Abstract

The financial industry plays a significant role in Mainland Chinese and Hong Kong economies and has aroused increasing managerial and academic interests in recent decades. Individual investors are becoming more cautious towards financial investment which makes it difficult for financial service providers to formulate marketing strategies after experiencing several financial crises. Prior research has suggested that financial investment behaviour would be affected by various factors, including the demographic characteristics of individuals; however, they seldom study the differences in financial investment behaviour between Mainland Chinese and Hong Kong investors or provide an easy-to-use approach for practical usage. This exploratory study aims at filling the identified research gap by proposing linear regression models of the financial investment behaviour of Mainland Chinese and Hong Kong investors. Based on the results of regression analyses, (i) there exist significant differences in financial investment behaviour between Mainland Chinese and Hong Kong investors, and (ii) investors’ psychological, sociological and demographic factors are significant predictors of their investment behaviour/preferences. Thus, financial service providers are able to predict the investment behaviour/preference of its customers and formulate marketing and strategic decisions, such as customizing the financial investment portfolio of customers on the basis of regression models built.

Introduction

As an international financial centre, Hong Kong offers a variety of financial products, such as mutual funds, stocks and bonds, for individual investors to invest. Due to the close proximity, low tax rate, similarities of language and culture and global access, Hong Kong remains the top offshore investment destination for Mainland Chinese investors. 1 These facts encourage the financial industry in Hong Kong to review marketing strategies for targeting this fast-growing market segment, that is, Mainland Chinese investors investing in the offshore Hong Kong market.

At the same time, individual investors are becoming more cautious towards financial investment and make it difficult for financial service providers to formulate marketing strategies after experiencing several financial crises. 2 Indeed, financial service providers face the challenge of understanding the investment behaviour and preferences of their customers for long-term benefits. 2 In order to have better market analysis and customer relationship management, various finance theories have been proposed by researchers.

Traditional finance theories assume that investment behaviour is rational. 3 However, well-known events such as the financial tsunami between 2007 and 2008, displaying apparently irrational behaviour, have caused a rethink in the domain, and the emerging field of behavioural finance has become a popular field of study in an attempt to explain this irrational behaviour. Under the theory of behavioural finance, researchers suggest that the investment behaviour of individual investors in real life is influenced by a combination of specific psychological factors, such as overconfidence, 4,5 representativeness 4 and herding behaviour. 6

The research focusing on psychological investment behaviour, however, steers away from sociological factors and personality traits. It seems investment behaviour is a complicated domain that combines both rational and emotional elements rather than just one. Furthermore, behavioural finance is not purely based on psychological factors but also sociological factors in the study of investment behaviour. 7 Moreover, demographic factors such as age and gender are also important in explaining investor behaviour. 8 Behavioural finance seems to explain reality and to provide a better framework in the way the investors behave. It is crucial to take psychological, sociological and demographic factors into account to explore the major attributes of how investors behave. 7,9

A review of the existing literature demonstrated that researchers focus mainly on identifying factors influencing investor behaviour and/or examining their impact on investment decisions. 10 –12 Studies seldom investigated how to predict investors’ preference based on the factors influencing their behaviour. This gap is probably due to researchers lacking access to the huge volumes of strictly confidential financial transaction data required to draw such conclusions from studying real behaviour.

In order to gain a deep understanding of investment behaviour of individual investors in Hong Kong and Mainland China, statistical analyses are applied in this study, aimed at identifying the differences in investment behaviour/preference between Mainland Chinese investors and Hong Kong investors and explaining investment behaviour determined by rational, emotional as well as demographic factors. Overall, several research questions are identified, including What are the factors in the difference of the behaviour identified in the previous literature? What are the major attributes to explain investment behaviour? How do the major attributes identified predict investors’ behaviour/preferences in Hong Kong and Mainland China?

Literature review and hypotheses development

Importance of understanding consumer behaviour in financial market

In today’s increasingly competitive business environment, a clear understanding of sophisticated consumer behaviour is a key element for ensuring success. There are many scholars who have examined the definition of consumer behaviour. In general, consumer behaviour is the study of customers and the processes they use to choose, consume and dispose of products and services that satisfy their needs and influence their experience. 13

Understanding the underlying mechanisms that to lead to these customers’ responses, therefore, helps business organizations make better managerial decisions, regarding providing the right product or service to their customers. 14 An in-depth understanding of consumer behaviour further helps business organizations to plan for the future buying behaviour patterns of customers and formulate the appropriate marketing strategies in order to build long-term customer relationships.

In financial markets, investors are the customers or consumers. Exploring the behaviour of investors is therefore important for financial institutions to devise appropriate strategies and to market appropriate financial products or offer new financial products to investors in order to better satisfy their needs. To study investor behaviour, researchers have largely adopted the concept of behavioural finance during the last decade. 3

Overview of behavioural finance

Behavioural finance refers to the application of psychology to finance. 15 Behavioural finance offers an alternative tool to study investor behaviour and the causes of market anomalies. Scholars have applied behavioural finance to explain financial market anomalies such as stock market bubbles, overreaction and underreaction to new information 16,17 that do not conform the traditional finance theory. For example, Shefrin and Statman 18 found that excessive optimism creates speculative bubbles in financial markets. Researchers also widely applied behavioural finance to explain emotional investor behaviour in recent years. Frankfurter and McGoun 19 also indicated that psychology and sociology is the essence of behavioural finance. However, according to the available literature described above, researchers have emphasized the importance of psychological factors and overlooked other factors in the concept of behavioural finance.

Other researchers support the view that sociological and demographic factors are also important to explain investor behaviour. 7,8 Though some researchers have studied the impacts of other factors such as gender or age on investment behaviour, these studies only explored the influences with regard to investor behaviour but did not discuss any findings about the financial decision-making process of investors or predict their preference on financial products. For example, Yang 20 investigated, through case studies, the influence of both gender and age differences towards financial investment behaviour in terms of overconfidence, account-open time and trade frequency. These studies within the field of behavioural finance provide evidence that demographic factors such as age and gender should be considered when studying investor behaviour.

Overall, in order to make the research closer to reality and to better comprehend the way the investors behave, this study took psychological, sociological and demographic factors into account to explore how and why investors behave differently. Identifying the major attributes to explain investment behaviour by leveraging psychological, sociological and demographic factors is thus essential for this study in order to address the gap in knowledge.

Key attributes influencing financial investment behaviour

In general, research in behavioural finance provides evidence that investors’ decisions are affected by behavioural factors. 21 Researchers found that investors do not behave in a merely rational manner across financial markets and there are a variety of factors influencing their decision-making in investment; among those factors, psychological factors, sociological factors and demographic factors are the major elements. 22 –24 To study behaviour under more realistic conditions and to better categorize the way investors behave, this study identifies and evaluates the major attributes in the literature explaining investment behaviour under three constructs, namely, the psychological factor, sociological factor and demographic factor, and how these attributes impact on the investors’ decision-making.

Key psychological attribute

Regarding the psychological factor, individual investors are driven by experience or through an investment appraisal process to make investment decisions. 25 –27 Past experience, as a consequence, affects investors’ risk perception in terms of attitude to risk and risk tolerance. 28 This is also supported by Byrne, 29 indicating the positive correlation between investment experience and risk. Researchers further pointed out that accumulated investment experience significantly affects investment decisions of individual investors in terms of anchoring bias and overconfidence. 30 These indicate that the investment experience of individual investors forms a strong basis for investment decisions and is therefore included in this study by considering it as an important psychological attribute that influences financial investment behaviour.

Key demographic attributes

According to Maditinos et al. 31 and Sadi et al., 32 the demographic factor is one of the behavioural factors that plays a significant role in determining the behaviour and decisions of investors. For example, demographic factors influence one’s choice of investment products. 33 –35 Kabra et al. 36 found that the main factors affecting investment behaviour and investors’ decisions are age and gender. According to Huberman and Jiang, 37 age and the amount of funds held tend to indicate a negative correlation. Age is always an essential factor and has a significant relationship with investment behaviour according to the literature and thus is included in this study.

Gender is another crucial demographic attribute that affects the investment decision-making process and investor behaviour. 38 Many researchers suggested that there are gender differences in risk attitude and thus in the choices of financial investment products. 34,39 Many existing studies supported that female investors are more conservative than male investors when investing and tend to show greater risk aversion than male investors. 39,40 For financial service providers to offer financial products which are best suited for investors of different genders, understanding the gender difference in the investment behaviour of individuals is crucial and thus is taken into account in this study.

Key sociological attributes

According to the extant literature, education level, 41,42 income level 3,42 and marital status 9,42 are found to be significant sociological attributes determining investors’ behaviour and influencing their investment decision. Al-Ajmi 41 conducted an exploratory study and concluded that income level and education level are positively correlated with risk tolerance. Shaikh and Kalkundrikar 42 conducted an exploratory study and confirmed that income level, education level and marital status are factors affecting investors’ behaviour and decision-making. Fares and Khami 43 identified that the education level of investors is statistically significant to investment decision. Rizvi and Fatima 3 also found a significant positive correlation between income and investment frequency. More studies revealing the significant relevance of these sociological factors, including education level, income level and marital status, in investment decisions and investor behaviour can be found in the literature. 43,44 With the support of the literature review, these three attributes, income level, education level and marital status, are considered in this study.

Table 1 summarizes all the psychological, sociological and demographic factors and attributes of behavioural finance considered in this study.

Factors and key attributes considered.

The literature discussion above highlighted that financial investment behaviour is commonly influenced by demographic, psychological and sociological factors, and the major attributes that explain investment behaviour are age, income level, educational level, gender, investment experience and marital status. However, little research has been devoted to the behaviour of individual investors.

45,46

Furthermore, Hong Kong is the top offshore investment destination for the Mainland Chinese investors. Investors in Hong Kong are mainly mixed, with Mainland Chinese investors and local investors having different characteristics. In order to answer the third research question identified in Introduction, the following hypotheses are proposed:

Regression models and data

Regression models

To explore the problems in understanding financial investment behaviour as well as to study the effects of the six variables, as identified from literature review, on investment behaviour of the Mainland Chinese and Hong Kong investors, a quantitative interpretation of the literature review was conducted for subsequent exploratory study. Based on the hypothesis, a table of variables is created (Table 2) and three regression models are constructed.

Notation of variables.

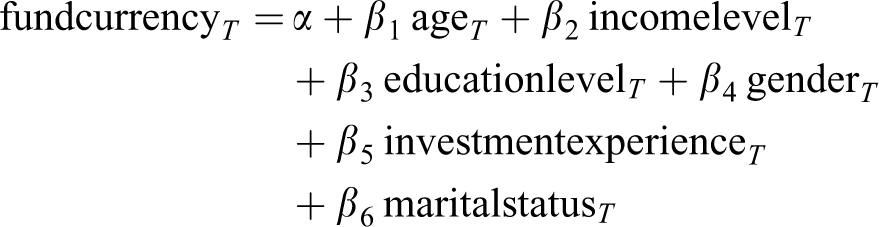

Model 1a

where the variable of the fund share amount held (

Model 1b

where the variable of the choice of country-specific financial investment options selected (

The first regression model helps give a general picture for understanding whether and how the six key attributes identified affect and predict the investment behaviour of both the Mainland Chinese and Hong Kong investors. In order to have an in-depth examination on the differences in investment behaviour between Mainland Chinese and Hong Kong investors, the second and third models are constructed to analyse how the six attributes identified affect investors specifically in Mainland China and Hong Kong in terms of the fund share amount held and choice of country-specific financial investment option selected, respectively.

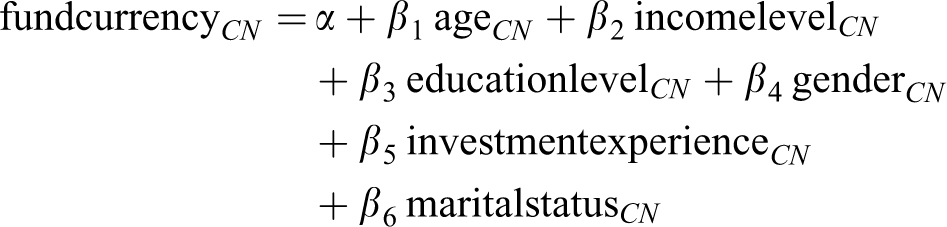

Model 2a

Model 2b

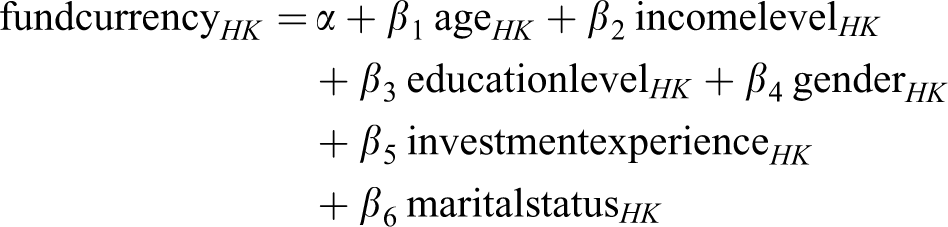

Model 3a

Model 3b

Data

To analyse how the major attributes identified under demographic, psychological and sociological constructs affect investors in both Hong Kong and Mainland China, financial transaction data and investors’ characteristics are collected and analysed to support this research. The data of customers from 2012 to 2014 were collected from a financial services provider listed in the Hong Kong Stock Exchange. In recent years, the number of its customers from Mainland China has been considerably increasing, and thus the institution desires to learn about the investment behaviour of mainlanders and understand the differences in investment preference between mainland Chinese and Hong Kong investors. This is the reason why the institution supports this research by providing the confidential data about its customers and makes this research possible by overcoming the obstacle – failing to access to the huge volume of financial transaction data that is confidential.

As the research aims to explore the individual investor behaviour, a relative large sample size is recommended in this kind of exploratory research for generating valid results. As mentioned by Saunders et al., 47 a larger sample size can help produce more reliable results as the samples can be more representative. In this research, 142,496 samples were collected from a financial services provider listed in the Hong Kong Stock Exchange, of which 87,057 samples were from Mainland Chinese investors and 55,439 were from Hong Kong investors.

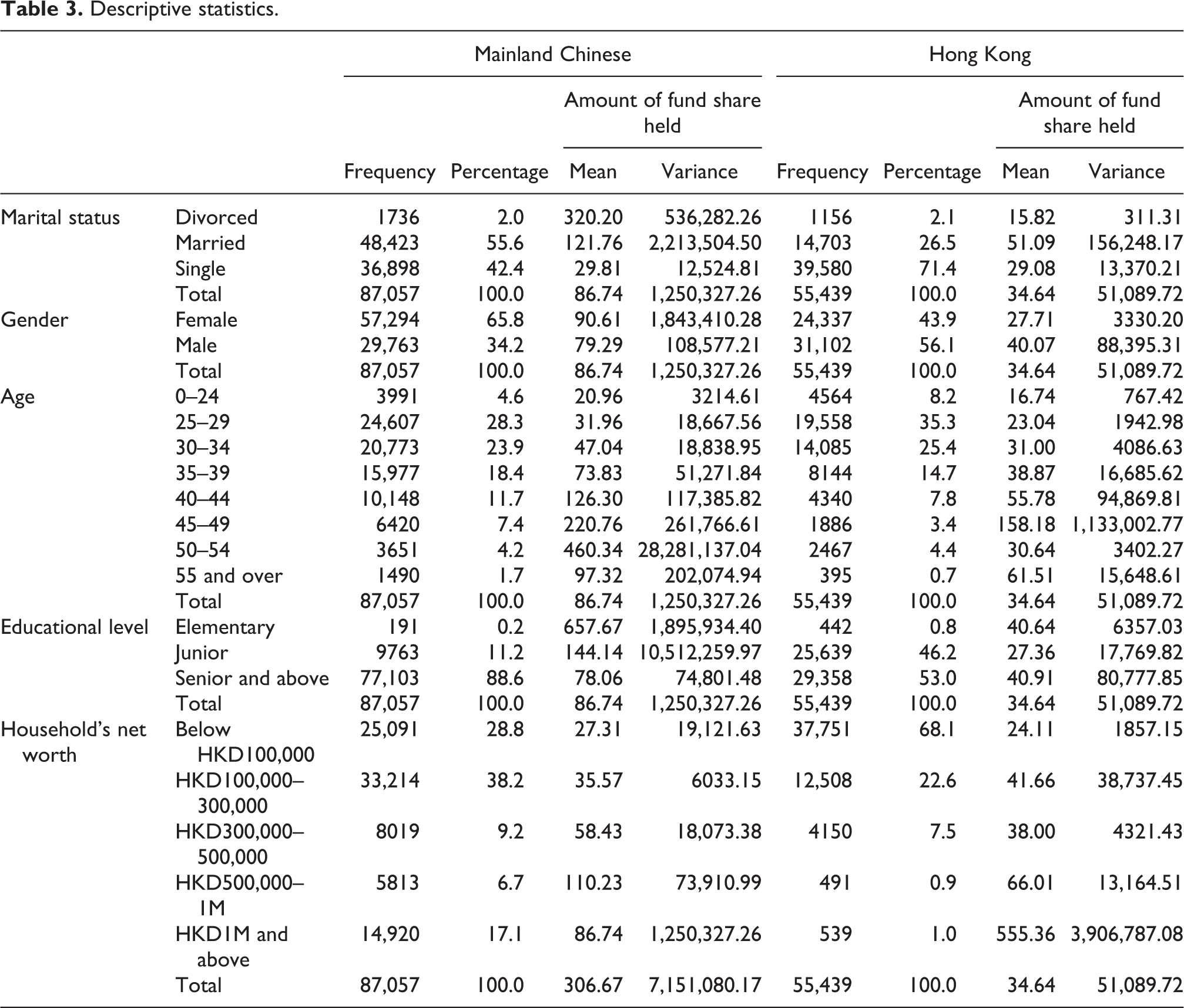

Table 3 provides descriptive statistics for investors’ characteristics.

Descriptive statistics.

Assumption analysis

To ensure the validity of the regression models, several requirements in applying multiple regression models, including linearity, multivariate normality, homogeneity of variance and multicollinearity, are tested. As mentioned by Poole and O’Farrell 48 and Antonakis and Dietz, 49 the models are only valid when these requirements are tested and satisfied. Before conducting the actual regression analyses, preliminary analyses are conducted to ensure the requirements for the regression models are fulfilled.

Linearity test

Figure 1 shows the significance of the linear relationship for model 1a. From Figure 1, the p value for all variables are <0.0001, indicating that significant linear relationships between all independent variables and dependent variable exist. Thus, the assumption of linearity for regression is fulfilled.

IBM SPSS Statistics (SPSS) output for multiple correlation coefficient.

Multivariate normality test

Figure 2 shows the histogram of the standardized residuals for model 1a. According to Stevens, 50 if residuals fit a normal curve, multivariate normality is not a problem. The histogram of the residuals of model 1a shows a symmetrical bell-shape and fairly normal distribution. Thus, the assumption of multivariate normality is fulfilled.

SPSS output for histogram of residuals.

Homogeneity of variance

Figure 3 shows the scatter plot of the residuals for model 1a. According to Osborne and Waters, 51 if residuals scatter randomly and close to the zero axis, homogeneity of variance is not a problem. Homogeneity of variance is not a problem for model 1a in our study as an almost horizontal band of points is scattered around and close to the zero axis, as shown in Figure 3. Thus, the assumption of homogeneity of variance is fulfilled.

SPSS output for analysis of residuals.

Multicollinearity

Figure 4 shows the values of the coefficients of determination (R 2) and variance inflation factors (VIF) calculated for model 1a. According to Hart and Sailor, 52 if tolerance (T), which is defined as T = 1 − R 2, is below 0.20, the multicollinearity problem is a severe problem. Furthermore, the attributes are moderately correlated if the value of VIF is between 1 and 5. 53 In our study, correlations are at acceptable levels as the T values for the six key attributes are over 0.20 and the VIF values are between 1 and 5. These indicate low multicollinearity and thus the assumption of multicollinearity is fulfilled.

SPSS output for the measure of tolerance.

Having fulfilled all the requirements, the multiple regression model 1a is confirmed to be valid and actual regression analysis is then conducted. Similar assumption analyses as discussed for model 1a are also conducted for models 1b, 2a, 2b, 3a and 3b, and all the requirements are fulfilled. In the next section, the results are reported.

Results and analysis

With the help of the 142,496 observation samples, regression analyses are conducted in this section to assess the relationships between the key attributes identified and the investment behaviour/preferences between Mainland Chinese and Hong Kong investors.

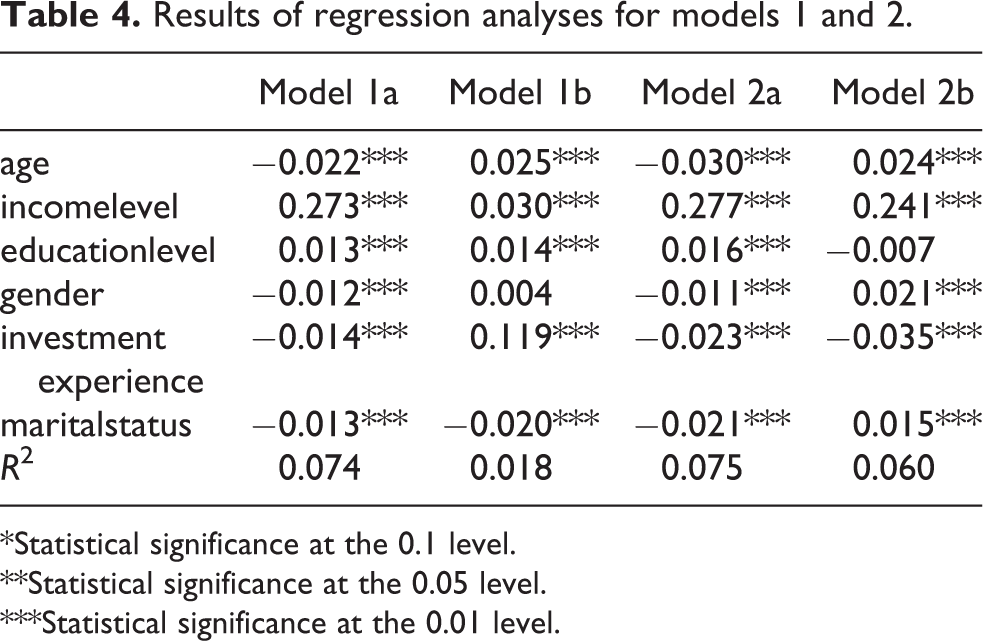

Tables 4 and 5 show the results for the standardized coefficients and adjusted R 2.

Results of regression analyses for models 1 and 2.

*Statistical significance at the 0.1 level.

**Statistical significance at the 0.05 level.

***Statistical significance at the 0.01 level.

Results of regression analyses for model 3.

*Statistical significance at the 0.1 level.

**Statistical significance at the 0.05 level.

***Statistical significance at the 0.01 level.

Effects of key attributes on investment behaviour/preference

From the regression results of model 1a (Table 4), all the six key attributes identified have a significant (at 0.01 level) effect on the fund share amount held when Mainland Chinese and Hong Kong investors are considered together. Thus, age, income level, education level, gender, investment experience and marital status are statistically significant predictors of the fund share amount held by Mainland Chinese and Hong Kong investors.

From the regression results of model 1b (Table 4), five out of the six key attributes, excluding gender (p value = 0.223 > 0.1), identified have a significant (at 0.01 level) effect on the choice of the country-specific financial investment option selected when Mainland Chinese and Hong Kong investors are considered together. Thus, only age, income level, education level, investment experience and marital status are statistically significant predictors of the choice of the country-specific financial investment option selected by Mainland Chinese and Hong Kong investors.

By leveraging the results shown in Table 4, it is concluded that the financial investment behaviour/preference of Mainland Chinese and Hong Kong investors, when considered together, are inseparable with regard to their demographic factor (i.e. age), psychological factor (i.e. investment experience) and sociological factor (i.e. income level, education level and marital status).

Effects of key attributes on the fund share amount held

From the regression results of model 2a (Table 4), all the six key attributes identified have a significant (at 0.01 level) effect on the fund share amount held by Mainland Chinese investors. Thus, it is confirmed that age, income level, education level, gender, investment experience and marital status are statically significant predictors of the fund share amount held by Mainland Chinese investors.

From the regression results of model 2b (Table 4), five out of the six key attributes, excluding education level (p value = 0.107 > 0.1), identified have a significant (at 0.01 level) effect on the fund share amount held by Hong Kong investors. Thus, only age, income level, gender, investment experience and marital status are statistically significant predictors of the fund share amount held by Hong Kong investors.

By leveraging the results shown in Table 4, it is concluded that the fund share amount held by Mainland Chinese and Hong Kong investors, when considered together, are inseparable with their demographic factor (i.e. age and gender), psychological factor (i.e. investment experience) and sociological factor (i.e. income level and marital status). The top three most significant attributes are age, income level and investment experience. The standardized coefficient of age is −0.030 for Mainland Chinese investors and 0.024 for Hong Kong investors. The standardized coefficient of income level is 0.277 for Mainland Chinese investors and 0.241 for Hong Kong investors. The standardized coefficient of investment experience is −0.023 for Mainland Chinese investors and −0.035 for Hong Kong investors. In spite of the differences in the magnitude of the three most significant attributes, the directions of the relationship are similar, except for age. For example, income level has a positive effect on the fund share amount held by Mainland Chinese and Hong Kong investors. However, age has a negative effect on the fund share amount held by Mainland Chinese investors but a positive effect on Hong Kong investors. In other words, younger Mainland Chinese and older Hong Kong investors tend to hold a higher fund share.

Effects of key attributes on the choice of the country-specific financial investment option selected

From the regression results of model 3a (Table 5), four out of six key attributes, excluding education level (p value = 0.141 > 0.1) and gender (p value = 0.325 > 0.1), identified have a significant (at 0.01 level) effect on the choice of the country-specific financial investment option selected by Mainland Chinese investors. Thus, it is confirmed that age, income level, investment experience and marital status are statically significant predictors of the choice of the country-specific financial investment option selected by Mainland Chinese investors.

From the regression results of model 3b (Table 5), five out of the six key attributes, excluding marital status (p value = 0.127 > 0.1), identified have a significant (at 0.01 level) effect on the choice of the country-specific financial investment option selected by Hong Kong investors. Thus, only age, income level, education level, gender and investment experience are statistically significant predictors of the choice of the country-specific financial investment option selected by Hong Kong investors.

By leveraging the results shown in Table 5, it is concluded that the choice of the country-specific financial investment options selected by Mainland Chinese and Hong Kong investors, when considered together, are closely correlated with the demographic factor (i.e. age), psychological factor (i.e. investment experience) and sociological factor (i.e. income level and marital status). The three most significant attributes are the age, income level and investment experience. The standardized coefficient of age is 0.015 for Mainland Chinese investors and −0.027 for Hong Kong investors. The standardized coefficient of income level is −0.020 for Mainland Chinese investors and 0.032 for Hong Kong investors. The standardized coefficient of investment experience is 0.140 for Mainland Chinese investors and 0.121 for Hong Kong investors.

Investment experience has a positive effect on the choice of country-specific financial investment options selected by both Mainland Chinese and Hong Kong investors. On the contrary, age and income level have different effects on the choice of the country-specific financial investment options selected by Mainland Chinese and Hong Kong investors. For example, younger Mainland Chinese investors and older Hong Kong investors tend to have the same choice of the country-specific financial investment option.

Table 6 summarizes the impacts of key factors and attributes on the investment behaviour of Mainland Chinese and Hong Kong investors. The table summarizes the relationship (direction and magnitude) between the key attributes, the fund share amount held and the choice of the country-specific financial investment options selected by investors.

Impacts of key attributes.

+: relationship in the positive direction; −: relationship in the negative direction; N/A: absence of a significant relationship.

Discussion

Practical and strategic importance of this research

With reference to the results of regression models 1 (Table 4), 2 (Table 4) and 3 (Table 5), there exist significant differences in the financial investment behaviour/preference, in terms of the fund share amount held and the choice of the country-specific financial investment option selected, between Mainland Chinese and Hong Kong investors. For example, the impact of age on the fund share amount held by and choice of the country-specific financial investment option selected by Mainland Chinese and Hong Kong investors is opposite. Similarities between the investment behaviour of Mainland Chinese and Hong Kong investors are also found. Particularly, the three most significant attributes, age, income level and investment experience, influencing investment behaviour for both Mainland Chinese and Hong Kong investors are the same, though the influence may in the opposite directions. Also, income level has a positive effect, while investment experience has a negative effect on the fund share amount held by investors.

In view of the similarities in investment behaviour for both Mainland Chinese and Hong Kong investors, financial service providers can utilize the findings to design and promote different financial investment products based on the demographic, psychological and sociological attributes, particularly income level and investment experience, of individual investors from Mainland Chinese and Hong Kong. The following targeted marketing strategy can be formulated: Target group 1: High-income investors

From the regression results of models 2a and 2b (Table 4), income level has a significant (at 0.01 level) and positive effect (0.277, 0.241) on the fund share amount held by both Mainland Chinese and Hong Kong investors. Financial service providers should therefore invest more money in advertising and strengthening their products, as well as designing a wider range of financial investment portfolios so as to attract these high-income investors to invest. Target group 2: Less experienced investors

From the regression results of models 2a and 2b (Table 4), investment experience has a significant (at 0.01 level) and negative effect (−0.023, −0.035) on the fund share amount held by both Mainland Chinese and Hong Kong investors. The possible reasons are listed below. As individual investors become more experienced, they become more conservative and show less enthusiasm in fund investment. Therefore, high-risk funds with a potential of offering higher returns are only attractive to less experienced investors. Financial service providers should then design higher yield funds and allocation funds so as to raise the investment interests of investors with less investment experience for the highest profits.

Furthermore, in view of the differences in investment behaviour between Mainland Chinese and Hong Kong investors, financial service providers can utilize the findings to design and promote different financial investment products based on the demographic attribute of age. The following strategy can be formulated for financial service providers to better tackle Mainland Chinese and Hong Kong investors: Target group 3: Hong Kong investors aged 45–49

The results of regression analyses of models 2a and 2b (Table 4) indicate that age is a statistically significant predictor for the fund share amount held by both Mainland China and Hong Kong investors. However, the results indicate that younger investors from Mainland China and older investors from Hong Kong hold a higher fund share. The results of descriptive analysis (Table 3) further identified that Hong Kong investors aged between 45 and 49 show great enthusiasm for investment and hold the highest fund share on average (i.e. 158.18 unit). Thus, Hong Kong investors aged between 45 and 49 should be the key age group for development and they are investors of great potential. Financial service providers should then invest more money in advertising and strengthen their products, as well as designing higher yield funds so as to attract these enthusiastic and high purchasing power Hong Kong investors aged between 45 and 49 to invest more in terms of frequency and money. In the following subsection, limitations of this research are discussed.

Limitations

In this research, financial transaction data and investors’ characteristics are collected from a single case company. Despite the fact that 142,496 samples were collected and used in the regression analyses, the empirical results may not represent fully the financial investment behaviour or investment preferences of all Mainland Chinese and Hong Kong investors, given the limited number of case companies. In the future, more financial transaction data and investors’ characteristics should be collected from other Hong Kong-based financial service providers to make the results more generalized and convincing.

Conclusions

The financial industry plays a significant role in the Mainland China and Hong Kong economies and has aroused increasing managerial and academic interest in recent decades. Unfortunately, after the financial crisis of 2008 and the global crisis of 2009, investors are becoming more cautious towards investments, especially in high-risk financial products. Furthermore, Hong Kong is the top offshore investment destination for the Mainland Chinese investors. Investors in Hong Kong are mainly mixed, with Mainland Chinese investors and local investors having different characteristics. These make it more difficult for financial service providers to understand customers’ financial investment behaviour and investment preferences.

Attempting to address the real-world challenges and research gap, this study has (i) empirically identified that demographic, psychological and sociological factors cause different investment behaviour and (ii) identified that the major attributes that explain and predict investment behaviour/preferences of Mainland Chinese and Hong Kong investors are age, income level, educational level, gender, investment experience and marital status. Regression analyses and data provided by one of the Asia’s leading financial service providers were used to help the financial industry formulate strategic and marketing strategies.

This exploratory study helps to fill the identified research gap and enable financial service providers to better understand their customers’ financial investment behaviour and investment preferences from the perspective of investors’ characteristics. With the huge volumes of confidential transaction data and investors’ characteristics available, the research results are believed to be able to reflect the real behaviour of individual investors from Mainland China and Hong Kong and can offer financial service providers a foundation for sustainable strategies formulation. In future research, it is suggested to extend the regression results to build a data mining model to market the most appropriate products to individual investors from Mainland Chinese and Hong Kong and to gain a better understanding of their financial investment behaviour in an effective and efficient manner.

Footnotes

Acknowledgements

The authors thank the editors and reviewers for their valuable comments and suggestions that have improved the quality of the article. The authors would like to thank the Department of Industrial and Systems Engineering, The Hong Kong Polytechnic University for their support in this work.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.