Abstract

Sustainable development goals call for urgent action with an aim to spur socio-economic growth along with the protection of the environment and resources. However, these goals are difficult to be achieved when finances are not mobilized to mitigate harmful resources. In return, numerous green bond manifestations appeared in the market, which are viewed as a bridge to have successful implementation of sustainable development goals. Therefore, the study is aimed to explore the relevance of green bonds, financialization, and sustainable environmental change mitigation technologies for environmental change in ASEAN economies. The initial outcomes confirm the long-run cointegration association between study variables and also explore the slope heterogeneity and cross-sectional dependencies. To explore the causal connections between the study variables, the current study employs CS-ARDL technique. The study finds significant contributions of sustainable environmental change mitigation technologies and green bonds in the reduction of pollution, hence improving climate quality. The short-run infers similar results with relatively lower magnitudes of coefficients as compared to the long-run. Negative error correction terms are used to confirm the stability of the model, which implies sustained convergence towards “steady-state equilibrium” in case of expected deviations. The results offer practical implications and recommendations.

Keywords

Introduction

Sustainable environmental change mitigation technologies are projected to diminish the adverse influence of manufacturing processes on climate quality. From technology and economic aspects, innovative technologies enhance products, services, production methods/processes, and management of businesses.1,2 Green technologies mitigate climate threats and are gaining attention because novel technologies like biomass processing, carbon mitigation technologies, climate management technologies, waste recycling technologies, and energy-saving technologies enhance the natural environment.3,4 Additionally, green technologies improve everyday life, human development and enhance climate quality.5–7 Climate-related technologies, clean technologies and socially responsible investments

8

address business and social demands without deteriorating the natural environment.9,10 Research and development in environmental technologies forces businesses to utilize economical and sustainable energy sources to facilitate the environment.11,12 In this lieu, renewable energy consumption reduces carbon emissions, meanwhile, green innovations and related technologies are efficient sources of energy as compared to traditional sources of energy.13,14 Carbon neutrality is the most popular goal among the SDGs, which focuses on attaining net zero emissions and has gained the attention of policymakers, governments, researchers, policymakers, and academicians15,16 and forces to use sustainable, green, and clean technologies to enhance the climate quality.14,17 Countries are putting a wide range of efforts to promote green technologies, e.g., GTB (green technology bank) of China promotes the green development of information technologies.18,19 Green Technologies promote the natural ecology and reduce pollution in emerging and emerged countries.

20

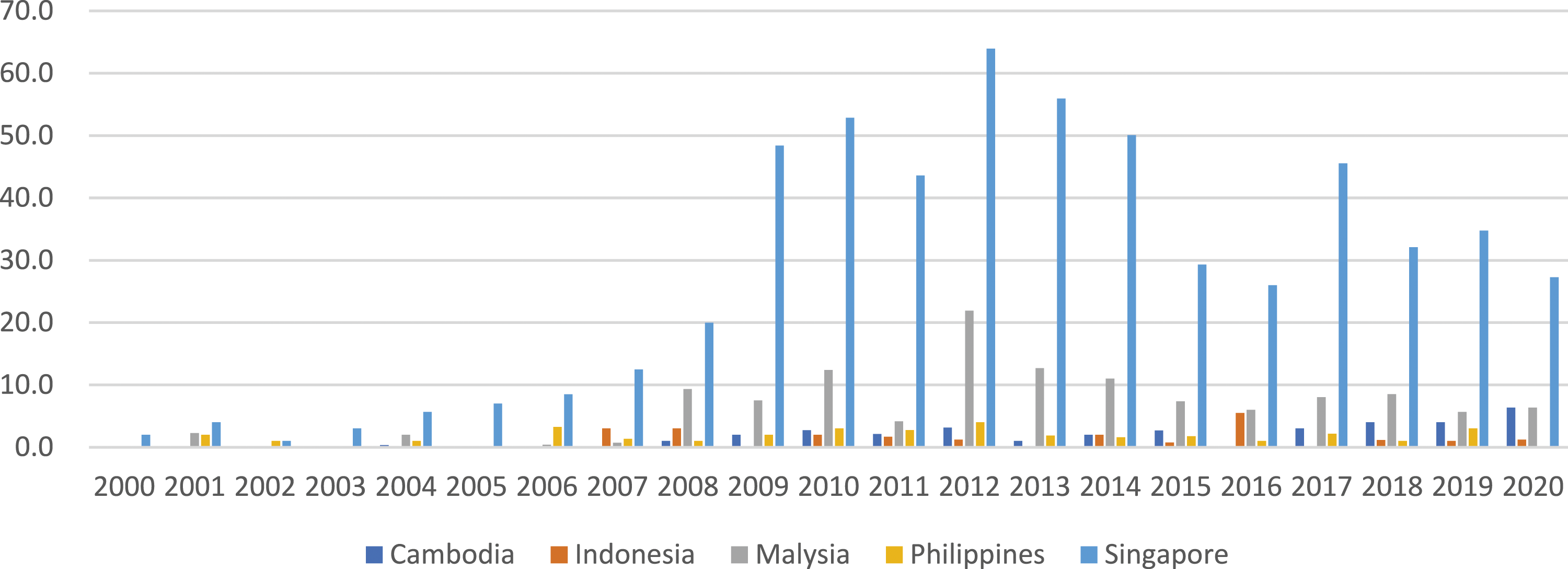

Registered patents for Sustainable environmental change mitigation technologies in ASEAN countries show mixed results (Figure 1) over the last two decades. Five countries are selected from ASEAN economies i.e., Indonesia, Malaysia, Cambodia, Singapore, Philippines because of the availability of data

1

for registered patents for Sustainable environmental change mitigation technologies. Secondly, ASEAN-5 sampling is being drawn because a pattern of economic activity can be observed in these particular economies which is sufficient to be recognized in order to scrutinize the impact on environmental quality.

21

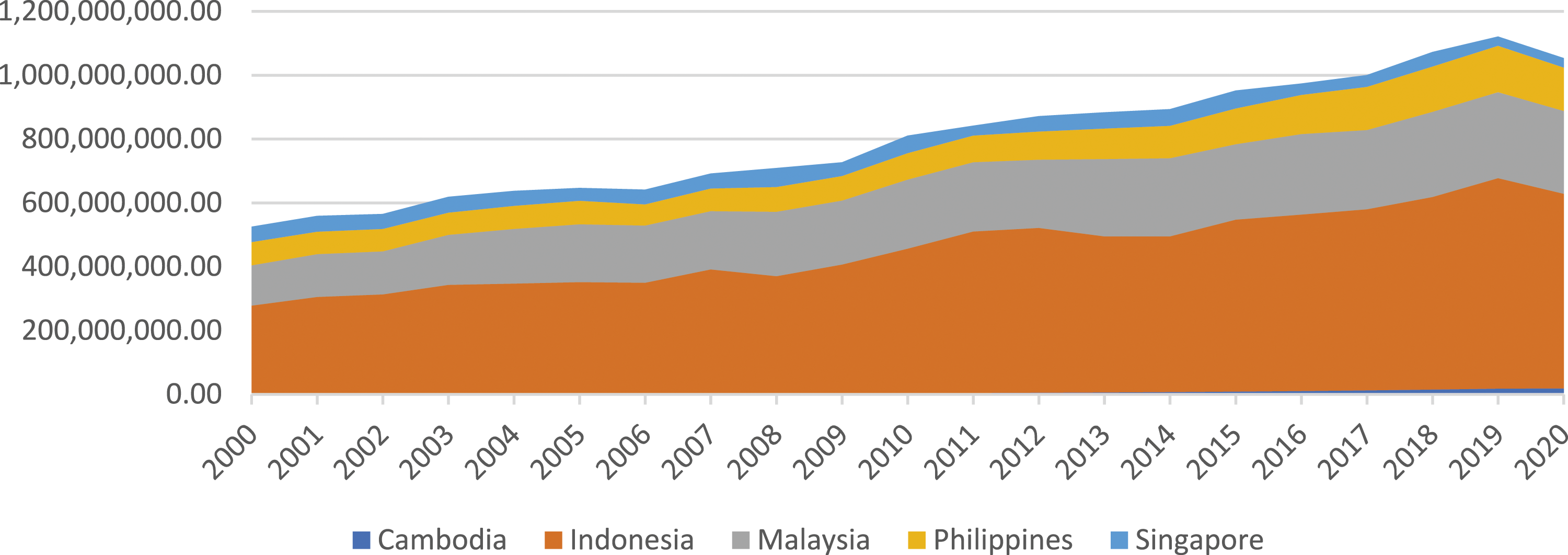

The advancement of industrialization in these economies also results in high energy consumption which is the ultimate reason of high emissions and the ASEAN region has received limited attention.22,23 Singapore shows the highest trends for environmental technologies and followed by Malaysia. The rest of the ASEAN economies exhibit similar trends in climate technologies. The ASEAN economies are very small in the development of environmental change mitigation technologies as compared to the entire world (Figure 2). The selected ASEAN economies show the highest carbon emission for Indonesia while Singapore and Cambodia show the lowest trends of carbon emissions (Figure 3). Figures 1 and 2 show, as the selected ASEAN economies exhibit a decline in the development of sustainable environmental change mitigation technologies, the carbon emission increase in these economies. However, ASEAN countries have tremendously reduced industrial carbon emissions. Apart from environmental technologies, the connection between financial advancements and climate issues receives the attention of academicians. However, few studies infer that financial advancement is the main cause of enhanced climate mitigation.24–26 A well-functioning financial ecosystem improves the performance and efficiency of the financial industry and improves economic development.27,28 However, improved economic growth results in enhanced levels of energy consumption and carbon emissions. Moreover, the advancement of financial and stock markets offers funds for new projects which cause a rise in energy demands and environmental pollution.29,30 Sustainable environmental change mitigation technologies patents (%) for selected ASEAN economies. Sustainable environmental change mitigation technologies patents (%) Worldwide. CO2 emissions for selected ASEAN economies in metric tons per capita.

Further to a discussion, the most sadden fact of present-day economy is low-rate investment. Before 2008 financial crisis, high-income economies’ growth was shoved by spending on consumption, education and housing. 31 However, due to the crisis, such spendings declined and those investment which should have made a recovery, never got an opportunity to be materialized. Thus, it demands change. After the crisis period, major global central banks made an attempt to revitalize spendings as well as employment with the help of slashed interest rates. Interestingly, the strategy proved to be effective to some extent. Moreover, policymakers also schooled investors to bid up stock and bond prices through capital market flooding via liquidity and interest rate, and foreign direct investment.32,33 This effort established financial wealth and stimuli consumption via initial public offerings in the form of investment. However, the said policy is not cost-effective and has reached to its limitations. Besides, monetary policy was also pushed to limits; hence, there is an absence of long-term investments along with infrastructure financing. In most economies, especially emerging ones, public sector is not in position to fill the gap, meanwhile, no interest can be seen from private sector. This is due to low return rate and risk factors. Currently, three challenges have been surfaced which need a proper strategy: (1) right project identification; (2) development of complex plans that integrate private and public both sectors (including multiple countries); (3) structured financing. However, this needs long-term planning, sleek budgeting and effective implementation of project. At the global level, there is a need of massive investment in green energy systems in order to sharpen the reduction of carbon emissions. Emerging economies especially are in need of substantial investments in green projects to attain sustainable development.13,34

Although, several studies explored the causes of carbon emission through financial advancement, but these studies considered a single proxy for financial advancement; however, the current study uses financial markets’ efficiency and access to financial institutions to proxy financial advancement. Similarly, the rapid growth of the green finance industry has increased the flow of funds for both private and public sector sustainable development projects. The proceeds of green bonds issued by the Worldbank have increased over 16 billion and are issued in twenty-three different denominations since 2008. 35 Muganyi, Yan 36 argue that green bonds help to achieve environmental quality goals in China. A green financing ecosystem ensures a reduction in environmental pollution where France, China, and the US are the top issuers of green bonds. 37 Green bonds enhance the sustainable utilization of natural resources, conserve biodiversity, control pollution, and enhance renewable energy efficiency.37,38 Green bonds reduce environmental issues and carbon emissions; however, empirical evidence of the connectedness of green bonds and environmental change is still limited from the ASEAN economies perspective.

Based on the above-mentioned arguments, the current research investigates the impact of sustainable environmental change mitigation technologies, sustainable finance, and financial advancements on environmental sustainability in ASEAN economies. The study employs advanced panel econometric models to explore slope heterogeneity, CSD (cross-section dependence), and cointegration using panel data over the period from 2011 to 2020. More specifically, the study integrates the impact of financial advancement and green bonds on low-carbon economies. The outcomes of the study exhibit that sustainable green bonds and sustainable environmental change mitigation technologies promote low carbon emissions. Similarly, access to financial institutions also improves environmental quality but the efficiency of financial markets is incapable to cope with environmental deterioration. The research work is presented in five sections: after the introduction part, the next segment explores the literature to find a reasonable gap and construct a theoretical framework. The variables, empirical tools, and data sources are debated in segment 3, while the following segment discusses the empirical outcomes, which is further followed by conclusion.

Review of relevant literature

Environmental change mitigation technology and climate issues

Discussing about environmental change mitigation technology and climate issues, the seminal work of Sikhar, Gaurav 39 is needed to be highlighted. The authors proposed the model which was developed through the implementation of various working assumptions. One prominent assumption is “full greening or full penalty of pollution inducing activity.” The theoretical assumption may be effective 100; however, in practical scenario, partial greening of an activity could be achievable. On the basis of economic viability, technological scope and legislative targets stationed by government and agencies, a firm is capable of taking a decision to opt for partial greening activities in their production phase where unavoidable and viable pollutants can be controlled and meddled. This establishes a situation where it is up to producer to take the decision to bear partial penalty payment for not implementing green norms and procedures. The partial penalty also covers the disengagement of organizations in eco-friendly mechanisms. Thereby, the maximum benefit of a supply chain can be gauged in such a scenario is possible through an “intricate function” that has a reliance on green cost and green financial burden, which would be implied together on a particular activity.21,40

It is also argued that the surroundings where manufacturing mode could be defined via data explosion and globalization. These certain characteristics lead to agile and malleable manufacturing in the last few years, however, they come up with challenges in the present environment. The first and foremost challenge is having the complexity in data integration because of various formats such as structured, semi-structured or unstructured.41–43 The integration of data is a crucial step as most of the organizations believe in the concept synergetic manufacturing. Another challenge is linked to the resilience of manufacturing processes at the global level. In the present environment, it is more difficult to achieve as social and political norms have made the system vulnerable to a great extent. Hence, the only solution to overcome such challenges is to introduce sustainable technologies which help economies to ease the burden of environmental pollution.17,19,44

The connection between environmental technology and climate quality is also explored by different researchers in different countries. Shan, Genç 14 argue that innovative green technologies help to attain SDGs without environmental deterioration. By employing the STIRPART model, the study explores the connectedness between green technology, per-capita income, energy consumption, and climate change mitigation in Turkey. Meirun, Mihardjo 45 employ BARDL (bootstrap autoregressive distributive lag) model and explore that green innovations are vital in the attainment of economic excellence without deteriorating the environment. The authors further argue though Singapore has attained magnificent economic growth, but still, the country is facing a climate mitigation problem. Hence, environmental change mitigation technologies provide a better solution for climate sustainability. From emerging and emerging economies, Shi and Lai 46 investigate the trends of green innovations and argue that North American and Western Europe regions are advanced in green technological development as compared to other emerging nations. Over the period from 1996 to 2017, Razzaq, Wang 2 investigate the asymmetric linkages between CO2 emissions and climate-related technological innovations in BRICS economies. The authors argue that environmental technologies mitigate the emissions of greenhouse gasses and carbon dioxides. Gu, Wang 47 argue the transfer of low-carbon technologies reduces the warming effects. Chien, Anwar 48 observe the EKC framework and argue that ICT (information and communication technology) reduces climate degradation. In the recent past, many studies endorse causal and dynamic associations between environmental technologies and climate issues49,50 and argue that environmental technologies reduce pollution issues. Iyer, Hultman 51 examine the implications of sustainable climate technologies and claim that these technologies are eco-friendly but the cost of implementation of these technologies hinders these implications. Lin and Ma 52 observe the heterogeneous impact of sustainable climate technologies on carbon emissions in different cities. From 35 OECD economies, Lu, Mahalik 53 investigate the influence of technology adoption and democracy on carbon emissions and find that democracy reduces pollution while trade liberalization enhances carbon emissions.

Financialization and climate issues

The connection between financialization and climate issues is explored by different researchers with mixed findings. Few authors claim financial growth enhances climate degradation, while few researchers reject it. One pillar of the relationship explores that financial growth enhances a well-organized financial ecosystem that sheds more financial resources to facilitate many schemes, consumption patterns, and production processes, which results in higher energy utilization.54,55 Therefore, environmental deterioration is evident from rapid financialization or vice versa. But, the other pillar claims that financialization promotes climate protection via efficient energy utilization technology.56,57 Prevailing research work justifies both destructive and constructive impacts of financial growth on environmental pollution. From China, Zhang 58 investigates the effect of financial growth on the emission of CO2. The authors find that financial growth increases carbon emissions. Khan, Khan 59 explore 192 economies by inspecting the heterogeneity of consumption of renewable energy, financial advancement, and carbon emissions. The authors find that financial growth enhances carbon emissions. Bouraima, Stević 60 and Haseeb, Xia 61 investigate the effect of globalization, financial growth, and renewable energy consumption on CO2 emissions under the umbrella of EKC. Their study not only confirms the cointegration but also infers the prevalence of “cross-sectional dependence and heterogeneity of slope parameters”. The authors also infer that financial growth results in higher carbon emissions. Sheraz, Deyi 62 explore the period from 1986 to 2018 and examine the connection between financial advancements and emissions of carbon dioxide in the G20 economies. The authors find that financial growth offers financial resources for the adoption of new industrial technologies, hence, leading to reduced carbon emissions. From Turkey, Rjoub, Odugbesan 63 examine financial advancements and climate deterioration. The authors find a strong moderating effect of financial advancement. From the agriculture sector of China, Koondhar, Shahbaz 64 investigate financial advancement and climate quality. The authors find that agriculture’s financial advancement is negatively associated with environmental quality over a period from 1998 to 2018. Using a longer data set comprising four decades, Li and Wei 65 investigate the carbon emission trends for 30 different provinces of China and explore that financial advancement is associated with carbon emissions.

Green financing (green bonds) and climate challenges

Investment opportunities and green bonds positively influence climate quality, therefore getting the attention of researchers. The implication of green loans and bonds is explored by Gilchrist, Yu, 66 and the authors infer that corporate environmentally responsible attitude enhances the natural ecosystem. Tuhkanen and Vulturius 67 claim that green bonds are a significant form of sustainable and green finance, yet there is a gap in the literature regarding the influence of green bonds on carbon neutrality. Fatica and Panzica 68 argued that after the Paris Agreement, green bonds have significantly reduced carbon emissions. Similarly, it claims that rapid industrial and economic growth has adversely affected the environmental quality while green bonds and green projects can enhance the climate quality.69,70 Wang and Zhi 71 advocate that green bonds are beneficial for economic advancements and climate protection. The authors further suggest that biodiversity funds, environmental funds, weather derivative funds, green investment funds, nature-linked securities, and debt for environmental swaps are important sources of green financing for climate change mitigation technologies. Muganyi, Yan 36 and Zhang and Qi 72 claim that fintech development and finance-related policies significantly reduce carbon emissions and urban economic development. The current study infers that sustainable climate change mitigation technologies, green bonds, and financialization disrupt the drifts of CO2 emissions.1,73

Data description and methodology

Panel designs are normally used to address the accuracy issue through data collection process. The present study used panel cointegration due to higher number of T compared to N. Hence, in this scenario, conventional approaches such as random or fixed effect model cannot be used due to inappropriate measures. Since, ASEAN economies are grouped due to similar characteristics such as ecological or biological Thus, CSD, slope heterogeneity and stationarity issues exist in such economies that is observed in the nature of panel data. CSD test is employed due to widespread coordination and cooperation within ASEAN. Also, ASEAN economies do have somewhat similar economic growth rate but their relative strength varies. Therefore, the slope homogeneity test is used, which is followed by unit roots and cointegration tests. The current research starts with the detection of CSD (cross-section dependence), which may arise from unexpected volatility, interdependencies of residuals, and due to global shocks in several macroeconomic pillars. If any study fails to address the CSD issues, the analysis and findings would be considered inappropriate and biased.77,78 For this reason, the CSD test introduced by Pesaran 79 is employed. After exploring the CSD properties of data series, the study evaluates the stationarity of the variable, which is a common characteristic in panel data. The stationarity problems have been classified into three different generations. In this regard, Levin, Lin 80 assume unit root issues in panel data (homogenous in nature), however, Im, Pesaran 81 consider unit root issues in panel data (heterogenous in nature). As the study initially assumes the likelihood of CSD existence, hence, the study primarily focuses on the robust arguments of Pesaran 82 and Bai and Carrion-I-Silvestre. 83

After exploring the stationarity of the variables, the study detects the existence of slope heterogeneity using the econometric approach introduced by, 84 which is a modern version of Swamy. 85 The null hypothesis infers the existence of slope homogeneity. Without adequate investigation of slope heterogeneity, the coefficients, estimation, and findings of the study cannot be considered reliable and credible. After investigating the slope heterogeneity of coefficients, the next step is to explore the long-run cointegration between variables of the model. Therefore, we employ the cointegration test introduced by Westerlund and Edgerton 86 and Banerjee and Carrion-i-Silvestre, 87 and these panel cointegration tests can deal with correlated errors, slope heterogeneity, and CSD. Once the cointegration is confirmed, we employ the CS-AARDL model, which captures slope heterogeneity, structural breaks, and CSD. 25 Since panel estimations produce unreliable outcomes due to CSD existence and slope heterogeneity issues. Therefore, such issues are handled by CS-ARDL in an efficient manner. Interestingly, techniques such as FMOLS and DOLS do not cater to such issues, hence, CS-ARDL has benefits over others. Besides, compared to panel ARDL approaches, CS-ARDL is robust to address various problems such as “misspecification biases, serial error correlation, cross-sectional dependence, non-stationarity and the endogeneity bias.” CS-ARDL also has the potential to address arbitrary integration. Thereby, the study utilizes CS-ARDL approach to measures long and short-run coefficient values since the approach is appropriate to handle heterogeneity and CD problems. 88

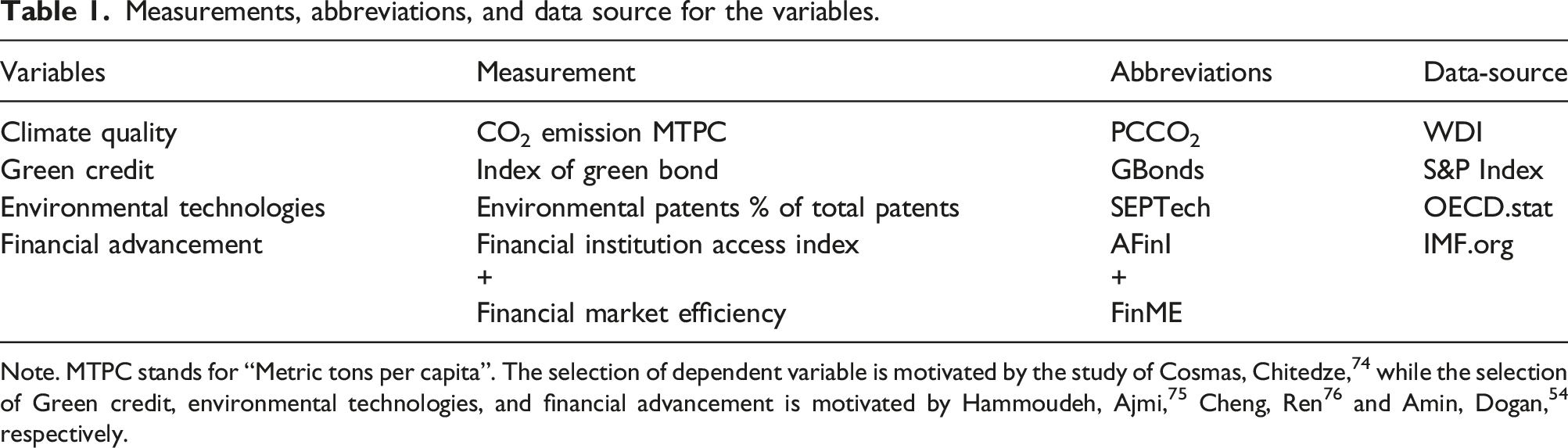

Thus, by following the aforementioned criteria, researchers are allowed to fulfil the objectives in order to verify “the validity of the assumption of constant slopes.” Moreover, the study is able to identify any sign of CSD in panel data which is a necessary step to be taken. After following these steps, the study is able to analyze the proposed relationship between variables with the accurate and appropriate econometric approach and estimation method that would provide more accurate outcomes. This study used per-capita CO2 emission as the dependent construct, while Environmental Patent technologies (EPTech), green credit (measured through green bonds: GBonds), and Financial Advancement (measured through access to financial institutions; AFinI and financial market efficiency; FinME) as explanatory variables. The model is presented through equation (1):

Cross sections (ASEAN-5 countries) are presented by symbol i, while t indicates the period. Moreover, regression from equation (1) is given as:

where PCCO2 is expressed with a title like Wit which is the main outcome variable, while all the explanatory variables (CETech, GBonds, AFIns; FinME) are presented in term Zi, t− 1. Moreover, dependent and independent variables average is given by

While the short run estimators are given as:

where in aforesaid expression: Δi = t − (t − 1)

Measurements, abbreviations, and data source for the variables.

Note. MTPC stands for “Metric tons per capita”. The selection of dependent variable is motivated by the study of Cosmas, Chitedze, 74 while the selection of Green credit, environmental technologies, and financial advancement is motivated by Hammoudeh, Ajmi, 75 Cheng, Ren 76 and Amin, Dogan, 54 respectively.

CSD outputs.

Note. *** indicates the level of significance with 1 % confidence interval.

Results and discussion

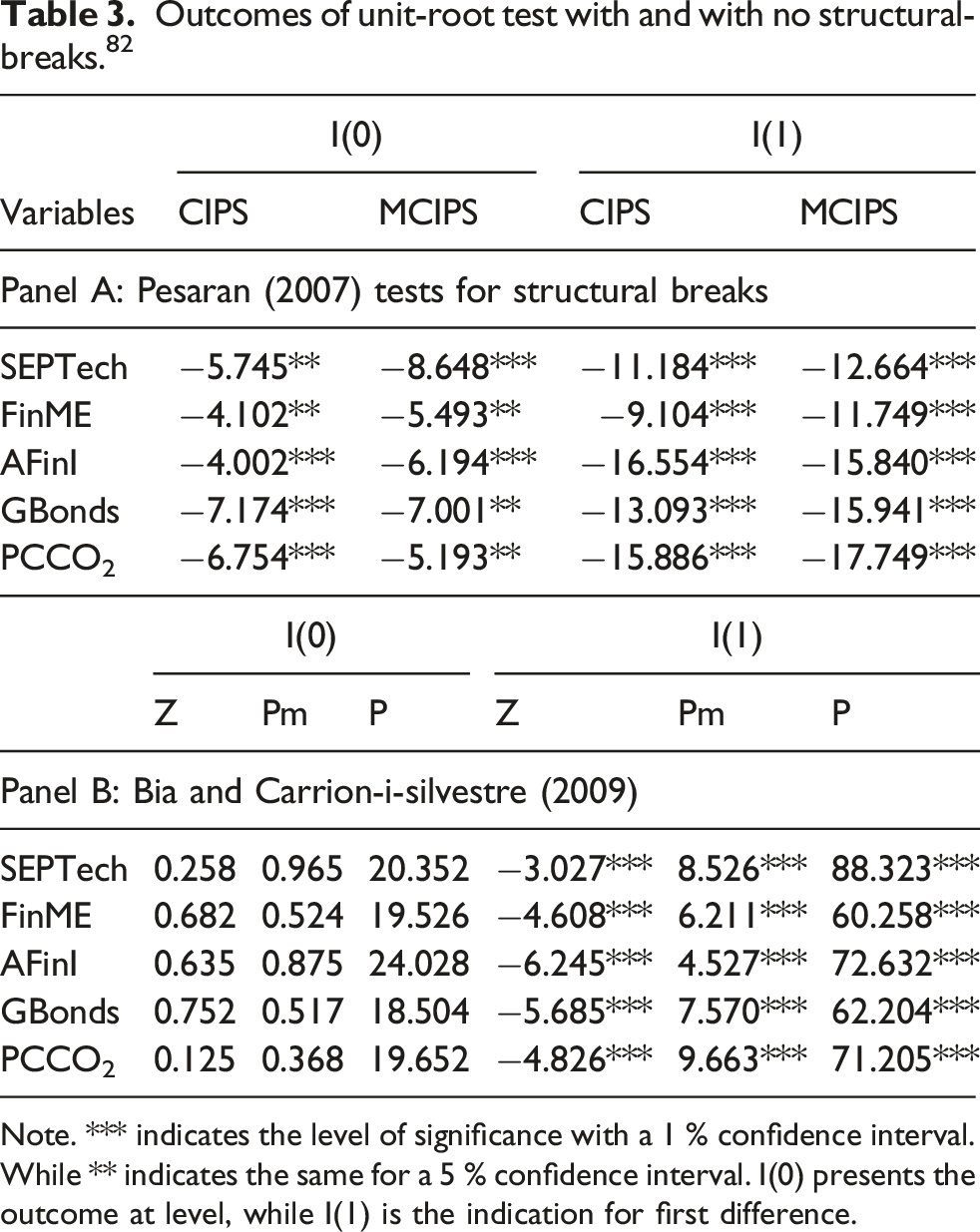

Outcomes of unit-root test with and with no structural-breaks. 82

Note. *** indicates the level of significance with a 1 % confidence interval. While ** indicates the same for a 5 % confidence interval. I(0) presents the outcome at level, while I(1) is the indication for first difference.

Estimation for heterogeneity of slope coefficients.

Outcomes of panel cointegration tests of Westerlund and Edgerton. 86

Note. *** indicates the level of significance with a 1 % confidence interval.

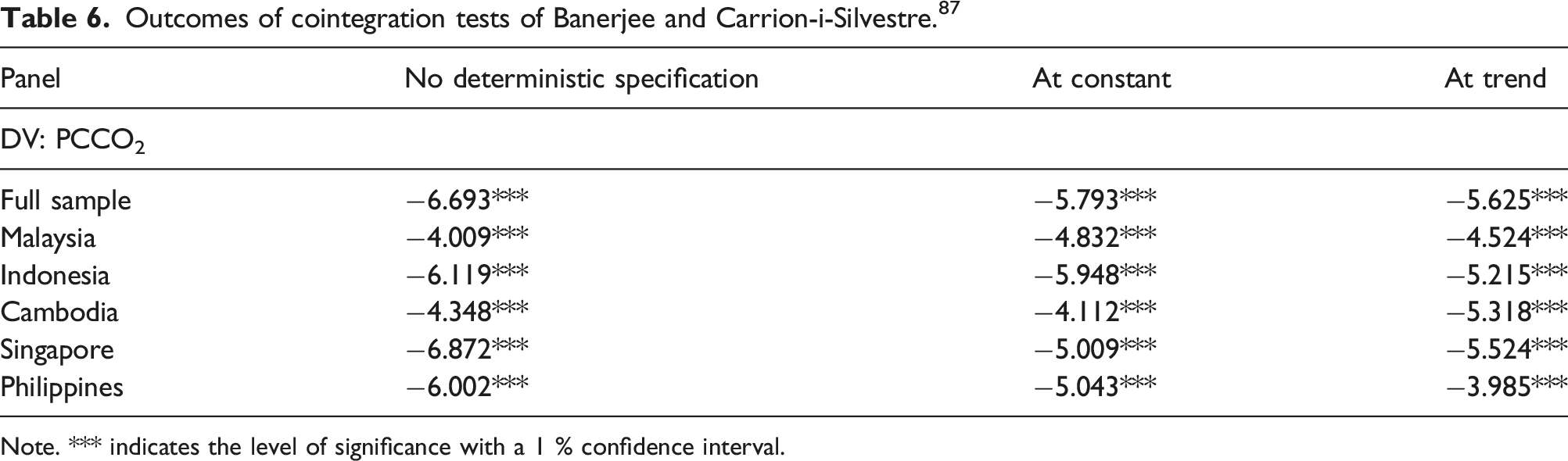

Outcomes of cointegration tests of Banerjee and Carrion-i-Silvestre. 87

Note. *** indicates the level of significance with a 1 % confidence interval.

Outcomes of CS-AARDL model for long-run and short-run.

Note. *** indicates the level of significance with a 1 % confidence interval. While ** indicates the same for a 5 % confidence interval.

From Nigeria, Odugbesan and Adebayo 94 investigate the stimulus of financial advancements on emissions of CO2, and observe a positive-significant connectedness between financial advancements and carbon emissions. Taking a global sample, Jiang and Ma 95 explore that financial advancement induces positive trends in carbon emissions, hence, mitigating the environmental quality. However, the authors find an insignificant association between the variables in emerging economies. The positive linkages between the efficiency of financial markets and emission of CO2 may be because the capital markets of ASEAN countries allow the firms to avail debt and equity financing which leads to enhanced economic development via the consumption of traditional energy. Reducing this trend of increasing carbon emissions through the efficiency of financial markets requires strict supervision of financial markets to discourage investments in traditional energy sources.

Outcomes for robustness estimations.

For the short run, Table 7 presents the outcomes of the CS-ARDL model. Sustainable environmental change mitigation technologies (SEPTech) are significantly and negatively connected with environmental quality. The efficiency of financial markets is extremely accountable for enhanced carbon emission, while access to financial institutions reduces environmental deterioration. Finally, the issuance of green bonds also enhances the climate quality by diminishing carbon emission in the short run.

Bekun 98 and Glomsrød and Wei 99 endorse similar findings and claim that green finance diminishes the global ingesting of coal and enhances the feasting of renewable energy, therefore mitigating global climate deterioration. Furthermore, ECT (error correction term) infers the “response magnitude” or “speed adjustment” of the outcome variable (PCCO2) to variations in explanatory variables of the current study. The ECT coefficient is inverse and significant, which confirms the convergence towards equilibrium with an annual adjustment rate of 32%. Table 8 exhibits the robustness of findings, where the Table makes it clear that there exists an inverse and significant association between the sustainable environmental change mitigation technologies (SEPTech) and carbon emissions with AMG and CCEMG estimations. Furthermore, green bonds and access to financial institutions reduce the emission of CO2, while the efficiency of financial markets enhances carbon emissions with both estimators, 100 see Table 8).

Conclusion and policy implications

For international communities, climate change threat is viewed as a topic of concern in recent years. Regardless of sequential meetings and arguments within academia and practitioners, economies are failed to get rid of the threat. Because of excessive usage of non-renewable sources, ASEAN region made huge contribution to the threat, due to which it becomes more difficult to be removed permanently. In this context, sustainable environmental change mitigation technology is vital for the enhancement of climate quality. In this regard, the UN has defined SDGs for industry, structure, innovations, and climate action with 17 other labels that trigger global sustainability. Similarly, plenty of literature investigates the impression of financial advancement on the emission of carbon dioxide on a large scale; however, less attention is paid to the impact of access to financial institutions and the efficiency of financial markets on climate change. Meanwhile, in a complex financial ecosystem, financing and investing activities are confined to conventional sources of energy, which results in enhanced greenhouse gas and carbon emissions. The complexity of the financial ecosystem enhances the need to utilize green bonds, and sustainable finance for environmental protection. The study considers a panel examination to analyze the impact of sustainable environmental change mitigation technologies, access to financial institutions, efficiency of financial markets, and green bonds over a period from 2011 to 2020 from ASEAN countries. The current research work utilizes the CS-ARDL model to estimate the connectedness between dependent and independent variables. It is clear from the results of the long-run ARDL model that sustainable environmental change mitigation technologies, green bonds, and access to financial institutions mitigate carbon emissions. However, sustainable development goals can not be achieved unless corporate firms and private investor mobilize finance for it. Practitioners are also obliged to devote themselves in green education and focus on consumer’s green preferences. Also, the increasing awareness of investors in terms of green initiative helps firms to design sustainable products and promote green mandate in society. Since, green bonds help in carbon reduction, therefore, investors’ trust is crucial for green bond investment. The study, thus, calls for green bond initiatives to be considered by corporate firms. Also, a deeper understanding of green financing help in the implementation of sustainable climate policies and offer a platform to shift the focus of resource toward zero carbon projects. Also, in order to acknowledge ecological adversities linked with financial inclusivity, it is quite obvious for emerging markets to motivate their financial markets more inclusive and eco-friendlier. In this context, it is crucial for economies to determine financial risks that are associated with environmental risks. This way proactive measures can be taken to make financial services environmentally friendly. Also, the proposition of green financial schemes should be considered by institutions to neutralize the damage inflicted by financial institutions.

Based on the findings, ASEAN economies must devise diverse policy brackets at the state and provincial levels. Policymakers in ASEAN economies should find ways to generate sustainable jobs at the macroeconomic level. This helps in creating a positive impact as a green workforce means less emission. Promoting green jobs would also increase the green consumption basket in society, which means the per capita income will increase, which will eventually enhance environmental conditions. Besides, effective development in green finance areas may extend the scope of financial support specifically for green projects, which would counterbalance the consequences of inflation on green project development. In the end, efforts will be diverted toward renewable energy consumption. Concerning the provincial level, ASEAN policymakers should constitute more incentive policies in those provinces where a sustainable development path is difficult to be maintained. Contrarily, at the regional level green subsidies and loans, pressure policies such as carbon taxes should be promoted in order to achieve sustainable development. Besides, uniform policies are essential to be counted generally because this could be an underlying issue that would make it difficult for economies to achieve sustainability in the long-run. In addition, to regulate climate control from the demand side also, the study also elucidates how the trend of low carbon and environmentally friendly goods/services has been emerged in the long-term; however, the shift can be hindered due to external shocks or critical events. This indicates that there is a need to find innovative ways and integrate the demand side with the supply side of environmental policies.

The efficiency of financial markets enhances carbon emissions. Almost similar sign of coefficients is observed in the short run with slightly different magnitudes. AMG and CCEMG estimators endorsed similar outcomes. Based on these findings, the study proposes the following policy recommendations. In the current era, the adoption of sustainable environmental technologies is a serious issue. A huge capital investment is required for replacing traditional technologies with eco-friendly technologies. ASEAN economies should propagate climate regulations to overcome hindrances in the implementation of climate patents in different sectors. In this regard, removal of industries using traditional energy sources, or imposition of tax on heavily polluting enterprises may be fruitful. Moreover, financial markets and financial institutions lack climate regulation policies; hence, the businesses result in higher carbon emissions. Therefore, the study suggests that efficient financial markets regarding climate regulation can ensure an eco-friendly environment. ASEAN countries should encourage capital markets to develop green growth-inclusive policies to trigger green financing for the development of eco-friendly technologies. In this regard, the promotion of green and sustainable financial instruments i.e., green bonds would promote environmental quality. The proceeds of green bonds would facilitate the development and implementation of green technologies for climate change mitigation. Also, in the absence of standardized and universally accepted framework of green bonds, the current market depends on “private governance regimes”. Although their brutal focus on project evaluation, fair reporting, and clean and standardized procedures enlighten transparency and disclosure, which are the two success parameters of the green bond market. However, credibility is still an issue to be addressed to make it easier for investors to opt for sustainable investment.

The future researcher may compare the impact of traditional versus environmental technologies to explore the relationship introduced in this study. The researcher may compare the ASEAN with Asian or European economies. Moreover, it would be fruitful if the future researchers divide the sample period in different subsamples or divide the sample period on the basis of different conditions or methods introduced by Shahid and Sattar 101 and Shahid. 102 Subsample analysis may provide more fruitful results, but we rest it for future researchers to incorporate the suggestions.

Footnotes

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by the Ho Chi Minh City University of Economics and Finance (UEF), FPT University. This research is partly funded by University of Economics Ho Chi Minh City (UEH), Vietnam.