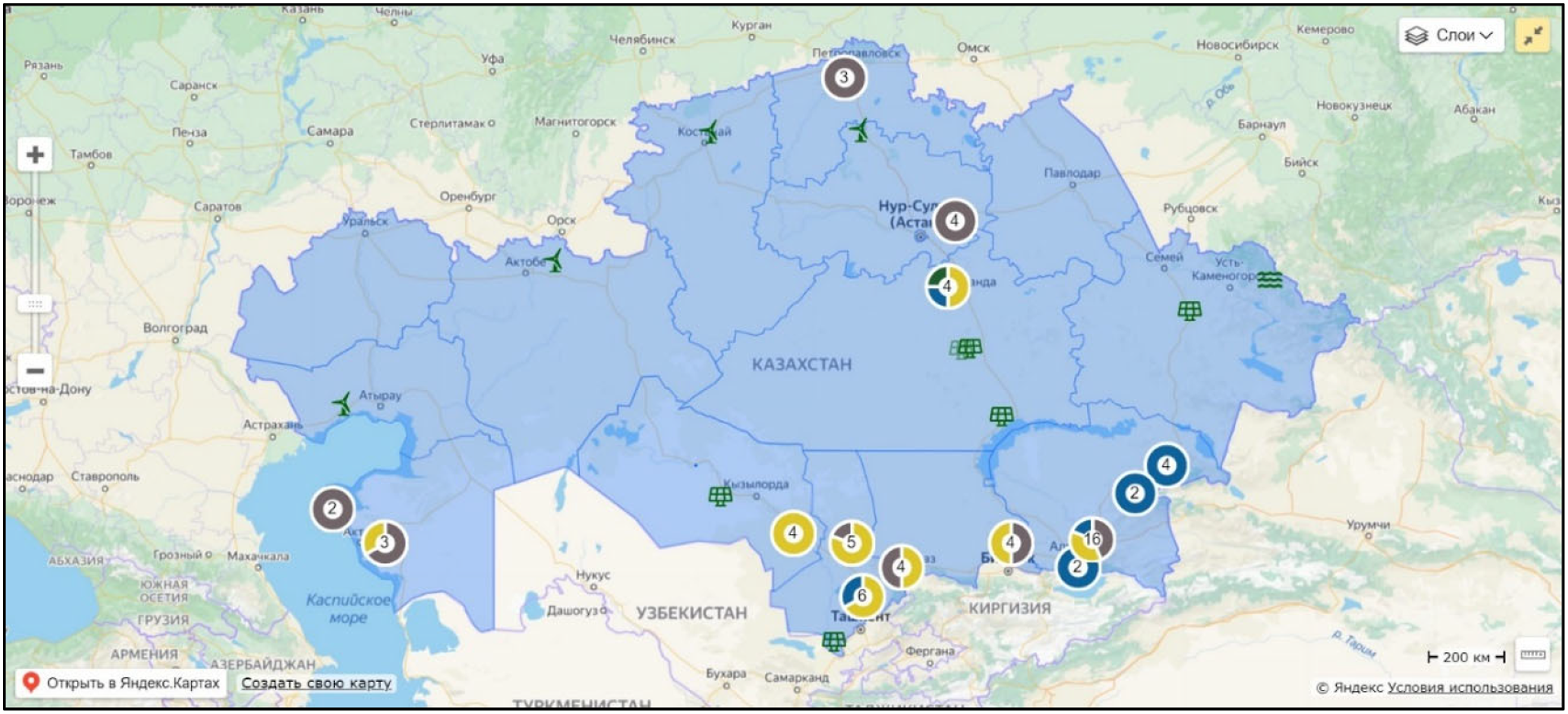

As of 2020, Kazakhstan launched 19 new RE projects worth $1.1 billion (Makszimov, 2020). In November 2020, the government approved the Zhanatas Wind Project worth US$95.3 million to support the construction of a new wind farm in southern Kazakhstan (EBRD., 2020). As of 2020, there was a total of 101 renewable energy facilities in Kazakhstan, including 37 solar power plants, 37 small hydropower plants, 22 wind power plants, and 5 biogas power plants (USAID, 2020a) (See Figure 1 for mapping of some of these projects) Distribution of renewable energy objects in Kazakhstan. Source: Financial settlement center of renewable energy of Kazakhstan, https://rfc.kz/en/vie/yamaps

Legal and Regulatory Framework

In 2013, the government adopted the “Nation Concept on Transition to a Green Economy up to 2050” setting the 50% renewables target by 2050 (PWC, 2021). According to the NDC, the share of RES, including large hydroelectric power plants, in domestic electricity demand should increase from 11% in 2020 to 32.7% in 2030. In 2013, the government adopted “Action Plan for the implementation of the Concept for the transition of the Republic of Kazakhstan to a green economy for 2013–2020” (Resolution of the Government of the Republic of Kazakhstan, 2013). A new strategy is currently being developed with regards to strategies of low-carbon development in Kazakhstan until 2050, which was scheduled for completion in June 2021 (Satubaldina, 2021).

The “Kazakhstan 2050” Development Strategy is a long-term basis for all state planning documents, including strategic plans of various ministries and government bodies. One of the strategic objectives of the state is the transition to a low-carbon economy and a reduction in GHG emissions to mitigate the impact of climate change. It also sets the RE target to cover “at least half of the country’s total energy consumption” by 2050 (Nazarbayev, 2012). In May 2021, the government announced its plan to achieve carbon neutrality (a net-zero target) by 2060 (PWC, 2021; Satubaldina, 2021).

In 2009, Kazakhstan adopted “Law on Support for the Use of Renewable Energy Sources” (Kazakhstan, 2009; Sospanova, 2019), which mandated a scheme for purchasing and sale of RE-generated electricity. In 2013, the government adopted a mechanism of feed-in tariffs (FIT), and in 2017, it switched to an auction mechanism (Dyusenov, 2019). Kazakhstan was the first country in the Central Asian region to introduce auctions for RE. The auction scheme was launched in 2018 as a transparent and inclusive mechanism to select RE projects and ensure market-based prices for electricity from RES (Sopsanova, 2019). From 2018 to 2019, a total of 28 auctions were organized with a total capacity of 1255 MW offered and a total capacity of 1070 MW contracted (USAID, 2020b).

The law also established a Financial Settlement Center for the Support of Renewable Energy Sources [FSC] as the main institution responsible for RE procurement by providing the platform for centralized purchase and sale of RES-generated electricity (USAID, 2020a). FSC, thus, acts as a centralized buyer of renewable energy (PWC, 2021). Sale of RE electricity is carried out through power purchase agreements (PPAs) at an auction rate in the national currency tenge and by providing guaranteed access to the power grids (Sopsanova, 2019). Kazakhstan was also one of the first among post-Soviet countries to set up a renewables reserve pool as a means of increasing investments into renewable energy facilities (Karatayev et al., 2021).

Analysis and Policy Implications

Kazakhstan is the most advanced among Central Asian countries in terms of the ambitiousness of its renewables program and its elaborate legislative and policy framework. The Kazakhstani authorities have implemented some of the most innovative policies in the renewables sector. It was the first country in the region to introduce and implement auction support policy for renewable energy sources aimed to set clear rules for selection of RE projects and to establish competitive RE prices (IEA, 2020; Laldjebaev et al., 2021). Although implementation of some of these policies has occasionally been slow, Kazakhstan has managed to increase its total installed renewable capacity of operating RES to 1846 MW (885 MW hydro, 533 MW solar, 427 MW wind, and 1 MW bio) in 2020 (PWC, 2021), which was enough to reach its 3% renewable energy target by the end of 2020.

While the transmission grid is owned and operated by state-owned company Kazakhstan Electricity Grid Operating Company (KEGOC) with associated inefficiencies in the transmission and distribution networks (Karatayev and Clarke, 2016), the electricity market is fairly competitive at the retail level, with some 45 companies operating in this sector (IEA, 2020).

Despite progress, however, there are some gaps in the policy framework, especially when it comes to the regulation and implementation of RES policies. One area of improvement is a lack of clear rules with regards to permission to acquire land for renewable energy projects (Karatayev, 2021).

On the other hand, frequent amendments in the RE legislation and periodic shifts in regulatory institutions give a sense of instable policy environment. Policy instability and implementation gaps also increase investment risks (Laldjebaev et al., 2021). Moreover, Kazakhstan’s low standing on international rankings on accountability, rule of law and control of corruption makes its domestic energy market risky for foreign investment needed to accelerate the growth of the renewables sector (Karatayev and Clarke, 2016). The January 2022 unrest, the crackdown on social protest and the ensuing elite power struggle all bode ill for Kazakhstan’s progress on renewable expansion.

With an overall score of 56 (out of 100), Kazakhstan had “the second best governed natural resource sector in Eurasia,” according to RGI published in 2017 (NRGI, 2017). While the country performed poorly on the indices of democratic accountability and control of corruption, Kazakhstan’s sovereign wealth fund (SFW) was managed better than its peers in the region of Eurasia.

Results and Discussion

Comparative Assessment of Performance on Promotion of Renewable Energy in Azerbaijan and Kazakhstan.

Note: Spreadsheet adapted from Ecofys and GIZ, 2012; evaluation is based on material presented in the text.

The study has demonstrated that despite some similarities in the initial conditions, Kazakhstan adopted a more elaborate regulatory framework than Azerbaijan did. Moreover, the introduction of renewables in Azerbaijan has been sluggish, and, in fact, the Azerbaijani government has delayed the adoption of relevant renewable legislation for over a decade. As a result, Kazakhstan has performed relatively better on advancing non-conventional RE targets: the share of non-hydro RES in electricity rose up to 3% in Kazakhstan, but stagnated at 1% in Azerbaijan (as of 2020).

However, the analysis also points to several obstacles that impede further progress in both countries.

First, in transitioning to clean energy sources, legacy fossil fuel infrastructures continue to pose challenges for both Azerbaijan and Kazakhstan where the medium-term challenge is to foster a partial transition to low-carbon sources in an effort to reduce GHG emissions and mitigate fiscal impacts of energy transitions undertaken by major European countries in their quest to become energy self-sufficient (Guliyev, 2020b).

Second, like in other oil-dependent countries, in Azerbaijan and Kazakhstan the bloated state is poised to play a leading role in transitions to renewables sources. Here the state dominates the upstream and downstream of the energy sector, and state-owned companies often enjoy a monopolistic position. The state channels a portion of oil revenues to renewable investments such as the installation of solar panels and wind turbines. However, excessive and continuous state intervention undermines the very cause it is trying to promote. State preponderance in energy supply and electricity generation is likely to hamper the expansion of renewables as government over-regulation produces market distortions discouraging capital investment.

We can see how these processes unfold to shape RES policies in Kazakhstan and Azerbaijan. In both countries, policy instability, inadequate governance mechanisms and company risk perceptions seem to have hindered the inflows of FDI into their respective RES sectors. In Azerbaijan, in particular, the statist approach has delayed the adoption of relevant legislation for many years. While Kazakhstan has been more pro-active in introducing relevant legislative and regulatory frameworks, there too certain gaps in governance arrangements such as lack of clarity with regards to investment procedures and bureaucratic discretion are often identified as obstacles to a more rapid RE expansion (Mouraviev, 2021).

Third, quality of governance poses risks for renewable expansion. In both Azerbaijan and Kazakhstan, weaker accountability and oversight mechanisms in policy implementation raise the risks of corruption.

Conclusion and Policy Implications

Azerbaijan and Kazakhstan have embraced the energy transition discourse, but how well have they performed so far? This article has provided an overview of the status of non-conventional RES, RE targets, and legal and regulatory frameworks adopted in two post-Soviet countries, Azerbaijan and Kazakhstan. In addition, the study identified a number of gaps in state support schemes in each case. The results can be summarized as follows.

Persistence of legacy fossil fuel infrastructure inherited from the Soviet era will likely continue. Examples include coal-fired thermal plants in Kazakhstan and natural gas-based electricity generating plants in Azerbaijan and Kazakhstan. Change is difficult due to a considerable sunk cost in the inherited infrastructure and fossil fuel-linked vested interests seeking to maintain the status quo.

The phasing out of conventional energy sources and their replacement with non-conventional renewables is going to be a prolonged process. As elsewhere in the world, a radical transition to non-conventional renewables is unlikely. Renewables will likely be introduced incrementally.

Explanatory Variables and Outcomes.

One crucial difference in explaining different outcomes is the relatively more liberalized energy sector in Kazakhstan. This reflects different policy choices made by two governments in the initial stages of economic development (Ahmadov, 2011). During the post-communist transitions in the 1990s, Azerbaijan retained state ownership of the energy sector while Kazakhstan pursued the policy of privatization to foreign companies. Kazakhstan’s more elaborate framework targeting private sector firms indicates a more market-focused orientation compared to Azerbaijan where the government embarked on renewable policy much later and employed a more centralized and state-centric model of RE deployment with involvement of Gulf FDI.

Footnotes

Acknowledgments

The author wishes to thank Ingilab Ahmadov, Maria Lobacheva, Andrei V. Belyi, Marat Karatayev as well as two anonymous reviewers of this Journal for their helpful inputs. The usual disclaimer applies.

This research was conducted as part of the project titled “Monitoring Energy Transitions in Eurasia (Azerbaijan, Kazakhstan, Kyrgyzstan, and Ukraine): Analysis and Policy Implications” supported by Publish What You Pay (PWYP). Financial support from PWYP is gratefully acknowledged.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.