Abstract

Travis Bradford explores different policies which have proven to be successful in stimulating the development and deployment of renewable energy technologies, in particular photovoltaic (PV) electricity. Case studies from Asia, Europe and the US are compared and analysed in order to demonstrate the positive aspects of different programmes and policies used to successfully adopt and distribute PV electricity. Market-responsive programmes, renewable portfolio standards and municipal loan programmes show the best results overall, and thus future policies should be based on these strategies.

The world is rapidly moving to adopt smaller, more local sources of energy generation. From solar energy to biomass and biofuel to small geothermal and wind systems, energy users are increasingly attempting to harness local resources to provide them with vital energy in a cost-effective manner. Governments around the world want to accelerate this transition for many, and sometimes conflicting, reasons. Policymakers are looking to maximise a number of variables simultaneously in their pursuit of a good renewable energy policy, and different stakeholders may have different objectives for the intended outcomes of optimal policy.

The Prometheus Institute has recently completed a year-long study on what defines good policy for renewable energy deployment. The idea that motivated this study involved the existence and design of an optimal policy for building robust markets for distributed renewable energy solutions, specifically energy technologies that can be adopted at the point-of-use by energy users (as opposed to energy utilities) and that are carbon free and renewable.

While many technologies are being deployed in a distributed manner, no technology has had such broad penetration and support around the world as direct electricity generation from the sun, or photovoltaic (PV) electricity. From Japan and Germany to Spain and the United States, PV electricity has seen tremendous growth, averaging 25% growth for the last 25 years. Industry growth has accelerated in the last decade to over 40% annually, due mostly to the aggressive policies of Japan, Germany and Spain, as well as a few of the states in the United States, including California, New Jersey and Hawaii.

Though each of these jurisdictions has been successful in deploying distributed PV electricity, no two have achieved it in exactly the same way or within exactly the same policy framework. Conversely, other countries have tried variants of these strategies and have failed to stimulate similar growth. Most importantly, the policies that have led to rapid market growth over the last decade in Europe have proven to be both expensive and unable to respond to changing market conditions. Newer programmes that address these issues–-and as such appeal to a wider audience of stakeholders–-have arisen at both the national and state level in the United States. Lessons can be learned from studying these programmes.

What has worked?

To begin to understand the nuances among programmes, it is necessary to first identify and categorise various types of policies that have been successful in accelerating the deployment of distributed generation systems. In our study, we have provided case studies of leading policies in various countries (in Asia and Europe) and states (in the US) that have been on the forefront of solar manufacturing and adoption for distributed generation.

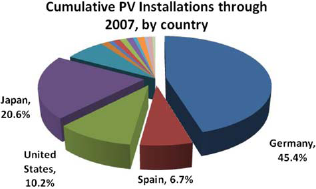

By including the policies–-past, present and proposed–-of Japan, Germany, Spain and various US states, policy regimes covering over 82% of distributed PV ever installed (Fig. 1), we have a survey comprehensive enough to make some assessments and generalisations about policies that were effective in stimulating the development of the global PV industry. While it may be telling that 13 policy programmes have driven so much of the global market, it is the similarities and differences in design that are most revealing.

Cumulative PV installations globally through 2007, by country

By developing the taxonomy of policies, which we intend to evaluate, this paper finds that each of the policies fit loosely into one of four categories: (1) market enablers such as net metering of electricity and interconnection standards for physical integration; (2) those that reduced upfront costs of new systems; (3) those that paid for the renewable energy output from systems installed; or (4) innovative financing options to bring down the cost of financial capital used to spread the system costs over their useful life.

Our framework also included an analysis of the stakeholders involved. The difficulty with the stakeholder analysis is that the views of typical stakeholders–-including companies, consumers, policymakers, utilities, etc.–-do not easily break down into categories. It is easy to construct a scenario where any of these stakeholders might be conflicted–-for example, a company may want to see both fast and stable market growth, which are likely to be in direct tension.

With our taxonomy and stakeholder assessment in mind, we defined the policy objectives that should be the target of each policy. There are approximately ten criteria (dimensions for measuring policy ‘desirability’) that are broken up among the three ‘archetypal’ stakeholder groups, including the following:

A strict growth advocate might include either an environmentalist or energy security person who would be most concerned about how much displacement of traditional energy with renewable energy there is, how quickly the policy decreases the time-to-market for deployments, and whether the policy increases political buy-in or the likelihood of passing the legislation. Essentially, this is a group that favours more and faster deployment, with less concern about the near-term economic impact–-or perhaps consists of those who see the cost of slow growth to outweigh even a high cost of acceleration.

A marginalist policymaker is more concerned about the social impact of change, including the degree of local job creation, the level of improvement of deployment economics or lessening the amount of public funding spent on incentive programmes. While probably not philosophically against renewable energy, marginalist policymakers see clean energy goals as one of many competing policy concerns that must be traded off to get political buy-in; the limited resources available must be used to best effect, even if such an approach might delay industry growth. This is a preference for low-impact growth over any growth.

An economist or industry purist would be most concerned about the degree to which a given policy leads to long-term, local sustainable markets for these technologies, increasing overall confidence through development of stable markets, lessening the amount of distortion caused by the policy and creating a robust and less centralised energy architecture to ease long-term adoption of these technologies. For these users, speed is not the appropriate proxy for market growth; instead their focus is on momentum and long-term reliable growth.

With any given policy, many of these policy objectives may be in tension with one another. We explore the degree to which these aims are divergent as well as places where they converge. Looking at how each of these approaches were created, which stakeholders supported and resisted these programmes, and how they fared once enacted is very instructive in informing the design of better programmes in the future.

Japan: an early success

Japanese electricity rates are some of the most expensive among International energy agency (IEA) countries for all consumer types. Due to the lack of domestic resources and the growth of energy demand, Japan has heavily relied on imported primary energy sources. The oil crisis of the 1970s had a tremendous impact on an economy that was highly dependent on oil from the Middle East (more than 70% of the primary energy in the early 1970s).

The Japanese Sunshine programme initially provided a 50% subsidy on the cost of installed grid-tied PV systems. The subsidy levels were set so that the net electricity cost to the customer was competitive with conventional electricity options. The subsidy was for PV modules, BOS and installation. The programme was open to participants from residential homes, housing complexes and collective applications. After achieving their price goals, the Japanese government rolled back the subsidy programme in 2003 and phased it out completely by 2005.

The intention of the Sunshine Program was to create a market where PV was the same price as the grid electricity that it displaced–-a situation referred to as ‘grid parity’. By 2004, the market was approaching this point of grid parity, and anticipated additional improvements in module price should have continued to make PV electricity more cost-effective.

What actually occurred was that module prices began to rise around the time of the end of the Sunshine Program and rose further through the middle of 2008, due to strong global PV demand created by the policy programmes in those countries that were also promoting PV. This led to a period of market shrinkage that is not likely to reverse until either global module ASPs come down substantially or additional policy programmes are established by the Japanese government.

Fortunately, both of these are forecast to occur soon. Spain's situation, described below, and global financial markets, which are making it marginally harder to obtain PV project financing, are causing demand issues, while normal supply expansion is bringing pricing back in line with historical trends. At the same time, the Fukuda vision announced in Japan in 2008 should help to support the cost of PV system installation by an additional 10%.

The lesson to be drawn is that programmes that support upfront costs must be responsive to market conditions–-particularly changes in the market price for components or systems–-or they will find that market conditions create perverse outcomes. Further, market-based programmes must plan carefully to avoid problems caused by the transition from a subsidised to an unsubsidised environment.

Germany's feed-in tariff raises the bar

In Europe, distributed renewable energy policy has been heavily geared towards domestic job creation, with targeted goals for renewable energy deployment as a secondary motivation. The feed-in tariff methodology favoured in Europe has been very successful in developing these markets, but at a high cost and with many distorting effects on the supply and price of the solutions.

The German Renewable Energy Act (EEG) law was established in 2000 and substantially revised in 2004. It was created to double the amount of renewable energy generated from 1997 to 2010, to a minimum of 12.5% of the total generation. The EEG's remuneration system is not based on average utility revenue per kWh (kilowatt hours) sold, but rather on a fixed, regressive feed-in tariff for renewable sources. Low-cost renewable energy producers are compensated at lower rates than higher-cost producers, providing strong incentives for the development and operation of renewable energy installations on lower-quality sites. Also, under the EEG, grid operators are obligated to purchase power from local producers; a nation-wide equalisation scheme has been implemented to reduce the cost differentials paid by grid operators in different parts of the country for the purchase of renewably generated electricity.

Since August 2004, the law has obliged electricity suppliers to purchase photovoltaic electricity at a predefined tariff. In 2006, grid-connected systems benefited from a feed-in tariff varying between 51.8 eurocents per kWh and 48.74 eurocents per kWh for a period of 20 years, but with a 5% per year price digression. A bonus of 5 eurocents per kWh is added for building facade-integrated systems.

The Act was considered effective because the costs for renewable energy are largely dependent on investment security. The structure of the EEG guarantees a particularly high investment security and credit interest rates, and risk mark-ups are low compared with other instruments. The costs for installing PV systems dropped by 25% between 1999 and 2004.

Although the EEG is credited with the solar boom of 2004-2008, critics such as the German Electricity Association (VDEW) complain that the EEG has the following flaws: (1) it is too expensive; (2) it contravenes market rules; (3) it leads to the additional need for regulation energy and the need for a vast extension of the grid; (4) the expansion of renewable energies allows only a few conventional power plants to be decommissioned; and (5) it does not fit into the European internal market from a legal point of view.

Spain booms then busts

Unlike the German feed-in tariff, the Spanish has no fixed price. It is calculated as a function of the mean price of electricity during the year in progress. For installations lower than 100 kW (kilowatts), the feed-in tariff corresponds to 5.75 times the mean price of electricity for 25 years (equivalent to 44.04 eurocents per kWh) and 4.6 times the mean reference price of electricity for the rest of installation lifetime. For installations greater than 100 kWp (kilowatt peak), the tariff changes to 3 times the mean reference price of electricity for the first 25 years (equivalent to 22.98 eurocents per kWh) and to 2.4 times the mean reference price of electricity for the rest of the installation life.

The Institute for Energy Diversification and Conservation, newly installed capacity in Spain amounted to 60.5 megawatt peak (MWp), bringing the total installed capacity to 118.1 MWp (including 15.2 MWp off grid) through the end of 2006. In 2007 and 2008, Spanish demand for PV electricity was off the charts, with nearly 2 GW installed in those 2 years, far higher than the original programme anticipated. The market's growth was over five times the expected cumulative market in just the first 2 years of a 5-year programme. What resulted was an expense rate for the programme of over 10 times the originally intended amount that occurred simultaneously with a national budget crisis. The government responded by establishing a lower feed-in tariff as well as a programme cap of 400 MWt per annum (with some additions for projects in the queue).

The net result is that all of the infrastructure that was so dearly paid for to create over one GW of annual capacity is now likely diminished in value. While the Spanish market may have scored well for growth, it failed abysmally at creating a stable, predictable regime, and has yet to find a pathway to a long-term unsubsidised market for distributed renewable energy.

The US uses a more market-oriented approach

The US policy environment, driven by various state initiatives, has been much more experimental. These include performance-based incentives (California), New Jersey Solar Renewable Energy Certificate Program and, most recently, activities to potentially finance these systems through tax-advantaged municipal bonds (Berkeley, California). These programmes are much harder to craft and have an increased risk of unintended consequences, but could offer important new models for market-enabling programmes.

The Energy Policy Act of 2005 was the first comprehensive bill to be passed on energy in over a decade, since the Energy Policy Act (EPACT) of 1992.

Despite criticism of the overall law, the 30% solar Investment Tax Credit (ITC) that was originally started for a 2-year term through this law has been instrumental in the tremendous growth of the US solar market. As of October 2008, this programme was extended through to the end of 2016, caps on size were lifted and restrictions on utilities taking the ITC were removed. Today, it is expected to have a sizeable impact on the growth of the US PV market.

States are supplementing the system costs as well. Most aggressively, the California Solar Initiative is aimed at transforming the solar market in order to make solar energy cost-competitive without incentives by 2017. The law also has the objective of providing 3,000 MWt of solar capacity by 2016. The California Public Utilities Commission recently created a 10-year, $3.2 billion programme to provide homeowners and businesses with rebates for installing grid-connected PV electricity. The programme is managed by the Pacific Gas and Electric Company (PG&E), Southern California Edison (SCE) and the California Center for Sustainable Energy.

The rebates are expected to decrease over time as solar energy becomes more cost-effective, but the 2007 levels for the rebates are below what was anticipated. Systems that are 50 kW and larger are offered performance based initiatives (PBIs) that will be paid monthly, based on the actual amount of energy produced for a period of 5 years. Residential and small commercial projects under the 50 kW threshold can also choose to opt for the PBI rather than the upfront expected performance-based buy down approach. However, all installations of 50 kW or larger must take the PBI.

As a result of the the California Solar Initiative Program, California is the dominant PV market in the US and the fifth-largest market for PV electricity in the world. More than 120,000 systems have been installed to date on homes and small businesses connected to the electric grid under the California Energy Commission's rebate programme.

Beyond the state and national levels, some of the most exciting activities in the US are occurring at the local and municipal levels. One example is Berkeley FIRST, a programme in development by the City of Berkeley. It is being designed to allow property owners (residential and commercial) to install electric and thermal solar systems and make energy efficiency improvements to their buildings and pay for the cost over 20 years through an annual special tax on their property tax bills. The City would provide the funding for the project from a bond or loan fund that it repays through assessments on participating property owners’ tax bills for 20 years.

The programme is designed to address many of the financial hurdles that are dissuading some people from undertaking major energy projects. First, there would be little upfront cost to the property owner. Second, the upfront capital costs would be repaid through a voluntary tax on the property, thereby avoiding any direct effect on the property owner's credit. Third, the total cost of the solar energy system and energy improvements should be comparable to financing through a traditional equity line or mortgage refinancing, because the well-secured bond will provide lower interest rates than are commercially available. Fourth, the obligation to pay the tax transfers with the property. Therefore, if you sell your property prior to the end of the 20-year repayment period, the next owner takes over repayment as part of the property tax bill. The city claims it is the first in the nation to approve such a programme, but the idea for such financing is not new.

After the announcement of the Berkeley programme, California enacted a law in July 2008 that allows cities and counties to make low-interest loans to homeowners and businesses to install solar panels, high-efficiency air conditioners and other energy-saving improvements. Other cities throughout the US are exploring similar programmes, for example, a recent ballot initiative passed in Boulder, Colorado. These types of programmes are slated to grow quickly in the next few years in terms of sophistication and rates of adoption.

Towards an optimal design?

One of the most robust conclusions of our recent study is that the countries that have stimulated the most growth in distributed energy generation over time have been those that have chosen a portfolio approach. One of the first integrated programmes in the world was the Japanese Sunshine programme, which began in 1994. Japan achieved market success and rapid deployment through a combination of system rebates (reducing upfront capital costs), net-metering (market enabler), project loan facility (financing options) and research-and-development programmes. Measured by originality and market growth metrics, this programme was a wild success.

Subsequently, Germany deployed a combination of feed-in tariff (paying for output), interconnection (market enabler) and loan programmes (financing option) in their 2004 revision to the EEG. While none of these was ideal, the combination created a fast-growing market with over 45% of cumulative global PV installations to date.

While it is useful to understand how the combination of various programmes unlocked growth in some markets, most analyses of the ‘success’ of policy programmes still focus on the volume deployed over a discrete time period as the only metric. However, defining success is still a matter of perspective, and the objectives of different stakeholders lead them to interpret ‘success’ differently.

Rather than normatively deciding which metric of success is the correct one, it is important to make sure that each of the basket of objectives represented by our three archetypical perspectives on objectives are being met. If not, a programme runs the risk of being undermined or limited in some way. Using these broader metrics, it is not yet possible to determine the success of the current ‘leading’ programmes, as three important outcomes of current programmes are still not known, including:

eventual market size and robustness;

eventual total cost of programme–-or net cost versus displaced sources;

future possibility of political backlash by ratepayers or policymakers.

In fact, the most recent evidence of the Japanese programme is that since its end in 2005, the market has shrunk and has not shown the ability to stand on its own–-quite possibly a failure from the perspective of establishing robust, unsubsidised markets beyond the programme horizon. Spain's programme turned out to be wildly expensive and had to be reduced by as much as 80% in 2009 versus 2008 or else risk severe financial implications for the government–-a very damaging outcome for the domestic PV industry.

Today's risk of unintended consequences in deploying more distributed generation is that programmes that are too focused on short-term growth–-weighted too much towards the objectives of ‘strict growth advocates’–-may grow too fast by being initially very expensive and may yet limit market growth over a longer time horizon when the inevitable backlash occurs. The recent experience in Spain with a boom-bust cycle and the institution of a market cap in 2009 and beyond is an example of this outcome. A global market relying on Germany for continued growth is highly exposed to a similar outcome there.

Given the experience of Japan and Spain, the question is how long the German market can remain the market of last resort. Already in 2007, a coalition of politicians and electricity ratepayer advocates were calling for a one-time 30% drop in the feed-in tariff rate in Germany. With the German market already using PV electricity to provide more than 100% of its peak load need and the surcharge to pay for the programme expected to climb to over 20% of the retail electricity bill of every German household and business, the answer is likely to be ‘not much longer’.

Beyond three or four GW of new PV installations per year, Germany is going to find it hard to justify the expense of new installations. If market prices for modules come down according to the forecasts above, the wealth transfer from electricity purchases to solar owners will be extreme, and the perceived value to the German clean energy position will be diminished. Germany will only be able to respond with either a physical cap on volume of the programme (as Spain did), a substantial change in the feed-in tariff rate (risky if under- or overpriced) or a change in the design of the programme (very disruptive to the world's largest market). None of these will benefit German installers or global component manufacturers.

An alternative strategy–-one being pursued in the US at both the federal and state levels–-includes more use of market enablers and innovative financing programmes, which are both the cheapest and broadest way to stimulate growth, though perhaps not the fastest. The advantage is that compromising in order to meet mutual objectives may end up creating more robust and larger markets for distributed renewable energy over time, with less likelihood of a backlash from competing stakeholder preferences.

In conclusion, while the last generation of policies in Japan, Germany and Spain helped to create a multi-billion-dollar global PV market, the next generation of policies cannot replicate yesterday's structures. These have proven to be both too expensive and to leave unfulfilled stakeholders who may be very interested in seeing more PV electricity but are not willing to ignore the total programme costs or long-term market development considerations. Market-responsive programmes such as tax credits, renewable portfolio standards and municipal loan programmes (i.e., Berkeley First) that are favoured in the US may have been initially slower to develop the market, but over the next few years should show that they are better suited to building long-term, cost-effective and widely supported markets where they are adopted.

Footnotes