Abstract

How do governments manage expectations from international capital keen on pressuring them into adopting market-oriented economic policies during times of crises? Studying executive communication in 267 annual state-of-the-union speeches in 12 Latin American countries between 1980 and 2014 reveals two broad options for strategic position-taking on economic policies. First, when times are dire, presidents not only talk more about the economy and less about social policy, but they also attempt to repurpose other policies as an investment in development. Second, economic turmoil encourages presidents to signal policies, which are appealing to international capital owners. However, while currency crises exert more enduring pressure, the effects of loan crises are more fleeting. Our results are particularly relevant to all who seek to understand how governments use public statements to address pressures from financial markets.

Introduction

For Latin American governments, access to international capital is crucial to finance state projects and to be able to underwrite current account deficits. Emerging markets, however, are perceived as risky and capital flows to the region tend to follow a pro-cyclical pattern; they flow in when times are good, and leave when times are bad, just when capital is most needed (Campello, 2013; Mosley, 2003; Wibbels, 2006). Signaling credibility to investors can therefore weigh heavily on government decision-making including inflation control (Remmer, 2002; Stokes, 2001), broader macroeconomic policies (Campello, 2015), infrastructure reforms (Henisz et al., 2005), or the exact terms of governmental debt issuance (Ballard-Rosa et al., 2022). Even left-leaning governments in the region cannot resist these pressures. Newly elected presidents need to appease volatile capital markets (Brooks et al., 2022) and in some countries, they have even abandoned their original state-oriented electoral platforms to address these pressures (Campello, 2015; Conaghan, 1996; Samuels and Shugart, 2010; Stokes, 1999). Indeed, many have argued that international capital has played no small role in gradually pushing Latin America toward a more market-oriented economic model over the course of the last three decades (e.g. Huber et al., 2008; Ubiergo Segura, 2007).

Governments are acutely aware that international capital can impose significant constraints on their policy options—even if some of their messages might get lost in translation (Naqvi, 2019). If incumbents are not perceived as favorable to capital, then this investment can pack up and move elsewhere (e.g. Campello, 2013, 2015; Conaghan, 1996; Kaplan, 2013; Pinto, 2013; Remmer, 2002; Samuels and Shugart, 2010; Santiso, 2003; Stokes, 1999, 2001). For example, the former Brazilian president, Fernando Henrique Cardoso, recalls that in the 1990s, governments had to constantly reckon with the preferences of international capital owners: “If foreign investors saw that a country like Brazil was not doing enough to modernize its economy, they could turn their backs on us overnight” (Cardoso, 2006: 236).

And while we increasingly understand how governments strategically access loans (Ballard-Rosa et al., 2022; Brooks et al., 2022; Cormier, 2022) and how markets (mis)perceive governments (Ballard-Rosa et al., 2021; Naqvi, 2019), we still have very little knowledge about how governments actively manage their reputation (Mosley et al., 2020: 220). The vital signal in this game is the language and speeches used by governments to build such confidence (Santiso, 2003: 34). In fact, apart from some work on central bankers (Baerg, 2020; Morris and Shin, 2007; Myatt and Wallace, 2014), there is little scholarship exploring how governments try to convince capital that their country is a safe investment opportunity.

We build on insights from work on the constraining effects of international capital to develop a theory of how presidents use their rhetoric to respond to pressures from international capital markets (e.g. Campello, 2013; Kaplan, 2013). Exposed to the pressures of international capital, presidents use highly visible government policy messages to manage expectations. Presidents frame their speeches in a manner that makes them more compatible with markets and therefore emphasize issues pertinent to investors. In addition, presidents also change the very nature of the policies they are announcing. Once the pressure is off, however, presidents react according to the nature of the pressure. If the national currency market was under stress, presidents are still aware of the force of decentralized markets and will stick with their reform plans. If, however, the crisis was due to pressure from the credit market, presidents will announce more interventionist policies in the subsequent year.

To test our argument, we analyze the underlying economic signal in 267 annual state-of-the-union addresses of 67 Latin American presidents across 12 countries between 1980 and 2014. These high-profile institutionalized messages are a particularly apt source for our purposes; they allow us to explore the saliency attached to policy issues with structural topic models (Roberts et al., 2014) and they also permit us to scale the economic policy position of these presidents (Slapin and Proksch, 2008).

Our paper makes two main contributions. Firstly, we explore how governments in emerging markets use language and speech to play the “confidence game” (see Blinder et al., 2008; Santiso, 2003). Governments rely on speeches to carefully manage market expectations by signaling economic policy shifts and highlighting specific issue areas. In times of economic pressure, Latin American presidents emphasize the saliency of the economy and they also shift their displayed economic position toward the preferences of the market. Interestingly, once this pressure begins to dissipate, whether presidents maintain this position or shift back toward their original position, seems to be dependent on the nature of the economic pressures they faced. Currency crises compel presidents to maintain market signals even after the worst of the crisis has passed, in contrast to credit crunches.

Secondly, to isolate the economic preferences of Latin American presidents, we develop a method of automatically identifying and scaling specific sub-dimensions from political texts. Using a dictionary approach, we first detect the sections in the speeches that address economic policies and then apply the Wordfish scaling model (Slapin and Proksch, 2008) to retrieve standardized, country-specific economic policy signals on a yearly basis. Our method automates what so far has been the manual parsing of a specific sub-dimension from texts. This will help advance the growing body of work on the identification and measurement of preferences from text (Grimmer and Stewart, 2013; Lucas et al., 2015), complementing existing efforts to measure the policy position of Latin American political actors based on text (Arnold et al., 2017; Izumi and Medeiros, 2021), expert surveys, (Coppedge, 1997; Wiesehomeier and Benoit, 2009), elite surveys (PELA, 2005; Power and Zucco, 2009) and roll-call votes (Alemán et al., 2018).

The Pressure of International Capital

The policy pressures exerted on Latin American governments by the exit threat of international capital have been well documented. The collapse of Import Substitution Industrialization across the region in the early 1980s precipitated a near-uniform process of structural economic reform, which fundamentally altered the exposure of these economies to international markets (e.g. Huber et al., 2008; Santiso, 2003; Ubiergo Segura, 2007). During the 1970s, many Latin American countries accumulated a large amount of debt (Gavin, 1997), and with the budget crises of the 1980s, Latin American governments defaulted on these debts. The need to attract inward investment, combined with the lack of domestic savings, particularly during a time of low commodity prices and high US interest rates resulted in a notable increase in the political power of capital (Campello, 2015).

During periods of economic crises, when such tensions are heightened, this dependence has resulted in left-leaning presidents reneging on their previous campaign promises (Campello, 2015; Samuels and Shugart, 2010; Stokes, 1999). When faced with funding constraints from global bond markets, stimulus-minded politicians were forced to engage in cycles of austerity (Kaplan, 2013). The increasing mobility of portfolio capital has therefore placed pressure on the tax share of capital across Latin America since 1978 (Wibbels and Arce, 2003) and has exacerbated the downward effect of trade openness on welfare spending (Kaufman and Segura-Ubiergo, 2001). When economic times are good and commodity sales booming, there is no shortage of foreign exchange and governments enjoy access to bond and bank credit markets (Campello and Zucco, 2016). Investments, both in the form of direct investment and portfolio investment, enter the country but in the light of a looming crisis, the exit threat of international capital places severe pressure on Latin American governments.

International capital pressure can come in different forms, for example, in pressure on the national currency (exchange market pressure, EMP) and/or in pressure on access to the credit market (credit market pressure, CMP) (see Campello, 2013). Currency crises characterized by a depletion in a country's international reserves or a sharp devaluation of the national currency, are often driven by sudden capital flight or change in the terms of trade, such as a collapse in commodity prices, combined with speculative currency attacks (see Campello, 2013: 266; also Reinhart, 2002). Such exchange market crises matter, not only because capital inflows appear to react to them (Lipschitz et al., 2002) but they are often followed by severe recessions (Calvo and Reinhart, 2002). The loss of international reserves and the increase in foreign debt, relative to the devalued currency, and given that export-led recovery of the balance of payments is not really an option, force governments to burnish their neoliberal credentials to attract foreign currency to stave off a catastrophic collapse (Campello, 2013: 266). These crises can severely limit a government's ability to access international capital and can feed into credit crises.

Credit market crises arise when governments struggle to raise credit on international or domestic markets. For many Latin American governments, financial integration and access to credit markets has facilitated increased spending and politically induced economic booms (see Kaplan, 2013). Credit market freezes can entail large declines in the volume of transactions in primary and secondary credit markets and increases in illiquidity (Benmelech and Bergman 2017). When the risk of sovereign default is perceived as high, credit markets can be reluctant to lend to national governments, and the cost of borrowing spikes. This means that investors, concerned with default risk, insist on fiscal discipline and economic orthodoxy, and Latin American governments, keen to maintain their image as a reliable debtor and ensure access to capital, will be willing to appease their creditors (Kaplan, 2013: 7–8; also Mosley, 2000, 2003). The US government's “Brady Plan,” which restructured Latin American debt from bank loans to bond-based debt, drastically increased the power of creditors across the region, as bond holders can now rapidly dump the debt of uncooperative Latin American countries in secondary markets, forcing greater compliance with market preferences (Kaplan, 2013).

There is a strong association between debt and currency crises, particularly for emerging markets. For example, an analysis by Reinhart (2002: 11) suggested that for a developing country subgroup, the probability of having a currency crisis, conditional on having defaulted is about 61 percent while the probability of defaulting, conditional on having had a currency crisis is around 46 percent. Currency crises can quickly evolve into credit crises as sovereign ratings collapse, risk premiums increase and access to international credit diminishes (see Calvo and Reinhart 2002; Wibbels, 2006). For this reason, we consider a more general economic crisis indicator—which we call international capital pressures. Such economic crises are key for Latin American incumbents and can even be politically existential. Voters across the region tend to be highly sensitive to economic performance (Murillo et al., 2010; Remmer, 2002; Stokes, 2001) and Latin American presidents are well aware that the economy matters for electoral calculations (Johnson and Schwindt-Bayer, 2009). The link between the economy's performance and governments’ popular support has been conclusively documented across the region (e.g. Carlin et al., 2015; Echegaray, 2005; Stokes, 1996; Weyland, 2003). Not only can severe economic conditions bring protests out onto the streets (Pérez-Liñán, 2007); recessions have also been found to correlate with the early end of presidential terms (Alvarez and Marsteintredet, 2009; Hochstetler and Edwards, 2009; Kim and Bahry, 2008). Given crises’ devastating economic effect and their potential existential political threat, presidents have a clear incentive to send a strong competency signal to calm the nerves of capital.

Using Government Speeches as Economic Signals

It is no surprise then that the pressures of international capital often foreshadow comprehensive economic reforms in Latin America (Bates and Krueger, 1993; Drazen and Grilli, 1993; Remmer, 2002; Weyland, 1998). Structural economic reforms, however, are costly, politically risky, and take time to implement—time that governments often do not have in the midst of a fast-moving crisis (Broz et al., 2016; Walter, 2013). As Paul Krugman points out, “following an economic policy that makes sense in terms of the fundamentals is not enough to assure market confidence […] one must cater to what one hopes will be the perceptions of the market” (Krugman in Santiso, 2003: 26). In this context, speeches and the language used by politicians are crucially important as part and parcel of crisis management and as an efficient way to manage market expectations. Government statements can help signal the commitment to low inflation and fiscal discipline, reassure investors, and assuage their fears, which in turn can reinforce the “cognitive regimes” of market participants (Santiso, 2003: 34). Speeches offer political elites a key opportunity to build a narrative about their economic reforms. While the policies themselves define the regulatory details, speeches allow for contextualization and provide a broader picture of where they want to lead the country. In short, we expect that prominent speeches play a key role in governments’ communication. Any change in economic policy-making will always be accompanied by its respective communication. 1

Political elites are indeed highly strategic in their use of communication. For example, electoral concerns have a significant effect on how parties and members of parliament use speeches on the floor. They not only affect senators’ choice of topics (Quinn et al., 2010), but they also shape the strategic allocation of plenary time and the messages conveyed on behalf of parties (Proksch and Slapin, 2012, 2015). Parties and presidents use speeches to manage coalitions (Arnold et al., 2017; Martin and Vanberg, 2008) and individual parliamentarians distinguish themselves from the party brand on the basis of their rhetoric (Maltzman and Sigelman, 1996). Governments also rely on highly visible communications that highlight their economic policy to manage and shape the expectation of markets on a regular and fine-grained basis (Baerg, 2014). After all, even moderate increases in uncertainty about debt overhang may lead to a complete stop of further capital supply from risk-averse creditors (Aizenman and Marion, 2001). For economic elites, such as central bankers, communication constitutes a key means to manage expectations (Baerg, 2020; Blinder et al., 2008). They resort to different communication channels (Reis, 2013), appeal to specific sectors rather than to the whole public (Morris and Shin, 2012) and sometimes even deliberately choose an optimal level of obfuscation in their communication (Morris and Shin, 2007; Myatt and Wallace, 2014).

Latin American presidents use important speeches to manage the expectations of investors in a similar vein, particularly during periods of economic downturns. Faced with pressures from international capital, presidents make use of their speeches to outline their policy responses, strategically addressing the now salient preferences of capital owners as part of the “confidence game.” They do so by cultivating the approval of a relatively small and insular financial community (Santiso, 2013) and by trying to counter capital flight through their commitment to economic stability, openness, and credibility (Calvo et al., 1996).

In this sense, presidents can use their speeches to send signals in two different, albeit related, ways: Saliency and subject matter. Firstly, in light of international capital pressures, presidents should devote more attention to economic policy areas—to the detriment of other topics. Assuming that capital prefers certain economic environments, such as stability, low taxation, openness, labor flexibility, and policies designed to stimulate growth, over others (Calvo et al., 1996), in their speeches, presidents will signal that the economy is their priority. Secondly, the subject matter of their speeches will also shift, and some topics should suffer to the detriment of others. For example, even though incumbents might be under pressure to highlight some form of compensatory mechanism to mitigate the impact of the crisis on their citizens (e.g. Garrett, 1998), they will try to strike a balance by emphasizing social policy areas that have an explicit link to the competitiveness of the economy. Focusing on topics related to the advancement of human capital via areas such as health or education ties these issues to the nation's economic wellbeing, while diminishing the space available to address traditional welfare topics (Avelino et al., 2005). Hypothesis 1: Faced with international capital pressure, presidents devote more attention in their speeches to the economy.

Highlighting the saliency of certain topics germane to the interests of capital, however, is only one part of the “confidence game.” Crisis situations, particularly in emerging markets, will make investors fear a backlash against the market model, which could include the risk of nationalization or default (Büthe and Milner, 2008; Leblang and Satyanath, 2006). Incumbents, therefore, need to send a strong and convincing signal to capital that they are pursuing an orthodox approach to recovery and are protecting investments. Presidents will not only emphasize the economy in their speeches; they will also signal a shift in their overall economic policy toward the preferences of capital: Hypothesis 2: Faced with international capital pressure, governments adopt more market-oriented economic positions.

Data and Models

To test our hypotheses, we rely on a corpus of 276 state-of-the-union speeches from 67 presidents in 12 Latin American countries (1980–2014). State-of-the-union speeches are a particularly apt source for our purpose, because they represent important building blocks of political communication and strategic position taking. As highly institutionalized events, these speeches are one of the most salient speeches a president can give, and typically, these addresses are covered by domestic news and by the international financial media. State-of-the-union speeches are therefore particularly well suited to address international market concerns by calibrating the saliency of specific topics and the accentuation of the nature of specific economic policies.

Table 1 summarizes our sample of state-of-the-union addresses. We build on Arnold et al. (2017), who collected these presidential speeches in 12 Latin American countries from websites and archives, covering the time period from the moment of each country's redemocratization until 2014 2 Before analyzing the corpus, we pre-process the text, removing accents, turning all text into lowercase, reducing words to their stems, and subtracting Spanish stop words 3 and any word that is related to the transcription of the speech.

Countries and time period under consideration. Data from Arnold et al. (2017).

Measuring Topics

We study the effect of economic crises on the choice of topics in the state-of-the-union speeches with a structural topic model (Roberts et al. 2014). Building on Blei et al. (2003) who introduced latent dirichlet allocation to model each document in a corpus as a finite mixture over an underlying set of topics, their extended model allows the mix of topics in each document (topical prevalence), and the words used in each topic (topical content) to depend on covariates.

We let topical prevalence covary with each president, capturing idiosyncratic preferences about the topics a president cares about. In addition, topical prevalence also depends on the general indicator for pressure from international capital, since we want to study whether times of economic duress go hand-in-hand with a different topic composition. In addition, we expect that topical content—the choice of words to describe a topic—will change during years of international capital pressure. We estimate the structural topic model using the complete corpus of all 276 speeches. Our analysis shows that 34 topics are a good fit for the data with national development being the most popular baseline topic in the corpus. 4

Measuring Economic Policy Positions in Three Steps

We are, however, not only interested in issue attention, but also in the economic policy positions presidents announce. While there have been recent advancements in identifying the positions of Latin American presidents on a general left–right scale (Arnold et al., 2017; Power and Zucco, 2014), positions on particular policy sub-dimensions over a continuous period of time have proven much more difficult to measure. To retrieve economic policy positions, we preselect those text passages and then use the Wordfish scaling model to quantify the latent ideal point (Slapin and Proksch, 2008). Given the size of our corpus, reading, and hand-coding hundreds of presidential speeches seemed prohibitive. We therefore develop an algorithm that takes over this task in three steps. 5

First, we determine key terms in economic policy making (Dictionary Step). Dictionaries have been widely used in Political Science and are a well-established tool to study political ideologies (Burden and Sanberg, 2003; Kellstedt, 2000; Laver and Garry, 2000; Rooduijn and Pauwels, 2011; Young and Soroka, 2012), to identify documents that relate to a certain topic (e.g. Beauchamp, 2017; King et al., 2013; Puglisi and Snyder, 2011), or to scale preferences (e.g. Eshbaugh-Soha, 2010; Ho et al., 2008). We, in contrast, want to identify the passages in each document that deal with a particular policy area. With the goal of choosing terms that unequivocally identify economic policy-making, we take our economic keywords from Laver and Garry (2000), from The Economist's list of Economics A-Z terms 6 and from party manifestos 7 and translate them into Spanish.

In the second step, we then use these words to deterministically identify the relevant passages on economic policy (Identification Step). When presidents speak about the economy, they do not change topics after each sentence, but address policy issues in one or more paragraphs at a time. Using this insight, we search for clusters of keywords to identify the relevant passages. The algorithm “learns” to select an optimal area around the economic keywords from a randomly chosen and manually annotated training set. Minimizing misclassification, the algorithm identifies a text string of length l around a given word i for a certain number of different terms m from our dictionary, and then defines n terms in the vicinity of the word i as belonging to economic policy making.

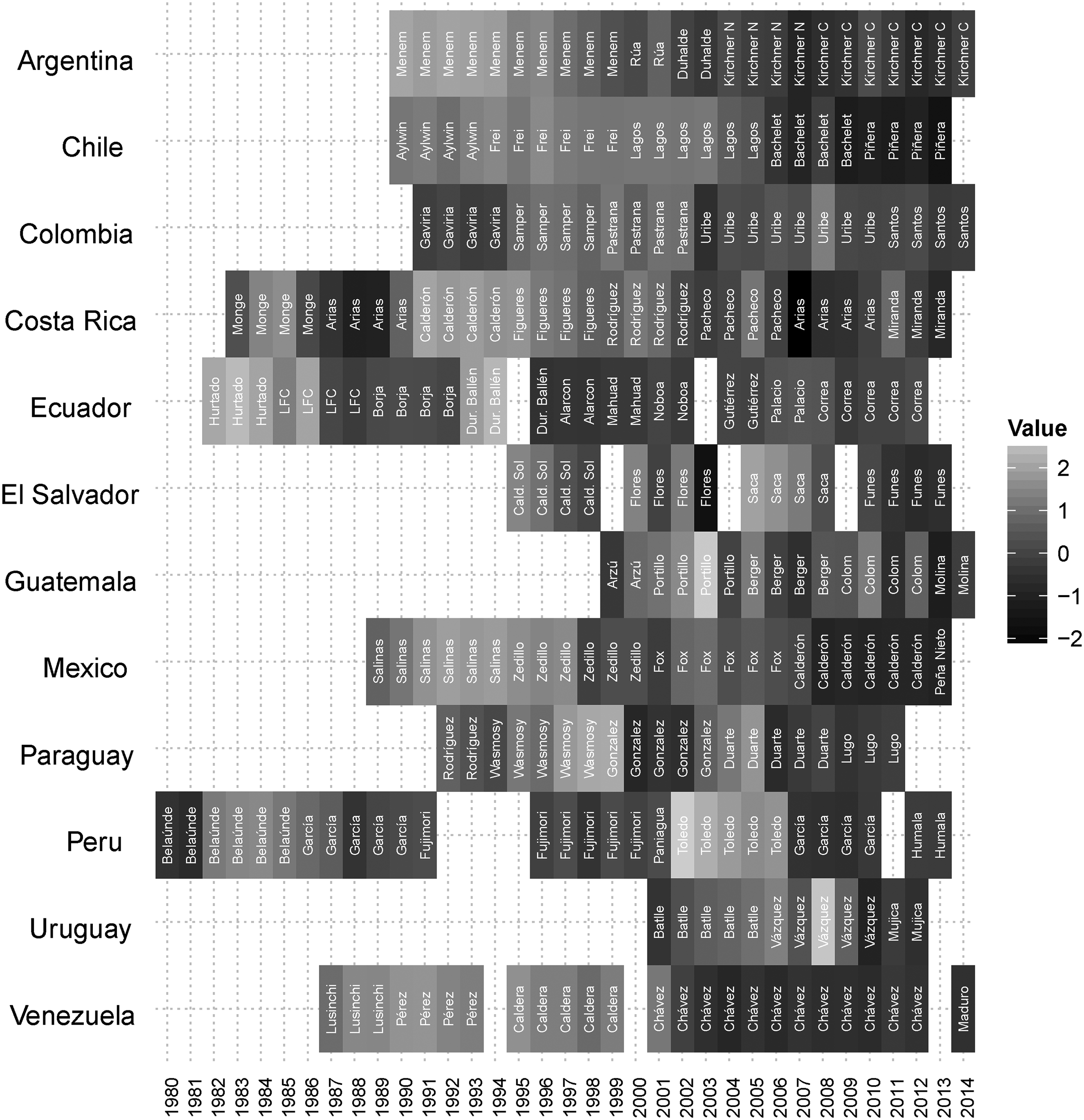

Finally, using the identified passages on economic policy making, we measure the economic position (Scaling Step) with the Wordfish model (Slapin and Proksch, 2008). Estimating a separate model for each country, we retrieve a standardized, latent position of each speech on economic policy making. 8 Presidents’ displayed preferences for economic policy are comparable within, but not across countries. Figure 1 reports results. More state-oriented economic preferences are depicted in darker gray and more market-oriented economic preferences are in lighter gray. The results are in line with substantive knowledge about Latin American politics, be it the evidence for the pink tide in the new millennium or the positions of well-known individual presidents like the Kirchners in Argentina, Hugo Chávez in Venezuela, or the more moderate social democrat Michelle Bachelet in Chile. Álvaro Uribe in Colombia is a particularly interesting case. The main ideological dimension in Colombia strongly relates to security concerns and Uribe is typically considered a conservative politician on this main dimension (Arnold et al., 2017). We find, however, that his economic policies are much more moderate and place him on a scale more toward the average economic position of his colleagues (within Colombia).

Economic positions of Latin American Presidents (Countrywise z-scores). More market-oriented announced economic policy positions with lighter shading; more state-oriented announced economic policy positions with darker shading.

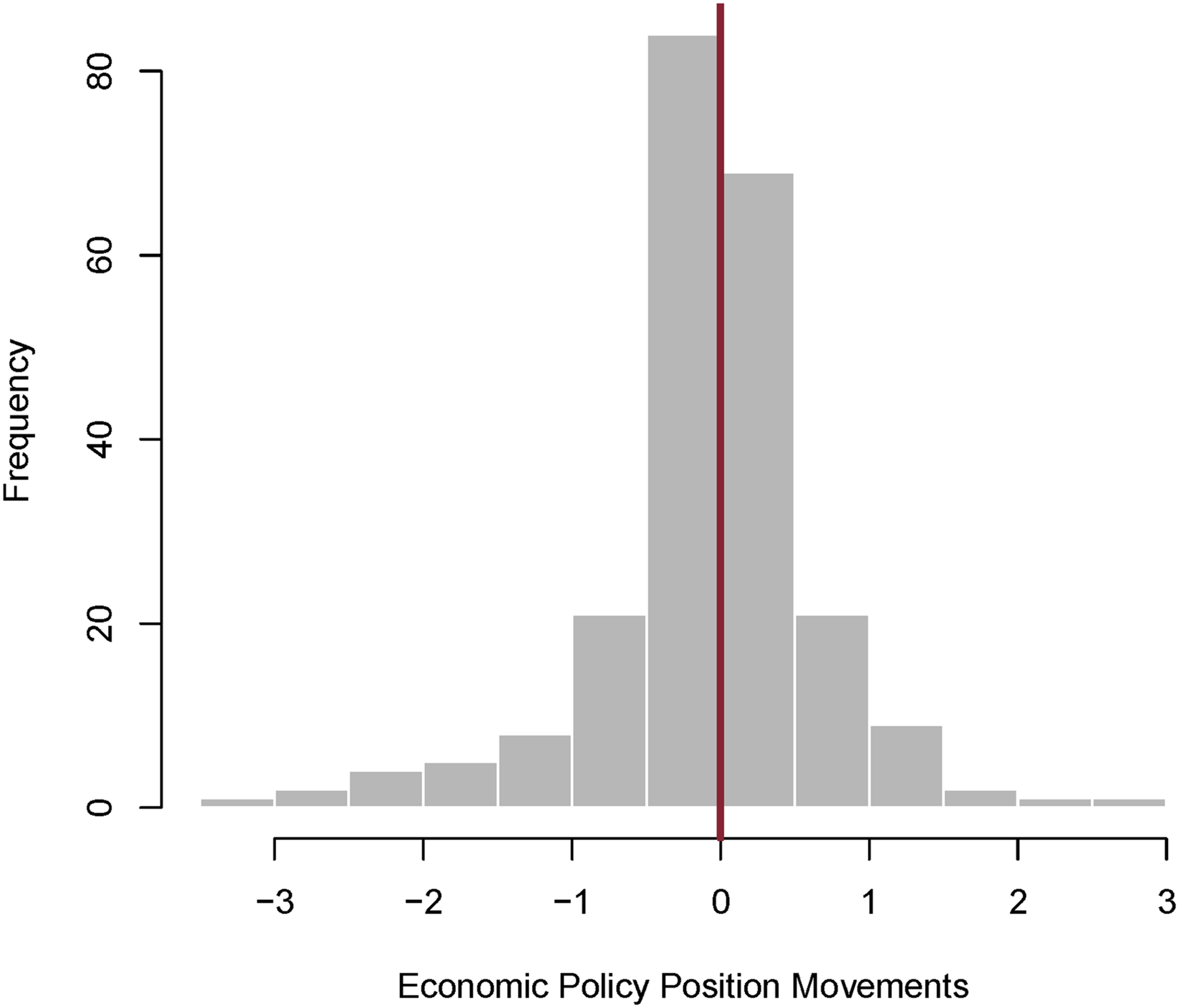

We can now also measure the size and ideological direction of policy movements along this economic dimension by calculating the difference between time t and time t−1 for each individual president. 9 Figure 2 provides a general overview of presidential shifts in economic preferences for our sample of 67 presidents. Negative values represent moves toward more state-oriented economic policies, while positive values represent moves toward more market-oriented policies. In a large proportion of cases, we can observe only small shifts in presidents’ economic policy positions. But not all policy movements are unidirectional. In fact, there are slightly more shifts to the economic left in our data, as there are to the economic right. Finally, not all policy movements are of the same magnitude. Some are very small indeed, while others represent significant jumps to either side of the economic left or right.

Shifts in announced economic policy positions.

Measuring International Capital Pressure

Our theory centers on the pressure international capital is exerting on governments. Given the complex relationship between credit and currency crises, for our main proxy for international capital pressure, we follow Campello (2013) and Eichengreen et al. (1995) and use a measure of EMP:

10

We also use a second proxy, which combines a measure of CMP with our measure for EMP to create a more general measure of international capital pressure. For this, we build two indicators—a bank pressure index and a bond pressure index. This is based on public and publicly guaranteed debt from bonds that are either publicly or privately placed and private and publicly guaranteed commercial bank loans from private banks and other private institutions. This data comes from the World Bank's Development Indicators. We take the annual change in the bond and bank-lending as a percentage of GDP for each country and weight these annual changes with their respective standard deviations. We code CMP as 1 for any year with a severe credit crunch in either the bond markets or the banking sector. International capital pressure then takes the form of 1 for any year where there is either a currency or credit crisis and 0 otherwise.

Analysis of Presidential Speeches

We expect that presidents will tailor the saliency, and the subject matter, of their speeches during times of heightened international capital pressure. For example, in March 2016, former Argentine president, Mauricio Macri, was compelled to discuss the legacy of Kirchnerism and Argentina's loss of economic credibility on the international stage. 11 In a similar vein, in his 1998 state-of-the-union address, Mexico's Ernesto Zedillo defended budget cuts in the light of pressures from international capital. 12 And in 2002, his successor, Vicente Fox, advocated for free-market reforms in his annual speech, stressing economic and political stability even in times of austere economic policies. 13

Presidents Highlight Economic Topics

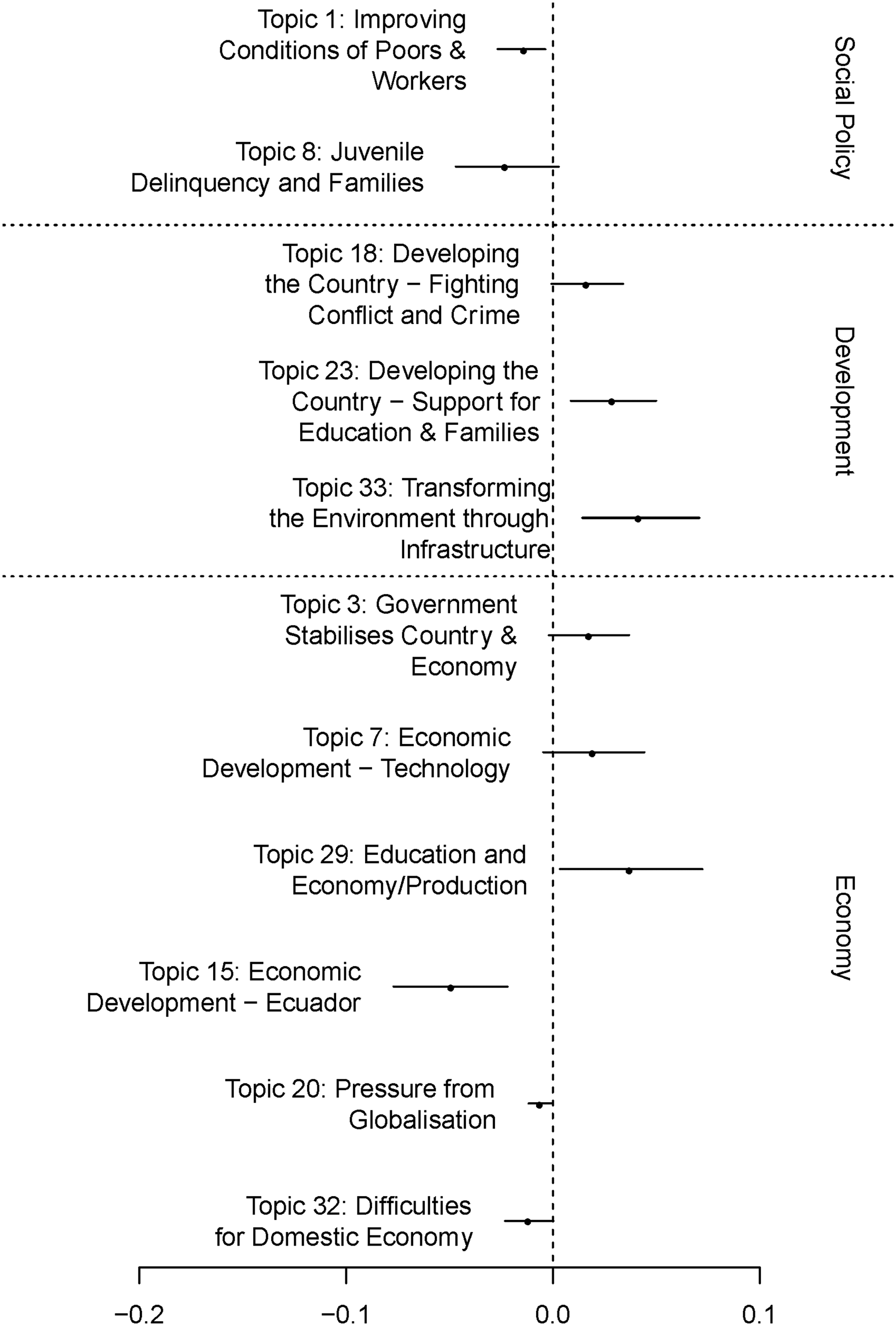

So, what are the issues that Latin American presidents highlight in their speeches during economic crises? While the model overall defines 34 topics, only eleven of these topics appear salient during times of crises. 14 Figure 3 depicts all topics for which we find a systematic difference in topic proportions between a year with pressure from international capital and a year without such pressure. The point estimate is represented with a circle, while the bar indicates uncertainty at the 90 percent confidence level. In the light of pressure from international capital, the two social policy topics—improving conditions of the poor and of workers, and juvenile delinquency—receive less attention in presidential speeches. Instead, presidents stress the development of the country. The fight against crime, supporting education and families, transforming the environment and building infrastructure are repurposed for the economic well-being of the nation. With regards to the economy, presidents systematically talk more about stabilizing the country, developing the economy through technology and increasing productivity through investment in education. Presidents avoid talking about pressures from globalization and about (general) difficulties for the domestic economy.

Expected shifts in topic proportions in state-of-the-union speeches from years when Presidents are exposed to international capital pressure. Figure shows only topics finding systematically different attention. Confidence level at 0.9.

We can contrast the most frequent word usage of presidents in their state-of-the-union addresses during years with pressure from international capital and compare them with years without pressure (Table 2). During the years we identify as in economic crisis, the core vocabulary of presidents relates to economic hardship, indicating that incumbents do indeed react to difficult economic times.

Typical terms during years with pressure from international capital and years without pressure from international capital. Calculation based on Structural Topic Model.

These findings are in line with our theoretical expectations and corroborate H1. Exposed to economic pressures, presidents tone down all social policy topics. Yet, if such policies can be tied to developmental issues as, for instance, building human capital (topic 23 and topic 29), the topic receives more attention. Fighting conflict and crime (topic 18) receives attention if it has a clear link to the development of the country. Even if a topic is likely to go hand-in-hand with an expansion of the state—such as transforming the country's infrastructure (topic 33)—presidents will pay it more attention if it helps emphasize the competitiveness of the economy. In sum, presidents stress those topics that are in line with what international capital owners want to hear.

Economic Positions and Pressure from International Capital

To study presidents’ announced shifts in economic policy making, we run a regression analysis of the policy changes in a given year on our different proxies for international capital pressure. We also add controls for different substantive mechanisms and fixed effects for years and countries. To account for potential political business cycles, we consider executive or legislative elections in a given year. The percentage of seats held by the executive's party in the legislature is an indicator of presidential legislative strength while the average age of political parties serves as a proxy for the stability of the political environment (Beck et al., 2001). We further control for constitutional prerogatives using a measure of presidential power (Doyle and Elgie, 2014). Finally, GDP growth from the World Bank's World Development Indicators reflects the state of the economy. 15

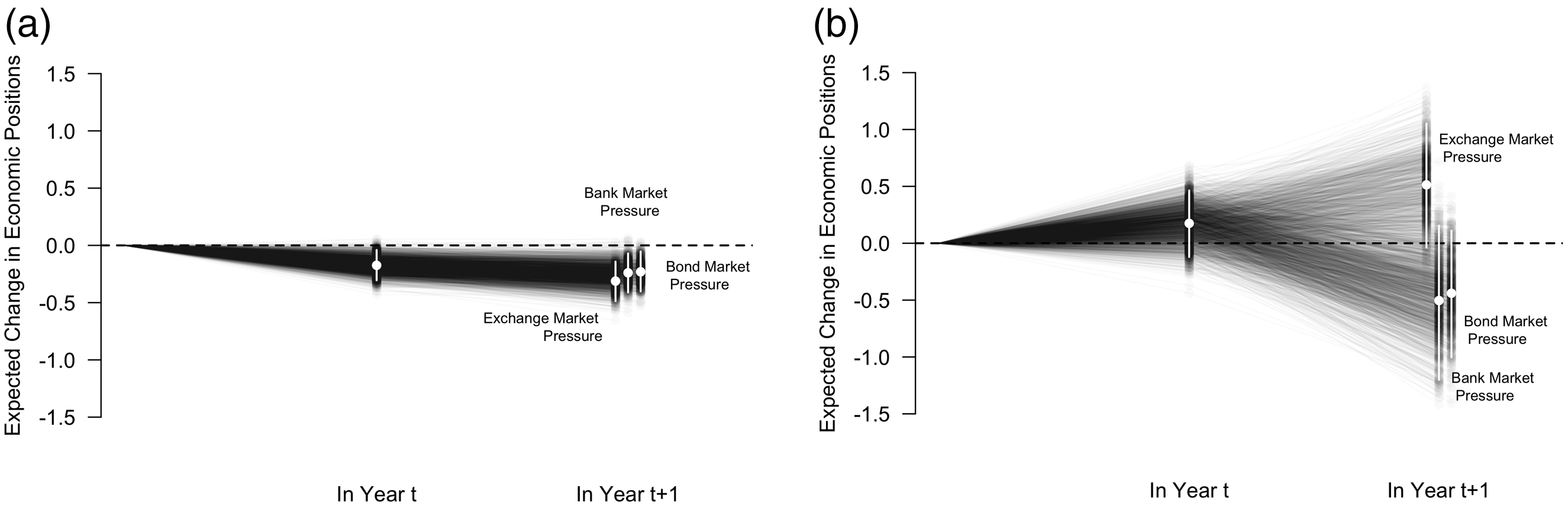

We summarize our main findings in Figure 4(a) and (b), which show the expected values for policy shifts based on sampling from the final regression equation (King et al., 2000). 16 The first data point at time t indicates how presidents shift their position in years without pressure from international capital (Figure 4(a)) and with pressure from international capital (4b). The second data point at time t + 1 displays presidents’ expected movement the year after. To illustrate the second year, we take a randomly chosen expected value of a policy shift from the first year as starting point and then add an expected value of a policy shift for the second year. Note that we distinguish between the different possible origins of international capital pressure, i.e. EMP, bank market pressure and bond market pressure.

Expectedshifts in the announced economic positions during international capital pressure. confidence level in White at 0.95. Mean expected shift as the White point. (a) Without crisis. (b) During and after a crisis.

Figure 4(a) shows presidents’ expected movement without crises. As a default, presidents move slightly toward more state-oriented policy positions—and this persists into the second year. Things look different in years with international capital pressure. Presidents then tend to move toward more market-oriented economic policies. Their reaction during the year after the crisis depends on the nature of the pressure. If the pressure comes from the exchange market, then policies in the year after the crisis are even a bit more market oriented. In contrast, after CMP, presidents announce more state-oriented economic policies. While this proves to be the case for both bond and bank-based pressure, this effect is more dramatic for the latter. In short, the legacy of crises depends on the type of economic pressure. EMP would appear to compel presidents to continue to send market friendly economic signals even after the moment of capital pressure has passed. The effects of CMP are more fleeting. Once access to credit has been secured, presidents revert to more expansionary policies. 17

Why might this be so? We don’t have a definitive answer but perhaps work by Kaplan (2013) can offer some insights. Kaplan (2013) has argued that when foreign debt is largely comprised of bank loans, each bank has a very high stake in the future solvency of the borrower, and they continue extending lifelines to the borrower to prevent a default. Banks therefore give rise to a moral hazard problem and allow stimulus-minded politicians to expand the public economy in line with traditional political business cycles (Kaplan, 2013: 46–47). Currency markets, on the other hand, constantly monitor and evaluate the actions of the government and such crises often result in a severe recession (Calvo and Reinhart, 2002). This may render the effects of such crises more enduring. With a looming currency crisis, and subsequent recession, governments may have to tread carefully as they will be eager not to lose the support and trust of international capital. After a loan crisis, if presidents can access credit once again, they may feel less constrained to continue signaling to the market and so have the freedom to shift back toward more state-oriented economic policy-making in line with the preferences of the electoral constituency. While international capital pressure in different forms will force governments to signal market-friendly positions in the immediate wake of these crises, not all crises will have the same effect on the endurance of these signals.

Meaningful Economic Signal or Hot Air?

Our empirical analysis indicates that Latin American presidents tailor their economic signal depending on the circumstances facing their country. But are these signals actually meaningful? If presidents are using these speeches to signal to markets, then we might anticipate these signals would be noticed—otherwise, they are just hot air. We do think that markets will react to these speeches. To establish this empirically, we would need to be able to isolate which aspect of the international capital markets is accurate to examine and secondly, we would have to try and account for the positive signal that markets may already have inferred from the administration. That is, by the time the speech is delivered, the anticipation of a positive economic shift might already be baked into market movements.

One thing we can do, however, is explore how the international financial media responds to these speeches. There are numerous studies demonstrating that markets react to international media (e.g. Alomari et al., 2021; Capelle-Blancard and Petit, 2019; Zhang et al., 2016). If these speeches cause reactions in the financial press, then this might translate to actual market responses. 18 To explore the effect of these speeches on the financial media, we analyze stories from the Reuters Financial News Collection (n = 106,521), spanning the period from 2006 to 2012 (Ding et al., 2014). From this text corpus, we collect all news stories that carry the name of the country, the name of any president, the word “message”, or the word “president” and then we select those news articles that have at least two of these terms during the 90 days before until the 90 days after the respective state-of-the-union speech.

We take a straightforward dictionary approach to measure the financial uncertainty of the financial newswire from Reuters. The starting point are all articles that we selected with our keywords. Aggregating all articles from the same day and using the dictionary from Loughran and McDonald (2011), we then count how many terms expressing uncertainty go out via the Reuters news wire each day. Across the 180 days in the 11 countries over eight years, we can measure the daily financial uncertainty with regards to a particular country on 6263 days. As any count variable, our uncertainty measure is right-skewed and has a minimum of zero, a maximum of 154, a median of nine, and a mean of 12.07.

With this data, we then estimate the local average treatment effect (LATE) of the state-of-the-union speeches on the uncertainty expressed in the international financial media. We implement the non-parametric regression discontinuity design (RDD) framework (Calonico et al., 2014; Cattaneo et al., 2019), and use the date of the speech itself as the discontinuity. Speeches displaying a more market-friendly position should be received differently from those speeches that take a more state-oriented stance. To distinguish between more state-oriented messages and more market-oriented messages, we divided our sample on the grounds of a countrywise median of the preferences for economic policy-making expressed in the speech. 19 In addition, we also investigate the effect of crises. We thus calculate the LATE in six different samples. We distinguish between media reactions to all market-oriented speeches vs. media reactions to all state-oriented speeches. We also further subset each of these data sets and consider speeches that were given during a year of financial crisis vs. a year without any financial crisis. We then analyze the RDD designs for each of these six scenarios with financial uncertainty as our dependent variable.

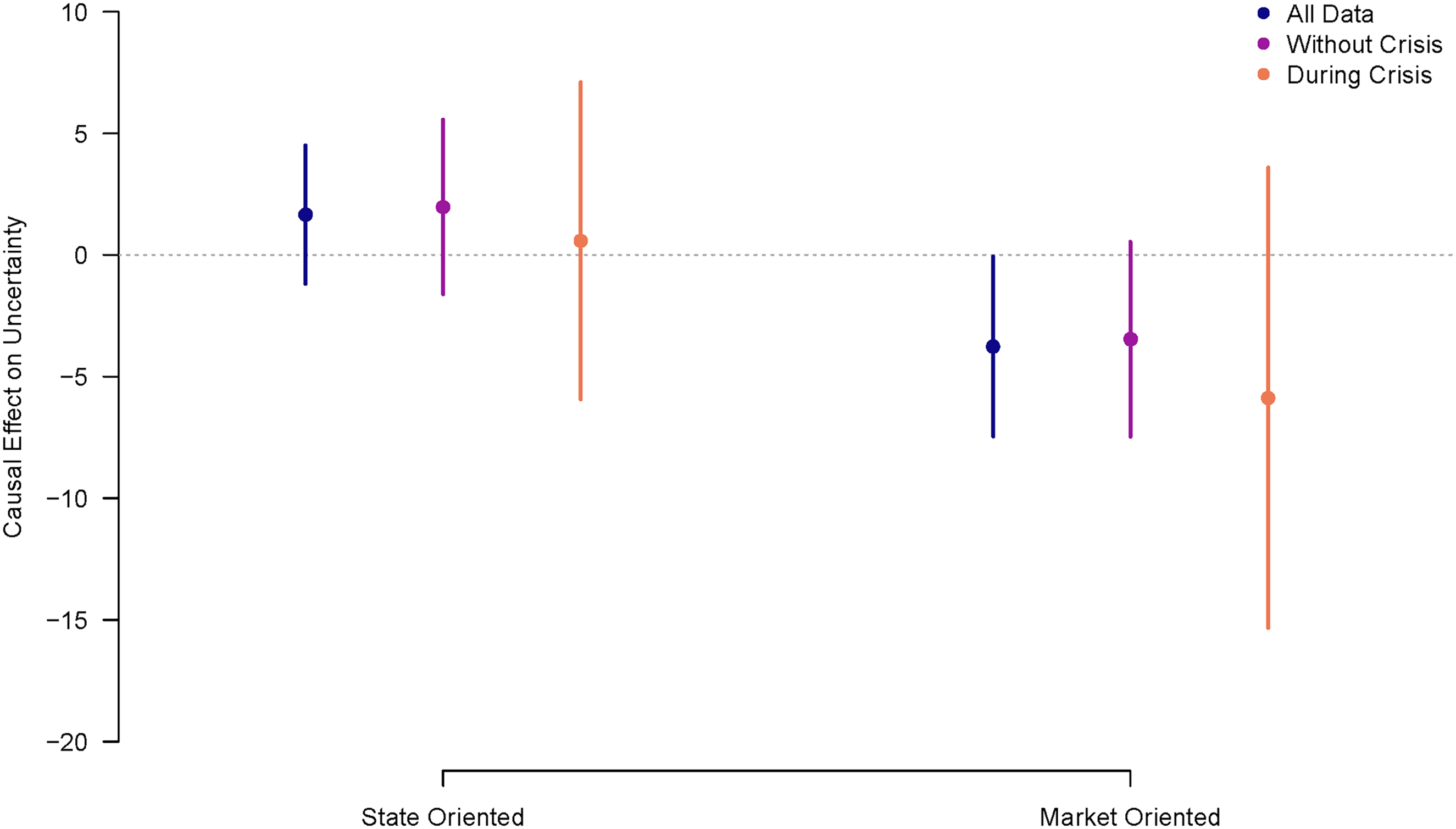

Figure 5 summarizes our findings. 20 A speech in which presidents announce state-oriented economic policies on average tends to slightly increase the uncertainty in the international media. However, this effect is not distinguishable from zero on statistical grounds. In contrast, speeches that are explicitly making the case for a market-oriented economic policy decrease media uncertainty. While the point estimates for the complete data set and the data on the years that are not in crisis show a similar reduction in uncertainty, the point estimate is the strongest during years of economic crisis. The effect for the complete data is distinguishable from zero at 95 percent confidence level. When splitting the sample, the reduced sample sizes naturally increase the margin of error, but the substantive message remains the same and the results are in line with our theoretical expectations. If a speech conveys a state-oriented economic policy platform, there is no effect from a presidential speech. But presidents do indeed manage to smooth the markets with their speeches when they announce more market-oriented economic policies, effectively reducing the anxiety among international investors. When presidents signal more market-friendly positions or signal a move toward more market-friendly positions, then this results in lower levels of uncertainty in the international financial press.

Causal effects from the state-of-the-union speeches on the uncertainty expressed in articles on the respective countries in the reuters financial news corpus. Data covers 2006–2012.

Conclusion

Previous work has provided us with important insights into the economic (Remmer, 2002; Stokes, 2001), political (Samuels and Shugart, 2010) and international (Campello, 2013; Kaplan, 2013; Pinto, 2013) pressures on economic policy making in new democracies. But while we know that international capital imposes significant restraints upon governments, we lack theoretical and empirical understanding of how exactly governments manage expectations from capital owners (Mosley et al., 2020).

In this paper, we argue that rhetoric is a fundamental tool of risk management for presidents. Using a text corpus of 276 state-of-the-union speeches from 67 presidents in 12 Latin American countries from 1980 to 2014 we examine how these governments use highly visible speeches as a signaling device, to reassure international capital owners in times of economic duress, when the threat of capital flight and credit shortages are highest.

To isolate the economic signal presidents send, our study showcases a method to automatically extract sub-dimensions in texts. Scaling preferences on a more fine-grained level further diversifies the already existing toolkit for the analysis of political text (e.g. Grimmer and Stewart, 2013; Laver et al., 2003; Laver and Garry, 2000; Slapin and Proksch, 2008). With our novel method, we overcome empirical obstacles by providing the first cross-national time-series data on announced economic policy preferences in 12 Latin American countries since their redemocratization.

Our results show that presidents adjust the salience of topics in their speeches, but also shift their policy positions in response to the pressures of international capital during times of crises. Firstly, executives emphasize topics that directly appeal to capital holders. They tone down mentions of compensatory social policies and repackage such topics as a means for economic development. Fighting crime, support for education and families, and investments in infrastructure, for example, are forms of social policies, but when times are dire they are disguised as economic policy and productive investment.

Secondly, in an effort to secure the confidence of capital and to maintain access to credit, Latin American presidents shift their economic policy positions toward market-friendly policies. Interestingly, we find that the durability of these signals is dependent on the form that these economic pressures take. When they stem from exchange markets, Latin American presidents continue to signal to international capital, even after the crisis has waned. In contrast, when such pressure was exerted by credit markets and a credit crunch has passed, Latin American presidents use their renewed access to credit to shift their economic signal back toward redistributive and state-oriented economic policies.

The dynamics we describe in this paper further qualify the debate on economic policy switching in Latin America (Campello, 2013; Kaplan, 2013; Pinto, 2013; Remmer, 2002; Samuels and Shugart, 2010; Stokes, 2001). Presidents can signal a shift in economic position before such a shift materializes and they can do so even without a related shift in actual policy. Speeches may therefore be a cheap way for a government to cushion the blow of economic crises. Nevertheless, such a strategy may run the risk of gambling away the trust that governments are trying to build vis-à-vis actors with convincing exit options. Of course, given that Latin American presidents are directly elected, and their popular mandate is usually related to their pre-election pledges, such shifts in policy positions in response to exogenous and unaccountable actors may in turn undermine the quality of representation (e.g. Conaghan, 1996; Johnson and Schwindt-Bayer, 2009). In this sense, our findings also add to the discussions around the so-called left turn (Baker and Greene, 2011; Murillo et al., 2010; Roberts, 2015) and to more recent debates about voters’ capabilities of attributing responsibility for economic performance (Campello and Zucco, 2016; Hellwig and Carlin, 2020; Zucco and Campello, 2020). The relationship between these speeches, actual changes in economic policy and economic outcomes is an important but complicated one. It is beyond the scope of this paper and we leave it for future research to explore.

The focus on appeasing the fears of international investors above other concerns may come with normative implications, above and beyond new democracies. The Latin American populist experience rooted in a crisis of representation merely preceded the European populist turn marked by the Great Recession and a lack of responsiveness toward the median voter (Clements et al., 2018). It is no surprise that the (rather timid) calls for a renewed Bretton Wood system to reign in the primacy of the financial sector, which were unheeded at that time, were gaining prominence in the crisis triggered by the Covid-19 outbreak. Our results underscore the power that exchange markets in particular are able to exert on otherwise sovereign governments.

Supplemental Material

sj-docx-1-pla-10.1177_1866802X231210581 - Supplemental material for How Presidents Answer the Call of International Capital

Supplemental material, sj-docx-1-pla-10.1177_1866802X231210581 for How Presidents Answer the Call of International Capital by Christian Arnold, David Doyle and Nina Wiesehomeier in Journal of Politics in Latin America

Footnotes

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.

Supplemental Material

Supplemental material for this article is available online.

Notes

Author Biographies

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.