Abstract

The market for delivery of e-commerce parcels to consumers in Sweden is considered to exhibit high competition. Aggregate data from the Swedish Post and Telecom Authority shows the market shares, with the Universal Service Provider as the dominant actor with 50 %. We identify the market structure according to the dominant-fringe-firm model. In this study, we employ a disaggregated methodology to analyse the competitive situation concerning e-commerce delivery for consumer goods. We observe the delivery options provided by the 200 largest e-commerce companies, measured by turnover in 2022, to the urban parts of a medium-sized town in Sweden. By making ‘fake’ purchases online, we register the delivery companies offered by the different e-commerce companies, prices for delivery, and the purchase limit for free delivery. Consumers mostly have a maximum of three delivery companies as options, and in almost one third of the cases only one available option. Our study shows that the number of delivery companies significantly covariates with lower delivery prices for consumers. E-commerce companies without free delivery have a higher delivery price than those who have, and the limit for free delivery correlates positively with the delivery price. It seems that some e-commerce companies offer a low delivery price and a low purchasing limit for free delivery and others do not. Our study indicates that the market may be progressing to a more ordinary oligopoly with a few companies that might end up like intensive Bertrand price competition or like a Cournot one, with higher prices and profits. Regulatory authorities and competition authorities must carefully monitor the competitive conditions before allowing mergers; review and possibly advise against governmental subsidies; consider price or profit limitations, but at the same time protect the Universal Service Obligation.

Introduction

The parcels market is characterized by being more competitive than the letter market. In Sweden, the Swedish Post and Telecom Authority (PTS, 2023a) reports the Herfindahl-Hirschman index (HHI) for the volume of total domestic parcel deliveries in 2022 to be 3,000 and for Business-to-Consumer (B2C) domestic parcels to be 3,300. The values have fallen from 4,400 and 4,300 respectively since 2018 mainly because smaller distributors gain market shares from the four biggest ones. As a comparison, for the letter market in 2022, HHI is reported to be 6,200 (PTS, 2023b).

PTS (2023a) has identified a total of 14 companies in B2C parcel delivery in Sweden. Nine of these companies provide delivery through postal agents, with six ensuring coverage across all regions in Sweden. Twelve of them extend their delivery services to all regions, while eight cover all 290 municipalities in Sweden. The parcel delivery companies in Sweden in 2022 were (in order of market share) Postnord, Instabee, DHL, Schenker, Bring Parcels, Early Bird, Airmee, Best Transport, UPS, Asendia, Bussgods, Citymail, Fedex and Jetpak (Levin, 2023; PTS, 2023a). The overall conclusion is, according to PTS, that of intense price competition within the B2C segment. The Universal Service Provider (USP) Postnord has the biggest market share with 50-55 %. Instabee is a relatively new actor on the Swedish market, because of a merger in 2022 between Instabox and Budbee and has 10-15 % of the market. DHL, Schenker and Bring has 5-10 % each and the remaining delivery companies below 5 % each.

However, aggregate measures do not give the full picture of how competition works for single transactions. Distributors may be more established in specific areas, like Citymail in the letter market in Sweden, or for deliveries of specific products. In e-commerce, the companies selling the goods choose which parcel delivery companies to co-operate with, and they may only offer distribution by one or a few of the available distributors. In addition to fewer alternatives today, it could also result in weaker competition and even fewer delivery alternatives in the long run.

To understand more about competition, we apply a disaggregated approach. The object of our study is domestic parcel deliveries to private consumers (B2C). We measure the choice opportunities for the consumers for parcel deliveries in Sweden regarding e-commerce for goods that are sufficiently small to have parcel box as a possible option. Delivery options may change over time and the options today will affect those available in the future. In the short run it is probably most important for the consumers which options they have in form of delivery: to their home, to a parcel box, or delivery to a postal agency, and the price for the different alternatives. Which company that carries out the delivery probably matters to a much smaller degree for the consumers. In the long run though, service quality and price could be highly dependent on the number of delivery companies that each e-commerce companies co-operate with today, their cost-structures and competitive strategies. If the number of delivery companies becomes smaller over time this could mean fewer and more expensive delivery options for the consumers. To find out what might happen in the future we focus on the delivery companies offered by the different e-commerce companies together with delivery prices and their variation.

A deeper knowledge about competition based on a disaggregated approach can complement the aggregate measures of competition on the national level. As many other industries in the transport sector, like rail or air transportation, aggregate market shares may overestimate competition on a certain route or connection, or for a specific product or place, where few or even only one operator provide services. There is detailed knowledge about receivers’ distances to access points like letter boxes or postal agents (see e.g. PTS, 2023b). However, if consumers’ choices in practice are limited to few or only one distributor, the accessibility may decline over time. If many e-commerce companies only offer few of the available parcel delivery companies, few distributors may survive in the long run. An oligopoly with less intense competition may arise. This could result in worsened service and to higher delivery prices especially as the price for delivery is only a smaller fraction of the total price paid for the product. The results of a disaggregated study can therefore provide a more complex picture of the market structure and have policy implications for the provision and financing of the Universal Service Obligation (USO) and the need for revised regulation of the parcels market. The applied methodology can be used as a model for similar studies about other markets or in other countries.

The overall objective of this study is to analyse the competition in e-commerce parcels delivery in Sweden. The next section analyses the current market structure in Sweden with the dominant-fringe-firm-model. The following setion describes in detail the data collection in this study and compare it to some previous similar studies. Then the result of our empirical study is presented. The section after that discusses the results and what might happen with competition and prices in this market in Sweden and comparable countries in the coming years, some policy implications and proposals for future research.

Market Analysis

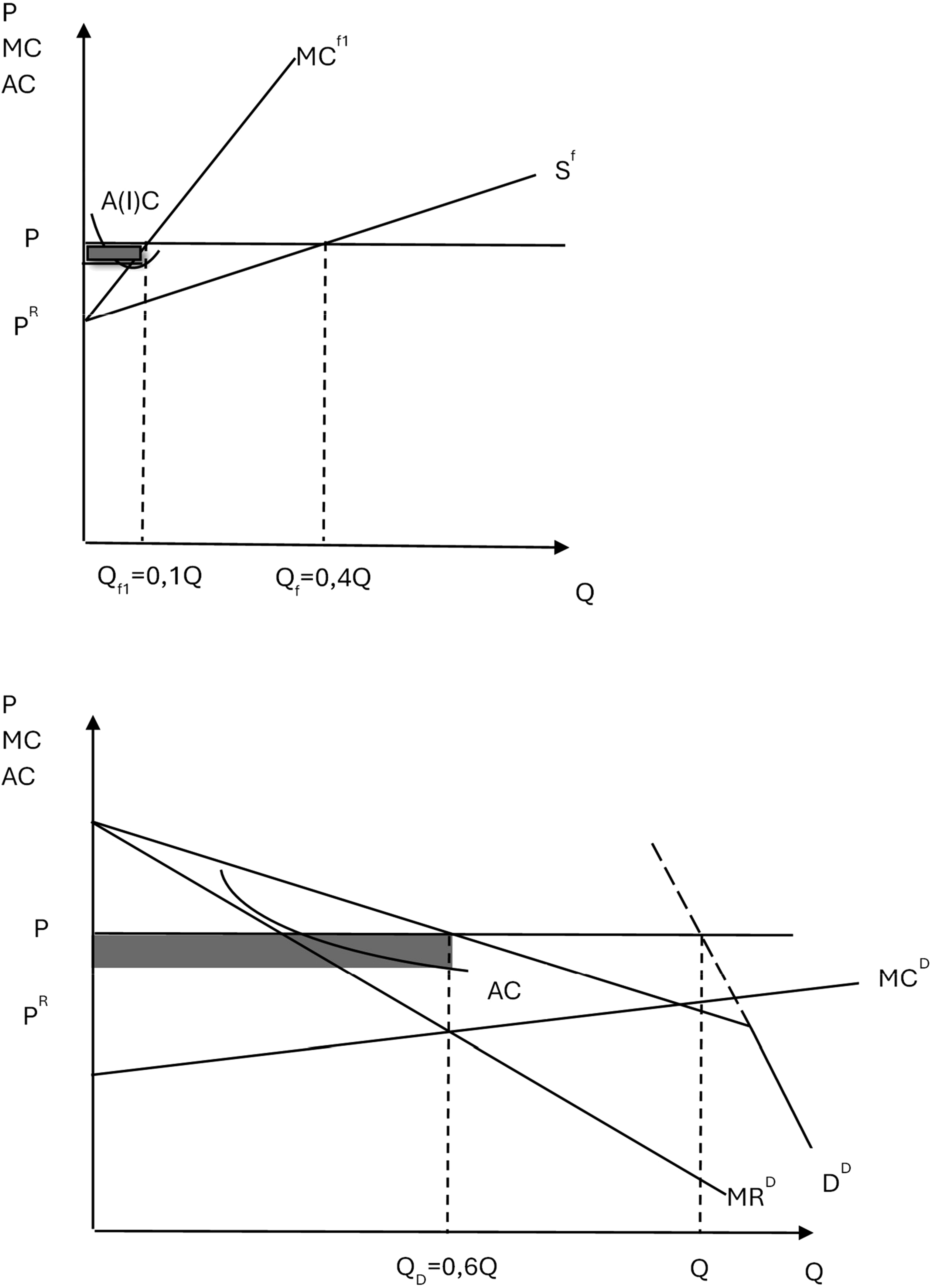

Considering the existing market shares in the studied industry, with Postnord as the dominant actor with over 50 %, three other actors sharing most of the rest, and a number of small firms, we apply a standard dominant-fringe-firm-model (see e.g. Carlton and Perloff, 2015) to analyse the current market structure. Despite being a state-owned firm, Postnord is profit-maximizing (Postnord, 2022), and the other, private actors can be expected to be the same. In Figure 1 we illustrate the current market structure where the upper section shows the fringe firms and the lower section the dominant firm Postnord. A Model of the Current Competitive Situation

The dominant firm is in the model assumed to have lower costs than the rest and to be the price setter. The solid demand curve in the lower section represents the residual demand curve for Postnord. The residual demand curve is the part of the market demand not supplied by the other firms in the market. The reservation price is the price needed for the other firms to cover their costs. If they do not cover their costs they will leave the market. Below the reservation price (PR) it will have monopoly as no other firm can cover its variable costs below this price. Above this price, the dominant firm’s residual demand is the total demand minus the supply from the other firms. In the upper section, the marginal cost curve of one fringe firm (MCf) is its supply curve. The total supply from the fringe firms (Sf) is here supposed to be the sum of four individual actors. This could represent Instabee, Schenker, DHL and the total of the remaining small firms.

The dominant firm maximizes its profits at the quantity QD where its marginal revenue equals its marginal cost. The price is determined by its residual demand curve. The more fringe competitors, the flatter the residual demand curve will be and the force of competition on limiting the price will be stronger. The market price (P) set by the dominant firm becomes the same for all operators. Each fringe firm produces the quantity where this price equals its marginal cost, so one firm produces Qf1 and the total supply from the fringe firms is Qf. Together, the supply from all firms equals total market demand. The figure is drawn so the dominant firm, representing Postnord, has a 60 % market share and the other three larger and the small fringe firms have ten percent each, which approximates the current situation according to PTS’ data.

The possibility to make profits is determined not only by the variable costs, shown by the marginal cost curves, but also the fixed costs. The total average cost (AC) consists of total variable and fixed costs divided by the quantity. As postal services have significant fixed costs, average costs will fall as long as they are larger than the marginal cost. In the figure, we have sketched AC-curves for the firms illustrating this relationship and the resulting profit is marked. The profit can be calculated as total revenue minus total costs and is illustrated as average price minus average cost multiplied by quantity. For firms having economies of scope, like DHL and Schenker who also delivers heavier goods, this curve should be interpreted as the average incremental cost (AIC), i.e. the additional cost per unit for those firms from providing parcel delivery given that they already deliver other goods. The size of the profit depends on the produced quantity, economies of scale and scope, and differences in variable costs.

In the current situation with one dominant firm, this firm can be expected to be the price setter with the restriction on price given by the other competing firms. This model indicates that the price competition is not as strong as it may appear. If the market will grow towards more evenly distributed market shares, a standard oligopoly model would become applicable. What happens then depends on the competitive strategies from the firms involved. If they engage in Bertrand competition, the firms will try to compete with price and undercut the other firms’ price as long as they cover the total costs. This may become an intense competition to benefit the consumers. If they compete according to the Cournot model, the firms will on the other hand determine their quantity (capacity and where to deliver) to maximize their price and profits given all other firms actions at the expense of the consumers.

Methodology

Data Collection

We apply the disaggregated methodology by choosing the 200 largest e-commercial companies measured by turnover in 2022 for consumer goods in Sweden and study the delivery companies offered by each e-commerce company for two urban addresses in the medium-sized Swedish town Linköping. Based on a list of the 250 largest e-commerce companies (Market.se, 2023) we choose from largest to smaller until we have 200 companies that fit our restrictions. 1 Companies that mainly sell their goods over the counter in their stores are not included in the list. In this study we exclude some companies due to selling food, only selling goods that is too large to deliver in a parcel box, only selling very expensive goods that will not be delivered in a parcel box and to bankruptcy. 2 We collect 200 observations by making ‘fake’ purchases online from the largest 200 e-commercial companies for consumer goods in Sweden. We select one item from the company’s website and carry out all steps up to the last which is the payment when we cancel the order. All the possible options regarding available delivery companies, their prices, and if and under what condition delivery is free for the customer are documented. We choose a good that is small enough to be delivered in a parcel box with a value below the free shipment threshold. 3

All offered delivery companies are registered, and their cheapest delivery alternative if any of them offer more than one way of delivery. If the company does not clearly state the limit for free delivery (always, above a certain purchasing amount, or never) we test to find the limit of free delivery up to 2,000 SEK 4 and after that assume that delivery is never free.

The data were collected in the weeks 2-5 2024 to two addresses in the urban parts of the medium-sized Swedish town Linköping. The available delivery companies for a consumer at a specific address might differ due to locality. By choosing central urban addresses with all available delivery companies as possible delivery options, we are aiming for the largest number of alternatives for the consumers. Rural delivery options are probably fewer. The reason to choose the largest e-commerce companies is that they can be expected to cooperate with the largest number of delivery companies. Smaller companies may be expected to sign delivery contracts with fewer delivery companies than the largest do. Thus, we intend to map the upper level of delivery options given to consumers when e-shopping consumer goods.

Similar Studies

Copenhagen Economics (2023) made a comparative analysis of the possibilities for parcel delivery services in rural and urban areas in Sweden, with a particular emphasis on the practical availability of diverse parcel distribution options to consumers. The primary focus was directed towards the extent to which consumers could choose among multiple parcel delivery services. They conclude that competition among e-commerce companies is anticipated to drive them to select the delivery operator capable of providing the most favourable terms, encompassing both expeditious delivery and cost-effectiveness. Consequently, if a particular e-commerce company extends a specific delivery option to its customer base, it is plausible to expect a parallel offering from comparable e-commerce companies. Their conclusion could indicate that if each e-commerce company today only offer a few of the available delivery companies, in the long run most e-commerce companies will offer the same few of them. This could lead to the other competitors leaving the market in the long run with less competition and worse delivery service.

Hägglund and Wikström (2023) sent a questionnaire to ten parcel delivery companies and 25 randomly selected relatively small e-commerce companies. They also carried out ’fake’ online shopping to one address from the 25 randomly selected e-commerce companies. Their conclusion was that e-commerce companies have incentives to exclusively provide parcel delivery services through a single delivery company and that e-shoppers are confronted with a limited number of delivery options and a few selections of delivery companies to choose from. They conclude that there is an opportunity for both e-commerce companies and parcel delivery companies to raise their prices.

According to Cardenas et al. (2017) more efficient logistics in urban areas is important for the success of e-commerce. In densely populated areas the last mile of delivery means pollution and congestion. Parcu et al. (2023) point out that e-commerce companies, delivery operators and traditional postal operators compete in the growing dynamic e-commerce market, where delivery is an important part. They find that Amazon is vertically integrating delivery, while smaller e-retailers are less interested to deliver themselves. Strobel et al. (2023) consider the decline in letter volumes and the increase in parcel volumes to see how the Universal Service Provider will be affected. They point out that the degree of competition in the market for parcel distribution in different countries will be important for the sustainability for their USP. Jaag and Finger (2017) describes different strategies applied by the USP in different countries to meet the challenges of digital competition and decreased mail volumes. The US Postal Services go on to focus on their traditional business with mail and parcels, while the focus for the Swiss Post and New Zealand Post is to develop their post office networks and also develop hybrid and digital services.

While Copenhagen Economics in a small part of their study also incorporated a sample of five e-commerce companies and Hägglund and Wikström included 25 randomly selected relatively small e-commerce companies to one address, our sample is the 200 largest e-commerce companies for consumer goods in Sweden, based on turnover. Our study provides a more comprehensive picture of competition than the previous ones.

Results of Our Study

Presence of the Delivery Companies for Consumers

According to PTS, there are 14 delivery companies within the B2C segment in Sweden. Our study finds one additional delivery company: DSV, but in total only eleven. There are no delivery options from Asendia, Jetpak, Bussgods or Fedex. The two former ones do not cover all municipalities in Sweden which can explain why they were not present in our study. However, both Bussgods and Fedex have parcel delivery in all 290 municipalities in Sweden (PTS, 2023a). All the eleven available delivery companies offer home delivery (Airmee, 2024; Best, 2024; Bring, 2024; Citymail, 2024; DHL, 2024; DSV, 2024; Early Bird, 2024; Instabee, 2024; Postnord, 2024; Schenker, 2024; UPS, 2024). Bring, Citymail, Instabee, and Postnord offers parcel box. The parcel box network has grown rapidly in Sweden since 2020 (PTS, 2023b). In 2020 there were a network with 134 parcel boxes and in 2023 there were a network with 7017 parcel boxes. Postnord has increased their parcel box network with 300 % between 2022 and 2023 and Instabee has 2023 parcel boxes in 285 of 290 Swedish municipality’s. Delivery to a postal agent is available from Bring, Citymail, DHL, Postnord and Schenker. Table A3 in Appendix 3 shows these possible delivery options by the delivery companies present in our study.

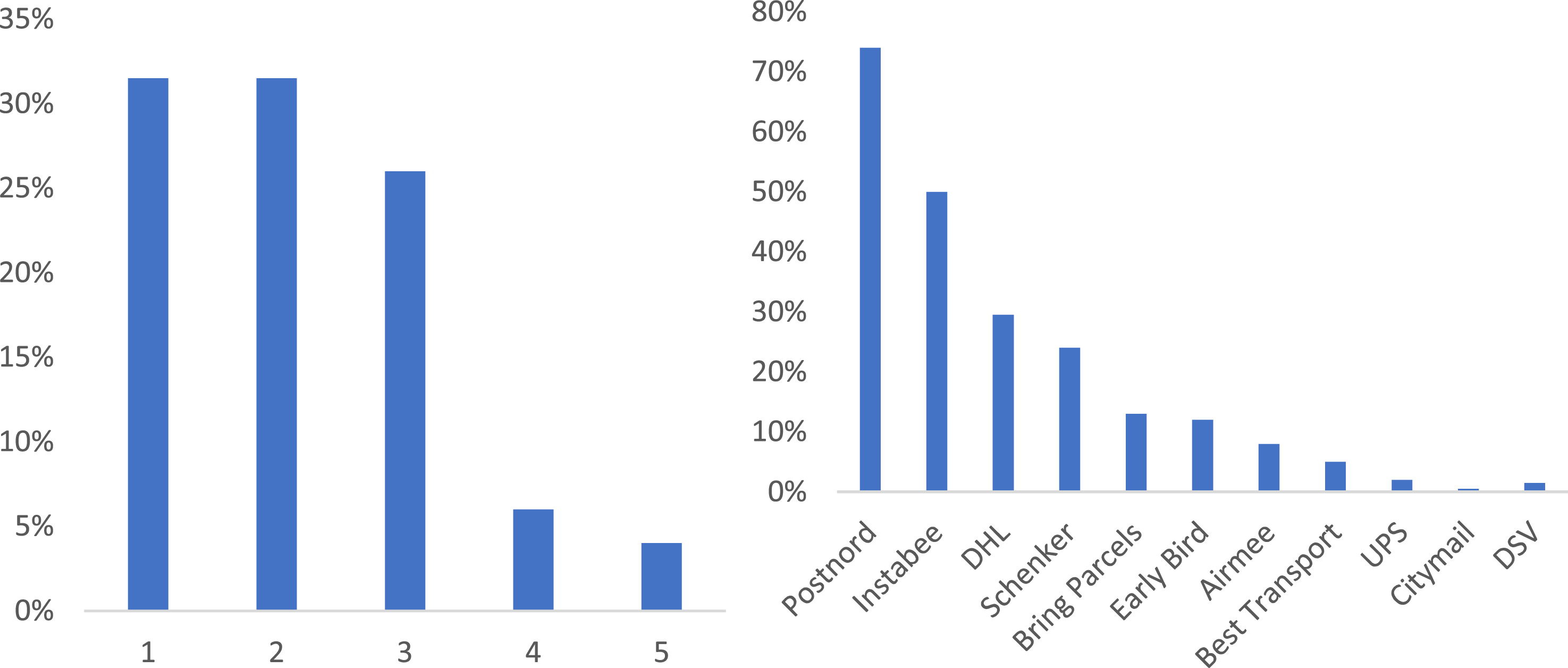

Our examination has not accounted for potential variations in services offered by a single company, such as door delivery or postal box delivery. We only register which delivery companies each e-commerce company offer and the cheapest option by each delivery company. Figure 2 underscores that a significant proportion of e-commerce companies offer only one, two or three distinct delivery companies to the consumers, and that Postnord emerges as the predominant delivery company, featured in over 70 % of the cases. Additionally, Instabee enjoys a notable presence, being offered in 50 % of the cases. Number of Available Delivery Companies From Each e-Commerce Company, in Percent (to the Left). Availability of Different Delivery Companies, in Percent (to the Right)

It is important to acknowledge that our sample originates from two central addresses within the municipality of Linköping. Nevertheless, despite this urban concentration, a significant portion of e-commerce establishments continue to limit their delivery options to three or fewer delivery companies. It is plausible that the availability of diverse delivery services may be even more restricted in rural areas. The findings presented in Figure 2 underscore that within the central parts of Linköping, consumers are predominantly presented with a choice among one or more out of only four delivery companies: Postnord, Instabee, DHL and Schenker. Notably, UPS and DSV emerged as available options in merely 2 % of the e-commerce companies’ delivery options, while Citymail featured in only 1 %. From the data in Figure 2, it appears as four delivery companies collectively hold a significant market share in parcel delivery services. Despite Instabee’s reported market share of 10 %–15 % of the total market, according to PTS, our data show that Instabee holds a strong position as an available option in the e-commerce parcel delivery market in Linköping.

The number of delivery companies offered to consumers by e-commerce companies might depend on their size. Table A4 in Appendix 3 shows that it seems to be a correlation between the number of delivery companies and the size of the e-commerce company. On average 2.20 delivery companies are offered by the 200 e-commerce companies. The one hundred largest offers on average 2.33 delivery companies while the 100 smallest of them on average offer 2.06 delivery companies to consumers.

Price for Delivery for Consumers

It cannot be determined if the price for delivery is the same as the price the e-commerce companies pay to the delivery company for a specific delivery. However, we assume that they treat all delivery companies equally, with the same mark-up, thus making the offered delivery price reflecting the price paid to the deliverers.

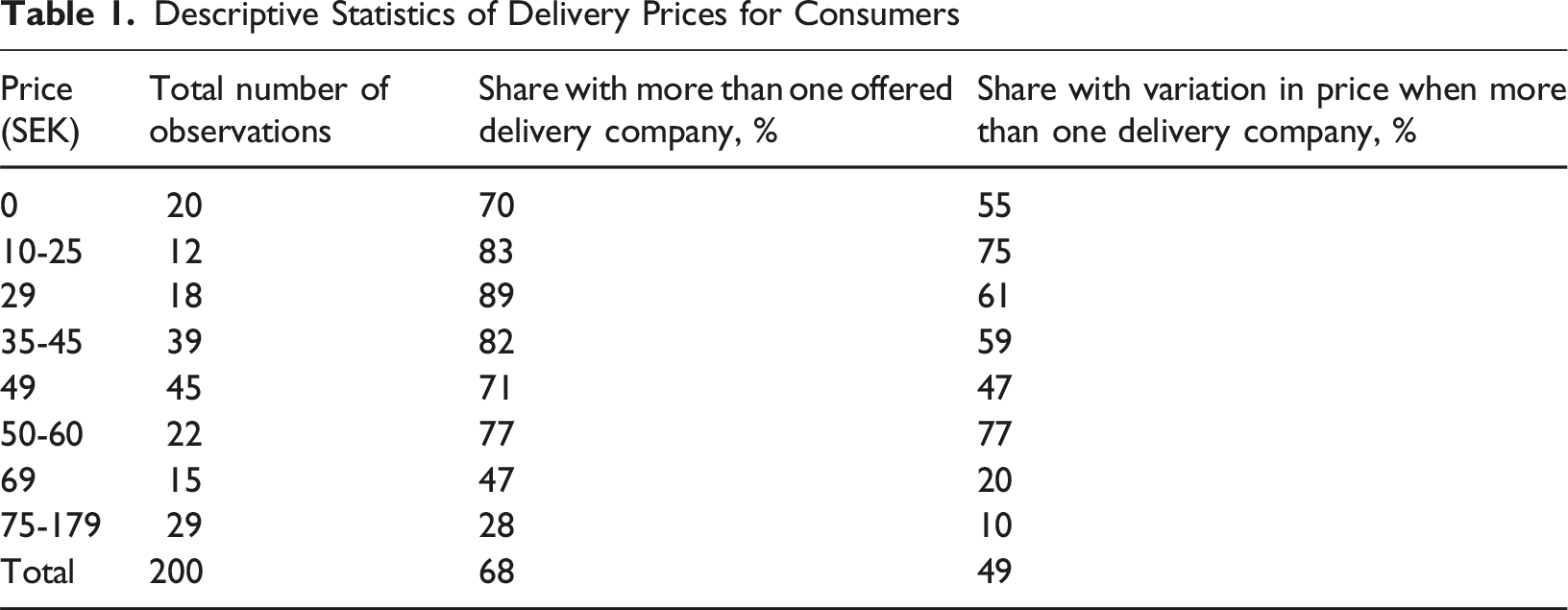

Descriptive Statistics of Delivery Prices for Consumers

Prices With Different Number of Delivery Companies

Delivery Price With Different Number of Delivery Companies, Based on Table A5

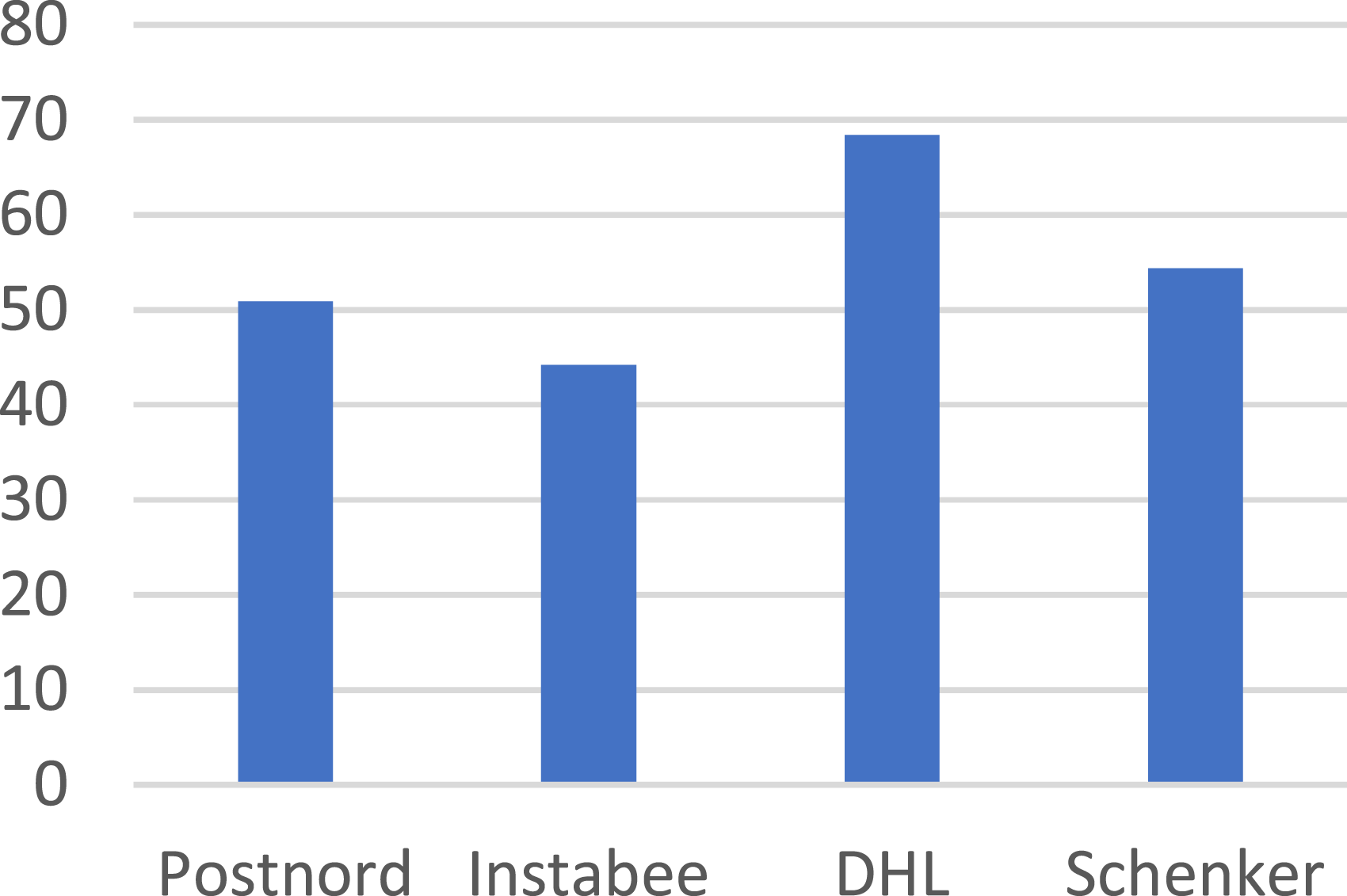

To further evaluate the possible impact of competition on pricing, Figure 3 presents the average prices offered by the four most offered delivery companies in our study. Notably, Instabee has the lowest average price at 44 SEK, while DHL has the highest at 68 SEK. It is worth noting that Early Bird offers an even lower average price of 35 SEK, a data point excluded from Figure 3. The Average Delivery Price From the Four Largest Delivery Companies

Upon close examination of the pricing dynamics between the two leading delivery companies in this study, it becomes apparent that when both Postnord and Instabee are available as options from e-commerce companies, their average prices are practically identical. Postnord’s average price stands at 43.4 SEK, closely paralleled by Instabee’s average price of 43.7 SEK.

Tables A6-A9 in Appendix 3 focus on the four most frequently offered delivery companies to show how often they are the sole delivery company, how often they are one of two or more delivery companies and how often they in that case are more expensive than the lowest offered price. Postnord, which is an offered delivery option by 75 % of the 200 e-commerce companies, is the sole delivery company in 23 % of those cases. Their offered price to the consumers is higher than the lowest offer in 37 % of the cases when they are one of at least two delivery companies. Instabee, which is an offered delivery option by 50 % of the e-commerce companies, is never the only delivery company. This might explain why their average price is lower as presented in Figure 3. Their offered price to the consumers is higher than the cheapest offer in approximately one third of the cases when they are one of the delivery companies. DHL, which is an offered delivery option by 30 % of the e-commerce companies, is the sole delivery company in 25 % of those cases. Their offered price to the consumers is higher than the cheapest offer in 59 % of the cases where they are one offer among others. Finally, Schenker is the only offered option in 13 % of the times they appear, which is by 24 % of the e-commerce companies. When more than one delivery company is offered, they are more expensive in 19 % of the cases.

Purchasing Limit for Free Delivery for Consumers

E-commerce companies have different limits for how much the consumers must order for to receive free delivery. Table A10 in Appendix 3 shows numbers and shares with different limits for free delivery. It can be concluded from the table that the limit for free delivery varies a lot. Ten percent of the e-commerce companies always offer free delivery, while 26 % never does. There is a trade-off between attracting customers by always offering free delivery, inducing each customer to order more to receive the free delivery, and financing of the delivery cost by having the customer pay for it separately instead of including it in the price of the consumer goods. The strategy applied by the e-commerce companies are obviously differing.

Free Delivery Under 2,000 or not and Number of Delivery Companies Offered by the e-Commerce Companies

Table A11 in Appendix 3 shows an OLS regression that also includes a dummy for not offering free delivery, at least not for any purchase amount up to 2,000 SEK, while Table A12 shows a model that instead includes the limit for free delivery for the 148 e-commerce companies that have a limit that is 2,000 SEK or lower. Tables A11 and A12 shows that the number of delivery companies offered by e-commerce companies and a lower purchasing limit for free delivery for the consumers both significantly covariates with a lower delivery price. This implies that fewer delivery companies coincide with both a higher price for delivery and a higher purchasing limit for free delivery or no free delivery at all.

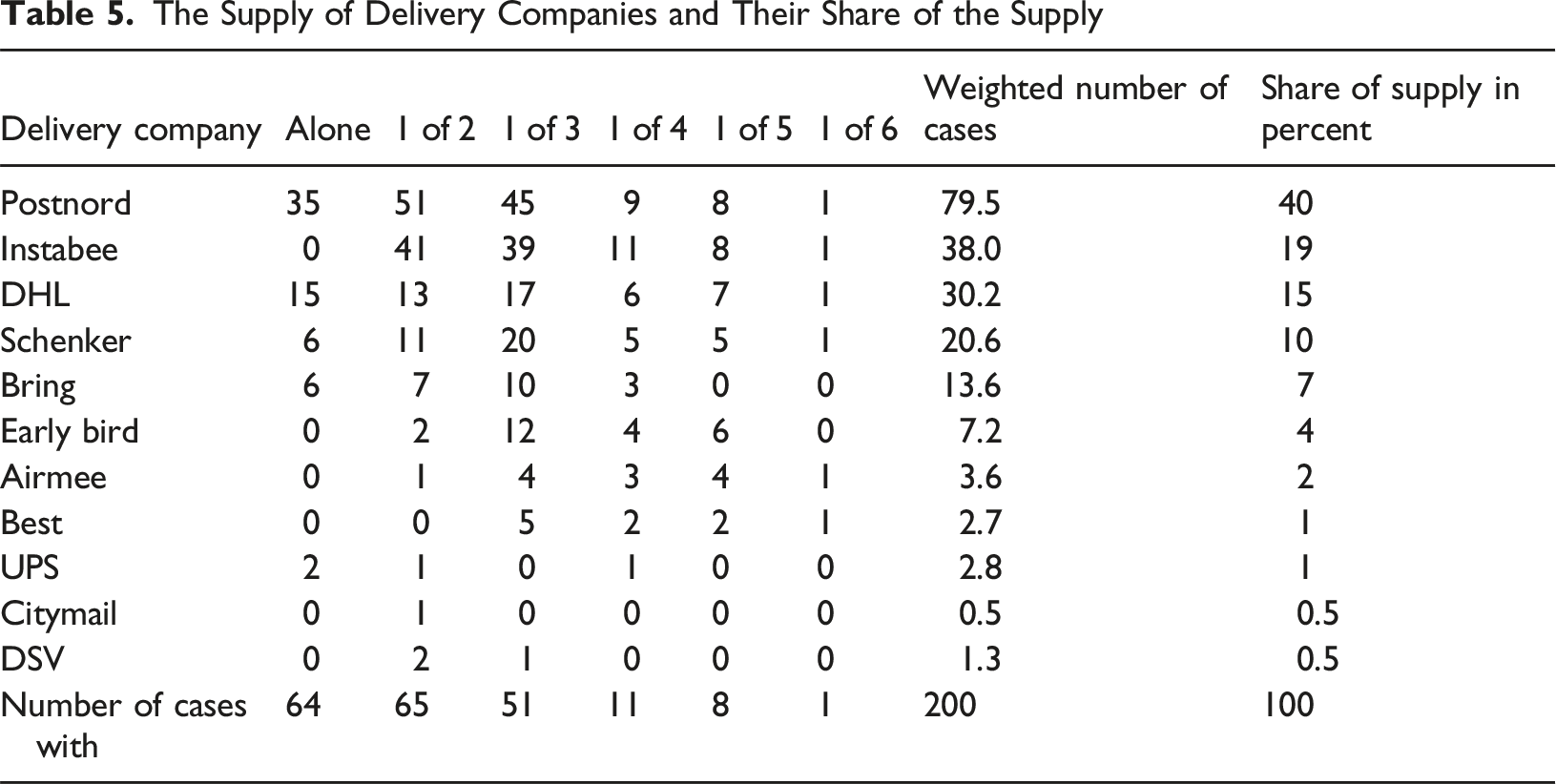

Supply of Delivery Companies to Consumers

The Supply of Delivery Companies and Their Share of the Supply

The weighted number is calculated as in the following example: Being one of five offered delivery companies eight times gives a weighted number of 1.6. To be a share of supply this is divided by 200. Which delivery company the consumers will actually choose will also be affected by the variation in delivery price by the different delivery companies, and the market share will also be affected by the size of the e-commerce company. Table 1 showed that there is a variation in price for 49 % of the e-commerce companies that offer more than one delivery company.

Discussion

Conclusions

The disaggregated approach turns out to support some of the national data but provides new evidence about variations in the supply and prices compared to the overall picture. We can observe eleven active e-commerce delivery companies in our study, three fewer than in the data from PTS. There seems to be a trend towards consolidation with four companies (Postnord, Instabee, Schenker, DHL) having the vast part of the market. In PTS statistics these firms together have near 5/6 of the market, and 84 % of the supply in our sample, considering the weighted shares presented in Table 5. The remaining companies make up the rest with Bring and Early Bird being the only more significant ones. Even the supply of the individual company is similar to their market shares according to PTS. Postnord has a somewhat lower supply and Instabee and DHL holds a higher supply in our study compared with their national market share in 2022. This may be explained by our focus on the central parts of a town and not knowing how price differences affect the choice by consumers. Thus, the dominant-fringe-firm model introduced in the second section appears to be supported not only by PTS figures but also from our study. It could also point at the beginning of a future change to only four companies with more equal shares.

Consumers typically have no more than three delivery companies as options; in nearly one third of the studied cases there was only one available option. Even if there are 14 companies altogether on the market, in practice our study underlines that the market is mostly in the range from monopoly to three competing ones. Moreover, the share with more than one option clearly decreases with a higher price of delivery. In our study, Postnord was the sole deliverer in 35 of the 200 observations and was not an offer in 50 of them. DHL was the sole deliverer in 25 % of the cases they were among the options and Schenker in 13 %. Instabee was never the sole delivery option.

From our study, it appears as Postnord and Instabee competes intensely with price. Even if Postnord has a somewhat higher price on average, when both companies are available options, the price is virtually the same. Schenker and most notably DHL have somewhat higher prices. Postnord had an offered price that was higher than the lowest in 37 % of the cases where they were among the delivery options. The same number for Instabee, DHL and Schenker were 34 %, 59 % and 19 % respectively. As the latter have higher prices on average, it suggests that they only offer delivery when their price is fairly competitive. Offering free delivery is a strategic choice for the sellers as they on the one hand can trigger consumers to buy more, but on the other hand may lose revenues or rise prices for the goods. Our study finds new evidence that those without free delivery also have a higher delivery price than those who do have a limit, and that the limit for free delivery correlates positively with the delivery price.

Our study shows that the number of delivery companies significantly covariates with lower delivery prices and that the purchasing limit for free delivery also significantly covariates with the delivery price. It seems that some e-commerce companies offer a low delivery price and a low purchasing limit for free delivery and others do not. One possible explanation is that some e-commerce happens to (or strategically choose) to co-operate with several delivery companies and therefore can negotiate a lower delivery price they pay them. Our study indicates that the number of delivery companies offered to consumers increases with the size of the e-commerce company. Another explanation could be that the competition is higher in some e-commerce industries and therefore the companies in those industries co-operate with more e-delivery companies to be able to compete with lower delivery costs. A third possible explanation is that industries that have lower delivery costs attract the most delivery companies that wants to deliver. This would be an interesting area for future research.

Future Policies

It can be assumed that parcel volumes will continue to grow, although in a smaller rate than before, especially compared to the years during the pandemic, not only in Sweden but in comparable countries. Will the market shares of the current operators remain the same on a growing market, if not how and why will they change? Two trends are possible: either a consolidation between existing firms or increased competition as the market expands. It is important that regulatory authorities and competition authorities carefully monitor the market and make careful considerations before allowing mergers; review and possibly advise against governmental subsidies to specific delivery companies. They should monitor the competitive conditions and at the same time ensure that the Universal Service Obligation is fulfilled.

In Sweden, will Postnord’s dominant position remain, be strengthened, or weakened? Postnord is struggling with falling letter volumes and the financing of the universal service obligation concerning services in sparsely populated areas. Parcel delivery needs to be an important source of revenue. Postnords investment in parcel boxes might be a strategy to try to uphold their market share. In our study, Postnord appears as an alternative in the majority of the cases. Can the other companies increase their market shares by being able to reduce costs or benefit from economies of scale or scope due to increasing volumes? The Post and Telecom Authority needs to balance the USP’s need for making profits with preserving competition. The current regulation with prices related to costs for each products limits the scope for the USP cross-financing between different products thus easing the provision of the USO. Future regulation may open for more application of Ramsey-pricing to avoid cost-enhancing subsidies. (Andersson and Ivehammar, 2024).

Another intriguing question is how the major three other companies can survive with smaller market shares. Is it because they rely on economies of scope (DHL and Schenker are mostly active in the market for delivery of heavier goods) or from economies of density and lower absolute costs (Instabee is most present in densely populated areas and do not work with postal agents)? Two other possibilities are either that Postnord has large profits from parcel delivery while the others have satisfactory profits, or that the other delivery companies might leave the market in the long run. After the removal of the state monopoly in the letter market in Sweden in 1993, a large number of new postal companies started business, mostly on local markets. At the most, around 100 had acquired a license from PTS. Fairly quickly most of the local operators exited the market and today they constitute only 0.2 % of the market (PTS, 2023b). Will the same trend develop on the parcels’ delivery market, and the current four big companies turn into an oligopoly or even fewer delivery companies will remain in the market? Already, Instabee is a result of a merger between two relatively new companies. Will the merger between Instabox and Budbee to Instabee result in a company that will increase the market share over time? If so, the result may be either Bertrand oligopoly that is good for the consumers or Cournot oligopoly that is less beneficial for them. In the latter case, regulators may consider some price or profit regulation to minimize the negative effects for the consumers.

Finally, how can higher prices sustain? As the alternatives are presented during the purchase, consumers are well informed about the different offers. We do not know to what extent consumers actually choose alternatives with anything but the lowest price, but if they are selected, what other factors (proximity to consumer, brand loyalty etc.) are important?

Future Research

The disaggregated approach applied in this study has turned out to provide more detail about the variations in supply and prices for parcel deliveries. Further research can benefit from similar approaches, and can cover more areas: the biggest cities, small cities, rural areas surrounding cities, sparsely populated remote areas, or extend to e-commerce by companies mostly selling over the counter. Similar approaches in other countries can provide more knowledge about a growing industry and the resulting market performance. It can thus be useful for the regulators facing decisions about whether to intervene, and if so, what policies that are relevant. Another intriguing area for research is the abovementioned about consumers’ choice, and what other factors than price are important. Future research on consumer preferences regarding home delivery, parcel box, and postal agents is needed to gain a deeper understanding of consumer choices and preferences to be able to understand the development of the parcel delivery market.

Supplemental Material

Supplemental Material - Competition in e-Commerce Parcels Delivery – A Disaggregated Approach

Supplemental Material for Competition in e-Commerce Parcels Delivery – A Disaggregated Approach by Pernilla Ivehammar, Linnea Tengvall, Peter Andersson in Competition and Regulation in Network Industries

Footnotes

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.

Declaration of conflicting interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Supplemental Material

Supplemental material for this article is available online.

Notes

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.