Abstract

This study introduces a theoretical framework for the Turkish natural gas market based on the principles of game theory and industrial organization. It investigates the effects of the legal and ownership unbundling on consumer surplus, social welfare, and competition. The model considers a mixed oligopoly with a transmission system operator (TSO), a state-owned incumbent, and a private firm. The state-owned incumbent is assumed to maximize consumer surplus and its own profit, while the private firm is assumed to be profit-maximizing. Additionally, the state-owned incumbent is assumed to be less efficient than the private firm. The game consists of three stages. In the first two stages, the state-owned incumbent and the private firm sequentially choose contract sizes in the upstream market. In the last stage, a contract size-restricted Cournot game is played. The findings of the study suggest that legal unbundling appears to offer greater advantages for consumer surplus and social welfare compared to ownership unbundling, particularly when considering key factors such as third-party access, non-tariff discrimination, and import liberalization. The results indicate that adopting the role of a Stackelberg follower by the state-owned incumbent in the upstream market is advantageous in terms of consumer surplus, social welfare, and competition under both unbundling approaches.

Keywords

Introduction

Energy is at the heart of most critical economic issues facing the world today. The growth in population and the corresponding increase in consumption levels over the last two decades have led to a rise in demand for energy. Therefore, the issue of regulations and competition for energy commodities, especially natural gas, has become a controversial topic for countries. There are numerous factors that affect market structure in natural gas, including limited production, inadequate transportation capacity, vertical mergers, third-party access, and non-tariff discrimination (Weir, 1999). In this context, the European Commission has published a regulatory framework for the EU gas markets, and unbundling is one of its most critical aspects (Growitsch & Stronzik, 2014).

Legal and ownership are two different types of unbundling. Ownership unbundling is the most comprehensive regulation for vertical integration. The company that owns and operates transportation activities cannot engage in additional business activities such as production and import. Under legal unbundling (also known as modest form of ownership unbundling) vertically integrated companies are legally separated but may still be part of the same business establishment as long as their decision-making systems and operations operate independently from each other. Both unbundling approaches are topics of ongoing debate in the literature. The question of which unbundling approach is more effective than the others continues to be a topic of political discussion as well (Bolle & Breitmoser, 2006; Brandao et al., 2016; Cremer & Donder, 2013; Höffler & Kranz, 2011; Pollitt, 2008).

Türkiye holds a strategic position in the regional natural gas market. It can play the role of a hub that brings together energy consumers and suppliers from Europe and Asia. The current structure of the Turkish natural gas market heavily depends on imports. Firms import gas from foreign suppliers, mainly with long-term contracts. Furthermore, there is a vertically integrated state-owned firm, BOTAŞ, which operates import, transmission, and storage activities in the market. It maintains separate accounts (also called accounting unbundling) for each of its activities.

This study is dedicated to achieving three different objectives that significantly contribute to existing literature. Firstly, it aims to establish a framework for the Turkish natural gas market that specifically addresses the vertically integrated state-owned incumbent. In this regard, industrial organization principles are applied, taking into account legal and ownership unbundling. The second objective is to assess the most effective role for the state-owned incumbent in the market. Lastly, the third objective is to identify how market equilibrium changes based on the choices of both contract size and quantity when a state-owned incumbent seeks to maximize both consumer surplus and its own profit. To achieve the second and third objectives, this study employs the Stackelberg and Cournot models in a sequential game structure to examine strategic interactions between the state-owned incumbent and a private firm in a mixed oligopoly in terms of consumer surplus, social welfare, and competition. Moreover, quantitative analysis is employed to enhance the comprehensibility of the theoretical model, involving simulations under different scenarios. The industrial sector data of the Turkish natural gas market is calibrated for simulations. Comparative statics is used to provide a more comprehensive policy analysis.

Our study contributes to the existing body of knowledge by establishing a theoretical model to assess the effects of legal and ownership unbundling in the context of the Turkish natural gas market, which includes a transmission system operator (TSO), a state-owned incumbent, and a private firm. Bolle and Breitmoser (2006), Höffler and Kranz (2011), Cremer and Donder (2013), and Brandao et al. (2016) investigate the impact of legal and ownership unbundling through theoretical models. All of these models assume that incumbent and private firms operate based solely on profit maximization. In contrast to these studies, our model enriches the literature by introducing a state-owned incumbent that is not solely focused on profit maximization.

The competition between public and private firms is extensively studied in the literature of mixed oligopoly. Equilibrium analysis is conducted by considering Cournot and Stackelberg competition in the market, with a public firm maximizing welfare and private firms maximizing profits (Cremer et al., 1989; De Fraja & Delbono, 1989; Fjell & Pal, 1996; Harris & Wiens, 1980; Sertel, 1988; Ware, 1986). Then, Wen and Sasaki (2001), Nishimori and Ogawa (2004), and Lu and Poddar (2005) examine the quantity and capacity decisions in mixed oligopoly model under various market structures.

In recent years, there is a growing interest in the study of mixed markets between consumer-oriented and profit-oriented firms. The objective function of a consumer-oriented firm is to maximize both consumer surplus and profit (Fanti & Buccella, 2017; Floresa & Garcia, 2016; Goering, 2008; Kopel & Brand, 2012; Lien, 2002; Nakamura, 2013). Then, Nakamura (2014) and Chen et al. (2019) analyze the capacity and quantity decision behaviors of firms in mixed markets under different competitive scenarios.

In our study, a particular scenario within the context of a mixed oligopoly is presented, which is of significant interest for public policy. It contributes to the mixed oligopoly literature by conducting a market equilibrium analysis for both quantity and contract size within the context of the natural gas market. This analysis considers a scenario in which a state-owned incumbent aims to maximize both consumer surplus and profit.

In the context of unbundling approaches, Höffler and Kranz (2011), Cremer and Donder (2013), and Brandao et al. (2016) conduct equilibrium analyses where firms in the downstream market engage in Cournot competition. Unlike their studies, our study performs equilibrium analysis, considering the strategic relationships between contract size choices of firms in the upstream and quantity choices in the downstream market within a three-stage game framework. Accordingly, a sequential move structure is used in the upstream market, taking into account the state-owned incumbent’s role as the Stackelberg leader or follower. In the downstream market, competition among the state-owned incumbent and private firm is examined under a simultaneous move structure.

In contrast to the studies by Bolle and Breitmoser (2006), Höffler and Kranz (2011), Cremer and Donder (2013), and Brandao et al. (2016), our model considers the state-owned incumbent which is legally separated from the transmission system operator (TSO), but both still operate under the same government entity. There are two cases for ownership unbundling. In the first case, the TSO and the state-owned incumbent are completely separate in terms of ownership, but they are both still public firms. In the second case, the TSO remains a state firm within the scope of security of supply, while the state-owned incumbent is regarded a private firm that maximizes profits. Furthermore, the assumptions include asymmetric unit costs for the state-owned incumbent and private firm. In line with the study by Sertel (1988), the private firm is considered more efficient than the state-owned incumbent. Third-party access is available for natural gas imports without any non-tariff discrimination, allowing the private firm to operate in both the upstream and downstream markets. The transmission tariff is exogenous to the model and is regulated with the objective of maximizing welfare. The transmission system operator (TSO) is solely responsible for gas transportation in the midstream.

The paper is structured as follows. Section 2 outlines the conceptual framework of the model. Section 3 presents the basic ingredients of the theoretical model within the context of legal and ownership unbundling. In Section 4, simulations, calibration, and the discussion of comparative statics findings are provided. Finally, Section 5 offers conclusions and suggestions for future research. Additionally, Appendix A and Appendix B contain the comprehensive solutions for our theoretical model.

Literature review

The exploration of the literature review begins with an analysis of the presence of public firms in mixed oligopoly, emphasizing the foundational premise of our study that revolves around the coexistence of both public and private firms. This examination serves as a bridge to explore how firms with different objectives make decisions about capacity and quantity within the market structure. Integrating these insights with our current research, the focus then shifts to the examination of market equilibrium literature in the context of unbundling.

Presence of public firms in mixed oligopoly

A mixed oligopoly defines a market in which a limited number of firms supply either homogenous or differentiated goods. The objective of at least one of these firms deviates from the goals of the others. The term “mixed” refers to the concept of mixed economies, which denotes the coexistence of private and public firms within an economic framework (De Fraja & Delbono, 1989). The pioneering research conducted by Merrill and Schneider (1966) made a substantial contribution to the literature on markets characterized by competition between public and private firms. A body of literature emerges that explores scenarios analogous to those examined in their seminal work. The main focus is on evaluating the welfare implications of various mixed oligopolies while considering the public firm as a welfare maximizer.

Merrill and Schneider (1966) show that a state-owned firm operating within an oligopolistic industry can lead to improved market outcomes, including lower consumer price. Harris and Wiens (1980), Ware (1986), Sertel (1988), De Fraja and Delbono (1989), Cremer et al. (1989), and Fjell and Pal (1996) assume that the main objective of a public firm is to maximize the summation of consumers’ surplus and producers’ surplus. Ware (1986) investigates a situation where a market starts as a natural monopoly but needs to accommodate new entrants due to increased demand. The study examines the cases of an incumbent public firm and a new entrant firm in the mixed duopoly. The firms have identical cost functions, which include fixed cost, constant variable capacity cost and increasing marginal cost. First, the public incumbent firm chooses its capacity, and then the new entrant decides on its capacity. Finally, both firms engage in a Cournot-Nash duopoly game. The results indicate that the incumbent public firm might struggle to effectively encourage entry due to its emphasis on maximizing welfare rather than maximizing profit (Nett, 1993). In contrast to Ware (1986), our study incorporates the assumption that the private firm has lower costs. In contrast to these studies, the public firm is assumed to maximize consumer surplus and its own profit instead of acting as a welfare maximizer.

De Fraja and Delbono (1989) conduct the study where

Matsumura (1998) conducts a study that follows a similar path with De Fraja and Delbono (1989). The study emphasizes that welfare maximization approach by a public firm does not lead to optimal outputs if the number of private firms in the market is exogenous. However, in contrast to De Fraja and Delbono (1989), Matsumura (1998) puts forward that the public firm should be privatized at least partially instead of fully nationalization. Furthermore, Matsumura and Kanda (2005) indicate that in the short term, partial privatization is the preferred policy, but in the long term, full nationalization becomes preferable as long as free market entry is provided (Fujiwara, 2007). Apart from partial privatization, our study assumes that the state-owned incumbent maximizes only its profit as the private firm in the market under ownership unbundling (Case 2).

The early body of literature illustrates scenarios in which public firm competes with privately owned domestic firms. In contrast to prior studies, Fjell and Pal (1996) take a different approach by analyzing a scenario where a public firm competes alongside both domestic and foreign private firms. The inclusion of foreign firms introduces a notable change, prompting a shift in the objective function of the public firm. Instead of adhering to the conventional strategy of maximizing the combined consumer and producer surplus within the domestic market, this study excludes the producer surplus of foreign firms. They also adopt the same assumptions with De Fraja and Delbono (1989) that there are no capacity constraints and firms have the same technology and identical increasing marginal cost. They find that while entry by a domestic private firm leads to decrease in outputs of a public firm, entry by a foreign private firm leads to increase in outputs of a public firm. From welfare point of view, the entry of a domestic private firm enhances welfare, while the impact on welfare from the entry of a foreign private firm is uncertain. However, welfare tends to increase if a foreign private firm enter the market and there are relatively few domestic private firms compared to foreign ones. In contrast to their approach, the presence of foreign firms in the market is not a constraint in our study since the public firm is already engaged in consumer-oriented approach rather than producer surplus. Our main focus is to show how the market equilibrium changes when a private firm enters the market as long as it is more efficient.

An alternate form of mixed oligopoly described in the literature involves non-profit firms (NPF), also known as consumer-friendly or socially concerned firms, competing against for-profit firms (FPF). The objective function of a socially concerned firm is to maximize both consumer surplus and profit (Fanti & Buccella, 2017; Floresa & Garcia, 2016; Goering, 2008; Kopel & Brand, 2012; Lien, 2002; Nakamura, 2013).

Goering (2008), Kopel and Brand (2012), and Fanti and Buccella (2017) investigate how market equilibrium is affected by the behaviors of socially concerned firms under managerial delegation. In contrast to the assumptions in these studies, our model rules out any principal-agent complications; in other words, public managers share the same goal as public authorities. On the other hand, the studies of Goering (2008), Nakamura (2013), and Floresa and Garcia (2016) focus on investigating how NPFs’ emphasis on consumer surplus affects the market output and overall welfare. These studies generally assume that the weight or priority that an NPF assigns to consumer surplus versus its own profit reflects its commitment to social benefits or profitability (Floresa & Garcia, 2016). When the weight of consumer surplus is at negligible levels, it causes the NPF to behave quite similarly to a FPF or vice versa. NPFs attempt to allocate equal or different weights to both profits and consumer surplus in order to optimize output and profit. In line with these studies, the objective function of the state-owned incumbent is modeled using convex combination of consumer surplus and its own profit.

Goering (2008) examines scenarios of mixed duopoly and oligopoly to analyze the welfare and output effects of operating in a market alongside NPF. The study discusses three types of Cournot competition: one involving a private NPF against a FPF, another between a FPF and a public firm, and a third with all three types. The NPF aims to maximize consumer surplus and its own profit, while the public firm maximizes welfare. The study assumes a linear inverse demand and constant marginal production costs for both firms and the private NPF is less efficient compared to others, while the public firm is identified as the most efficient firm. The extent to which the NPF prioritizes social concern is determined endogenously. The study shows that the NPF has the potential to either increase or decrease welfare. If the non-profit firm (NPF) outperforms the for-profit firm (FPF) in terms of cost-efficiency and operational effectiveness, prioritizing social concern can improve welfare. Conversely, if the opposite holds true, emphasizing social concern might reduce welfare. Floresa and Garcia (2016) draw attention to the following aspect in relation to the study of Goering (2008). The underlying logic behind the outcome is quite straightforward. As the NPF places a greater emphasis on consumer surplus, its output rises, while the FPF’s output decreases due to the NPF’s actions. Lien (2002) also emphasizes that if the decrease in output by the FPF is not as substantial as the increase in output by the NPF owing to efficiency, the overall production output increases due to the heightened altruism of the NPF. However, this might not necessarily result in an increase in welfare. In contrast to settings in these studies, our study examines a case where the public firm is consumer-oriented. The consumer-oriented approach is not given endogenously, but exogenously. Our study also analyzes the case of a state-owned incumbent as a Stackelberg leader and follower.

The prevailing belief is that an increase in social concern or responsibility inherently results in enhanced welfare. However, Goering (2008) challenges this assumption, indicating that this causality is not universally valid. Social welfare might also depend on the efficiency of the NPF. Consequently, increasing social concern could potentially lead to a decrease in social welfare. This underscores the necessity of considering the impact of social concern alongside the efficiency of the NPF. In line with Goering (2008), our model addresses how consumer surplus, social welfare, and competition change when private firms enter the market with cost advantages over the consumer-oriented state-owned incumbent.

Lien (2002), Goering (2008), Kopel and Brand (2012), and Fanti and Buccella (2017) assume in their studies that the market has linear demand and firms maintain constant marginal costs. Unlike their studies, Floresa and Garcia (2016) explore the consequences of NPF on output and welfare, considering linear demand and quadratic cost functions. They show that the output of NPF increases in response to its heightened concern for consumer surplus. The FPF decreases its output as a result of this action. Considering the rise in marginal costs with increased output, the NPF’s marginal cost increases, while the FPF’s marginal cost decreases due to the NPF’s increased concern for consumer surplus. Ultimately, when the NPF’s marginal cost becomes significantly higher compared to the FPF’s marginal cost, the effect of output replacement takes precedence over the effect of output expansion. Hence, it does not result in an increase in welfare. To be more specific, regardless of whether the NPF holds an efficiency advantage over the FPF or not, if the NPF’s focus on consumer surplus is significant, welfare decreases (Floresa & Garcia, 2016).

Capacity and quantity decisions in mixed oligopoly

The significance of capacity and quantity decisions as strategic instruments in the oligopoly market is widely acknowledged. Spence (1977), Dixit (1980) and Bulow et al. (1985) conduct the study within the context of the pure oligopoly market. Spence (1977) proposes that private firms might employ excess capacity to deter potential new entrants. Dixit (1980) concludes that private firms would not use excess capacity to deter entry in a perfect equilibrium. However, Bulow et al. (1985) indicates that a private firm could retain excess capacity to discourage entry, thus supporting Spence’s approach (Zhang, 1993).

Wen and Sasaki (2001), Nishimori and Ogawa (2004), and Lu and Poddar (2005) conduct their study on capacity choice in mixed oligopoly. However, the literature examines how capacity and quantity choices affect welfare in the context of mixed oligopoly markets. Wen and Sasaki (2001) assume a repeated mixed duopoly with homogenous goods. Both public and private firms possess identical constant marginal cost functions. They claim that the public firm can opt for excess capacity to enhance overall welfare. Nishimori and Ogawa (2004) analyze mixed duopoly market with a homogeneous good. A public firm produces less efficiently than a private firm while both firms have quadratic U-shaped cost functions that minimize long-run average costs when capacity matches quantity. Their study demonstrates that when the public firm acts as a Stackelberg follower, it deliberately chooses under capacity to encourage the private firm to expand its production. The public firm can increase welfare by lowering its capacity from the optimal level, thereby motivating the private firm to raise its output. The variations in results compared to Wen and Sasaki (2001) arise from varying assumptions regarding cost functions and the structure of the game (Nishimori & Ogawa, 2004).

Furthermore, Nakamura (2014) and Chen et al. (2019) investigate that how firms in a mixed duopoly with substitutable goods, make decisions regarding their capacities. One firm is socially concerned, aiming to maximize both its profit and consumer surplus, while the other is a profit-maximizing firm. The market operates under a linear demand function, and both companies have U-shaped cost functions that assist them in minimizing costs over the long term, much like previous research by Nishimori and Ogawa (2004) and Lu and Poddar (2005). Whereas Chen et al. (2019) obtain equilibrium output under Cournot and Bertrand competition, Nakamura (2014) considers only the Cournot competition with two stage game: firstly, the firms choose their capacities, and secondly, they decide on quantities based on these capacities. The move structure of this game differs from Nishimori and Ogawa (2004), which focuses on Stackelberg approach. Their model also incorporates two variables that take into account both product differentiation and the level of importance assigned to consumer surplus. Based on the values of these variables, some intriguing conclusions emerge. For instance, the profit-maximizing firms tend to opt for overcapacity, regardless of the diversity of their products or the level of importance given to consumer surplus. If the products are homogeneous, and even if the weight assigned to consumer surplus is significantly higher, then the socially concerned firm chooses overcapacity. Unlike the previous studies, our study examines the impact of the state-owned incumbent behaviour under sequential move structure. In addition, our study also examines the effects of contract size choices on consumer surplus, social welfare, and competition.

Market equilibrium under unbundling

From an industrial organization perspective, market equilibrium outcomes can also be affected by structures of the firms. In this context, regulations play an important role in markets. Legal and ownership unbundling is a regulatory framework that seeks to create competition in the context of third-party access and non-tariff discrimination. This can be seen as a way to reduce market power of dominant firms and improve efficiency (Cavaliere, 2007).

The literature contains only a few theoretical models that examine the effects of ownership unbundling and legal unbundling on social welfare in natural gas markets. While Pollitt (2008) and Growitsch and Stronzik (2014) provide empirical analyses, Bolle and Breitmoser (2006), Höffler and Kranz (2011), Cremer and Donder (2013), and Brandao et al. (2016) establish theoretical models to compare the legal and ownership unbundling approaches. The discussions typically do not include independent analyses considering the incumbent as a state-owned company with a different objective function. In this regard, our study stands out from the rest.

Bolle and Breitmoser (2006) analyze the impact of unbundling approaches under Cournot competition in oligopoly market. They examine the consequences of both ownership unbundling and legal unbundling within regulated networks, specifically considering how these approaches might affect consumer prices. Their findings indicate that, in general, ownership unbundling does not necessarily result in lower consumer prices. In contrast, based on their model, legal unbundling could lead to more favorable consumer prices.

Höffler and Kranz (2011) and Cavaliere (2007) emphasize that one of the main reasons for separating a vertically integrated firm is to prevent it from engaging in possible discriminatory behavior towards competitors. Pollitt (2008) empirically examines the effects of unbundling approaches for energy transmission networks. The study posits that there is often uncertainty about whether ensuring non-tariff discrimination is difficult when applying legal unbundling. It also indicates that unbundling can be used as a tool for achieving market liberalization. Thus, ownership unbundling is more effective than legal unbundling. Höffler and Kranz (2011) analyze the impact of unbundling under Cournot and Bertrand competition in oligopoly markets. The study shows that if transmission tariff are regulated and legal unbundling ensures that the network company only aims to maximize its own profits, then legal unbundling results in higher consumer surplus than ownership unbundling.

Furthermore, Growitsch and Stronzik (2014) validate the theoretical conclusions put forth by Höffler and Kranz (2011). The study states that the decision about which approach is advantageous can be made based on its impact on welfare. It further contends that the implementation of ownership unbundling can help prevent potential discrimination in network usage by third parties. Consequently, this can enhance market competitiveness, lowering the likelihood of vertical foreclosure. However, the study also points out that ownership unbundling might result in a decrease in economies of scope, subsequently affecting operational efficiency. Empirical examination of the study reveals that there is not substantial evidence suggesting that ownership unbundling offers greater benefits than legal unbundling in the context of social welfare. Nonetheless, introducing legal unbundling, which is a modest approach than completely breaking up vertically integrated does lead to a reduction in end-user prices.

Cremer and Donder (2013) argue that unbundling of upstream and downstream firms could lead to lower efficiency. Brandao et al. (2016) find that legal unbundling leads to lower end-user gas prices than ownership unbundling Furthermore, Cremer and Donder (2013) study the effects of unbundling on equilibrium network size. Their model assumes that a single firm operating the network in the upstream market chooses the network size, and then two firms compete in quantity in the downstream market. Under legal unbundling, the upstream firm maximizes its own and downstream profit, whereas under ownership unbundling, the upstream firm maximizes only its profit. In both cases, the downstream firm only considers maximizing its own profit. Both Höffler and Kranz (2011) and Cremer and Donder (2013) assume a market with one upstream firm and several downstream firms. However, Cremer and Donder (2013) make different assumptions than Höffler and Kranz (2011). They assume that the upstream firm considers the downstream firm’s profit in its objective function while choosing network size. Our study differs from them in terms of market structure. Firms are active in both upstream and downstream market that import gas and supply it to the consumers. The TSO operates the transmission activity in the midstream. Under legal unbundling, the state-owned incumbent considers TSO’s profit function. Additionally, the transmission tariff is regulated with the objective of social welfare maximization.

Our study is most closely related to the study by Brandao et al. (2016). The structure of the game in their model is as follows: first, the regulator decides the access price under the second-best tariff. Then, the entrant decides whether to buy gas from the incumbent or foreign countries. Next, the incumbent and entrant compete in quantity in the downstream market. In our model, both firms import gas from foreign countries by choosing contract sizes in the upstream market within a sequential move structure. Then, they compete in quantity in the downstream market. In contrast to settings in their model, the incumbent is not solely profit maximizer and the transmission tariff is exogenous.

The model

Our mixed oligopoly model, marked by specific and significant restrictions, aims to create a more streamlined framework for the Turkish natural gas market. These restrictions are designed to simplify the model’s complexity, and encompass several pivotal factors. First, the model makes the homogenous product assumption and assumes complete knowledge on the regulator about the state-owned TSO. Second, public managers share the same goal as public authorities. Third, the model takes into account legal and ownership unbundling approaches.

Our model adopts a static partial equilibrium approach, which offers a framework for analyzing the Turkish natural gas industry market dynamics. Within this approach, several key attributes define the behavior of firms. It is assumed that all participating entities in the upstream and downstream markets operate with the same level of technology and a fixed cost. Unlike the conventional assumption of increasing marginal costs, firms in this model, except for the TSO, maintain a quadratic cost function with unit costs. While capacity constraints are not explicitly enforced, the choice of contract size, similar to capacity is emphasized. This becomes particularly evident in industries such as the natural gas sector, where external dependency factors and contractual elements like take-or-pay agreements play a significant role.

Considering the natural gas market structure, the model is formulated as a mixed oligopoly with homogeneous goods. The market demand is assumed to be linear, following the Cremer et al. (1989), De Fraja and Delbono (1989), Fjell and Pal (1996), Ware (1986), Nishimori and Ogawa (2004), Lu and Poddar (2005), Goering (2008), and Nakamura (2014). The inverse demand is given by

The slope of the inverse demand function is assumed to be negative, taking into account the negative price elasticity of demand in the Turkish natural gas industry market. This is in line with studies of elasticity by Golombek et al. (1995), Al-Sahlawi (1989) and Erdogdu (2010).

Firm zero is the state-owned transmission system operator (TSO), while firm 1 is the state-owned incumbent and firm 2 is privately owned. Firm 1 and 2 share a unit cost

The cost function of firm 0, namely TSO, is given by

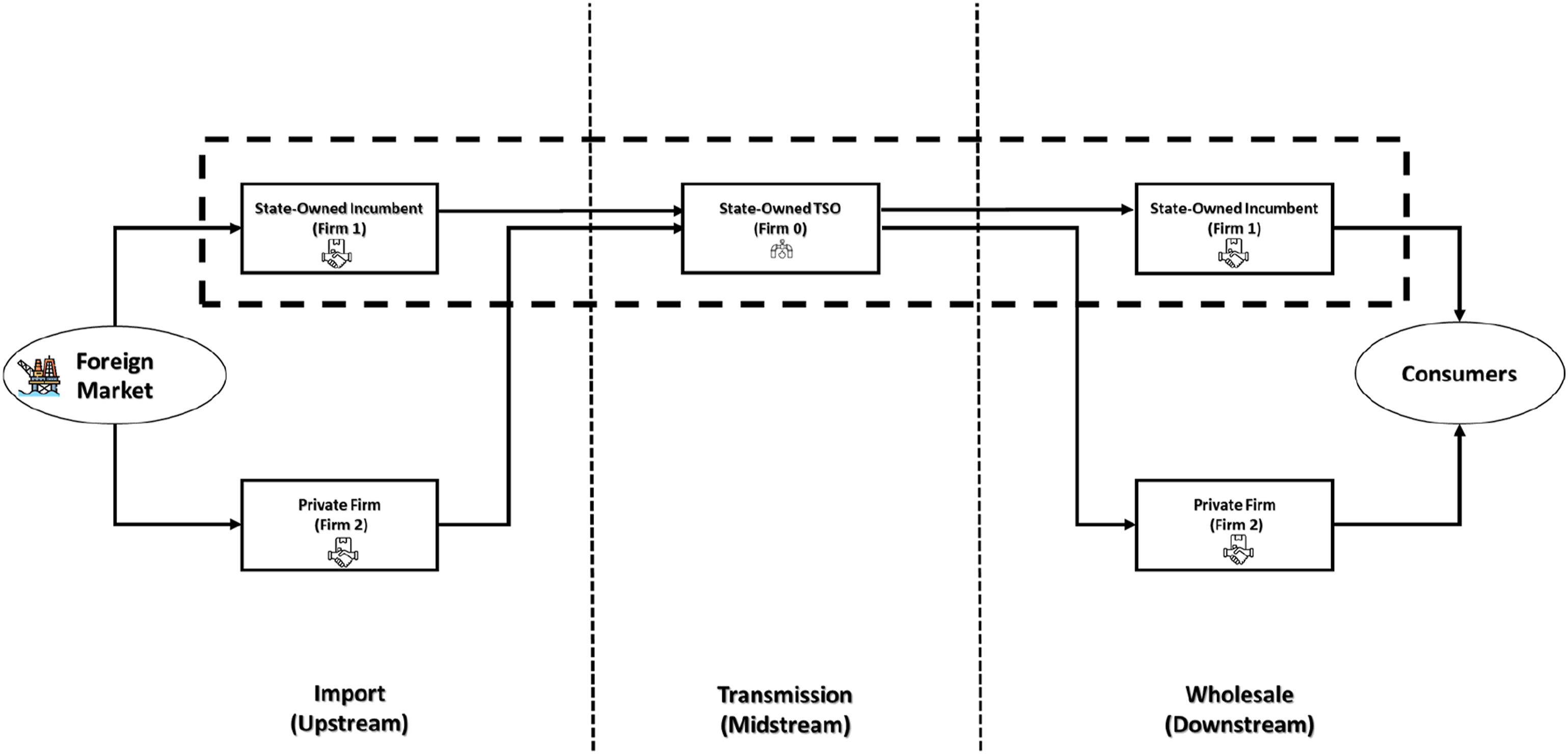

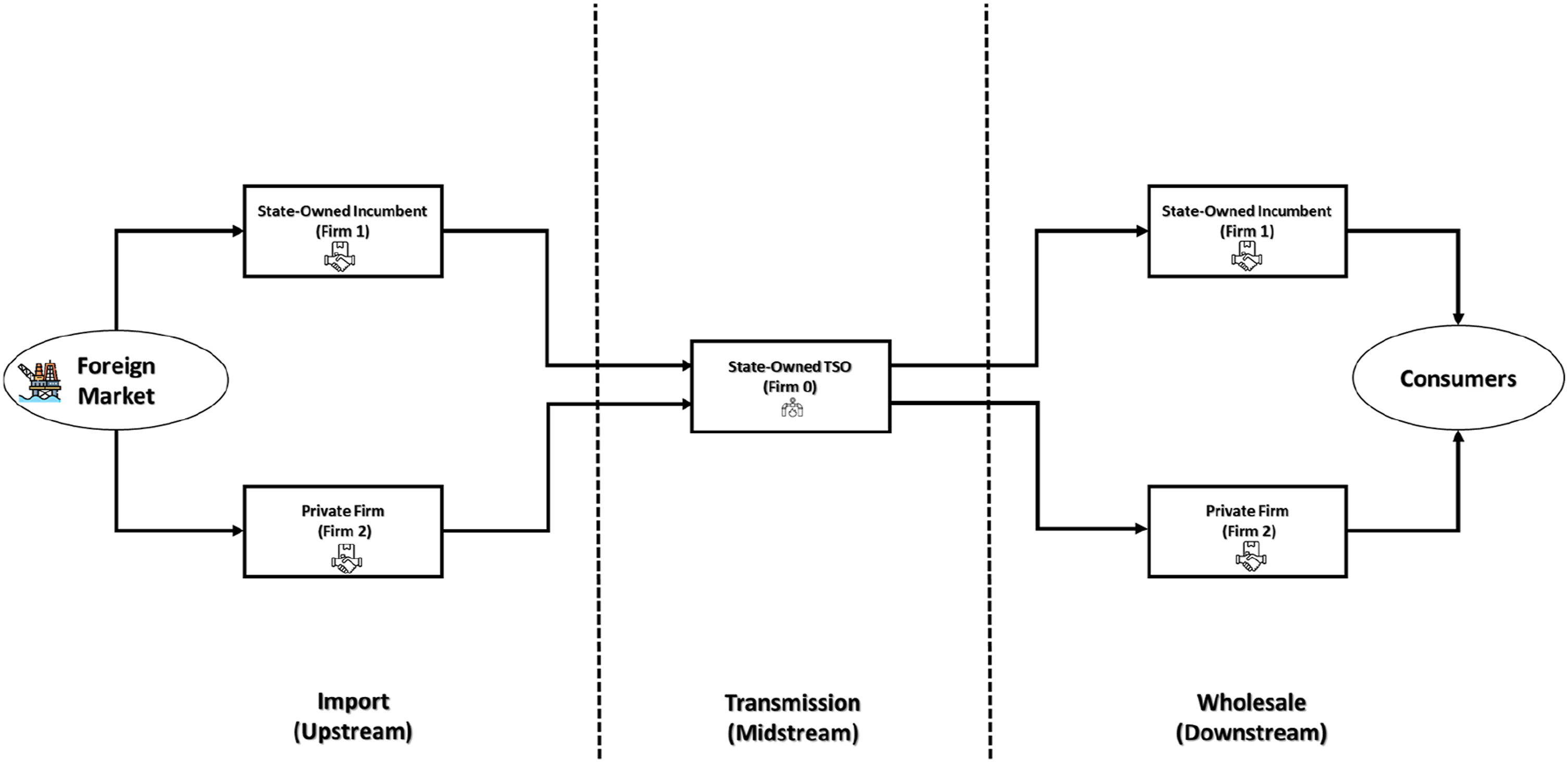

Now, we introduce the market structure for legal and ownership unbundling cases. Legal unbundling, where both the TSO and the state-owned incumbent operate within the same corporate group, as depicted in Figure 1. Ownership unbundling is examined from two distinct perspectives. First, the TSO and the state-owned incumbent are separated under the regulatory framework of ownership unbundling (Case 1), but they still remain state-owned (Figure 2). The second perspective involves the TSO remaining publicly owned due to security of supply concerns. However, the state-owned incumbent acts as the private firm, with its sole objective being profit maximization under the ownership unbundling framework (Case 2). Market structure under legal unbundling framework. Market structure under ownership unbundling (Case 1) framework.

Cremer and Donder (2013) assume that the network access charge represents a direct transfer between the subsidiary of the upstream firm and the downstream firm under legal unbundling. Höffler and Kranz (2011) state that legal unbundling offers stronger incentives for investments aimed at reducing marginal costs. Brandao et al. (2016) put forward that the incumbent pays the transmission tariff, but the joint profit of the incumbent and TSO is not affected under legal unbundling. In the light of these studies, our model assumes that marginal cost of the TSO is lower than the regulated tariff within the same economic entity (legal unbundling). The logic behind this assumption is that the regulator sets the tariff as TSO’s marginal cost to avoid non-tariff discrimination and maximize welfare. However, if the TSO is part of the same corporate group as the state-owned incumbent, the marginal cost of TSO decreases further. This is formulated in a functional manner consistent with Bremberger et al. (2012). The TSO’s marginal cost is assumed to be

Following Vives (1986), Nishimori and Ogawa (2004), Lu and Poddar (2005), and Nakamura (2014), it is assumed that the cost function is U-shaped, which implies that the long-run average cost is minimized when the output equals the contract size (capacity),

This particular cost structure can be compared to the type of cost structure more commonly seen in the literature that deals with sequential move structures regarding capacity and quantity settings in oligopoly models. In the literature, it is often assumed that producing beyond the planned capacity is costlier than staying within the chosen capacity limit. Although maintaining unused capacity incurs its own costs, the expenses associated with having too much or too little capacity are typically not treated as equal. In this context, Vives (1986), Nishimori and Ogawa (2004), and Lu and Poddar (2005) consider this cost structure where the costs of excess or under capacity are the same.

Natural gas markets typically involve long-term contracts that include take-or-pay clauses. These provisions mandate that purchasers make payments for a contractually defined minimum volume of output, regardless of whether they actually receive the delivered good (Masten & Crocker, 1985). In some situations, demanding more gas than the contract size can also result in additional costs due to fluctuating market prices. Thus, U-shaped cost function is selected to ensure that the model generates results that closely reflect real market conditions. Without this approach, the model would imply that firms always choose exact capacity.

Additionally, there is the assumption

The objective function of the TSO is the profit given by

The profit function of firm

Note that the objective function for the private firm is the sole profit maximization. The model specifies social welfare (SW) as the sum of both consumer surplus and the profits of the firms taking part in the national gas system. It is given by

Different objectives emerge for the state-owned incumbent within the contexts of legal unbundling and ownership unbundling. When considering legal unbundling, the state-owned incumbent aims to strategically maximize a convex combination of the consumer surplus and joint profits of the corporative group. Contrary to this model, Goering (2008), Kopel and Brand (2012), Nakamura (2014), Fanti and Buccella (2017), and Chen et al. (2019) describe the objective function of a socially responsible firm by using a linear combination of consumer surplus and the firm’s own profit. Both models theoretically follow the same direction, but only

Under legal unbundling, the objective function of the state-owned incumbent is defined by

We assume that the parameter

If the parameter

In the case of ownership unbundling (Case 1), the state-owned incumbent focuses on maximizing both consumer surplus and its own profits. Under ownership unbundling (Case 1), the objective function of the state-owned incumbent is defined by

Three-stage sequential games

An equilibrium analysis is conducted under three-stage sequential game structures, taking into consideration the legal and ownership unbundling. The key distinction is whether the state-owned incumbent firm acts as a Stackelberg leader or a follower when choosing its contract size in upstream market. In the downstream market, both firms choose quantity simultaneously.

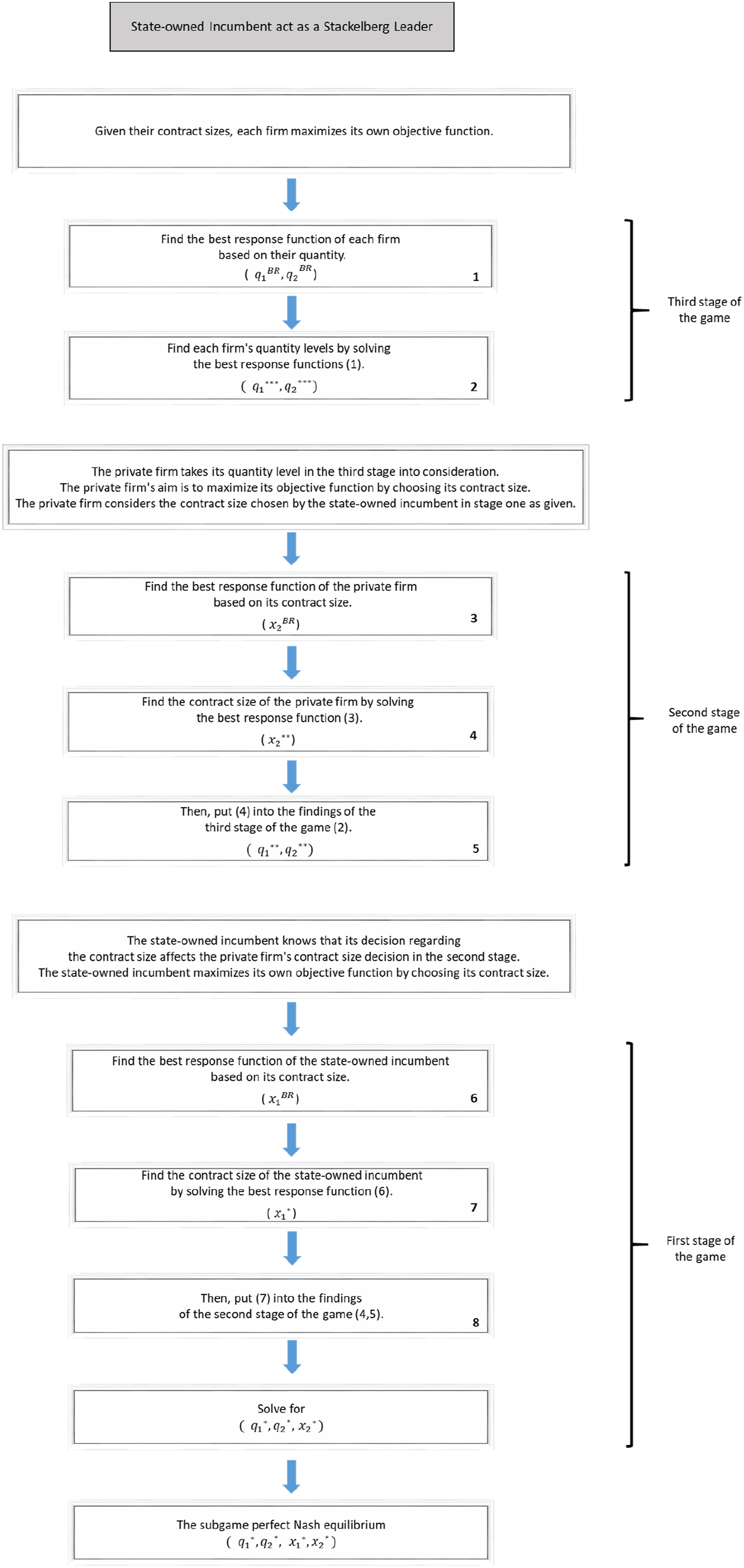

In the first scenario, the firms make decisions regarding contract size and quantity in the following three-stage games: • The state-owned incumbent chooses contract size first, then the private firm chooses contract size, and in the third stage, both firms choose quantity simultaneously.

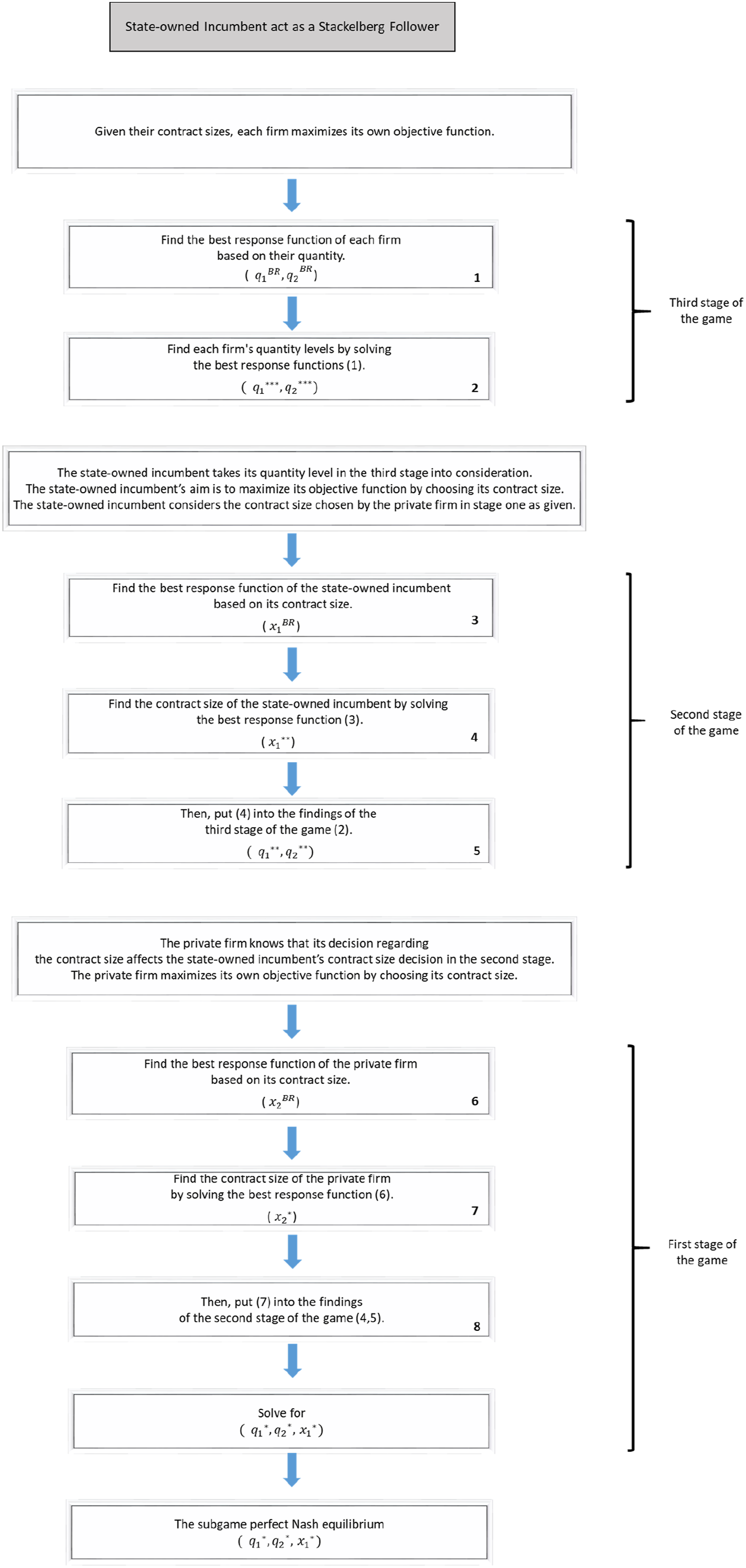

In the second scenario, the firms make decisions regarding contract size and quantity in the following three-stage games: • The private firm chooses contract size first, then the state-owned incumbent chooses contract size, and in the third stage, both firms choose quantity simultaneously.

The subgame perfect Nash equilibrium is determined through backward induction, as summarized in Figures 3 and 4. Our theoretical results are cumbersome and the interpretations of equilibrium outcomes are challenging. Therefore, we perform a simulation analysis by calibrating the industrial sector of Turkish natural gas market. The equilibrium results for the theoretical model are relegated to Appendix A. A flowchart illustrating how the subgame perfect Nash equilibrium is obtained for the Scenario 1. A flowchart illustrating how the subgame perfect Nash equilibrium is obtained for the scenario 2.

Simulations

In this section, simulations for the first and second scenarios are conducted with the aim of providing quantitative results regarding the effects of different unbundling approaches on consumer surplus, social welfare, and competition.

Initially, specific functional forms of the theoretical model, such as elasticity and slope, are determined and calibrated using data from the Turkish natural gas market (Section 4.1). Subsequently, simulations of the different scenarios are performed, and the results of the comparative statics are analyzed (Section 4.2).

Calibration

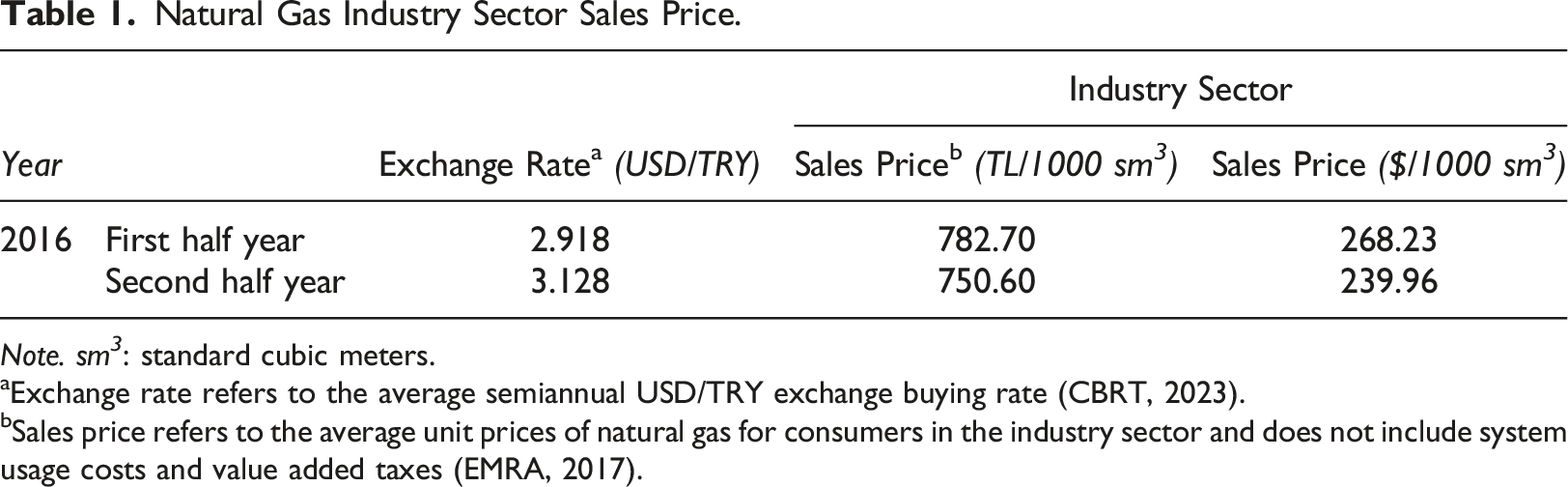

Natural Gas Industry Sector Sales Price.

Note. sm 3 : standard cubic meters.

aExchange rate refers to the average semiannual USD/TRY exchange buying rate (CBRT, 2023).

bSales price refers to the average unit prices of natural gas for consumers in the industry sector and does not include system usage costs and value added taxes (EMRA, 2017).

First, the parameters of the inverse demand function for the Turkish natural gas industry sector are calibrated in order to perform the simulations. There are studies in the literature regarding the price elasticity of demand for different sectors of the natural gas market using different time series. Golombek et al. (1995) express the price elasticity value as ranging from

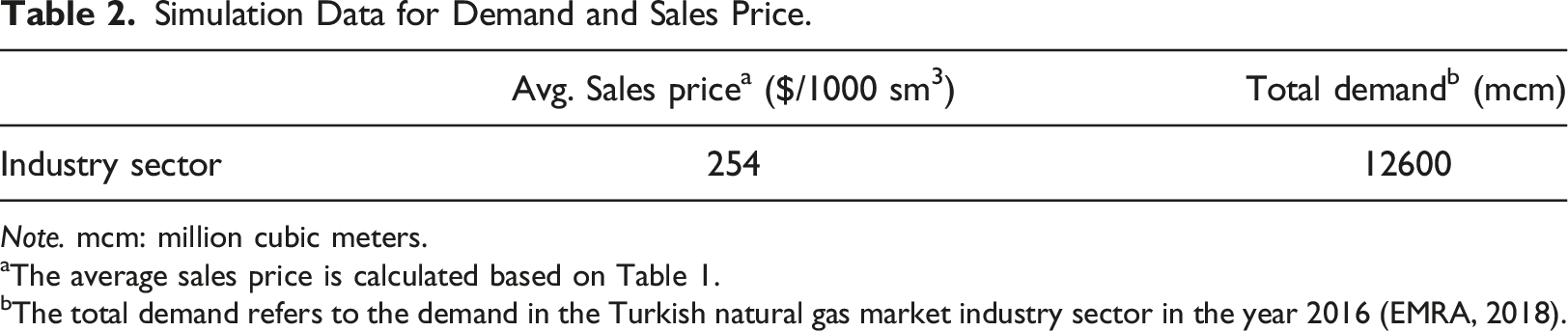

Simulation Data for Demand and Sales Price.

Note. mcm: million cubic meters.

aThe average sales price is calculated based on Table 1.

bThe total demand refers to the demand in the Turkish natural gas market industry sector in the year 2016 (EMRA, 2018).

Now, let us turn to the calibration of the cost function for firms. All firms are assumed to import gas solely through long-term contracts in the model. The long-term contract prices are confidential information. Thus, based on the average sales price which is shown in Table 2, the average purchasing gas price for the state-owned incumbent is assumed to be

The objective function of the state-owned incumbent includes consumer surplus, except in ownership unbundling (Case 2). The weight parameter

The regulator does not strategically set the transmission tariff, but instead implements a second-best tariff approach. The TSO’s primary role is to ensure that all gas units required by both the state-owned incumbent and private firm are transmitted. Essentially, the TSO takes its costs and prices as given. In this context, energy regulators tend to favor second-best tariffs, aiming to maximize overall welfare as long as regulated activities do not result in economic losses (Brandao et al., 2016). Setting the tariff equal to the TSO’s marginal cost is a way of maximizing welfare. This assumption allows for a clearer demonstration of effects of unbundling approaches. According to the Turkish natural gas market data in 2016, tariff is equal to

Furthermore, our model assumes that there is sufficient capacity in the market. The factors of storage and LNG capacity, which is another source of natural gas supply, are not considered in the model. Firms are assumed to supply gas to the market through long-term contracts with take-or-pay clauses. Choosing under capacity (contract size) in this context may not seem meaningful from real-market perspective. However, since these contracts are subject to the long term, there is a chance to deliver less than the current contract size in one year and make up for it in the following year. Therefore, an assumption is made in this context that the choices of over and under capacity in terms of contract size will not lead to costs that significantly affect prices in the long run. The focus is to illustrate the behaviors of firms in choosing contract size under legal and ownership unbundling and its effects on the market equilibrium outcomes.

The Herfindahl-Hirschman Index (HHI) is widely used in studies to measure the competitiveness of an industry in terms of market concentration. The European Union Agency for the Cooperation of Energy Regulators (ACER) sets the HHI target at

Comparative statics results

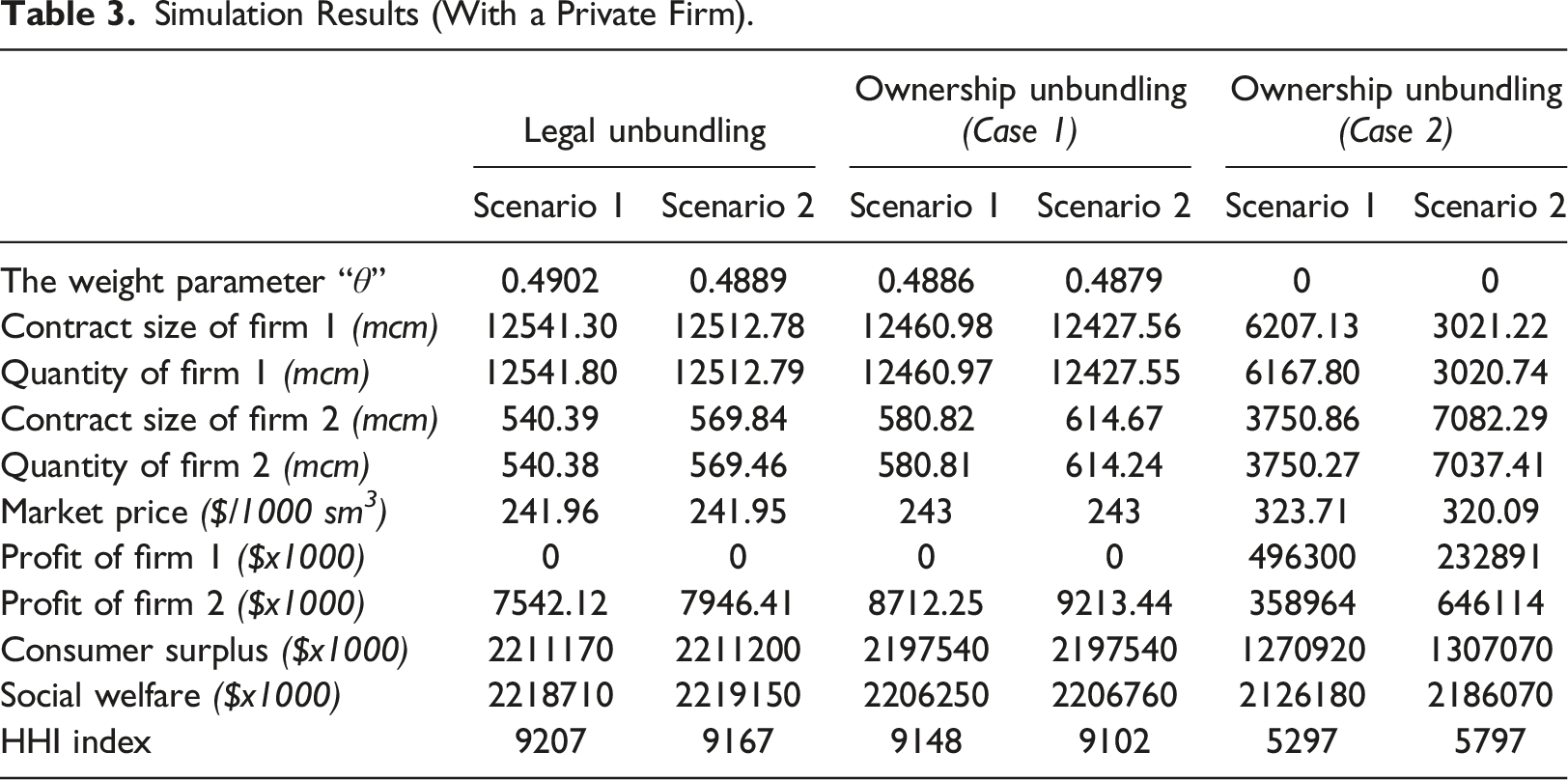

Simulation Results (With a Private Firm).

Under legal unbundling, consumer surplus, social welfare, and market competition are all higher when the state-owned incumbent is a Stackelberg follower (Scenario 2) compared to when it is a Stackelberg leader (Scenario 1). In ownership unbundling Case 1, the objective function of the state-owned incumbent includes consumer surplus and its own profit. In this case, whether it acts as a leader or follower does not change consumer surplus. However, when it is a follower, social welfare and market competition all increase. In ownership unbundling Case 2, the objective function of the state-owned incumbent is profit maximization, similar to the private firm. In this case, when it acts as a follower, consumer surplus and social welfare increase. However, competition is low compared to when it is a leader.

Under each unbundling scenario, when the state-owned incumbent acts as a follower, the best outcomes are observed in terms of social welfare. This is in line with De Fraja and Delbono (1989) who emphasize that a public firm pursuing welfare maximization also achieves the best results when it acts as a follower. Regardless of whether the state-owned incumbent acts as a follower or leader, under legal unbundling, consumer surplus reaches its highest level when compared to ownership unbundling (Case 1 and Case 2). In terms of competition, ownership unbundling is superior to legal unbundling. The best outcome for competition is in ownership unbundling (Case 2), where firms maximize their own profit.

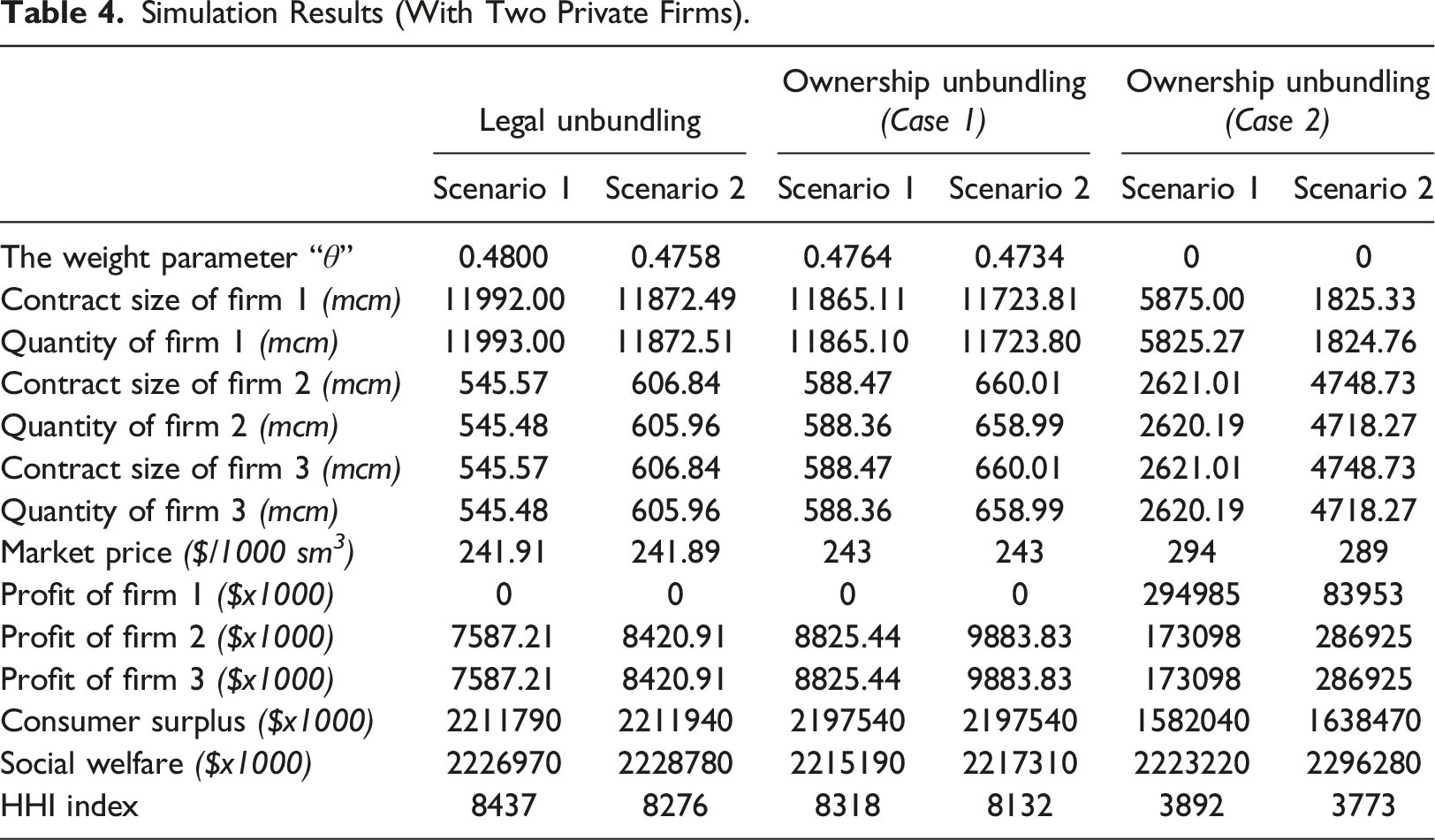

Simulation Results (With Two Private Firms).

In the case of ownership unbundling (Case 2) as presented in Table 4, it is worth noting that it performs the best with respect to social welfare and competition. Social welfare encompasses both consumer surplus and producer surplus, so it is important to understand how each is affected. In this scenario, consumer surplus decreases, while producer surplus increases. This increase in producer surplus contributes to the overall improvement in social welfare. Additionally, the boost in competition is driven by all firms pursuing profit maximization.

Another issue concerns the positive impact of increasing the number of private firms on market equilibrium outcomes. De Fraja and Delbono (1989) suggest that profit maximization for public firms, instead of welfare maximization, may potentially increase overall welfare in a market with an optimal number of firms. However, when this matter is considered within the context of the Turkish natural gas market, the strategic nature of gas as an energy source and its high dependence on imports make it a controversial topic.

In the context of a strategic product like natural gas, is the increase in social welfare and competition, despite the decrease in consumer surplus, acceptable from the consumer and public perspective? Because a reduction in demand or significantly higher prices for natural gas that adversely affect development could open the door to other socio-economic problems. For example, it may result in reduced industrial activity, electricity production, and even an overall decrease in the country’s total production. In other words, the increase in energy costs could affect all segments of society. On the other hand, unexpected situations, such as a pandemic or restrictions on access to raw materials due to conflicts of interest between countries, can lead to conflicts more quickly and clearly in sectors where only profit-maximizing firms operate. Sertel (1988) emphasizes that the presence of a public firm in the market has a regulatory impact on other firms. In this regard, a public firm should be evaluated not only in terms of its own efficiency but also in terms of the overall efficiency of the industry. On the other hand, Wright (2005) puts forward that more liberalization can bring a security of supply problem. For this reason, it is important to increase the number of efficient private firms by providing third-party access in the market from the perspective of competition. However, from the perspective of security of supply, it is also important for the public firm to have long-term contracts in its hands to a certain degree that will not affect competitive conditions. For this reason, the findings under ownership unbundling (Case 2) in Table 4 emerge as a different issue that needs to be modeled with the consideration of different market elements. One of these could be the issue of partial privatization.

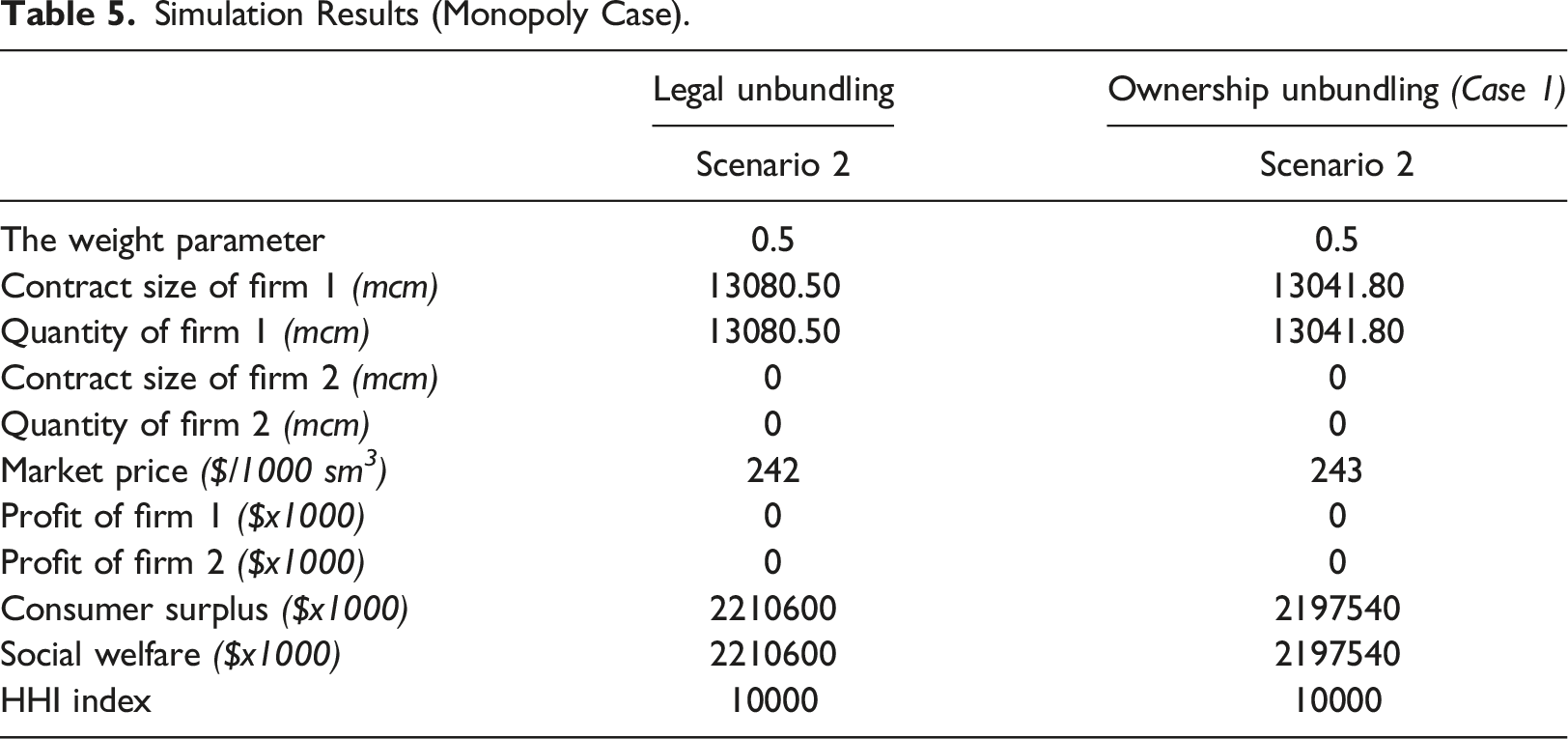

Simulation Results (Monopoly Case).

In terms of choosing the contract size, the findings in Tables 3 and 4 also hold significance for the market dynamics. The state-owned incumbent needs to increase total output to maximize consumer surplus, so it sets a price at its marginal cost. In the case of legal unbundling, both the state-owned incumbent and TSO are part of the same economic corporation. Thus, even if the regulator chooses a tariff equal to the TSO’s marginal cost, the state-owned incumbent benefits from certain advantages because of its affiliation with the same corporation. The state-owned incumbent uses the revenue provided by the TSO as a cost-reducing tool. Hence, the increase in output by private firms translates into income for the state-owned incumbent under legal unbundling. This, in turn, supports the idea of the state-owned incumbent reducing costs and making a more significant contribution to consumer surplus. Consequently, under legal unbundling, the state-owned incumbent chooses under capacity (contract size) to ensure that private firms also have a share in the total output. Since private firms are profit-oriented, operating with excess capacity (contract size) is a favorable strategy for them to boost their outputs.

In a three-stage game, being a Stackelberg follower for the state-owned incumbent in the upstream market, where the contract size is chosen first, is an approach that contributes to the market equilibrium outcomes. Certainly, this is in line with Pal (1998) and Nishimori and Ogawa (2004) in the findings presented in the literature regarding mixed oligopolies. Nishimori and Ogawa (2004) emphasize that in the Stackelberg follower game structure, the public firm, which aims to maximize welfare, can enhance welfare by encouraging the private firm to produce more. Thus, the public firm tends to choose under capacity. Similarly, Pal (1998) indicates that in the case where the public firm is a follower, it directs its efforts towards increasing the private firm’s output by producing less. In contrast to their studies, this model reveals that, under legal unbundling, the state-owned incumbent which aims to maximize consumer surplus, profit of TSO and its own profit, chooses under capacity (contract size), regardless of whether it is a Stackelberg follower or leader. This highlights that the state-owned incumbent chooses the contract size as a strategic tool under legal unbundling. In ownership unbundling (Case 1 and Case 2), the state-owned incumbent behaves differently. There is no additional revenue for it in increasing the outputs of private firms to enhance consumer surplus under ownership unbundling (Case 1). Therefore, it tries to maximize consumer surplus by choosing over capacity (contract size). On the other hand, firms aiming for profit maximization in all unbundling approaches attempt to boost their profits by increasing the total quantity through choosing over capacity (contract size).

Conclusion

This study analyzes legal and ownership unbundling approaches within a theoretical framework and provides potential policy recommendations for the market. Non-tariff discrimination, third party access and import liberalization are the most important arguments that will ensure that the unbundling models are fully formed at the desired level. Under these assumptions, legal unbundling is more beneficial for consumer surplus and social welfare than ownership unbundling, considering the Turkish natural gas market dynamics. This result also supports other studies in the literature, such as Bolle and Breitmoser (2006), Höffler and Kranz (2011), Cremer and Donder (2013), and Brandao et al. (2016). In terms of competition, ownership unbundling brings more advantages than legal unbundling. However, focusing solely on competition in the Turkish natural gas market may lead to the implementation of ineffective regulations from a consumer perspective. Eroğlu (2010) also emphasizes that adopting unbundling alone will not foster competition; hence, it should be implemented alongside other essential regulations within the framework of general competition policies. Therefore, the entry of more effective private firms into the market through import liberalization is the most critical factor in establishing competition.

In both unbundling approaches, TSO remains a state-owned entity due to security of supply concerns. It will not lead to any structural problems for the market as long as the regulated tariff is set within the scope of the second-best tariff, and third-party access is available. On the other hand, Sertel (1988) argues that public firms may participate in the market as a regulatory tool. The Turkish natural gas market relies heavily on imports, and the demand in the market is mainly satisfied through the long-term contracts. Thus, the presence of the state-owned incumbent as a Stackelberg follower in the market could help prevent prices from significantly exceeding average marginal costs and also contribute to supply security.

Furthermore, Türkiye continues to work on natural gas exploration. In a scenario where Türkiye becomes self-sufficient in natural gas, and the long-term contracts expire, it would be interesting to study the effects of partial privatization of the state-owned incumbent on the market equilibrium outcomes under different unbundling approaches.

Supplemental Material

Supplemental Material - Legal and ownership unbundling in the Turkish natural gas market: A comparative analysis

Supplemental Material for Legal and ownership unbundling in the Turkish natural gas market: A comparative analysis by Yunus Emre Gürler, Sinan Ertemel, Matthias Finger, and Muzaffer Eroğlu in Competition and Regulation in Network Industries

Footnotes

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Supplemental Material

Supplemental material for this article is available online.

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.