Abstract

Due to the current economic downturn, Singapore has experienced one of its most severe recessions since independence. The financial crisis, which caused a fall in prices at most of the world's leading stock exchanges and a sharp decline in industrial production, has also had a negative impact on the city-state's export-dependent economy. The analysis outlines the economic downturn and the decline of Singapore's export economy since the beginning of the crisis in late 2008. Central to the analysis are questions regarding the social consequences of the current economic crisis and the amount of losses Singapore's state-owned holding companies, Temasek and GIC, experienced when some of the world's biggest investment banks, such as Merrill Lynch, went into bankruptcy.

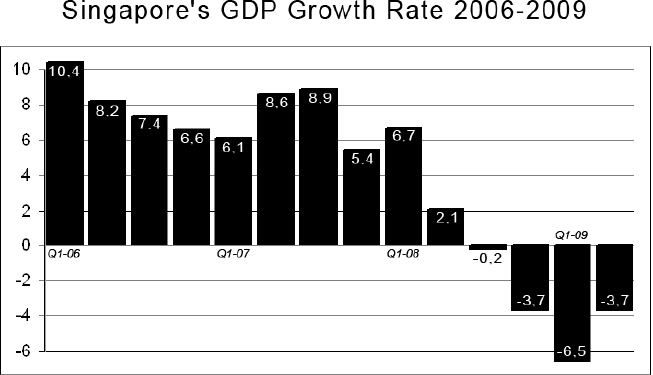

The Statistical Picture of the Recession

In July, the Singapore government raised its full-year economic forecast for the year 2009 as the economy showed sharp growth in the April-June period. Following four consecutive quarters of contraction, Singapore's gross domestic product (GDP) grew by an annualised 20.4 per cent in the second quarter. This may mark the end of the city-state's worst recession in more than four decades.

Even with this sharp growth in the second quarter, however, Singapore's economy is still in a state of turmoil as a result of the economic crisis that followed the end of investment bank Lehman Brothers in September last year. After more than a year in sharp recession, the latest growth may just be a first sign of economic recovery while large parts of the city-state's economy are struggling with the consequences of the worldwide financial crisis. And while the economy grew by 20.4 per cent in the second quarter compared with the previous quarter, this still amounts to a 3.7 per cent contraction when compared with the year before.

It was in November last year when the Monetary Authority of Singapore (MAS), which acts as the city-state's central bank, gave initial warnings that the economy would continue to weaken after it slid into economic turmoil in the third quarter of 2008. The latest data had just shown that the economy shrank 6.8 per cent compared with the second quarter, which had already contracted by 5.3 per cent (AP 2008a). Hit by the global downturn, the island's export-dependent economy went into a recession, hurting corporate profits and sparking job cuts in the following months.

It was in 2001 that Singapore's economy last went into a recession, a consequence of economic restructuring in the region that followed the Asian crisis in the late 1990s. But after four quarters of consecutive contraction between the second quarter of 2001 and the first quarter of 2002, the economy recovered and showed strong growth again. Exhibiting constantly high growth rates between 2004 and 2007, Singapore was one of the strongest economies in the region. But with it being deeply connected to the world market and highly dependent on exports to Japan, the US and Europe, the latest economic crisis had immediate consequences for the city-state's economy. The global economic downturn not only dried up the demand for Singapore's exports, but it also hurt the financial sector – a sector that had become increasingly important over the previous few years when the government began to alter the city-state's economic structure. As a consequence of the global economic downturn, manufacturing, which is still the backbone of the economy, nearly slid by 10 per cent in the third quarter of 2008, while construction fell by the same rate and even services plunged by 22 per cent compared with the previous quarter (AP 2008b).

The fourth quarter of 2008 saw an even more serious decline in economic growth when the nation's GDP fell by 12.5 per cent, which was the biggest drop since the Ministry of Trade began to keep records in 1976. Based on the contraction in the second quarter, the government had estimated a downturn of less than nine per cent for the fourth quarter and was alarmed by the latest economic data. In the wake of the crisis, the government had to downgrade its previous growth estimates for 2009, which ranged between a contraction of one per cent and an expansion of nearly two per cent. This forecast had to be adjusted to a 2 per cent contraction. Forecasting an annual contraction in this range, the city-state's economy was felt to be in the worst shape it had been in since 2001 when GDP fell by 2.4 per cent (AFP 2009a).

Early in 2009, the economic picture grew even bleaker when statistics revealed that in the previous quarter the economy had shrunk more than it had ever done over the previous 30 years. Singapore's economy had contracted for three straight quarters by then and the city-state slid into the severest recession ever along with Japan, Hong Kong and other important economies in the region. The manufacturing sector was still undergoing contraction and important manufacturers began to cut jobs as exports continued to decrease. New adjustments to the growth estimates now expected the economy to shrink between two and five per cent in 2009, as Prime Minister Lee Hsien Loong said in an interview (Bloomberg News 2009).

The latest news about a two-digit growth rate in the last quarter is the first sign of recovery in view of Singapore's economy having been in a bad shape for more than a year. The most dramatic economic downturn was witnessed in the first three months of 2009 when the country's gross domestic product plunged about 20 per cent compared with the previous quarter and fell 11.5 per cent compared with the year before. In the face of the worst economic performance for nearly 40 years, the government had to downgrade their economic forecast to a contraction of between six and nine per cent for 2009 (WSJ 2009a). This is much higher than in other Southeast Asian countries. Neighbouring Malaysia, like Thailand, is also likely to remain under pressure due to the collapse in global trade and expects its GDP to decline, although at a lower rate than in Singapore.

Singapore's GDP Growth Rate, 2006-2009

In a poll conducted by news agency Reuters in late 2008, analysts forecast that Singapore would be the worst-performing economy in Asia in 2009 as it was likely to remain entrenched in one of the severest recessions in the city-state's history. Singapore was (and still is) facing a rapid deterioration of its economic environment due to its openness to external trade. Its export-to-GDP ratio is more than 180 per cent, compared with an Asian average of 60 to 70 per cent (Reuters News 2008). This makes the Singaporean economy highly vulnerable to external shocks such as the current economic crisis. The manufacturing sector was therefore expected to be hit harder by the economic downturn and job losses in the sector were expected to rise sharply as a result.

Decreasing Exports and a Rise in Retrenchments

As a first reaction to the global economic downturn exports plunged in the second half of 2008. The total amount of exports fell 15 per cent in October last year as demand from the USA, Western Europe, and Japan began to decrease. Electronics, which accounted for a third of all manufacturing, fell by 14 per cent, while pharmaceuticals, which made up 22 per cent of industrial production, dropped by 31 per cent. Overall, industrial production was reported to have dropped by 13 per cent (AP 2008c).

In January 2009, Singapore's non-oil exports, which accounted for two thirds of the city-state's gross domestic product, plunged another 35 per cent as global demand continued to collapse. In the preceding months, manufacturing again fell by 10.7 per cent compared with the previous year and even services dropped a revised 1.3 per cent in the fourth quarter of 2008. It was only the construction sector that gained a revised 18.5 per cent due to large government spending (Bloomberg News 2009). Once again, the drop in exports was led by electronic products, which decreased by nearly two fifths compared with the situation a year earlier, and chemicals, which dropped 31 per cent. By then, exports had fallen for nine consecutive months as the main markets for Singapore's goods and services showed declining demand. Exports to Europe fell 13 per cent in December 2008, while sales to the US market dropped to half the amount they had reached a year before. Even the city-state's exports to neighbouring Malaysia fell by 40 per cent in that phase (AP 2009a).

In the first quarter of 2009, the situation was far from becoming any better as non-oil exports once again fell by 26 per cent. Manufacturing, which still accounted for a quarter of the city-state's economic output, slumped by 29 per cent compared to the first quarter of 2008. Due to Singapore's high export-dependency and the ongoing weakness of global demand for goods and services, the city-state's currency, the Singapore dollar, began to lose more than a tenth of its value against the US dollar, making it one of the worst-performing currencies in Asia in the current economic crisis (WSJ 2009a; Time 2009).

It was not until the second quarter of 2009 that export statistics faired slightly better when manufacturing fell by only 1.5 per cent compared with the previous year, a significant improvement over a revised 24.3 per cent decline in the first quarter of 2009. Services declined by 5.1 per cent, while the construction sector grew another 18.3 per cent, still profiting from the government's large economic recovery packages. The first positive development for months led many analysts to predict that the city-state's economy was likely to record positive growth rates again by the third or fourth quarter of the year. As open economies such as Singapore's suffer the most from a global economic downturn, they are likely to be the first to see high growth rates again when global markets start to recover and demand for their exports will grow again (FT 2009a).

All in all, the economy remained in a severe state of crisis when manufacturing output fell even more sharply than expected in June 2009, pulled down mainly by a deep contraction in the key electronics sector. Once again, the Economic Development Board (EDP), the city-state's key development institution, had to report that industrial production had sunk by 9.3 per cent compared with the previous year. As in the months before, it was mainly the electronics sector which showed the strongest contraction, with its output down an annual 20.4 per cent, while chemicals dropped 8.9 per cent, due mainly to slower growth in the biomedical sector. Biochemicals, a field which includes some of the world's most important drug producers, is highly volatile to economic crisis as pharmaceutical companies routinely close production facilities down in the event of sales decreasing (AFP 2009b).

Although the latest forecasts predict a slightly better economic performance in 2009 than previous analyses have done, Singapore's economy is shrinking this year and industrial and service output will decline further. Analysts expect manufacturing to decline by an overall 7.1 per cent in 2009, while financial services – one of the backbones of the city-state's economy – are expected to shrink by 3.0 per cent and wholesale and retail trade by 11.7 per cent. Although business in the third quarter is expected to shrink by 3.0 per cent, analysts see the economy returning to growth in the fourth quarter. But even with this positive development, the official rate is expected to jump to 3.8 per cent this year from 2.6 per cent in 2008, and many workers will face lower wages and longer working hours as their companies go on struggling with the global economic recession (AP 2009b).

When demand for goods and services declined sharply, Singapore's employers immediately hired fewer workers in a bid to cope with the initial phase of recession. While more than 71,000 new jobs had been created in the second quarter of 2008, the number of new positions dropped to less than 58,000 in the third quarter, as government statistics showed – the least number of new jobs created since the first quarter of 2007 (Bloomberg News 2008). Overall, some 2,000 workers had been made redundant in this initial phase of the current economic crisis, 1,500 of whom were from the manufacturing industry. It was the computer industry that was hit hardest by the economic downturn, and state-owned Chartered Semiconductor Manufacturing, one of the world's largest chip makers, had to ask its employees to work fewer hours as demand dropped and announced plans to cut wages by as much as 20 per cent.

The situation on the labour market became even worse in the fourth quarter of 2008 when around 8,100 workers were either laid off or faced retrenchments in the near future. This was nearly a 10 per cent increase compared to the first nine months of the year when some 7,400 workers had lost their jobs (Channel News Asia 2009). Statistics published by the Manpower Ministry in January showed that the unemployment rate had risen to 2.6 per cent in December 2008 from 1.7 per cent in December 2007. In the fourth quarter of 2008, the number of new jobs created sank to less than 27,000, about half those created in the previous quarter. Once again, it was the manufacturing sector that was hit hardest, shedding 6,200 jobs by the end of the year (AP 2009c).

While the second quarter of 2009 particularly showed signs of economic recovery, the labour market was still in a state of crisis in the first half of 2009. Singapore's service industries, still the most important sector for employment, had shrunk for three quarters in a row and exports had dropped for 14 consecutive months when the government predicted that another 18,600 jobs would be lost by July. And even the government's efforts to prevent job losses – especially by handing out cash to companies to reduce their wage costs – haven't helped to prevent the cuts in employment (Reuters 2009a).

Official statistics indicate an overall unemployment rate of 3.3 per cent at the end of the second quarter, but the number of people employed fell by nearly 13,000 between April and June, twice as many as in the first quarter of the year. The problems on the labour market can best be seen from developments at Seagate Technology, one the city-state's most important computer hard-drive makers. Forced to cut production costs by more than USD40 million per year, the company had only recently announced the closure of some of its manufacturing facilities in Singapore, where 2,000 workers had lost their jobs. Seagate, which employs a total of 8,000 workers in Singapore, is planning to close its hard-drive factory at Ang Mo Kio New Town and relocate production to Thailand, China or Malaysia to lower its production costs (Reuters 2009b). The company's drive to relocate its production facilities and therefore to cut jobs in Singapore is just one of an increasing number of examples of how the city-state's export-dependent economy is being hit by the current economic crisis as demand for goods and services decreases sharply in its main markets in the USA, Western Europe and Japan.

Negative Impacts on the City-State's Global Investment Strategies

Months before the outbreak of the current economic crisis, state-owned holdings in countries such as China, Russia or even Singapore were seen as a potential threat to the corporate sectors of Western economies. Due to the enormous wealth they had accumulated in the years before, these holdings became able to buy significant stakes in huge and important companies in the finance and banking sector as well as in sectors seen as strategically sensitive by the respective governments. The Singapore government manages two such state holdings, namely Temasek Holdings, which controls such important companies in its portfolio as Singapore Airlines, Neptune Orient Lines (NOL) and Chartered Semiconductor Manufacturing, and the Government of Singapore Investment Corporation (GIC), which manages the city-state's huge reserves.

While the investment strategies of the GIC, chaired and managed by former Prime Minister Lee Kuan Yew, are still kept from the public and parliament, Temasek's investment has sparked some public interest – especially among those in the financial sectors of Asian and Western countries. The company, chaired by Ho Ching, the wife of acting Prime Minister Lee Hsien Loon, controls some of Asia's best-known firms, and in October 2008 it reported a record profit of more than 18 billion Singapore dollars (some USD12 billion) in its financial year up to March. With a portfolio that it estimated to have increased in value to USD185 billion, it is listed among the largest sovereign wealth funds in the world by analysts at Citigroup Global Markets. 1

All figures as stated in AFP 2008.

In addition to banks in Indonesia and China, the holding started to buy stakes in leading financial institutions in Western Europe and the United States, a billion-dollar stake in US bank Merrill Lynch being one of the most important investments in the months ahead of the economic crisis. With the outbreak of the financial crisis in 2008, the Singapore wealth fund was beginning to show massive paper losses from its exposure to some of the world's most ailing banks. Since 2007, the holding had been building up multi-billion-dollar stakes in the once-mighty Merrill Lynch, which is now owned by Bank of America, as well as stakes in Barclays and Standard Chartered, both British banks. Even as first signs of serious problems in the global banking sector became apparent in the first half of 2008, Temasek continued to channel money into the financial services industry, which accounts for some 40 per cent of its huge portfolio.

With such a big amount of capital invested in the global financial sector, the holding had to face huge paper losses of up to USD2 billion when leading banking institutions around the world went into a severe crisis. Its stake in investment bank Merrill Lynch caused particularly huge losses. While the holding had bought the stakes for an average of USD23 a share, these immediately dropped to less than USD12 when the financial crisis started rocking the economy. Temasek had bought stakes in Merrill Lynch for about USD5 billion between December 2007 and the summer of 2008, but by early January their value had dropped to less than USD2.7 billion – a loss of nearly 45 per cent. 2 After crisis-ridden Merrill Lynch had been taken over by Bank of America in January 2009, Temasek sold its 3.8 per cent stake in the US-centric bank, thereby losing another USD1.3 billion. The loss attracted exceptionally fierce criticism from the usually muted pro-government local media as well as from investors and financial experts, pointing to the fact that the bank's shares had gained more than 70 per cent after the holding's exit. 3

The holding was able to sell some of its stakes in Merrill Lynch at low prices in the first and third quarters of 2008 and therefore generated a modest profit which helped to defray some of Temasek's losses up to that point. But in September that year, when Merrill Lynch shares plunged in concerns about the US banking sector, the holding's investment suffered again. See also FT 2009b.

Reuters News 2009a; AFP 2009c. Meanwhile, Bank of America reported huge losses for the third quarter of 2009 and its share dropped an impressive five per cent in value in mid-October.

Not only Temasek had to face huge losses, though; all of the city-state's hard-earned reserves, which are tied to global investments, have plunged by unprecedented amounts over the past year. The DBS Group, 4 part of the Temasek Holdings and one of Southeast Asia's biggest banks, also suffered from a 40 per cent drop in profits in the fourth quarter of 2008, its worst result for years. The negative result included the falling value of its stake in Thailand's TMB (Thai Military Bank) and costs for restructuring after 900 jobs had had to be cut in the third quarter. 5 For the first quarter of 2009, the DBS Group once again had to report a 28 per cent drop in profits as bad dept charges tripled amid the prolonged economic slowdown (AP 2009d).

DBS Group see http://www.dbs.com/home/Pages/default.aspx.

Shares of other leading banking institutions in Singapore such as the United Overseas Bank and the Overseas Chinese Banking Corp. dropped 42 per cent and 23 per cent respectively (see Reuters News 2009b).

Singapore's second sovereign wealth fund, the Government of Singapore Investment Corporation (GIC), also had to face huge losses due to its global investment strategies. While detailed information on these losses is hard to obtain, it is assumed that global woes and poor investment decisions will have reduced the city-state's reserves significantly. The country's foreign reserves managed by GIC had been estimated at some SGD550 billion, and if the losses are similar to Temasek's, then the fund may have lost around SGD170 billion (Star 2009a). Even the Monetary Authority of Singapore (MAS), acting as the central bank, had to admit that the financial crisis and global recession had battered its assets, provoking total losses of more than SGD9.2 billion, or 3.5 per cent of the bank's average assets (AP 2009e).

Coping with the Consequences: The Government's Stimulus Package

Just weeks after the finance markets went into a global slowdown and capital flows began to run dry, the Singapore government announced the first of a number of measures to cope with the recession. On 16 October a joint statement by the MAS and the Ministry of Finance declared that the government would be setting some SGD150 billion aside to guarantee all the bank deposits in the city-state until the end of 2010. While deposits were already ensured for up to SGD20,000 under an existing scheme, the government was expanding its guarantees to all Singapore dollar and foreign-currency deposits of individual and non-bank customers in banks, financial institutions and merchant banks licensed by the MAS. The measure deemed necessary to help the banking system remain sound, especially in view of the situation of the DBS Group, which is one of Asia's largest lenders (AFP 2009d).

This was followed by a further step in December when the government announced it would be convening its National Wage Council (NWC) in early January to prepare for cuts in employers’ pension contributions. The NWC last cut employers’ contributions to the CPF, the retirement fund for Singaporean workers, by three percentage points to 13 per cent in October 2003 to cope with the negative effects of the SARS outbreak. The cuts had only been partially restored by 2007. Although many analysts expected another cut in contributions to be made, the NWC did not change the current contribution rate, which stands at 14.5 per cent of an employee's monthly salary (Reuters News 2009c). Other measures were taken to cope with the crisis, however, and these were embraced in a large stimulus package announced in January 2009 to cope with what has emerged as one of the worst recessions the city-state has ever encountered.

The stimulus package of more than SGD20.5 billion, or eight per cent of the city-state's GDP, is one of the largest measures announced by any government in the Asia-Pacific region. Tharman Shanmugaratnam, Second Minister of Finance, said in his budget speech in parliament that the package included a wide range of measures to help preserve jobs and stimulate the financial sector. In addition to a reduction in corporate income tax from 18 to 17 per cent, which is estimated to cost SGD400 to 500 million, the stimulus package includes SGD5.1 billion to help companies retain their workers and another SGD2.6 billion to support low-income households. A further SGD2.6 billion is intended to help to enhance business cash flow and competitiveness, while another SGD5.8 billion has been set aside to help free up lending. Lastly, the package also includes SGD4.4 billion in infrastructure, education and health-care spending (AFP 2009e; WSJ 2009b). Although consumption only amounts to about 40 per cent of the city-state's GDP – far less than in other Asian economies – only minor steps had been taken to back consumption up. A 20 per cent income-tax rebate was limited to only one year and a cut in the seven per cent goods and services tax was not considered at all.

To finance this large stimulus package, the government will have to draw on the city-state's huge reserves. Some SGD4.9 billion of the package will be taken from this source, mainly from Singapore dollar savings accumulated in previous years’ budgets. It is the first time that the government has had to draw on the reserves to cope with an economic recession. In a speech held at a community event, former Prime Minister Goh Chock Tong made it clear that the government would only draw on the country's reserves in times of economic crises and that the money would not be used to support any welfare programmes (Reuters News 2009d).

But even these measures were unable to prevent Singaporean workers from losing their jobs. In fact, the disappearance of jobs has become the biggest single problem here apart from the economic crisis itself. It is affecting everyone – from the highly educated to the uneducated. While it is the finance sector and other advanced service industries which are being hit particularly hard by the current crisis, the biggest impact is actually being felt by graduates, who make up more than half the number of the new jobless. Government statistics show that the number of unemployed graduates more than doubled in December 2008, rising from 6,200 a year earlier to 14,800, and the largest number of dismissed workers in Singapore consists of degree and diploma holders (Star 2009b). In an attempt to cope with the growing number of unemployed graduates, the government announced a scheme in early 2009 to offer subsidies to recession-hit banks and financial institutions that take new graduates on. 6

Such firms will be given subsidies for the recruits’ allowances for up to a year if the companies take on a minimum of ten new graduates.

As the economy slid into recession, demand for labour plummeted and major projects were delayed or cancelled altogether. As a consequence, not only more and more Singaporeans lost their jobs, but a growing number of foreign workers also got laid off. In the years of prosperity, Singapore's shipyards, construction sites and factories were hiring almost 800,000 foreign workers, most of whom were low-skilled workers from neighbouring countries. But this situation has changed dramatically in the last months. Although hired for a fixed period, more and more of these foreign workers are being sacked by their employers and have to leave the country if they are unable to find any other employment. The problem got some public attention when a group of around 150 Bangladeshi migrant workers staged some rare protests to make people aware of their situation. The workers gathered outside Singapore's Ministry of Labour, urging the government to give them work and help them collect their outstanding salaries now that their employers – Singapore shipping firms – had made them redundant (Reuters News 2009e).

In a public statement, a representative of the Bangladeshi workers said that most of the workers protesting had been promised a monthly salary of at least SGD400 and a work permit lasting two years. But with no more work to be had at the shipyards and no pay for nearly four months, many of them were worried that they would be deported. A large number of them had had to take out loans of up to SGD7,000 from money-lenders back home to pay an agent's fee for finding them employment in Singapore (Reuters News 2009f). Experts predict that in the next two years the crisis may force some 200,000 unemployed foreign workers to leave the country – more than a quarter of its migrant labour force. Given a deepening of the economic crisis, another 100,000 locals may also leave the country for better jobs and income.

The dismissal of foreign workers is just one way Singapore is dealing with an intense labour-market situation, a method that proved successful in earlier recessions. Another strategy is to reduce employees’ working hours and lower their salaries. Unlike companies in many other countries that cut jobs at the first sign of economic trouble, many of Singapore's largest companies are controlled by the government, and staff redundancies at these government-linked companies are therefore considered a last resort to cope with a crisis, after making pay cuts, reducing employer contributions to the CPF and unpaid leave. Although official statistics are hard to obtain, it is estimated that up to a tenth of the workforce has agreed to take unpaid leave or accepted lower salaries (Time 2009). So far, this has helped to keep the unemployment rate at a lower level than expected, but it remains to be seen how things will develop if the city-state's economic situation fails to improve in 2010.

Conclusion

Being highly dependent on the export of goods and services, the Singapore economy has been hit particularly hard by the current economic crisis, and due to the global investment strategies of its state-owned holding companies Temasek and GIC, the city-state has had to report huge losses in public reserves in recent months. Despite comprehensive government spending, companies in the manufacturing sector as well as in banking and finance have had to cut jobs and thousands of workers have been laid off since the outbreak of the crisis. While many well-educated Singaporeans are finding it increasingly difficult to get adequate jobs in the once-booming modern sectors of the Singapore economy, the rare protests staged by Bangladeshi workers earlier this year have pointed out that it is the large group of foreign migrant workers that particularly has to bear the consequences of the current recession.

What is most worrying for Singapore's citizens, though, is the high amount of losses suffered by the city-state's sovereign wealth funds, Temasek and GIC. With the impact of the financial crisis probably just starting to hit the global economy, there are likely to be more disappointments ahead for both of the holdings and their investment portfolios. Even if the latest positive growth figures are more than just a short-lived episode, substantial parts of the city-state's reserves have been lost as Temasek's and GIC's investment strategies prove to be less successful than expected in times of severe economic crisis and even more money will have to be spent to cope with some of the worst consequences of the current recession. Since the Government of Singapore Investment Corporation does not provide any information about its investment strategies and its profits and losses and the annual review published by Temasek only paints a superficial picture of the holding's economic situation, the people of Singapore, whose money the two funds are ultimately controlling, still do not know exactly how badly Singapore has fared during the latest economic turmoil; most of what is “known” about the current crisis in Singapore and its consequences for the wealth of the country is actually based on estimates by economic analysts.

The lack of transparency regarding the investment strategies of the city-state's most important holding companies makes it particularly difficult to analyse the current economic situation in Singapore. There can be no doubt that the economy is experiencing its deepest recession since the city-state's independence in the mid-1960s. While there is a certain stock of statistical figures on declining industrial output, decreasing exports and the negative impact of the crisis on the labour market, precious little information is available on the financial situation of the two holdings and the current development of the city-state's reserves in times of severe recession. Temasek, for example, has never provided any historical financials to back up its claim of overseeing its portfolio prudently, nor has it released any detailed results showing how money – the money of the people of Singapore – flows among its subsidiaries, the holding company and its government shareholder. The situation at GIC is even worse than this.

Although opposition politicians believe that the mounting crisis has exposed flaws in the government's economic management, there has been remarkably little public criticism about the government's policies so far. This may be due to the fact that Temasek's and GIC's losses have not overtly affected the day-to-day lives of most Singaporeans. It is still unclear how far these losses may affect the Central Provident Fund (CPF), a state-run compulsory social-security programme. And as there is no clear evidence to show that these CPF funds may have disappeared with the funds’ recent losses, there has not been a public reaction against the two investment funds’ management teams yet or against the government, which oversees their financial activities.