Abstract

The study inspects the seven sectors of the Association of Southeast Asian Nations (ASEAN) economies to explore the impact of consumption of clean energy, green bonds, and green economic advancement on environmental, social, and governance (ESG) practices to attain sustainable development goals (SDGs). The ESG aspects are individually explored from 2011 to 2020. It is observed that the key determinants of ESG practices are green economic advancement, clean energy, and green financing. Moreover, these determinants positively and significantly track the ASEAN economies toward attaining SDGs. The determinants play a vital role in sustainable advancement even when explored individually using different regression models. The linkages between the explanatory and outcome variables remain consistent after controlling other variables like climate regulatory quality, foreign direct investment, and gross domestic product. The study provides solid implications for stakeholders, environmental activists, and governments of ASEAN economies. The findings also infer sustainable business practices via creating an association between ESG practices, green economy, clean energy, and green financing.

Keywords

Introduction

The “Plan of Transforming our World” was presented in September 2015. The theme of this plan is based on the agenda of Sustainable Development by 2030. The agenda incorporates the five Ps: planet, people, prosperity, peace, and partnership. This agenda entails the 17 sustainable development goals (SDGs) to address global social inequality and environmental deterioration. In recent years, environmental quality has faced severe threats. In this regard, academicians, experts, researchers, governments, and climate activists are paying particular attention to climate issues.1–3 Global action is expected by businesses, stakeholders, community members, and governments to attain a sustainable natural climate to buffer against serious threats. The severe problem from the corporate side is that the business groups are not reacting to the implications of sustainable goals in actual letter and spirit. In the annual report, 72% of firms worldwide publish the SDGs title. Only 20% of firms have developed quantitative tools to attain the SDGs. 4 argue that many industries and business groups still lack the measures to achieve the SDGs. Moreover, these industries and businesses face a challenge in implementing quantitative tools to measure sustainable goals. Business organizations are also facing the problem of data sources and methodological frameworks for coping with the SDGs. 5 Both the empirical and theoretical pillars of the prevailing literature explore the critical deficiency of business groups in examining their actions to address the SDGs. According to, 6 industrial performance and efforts towards attaining sustainable goals can be accessed through corporate performance and the essential measures taken to implement the quantitative measures. The literature supports environmental, social and governance (ESG) scores to measure sustainable performance. These scores are non-financial but highlight the anticipated commitment of organizations to attaining SDGs.7,8 The current study highlights the contributions of the Association of Southeast Asian Nations (ASEAN) towards achieving sustainable goals via ESG at the industrial level.

The literature documents that traditional and non-renewable energy sources are economical and cost-effective compared to green/clean energy sources. However, the extreme consumption of non-renewables deteriorates the climate quality due to more significant greenhouse gas emissions. However, the literature explores the significance of green/clean energy consumption for attaining sustainable goals, and this crucial role of renewable energy cannot be ignored.9–12 Therefore, researchers and policymakers are interested in exploring the impressions of green and clean energy in coping with climate mitigations and sustainable development. Eco-friendly green and clean energy consumption has the lowest impact on climate deterioration and is a panacea for attaining sustainable goals. The expected role of green and clean energies is crucial because countries invest significantly in developing these energy sources.13,14 In most ASEAN countries, there is still a gap in the consumption of clean/green energy sources for production in different economic units. The literature defines the green economy as lowering environmental hazards, advancing human well-being, enhancing social equity, and reducing ecological scarcity.15,16 In this regard, a green ecosystem comprising clean energy consumption and green financing helps achieve SDGs by nurturing present and future needs.15,17,18 The literature reveals that resources, clean/green energy, and sustainable development are the most recurrent keywords connected to green/sustainable economies during the last three decades. Furthermore, there is no worldwide recognized definition for the green economy; however, a green economy not only shields the natural climate but also exhibits some crucial economic aids, like financial solidity and the initiation of green jobs. Nevertheless, the literature concerning sustainable development and green economies is scarce in ASEAN economies.19,20

Finance plays a significant role in global economic growth, the industrial revolution, and human progress. For this purpose, it is the essential objective of the global financial ecosystem to deploy global savings in the most productive sector of the economy.21,22 The mismanagement and inefficient deployment of these savings may trigger environmentally harmful projects, leading to environmental deterioration.23,24 To seize the climate hazards, financial institutions should efficiently understand the importance of SDGs and promote projects intended to spread positive impressions on the natural environment. To cope with the issues, economies around the globe have adopted several techniques. For example, projects like green banks, fintech, green bonds, carbon market institutions, and community-intended green funds are categorized as green financing for sustainable development through different industries. The ASEAN economies have paid significant attention to issuing green and sustainable bonds.25–27 Figure 1 shows that ASEAN economies have issued green and sustainable bonds in huge amounts of US$ in millions. Moreover, these economies have also focused on issuing social and sustainable bonds to achieve sustainable development. Issuance of green, social, and sustainable bonds by ASEAN Markets (NikkeiAsia, 2022).

In addition, green finance offers funding for all sectors and includes ESG aspects while making investment-related decisions. Since the concept shifted from fringe to mainstream, investors have raised serious concerns regarding ESG success, its measurement, and the risks associated with ESG. The reason is that ESG-related issues might affect the safety and soundness of banks.28,29 Green loans and their environmental impact would be cleaved into the risk and cost assessment done by financial institutions. Firms’ investors may understand their holdings' potential costs and benefits through portfolio diversification, including securities that also consider ESG. Thus, scholars believe there is a need to look deeper into factors such as renewable energy and green finance that affect environmental quality from prospects.30–32

Thus, in light of the abovementioned debate and prevailing gaps, the current study explores the tendencies in sustainable practices via ESG scores. Moreover, the present study exhibits the role of a green economy, clean energy consumption, and green bonds in monitoring climate regulations, economic growth, and foreign investments. The current research work is organized as follows. In the next section, we critically review the relevant literature. The subsequent section presents the details of empirical methods and the data and sample used in the analysis. This is followed by a section that presents our empirical findings. In the final section, we discuss the implications of our findings for policy and practice and suggest directions for future research based on our study's limitations.

Literature review

Developed and developing economies are paying significant attention to SDGs to attain sustainable growth in 2030. In this regard, the researchers have explored many pillars of SDGs. These studies exhibit that green economy, green finance, and green/clean energy are the essential determinants of sustainable advancement practices that governments, industries, and business groups must follow for desirable results.33,34 Therefore, this section provides both empirical and theoretical pillars of sustainable advancement. The connection between sustainable development and green financing is explored by 35 in the Asian context, and the author infers that Asian economies require a shift to efficient technologies from natural resource-intensive mode, excessive greenhouse gas emissions, and massive consumption of fossil fuels to tack onto the sustainable development.36,37 In this connection, a green revolution in the financial ecosystem is beneficial.38,39 The researchers have also explored the factors hampering green investments and sustainable advancement. For instance, the role of green finance in attaining the SDGs and energy security is studied by researchers.1,24,40 The authors examine that global investments in energy efficiencies and renewable energy projects have been diminished by 3% during the year 2017, which is threatening the natural climate quality. Another critical finding of these authors is financial institutions' attention to investing in fossil fuel projects rather than green/clean energy projects. By doing so, financial institutions avoid the hazards associated with investments and low rates of returns from new technologies.

The previous studies also suggest countries must boost investments in green projects via green banking, green bonds, and carbon market instruments to achieve environmental quality and SDGs by 2030. 41 recommends that green and clean energy investments enhance economic development, while investments in the energy sector and socially responsible investments 42 contribute to sustainable growth. At the same time, 43 explores the importance of green finance in promoting sustainable practices and advancement. For this purpose, a crucial need is to encourage a green financial ecosystem, green activities, and green securities to advance green businesses and environmental sustainability.44,45 Similarly, 46 investigates the footprints of green finance and economic growth in 30 Chinese companies from 2007 to 2016 and argues that green finance promotes green economies and enhances proper ecological protection via green technologies. The authors further explore that green finances significantly contribute to green/clean economies and sustainable development.

The connection between green energy and sustainable growth is vastly explored in the literature; for instance, 9 contributes to the first few pieces of evidence that proposed sustainable, clean, and green development strategies. The authors suggest that sustainable and green energy strategies contribute to sustainable development via green wind, solar, tidal, and biomass resources. The connection between economic growth, renewable energy, and sustainable development from Brazil, Russia, India, China, and South Africa (BRICS) is explored by. 12 The authors find that BRICS countries have introduced quicker strategies for renewable energy investments to achieve SDGs. Similarly, 3 argue that renewable energy technologies positively affect sustainability development in the Middle East and North Africa (MENA), whereas 47 argue that renewable energy-based economies are essential for attaining the SDGs in G20 countries. 48 explores different renewable energy policies in African countries that can help sustain green growth. However, the environmental deterioration is merely based on excessive fuel utilization in African nations, leading to slow economic growth. Over the period from 1990 to 2018, 49 explore the carbon emission and environmental degradation from Organisation for Economic Co-operation and Development (OECD) economies. With the application of panel estimations, the authors find that decentralized carbon emission policies favorably impact climate quality. 50 explore the connectedness of environmental taxes, innovations, technological investments, and carbon emissions. The authors find that provincial growth in China enhances CO2 emissions and deteriorates climate quality. Moreover,50,51 while investigating the pre and post-COVID-19 period, explore the prices of commodities and economic advancement in China. The authors find that the volatility of natural resource commodity prices initiates the vulnerability in economic growth during COVID-19.

Many recent researchers have explored the connectedness between sustainable advancement and renewable energy.52–56 These studies infer that the literature does not significantly explore the association between sustainable development and green economy. 57 provided evidence of this dynamic linkage and developed different research questions regarding environmental-based green economic development. According to the authors, assessing the complexity of all spirals, ranging from human capital to social capital and the natural environment, is crucial for sustainable development. By shedding light on all spirals, the authors highlighted that all the factors related to the spirals influence each other; hence, it demands conclusions from different perspectives by assessing either one spiral or multiple spirals with nature capital.

Moreover, previous studies also find the spillovers between the importance of knowledge diffusion and climate quality. The crucial factors in attaining the SDGs and green economic advancement are explored by, 58 who argues that sustainable advancement, clean technology investments, and green growth are complementary pillars of SDGs. However, the author argues that sustainable advancement through green growth is impossible as climate deterioration continues. Most recently, 59 contributed strong evidence on SDGs to the existing body of knowledge, and they observed that green growth, circular economy, and sustainable practices contribute to SDGs introduced by UNs. 60 Therefore, countries should actively focus on these features of sustainable development. Furthermore, 61 explores the negative connection between conventional economic growth and climate quality. Thus, appropriate green economic advancement strategies must be implemented to attain the SDGs. Policymakers should develop green economic strategies to support science education and innovative green technologies.62,63 At the same time, governments should also establish policies to reduce the cost associated with innovative green technologies, corruption, and climate deterioration.

Methodology and data description

The study selects the ASEAN economies to explore the objectives of the current research work. The data is collected over the period from 2011 to 2020. The secondary data is collected from 200 companies divided into seven different sectors. We collect the data for ESG from Refinitiv, a global data provider company. Many studies have used data from this source. 64 The missing data not available on Refinitiv was collected from respective company websites. We measure the SDG progress via ESG scores. Therefore, all the pillars of ESG are taken as independent variables.

Variables with data sources.

We utilize the panel models because these models facilitate controlling variables that are not part of the study, like federal regulation, international agreements, and natural policies.65–67 In this regard, the fixed effects infer the association of variables within entities like countries, companies, or individuals.65,68,69 On the other hand, the random effect model generalizes the findings outside the sample under observation.

65

Finally, the effect of the error term can be controlled using OLS.

70

The study develops the following equations incorporating ESG as the primary outcome variable:

ESG indicates the environmental, social, and governance pillars in equation (1). GnB, CEngC, and GEA represent green bonds, clean energy consumption, and economic advancement. CRQ represents the climate regulatory quality, and FDI presents foreign direct investment. Equations (2) and (3) indicate a similar term for fixed and random effects. After investigating the combined scores of ESG, we use identical panel regression models to estimate separately the pillars of ESG.

Equations (4) to (6) indicate the environmental pillar of ESG with “EN” for the explanatory and control variables. The study develops the same for the social pillar of ESG with “SOC” in the following equations;

Finally, the Governance pillar (GOV) is represented by the following equations constructed for the basic models from the perspective of ASEAN countries;

The study employs descriptive statistics to infer the basic trends of data sets to ensure series capability for panel estimations. The study also employs correlation analysis and VIF (Variance Inflation Factor) to explore the degree of association among the constructs. Finally, AMG (Augmented Mean Group) is employed to cope with multifactor error terms and heterogeneity

71

and to obtain robust output.

72

The study presents the two steps involved in AMG estimators;

For the analysis, the study collects data from ASEAN economies, and the data set comprises different industries like basic materials, financial, technologies, health care, utilities, real estate, and telecommunication sectors.

Empirical results and discussion

The summary statistics for variables under study for ASEAN economies.

Note: SD stands for standard deviations, Jarque-Bera statistic is indicated by JB, while Prob presents the probability values for Jarque-Bera statistic.

Correlations matrix.

Note: The standard significance level is indicated via ***, which presents the significance at 1%, while the significance level at 5 and 10% is indicated with ** and *, respectively.

Variance inflation factor.

ESG Performance via Panel Analysis was conducted for Selected Industries from ASEAN Economies.

Note: The joint ESG performance is indicated in the table. The standard significance level is indicated via ***, which presents the significance at 1%, while levels of significance at 5 and 10% are marked with ** and *, respectively. DV shows the dependent variable, IV indicates the independent variables, and CV indicates the control variable. M-1 represents model 1, and M-2 and M-3 for the other two models.

Moreover, financial institutions are playing a central role in this green transformation. The author further explores that financial governance plays a significant role in greening the financial ecosystem, leading to the attainment of sustainable goals. Similarly, 76 proves that green bonds are an engine for sustainable advancement, energy projects, and infrastructure development. Nevertheless, the financial ecosystem relies more on investing in traditional energy projects like fossil fuels than green energy projects because of the risk associated with green financing. However, economies should focus on green financing for environmental advancement and to attain SDGs.

Moreover, the linkage between clean energy consumption (CEngC) and ESG pillars is also exhibited in Table 5, and coefficients are 9.77, 4.36, and 3.82 with all three models, respectively. These coefficients show that an upsurge in the level of investments in the consumption of clean energies has a constructive and direct impact on sustainable advancement in ASEAN countries. Clean energy consumption is prevalent in enhancing environmental quality by reducing the intensity of carbon emissions. The literature supports the current study’s findings as 9 explores the fact that the ratio of sustainability increases as renewable energy consumption increases in different economic sectors. Similarly, 77 argues that economies should shift from traditional energy uses to the consumption of renewable energies to enhance environmental quality and sustainable development. Moreover, 13 proves that clean energies like hydropower are a leading source of sustainable advancement in developing economies.

Table 5 also provides evidence of the strong impact of green economic advancement (GEA) on sustainable development in ASEAN economies. The three-panel models exhibit the coefficients 21.52, 20.80, and 18.01, respectively, all significant at a 1% confidence level. The results indicate that green economic advancement can quickly achieve sustainable development. The literature provides similar evidence. 78 highlights green economic advancement as a potential strategy to achieve long-term sustainable growth. From G7 countries, 79 explores the linkage between green economic development and sustainable advancement. The author finds that a positive relationship exists between the variables.

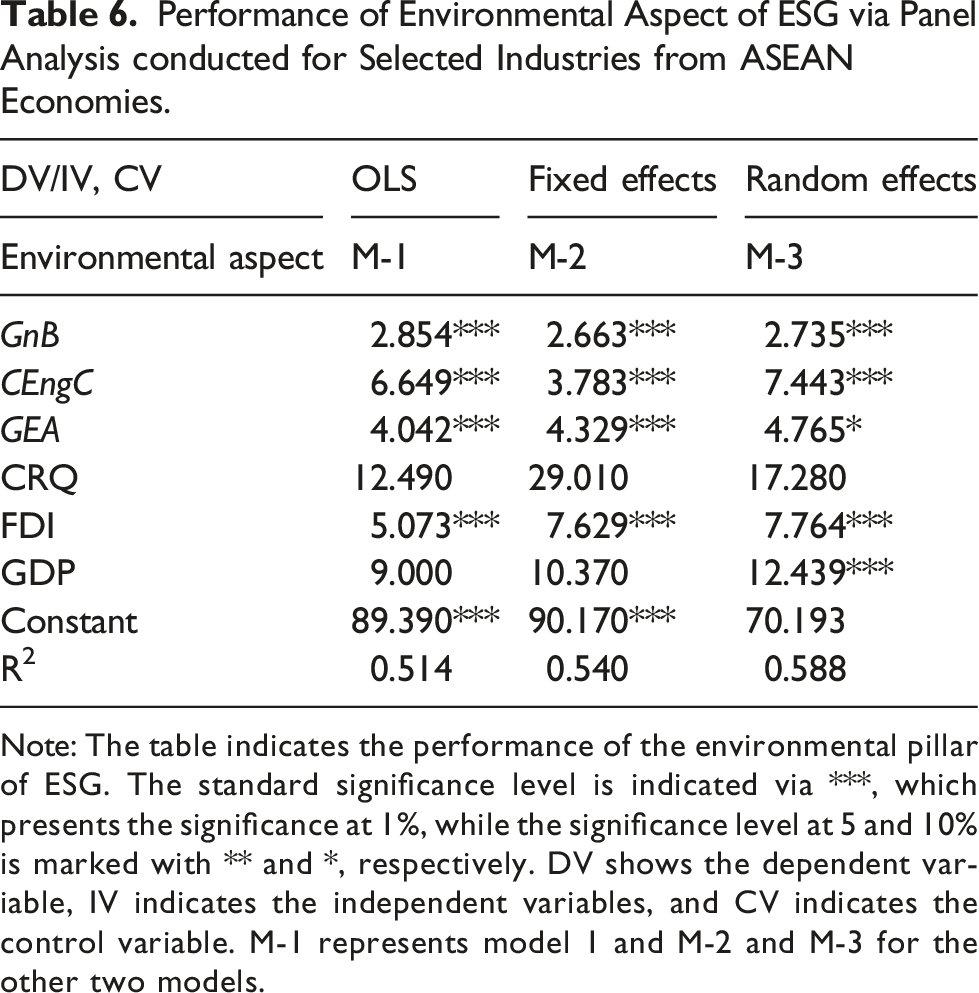

Performance of Environmental Aspect of ESG via Panel Analysis conducted for Selected Industries from ASEAN Economies.

Note: The table indicates the performance of the environmental pillar of ESG. The standard significance level is indicated via ***, which presents the significance at 1%, while the significance level at 5 and 10% is marked with ** and *, respectively. DV shows the dependent variable, IV indicates the independent variables, and CV indicates the control variable. M-1 represents model 1 and M-2 and M-3 for the other two models.

Performance of Social Aspect of ESG via Panel Analysis conducted for Selected Industries from ASEAN Economies.

Note: The table indicates the performance of the social pillar of ESG. The standard significance level is indicated via ***, which presents the significance at 1%, while the significance level at 5 and 10% is marked with ** and *, respectively. DV shows the dependent variable, IV indicates the independent variables, and CV indicates the control variable. M-1 represents model 1, and M-2 and M-3 for the other two models.

Performance of Governance Aspect of ESG via Panel analysis conducted for selected industries from ASEAN Economies.

Note: The table indicates the performance of the Governance pillar of ESG. The standard significance level is indicated via ***, which presents the significance at 1%, while the significance level at 5 and 10% is marked with ** and *, respectively. DV shows the dependent variable, IV indicates the independent variables, and CV indicates the control variable. M-1 represents model 1, and M-2 and M-3 for the other two models.

Table 8 gives the inferences for the governance pillar of ESG scores. It is clear from the coefficient (2.73, 2.745, 2.863) with all three models that investments in green bonds contribute to achieving sustainable goals. Hence, the governance aspect regarding sustainable development is becoming robust in selected industries from ASEAN economies. Similarly, green energy consumption helps better track the sustainable developments in ASEAN economies. Moreover, all three regression models exhibit the positive contributions of green economic advancement toward sustainable development.

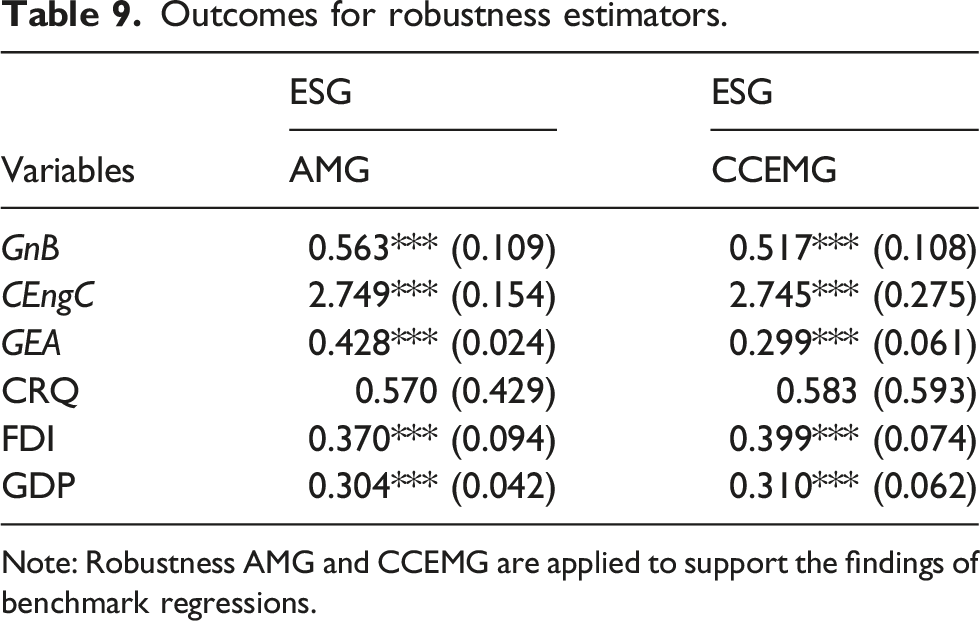

Outcomes for robustness estimators.

Note: Robustness AMG and CCEMG are applied to support the findings of benchmark regressions.

Conclusion and policy implications

The United Nations enlists the SDGs to cope with environmental threats. The business groups, industries, and countries play their respective roles in achieving SDGs. The current study investigates ESG strategies in the different industries' practices in ASEAN economies. Specifically, the consumption of clean energy, green bonds, and green economic advancement have been the key independent variables that stimulate ESG practices in selected industries from ASEAN economies, which are scarce in the literature. The panel estimators confirm the footprints between the explanatory and dependent variables by exploring how clean energy, green bonds, and green economic advancement positively influence ESG practices in achieving sustainable development. Such results indicate that ASEAN governments should efficiently promote the practices and strategies related to ESG scores by enhancing the consumption of renewable energies in all the selected industries, promoting investments in green bonds, and tracking the economies toward green advancement to achieve SDGs.

The green economic advancement in ASEAN countries can strengthen these economies in terms of ESG practices to track sustainable growth. Academicians, environmental activists, climate regulators, governments, and industries can take help from the findings of this study to develop and practice the ESG pillars effectively. The analysis contributes to the exciting debate on the time-varying effects of GDP, climate regulatory quality, and FDI on ESG. With these findings, it can also be concluded that when commercial firms protect the environment by utilizing eco-friendly resources and regulating the effectiveness of such resources, then chances will become high to get a fair share in achieving sustainable goals. Most SDGs rely on this notion of how effective communication resonates between public welfare and stakeholders of business organizations. Therefore, social governance is equally important to achieve SDGs. In this context, corporate governance in the form of effective management is needed to cover various aspects such as allocation of resources, work environment, employee performance, financial and risk management, and organizational structure. The outlined criteria would be of incredible help for economies to achieve SDGs. In light of the results, we can also assume that countries with high economic growth may have greater chances of successfully implementing ESG, which would further help achieve the ultimate goal.

In terms of practicality, the study also suggests that when firms recognize their environmental and social responsibilities, they would likely gain a chance to develop effective policies covering a series of objectives, including a quality work environment for stakeholders, their social well-being, and sustainable competitive advantage. The objectives further improve environmental, social, and economic outcomes, the three main pillars of SDGs. In light of the results, it is also important to note that organizations prefer cutting-edge technologies, use innovative procedures, and ensure clean consumption and a high recruitment ratio during high economic development. This means that such factors would lead to SDGs as the industry of a country thrives with a poverty ratio and high responsible consumption and production.

The results exposed that FDI helps in achieving SDGs. Therefore, it is also recommended that institutions' social and environmental performances be improved with proper regulation. Also, with increased net national income, the government’s useable revenues can be enhanced, which may motivate government institutions to invest in eco-friendly and social-friendly activities. In addition, with the help of corrective measures such as high taxes, the government may also exert pressure on firms that show poor ESG performances. In this regard, the government needs active participation to promote ESG disclosure systems that are broadly applicable since they would attract the attention of businesses, the general public, and investors. With this, the government can support their transition journey to make the economy green eventually.

The study further infers that controlling FDI, climate regulatory quality, and GDP enhances ESG practices via clean energy consumption, green economic advancement, and green bonds. Like the prevailing articles, the current study also entails limitations, such as utilizing ESG strategies to measure sustainable advancement practices. However, many other methods and constructs (like the Dow Jones sustainability index) prevail to measure the SDGs, but we rest it for the researcher in future eras. Future researchers may explore the relationship using primary data collected through questionnaires or interviews rather than employing secondary data. Moreover, the current study only considers the seven industries from ASEAN countries. However, future researchers may explore other sectors and economies. Conclusively, we recommend that future studies extend the literature by analyzing the time-varying effects of the model used in this study. For this purpose, future researchers may divide the extended period into sub-samples [see the study of80,81 for subsample division and analysis].

Footnotes

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This research is funded by the University of Economics Ho Chi Minh City (UEH), Vietnam (Research Grant No. 2023-07-31-1773).