Abstract

Meeting climate change goals requires both the decarbonization of the electricity sector and the electrification of much of the rest of the economy. However, the electricity sector is navigating major disruptions that are changing the regulatory and business landscape. This article focuses on the question of whether these changes would help or hinder electrification, taking transportation as an example. Like the electricity sector, transportation is undergoing a deep transformation. We suggest that businesses in both sectors will at some point offer aggregated services, repackaged as subscriptions, and traded on digital platforms. We also argue that data created by these activities would be so valuable that this could be reason alone to move toward this model. This could create synergies between companies that could eventually lead to a rebound effect of electrification, with more vehicle miles traveled and more electricity consumption than before.

Keywords

Introduction

Meeting climate change goals requires both the decarbonization of the electricity sector and the electrification of much of the rest of the economy (Farrow & Chen, 2018; Rockström, Sachs, Öhman, & Schmidt-Traub, 2013). However, the electricity sector is navigating major disruptions that are changing its regulatory and business landscape. New distributed energy resources (DERs), a combination of distributed generation, storage, and digitalization, allow households to generate, consume, shift, and reduce their electricity consumption, largely bypassing traditional utilities. This article focuses on whether these changes to the electricity sector will help or hinder further electrification, taking transportation as an example. This is an interesting question because electricity and transportation, both traditional sectors, are experiencing deep transformations and could have an intertwined future: electricity could provide the basic “fuel” for transportation, while transportation could be the major engine for growth in electricity demand.

New technologies in the electricity sector challenge the dominant position of utilities and could potentially lead to the “servitization” of the industry: instead of buying kilowatt-hours, customers would buy the service the electricity provides, such as cooling and heating (Watkins, 2017). Or instead of buying electricity as a commodity, consumers could purchase a product differentiated by its intangible attributes, such as “clean” or “reliable” (Fuentes, 2016). Or firms could provide services to help customers satisfy the residual demand not met by their home systems (Fuentes, Blazquez, & Adjali, 2019). In the transportation sector, new technologies challenge the dominant solo car ownership model in favor of a new model of “mobility as service,” which forgoes the acquisition of the asset, the car, instead of buying the service it provides directly (Cowen, 2018; Fulton, Mason, & Meroux, 2017).

Technological progress generally shifts the supply curve to the right which, for a given demand curve, results in lower prices, since the same quantity can be produced with less inputs and an increase in the quantity of demand. If technological innovations in the electricity and transportation sectors create similar impacts this would, in all probability, lead to more electrification of mobility. What would happen, however, if innovation in one sector resulted in impacts similar to a supply shock, but innovation in the other did not? While technological disruptions in transportation would most likely reduce the implicit price of mobility, changes in the electricity sector would not necessarily have this result.

A positive supply shock would be guaranteed if there are synergetic effects of combining transportation and electricity technologies though. In both industries, the combination of different but complementary new technologies challenges the dominant business model. We call this the “iPhone effect.” 1 In the power sector, the combination of photovoltaic (PV) panels + batteries + demand response gadgets would allow households to bypass utilities’ services and even disconnect from them altogether. In the transportation sector, the combination of sharing technologies + electric vehicles (EVs) + automation would free consumers from the need to own a car.

We, therefore, explore whether new electricity and transportation technologies together could create an even bigger “iPhone effect” arguing that businesses in both sectors will eventually offer aggregated services, repackaged as subscriptions, and traded on digital platforms. We also argue that the data created by such activities could be so valuable that this alone would reinforce such a move.

The article is structured as follows. The second section provides the conceptual framework of our analysis. In the third section, we provide an overview of the technological changes in each sector and discuss the potential impact on market structure, products, and services. The fourth section identifies the potential synergies in the application of new technologies in both sectors. In the fifth section, we discuss some potential regulatory implications and we conclude in the sixth section.

Conceptual framework

There could be a direct and/or an indirect transition from the use of fossil fuels in transportation to electricity. As Fouquet (2010) suggest, direct transition would occur if, thanks to new technologies, electricity ends up being cheaper, and with better qualities—more flexible, more stable, or cleaner—than the competing fuel. This direct effect would explain, in a first stage, a one-to-one transition from fossil fuels to electricity. This effect could be compounded further as lower implicit service prices could lead to rebound effects that lead to increased consumption (Sorrell, 2009).

An indirect effect could also drive electrification if there is a positive supply shock in complementary goods, that is, if the price of a good decreases, demand for the complementary good increases. Electricity and transport can be mutually complementary services, but the effect of electricity on transportation would be via prices while the effect of transportation on electricity would be via quantities. If the electricity price fell relative to the price of gasoline or diesel as a result of technological disruption, this would lead to an increase in electric mobility. If technological changes in transportation lead to an increase in EV miles traveled, electricity use also increases as a result.

The transition from transportation by horse to the motor car at the beginning of the 20th century illustrates this point. Travelers did not use cars to travel to the same places at the same frequency as they did when they traveled by horse. Motorization increased vehicle miles traveled due to the implicit price reduction in travel and increased their comfort (positive supply shock) leading to car users traveling more (rebound effect). Innovation in motor vehicles (lower implicit prices) created the need for substantial investments in road networks (a complementary good), which facilitated longer and more frequent trips (Srinivasan, 2017). This complementary impact can also be described by the increase in a given market’s size when technological disruption allows incremental demand from groups that were previously underserved (The Economist, 2017a, 2019).

We analyze the impact of transport and power technologies, not in isolation, but to the extent to which they can create potential synergies that replicate the effects of a supply shock, a rebound effect or an indirect impact. This could ultimately lead to more vehicle miles traveled and more electricity consumed than would have been the case if both sector’s technologies operated in isolation.

Technological disruptions in the electricity and transportation sectors

In order to help understand the interconnections of technological disruptions, we first consider in this section each sector individually. We provide an overview of the technological changes in each sector, and then outline how they impact market structures, products, and services, and the extent to which they could create a supply shock. New technologies have the potential to disrupt these sectors as they challenge existing market structures and incumbent firms. They also have the potential to transform the nature of their industry products, possibly creating more intangible services without the need for physical goods (Fuentes-Bracamontes, 2016).

Utility death spiral, electricity services but no supply shock

The power industry faces major technological, economic, and institutional challenges. Significant shifts are taking place with the increased deployment of renewable technologies and the rapid development of on-site generation, information, and control technology. PV panels, batteries, and demand appliances, when combined, can help reduce the reliance on the grid and the utilities’ generation capacity. Hypothetically, this could lead to households producing electricity independently. These technologies also reduce the barriers to entry for third parties, other than incumbent utilities, to participate in the industry. Such shifts challenge the dominant role of existing electricity supply companies and question the viability of the products currently offered by the utilities (Fuentes, 2016).

The effect of these changes on consumer welfare, however, cannot be predetermined. DERs may enhance welfare as they afford consumers with more ways to meet their demand. These technologies could help end users consume energy according to their personal preferences, such as opting for low carbon and local energy sources, which might positively enhance the outcome of the utility maximization.

However, since electricity systems were built to meet total demand, behind-the-meter investments could lead to the duplication of some generation capacity and the reduced use of networks. On the upside, this would also lead to the most inefficient incumbent generation capacity being phased out. The downside would be that fixed costs assets would be used less, increasing the cost per unit of consumption. There is also an equity consideration; some households using DERs may get reductions in their electricity bill, but these savings would not necessarily be translated into system costs because of rate design issues where part of the fixed cost is recovered with variable costs (Borenstein, 2016).

DERs can, therefore, create formal and informal parallel markets. Households that install DERs can operate in both. They would see a shift in the supply curve to the right, as their capacity is added to the utilities’ capacity, resulting in access to more electricity at lower prices. However, households without the means to install new technologies would see a shift in the supply curve to the left, as the cost of providing them with electricity would increase due to the reduced use of fixed-costs assets. Lastly, utilities would see a decrease in the electricity demand, resulting in lower prices and in a mismatch between electricity rates and utilities’ costs (Houghton, Salovaara, & Humayun, 2019), and ultimately threatening the utilities’ financial viability.

To summarize, new technologies can have far-reaching consequences in the electricity sector, from opening the market to new players, leading to a reduced role for the incumbent utilities, to repackaging products as services. The impact of this shift on consumer welfare remains uncertain, however.

Capacity utilization, mobility as a service challenge: The car ownership model

There are three revolutions underway in the transport sector: “peer-to-peer” mobility, EVs, and automation; together, they have helped to create the concept of mobility as a service. Similar to the changes to the electricity sector, outlined above, the combination of these technologies threatens the dominant form of transport, car ownership. This section provides an overview of the implications of these new technologies individually and combined. We then discuss the extent to which these technologies could create impacts similar to a supply shock and how they could impact the transportation industry.

“Shared” mobility has always existed in the form of taxis, metro trains, buses, and so forth. This section focuses on “peer-to-peer” mobility: ride-sharing apps that match passengers with drivers for on-demand point to point transfers, like Uber or Lyft. These apps offer the flexibility for both sides of the transaction to easily enter and exit the market place at will, lowering information asymmetries, and entry barriers. These apps could challenge the car ownership model if consumers perceive that investing in a car is unnecessary, as they receive the same benefits of car ownership in a timely manner and at lower prices (Sprei, 2018). This shift would transform an upfront investment into a per ride expenditure. Of course, consumers acquire other indirect attributes when they buy cars, like status and independence from third-party providers. Thus people who do not value vehicle ownership, or who have a more utilitarian view of mobility, and who value the convenience of not having to worry about parking, for example, are more likely to be attracted to using ride-sharing apps.

EVs are highly disruptive to the automotive industry. The ability to master the internal combustion engine has been a significant barrier to entry for the automotive business. Now a firm could buy a motor, match it with a battery, and become an automotive manufacturer (McKinsey, 2019). An EV is essentially a computer and battery with wheels. In isolation, EVs do not challenge the private ownership of vehicles. The choice of EVs over the internal combustion engine is analogous to switching from coal to gas or renewables in power generation. Whether EVs are more environmentally friendly than combustion engine cars would depend on the source of the electricity used to power them.

Automation, self-driving cars, and connectivity could enable a significant increase in the utilization of vehicles. The average car is driven 11,000 miles per year and left idle for more than 90% of its life (National Travel Survey, 2017 in Weiss, Hledik, Lueken, Lee, & Gorman, 2017). Connectivity implies a change in the operation and design of transport systems that would reduce the time that cars remain idle. Automated transportation could help currently underserved groups like the elderly or people with disabilities be more mobile. For example, active retirees want the ability to get around, but they may not want the expense and hassle of owning a car (The Economist, 2019). Just as with the motorization, automation could change the transport system and land use, health, and the economic structure (Polzin, 2016), leading to substantial reductions in energy consumption and emissions.

In contrast to the technological innovations in the electricity sector, new transport technologies could lead to supply shocks and, consequently, to a decrease in the implicit price of mobility. The logic of this impact is as follows: A shared car can service more rides during its lifetime than a car owned by an individual. This more frequent use decreases the average cost per trip. EVs have higher upfront costs but lower maintenance costs than a combustion engine car. This means that, at a certain threshold of use, an electric car has a lower cost per trip than a car with an internal combustion engine. Sharing technologies would allow electric cars to pass this threshold. Connectivity and automatization would increase this effect for individual cars and, more significantly, across a fleet of cars. It would also be possible to optimize these technologies based on demand flow, traffic patterns, and utilization.

Potential synergies in electricity and transport disruptions

The previous section highlighted the potential for significant technological disruptions in both the electricity and transportation sectors. This section now brings this together by identifying the potential synergies in the application of new technologies in both sectors. We argue that together these synergies could result in a supply shock with a significant impact, leading to lower implicit prices and a rebound in the use of electricity, driven by increased levels of transportation.

Killing two birds with one stone!

Batteries are the common hardware components in new electricity and transportation technological disruptions. They are necessary for households to become energy independent and for EVs to be viable. As such, the more storage technologies improve, the more they enable a virtuous power-transport circle. Improving battery storage capacities would allow EVs to travel longer distances with a single charge and would make it easier for more households to become independent from a utility. Reducing the cost of batteries would be welfare enhancing since it would also reduce the total cost of providing services in the transport and power sectors. This could also increase the use of batteries, leading to economies of scale.

EVs can also contribute to the development of the smart grid by charging during off-peak hours, providing back up power to the grid and helping to incorporate other clean, renewable, zero marginal cost technologies (D’Aprile et al., 2016; Knupfer et al., 2018; Frankel & Wagner, 2017). The extent to which synergies between the transport and power sectors could be forged would depend on the direction and type of batteries developed, and where firms position themselves along the storage value chain. Electricity customers that become both producers and consumers (“prosumers”) could use EVs to offload excess electricity and get a discount with mobility companies.

Platforms, subscriptions, and horizontal integration

This section argues that electricity and transportation business models would converge as a result of technological disruptions. Electricity and transportation services could, for example, be traded on platforms and offered as bundled subscriptions. Having this convergence in their business models would likely create synergies that might eventually lead to more vehicle miles traveled and more electricity consumed than if the services were offered independent of one another. 2

Since services are intangible and heterogeneous, service providers need to package services in a way that establishes the delivery unit and also the scope and number of actions that constitute a delivered service. Because of the cost structure of new technologies, we suggest that electricity could be traded in long-term fixed-price schemes, such as memberships or contracts, in which energy services could be combined.

The economic intuition behind this change is as follows. Renewable energy can generate power from abundant resources at zero marginal costs. Since fossil fuel generated electricity, the element of scarcity is clearly evident; the question is how to price a homogeneous product when an increasing share of it comes from an apparently unconstraint resource. We know that prices should reflect scarcity and that there is not such a thing as a free resource, therefore, the scarcity source of renewables lies elsewhere. We argue that to discover this scarcity, markets that incorporate technologies with negligible short-term marginal costs require parallel markets with positive marginal costs to set prices. For example, we can think of the electricity sector as a fragmented sector, one that provides energy services and the other that provides reliability via installed capacity. Whereas the energy market is priced based on the cost of production, reliability has its own intrinsic supply and demand, that is, capacity is needed until the point where its marginal costs equal its marginal value (i.e. avoiding capacity shortage). With this cost structure, electricity could be traded in long-term fixed prices schemes that reflect the willingness to pay to have access to reliability, the constraint resource.

It is interesting to then explore how transportation might also follow such a path. Mobility is highly predictable most of the time. During weekdays, people go to and come from work and school at the same times, similar to electricity baseload demand. For some people, peak demand for transportation might be those trips that diverge from their usual schedules, such as visits to the dentist or a party on the weekend. As such, the prices for these services could be based on fees for basic and premium services (Helms, 2016). Peer-to-peer mobility apps could offer subscriptions for a given number of scheduled trips, with unscheduled add-ons. This would be similar to the two-part tariffs of mobile contracts, where the consumer pays for a number of minutes of calling time per month with extras at a premium.

Memberships and subscriptions work well when there is no rivalry in consumption, like Netflix stream services. While electricity and transportation do not have this characteristic, service providers could find value in offering this scheme as for them, the opportunity cost of a lost service may be more relevant than the actual marginal cost of delivering it. 3 They would, therefore, be willing to forgo some revenue per trip in exchange of a more stable revenue stream. Subscriptions would also afford providers with greater visibility of demand and data generation that could be used to optimize capacity utilization. Using these subscriptions, households could opt for whichever transportation and electricity features they preferred (see Fuentes et al., 2019). The price for these packaged services would be revealed by the buyer’s willingness to have access to these services, decoupling it from the cost of production.

In transportation, peer-to-peer mobility apps, like Uber or Lyft, already operate on digital platforms. On the electricity side, DERs can transform power markets into a series of nested markets connected through different platforms as if they were multiple-sided markets: a meeting place for a number of agents that interact through an intermediary or platform (Rochet &Tirole, 2003).

The important part is that these platforms can create demand-side economies of scale known as network externalities. Network externalities occur when the value of a product or service increases according to the number of people using it. Katz and Shapiro (1985) ascribe indirect network externalities to any situation where complementary goods become more plentiful and cheaper as the number of users of the goods increases. This is a similar concept to the rebound effect we described earlier.

Coupling transportation and power services in one platform could generate synergies between the two. A platform revenue model would charge users commission for connecting them with providers or vice versa. To be competitive, providers need to charge low margins. However, to be sustainable, this would require a large number of transactions. Providers need to become a one-stop shop where consumers and producers can transact all of their services to gain scale and compensate for the low margins per transaction that they might offer.

When we say that electricity and transportation will be traded on platforms, we need to distinguish between the physical platforms through which electricity is delivered—the transmission and distribution network—the physical network through which transportation is “consumed”—road, rail, and so on—and digital platforms. Contrary to physical networks, where after a certain point they can become congested or stop taking new users, digital platforms have more capacity as the marginal cost of adding one more user can be close to zero, and the fuel that is used to run these platforms, data, is a non-rival in consumption. Therefore, this horizontal integration could leverage the sunk costs of these platforms and, by adding services to them, they could be traded with lower overheads and lower transaction costs.

Data and predictability

Digitalization is another common technology in the disruption of the electricity and transportation sectors. Data generation can provide additional revenue streams for horizontally integrated firms, with the potential to generate more revenue than the actual revenue from the sale of electricity or rides (Foroohar, 2019; The Economist, 2017b). The consumption of electricity and transportation is highly habit dependent and therefore predictable. Transacting these services on digital platforms and via subscriptions would generate behavioral data. Such data could help companies predict the aggregate household demand for power and transportation more accurately, which could lead to operational costs savings. For example, it would be possible to link information on the time consumers leave their places of work, the approximate time of their arrival at home, and the sequence of appliances they use when they arrive. This could help transport and electricity companies plan for capacity expansion and utilization.

Digital technologies can enhance the number of variables, frequency, and granularity of data companies can collect on their consumers. In the past, it was only possible to collect observed actions. For example, a few decades ago companies would only collect data on daily sales. Later, the emergence of scanners made it possible to track those actions, for example, individual purchases, the exact time of purchase, and individual purchase histories, like it to inventory data (Einav & Levin, 2014). New technologies make it possible to keep track of previously unrecorded data that sheds light on the individuals’ decision-making processes. For example, Amazon would record what products were clicked before making a final decision of purchase.

New technologies also make it possible to understand previously unobservable data. For example, for technologies like the ride-sharing app, Uber collects instances when a consumer searches for a ride without ultimately deciding to make a request. This creates the opportunity to infer the maximum willingness to pay an individual may have for some service (Cohen et al., 2016). It also allows the possibility to natural experiments and counterfactual scenarios. 4 It is also possible to harvest non-price-related data relating to electricity demand. Torriti (2017) examines which appliances people use at peak time, according to family type, employment, income, number of children, house size and type, and age.

In sum, the proposition of this section is that the use and monetization of these data, generated as a by-product of electricity and transportation, while having the electricity and transportation, could constitute an important revenue stream for firms.

Local focus

Another consideration is the geographical aspect of new technologies. With more DERs being deployed, the boundaries between transmission–distribution and distribution–commercialization and generation are increasingly blurred, as these processes would occur more often in the same place, the household. On the other hand, the transport revolution discussed here is, in essence, an urban phenomenon (Fulton, 2017).

As such, policies at the municipal level could gain relative preponderance on the development of these two sectors, while national policies would see their influence reduced. This would present new challenges for electricity companies used to national policies but increasingly subject to more municipal legislation. It could fall within the jurisdiction of municipalities, for example, to limit the installation of PV panels near cultural or historical places as it could negatively affect their aesthetics or mandate PV panels as part of the construction code of a city.

The changing business models surrounding transportation might also affect urban design and encourage municipalities to repurpose areas. Hau Thai-Tang, from Ford, puts forward an interesting example: Think about gas stations today. They typically occupy prime real-estate locations. They’re on the corners of major intersections and thoroughfares. If you had a battery electric vehicle, and you no longer need to go to a fuel station as frequently because you can top off at home or at work—and if you couple that with autonomy and a vehicle that can actually go, by itself, to charge up while you’re doing something else—you probably wouldn’t need gas stations in those prime locations. (McKinsey, 2019)

How similar are the disruptions in the power and transport sectors?

We have argued in favor of potential synergies and shared challenges for DERs and mobility as a service. However, there are also significant conceptual differences between these technologies that we cannot ignore. DERs are a move from a centralized to a distributed system, while ride-sharing apps make the reverse transition. The nature of the services they provide is also different. The consequences of these contradictions/inconsistencies might lead to some of the synergies discussed before, like the horizontal integration, not to come to full effect.

DERs have the potential to shift the energy market from the classic centralized model of energy provision toward a distributed system, where households make more granular decisions. These decisions, aggregated, may not be optimal from a systemic point of view, that is, a household may decide to install a solar panel without any consideration as to the impact of the power system. Transport is, in essence, a distributed system that would be moving toward a more “centralized” system, through a digital network that concentrates and predicts decisions made by individuals through using data produced by these technologies.

New technologies, in particular, those concerned with connectivity and sharing, could help to coordinate these distributed decisions and could try to maximize the number of passengers per trip and/or minimize commuting times.

Also note that electricity services are different in nature to transportation services. Although both sectors seem to be becoming more service-oriented, the electricity sector is leaning toward more homemade, amateur production, while the transportation sector is leaning toward the professionalization of formerly decentralized services such as taxis.

Another barrier to access the benefits of these synergies is that there may be other policies with conflicting objectives already put in place. For instance, the road system may not be adequately prepared for an increase in transport. This would be evident from any congestion of physical infrastructure, with all the externalities associated with that. So far, we have treated both electricity and transportation as pure goods, where more consumption leads to higher individual utility, when in reality, they are intermediate goods. Individuals want electricity because of the services it provides, not for its own sake, and the same applies for transportation. For the sake of simplicity, we took the “more” is “better” approach as it is more generalizable. Further research could look into this on a case-by-case basis.

Regulatory implications

We argued that through the horizontal integration of these two sectors in a single platform, companies would obtain economies of scale, lower transaction costs, and obtain complementary data sets, potentially producing a rebound effect that could lead to increased demand for mobility and electrification. Assuming that these objectives are not at odds with other policy objectives, like reducing urban congestion, if renewable sources generated electricity, this could help address the aforementioned climate change problem.

How then can we make sure that these synergies occur? Should this be left entirely to markets? Does regulation play a role? One positive aspect of regulation could be the local focus of this transformation. How to regulate digital platforms infrastructure is an open question that would require innovative approaches. Local jurisdictions, rather than national or supranational entities, may have more flexibility to come up with new regulatory frameworks.

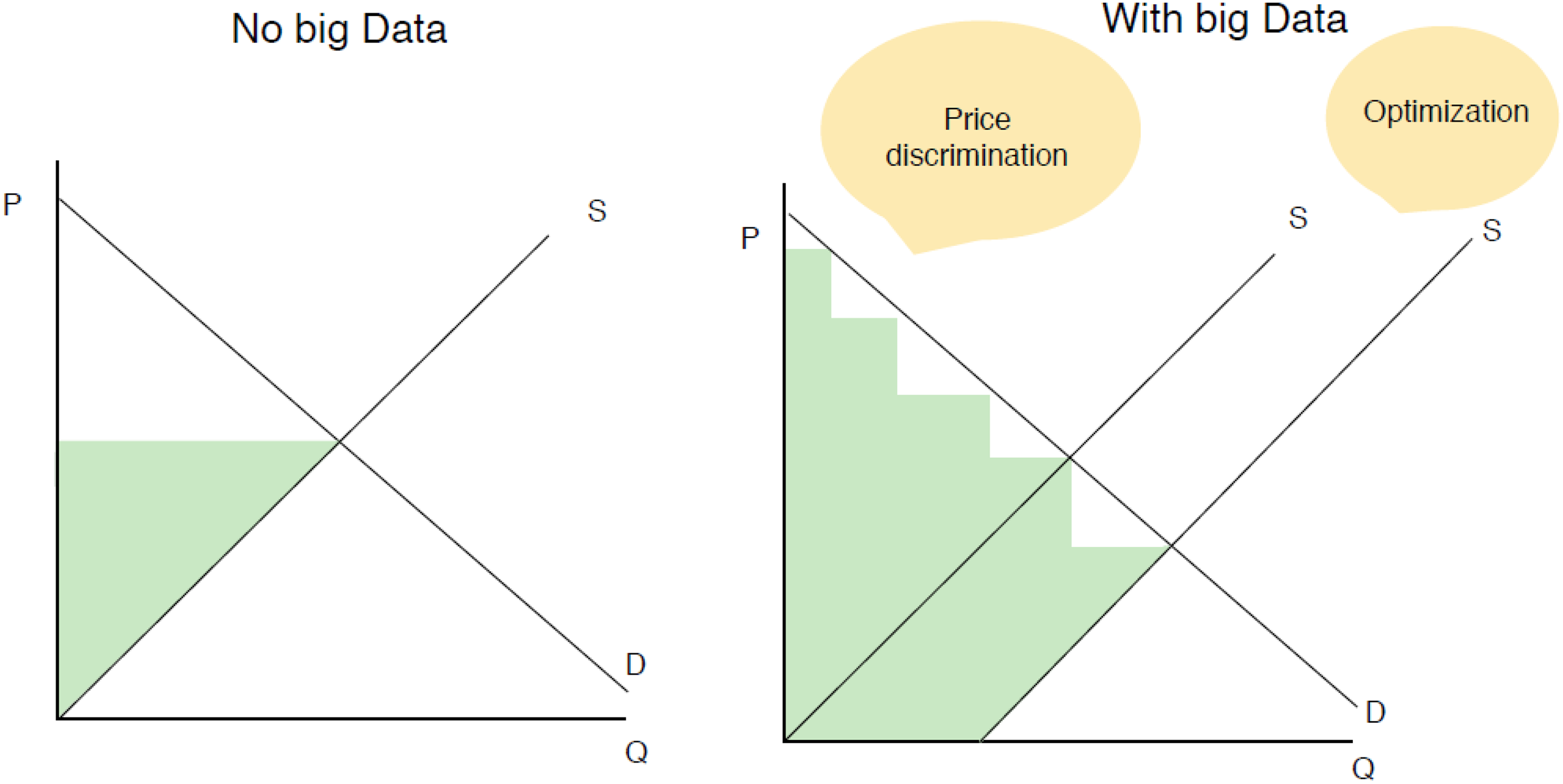

The previous section argued that gathering, analyzing, and selling digital data generated from recurrent activities in both power and transport would be a second, possibly more significant, revenue stream than that generated by power and transport services. There is, however, a regulatory issue to consider since the collection and storage of behavioral data could be a double-edged sword in terms of consumer welfare. On the one hand, as mentioned previously, having a system to centralize this data could help optimize the transportation and power systems. Big data could help, for instance, to better forecast demand for these services and avoid investing in idle capacity. Nonetheless, granular consumer data could also help to discriminate demand; in order to extract the maximum, consumers would be willing to pay for a package of bundled services. Figure 1 illustrates how this might manifest: the supply and demand curves with no big data show the consumer surplus (in white) and the producer surplus (in blue). When companies can use big data, supply should shift to the right. They can achieve cost reductions as they optimize their services by eliminating waste. But they can charge higher prices according to segments of demand by having more accurate descriptions of consumers’ willingness to pay. This by itself would not imply lower welfare, as ultimately the sum of the consumer surplus and producer surplus remains the same. However, there is an equity consideration as the producer surplus grows at the expense of the consumer surplus.

Impact of big data utilization on supply and demand curves.

There is clearly an asymmetry of information between firms and consumers. Regulators can play a key role to reduce this mismatch. One of the reasons for this uneven distribution of information is because data producers obtain this data for free, as a by-product of the use of their products, and not compensating customers for it. Also, that it is only observable and codified, in aggregate with data from other consumers, by them. Other authors have suggested companies compensate those who generate the data by sharing profits from their targeted advertising (Arrieta-Ibarra, Goff, Jiménez-Hernández, Lanier, & Weyl, 2018; Posner & Weyl, 2018).

Conclusion

This article considers the possible technological disruptions to the electricity and transportation industries that, if they were to come into full effect, would threaten the viability of the current dominant paradigms in both industries, solo car ownership and the role of the utility. We, therefore, consider the potential impact of the demise of these two paradigms and attempt to answer whether it would result in the electrification of more sectors of the economy?

To answer this question, we considered the potential synergies between these disruptive technologies and whether they would reinforce each other’s development, ultimately leading to more mobility and more electricity consumed than would have been the case in the absence of one of them. We argue that the coupling of electricity and transportation into a single overarching platform would allow companies to achieve economies of scale, lower transaction costs, and obtain complementary data sets, potentially producing a rebound effect that could lead to increased demand for mobility and electrification. If renewable sources generated electricity, this could help address the climate change problem.

Future research could hypothesize about the resulting new industry structure. We suggest it could focus on one of the following three hypotheticals: Having sunk their fixed costs, utilities would be in a position to offer long-term contracts to electric mobility service companies with both parties benefiting: utilities would have more stability in their revenues, and transport companies would reduce the supply risk of a key input. Transport companies would produce their own power, like any other prosumer, that is, app-based service companies like Uber could even become electricity producers. Electricity-producing households would provide power to transport companies without intermediaries, and companies could deduct the value of this electricity from households’ transportation service bills.

We finish with a provocation, in line with Grossman and Hart (1986). If the future of electricity and transport is intertwined, where would one draw the line of how many more services to include? If horizontally integrated firms exist to reduce transaction costs, why not further extend the firms’ boundaries? When should a firm “produce” and when should it “buy”? What would be the equivalent of Amazon in the energy sector? These are questions for future research.

Footnotes

Authors’ note

An earlier version of this article was given the Best Paper Award at the 8th Conference on the Regulation of Infrastructures, in Florence, Italy, June 20–21, 2019.

Acknowledgements

We are grateful to participants at the conference and to two anonymous referees for their comments and suggestions that helped to improve the article considerably. BM acknowledges financial support from Spanish Ministerio de Economía y Competitividad (RTI2018-093365-B-I00). Nonetheless, we are of course responsible for all errors and omissions.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was financially supported by Spanish Ministerio de Economía y Competitividad (ECO2015-68367-R).