Abstract

Keywords

Introduction

The relationship between Corporate Social Responsibility (CSR) and firm value has been a focal point of scholarly debate, yielding diverse and often conflicting results.1–5 Understanding how CSR initiatives affect firm value is crucial for managers and investors, with many stakeholders increasingly concerned about corporate activities’ ethical and societal impacts. On the one hand, CSR is viewed as a strategic tool that can enhance corporate reputation, 6 mitigate operational risks, 4 and drive long-term financial performance.7,8 Conversely, critics contend that the costs associated with CSR may outweigh its benefits, potentially diverting resources from core business operations and harming firm value. 9

Previous studies have explored the linear relationship between CSR and firm value, often with contradictory findings. For instance, some research suggests a positive relationship, where CSR activities lead to increased company value through improved stakeholder relations and stronger market positioning. Garousi et al. 10 demonstrated that investors, aware of a company’s social responsibility rating, can make more accurate estimations of the firm’s fundamental value. In other words, investor estimations without awareness of the responsibility rating and using traditional financial statements overestimate (underestimate) the company’s essential value when social responsibility performance is negative (positive). Consequently, social responsibility carries informational value and constitutes a part of the relevant information in investors’ decision-making.

Similarly, Chung et al. 2 documented that CSR activities enhance firm value. In contrast, other studies indicate a negative or insignificant relationship, attributing this to the private costs and managerial distractions associated with CSR activities. Hajiha and Sakeri 11 found no significant relationship between social responsibility and firm value. Furthermore, Servaes and Tamayo 5 and Hu et al. 12 revealed a negative relationship between CSR and firm value. However, emerging evidence points towards a more complex, nonlinear relationship, where the impact of CSR on firm value may vary depending on the level of CSR engagement. In this regard, the findings of Chen and Lee 13 suggest an asymmetric relationship between social responsibility and firm value.

Despite extensive research, the intricacies of the CSR-firm value relationship remain poorly understood, particularly across different economic contexts. Most existing studies have predominantly focused on developed markets, creating a gap in understanding how CSR affects firm value in emerging economies. This study addresses this gap by investigating the relationship between CSR and firm value in Iran, an emerging market with unique economic and regulatory characteristics. Thus, this paper aims to examine both the linear and nonlinear effects of CSR on firm value, employing a Panel Smooth Transition Regression (PSTR) model to capture potential nonlinearities in this relationship. These contrasting perspectives are also explained through theoretical foundations in this study. The PSTR model allows for a more nuanced analysis, acknowledging that the impact of CSR on firm value may not be constant across different levels of CSR engagement. By examining the CSR-firm value relationship within the Iranian context, this study contributes to the broader literature. It provides insights into how CSR practices influence firm value in emerging markets. The findings are expected to have practical implications for managers, policymakers, and investors, assisting them in navigating the complexities of CSR strategies and their financial consequences.

In summary, this study seeks to reconcile the conflicting findings of previous research by adopting a nonlinear approach to understanding the CSR-firm value relationship. Subsequent sections will elaborate on the theoretical underpinnings, research methodology, and empirical analysis that guide this inquiry.

Literature review

Corporate Social Responsibility (CSR) is a strategic approach in the modern business world, signifying companies’ commitment to engaging in activities that serve economic interests and address social welfare and environmental protection. 14 This concept has increasingly garnered attention in recent years and has become a key factor in determining brand image and corporate credibility. Companies committed to social responsibility typically strive to positively impact society and the environment, considering initiatives such as supporting social projects, reducing greenhouse gas emissions, and improving employee working conditions. 15 From a positive perspective, companies investing in CSR generally benefit from increased customer loyalty, attracting new investors, and improving stakeholder relationships. 7 These factors can enhance the company’s financial performance. 16

Conversely, rival perspectives highlight the negative impacts of social responsibility on corporate value. The private cost hypothesis suggests that investing in CSR may divert resources from the company’s core operations, potentially leading to decreased profitability. 17 In other words, the costs associated with CSR initiatives can adversely affect the company’s financial performance and competitiveness. 18 The literature on the relationship between Corporate Social Responsibility (CSR) and firm value has been extensive, yet the findings remain inconclusive and often contradictory. Scholars have debated whether CSR initiatives enhance firm value or impose additional costs that may detract from it. 19 This section reviews the critical theoretical perspectives and empirical findings related to CSR’s linear and nonlinear impacts on firm value.

The Social Impact Hypothesis, initially proposed by Cornell and Shapiro 20 and supported by Nollet et al. (2016), posits that strong social performance leads to better financial performance. This hypothesis is grounded in the idea that CSR activities can enhance a firm’s reputation, reduce business risks, and foster stronger relationships with stakeholders, ultimately driving long-term financial gains. 7 Empirical evidence supporting this view includes studies by Greening and Turban 21 and Chung et al., 2 who found that firms with robust CSR practices tend to attract more investment and, therefore, improve operational performance and increase market value.22,23 According to the Social Impact Hypothesis proposed by Cornell and Shapiro 20 and based on the presented evidence, it can be concluded that the realisation of corporate social responsibility (CSR) reduces adverse events within the company, thereby enhancing financial performance and firm value. Jo and Harjoto 24 demonstrated that CSR can increase a company’s market value. Additionally, Giuliano et al. 25 showed that CSR enhances both firm value and productivity. Furthermore, Salehi et al. 16 indicated that corporate social responsibility directly relates to the company’s future financial performance.

However, the Private Costs Hypothesis challenges this optimistic view by arguing that CSR activities often entail significant costs that may outweigh their benefits. Becchetti et al. 26 and Wang 27 contend that investing in CSR can divert resources away from a firm’s core operations, leading to reduced profitability and competitiveness. Aupperle et al., 28 Servaes and Tamayo, 5 and Hu et al. 12 provide empirical support for this perspective, showing that the financial burden of CSR initiatives can lead to diminished firm value, especially when the costs of such initiatives exceed the associated benefits.

In addition to the private costs, the Management Deception Hypothesis and the Focus Hypothesis offer further explanations for the potential negative impact of CSR on firm value. The Management Deception Hypothesis, rooted in agency theory, suggests that managers may use CSR to advance their personal interests rather than those of shareholders. This can result in resource misallocation and a decline in firm performance over time.29,30 On the other hand, the Focus Hypothesis argues that the shift in focus required to engage in CSR may detract from a firm’s primary objective of maximising shareholder value. Becchetti et al. 26 and Goel and Takor 31 found that firms investing heavily in CSR may incur substantial operational costs, leading to lower profitability and a decline in market value, particularly in the short term.

The existing literature also suggests that the impact of CSR on firm value is not always linear. Chen and Lee 13 have identified a nonlinear relationship between CSR and financial performance, often described as an inverse U-shaped curve. These studies suggest that while moderate levels of CSR can enhance firm value, excessive investment in CSR may lead to diminishing returns. For example, Chen and Lee 13 found that CSR positively affects firm value only after reaching a certain threshold, beyond which the costs of additional CSR activities outweigh the benefits.

The present study builds on this body of literature by exploring the nonlinear relationship between CSR and firm value within the context of the Iranian market, employing a Panel Smooth Transition Regression (PSTR) model. This approach allows for identifying potential threshold effects in the CSR-firm value relationship, offering a more nuanced understanding of how different levels of CSR engagement impact firm value. The findings of this study are expected to contribute to the ongoing debate by providing empirical evidence on the asymmetric effects of CSR in an emerging market context.

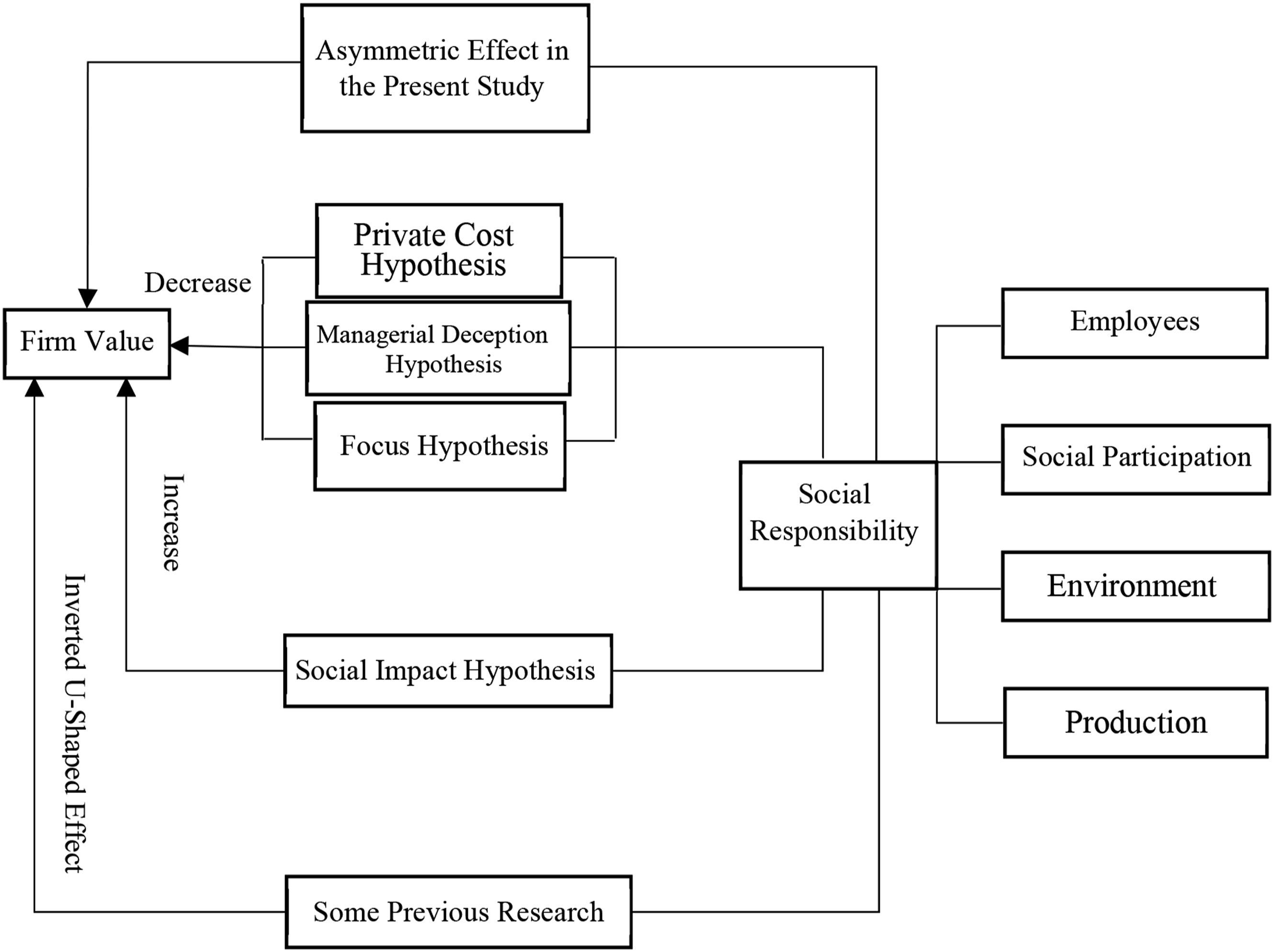

Hence, the present study expects that investment in social responsibility alone does not increase or decrease the trust of shareholders and the firm value, and this should be accompanied by planning, purposefulness, expertise, skill and transparency. Otherwise, firms cannot reduce their operating costs, which means that they cannot reduce operating costs and thus increase the firm’s value. Also, if economic resources are used and allocated more efficiently and external costs are endogenous, operating costs will decrease, and the firm value will increase. According to available literature and evidence, the definitive outcome of the impact of social responsibility on the firm value cannot be predicted. Therefore, the present study aims to investigate the effects of social responsibility on the firm value in terms of levels of activity and investment in this area in the Iranian economy. According to the existing literature and background (Figure 1), the research hypothesis is presented as follows: Hypothesis: There is an asymmetric relationship between corporate social responsibility and firm value. Conceptual framework of the relationship between social responsibility and firm value.

Research method

The present study is quantitative research in which the econometric method of panel smooth transition regression (PSTR) model was used to test the research hypothesis. The required data were collected through the Tehran Stock Exchange (Kedal) and Rahavard-Nowin software databases. The data are primarily derived from the audited financial statements and board reports of the TSE, which are a reliable source of information.32–37 First, the data were sorted using Excel software and then analysed using Win Rats-9 software.

Specification of panel smooth transition regression model

The panel smooth transition regression model with two limit regimes and one transition function has been specified by Gonzalez and Terasvirta

38

in this way:

The transition function of

Like Gonzalez et al.,

38

the transition function is logistically specified in this way:

In equations (2) and (3),

In such a model, if the corporate social responsibility is less than the threshold level c, the impact of corporate social responsibility on the firm value will be

The transition variable can be selected among the explanatory variables, the log of the dependent variable or any other variable outside the model that is theoretically related to the studied model and causes a nonlinear relationship.

39

Given the aim of the present study, which is to investigate the impact of corporate social responsibility on firm value and consider the question of whether the effect of corporate social responsibility on firm value during different regimes is affected by the type of regimes and various levels of corporate social responsibility or not, corporate social responsibility has been used as a transition variable. In this study, to investigate the impact of corporate social responsibility on firm value,1,13,40 equation (6) was used.

According to the theoretical foundations of the research, corporate social responsibility as an explanatory and influential variable on firm value is entered into equation (6) to investigate the impact of corporate social responsibility on firm value. Therefore, the model of the present study considering the above-mentioned explanatory variables is specified as a general state of the panel smooth transition regression model, as follows.

This method has been used in recent financial and accounting studies.13,41,42 It can be said that the age of using this method in accounting studies does not reach more than 5 years, although the results of this method, derived from literature and strong theoretical foundations, cannot be ignored.

Defining the variables

The dependent variable

The dependent variable of this study is the firm value, which, according to the research conducted by Chen and Lee,

13

Tobin’s q (Qb) ratio is used in this way.

Transition variable

Corporate social responsibility (CSR)

Corporate social responsibility includes four dimensions of employee information disclosure (EMPD) (cash earnings sharing, retirement benefits, poor health and safety, and reduced workforce); social participation information disclosure (COMD) (charitable donations, innovative donations, negative economic impact and non-payment of taxes), rate of production information disclosure (PROD) (product quality, product safety, payment of fines for product safety and payment of penalties for negative advertising), and the rate of environmental information disclosure (ENVD) (clean energy, air pollution control and greenhouse gas reduction, hazardous waste generation and payment of fines for waste management violations).

Sentences in the text of the notes attached to the financial statements were used to analyse the content. The total value of corporate social responsibility disclosure is obtained from the sum of the partial value of corporate social responsibility dimensions and can be calculated using equation (9).43,44

The total score of corporate social responsibility disclosure is calculated using equation (10).

Employee relations information disclosure rate (EMPD)

The following six criteria are needed to show the employee relations information disclosure rate. 1) Employee environment health; 2) Employee training; 3) Employee benefits; 4) Employee characteristics; 5) Employee share ownership; 6) Safety and health of employees (ISO 18000).

The disclosure score of employee relations is obtained using the following formula.

EMPD: Employee Relations Disclosure Score; A: Disclosure score for each of the criteria of employee relations in firm i; The number 6 in the denominator represents six criteria related to the disclosure rate of employee relations.

Disclosure of information related to social participation (COMD)

The following six criteria are needed to indicate the extent of disclosure of information related to social involvement. 1) Cash donation program; 2) Charity program; 3) Scholarship program; 4) Sponsors for sports activities; 5) Supporters of national pride; 6) Public projects.

The disclosure score of the social participation dimension is obtained through the following formula.

COMD: Social participation disclosure score; B: Disclosure scores for each social participation criteria in firm i; the number 6 in the denominator represents six criteria related to the disclosure rate of social participation.

Production information disclosure rate (PROD)

The following four criteria are needed to show the production information disclosure rate. 1) Product safety; 2) Product quality (ISO 9000); 3) Product development; 4) After-sales service.

The disclosure score after production is obtained through the following formula.

PROD: Production disclosure score; C: Disclosure scores for each of the production criteria in firm i; the number 4 in the denominator represents four criteria related to the rate of production disclosure.

Environmental information disclosure rate (ENVD)

The following four criteria are needed to indicate the environmental information disclosure rate. 1) Air pollution control; 2) Prevention and compensation program; 3) Protection and use of recycled products; 4) Award in the area of environment (ISO 14000).

The environmental dimension disclosure score is obtained through the following formula.

PROD: Environmental Disclosure Score; D: Disclosure scores for each environmental criteria in firm i; the number 4 in the denominator represents four criteria related to the rate of environmental disclosure.

Control variables

In the PSTR method, there is a limitation that the number of control variables must be kept to a minimum. 38 Therefore, in the present research, due to the use of this method to examine the nonlinear relationship between corporate social responsibility and firm value, only those variables have been utilized for which the existing literature discusses a substantial relationship with the dependent variable. Accordingly, the research model employs three variables: institutional ownership (INS), debt ratio (Debt), and firm size (Size).45,46 The nature of the relationship between these variables and the dependent variable is described as follows.

Percentage of institutional shareholders (INS)

Percentage of institutional shareholders. Several studies have examined the impact of institutional shareholders on firm value. Several studies show an asymmetric relationship between institutional stakeholders and firm value. 32

Firm size (size)

The natural logarithm of assets at the end of the period. It is justifiable from a theoretical perspective of firm size or political costs since it is believed that large firms are more in the vision of policymakers, and this factor may reduce the form value in the long term. Connolly and Hirsechi 47 also found that firm size increased Tobin’s q ratio (Qb).

Debt ratio

The ratio of total debts at the end of the period divided by the total assets at the end. Lin and Chang 48 found an asymmetric relationship between the debt ratio, firm value, and Tobin’s q criterion. Accordingly, when the debt ratio is less than 9.86 percent, Tobin’s q ratio will increase by 0.0546 percent per one percent increase in the debt ratio. Also, when the debt ratio is between 9.86 and 33.33 percent, Tobin’s q ratio will increase to 0.0057 per one percent growth in the debt ratio. However, when the debt ratio is more than 33.33%, there will be no relationship between the debt ratio and the firm value of Tobin’s q criterion.

Statistical population and sample of research

The statistical population of this research included all firms listed on the Tehran Stock Exchange operating in the Tehran Stock Exchange during the years 2011–2019. The present study selected sample firms based on the following criteria. 1) To increase the comparability of the data, firms whose fiscal year does not correspond to the last day of the year were excluded. 2) Investment firms, banks and insurance firms were excluded due to differences in the procedures used in preparing financial statements. 3) Firms with a trading log of more than 3 months were excluded. 4) Firms that were not listed on the Tehran Stock Exchange before 2011 were excluded, and these firms should have been members of firms listed on the Tehran Stock Exchange during the study period. 5) Firms whose required information was not available were excluded.

Accordingly, the number of selected firms based on the criteria mentioned above was 158 firms during 2011–2019.

Results

Descriptive statistics

Descriptive statistics of variables.

Correlation analysis

Descriptive statistics of variables.

*Sig. at 0.10. **Sig. at 0.05. ***Sig. at 0.01.

Stationarity test

Null: unit root (assume common unit root test).

*Sig. at 0.10. **Sig. at 0.05. ***Sig. at 0.01.

Linearity versus nonlinearity

L.M. and L.R. tests for linearity.

*Sig. at 0.10. **Sig. at 0.05. ***Sig. at 0.01.

Test results of the threshold value in PSTR estimates.

*Sig. at 0.10. **Sig. at 0.05. ***Sig. at 0.01.

Interpretation of results

The analysis reveals a nonlinear relationship between CSR disclosure and firm value. Specifically, CSR positively affects firm value in the first regime, where CSR disclosure is below or equal to 0.80. This positive impact aligns with the social impact hypothesis, which suggests that enhanced CSR activities can improve a firm’s reputation and stakeholder relations, thereby increasing its market value. In contrast, in the second regime, where CSR disclosure exceeds 0.80, the effect becomes negative, consistent with the private cost’s hypothesis. This indicates that excessive CSR disclosure may lead to higher operational costs and reduced firm value, potentially due to managerial distraction or increased resource expenditure.

Overall, the results support the hypothesis of an asymmetric relationship between CSR and firm value, demonstrating that the impact of CSR is not uniform but depends on the level of CSR engagement.

Results of estimation of the panel smooth regression model

Parameter estimates of the PSTR model.

*Sig. at 0.10. **Sig. at 0.05. ***Sig. at 0.01.

The slope parameter (γ), which indicates the transition speed from one regime to another, was obtained at 985.764, and the threshold of corporate social responsibility was 0.80. The threshold number is the two regimes’ turning point and distinguishing point expressed in the smooth transition regression model. However, it should be noted that the first and second regimes of the limit states of the smooth transition regression model are panel. In fact, according to the observations of the transition variable, the values of regression coefficients fluctuate between these two limit values.

The value 0.80 indicates that corporate social responsibility’s impact on the firm’s value varies before 0.80 and after 0.80. Thus, corporate social responsibility up to the level of 0.80 has a positive effect, and above this percentage, it has a negative impact on the firm’s value. The regression F statistic is 145.305 and is significant. In other words, the total number of independent variables could explain the changes in the dependent variable. Also, the adjusted coefficient of determination of the model is 0.74. It indicates that independent variables explain 74% of the changes in the dependent variable and indicates the high explanatory power of the model. The Durbin-Watson statistic is 1.94, indicating no correlation between the error terms.

As the figure in Table 6 shows, corporate social responsibility positively impacts the firm value in the first regime and negatively affects the firm value in the second regime. Thus, by increasing the corporate social responsibility disclosure to a certain level (0.80), the firm value increases and then by increasing the corporate social responsibility disclosure, the firm value decreases. Hence, it cannot be stated that corporate social responsibility disclosure and, more importantly, participation in these activities obliges firms to their stakeholders. Based on the first regime (up to the threshold of 0.80), it can be justified through the social impact hypothesis and the private cost hypothesis. Based on these results, the research hypothesis that states an asymmetric relationship between corporate social responsibility and firm value cannot be rejected.

Additional analyses

This study utilized Tobin’s Q (QB) as an economic measure of firm value. However, to ensure the robustness of the results and in line with prior research,49–51 return on assets (ROA) was also employed as an accounting-based measure of firm value. To examine the nonlinear impact of Corporate Social Responsibility (CSR) on ROA, Model 15 is estimated as follows:

Parameter estimates of the PSTR model.

*Sig. at 0.10. **Sig. at 0.05. ***Sig. at 0.01.

The findings show that the threshold of corporate social responsibility was 0.65. The value of 0.65 indicates that the impact of corporate social responsibility on return on assets is different before 0.65 and after 0.65. Therefore, corporate social responsibility has a positive effect up to 65% and a negative effect above this percentage on return on assets as an accounting measure of corporate value. These findings reaffirm the findings of the previous section and state that corporate social responsibility has two different regimes (first positive and then negative) on corporate value. Therefore, by increasing the corporate social responsibility disclosure score to a certain level (0.65), the value of the company (as measured by return on assets) increases, and then by increasing the disclosure of corporate social responsibility, the return on assets, which is a measure of corporate value, decreases. Based on these results, the research hypothesis regarding the asymmetric relationship between corporate social responsibility and corporate value cannot be rejected.

Discussion

This study investigated the nonlinear relationship between Corporate Social Responsibility (CSR) and firm value, focusing on both linear and nonlinear impacts within the Iranian context. The findings reveal a nuanced relationship, highlighting that CSR impacts firm value differently at varying levels of CSR engagement. Specifically, CSR positively impacts firm value up to a threshold of 0.80. Beyond this point, the impact becomes negative. The findings in the first regime are consistent with the results of Farooq et al., 6 as their findings indicate that corporate social responsibility enhances the market value of firms. These results may emphasise the importance of CSR activities and initiatives, which can improve the company’s reputation, increase investment attraction, and establish stronger relationships with stakeholders. They argue that the increase in market value may stem from investors being more inclined to invest in companies that take on greater social responsibility, as this can indicate that such companies are committed to sustainability and long-term growth.

The results align with the Social Impact Hypothesis in the initial regime. This hypothesis suggests that strong CSR performance enhances firm value by improving stakeholder relations and reducing operational risks. Our findings confirm that up to the threshold, CSR activities positively influence firm value, supporting the notion that initial CSR efforts can be advantageous by attracting investment and fostering a better market position.

However, in the second regime, where CSR exceeds the 0.80 threshold, the negative impact on firm value corroborates the Private Costs Hypothesis and Management Deception Hypothesis. The Private Costs Hypothesis posits that excessive CSR investment may divert resources from core business activities, reducing profitability. This is evident in our results, where CSR beyond the threshold imposes additional costs that outweigh benefits. The Management Deception Hypothesis further explains this decline, suggesting that excessive CSR may be used as a facade to mask managerial opportunism or inefficiencies, leading to a decrease in firm value as investors become sceptical. The findings of the second regime are consistent with the results of Servaes and Tamayo 5 and Hu et al., 12 as they demonstrated a negative relationship between corporate social responsibility and firm value. In other words, corporate social responsibility has led to a decrease in the market value of firms. The analysis of these findings indicates that CSR cannot be regarded as a universal strategy for enhancing firm value. In other words, in circumstances where companies invest in CSR in an unproductive or poorly planned manner, these activities may decrease market value instead of strengthening financial performance.

Nevertheless, the findings of the present research differ significantly from two strands of literature that refer to both positive and negative relationships between corporate social responsibility and firm value, as it analyses this relationship across two distinct regimes, reflecting a more in-depth examination of this crucial issue. Overall, the findings of this research indicate the nonlinear impact of corporate social responsibility on firm value. These findings are consistent with previous research suggesting a nonlinear relationship between CSR and firm value. 13 The study extends this understanding by applying a Panel Smooth Transition Regression (PSTR) model, which effectively captures the asymmetric effects of CSR on firm value in an emerging market context.

The results highlight a nuanced relationship between CSR and firm value, which aligns well with both the Social Impact Hypothesis and the Private Costs Hypothesis but particularly supports the latter theory in explaining the nonlinear findings.

Initially, the study found that CSR positively impacted firm value up to a certain threshold (0.80). This outcome is consistent with the Social Impact Hypothesis, which posits that strong CSR performance can enhance a firm’s reputation, build stronger stakeholder relationships, and drive financial gains. According to this hypothesis, firms engaging in CSR effectively can improve their market position, attract more investment, and reduce operational risks, thus increasing firm value. This positive relationship observed in the study, where CSR benefits firm value up to the threshold, supports the idea that CSR initiatives can create substantial social value, translating into financial value for the firm.

Beyond the threshold, the study reveals a negative impact of CSR on firm value. This decline aligns with the Private Costs Hypothesis, which argues that the costs associated with CSR activities can outweigh their benefits. According to this hypothesis, excessive CSR investments can divert resources from core business operations, leading to inefficiencies and reduced profitability. The negative impact observed in the study when CSR disclosure exceeds the threshold can be attributed to these increased private costs. Firms may face higher operational costs, reduced focus on core activities, and potential managerial distractions, diminishing overall firm value.

While the primary explanations for the study’s results are rooted in the Social Impact and Private Costs Hypotheses, the Management Deception Hypothesis and the Focus Hypothesis also offer supplementary insights. The Management Deception Hypothesis suggests that managers might use CSR to serve personal interests rather than shareholder value, which could contribute to the decline in firm value observed beyond the CSR threshold. Similarly, the Focus Hypothesis indicates that an overemphasis on CSR might divert attention from core business strategies, further explaining the adverse effects observed.

In summary, the study’s findings that CSR positively impacts firm value up to a threshold, after which it has a negative effect, are best explained by the Social Impact Hypothesis for the initial positive phase and the Private Costs Hypothesis for the subsequent negative phase. The nonlinear relationship captured by the Panel Smooth Transition Regression (PSTR) model underscores the importance of balancing CSR activities to optimise their impact on firm value. This approach provides a more nuanced understanding of CSR’s effects, offering valuable insights for managers and investors navigating CSR strategies in various economic contexts.

Conclusion

This study contributes significantly to understanding CSR’s impact on firm value by highlighting linear and nonlinear effects. The results demonstrate that CSR can enhance firm value up to a certain threshold (0.80) but may lead to diminishing returns and negative impacts beyond this level. This nuanced relationship offers valuable insights for managers and investors, emphasising the importance of balancing CSR investments to avoid potential negative repercussions.

Limitations

While the study provides valuable insights, several limitations should be noted. First, the research is limited to firms listed on the Tehran Stock Exchange, which may not be generalisable to firms in other emerging or developed markets. Second, the study’s focus on CSR disclosure may not fully capture the qualitative aspects of CSR activities, which could also influence firm value. Finally, the analysis period is limited to 2011-2019, and the impact of recent global economic changes or new CSR regulations beyond this period is not considered.

Implications

This study’s findings, which reveal a nonlinear relationship between Corporate Social Responsibility (CSR) and firm value, have significant managerial implications. Recognising this nonlinearity, managers must identify their firms’ optimal level of CSR engagement to maximise value creation. This requires a thorough cost-benefit analysis of CSR activities, considering industry-specific characteristics and competitive dynamics. Furthermore, CSR initiatives should be strategically aligned with the firm’s overall business strategy and long-term objectives rather than treated as peripheral activities. Transparency and rigorous reporting of CSR activities, based on established standards, are crucial for building trust with investors and other stakeholders. Continuous monitoring and evaluation of CSR effectiveness and avoidance of superficial CSR efforts are also paramount.

Policymakers also have a vital role in promoting and enhancing effective CSR. Instead of imposing mandatory regulations, they can incentivise corporate self-regulation in CSR through tax incentives and facilitated access to financial resources, thereby improving CSR performance. Developing national CSR standards and promoting the adoption of international standards enhances transparency and comparability of corporate CSR activities. Further research on CSR is essential for a deeper understanding of the relationship between CSR and firm value, leading to more effective policies. Collaboration with the private sector through workshops, conferences, and establishing dialogue platforms facilitates the development and implementation of more effective strategies for advancing CSR and creating sustainable value for society.

Suggestions for further research

Future research could explore the CSR-firm value relationship in different emerging and developed markets to determine the generalizability of the findings. Additionally, examining qualitative aspects of CSR and their impact on firm value could provide a more comprehensive understanding. Researchers might also investigate the effects of recent global economic shifts and regulatory changes on the CSR-firm value relationship.

Linking to literature and theory

This study extends existing theories by demonstrating a nonlinear impact of CSR on firm value, which complements the Social Impact Hypothesis and challenges the Private Costs Hypothesis and Management Deception Hypothesis. Using a PSTR model contributes to a more nuanced understanding of CSR’s effects, aligning with and expanding upon previous research on the asymmetric relationship between CSR and firm value. 13 This approach offers a theoretical foundation for future studies exploring the complexities of CSR in various economic contexts.

Footnotes

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.