Abstract

Idiosyncratic risk (IDR) is defined in general as the uncertainties of return to investors from an investment portfolio leading to diversification or hedging to mitigate and avoid such risks. This article aims to analyze the IDR of banking sector on oil (OI), stock market indicator (SMI), and fiscal indicator (FI) of Sultanate of Oman. This article examines the IDR of six banking sectors listed in Muscat Security Market (MSM), from 2009 to 2015. Financial modeling is used to determine the IDR of banking sector treated as an independent variable. This study uses three main critical dependent variables, OI, SMI, and FI. The ordinary least squares regression results depicted that there is a statistically significant impact on all of SMIs in MSM 30 share price and its market capitalization with direction of oil exports as OI being significant, as well as total expenditure as percentage of gross domestic product is significant as FI at different significant levels 1%, 5%, and 10%. The findings of the research indicated a weak investor’s protection mechanism and strongly recommend heightened government focus on stressing the importance of having a formal system based on stability, safety, transparency, and supervision of the implementation of contracts so as to protect small investors, eventually leading to increased investments in stocks. Facilitation and encouragement to foreign direct investment will also lead to increase in the performance of fiscal management indicators and improve the export prices of oil, giving a boost to the economic and financial system of the nation.

Introduction

In the last half century, energy and oil sectors have played a significant and vital role in the economic growth of countries exporting and importing oil. In fact, oil prices are the determining factor in any energy sector and have the potential to affect stock prices in multiple ways. Firstly, the oil prices can have a direct effect on earnings and growth rates which is reflected on cash flow, thereby influencing stock valuation models. Secondly, variation in oil prices affects macroeconomic factors thus affecting equity risk premiums, discount rates with the culminating effect again on cash flows in stock valuation models. Capital asset pricing model theory suggests a positive relation between risk and return in the stock market, 1 supplemented by many theoretical and empirical studies 2,3 which propound that they play a vital role in the diagnosis of stock price behavior.

The idiosyncratic risk (IDR) helps explain the importance and implications for investment portfolio decisions. 2 IDR importance has extended to emerging financial markets, whose stock returns are characterized by greater volatility 4 compared with developed countries. 5 It is one of the most innovative issues to focus on stock and market risk and endeavors to minimize these risks becoming imperative in order to mitigate the negative sign in financial position of any firms. Barber and Terrance 6 in their study have opined that both individual investor’s portfolios and mutual fund investment portfolios are undiversified. The investor’s behavior toward IDR focuses on human capital and private equity models. This lack of diversification brings to focus that the total risk of individual stocks is the best measure of the relevance of risk. 7

The IDR of stock plays a vital role in the growth of investments and is a critical decision for investor because many investors do not invest in a fully diversified investment portfolio, some investors invest, while others attempt to capitalize on stock mispricing; hence, the exposure to risk is high in IDR. 3 IDR has less correlation with market conditions’ risk and can be avoided by diversification of investment portfolio since the IDR has more variation in a single asset of stock rather than market risk. IDR is defined in general as the uncertainties of return to investors from an investment portfolio leading to diversification or hedging to mitigate and avoid such risks. On the contrary, systematic risk is the risk emanating from the system and hence has a direct effect on macroeconomic factors that affect all market assets including individual assets and portfolio, and even if the investors increase or diversify the assets or sectors, this risk is very difficult to eliminate by diversification. 8 Other study explained that the cash flow growth is reflected in the variations of risk of financial markets. 9

In the last one decade, especially after the financial crises, controlling IDR has been the main issue of concern for all governments and corporates, and most of the company focused on how to diversify their assets in order to effectively minimize their risk exposure. Sultanate of Oman is one of the members of the Gulf Cooperation Council (GCC) and its economy is heavily dependent upon oil which till date remains the main source of revenue for the government. In the recent event of oil crisis and slowing down of the world economy, like other GCC nations, Oman too is worried about how to diversify its economy beyond oil as declining oil prices had hugely impacted the economic growth of Oman, and the government is keen to find ways to diversify its investment portfolio. The decline in economic growth due to decreasing oil price impacts the industrial, service, and financial sectors of the countries, especially the banking sector which is the backbone of any economy for its progress. Any negative impact on the banking sector leads to decline in business activities as it severely hampers the free flow of money in the economy, affecting the manufacturing sector and thereby international trade.

It is an established fact that risk always plays a prominent and crucial role in financial markets. According to one study, 10 the investor risk are the elements required to explain many characteristics in previous financial data considered as anomalies. IDR has more effects on long-term performance of banks by affecting their future revenues, although the systematic risk has attention of asymmetry information and market inefficiency. Actually, IDR assumes great importance of both managers and investors as it comprises a larger proportion of the bank risk, 11 and it supports the bank irrespective of the expected stock return is able to balance the current inherent risk 12 ; this issue can help the investors to evaluate the innovation process of investment as a whole of portfolio risk and compare it with systematic risk volatility.

Hence, in this study, an attempt is made to understand the importance of IDR as one type of risk which affects the investor decision-making as he seeks to control and diversify investment portfolio in order to mitigate its effects. It has application for the banking sector too, being one of the important sectors of the economy and the main contributor in economic and financial revenues growth of different sectors such as oil (OI), stock market (SMI), and fiscal indicator (FI) of the country.

This study sheds light on the type of risk that investors should avoid or mitigate by knowing their effect to an attempt to build strategic alternatives and early forecast indicators that contribute to maintaining the growth of companies continuously in all types of markets and contribute in positive way in the economic growth of the country’s financial and economic sectors. In the context of Sultanate of Oman, this study is a pioneering work as it seeks to explain the impact of IDR on the most important sectors of the economy, which are a major source of income for the Sultanate, and it also contributes to building a theoretical framework that attempts to explain the impact and relationship of this risk on the other crucial sectors of the economy.

The organization of the article is as follows. An introduction spells out the importance of the IDR and its impact followed by the literature survey of the various research conducted, and their findings that form the basis of the inquiry of this research. In the next section, methodology used for the study is explained and outlined, including the variables being considered and statistical tools used to perform the empirical study. Lastly, the results obtained are discussed and conclusion drawn from the result obtained in the research.

Literature review

Many studies explain the types of risk and how these risks effect the economic growth sectors. Buraschi et al. 13 suggest that, in the market, risk is a main factor and effects on bond market by increasing credit margin spread rate. In another study, Connolly et al. 14 focus on how risk effects asset allocation, and they show that high risk will achieve higher bond returns compared to stock returns. According to the study by Campbell et al., 3 variation in IDR in the firm level gives more attention to new technology research to mitigate the risk In another study, 15 the results show that research and development (R&D) is one of the main factors helping to minimize the IDR and positive correlation between R&D and risk and also it can support future prediction. Xu and Malkiel 16 find a positive relationship between IDR and the expected earnings growth rate.

Although many theoretical studies have interest in this topic in finance field, there has been little empirical studies of the effects of IDR on growth rates of economic sectors. The main factor to explain the effect of IDR is the observed risk which determines agents’ financial decisions; this issue is examined in the study by Holmstrom and Paul, 17 finding that the variation in agent income reflects the variation in exogenous shocks to output as underlying risk. Castro et al. 18 pointed there is IDR effect on employment size in economy as employment factor plays a vital role in developing the gross domestic product (GDP) rate, while Cunat and Mark 19 use a similar method but focus on the effects of IDR on trade of market. Koren and Silvana 20 argue that because of no threats in the innovation process. The economics of the advanced countries' can diversify and control business risk by increasing the types of products, which have the capability to absorb the variations of idiosyncratic risk and thus ease the path of faster economic developed.

Basher and Sadorsky 21 find that oil price risk is related to a variety of stock returns. Nandha and Hammoudeh 22 examine the relationship between beta risk in the market and stock returns that will change the oil price risk and exchange rate sensitivity.

Aloui et al. 23 find that there is asymmetric significant impact of oil price risk on emerging markets, because these markets have special characteristics and conditions, but Maghyereh 24 focuses on the level of energy consumption in the country and finds whether the energy intensity is high, which in turn leads to high trading in stock prices and high performance of oil prices.

Other studies have also discussed the effects of IDR on economic performance growth such as the study of Caggese 25 which give on insight microeconomic practical that firm depend on the degree of diversifications of shareholders to have safety investments and more innovations activities without any consideration of ownership structure of firms. Gilchrist et al. 26 show the negative relationship between investment portfolio as factor of financial performance and IDR and this issue depends on the business cycle activity.

Atkeson et al. 27 explain the variations in IDR and show that risk is playing a vital role in diagnosing the financial reputation of firms and corporate sector; this risk will effect policies of firms based on the IDR level. Other study 28 presents that IDR can lead to less investment portfolio of firms by insiders and the result finds it more strictly to share specific risks of firms.

The macroeconomic theory propounds that in case of unobservable idiosyncratic shocks within the public sectors they render the IDRs uninsurable due to the attainment of inefficient competitive equilibrium and uninsurable IDRs and this happen if the market for asset allocation is compatible and competitive. This assumption supports the result of study 29 by showing that competition and efficiency of firms in economy is different based on uninsurable idiosyncratic shocks. Krusell and Smith 30 suggest a model when the firms are in bad behavior, and this will increase unemployment and the returns related to a negative covariance of idiosyncratic uncertainty. Jiang et al. 31 find there is a negative relationship between IDR and future earnings and returns because of selective disclosure in this issue. Regarding bank risk, Zhongyuan et al. 32 find that a positive relationship between deposits and bank risk is also a negative relationship between the ratio of interest income and total loans and bank’s risk.

In our research study, we focused on three main growth pillars of the banking sector oil price, stock market, and fiscal factors. The current study by understanding critical selected factors during the difficult phase of an emerging market which become critical due to regional turbulences influencing the economic growth of the entire region. Our study is different from other studies in explaining IDR on fiscal management factors by adding value to finance research field and managing the public finance drivers.

Methodology of study

Models of study

In order to find the impact of IDR, this study employs six numerical financial equations that are discussed subsequently. The first equation is used to calculate the return for the concerned period and the second equation is used to compute the market rate of return. Thereafter using ordinary least squares (OLS) regression test in the third equation keeps stock return as dependent and market return as independent variables. The R 2 value is the systematic risk and 1 − R 2 value is the IDR.

The first equation is to compute the stock return for the concerned period using the following formula

Here RS is the return of stock, P 0 is the price of stock at the beginning of the period, P 1 is the price of stock in current period, and Dp is the dividends paid in cash during the period.

The second equation explains the process of calculating the market rate of return after incorporating the periodic stock return calculated using the first equation

Here Rm is the market rate of return, Rs is the absolute stock return as in first equation, and n is the number of periods of stock return.

The third equation uses OLS regression as step 3 where stock returns are the dependent variables and market return is the independent variable to find the IDR also known as unsystematic risk, which focuses on a stock and not on whole investment portfolio assets and could be avoided through diversification of portfolio investment. In contrast, the systematic risk focuses on the overall risk that affects all assets.

Here Rm is the market rate of return and R is the return of stock.

Next step is to find the R 2 as systematic risk and 1 − R 2 is the IDR, the independent variable.

This study uses three dependent variables, viz, OI, SMI, and FI, wherein OIs are expressed through two variables, such as direction of oil exports (DOEs) and oil production (OP), while stock markets are measured by two variables, such as Muscat Security Market (MSM) 30 share price (MSMSP) and market capitalization (MC); FIs are represented by total expenditure as percentage of GDP (TEGDP) and investment expenditure as percentage of GDP (IEGDP). These variables are formulized in three equations which are the three main hypotheses of this study.

Here IDR it is the IDR as calculated in above three equations, OI it is the OIs measured through two variables DOEs and OP, SMI it is the stock market measured through two variables MSMSP and MC, and FI it is the FIs measured through two variables TEGDP and IEGDP.

Data collection

This study used data from all the six banks (whole population) listed on the MSM in the Sultanate of Oman over the period 2009–2015. The data were collected and derived from available annual reports of all the banking company guide 33 and Central Bank Reports. 34

Empirical results and discussion

Quantitative methods in the form of financial models are used in this study to compute the IDR, and descriptive statistics obtained are explained. Finally, OLS regression is used to test the hypotheses of this study.

Descriptive statistics

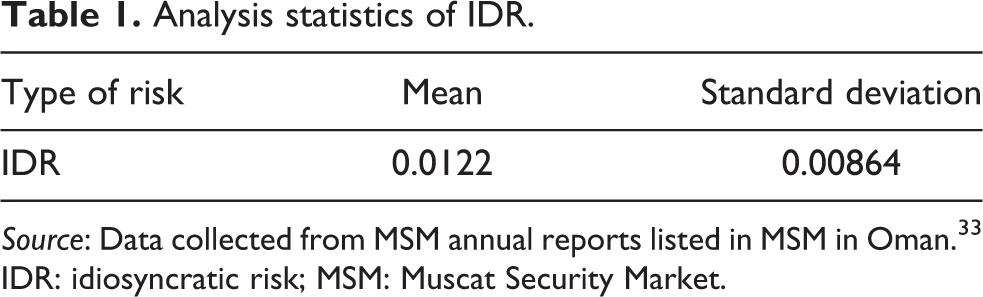

Table 1 shows the analysis of IDR in all banking sectors listed in the MSM for the period 2009–2015. The mean 0.0122 representing all bank population is calculated using the regression test between stock returns and market return of each bank to find the IDR. The calculated standard deviation is 0.00864, and it is obvious from the result that the IDR mean is low. This result explains that the banks in Oman have the ability to meet risks and reduce them to the minimum as these risks are internal and can be controlled through diversification strategies in their investment portfolio. This is done to ensure that shareholders interest, particularly the small investors in the banking portfolio, is safeguarded and protected, as the regulatory authorities also do not want these investors to suffer and lose confidence. The banks of the Sultanate of Oman have also committed themselves to implementing the BASEL I, II, and III standards for capital adequacy and compliance with operational risk standards, which are key to the success of local banks and the starting point for international expansion through increased interbank trade.

Analysis statistics of IDR.

Source: Data collected from MSM annual reports listed in MSM in Oman. 33

IDR: idiosyncratic risk; MSM: Muscat Security Market.

Figure 1 shows two variables used to measure the analysis of SMIs in Oman. The variables are collected from the Central Bank Report 34 in Oman for the period 2009–2015. The values calculated is based on the growth rate showing the best year in both variables as in 2013 of around 0.20 and year 2011 depicts as the worst/bad indicator for both variable indicators. The MC has been stable relatively in all years except in the year 2011 which is a positive sign but MSMSP had more variations and has negative indicators in the years 2011, 2014, and 2015. We note that the market price index is still not constant and was negative except for 2012 and 2013, and the result can be explained that the market is working to restructure the investors in financial sector and the political changes surrounding the market had an impact on the variability of the results during the study period as reflected in the difference in the market share of banks.

Growth rate of stock market indicators. Source: Central Bank Report in Oman. 34

Figure 2 shows the two variables used to measure and analyses the OI in Oman. The variable values are derived from Central Bank Report 34 in Oman for the period 2009–2015. The values calculated the growth rate and the results showing the best year in both variables as 2010 and negative indicator is in the year 2014 for both indicators. DOEs and OP are stable and are construed as a positive indicator, whereas the oil exports increased more in 2010 and 2013 except in the year 2014 but again registered an increase after 2014.

Growth rate of oil indicators. Source: Central Bank Report in Oman. 34

The results can be explained by the fact that the oil index is an indicator that plays the main role in the economy of Sultanate of Oman, where the production of oil has decreased gradually due to low sale prices of oil globally and the existence of some balances in the world economy, which has led to some of the determinants and variations of production oil process and size of the oil export process.

Figure 3 shows the two variables used to measure and analyses the FIs in Oman. The variable values are collected from the Central Bank Report 34 in Oman for the period 2009–2015. The result shows the TEGDP has decreased in the years 2013, 2014, and 2015 as compared with other years and IEGDP becomes positive after 2012 where it was in negatives. These results can explain that the government’s fiscal policy as well as monetary policy determines the economic policy of the Sultanate of Oman and the government had worked in a balanced manner to maintain stability. The government tried to reduce capital expenditure as part of reducing expenses in an effort to control expenditure and reduce the country budget deficit and focused on improving the infrastructure of the country, which contributed positively to improve fiscal policy indicators.

Growth rate of FIs. Source: Central Bank Report in Oman. 34 FI: fiscal indicator.

OLS regression analysis

Table 2 shows the OLS regression analysis of IDR on SMIs. The output informations of banking sector listed in MSM for the period 2009–2015. The results show that all indicators of MSMSP and MC measured are significant at level 5% and 1% where sig is 0.021 and 0.001, while the t-value is −3.712 and −7.938, and the relationship is high at 88% and 97% reflecting high R 2 at 77.5% and 94%.

OLS regression analysis of IDR on SMIs.

Source: OLS regression analysis test from SPSS program.

IDR: idiosyncratic risk; SMI: stock market indicator; MC: market capitalization; MSMSP: Muscat Security Market 30 share price.

*Sig at p < 0.10.

**Sig at p < 0.05.

***Sig at p < 0.01.

This result can be explained by the fact that the Omani financial market relies on innovative activities in managing risk to improve the quality of services provided by banks while enhancing the level of technology, which is reflected in improving the revenues in the banking sector and increasing the market share of banks, thus raising the market share value of the banks. Ever improving administrative performance is avoiding risks, which in turn envisages increase in spending for R&D activities, leading the bank to higher risk exposure due to uncertainties of such investments in R&D. These results are consistent with other similar studies 31,32 and establish that there exists a relationship between IDR and returns.

IDR impact on OIs is measured by DOEs and OP as shown in Table 3. The results show that only DOEs indicator is significant at level 5% (0.021), while the t-value is −4.217, and the relationship is high at 90.4% and R 2 is 81.6%.

OLS regression analysis of IDR on OIs.

Source: OLS regression analysis test from SPSS program.

IDR: idiosyncratic risk; OI: oil indicator; DOE: direction of oil export; OP: oil production.

*Sig at p < 0.10.

**Sig at p < 0.05.

***Sig at p < 0.01.

In our opinion, this study further contributes to the literature on the impact and effect of IDR on OIs especially in net oil exporting nations like Sultanate of Oman as the entire GCC countries stock markets play a crucial role to examine the oil price market as majority of the economics of GCC are largely dependent on oil exports revenues.

This region has about 48% of the world’s proved oil reserves and controls globally about 30% of oil exports according to the BP Statistical Review of World Energy (June 2013). 35 The oil sector plays a major role in determining their GDP, and thus any variations of oil prices have direct effects on macroeconomic factors in these economies and firm’s profits growth which in turn affect stock prices. As diversification of oil prices portfolio is not easy, therefore, the IDR is requiring compensation leading to a risk premium which is stock returns related to oil price risk exposure. The best solution to diversifiable risk is collecting a proportion of liquid to hedging in financial markets.

Finally, the third dependent variable is FIs measured by TEGDP and IEGDP as reflected in Table 4. The results reveal that there is an impact of IDR on only one variable of FIs that is TEGDP at significant level 10% (0.097), while the t-value is 2.156, and the relationship is 73.3% and R 2 is 53.7%.

OLS regression analysis of IDR on FIs.

Source: OLS regression analysis test from SPSS program.

IDR: idiosyncratic risk; FI: fiscal indicator; TEGDP: total expenditure as percentage of GDP; IEGDP: investment expenditure as percentage of GDP.

*Sig at p < 0.10.

**Sig at p < 0.05.

***Sig at p < 0.01.

This result explains testability of fiscal policy of the government of Oman which plays an important role in effect of TEGDP as well as IEGDP. Better fiscal management decision process impacts the economic and financial balances when managing the fiscal policy of the country. All these factors become responsible in decreasing the IDR in the banking system acting as the hallmark of a strong and stable banking system in Oman with easing of the interest rates margin and is consistent with the study of interest rate spread in Omani banking system, 36 wherein the research focused on monetary policy to exploit risk of liquidity in the banking sector by providing the margin competitive interest rate.

Many previous studies 21 –23 show the same result as the current study and discuss the importance of oil price risk, and these results show there is an impact of stock returns and beta risk on oil price variations. Especially in emerging markets, this issue is a great importance because these markets have focus on energy consumption.

Finally, financial markets and banks in Oman are different from other advanced markets due to limited investment opportunities and liquidity available that will have an effect on oil export revenues leading to mispricing in these markets. In this view, the bank of Oman should improve the functions, monitoring, and analysis of banking risks which eventually will lead to improving the macroeconomic decisions-making, resulting in better protection for the banks against financial imbalances. In addition, monetary and regulatory policy must take into account all the different effects of operations on bank risk to build a more robust banking system and usher enhanced better coordination and cooperation between banks and other national and international banks to prevent the possibility of risk. These results too are consistent with the studies 18,19 which explain that IDR plays a vital role in economic development and as growth factors of public finance. Other study 26 shows opposite result between matching with investment portfolio and IDR based on business cycle activity.

Conclusion

In recent years, there has been an increase in risk in all industrial, service, and financial sectors, affecting the financial position of these sectors, and acted as a threat to the survival of these sectors in the market. Without a doubt, the global financial crisis was an empirical lesson for all companies and banks to always think about how we can build early models in forecasting and hedging to mitigate risks. The banking sector plays a significant vital role in building the economy of countries and contributes to the growth of gross domestic product in addition to the intermediate process of building relations and international trade through mutually benefitting trade agreements of companies leading to increase in implementation of international trade transactions. The risks in the banking sector are considered to be sensitive to both systemic risks and unsystematic risks.

Thus, the study opines that in emerging countries such as Sultanate of Oman which are characterized by weak investor’s protection mechanism will have an impact on the IDR. The study also indicates that the power of large shareholding will discourage foreign investors in holding and controlling of firms stocks. The volume of stock trading of small and foreign investors is weak in MSM as compared with other countries indicative of the dire need to revise the standards of MSM to encourage these investors to indulge more actively in stock trading in the market and this will in turn support the stability, safety, transparency, and supervision of the implementation of contracts, as well as paying attention to follow up the issues of small investors. Thus, the stability of financial market will encourage foreign investors to increase their investments in the Omani financial market through applying professional investment standards and the application of free market concepts.

The increase attention of these investors is reflected positively on the increase in confidence in trade transactions between countries as the strength of the Omani financial market contributes to the revival of a strong and positive image of the Omani economy and indicates that the procedures and regulation of internal and external trade are effective, thereby increasing the exports both in products and services as well as participation in oil and gas contracts. The recent slowdown in international financial markets has further contributed to the weakness of attracting investors, whether small or foreign investors, to enter the Omani financial market. Economic diversification is the key to enhanced growth of the economy and one of the initiatives could be the development of the tourism sector, through the creation of the adequate infrastructure and provision of services to encourage internal tourism movement, adoption of the system of integrated tourism centers and complexes, and attracting foreign capital to invest in tourism projects, thereby decreasing the dependence of the government on the contribution of oils sector on its GDP. All these measures help strengthen the Omani economy and contribute to the effectiveness of oil prices and improve the level of its exports sector.

The focus of our research study is on IDRs impact on banking sector three main pillars of growth in the financial and economic sector such as oil price, stock market, and fiscal factors. Our study is different from other studies as we seek to find and establish the impact of IDR on fiscal management factors and establish that in developing nations, it is one of the key drivers to managing and nations the public finances. This study aims to analyze the effect of IDR as a one type of risk in banking sector on OI, SMI, and FI of Sultanate of Oman. The OLS regression model indicates that there is a statistical significant impact on all of SMIs in MSMSP and MC, though only DOEs as OI are significant; on the other hand, the TEGDP is significant as FI at different significant levels 1%, 5%, and 10%. The data used is for the period of 2009–2015, which is a limitation of this study as a longer period could have justified the results even more.

The study strongly recommends that the government focus on stressing the importance of having a formal system to protect small investors which eventual will lead to increased investments in stocks. Moreover, the government should formulate policies in order to encourage foreign investors to invest in the capital markets of the country. This is only possible if enough attraction is created in order to induce foreign investors to invest in country’s financial stocks. The further areas of research inquiry could be additional focus on other variables both dependent and independent such as systematic risk, monetary indicators excusing financial modeling techniques.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.