Abstract

In recent years, many European states have begun heavily investing in hydrogen (H2) technologies and as of July 2021, several have published detailed national hydrogen strategies. Nonetheless, it is evident there are emerging differences between these states regarding the scale, ambition and sophistication of their H2 plans. Such strategies also have implications for existing energy regimes that remain strongly dependent on fossil fuels alongside greater integration of renewables. Emerging H2 firms and technologies further disturb energy policies by either requiring a partly new, or at least modified, European energy infrastructure. Will such changes produce commercially dominant H2 businesses that could distort the broader energy market and confer a leading position upon a few countries and firms? There is also uncertainty over whether H2 technologies will support renewables by providing a ready means of energy storage, or whether investment in hydrogen could, paradoxically, displace some of the commercial interest in renewables. Finally, questions have been posed about the green credentials of H2 technologies. There are significant differences in how hydrogen is generated and much debate about the hydrogen colours. This paper employs a comparative analysis of three European national hydrogen strategies, offering a contrast between Germany, the UK and Portugal. The interaction between these and the EU level is mapped. Also explored is whether the various national styles favour more cooperative or competitive policy-making. The comparison with the UK allows us to explore some impacts Brexit may have on British H2 ambitions. To interpret these strategies, we employ the Multi-Level Perspective on energy transitions, which focuses on how different actors have a variable influence at mutually reinforcing levels of policymaking (niches, regime and landscape). These include EU institutions, national governments and agencies. Energy and technology firms and research networks are also crucial. We draw attention to several fundamental regulatory challenges that H2 strategies raise. Also highlighted are differences and similarities between countries and the wider possible trajectories for future hydrogen development.

Hydrogen and European policies: Introduction

Interest in hydrogen to reduce overdependence on fossil fuels is certainly not new. The oil supply shocks of the 1970s resulted in speculation over an imminent breakthrough of hydrogen technologies (Solomon & Banerjee, 2006: 781). However, the present momentum derives mostly from the realisation that achieving net-zero GHG emissions is urgent in the context of the Paris climate change agreement, but that this is far from straightforward to achieve. Also different this time is the scale of investments and the ambition for H2 technologies.

For example, one objective is that hydrogen will help expand the renewables sector by offering a cost effective and reliable means to store energy generated by wind or solar off peak, and thus address the ubiquitous base load problem. A secondary aspiration is that H2 technologies may be used where renewable electricity will struggle to replace fossil fuels, notably in hard-to-abate sectors such as motor transport. Capros et al. (2019) have argued that electrification may ultimately reach only around 50% of total energy demand, leaving a need for diverse energy solutions such as hydrogen and synthetic hydrocarbon fuels. In addition, the increasing use of Natural Gas (NG) faces climate and energy security concerns. Because so much of the European NG supply is dependent on Russian, Gulf State or American (fracked) imports, this presents a strategic political risk but it is also an opportunity for hydrogen (Prahl & Weingartner, 2016; Brauers, et al., 2021; Szabo, 2020; Field & Derwent, 2021).

Contemporary H2 policies often distinguish between the so-called ‘colours of hydrogen’, which invokes colours as metaphors to communicate how a particular H2 molecule is produced. So-called grey hydrogen is produced industrially from fossil fuels such as NG. Blue hydrogen is engineered with carbon capture and storage (CCS) whereas green hydrogen comes from the use of renewable energy (Griffiths et al., 2021: 102028; Dawood et al., 2020: 3853). Blue and green H2 are usually both described as clean hydrogen due to their stronger environmental credentials. Recent EU plans consider green hydrogen as central to fully decarbonising large-scale applications in industry, transport, heat and power. However, these documents are also careful not to rule out a part for other forms of H2, at least in the short term (EC European Commission, 2020: 3–5).

In a general overview of the potential for H2 technologies, the International Renewable Energy Agency (IRENA) has underlined the importance of national hydrogen strategies. This is because they encourage the setting of policy priorities, reveal the importance of guarantees of origin and technical standards, as well as provide opportunities for integrating an emerging H2 governance system with civil society or industry (IRENA, International Renewable Energy Agency, 2020). According to the Hydrogen Council (McKinsey & Company. Hydrogen Council, 2021), more than 30 countries have released hydrogen roadmaps. These include Australia, Germany, France, Canada, Japan, China, Norway, Portugal, Netherlands, Finland and Chile. Internationally, there is growing financial support from governments, and commercial investors, with countries pledging more than USD $70 billion for hydrogen development (McKinsey & Company. Hydrogen Council, 2021). (Albrecht et al., 2020) argue that, by 2025, hydrogen strategies can be expected to cover countries representing over 80% of global GDP. Internationally, hydrogen production is gaining momentum, reinforcing H2 as the main future energy carrier and a renewable feedstock for industrial processes.

The EU has also stepped up its ambition on hydrogen by including it as part of the wider-reaching ‘New Green Deal’ and framing it as a key technology to lead the transition to a net-zero GHG emissions by 2050. However, Europe is far from being self-sufficient in clean energy production, meaning that the scope for specifically green hydrogen pathways is challenging. Because many EU countries rely on North African countries as green energy suppliers, this suggests European green hydrogen pathways will require an international dimension and cannot be exclusively European.

While national hydrogen strategies are our dependent variable in this study, the interplay with the EU level is also necessary to consider, given the relevance for the EU’s New Green Deal and the EU’s leadership on climate change (Elkerbout, et al., 2020). The existence of this twin level of ambition, both at the EU level and then again at the national level, raises issues of synergies between policies (Szulecki, et al., 2016). Although the role of the European Union appears to be important, it has largely been confined to supporting, financing and stimulating the growing hydrogen sector. The most important recent EU statement of ambition was the ‘Hydrogen strategy for a climate-neutral Europe’, announced by the European Commission in July of 2020 (EC. European Commission, 2020). This set a target of a 40 GW electrolyser capacity target for 2030 (up from less than 0.1 GW today). Notwithstanding this, the decisive actors often remain at the national level, although the theoretical approach we employ here stresses the interaction of multiple actors at variable levels (micro, meso, macro, etc.).

It is also important to note complexities over the temporalities of hydrogen development, that is, the long-term future versus the short-term. Developing hydrogen as a novel storage mode for renewable electricity has been viewed as probably the most essential long-term objective, allowing an expansion and deepening of electrification to make strategic inroads into heating and transportation. Conversely, in the shorter term, there is considerable scope for the European gas and chemicals sectors to employ hydrogen as a means to partly decarbonise themselves. However, these sectors typically favour grey or blue hydrogen strategies rather than green trajectories. Therefore, a crucial question for national and EU policies is asking what shade of hydrogen will emerge as dominant, if any.

Literature review

Heretofore, much of the existing literature on hydrogen has been dominated by technical and natural science disciplines focussing on narrow technological issues with less attention given to regulatory and policy affairs. In 2006, Solomon and Banerjee noted the emergence of H2 plans and policies, but, at that stage, private actors such as the large motor vehicle manufacturers, energy majors and fuel cell companies often led them. Today, the focus is more on national and international plans as well as the need for agreement on technical standards and certification. This entails mutual recognition of harmonised standards over the ‘colours’ of hydrogen, a process yet to emerge (Abad & Dodds, 2020). The EU has made an early foray into this space with its EU CertifHy initiative (CertifHy project, 2019), which sets an upper limit for the carbon footprint associated with any hydrogen produced from renewable energy sources 1 .

Griffiths, et al. (2021) adopt a socio-technical perspective to highlight the importance of the heavy industrial sector (chemicals, refining, etc.) for hydrogen, which is in contrast to the attention usually lavished on associations with renewables. They also argue that low carbon hydrogen technologies will likely require extensive financial support to compensate for higher costs, while noting that national strategies on hydrogen should be assessed more critically: ‘those strategies that will ultimately prove most effective will likely include both clear goals with quantifiable targets and the proposed mechanisms (fiscal and economic, policy, technological) to achieve them’ (Griffiths, et al., 2021; 31–37). Finally, it must be stressed that much of the policy support for hydrogen that has featured over the last 20 years has been to support research and development, whereas in the future what will be required are more substantive market creation and regulation policies, with increasingly a focus on reducing the costs of hydrogen production and transmission (Nastasi, 2019: 40–41). When it comes to costs, producing renewable hydrogen in a specific location is influenced by the type of renewable energy sources available and associated capacity factors, while transport costs depend on the volume of hydrogen transported, the distance, and the physical state in which hydrogen is transported - the ‘packaging’ mode (EC. European Commission, 2021).

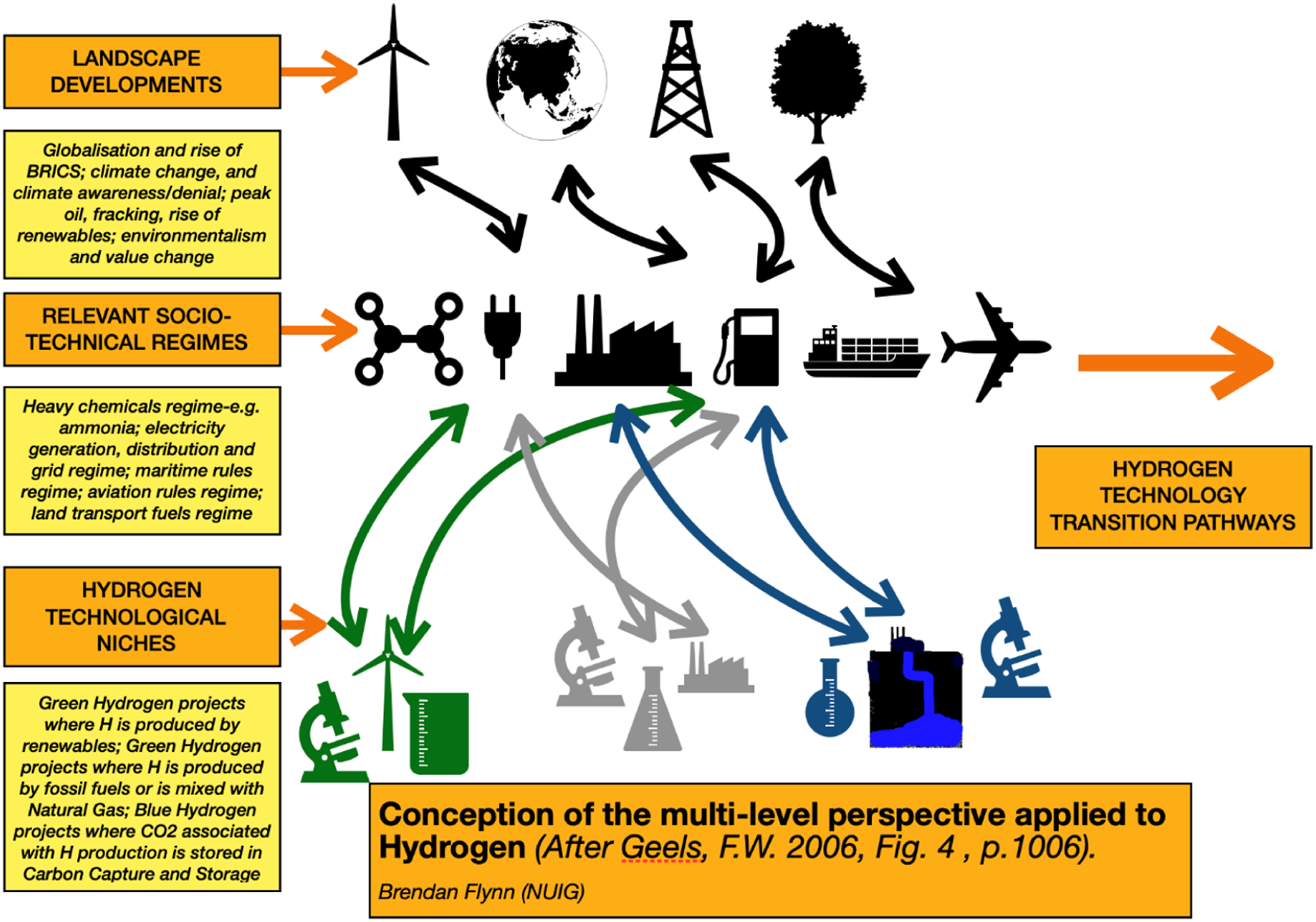

This article draws extensively on the grey literature that is relevant for each country and their national hydrogen plans. Here, the Multi-Level Perspective (MLP) on energy transitions (Geels, 2019; Kanger, 2021) theoretically informs the research design adopted. This approach studies hydrogen transitions by examining the different actors who have a variable influence at distinct, but mutually reinforcing, policymaking levels (niches, regime and landscape). This MLP approach is primarily associated with the Dutch school of technology transitions (Smith, 2003, p.128), and especially with the work of F.W. Geels (2019). Within the MLP literature, the terms niche, regime and landscape have quite specific meanings (Geels, 2006, p.1000). However, what is crucial is the interaction dynamics between these levels, which can produce substantive transitions: ‘transitions come about when co-evolutionary dynamics at different levels align and link up’ (Geels, 2006, p.1000).

According to the MLP literature, niche practises are evident in the activities of early adopters, sites of use, innovation, experimentation or resistance. Niches would typically then be start-up firms, laboratories or specific H2 R&D teams within much larger well-established companies. There are usually a number of these niches for each given technology, each exploring different approaches. Some niches interact with each other, learning, co-operating and merging; just as often they are competing. At the regime level, we find the rules and the regulatory arena in which any new technology is attempting to break through. The regime relates to where and how hydrogen technologies could emerge as initially a new trend, and later as a mature technology pathway. For hydrogen, the most immediate regime in question are the various national energy policy regimes, or more specifically national electricity systems and grids (a regime within the wider energy system). Also relevant could be regimes for the heavy chemical industry sector or even the transport sector. It is at the regime level that national governments and EU institutions are more obviously evident as regulators. At the landscape level within the MLP account, we find significant structural changes in society, technology and the economy. The most obvious example of such a macro trend today is climate change. One could also mention here the rise of the internet, globalisation or the growth of renewables. The Covid-19 pandemic and Brexit could also be included in this category as ‘landscape’ level exogenous shocks.

National approaches to the emerging hydrogen value chain: Germany, United Kingdom and Portugal (case studies)

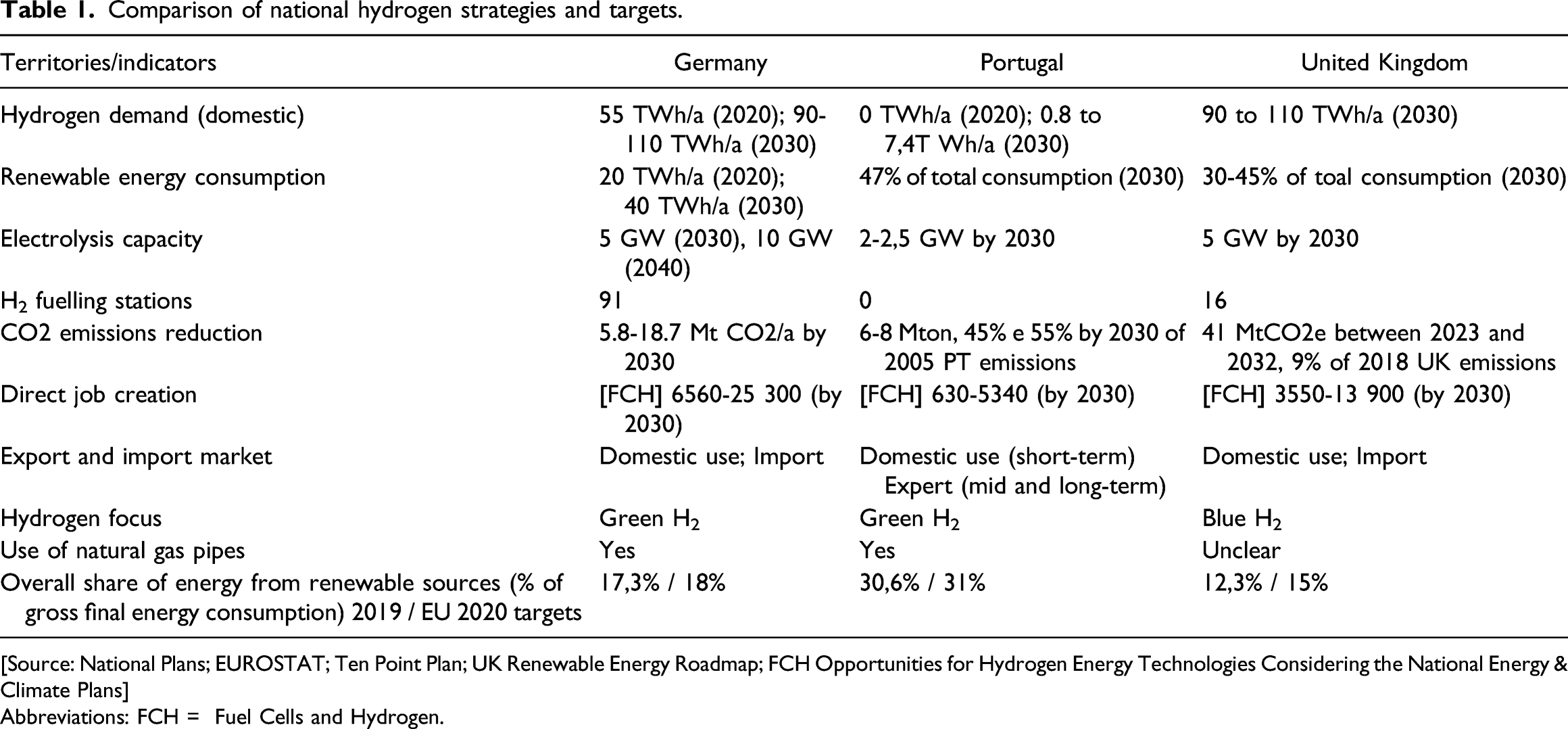

Comparison of national hydrogen strategies and targets.

[Source: National Plans; EUROSTAT; Ten Point Plan; UK Renewable Energy Roadmap; FCH Opportunities for Hydrogen Energy Technologies Considering the National Energy & Climate Plans]

Abbreviations: FCH = Fuel Cells and Hydrogen.

Because so much of the future development for H2 technologies has been linked to renewable energy generation, distribution and above all storage, it is important to understand if these two diverse ‘families’ of technologies will be partners. It is possible they could rivals, in terms of the access to finance or governmental support. Accordingly, we are interested if some countries decide to mainly focus on H2 strategies designed to provide renewables with a storage solution and grid stability, or if other states encourage H2 technologies that have direct energy application, say as a transport fuel. As regards our hypothesis, we assume that a range of copying, learning and analogous modes of national policymaking will be found, along with significant national divergences. We also assume asymmetries regarding the variable importance of the EU level against that of national governments, firms and research networks. In some countries, key decisions on hydrogen will remain mostly national, with the EU playing a residual role. In other states, the relationship may be reversed. Equally, the scope for conflict between EU and national strategies should be variable as well, with some states adopting a direction that could lead to regulatory problems at the EU level. Obviously, of most interest here is the UK, which one would assume after Brexit is the most likely country to deviate away from EU policy leadership on hydrogen.

Germany

Germany’s National Hydrogen Strategy (Germany, Federal Ministry for Economic Affairs and Energy-Germany. BMWI [GFMEAE-GB], 2020) was released in June 2020 following the collaboration of five federal ministries. It proposed significant legislative changes, and ultimately adopted a pragmatic approach over the ‘colours of hydrogen’. While blue hydrogen is a very small part of the plan, a bridging strategy is adopted for a steady shift from ‘grey’ to ‘green’ pathways. Following the logic of a bridging fuel solution, projects in which NG and hydrogen could be co-deployed are therefore a crucial feature of the German strategy. The German plan envisages overall demand for hydrogen consumption to more than double by 2030 and to meet this, renewable hydrogen production must significantly rise. By 2030, the Germans envisage that between 13–16% of their total hydrogen production could be from green hydrogen sources. However, this share is expected to significantly rise by 2050 (Raksha et al., 2020).

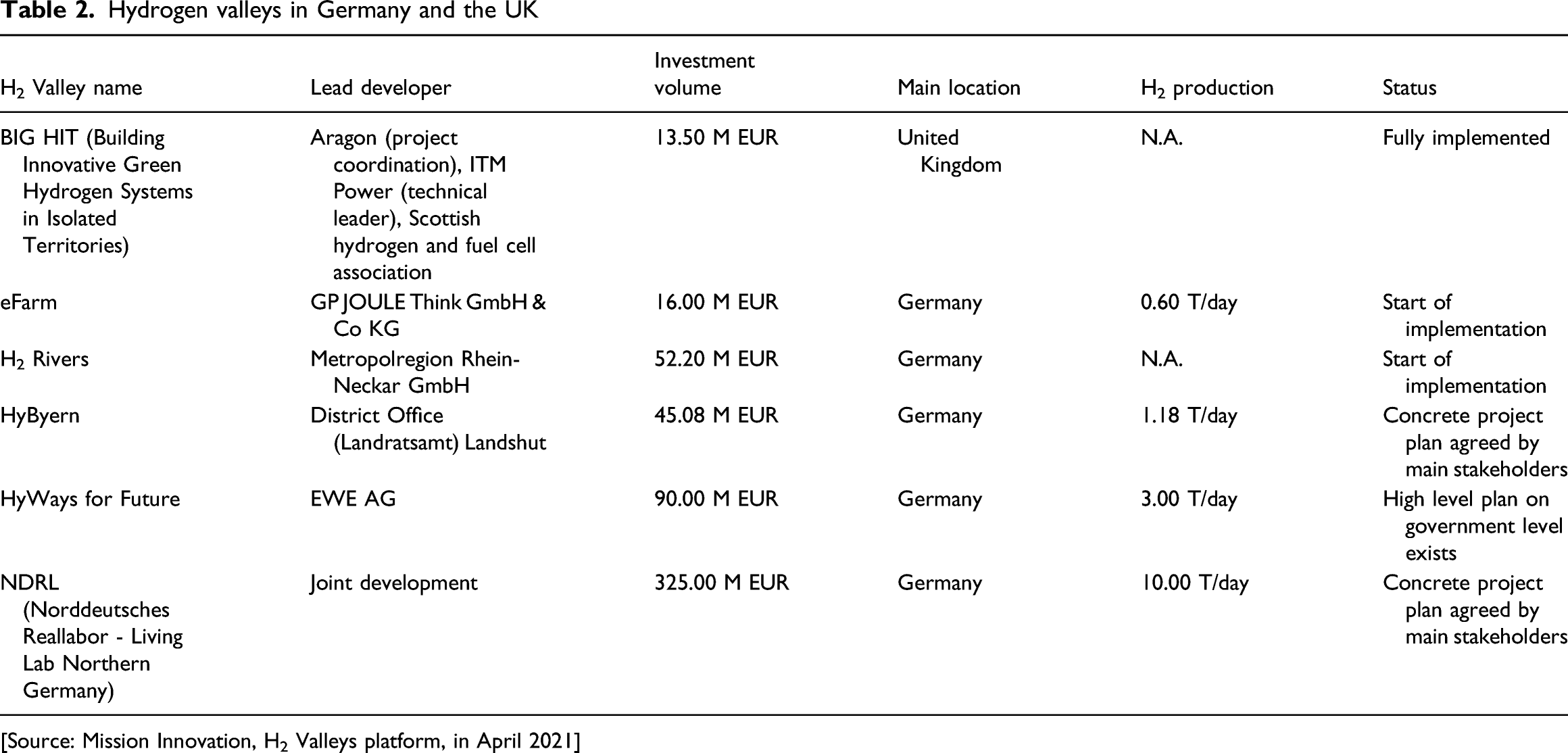

Hydrogen valleys in Germany and the UK

[Source: Mission Innovation, H2 Valleys platform, in April 2021]

German plans and support for hydrogen should be understood within the wider domestic political context of their energy transition, the ‘Energiewende’, which has provided a support framework by systematically justifying an expensive shift away from nuclear and fossil fuels. However, because it also threw up hard lessons about costs and complexity, amidst controversial exceptions for domestic coal (Fischer, et al., 2016), it has also pointed to the need for political feasibility to underpin ambitions. Hence German pragmatism about ‘grey’ hydrogen as a bridge to ‘green’ pathways.

The German approach to hydrogen for the transport sector focuses on the heavy-duty vehicles niche (trucks, buses, etc.) which leads to dedicated support for hydrogen-based fuel cell technologies and hydrogen synthetic liquid fuels. Some firms have already developed specific products. For example, since 2020, at least one German regional transport agency, in Lower Saxony, has been operating a fleet of Alstom hydrogen fuel cell trains 5 . To support green transport and large investments in refuelling stations, the German government has pledged €3.6 billion, with a further €3.4 billion available in grants, all for the construction of refuelling and charging infrastructure for heavy-duty vehicles, buses and trains. The number of refuelling stations provides a good indicator of the increasing ambition level and of success in sustaining this. Whereas in 2014 Germany set an ambitious target of 100 Hydrogen Refuelling Stations (HRSs) for 2020, by the first quarter of 2021, Germany had 91 hydrogen filling stations. Germany then has both a track record of ambitioning and of achieving such audacious targets.

When it comes to aviation and maritime sectors, the German plan notes the difficulty of decarbonising these sectors via electrification. Hydrogen has been identified as an energy source that could help aviation decarbonise and the German strategy mentions a quota for green fuels in the aviation sector of at least 2% by 2030. The strategy also provides for €25 million from ‘Maritime Green’ funding instruments and another €25 million for hydrogen and hybrid aviation fuels.

Reflecting an overall very high level of ambition, Germany received 200 hydrogen project applications in the 2021 IPCEI call (Important Projects of Common European Interest). These applications came from major industrial firms (ThyssenKrupp, Steag, Air Liquide, H2V, Uniper, Siemens Energy, Engie) which reveals how important the private sector is for German plans regarding hydrogen and how H2 technologies have gone mainstream as part of their portfolio of investments. Many well established German firms now regard hydrogen as vital for their future positioning.

Portugal

Two months after the German plan was released, Portugal published its National Hydrogen Plan (EN-H2). This placed hydrogen centre stage in facilitating the energy transition for Portugal. Compared to Germany, the Portuguese plan is distinctive for focussing on green hydrogen, not even mentioning the other rainbow of possibilities. Of course extensive co-operation with existing energy infrastructure is not ruled out. Indeed, there is a target of between 10-15% of the natural gas network being injected with renewable hydrogen by 2030 (de Sousa & Cascão, 2020). The idea here is using ‘green hydrogen’ to transform a grey legacy fuel. Moreover, the Sines Project 6 , involves the production of green hydrogen on an industrial scale at an existing LNG terminal.

Portugal is also distinctive for seeking to implement a cross-border support mechanism, based on the REDII Directive, which would be applied to trans-national green hydrogen projects and related renewable energy sources. In other words, Portugal hopes to become an exporter of green hydrogen receiving incomes and subsidies from other member states for this. The Sines project aims to export hydrogen to the Netherlands as part of a broader strategic partnership with the Dutch. Further possible alliances with Germany and Luxembourg have been also identified in this project.

At the centre of the EN-H2 is a key role for REN – Redes Energéticas Nacionais, a commercial concession holder that combines the national gas distribution system with the electricity grid in a single utility. This distinctive regime level feature makes policy integration much easier and should mean that the regime level in Portugal is widely open to hydrogen innovations. Portugal also has a particular emphasis on using H2 technologies for solving problems associated with intensive heavy industrial processes. This would involve Portugal becoming a hydrogen supplier to the chemical industry cluster in the Netherlands, or Belgium and Germany. There is also interest in synthetic fuels for the maritime transport and aviation sector. The EN-H2, like the German plan, makes distinctions between the medium and long-term ambition, but, in this regard, one can note differences with the German case. A target of between 50-100 H2 refuelling stations is set for 2030 whereas Germany is close to that already (Diario da Republica Eletronico DRE, 2021).

Portugal has an advantageous position in renewables production due to its long coastline, geographic location and a competitive advantage already demonstrated in terms of the production of low-cost renewable electricity, which has been seen in recent energy auctions (a weighted average tariff attributed to solar energy of € 20.33/MWh). However, according to the EN-H2, Portugal will only take its place in the wider European H2 market after its energy and industrial sectors are fully decarbonised, and its internal hydrogen market and economy are more stable.

The UK

The UK government released its hydrogen strategy in August 2021 with a headline goal of 5 GW of hydrogen production by 2030 (UK government, 2021). The document also promises 8000 jobs, a £240 million Net Zero Hydrogen Fund, as well as revenue mechanisms for private sector investment. Given how recent this plan is, our observations about Britain are mostly based on the policy documents released before that formal strategy was launched. This also underscores how the UK is a relative latecomer in having a formal national hydrogen strategy. Moreover, the development of this new strategy outside the regulatory reach of the EU, notably free from EU competition law requirements, remains somewhat opaque. What is clear is that industry, power (electrification, storage) and transport are the main focus of British hydrogen ambitions. Although the UK has only two H2 Valleys identified (Table 2), these appear to be well advanced. One distinctive feature of the British approach is to frame their national hydrogen plan as partly an industrial renewal and development strategy and there is a focus on commercial competitiveness by ensuring that the UK is not dependent on H2 imports (UK government, 2021: 13).

Overall, the main UK policy features within the midterm plan (to be accomplished by 2030) include: expanding British offshore wind developments (40 GW to be installed); establishing four industrial cluster CCUS projects; a possible ‘pilot hydrogen town’; financing the introduction of 4000 EV/FC buses; and ensuring that the legal and regulatory frameworks will be in place by 2030 (UK government, 2021 24–25). As of late 2021, the UK has 16 refuelling stations opened or planned and a hydrogen fuel passenger ferry is being developed in Orkney, Scotland. There is also Hydroflex, a hydrogen train developed by the University of Birmingham (2019), and there are several projects involving FCE buses around the UK, such as the Wrightbus FCE buses for London and Aberdeen (Wrightbus. “Our History, 2021). There is some British interest in the aviation sector, seen in projects such as the HyFlyer developed by ZeroAvia (ZeroAvia. Infrastructure grants, 2021) and the hydrogen research project Enable H2 (EnableH2 Project. Technologies, 2020).

Somewhat complicating things, the Scottish government have decided to make its own hydrogen strategy, which was released in December 2020 7 . Scotland, which has a distinctive profile on energy policy (McEwen, et al., 2019; Munro, 2019), has a strategy that focuses on energy exports. Projects involving green hydrogen are to be developed across Scotland involving offshore energy facilities, with the goal of adding £25 billion annual gross contribution to Scotland’s Gross Value Added (GVA). However, Scotland, in its hydrogen policy statement also focuses on a ‘greyer’ energy pathway until 2045, setting goals on clean hydrogen instead of green hydrogen, and having NG reforming aligned with CCS systems as its main source of hydrogen production (Scotland, Directorate of Energy and Climate Change, 2020). In this respect, it is more like German policy, albeit with an export orientation.

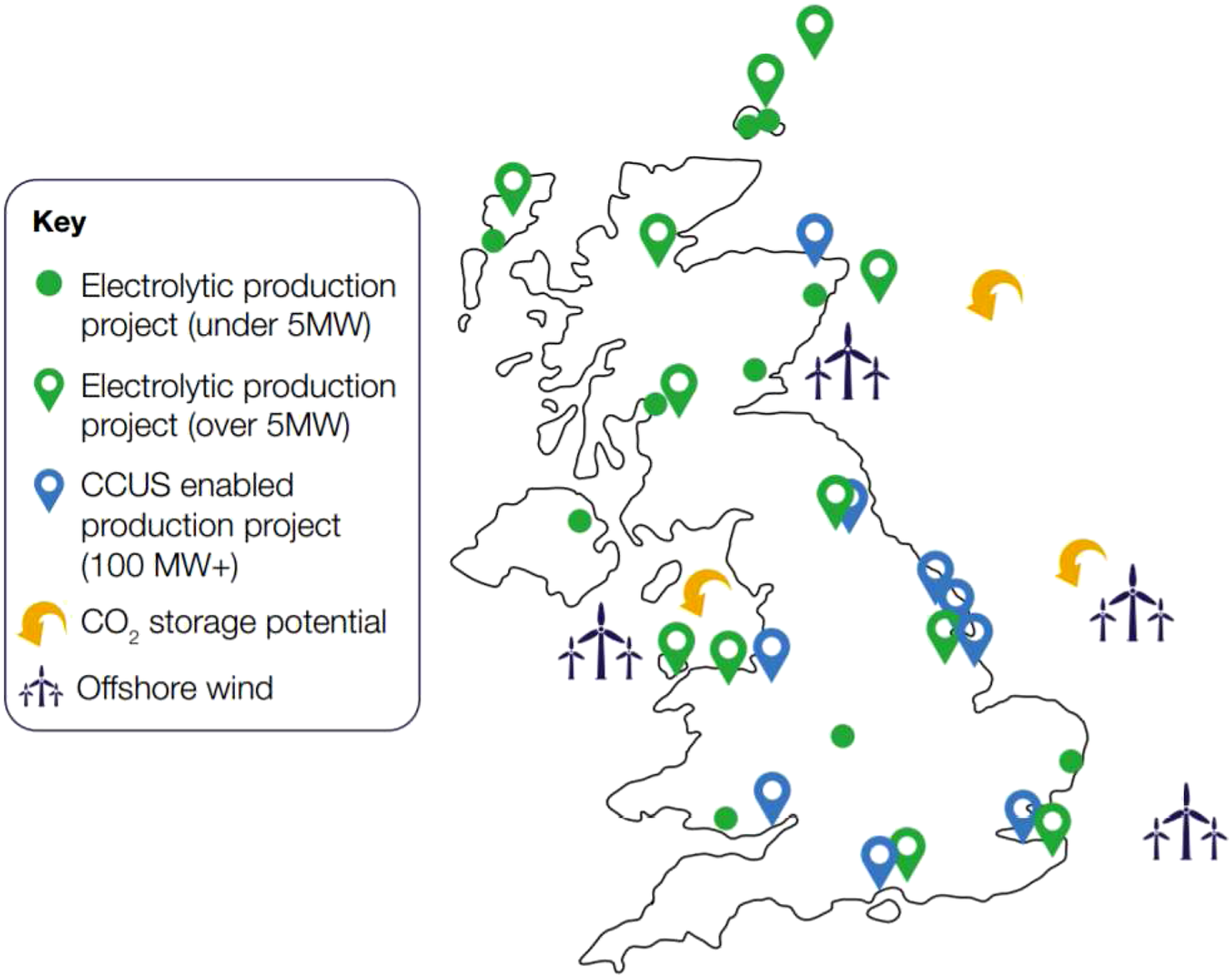

This combination of blue and green hydrogen in the UK system is revealed in Figure 1, which presents the hydrogen proposed projects in the UK and highlights the production mix envisioned in its long-term hydrogen strategy. The UK is in an advantageous position regarding the hydrogen market establishment because of its widespread experience in the use of natural gas, its expanding offshore wind sector and its favourable geology for large-scale storage of hydrogen places. The UK has one of four operational underground structures for hydrogen (95% purity) in the world, a bedded salt cavern system in Teesside (UK) (Zivar et al., 2021). By way of contrast, the German approach is to rely on CO2 storage in neighbouring countries. Both Germany and the Portugal do not state specific investments in blue hydrogen technologies, only mentioning possible European funds (e.g. Innovation Fund) for temporary low-carbon hydrogen solutions, whereas the British pledge up to 1billion£ for CCUs and set four CCU hubs to be operational by 2030 (UK Government, Department for Business, Energy, and Industrial Strategy, 2020). Thus, the UK expects to use its natural features, using many marine site for carbon capture and storage but also to develop both green and blue hydrogen (electrolytic and CCUS-enabled hydrogen). Proposed UK electrolytic and CCUS-enabled hydrogen production projects [Source: UK Hydrogen Strategy, August 2021. https://www.gov.uk/government/publications/uk-hydrogen-strategy ]

Energy transitions, hydrogen synergies and renewables

Because the Portuguese hydrogen strategy relies exclusively on green hydrogen production it also requires high-level investment in the development of wind and solar to decrease the cost of clean energy as part of the future H2 generation process. Therefore, investment in H2 also requires huge investment in renewables meaning that synergies are strong. As of 2018, Portugal had already about 51% of its total electricity production coming from renewable sources (44% of the total renewable production coming from hydropower, 41% from wind, 10% from biomass and 3% from solar photovoltaics). Given this level of renewables as part of overall generation capacity, greater synergy between hydrogen and renewables is plausible in the Portuguese example.

Germany also has a clear emphasis on using renewables as an energy source for hydrogen production, at least in the medium term. Acknowledging the need for future imports of hydrogen, Germany is exploring partnerships with other countries and is contacting African states, South American countries such as Brazil and Australia. Indeed the German plan has an entire section on international trade in hydrogen and a significant portion of their future ‘green’ H2 supplies may well be imported rather than domestically produced, although this obviously depends on the scale of demand. The German approach also makes clear that the introduction of FCEVs 8 is intended to complement battery-powered mobility and not to compete with that sector. In this regard, Germany intends to maintain its current competitive advantage in ecological technologies, becoming one of the leading nations for green hydrogen engineering.

However, most German hydrogen production is still based on fossil fuels, with refineries and the chemical industry (ammonia and methanol production) being both major consumers and primary producers of hydrogen. These integrated industrial sites using fossil fuels, the so-called ‘legacy’ grey hydrogen, challenges Germany to develop a distinct and viable infrastructure for green hydrogen. The development of Germany’s transport sector has important commercial partners such as Alstrom and Siemens. Such networks have significant political and legal implications because it suggests Germany will have a clear interest in securing a competitive wider European marketplace for hydrogen trade and transfer, with all that this entails. Notably, what is required is at least a minimal technical harmonisation of standards for safe storage and distribution and a mechanism to allow fiscal incentives for imported hydrogen, which ensure that non-German producers of hydrogen can avail of German taxpayer support.

In the UK, hydrogen policies are correlated with the British Clean Growth Strategy, designed to ensure there are options to deploy CCUS at a large scale in the 2030s. Britain has also updated their Renewable Transport Fuel Obligation (RTFO) and produced a 10 Point Plan for a Green Industrial Revolution (HM Government, 2020) with a complete chapter about hydrogen development. The RTFO was designed to drive increased bio/green content of fuels (a 0.3% increase of renewable fuel share of fossil fuel per annum is envisaged). It will also lead to more renewable transport fuel certificates (RTFC) in the UK and a differentiation of fuels based on the origin of sustainable material. Under this regulation, ‘grey’ hydrogen will be treated in the same way as fossil fuels. Therefore, there is at least some support in the UK approach for fostering synergies between hydrogen and renewables.

Natural gas and hydrogen: Friend-enemies?

Hydrogen technologies and the existing natural gas infrastructure have a somewhat interdependent nature: on the one hand, hydrogen can be quite easily integrated into existing NG pipelines and networks; while on the other hand, in the long-term it has to potential to replace NA as a feedstock fuel and energy source. It is both an ally and a rival. Therefore, while NG blending is seen as having great potential in all plans, Europe will also see purely hydrogen domestic pipeline systems being tested, which will require the development of the appropriate regulations and conditions.

For the UK government, Green hydrogen is defined as a development fuel, with hydrogen created from biomethane through Steam Methane Reforming (SMR 9 ). This choice generates a relatively easy route to creating green hydrogen independent of NG supplies. However, the UK NECP draft reveals a scenario where natural gas will be used for conversion to hydrogen, bringing the reliance on imported NG to its highest level by 2040 (UK Government, 2019). Therefore, in the British case the link between natural gas and hydrogen will likely remain very strong, although there is also support for biofuels and sustainable hydrogen. Moreover, if natural gas prices continue to exhibit significant cost increases as they have in 2021-22, there will be a huge commercial incentive to reduce this dependency on NG.

By way of contrast, Portugal is betting on hydrogen precisely in order to reduce its consumption and dependence of natural gas and other petroleum products. Historically, Portugal has a high energy dependence on imported fossil fuels, between 80% and 90% until 2009, and is now working towards reaching 65% by 2030 (Portuguese Government, 2020). These fossil sources have a very significant weight in the final consumption of energy (77.9% by 2017), and the cost of importing them represented around 8.4 billion euros over the last 3 years. Consequently, Portugal seeks to expand its solar and wind resources and add value to these by using their electricity to create H2. However, in the short term the Portuguese also recognise the logic of natural-gas grid blending with clear goals set for this. Thus, even where the ambition in the long-term is to produce an alternative energy source, there is still a recognition of the need to work closely with NG networks and industry.

German plans portray NG networks as hydrogen’s ally. However, what is immediately in question is to what extent are the existing European regulatory frameworks for natural gas appropriate for either blended H2 or exclusive H2 pipelines? Noticeably, the latter will require dedicated regulation but already a low level of blending is permitted in existing NG pipes. Germany is distinctive here in pioneering such blending and has preferred a precautionary low level of 2% H2 when dealing with compressed natural gas (CNG) but otherwise tolerates a very permissive 10% level for regular NG pipelines (Pototschnig & Piebalgs, 2021). Given that Germany will likely be an importer for H2, there is a clear logic here for some EU level of regulatory co-ordination if not harmonisation, which Germany is likely to be a leading position to influence. Because hydrogen is not easy to transport safely and cheaply, it likely favours adjacent states who can share pipelines to nearby German industrial plants. Of geopolitical interest is that this network may also include Russia, which has been a traditional supplier of NG to Germany and has an interest in hydrogen co-production and distribution with NG (Shiryaevskaya, Anna. Bloomberg News, 2018).

Multi-level perspective discussion

Governments tend to be positioned in the driver’s seat on the energy transition, by providing numerous incentives and setting clear priorities. However, this push does not imply a ‘one size fits it all’ approach, as some EU countries have clear targets but do not have the appropriate national policies in place yet. Different challenges and socio-economic or environmental situations constrain them.

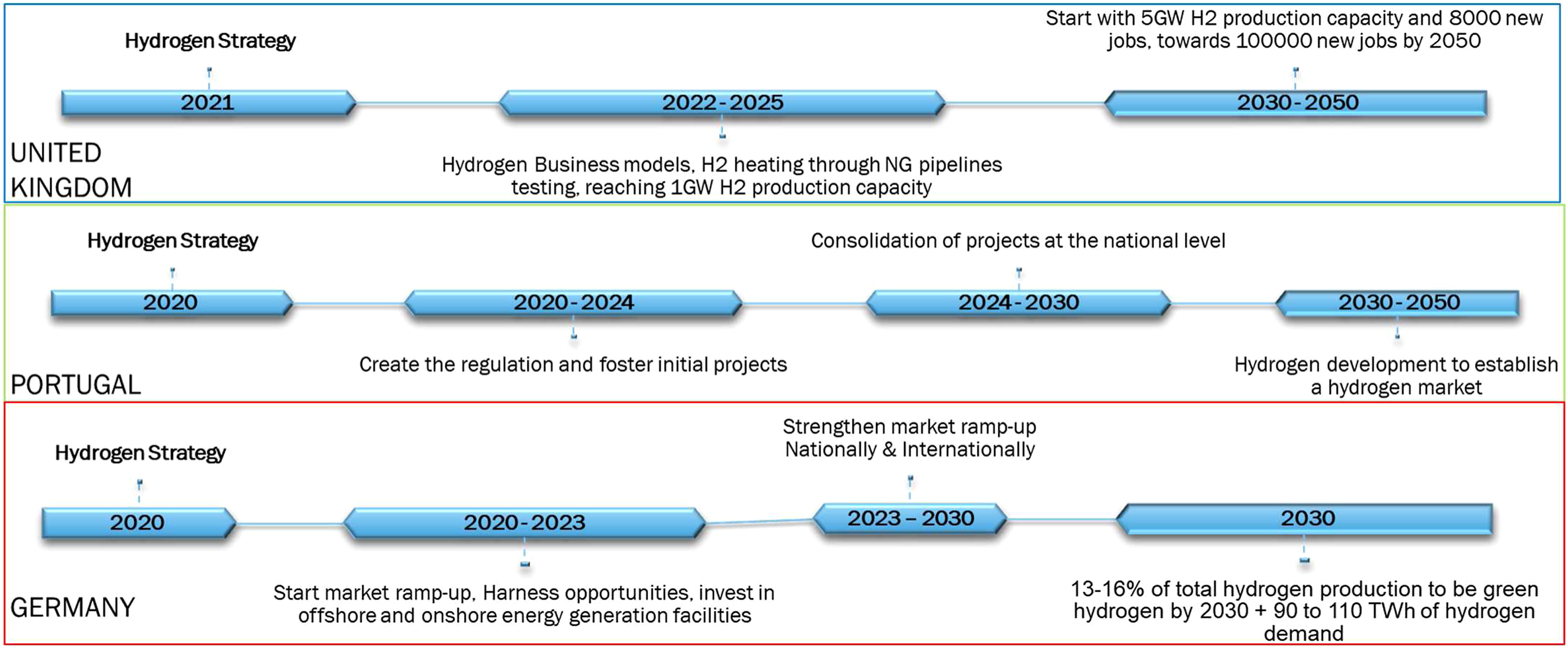

Similar to the EU Net-zero plans, hydrogen strategies also have long-term objectives, set out for the next decades until 2050 (summarised in Figure 2). In the short term, Germany, Portugal and the UK see blending hydrogen into the natural gas network as a lucrative way to integrate it into the existing gas infrastructure in terms of CO2 emissions, with national differences only emerging over the long-term aspirations for green H2. Covid19 recovery plans will also likely influence these blueprints in unpredictable ways. In contrast to the UK’s focus on blue hydrogen, German policymakers work with legacy ‘grey’ producers, at least in the short term. For both Germany and Portugal, the primary actors who are influential concerning ‘grey’ pathways, namely natural gas utilities, appear to be in some ways rivals to green grids and ambitious plans for cleaner electrification. The role of the EU here appears to be imbued with national ambitions and leadership; which is seen most clearly in how both Portugal and Germany linked their specific national hydrogen plans to their roles in chairing the rotating EU Council presidencies. They seized on their hydrogen plans as a means to demonstrate their green recovery credentials and to illustrate their capacity for EU level leadership on energy transitions. Hydrogen national plans’ timeline for Germany, the UK and Portugal. [Sources: Multiple-compiled by the first author]

We suggest that any country that has set its energy policy on a continuing expansion of renewables will be interested in hydrogen to solve the problem of electricity storage and enhance grid stability; however, the degree of ambition for green hydrogen is variable. Portugal explicitly wants to generate H2 from renewables not just use H2 to further the share of renewables. Yet all three countries realise it will take a long time before H2 production from renewables will be a significant share or cost-effective. Hydrogen technologies are relevant for several regimes and not just the obvious ones of electricity or natural gas distribution, but also the complex regimes for chemicals, heavy industry, transport, etc. Moreover, while there is a plethora of activity and innovation at the niche level, it is at the regime level that policies for hydrogen are yet to be implemented. National plans are in place, at least for many states. How these plans will be executed remains very much an open question.

At the landscape level, we find significant structural changes favouring hydrogen. New landscape drivers such as the surge in natural gas prices in 2021, the ongoing controversy over fracked gas, and a wider critique on the overreliance on natural gas as a bridging fuel, have all created clear incentives for alternatives to NG. Brexit could also be included in the landscape category as a political shock to the EU, but it is still not clear to what extent it has affected hydrogen, other than it creates a regulatory opportunity for the UK to deviate from EU norms. However, it is quite evident that while the UK does have some different approaches, notably an interest in so-called blue hydrogen, the emerging British hydrogen market needs to be able to trade with European partners, as much as global ones. Therefore, it seems likely that the UK will not want to deviate too much from its European neighbours. As EU technical standards for storage and distribution evolve these may be closely replicated by the UK for that reason. There are also overlaps via shared hard infrastructure-gas pipelines to EU states that may become conduits for blended H2/NG. British Offshore wind farm investments could also benefit from greater North Sea grid co-operation, which includes a possible shared ‘energy island’, which could augment more solid plans for a growing UK North Sea hydrogen storage network (Bryant, 2021; Stones, 2021)

The one real scope for British divergence and competitive advantage is likely to be around the ability of the UK Treasury to subsidise key projects without any Commission scrutiny or limits. Equally, some environmental and maritime planning requirements, as inherited courtesy of EU law, may be revised if they pose an impediment to British hopes for CCS sites and technologies. Given that many of these are on sensitive coastal locations this potentially simplifies things for British developers of H2 CCS projects.

However, the UK’s accumulated public debt levels may limit the overall ‘subsidy envelope’ for hydrogen projects. Moreover, the EU regulatory approach is actually permissive of very high levels of subsidy as long as these are distributed via open, transparent and competitive means, notably capacity auctions. It is also usually a condition of the Commission’s approval that funds would only be delivered for hydrogen produced by renewable energy sources, revealing how the EU may become but more ambitious but also less tolerant of the competing claims of ‘grey’, ‘blue’ or ‘green’ H2 projects.

Summarising the discussion using the MLP approach, Figure 3 sketches out how the MLP approach interprets technology transitions for hydrogen and identifies fundamental regulatory challenges at different levels. The MLP approach emphasises that without this sort of interaction at multiple levels, a transition is unlikely to happen. Hydrogen niches are the individual examples, projects, initiatives for how this transition can proceed and how this technology can be applied. However, the regime level is where hydrogen technologies emerge, initially as a new trend and later as a mature technology pathway. Conception of the multi-level perspective applied to hydrogen [based on Geels 2006]

None of the countries examined here exhibit evidence that the various ‘regimes’ (for electricity, transport, etc.) were interested in co-opting and controlling emergent hydrogen niches. Rather than presenting them with disruptive change, hydrogen niches are typically seen as providing well-established regimes, such as chemicals, with new ways to face the challenges of decarbonisation. For now, it seems that all countries are following a more cooperative approach to policy-making, although competition may emerge once hydrogen reaches more technologically mature levels.

Conclusion

In the longer term, the EU will increasingly have to consider regulatory and competition policy issues associated with national hydrogen strategies because they have the potential to create market impacts that could lead to monopolies, dominant positions and preferential trading conditions based on rules and subsidies. Germany, a leader in hydrogen production and consumption, was one of the first EU countries to release a national hydrogen strategy, even before the EU strategy itself. The UK is something of a latecomer, establishing a national hydrogen strategy in 2021. Portugal as a small state, with its national hydrogen strategy released right after the EU strategy, offers an appealing and valuable contrast to the previous countries.

It is interesting that at the level of rhetoric and political signalling, both Portugal and Germany have linked their specific national hydrogen plans (both delivered in summer 2020) to their relative roles in chairing the rotating EU Council presidencies. The EU’s regulations governing permissible state aid (subsidies) for environmental protection are promised to be reviewed shortly as part of the present wave of reviews on climate targets, policies and measures (Banet Catherine, 2020). If the EU, perhaps under German pushing, continues to be indulgent in how generous national treasuries choose to be in supporting hydrogen technologies, then leaving the EU will not appear to have made that much of a difference for the UK. Moreover, regulatory conflicts between national strategies and EU ambitions seem to be limited, at least for now.

Above all, we note the importance of the colours of hydrogen as a distinctive issue for regulation and national plans. The UK has a very distinctive focus on ‘blue’ hydrogen pathways, which will involve CCS technologies and making use of many redundant underground sites (especially in coastal/marine areas). While German policymakers will certainly anticipate some CCS-H2 approaches (notably in tandem with CO2 reductions for the cement sector), there appears to be greater interest in working with legacy grey hydrogen producers in the short term, and only aspiring to more ambitious (and risky) purely green hydrogen pathways over the longer term to 2050.

The primary actors, who are influential as regards ‘grey’ hydrogen pathways, for both Germany and Portugal, are nationally situated natural gas networks, suppliers and distributors. They typically constitute a complex but politically salient socio-technical regime in every state. In some ways, they rival the national electricity grid (although in Portugal they are co-joined) which has a priority in seeing hydrogen used to store renewable electricity and add baseload. In the case of Germany, we would also draw attention to the influential chemicals sector as also playing a role here in pushing for ‘grey’ legacy hydrogen approaches. At the regime level, the extent to which hydrogen technologies are recognised as a threat or rival to now powerful regimes – such as chemical production, land transport and electricity – is a pivotal dimension in analyses of this sort and requires more detailed examination beyond the scope of this paper.

As regards the EU’s role, probably the most urgent matter is to advance from funding pilot projects to becoming a global regulatory leader, excelling in the harmonisation of technical standards and policies. Only then, can the EU give clarity on the safety and environmental credentials of the many colours of hydrogen, a vital move to support investors and facilitate cross border hydrogen investment. Our findings support recommendations that would be useful to both national, EU level and international hydrogen policy-makers, since the success of any national strategy may well ultimately depend on supportive measures from the EU and global partners. In particular, we draw attention to the need for further studies and that researchers should be alert to complex interaction effects between all three levels of niche, regime and landscape. We also observe how this precious molecule has unique spatial features as regards its potential trajectory of development. Ideally, it can be deployed in local hydrogen valleys, which combine all actors of the hydrogen value chain from production to end-users. Equally obvious, is the commercial and technical logic of cross border trades, in the short term using existing natural gas networks if suitably modified. Such trade requires technical regulatory standards to underpin it and momentum for such appears to be at an early stage.

Finally, we underline here that many interrelated, if not fundamental, regulatory fissures and challenges for H2 technologies exist in a European context. Hydrogen is becoming mainstream as regards technology and investment. However, it is not yet a mainstream regulatory concern. Probably the most important challenge is the extent to which national and EU plans or policies favour grey or blue over green hydrogen in the short term, and, how ambitious they are about green hydrogen in the long-term. While there are undoubted differences between the countries studied here and more generally across Europe, there is also a widely shared enthusiasm that the hydrogen’s hour has finally come.

Footnotes

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This study is supported by H2020 Marie Skłodowska-Curie Actions (86115).