Abstract

In late 2002, the Chinese government launched an initiative to extend the coverage of health insurance in rural China with the New Rural Cooperative Medical System (NRCMS). It covered all of rural China by 2008 and is being continuously adapted and developed. This study explores two conflicting goals in the policy design: universal coverage and voluntary enrolment. Local governments often faced the problem that only insufficient numbers of villagers were enrolling voluntarily. They developed different strategies to cope with it: Complementary outpatient reimbursement via medical savings accounts (MSAs) effectively transferred villagers’ premiums back to them, thus making the NRCMS more attractive. Adapting the premium-collection process to the local context or utilising collusive practices allowed them to pay premiums on behalf of the villagers from the insurance funds. These strategies undermine the effectiveness of the NRCMS as a risk-pooling mechanism, facilitate latent coverage gaps and turn it into a tax-funded service.

Introduction

China's rural healthcare system has undergone many radical changes in the past several decades: During the Cultural Revolution, its approach of providing basic healthcare via barefoot doctors and the Cooperative Medical System (CMS) was seen as a model for the so-called “Third World.” In the course of economic reforms in the 1980s, the CMS largely collapsed. Due to a massive budgetary retrenchment of the local state, rural healthcare facilities came to rely almost entirely on out-of-pocket payments by the patients (Duckett 2011). As a result, illness became the main cause of rural impoverishment during the 1990s.

Combatting illness-induced poverty was a central goal of policy initiatives to rebuild the CMS. After two failed attempts in 1991 and 1997, the third initiative, in 2002, the New Rural Cooperative Medical System (NRCMS), succeeded in extending health-insurance coverage to the majority of the rural population (Cao 2009; Central Committee and State Council 2002). Successive cohorts of rural counties implemented the system, and by 2008 it was available in all areas of rural China. Both the CMS and the NRCMS (in theory) used social pooling to redistribute the equal financial contributions of their members according to their needs, and thus constitute forms of institutionalised community solidarity. In practice, however, such redistribution was often limited due to the use of household savings accounts instead of or next to pooling accounts. While the CMS was based on subsidiarity and mainly financed by the villagers’ premiums, the NRCMS received the bulk of its funding via earmarked financial transfers from the central and provincial governments, and thus had much greater financial capacity. The NRCMS funds were pooled on the county level, rather than on the township or village level as was the case with the CMS, and thus could offer better risk protection. With regard to the reimbursements the villagers could receive, the NRCMS focused on financial shock caused by catastrophic illness and inpatient treatment, which was to prevent illness-induced poverty. The CMS systems of the 1990s had very diverse reimbursement plans.

Both the CMS and NRCMS were characterised by conflicting goals: They were supposed to be voluntary systems in which rural households could decide on an annual basis whether or not to enrol. However, they were also meant to achieve a high level of coverage of the rural population. Voluntary enrolment in the CMS and NRCMS has been interpreted as a way for the central government to monitor the local governments and to ensure their responsiveness to the people's interests (Klotzbücher and Laessig 2009; Klotzbücher et al. 2010). But both before and after 2002, voluntariness was often a formal policy rather than an actual administrative practice.

In economic theory, adverse selection addresses the problem of asymmetric information in insurance markets (Pauly 1974): In voluntary insurance systems, universal coverage is unlikely to be reached due to the existence of different risk classes. Low-risk consumers tend to opt out of systems pooling them with high-risk consumers, thus decreasing coverage and undermining the sustainability of insurance. Previous research has already confirmed the existence of adverse selection in cooperative health insurance systems (Wang et al. 2006; Zhang and Wang 2008). Higher income groups in rural China displayed a preference for commercial insurance programmes with effective inpatient reimbursement, whereas lower income groups preferred CMSs focused on outpatient reimbursement (Gu, Gao, and Yao 2005). Furthermore, various studies have linked specific patterns of local NRCMS regulations to the willingness to enrol (Brown and Huff 2011; The Ministry of Health 2007: 41–46).

By focusing on the effects of the goal conflict in a local context, this study will explore the issue of voluntary enrolment in the NRCMS from a new perspective. After shedding light on the goal conflict's administrative and political background, it will analyse its practical implications in the implementation process and address two questions: First, why was voluntary enrolment a problematic norm in the local administration of the CMS and NRCMS? Second, how did the conflicting goals of maintaining a policy of voluntary enrolment while simultaneously achieving high coverage rates influence the implementation process and outcomes of the NRCMS?

Following the theoretical framework of actor-centred institutionalism – an extended rational choice approach – this study reconstructs the implementation process via the explanatory elements of the actor constellation, institutional setting and mode of interactions, and visualises them in the form of decision trees (Scharpf 1997). Rather than being an in-depth case study, it provides a general argument about the effects of the goal conflict on the implementation process that, given the necessary adaptations, is potentially applicable to other, similar social policy programmes. The data supporting the argument was collected via semi-structured interviews during fieldwork in four county-level jurisdictions in rural China, which are described in more detail in a section below. The study also relies on informal interviews, data from statistical yearbooks and the official NRCMS evaluation reports (Chen and Zhang 2013; Pilot Evaluation Group 2006; The Ministry of Health 2007), as well as Chinese journal articles, monographs, survey data and administrative documents.

This paper argues that adverse selection, low levels of trust and the existence of large marginalised groups in rural China were fundamental obstacles for local governments to achieve high rates of voluntary enrolment. They faced the dilemma of either failing to achieve their enrolment targets or taking considerable political risks by coercively enrolling people. To mitigate the goal conflict, local governments adapted the NRCMS in various ways, trying to make it more attractive or to manipulate the premium-collection process. These adaptations often decreased the effectiveness of the NRCMS, transformed it into a fully tax-funded service and slowed down the expansion of formal social protection.

The following section of this paper will briefly introduce the administrative and political background of the voluntary enrolment norm, which the NRCMS inherited from the CMS. The study then turns to the impact of the conflicting goals of the NRCMS in the implementation process, focusing on the general dynamics of premium collection under the formal NRCMS rules. The next part will examine different approaches taken by county governments to adapting the NRCMS to mitigate the goal conflict, presenting local governments’ specific strategies in the context of different levels of administrative capacity and the preferences of the villagers. The conclusions and a discussion of the interpretation of data in this study will be presented in the last section.

Voluntary Enrolment: A Brief Introduction

The contradiction between voluntary enrolment and universal coverage has characterised the (NR)CMS since the Maoist period. However, in the context of different power configurations in the central government and a changing institutional setting at the local level, the contradiction generated very different effects in different periods. The organisation of a voluntary cooperative insurance system in rural China generally faces problems of adverse selection and a potential distrust among the population of the local authorities and their abilities and integrity. Furthermore, solidarity and the readiness to mutually aid are strong within family and kin relationships, but relatively weak between people who are not related to one another by family ties or friendship. This increases the difficulties of institutionalising a generalised redistribution of resources on a voluntary basis, as people tend to see illness as a family affair rather than an issue of public policy (Wu 2004). To be effective, the systems need to cover a high share of the local population, but many will likely not enrol voluntarily.

Especially during the Cultural Revolution, the CMS received strong support from the central government (Wang 2009). At the local level, it was institutionally embedded in the collective economy: local cadres had direct control over the economic resources and could deduct the premiums for CMS before the distribution of work points. After decollectivisation, the rural households controlled the economic resources, so the cadres needed to go from house to house and ask for the premiums to be paid. The former mechanism was latent, effective and relatively well accepted, as people did not actually get to choose whether or not to enrol. When the work points were distributed, they had already contributed, and demanding their contributions back would have meant unilaterally breaking the solidarity. The latter mechanism gave the villagers the opportunity to make their own decision before payment and, for the reasons described above, many were not ready to pay.

The process of premium collection became very time-consuming, psychologically difficult and conflict-prone. Furthermore, national politics were characterised by the opposition of pro-government and pro-market forces, in which pro-market forces were largely dominant. The central government's preferences regarding the CMS were unstable, and some provinces supported it while others opposed it. Under these conditions, premium collection and voluntariness became a critical weakness of the CMS (Cao and Zhang 1990; Cao 2009; Duckett 2011; Han and Luo 2007: 224; Huang 2013; Müller 2014).

The increased difficulties of premium collection contributed to the collapse of the CMSs during the 1980s. In order to achieve high enrolment rates, cadres now frequently needed to resort to pressure and coercion. As Bloom and colleagues noted:

Most successful [CMS schemes] are not fully voluntary. […] [I]n the 1987 study, in three-fifths of villages with a scheme, more than 90 per cent of their populations were members […]. This is not the pattern one would find if households could decide each year whether they wished to contribute. The success of a scheme depends on the ability of local leaders to ensure that people join and remain in for several years. (Bloom, Tang, and Gu 1995: 435)

In wealthy areas, the organisational structures of the local economy provided the basis for alternative models of premium collection. In most areas, however, the political “authority” of grassroots cadres was indispensable (Klotzbücher 2006: 217, 227–233; Wang 2006: 134–137).

The Ministry of Finance (MoF) and the Ministry of Agriculture (MoA) frequently

exploited this problem to denounce premiums as involuntary and illegitimate fees

adding to the “farmers’ burden” ( , nongmin

fudan) and contradicting the agenda of rural tax reforms (Bernstein and

Lü 2003). The Ministry of Health (MoH) managed to launch two policy initiatives for

the CMS, with premiums and village levies as core sources of funding (Central

Committee and State Council 1997; State Council 1991a, 1991b). The centre set

national coverage targets – of 50 per cent of the rural population by 1995, and 70

per cent by 2000 – and encouraged local cadres to collect premiums for CMS (World

Bank 1992: 98). Both initiatives were subsequently sabotaged by being accused –

mainly by the MoA and the MoF – of constituting a financial burden for the rural

population. These accusations brought the CMS into direct conflict with the

prevailing policies of decreasing the rural population's load of random fees and

charges, thus delegitimising it as a policy. When the initiatives came under attack,

local coverage targets and the use of village levies for the CMS were strictly

forbidden. This increased the career risks for local cadres engaged with the CMS and

strongly undermined their commitment to the policy, which contributed to decreasing

CMS coverage. Under Zhu Rongji's premiership, commercial insurance companies were

the silent beneficiaries of these developments. Commercial insurance in rural areas

covered a larger share of the population than it did in urban areas and surpassed

CMS coverage in the rural middle-income areas (Cao 2009; Müller 2014; The Ministry

of Health 2004: 15ff).

, nongmin

fudan) and contradicting the agenda of rural tax reforms (Bernstein and

Lü 2003). The Ministry of Health (MoH) managed to launch two policy initiatives for

the CMS, with premiums and village levies as core sources of funding (Central

Committee and State Council 1997; State Council 1991a, 1991b). The centre set

national coverage targets – of 50 per cent of the rural population by 1995, and 70

per cent by 2000 – and encouraged local cadres to collect premiums for CMS (World

Bank 1992: 98). Both initiatives were subsequently sabotaged by being accused –

mainly by the MoA and the MoF – of constituting a financial burden for the rural

population. These accusations brought the CMS into direct conflict with the

prevailing policies of decreasing the rural population's load of random fees and

charges, thus delegitimising it as a policy. When the initiatives came under attack,

local coverage targets and the use of village levies for the CMS were strictly

forbidden. This increased the career risks for local cadres engaged with the CMS and

strongly undermined their commitment to the policy, which contributed to decreasing

CMS coverage. Under Zhu Rongji's premiership, commercial insurance companies were

the silent beneficiaries of these developments. Commercial insurance in rural areas

covered a larger share of the population than it did in urban areas and surpassed

CMS coverage in the rural middle-income areas (Cao 2009; Müller 2014; The Ministry

of Health 2004: 15ff).

After 2000, the central party leadership reached a consensus to endorse the CMS in rural areas and to support it with financial transfers (Liu and Rao 2006). The NRCMS was a compromise between pro-government and pro-market forces, as the main policy document about the NRCMS by the Central Committee and the State Council in 2002 illustrates: commercial insurance companies were allowed to continue their operations in the rural areas, and the NRCMS was not to be interpreted as a burden for the villagers (Central Committee and State Council 2002). Despite policy experts’ support for a compulsory system, the norm of voluntariness was retained. Policy experts thus suggested raising the priority of enrolment targets for local governments and making the level of NRCMS subsidies dependent on the level of enrolment (Carrin, Davies and Jiang 2002; Liu, Rao, and Hu 2002: 52f).

The centre largely followed these suggestions, and reproduced the old contradiction between universal coverage and voluntary enrolment to reconcile opposing political forces. Once again, local governments were confronted with contradicting policy demands, but the context had changed once more. This time, there was a stable consensus at the central level supporting the NRCMS. The financial transfers, furthermore, created not only incentives for the villagers to enrol, but also an interest of the higher levels of government in stable enrolment rates.

The Premium-Collection Dilemma of the NRCMS

The argument presented in the following two sections is largely supported by fieldwork conducted in four counties in rural China in 2010 and 2011. Access to the field was gained through the local health administrations on the city or county level. The overall duration of the stays were eight days in County A, seven days in District C, eight days in County B and four days in County D. Semi-structured interviews were conducted mainly with NRCMS staff in health administration, county hospital and township health centre staff, and village doctors. Furthermore, some informal interviews with farmers were conducted in the absence of cadres.

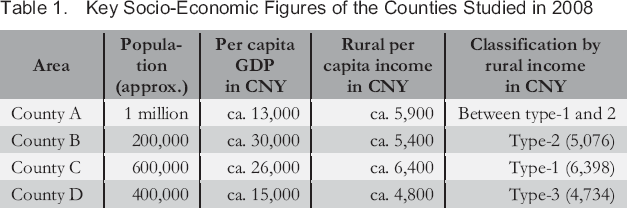

Table 1 illustrates some key socio-economic figures of the four counties in which I conducted field work. County A was a model county for the NRCMS and other health policy initiatives located in the less developed regions of Jiangsu Province. It had the largest population and the second-highest rural mean income among the four counties, but its per capita GDP was the lowest. County B was located near a large industrial centre in Inner Mongolia, District C was an urban district on the outskirts of a large, prosperous city in Hubei Province, and County D was a rural area in one of the least developed parts of Shandong Province. Even though County B was officially a “national poverty county,” County D ranked lower on both per capita GDP and rural income. According to the classification of the 2008 National Health Services Survey of the MoH, County D was a type-3 county and thus most representative of rural China, whereas none of the counties matched the standard of a poor type-4 county. County A, County B and District C were all type-1 or type-2 counties, and thus above average in socio-economic terms: they had rather favourable implementation conditions and their implementation results were arguably above average. The NRCMS was implemented in successive cohorts, in which localities with favourable socio-economic conditions, experience in health policy and large rural populations took the lead (State Council 2003). The implementation schedules of the counties in the study reflect this: County A began implementing the scheme in 2003, District C in 2005, County B in 2006 and County D in 2007.

Key Socio-Economic Figures of the Counties Studied in 2008

The Preferences of Local Governments

The following sections develop an interactive model of the premium-collection process based on the analysis of the preferences of local governments and villagers. The focus is on the perspective of the local governments, whose preferences with regard to premium collection can be summarised in the following hierarchy: they first and foremost sought to fulfil the target quotas for enrolment assigned to them; second, they sought to minimise the costs of premium collection; third, they attempted to avoid political risks, such as protests or petitions connected to violations of the voluntary enrolment norm.

In the counties where field work was conducted, fulfilling the enrolment quota was of paramount importance, and failing to meet the quota could in some areas lead to very harsh restrictions. A cadre in County B pointed out:

In the first year, the target quota was 70 per cent. If we had not made the quota, the NRCMS subsidies from the higher levels would not have been transferred. We achieved 71.6 per cent. […] No township has ever missed the quota. […] If we had not made the quota, there would have been no financial support and the pilot would have failed. (Anonymous 5 2011)

The cadres in the other counties under study often described premium collection as problematic, stressful and burdensome, yet no county had ever missed its quota (Anonymous 1 2010; Anonymous 3 2010; Anonymous 8 2011).

Between 2003 and 2008, enrolment targets were often included by provincial governments in NRCMS administrative documents. As the targets were handed down the administrative hierarchy, each level of government would add a few percentage points in its requirements for the next lower level. At the same time, the level of the targets increased by a few points every year. The targets usually oscillated between 60 and 80 per cent in the early years, and have remained above 90 per cent since 2009, when the State Council began to issue them directly. Some provinces included the quotas in public policy documents: Jiangsu, for example, demanded 60 per cent in the first year and 80 per cent in the second year; City Y adopted the rate of 60 per cent for 2003, and set a target of 85 per cent for 2004; County A – under City Y's jurisdiction – increased the 2004 rate by 5 per cent, demanding at least 90 per cent from its townships. Shandong, on the other hand, did not mention quotas in the main documents, but the local cadres reported their existence (Anonymous 2 2010; Anonymous 9 2011; Han and Luo 2007: 396f; Jiangsu Government 2003; State Council 2009; Wang 2006: 444f; Y City Government 2003).

Counties had limited discretion to set the quotas, which usually measured the share

of the number of enrollees in the overall population with a local, agricultural

household registration ( , bendi nongye

hukou). District C used this method, and the administrators described

it as appropriate (Anonymous 8 2011). County B was an outmigration region:

hukou figures were way above the actual remaining population

and would have set unrealistically high targets. County B instead used the

residential population figures (

, bendi nongye

hukou). District C used this method, and the administrators described

it as appropriate (Anonymous 8 2011). County B was an outmigration region:

hukou figures were way above the actual remaining population

and would have set unrealistically high targets. County B instead used the

residential population figures ( , changzhu

renkou) of the public security administration, which led to lower

enrolment targets. County A used demographic figures from the Bureau of Statistics,

which the local cadres saw as accurate. It allowed households with a

non-agricultural hukou to enrol – especially workers in township

enterprises (Anonymous 5 2011; Anonymous 9 2011).

, changzhu

renkou) of the public security administration, which led to lower

enrolment targets. County A used demographic figures from the Bureau of Statistics,

which the local cadres saw as accurate. It allowed households with a

non-agricultural hukou to enrol – especially workers in township

enterprises (Anonymous 5 2011; Anonymous 9 2011).

Township and village cadres were usually responsible for premium collection. Leading county cadres could exert pressure on them by, for example, publicly displaying support for the NRCMS or participating directly in its implementation (The Ministry of Health 2007: 108). Coverage targets were usually integrated into the leading cadre evaluations via performance contracts and were thus connected to bonuses and sanctions. All counties included in the field research had used contracts in their early implementation years to stabilise enrolment, and County A was still using them ten years after implementation. Most counties used hard targets, but even soft targets helped to exert pressure and influence whether or not township cadres could be promoted (Anonymous 1 2010; Anonymous 2 2010; Anonymous 5 2011; Anonymous 8 2011; The Ministry of Health 2007: 108; Wang 2006: 444f).

Premium collection was an expensive process, with administrative costs usually between 10 and 30 per cent of the overall amount of premiums collected. In County A, the administrative costs in 2003 were estimated to be almost CNY 1.5 million, or 20 per cent of the collected premiums. Of the costs incurred, 73.8 per cent were at the village level, 22.5 per cent at the township level and 3.7 per cent at the county level. Personnel expenditures were the largest part, followed by expenses for workshops and training, propaganda and transportation. In the remote and mountainous regions of Central and Western China, the costs of premium collection were sometimes even higher due to factors such as difficult terrain and low population density, along with the lower applicability of alternative collection methods (Pilot Evaluation Group 2006: 47; Wang 2006: 137–142).

Pressurised premium collection was connected to considerable political risks for

county governments, as grassroots cadres might violate the rules of the system,

which could in turn lead to petitions or whistleblowing by the villagers. There was

a high risk of funds being withheld or abused at the local level, and of village

cadres turning to coercive practices when the number of voluntary enrollees was

insufficient to fulfil the quota (Wang 2006: 137–142). Starting in late 2003, a

number of counties were exposed and criticised for violating the principle of

voluntariness and engaging in illegitimate premium-collection practices, and in

January 2004, the State Council criticised performance contracts, coercive enrolment

and other practices (State Council 2004; The Ministry of Health 2003a, 2003b). Such

criticisms were arguably often sparked by the complaints of villagers to the media

or higher levels of government (Anonymous 9 2011). After the centre emphasised

voluntariness in 2004, enrolment rates reportedly declined (Chen and Zhang 2013: 59;

The Ministry of Health 2007: 108). After 2005, voluntariness gradually ceased to be

a sensitive political issue at the central level. An evaluation report by the MoH in

2007 recommended tolerating local “adaptations” ( , biantong)

in the face of contradictory policies, as long as it did not cause the rural

population to dislike or actively oppose the NRCMS – for example, by refusing to

enrol, or filing petitions to higher levels of government (The Ministry of Health

2007: 145).

, biantong)

in the face of contradictory policies, as long as it did not cause the rural

population to dislike or actively oppose the NRCMS – for example, by refusing to

enrol, or filing petitions to higher levels of government (The Ministry of Health

2007: 145).

The Villagers’ Preferences

The preferences of the villagers with regard to the NRCMS depended strongly on the local socio-economic conditions, as well as their perceived economic self-interest and their disposition towards the government. The 1998 MoH survey claimed that 51 per cent of the rural population were willing to enrol in the CMS – slightly more than the centre's target of 50 per cent (Cf.: The Ministry of Health 1999: 130; World Bank 1992: 98) – and that willingness was lower in poor areas, with more than 60 per cent not willing to enrol. The 2007 evaluation report substantiated this basic correlation, but gives a more realistic assessment:

Summarising the opinions of administrators on all levels, one can assume that in areas with a relatively good economic situation, the share of villagers genuinely willing to enrol […] is 50 per cent at the most. In areas with a bad economic situation, 20 to 30 per cent voluntarily enrol. (The Ministry of Health 2007: 107)

Achieving high coverage was more difficult in poor than in wealthy areas.

The structure of local reimbursement plans had a considerable influence on the willingness to enrol among different groups of villagers. The CMS had three basic types of coverage models: first, exclusive coverage of outpatient expenditures for small ailments; second, exclusive coverage of inpatient costs and catastrophic diseases; and third, coverage of both. According to the MoH survey, the last was the most popular option: among those willing to enrol in the CMS, 55 per cent favoured such a model, whereas exclusive coverage of either outpatient or inpatient services was favoured by only 24 and 21 per cent, respectively (The Ministry of Health 1999: 130). Gu and colleagues found a similar hierarchy of preferences in their sample, and indicated that high-income households put a greater emphasis on risk-pooling for catastrophic and inpatient diseases, whereas low-income households value outpatient reimbursement and primary healthcare more (Gu, Gao, and Yao 2005: 281–285).

Wu furthermore distinguishes three ideal-typical dispositions regarding health insurance and the NRCMS. Some villagers understand the concept of health insurance and are supportive of the NRCMS, mainly due to their previous contact with “modern” urban life. Others distrust the idea of health insurance due to the influence of traditional values and see illness as a family affair rather than a public issue the government should take care of. Yet others are more opportunistic, tend to follow the group and put a particular emphasis on the direct and visible benefits of the system. The specific local configuration of those attitudes depends strongly on socio-economic development and can crucially influence the dynamics of enrolment and premium collection. Direct and visible benefits thus often played a crucial role in the implementation process (Wu 2004: 136).

The Premium-Collection Process

The following sections will reconstruct an abstract model of the premium-collection process. The mode of interaction is unilateral actions in a context of weak minimal institutions: The villagers are an aggregate actor incapable of coordinated action or collective negotiations. They have the formal right to enrol voluntarily, but may not be able to enforce it against the local government, which is a corporate actor consisting of the county government and administration, the subordinated township governments, the village cadres and other staff they might draft for premium collection.

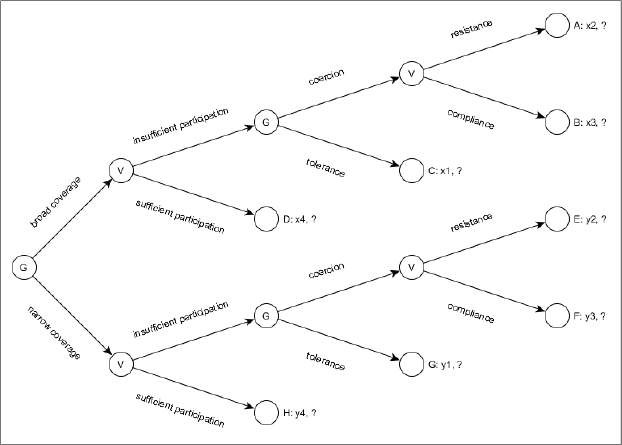

Figure 1 illustrates the dilemma of premium collection between the villagers (V) and the local government (G). It focuses on the decisions and payoffs of the local government, and conceptualises the villagers as an aggregate actor with unknown preferences that merely reacts to the government's decisions. The government's payoffs are put into an ordinal hierarchy of x4 > x3 > x2 > x1 and y4 > y3 > y2 > y1, with y4 > x4 and y1 > x1, but no clear specification of the relationships between the other payoffs.

Interaction Process of Local Governments and Villagers

As a first step, the government decides whether to use a broad or a narrow coverage package, and how to design the NRCMS in general. The villagers then react with a certain level of enrolment. When this level matches or surpasses the enrolment target, the government has succeeded in meeting the target while also upholding voluntary enrolment, and the premium-collection process comes to an end (outcomes D and H). As a rule of thumb, enrolment will be higher with broad coverage packages, which are, however, costlier to administer. Outcome H is more desirable for the government than outcome D if both can be achieved, but the enrolment rate would usually be higher with outcome D.

If the enrolment rate remains below the target, the government can choose to tolerate this (outcomes C and G) – a rather theoretical alternative which would mean to admit failure – or to turn to coercion to achieve the desired enrolment rate. If it chooses coercion, the villagers can either comply or resist – for example, by writing petitions to higher levels of government demanding their right to enrol voluntarily, or by leaking information to the press. However small the chance of successful resistance may be, if the local government chooses coercion, it is no longer fully in control of the outcome. The hierarchy of outcomes is D > B > A > C and H > F > E > G, with H > D and G > C due to the lower level of administrative costs. The remaining hierarchical relations are difficult to determine at this point and may differ between localities.

When voluntary enrolment was insufficient, township and village cadres still had a few strategies at their disposal to enhance enrolment which are not made explicit in Figure 1. For instance, they were able to offer privileged access to certain goods and services, such as credits or certificates for migrant workers, in exchange for the villagers to come to the village committee and enrol at a specified date and time. They also sometimes prepaid the missing amount themselves or through local enterprises, and later retrieved it from the villagers. Another strategy was for cadres to deduct premiums from other payments such as subsidies for agriculture or reforestation, or to add them to water and electricity bills. Using these strategies, the cadres often operated within a grey zone between legitimate and illegitimate practices (The Ministry of Health 2007: 109f, 2009d).

But still, the reliance on pressure and coercion was widespread and systematic. In

County A, the cadres explained that if a township failed to achieve its quota, they

would first try and find out the reason why people did not enrol, and then work to

“convince” them ( ,

zuo gongzuo) (Anonymous 1 2010). A cadre in District C

described this process as follows:

,

zuo gongzuo) (Anonymous 1 2010). A cadre in District C

described this process as follows:

If they are not willing to enrol, we convince them. We will visit each and every household, time and again, until we have made the quota. (Anonymous 8 2011)

“Convincing” the villagers could include making threats; therefore, the transition to coercion was rather smooth: “Actually forcing them would violate the regulations, but when we convince them our tone can be a little tough” (The Ministry of Health 2007: 110). Both pressure and coercion were connected to a substantial workload for the township and village cadres, and actual coercion was connected to political risks.

Strategic Adaptations of the NRCMS

Under the pressure of the conflicting goals and the political risks connected to them, county governments began to develop coordinated strategic approaches to systematically adapt the NRCMS and circumvent the problem of premium collection. In economically developed areas, local governments could rely on a broader mix of premium-collection methods (The Ministry of Health 2007: 157; Wang 2006: 137–142). This paper focuses on methods applicable in economically less developed regions and distinguishes three approaches: responsively adapting the NRCMS to the framework of existing rules, changing the rules and openly communicating this as innovation, and changing the rules collusively (cf.: Heberer and Trappel 2013). These three approaches facilitated a transformation of the NRCMS from a cooperative towards a state-sponsored system of health insurance.

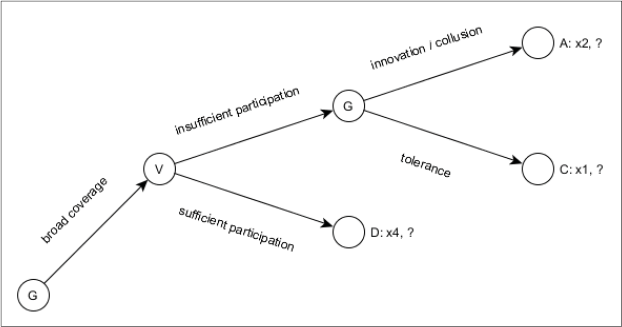

Figure 2 illustrates the impact of the strategies on the decisionmaking process, which now only has three outcomes (A, C and D) with x4 > x2 > x1. As a first step, adapting the NRCMS typically meant including new types of medical or administrative services and thus broadening coverage and the distribution of benefits. This raised the chances of achieving the quota voluntarily (outcome D). If this failed, innovative and collusive approaches could be used – either exclusively or in combination with one another – to achieve the required quota (outcome A) and avoid the political risks of coercion.

Premium Collection with Responsive Adaptation, Innovation and Collusion

Responsive Adaptation

Through responsive adaptation to the villagers’ preferences, the NRCMS was able to generate higher levels of voluntary enrolment (cf.: Klotzbücher and Laessig 2009). The villagers often preferred direct and visible benefits, which only outpatient reimbursement could offer (cf.: Wu 2004). Furthermore, marginalised groups, such as migrant workers or the poor, had a hard time benefitting from the system and thus had good reason not to enrol. Households below or slightly above the poverty line often did not benefit from the NRCMS due to the high copayment rates and the prevalence of ex-post reimbursement for inpatient services (The Ministry of Health 2007: 148). Migrant workers were usually required to enrol in the NRCMS with their entire households, but reimbursing health services consumed in the urban centres (where they lived most of the year) was often difficult or impossible. Responsive adaptation thus usually sought to broaden coverage of services and improve access to care.

The most common approach was the reimbursement of outpatient services, most notably

through household accounts administered by the government into which a part of the

funds would be deposited. These medical savings accounts (MSAs,  , jiating

zhanghu) were the chosen system by 60 to 80 per cent of the counties in

the early cohorts (Mao 2005). Studies on the CMS had already suggested a positive

impact of outpatient reimbursement on the willingness of villagers to enrol

(Klotzbücher 2006: 207–210; The Ministry of Health 1999: 130). MSAs furthermore

responded to a general lack of solidarity beyond family boundaries in the rural

areas. They usually contained (a part of) a household's premiums and excluded these

premiums from redistributive pooling, thus giving the villagers the feeling that

their money still belonged to them exclusively. The funds for redistributive pooling

mainly came from the governmental contributions to the NRCMS. In the NRCMS, the

highest enrolment rates for all income groups were achieved by MSAs, followed by

outpatient pooling (

, jiating

zhanghu) were the chosen system by 60 to 80 per cent of the counties in

the early cohorts (Mao 2005). Studies on the CMS had already suggested a positive

impact of outpatient reimbursement on the willingness of villagers to enrol

(Klotzbücher 2006: 207–210; The Ministry of Health 1999: 130). MSAs furthermore

responded to a general lack of solidarity beyond family boundaries in the rural

areas. They usually contained (a part of) a household's premiums and excluded these

premiums from redistributive pooling, thus giving the villagers the feeling that

their money still belonged to them exclusively. The funds for redistributive pooling

mainly came from the governmental contributions to the NRCMS. In the NRCMS, the

highest enrolment rates for all income groups were achieved by MSAs, followed by

outpatient pooling ( , menzhen tongchou) – the redistributive pooling of the

outpatient funds in the sense of institutionalised general solidarity, as opposed to

the familial solidarity institutionalised in the MSAs. The differences between

reimbursement models were more pronounced in the lower income groups: the poor had a

stronger preference for outpatient reimbursement (Mao 2005; The Ministry of Health

2007; Wu 2004).

, menzhen tongchou) – the redistributive pooling of the

outpatient funds in the sense of institutionalised general solidarity, as opposed to

the familial solidarity institutionalised in the MSAs. The differences between

reimbursement models were more pronounced in the lower income groups: the poor had a

stronger preference for outpatient reimbursement (Mao 2005; The Ministry of Health

2007; Wu 2004).

MSAs were feasible even for local governments with low administrative capacity. Much of the workload could be delegated to the township health centres (THCs). But MSAs were also criticised for their insufficient financial capacity, and for compromising the cooperative nature of the NRCMS in order to attract the villagers (Hu 2005). Their funds furthermore tended to accumulate unused and were sometimes used to compensate for other administrative expenses, leaving empty accounts (Pilot Evaluation Group 2006: 49f). MSAs effectively gave villagers their money back and excluded their premiums from social pooling – either partly or fully. The NRCMS thus became a government-funded insurance amended by household savings schemes, rather than the system of general solidarity and redistribution that the term “cooperative” points to.

Since 2006, the role of MSAs in the NRCMS gradually decreased – especially after the central government began to set quotas for the use of outpatient pooling (The Ministry of Health 2009c). The share of MSA funds in the accumulated NRCMS funds decreased from over 10 per cent in 2006 to approximately 2 per cent in 2011. These figures were approximately twice as high in Central and Western China, where premiums and MSAs had equal shares of 20 per cent of the funds for a while (Chen and Zhang 2013: 69f). Three of the studied counties had previously used MSAs, but had already switched to outpatient reimbursement by 2010. THC staff in County B explicitly described MSAs as a mobilisation measure of the early implementation years to raise enrolment (Anonymous 6 2011). In District C, the director of the county NRCMS Bureau praised MSAs for having been more appropriate than outpatient pooling in terms of distributive fairness (Anonymous 8 2011).

Another option to raise the attractiveness of the NRCMS was direct reimbursement – meaning, reimbursing services at the hospital directly after treatment. It effectively decreased villagers’ out-of-pocket payments, but was constrained by its high requirements for administrative capacity. It was more common for outpatient services and of particular advantage for low-income households with problems paying the full amount out-of-pocket before claiming reimbursement. Ex-post reimbursement – at the Bureau of Health or another organ – remained dominant for inpatient services, being easier to organise and more conducive to controlling the financial risks for local governments with a limited capacity of financial forecasting (The Ministry of Health 2007: 41–46).

Counties with large shares of migrant workers in their populations were able to raise the attractiveness of the NRCMS by adapting it to their needs. First, this required making services consumed out-of-town eligible for reimbursement, which in earlier years had depended on local initiatives but is currently being institutionalised more broadly (cf.: Klotzbücher and Laessig 2009). Second, regulatory details such as reimbursement rates or deadlines for claiming reimbursement made a considerable difference. A migrant worker from Chongqing working in Hangzhou explained that after a treatment in Hangzhou, he would have only three months to claim the reimbursement back in Chongqing (Anonymous 10 2011). Given the direct costs and the loss of income caused by such a trip, only very high reimbursement sums would be worth claiming. Travelling home to receive cheaper treatment with higher reimbursement rates is often the more attractive option in case of serious illness.

Innovation

County governments were also able to create or adopt innovations that, upon their positive appraisal by higher levels of government, could be subsequently extended. County A, for example, created a system of premium collection which directly deducted farmers’ premiums from their reimbursements. The innovation was first tried out in 2004 in several townships and then extended to the entire county. Premiums for the following year were directly deducted from villagers’ inpatient and outpatient reimbursements. According to the local government, more than 80 per cent of the premiums were collected gradually during the year at the THCs and village stations. This substantially reduced the workload, costs and conflict potential of the cadres’ premium-collection process at year's end (Anonymous 1 2010; Wang 2006; Wang et al. 2005; Y City NRCMS Administrative Committee 2005).

County A's administrative capacity and experience in health policy were above average. Many village health stations were directly managed by the THCs with regard to drug supply and financial accounting, and the government invested strategically in the computerised management of its THCs. This allowed for a delegation of the premium-collection process to township and village health facilities. The system was furthermore supported by a broad reimbursement catalogue and outpatient pooling – 65 per cent of the NRCMS funds reimbursed basic health services, rather than inpatient services (Wang 2006; Wang et al. 2005).

By 2008, County A's innovation had spread to more than 150 counties in more than 20 provinces (Wang 2008). Where the adopters’ conditions were less favourable, this innovation often played a smaller role in the mix of premium-collection methods. Lianyuan City in Hunan Province, for example, adopted it only for inpatient reimbursement, so its effects remained limited. Furthermore, Lian-yuan reported having some administrative challenges that may also have hindered the extension of the approach in other areas: premium collection became a fragmented process involving township NRCMS offices, contracted hospitals and birth-planning stations, which raised the requirements of coordination and information-processing (Liang 2006).

The Collusive Substitution of Premiums

Collusive strategies were also able to directly replace premiums with financial resources from the NRCMS funds. Funds that were administered at the township level and used for large numbers of small-scale transactions were difficult to monitor and thus very suitable for such purposes. A typical approach was to directly take money out of the villagers’ MSAs and put it in the account for the collected premiums, which was officially condemned in 2007 (The Ministry of Health, the Ministry of Finance, and the State Administration of Traditional Chinese Medicine 2007). Funds allotted for medical check-ups could serve similar purposes: Check-ups could, for example, be scheduled for unenrolled villagers without informing them. When they did not show up, the money was used for premiums. Both types of funds were also affected by other forms of abuse and embezzlement, such as the compensation of the administrative costs of THCs (Anonymous 9 2011; Pilot Evaluation Group 2006: 49f; The Ministry of Health 2007: 109).

The use of MSA funds for premiums appeared in local policy proposals as early as 2004 (Hu 2005). Zou illustrates this strategy at the example of one pilot county from the first cohort. The local government chose to use MSAs for outpatient reimbursement, into which CNY 7 of the individual premiums of CNY 10 were deposited. In 2003, the costs of premium collection for approximately 620,000 enrollees were reported to amount to over CNY 1 million – more than 16 per cent of the collected premiums. In 2005, the MSAs were no longer used for reimbursement, and from 2006 on 7 of the CNY 10 were used for premiums, leaving an effective premium of CNY 3 per villager. Wealthier townships paid the CNY 3 per capita themselves and collected no more premiums at all. The costs of collection remained at CNY 1 million in 2004 and decreased to 500,000 in 2006. At this time, there were approximately 760,000 enrollees (Zou 2008: 170–177).

This was not a lone case:

Many local governments used the “MSA” method to dispel the villagers’ doubts and increase their enthusiasm for NRCMS when the costs of premium collection were high. Between CNY 6 and 12 (including CNY 2 from the government) were deposited in these accounts. (Zou 2008: 211)

An administrator in District C confirmed the use of such techniques in remote and mountainous areas of Hubei Province (Anonymous 8 2011). The method provided a viable approach for counties lacking the administrative capacity to apply County A's innovation effectively – typically counties with MSA models in Central and Western China. Where the full amount of premiums was transferred to the MSAs, farmers could theoretically remain permanently insured by paying the full premium amount only once. In such cases, the NRCMS would be effectively transformed into a fully state-sponsored system of social security (Zou 2008: 211).

Most MSAs have been abolished in recent years, and local governments practising this type of premium substitution had to look for alternative sources of funding, which are not well documented. The outpatient-pooling funds that largely replaced the MSAs, and like them are rather withdrawn from scrutiny of higher levels of government, provide promising sources of premium substitution and other collusive practices. A group of villagers in County B, for example, insisted that small outpatient expenditures would not be reimbursed and that reimbursement was restricted to inpatient services, while their descriptions of the premium-collection process and the level of premiums largely matched those of the cadres (Anonymous 7 2011). County B had, however, formally used MSAs for years, and recently had shifted to outpatient pooling. As small ailments are far more common than catastrophic diseases, one would expect the local population to have a relatively sound knowledge of the respective reimbursement process. Another potential source of funds for substitution would be the surpluses of the NRCMS funds. Due to conservative management, the funds often retain surpluses, rather than being fully depleted at the end of every year (Zhang et al. 2010). NRCMS regulations limit the accumulated surplus to a maximum of 25 per cent of the overall funds, a benchmark often surpassed in practice (The Ministry of Finance and the Ministry of Health 2008, 2009). The share of premiums in the overall funds is about 20 per cent, so a legitimate surplus would theoretically be sufficient.

Conclusions and Discussion

The contradiction between a policy of voluntary enrolment and the goal of universal coverage has characterised (NR)CMS through different historical periods and has had different effects in the context of changing power configurations at the central level and changing economic institutions at the local levels. The inability of the centre to depart from this inherited contradiction in the 2002 NRCMS reform is arguably connected to consensual, negotiation-based modes of decision-making, which needed to accommodate opposing political forces. The buck of resolving the contradiction was passed down to local governments, who were largely unable to achieve their coverage targets via fully voluntary enrolment due to adverse selection, issues of trust, and the existence of large marginalised groups in the rural areas.

Local governments developed three larger strategies to overcome this contradiction: raising the attractiveness of the NRCMS via responsively adapting it to the people's preferences, creating innovative measures of premium collection that bypass these problems, and collusively substituting the villagers’ premiums with part of the NRCMS funds. Issues of premium collection were a central motivation for the vast majority of local governments choosing MSAs for outpatient reimbursement across very diverse socio-economic contexts.

The impact of each strategy on the effectiveness of the NRCMS was different. Based on the funding standards in place since 2006, they were all able to decrease the amount of funds available for pooling by up to 20 per cent. County A provided outpatient coverage without deductibles, thereby improving the coverage of chronic diseases and enhancing the capacity of the NRCMS to combat illness-induced poverty (cf.: Yip and Hsiao 2009). MSAs decreased the capacity of the NRCMS to combat illness-induced poverty and undermined its effectiveness as an insurance system. Informal and collusive practices facilitated a transformation of the NRCMS towards a fully tax-funded service, and slowed down the expansion of formal social protection in the rural areas. These practices arguably became widespread, but estimating their overall impact on the NRCMS is difficult.

The interpretation of data for this study was connected to some challenges due to the somewhat sensitive nature of the voluntariness issue. Only few Chinese studies directly discuss the problems of premium collection and voluntary enrolment, whereas the vast majority implicitly assumes that the NRCMS is a voluntary system. The author gave analytical priority to studies problematising the issue. The cadres in all counties studied confirmed the existence of enrolment targets when they were asked about them directly, and the analysis of provincial documents suggests that these targets were widespread. The cadres did not admit the use of coercive enrolment practices in their own jurisdictions, but they generally confirmed that premium collection was complicated, problematic and difficult to accomplish without the political authority of the grassroots cadres. Government statistics about the willingness to enrol must be interpreted carefully. Often, they are based on statistical figures provided by the MoH, and the reported share of people willing to enrol is slightly above the current target of enrolment (cf.: The Ministry of Health 1999: 130, 2009a: 18).

The level of conflict in premium collection seems to have decreased over the years, which is a very interesting development. According to the cadres in most counties, the intensity of the problem was highest when the implementation first began; over the years, rising NRCMS transfers raised the reimbursement rates and made the system more effective and attractive, and the people became increasingly used to it (Anonymous 2 2010; Anonymous 3 2010; Anonymous 4 2010; Anonymous 8 2011; Anonymous 9 2011). In County A, County B and District C – the above-average counties of the ones in which I conducted field research – I was able to conduct some informal interviews with villagers in the absence of cadres. They gave no indications of coercive enrolment practices or an interruption of annual premium collection.

But while the cadres’ arguments appear to be largely accurate, they still fail to fully explain the decreasing intensity of the goal conflict for two reasons: First, the official rate of enrolment continuously rose, from 75 per cent in 2004 to 92 per cent in 2008 (The Ministry of Health 2009b). During this time, the NRCMS was extended to more than 2,000 county-level jurisdictions with lower financial and administrative capacity and populations more hostile to the NRCMS than those in the first cohort. Second, premiums rose, while at the same time large parts of the NRCMS funds were retained rather than spent every year – especially in counties of the later cohorts with low administrative capacity (Zhang et al. 2010). The later cohorts thus tended to have worse implementation conditions and to offer inferior services compared to the first cohorts, yet they apparently achieved higher enrolment rates from the start. The strategies presented above can help to explain this apparent enigma.

Official enrolment rates have been steadily rising in recent years, and have even closed in on 100 per cent. In 2009 the MoF and the MoH criticised the widespread over-reporting of NRCMS enrollees by local governments, rather than coercive enrolment practices. This indicates that there may still be considerable gaps in health-insurance coverage. More research is needed to shed light on the effects of voluntary enrolment norms and informal financial and enrolment practices of local governments. Comparative studies of the implementation processes of other voluntary, tax-funded social protection programmes in urban and rural China could contribute to an informed assessment of the degree to which such implementation gaps change the nature of China's emerging welfare regime.