Abstract

This article considers EU and global developments that have affected the availability and affordability of food in the EU and explores the implications for farmers and consumers. Recent and imminent policy changes that may further affect food security, farm incomes and the future of rural areas are also reviewed. The key message is that all policy choices present a trade-off, and this is particularly evident when the sometimes competing goals of food security and sustainability are considered. Strengthening the consumer focus of agriculture and food policy in the EU may offer some solutions, whether that is by nudging changes in dietary patterns or targeting economic support to those at risk of food insecurity. Furthermore, a greater policy focus on innovation and technology adoption is also required to enable farmers to adopt practices that preserve productivity while also protecting the environment.

Introduction

Food security was at the heart of the foundation of the Common Agricultural Policy (CAP) in 1962. The early decades of the CAP can be characterised as the productivist era, when the emphasis was on increasing food production supported by an array of price support policies and a period of oversupply and product surpluses ensued in the 1980s and 1990s (Hennessy and Kinsella 2013). More recent iterations of CAP reform have focused less on production and more on environmental protection in the first instance and more latterly on the broader concept of sustainability. The European Commission’s presentation of the European Green Deal Plan, and the Farm to Fork and Biodiversity strategies in 2020 brought an additional layer of complexity and multifunctionality to the CAP. Consequently, the post-2020 reform had a firm ‘green orientation’ with a strong emphasis on the results and performance of environmental protection programmes. In recent decades, through a period of high agricultural productivity and stable world trade, the issue of food security became less central to the objectives of the CAP. More recently, however, global developments including Covid, geopolitical unrest and extreme weather events have reminded us that food shortages and affordability issues are a real threat, not just in the context of the developing world but also within the EU. Ensuring food security for the world’s growing population while also addressing sustainability challenges such as minimising negative environmental impact, ensuring a fair standard of living for farmers and protecting rural communities and economies will be a major challenge for policymakers in the years ahead.

This article considers recent EU and global developments that have affected the availability and affordability of food and the reaction of consumers and governments to these events. It also explores recent and imminent policy changes in the EU and examines the limited evidence available on the potential impact of these policies on the cost of producing food and its implications for food affordability. The key message is that all policy choices present a trade-off, and this is very evident when we examine the multiple, and sometimes competing, objectives of the CAP. While the need to tackle climate change and other forms of environmental degradation is irrefutable, there will be implications for rural areas, farm incomes, food prices and food security, issues which must also remain central to policy design.

Food security

Food security, defined by the World Bank (2024) as ‘all people, at all times, having physical and economic access to sufficient, safe and nutritious food to meet their dietary needs and food preferences for an active and healthy life’, is emerging as a concern not just in developing countries but also across developed economies, including the EU, as a greater number of individuals become at risk of food poverty. In the 2020–2 period, almost 8% of the EU27 population suffered from moderate or severe food insecurity (FAOSTAT 2023), indicating the presence of inequalities in food access and food security across member states. Delivering safe, nutritious and environmentally friendly food to consumers at an affordable price will be a key challenge for EU policymakers in the years ahead.

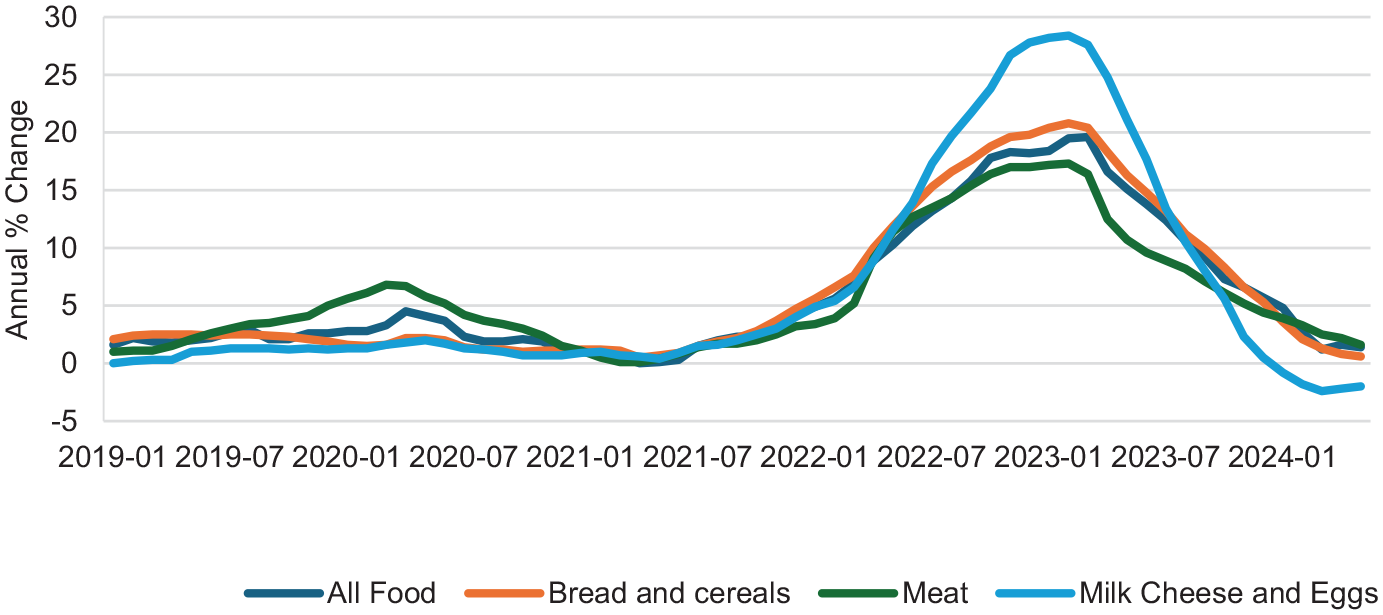

Geopolitical unrest was a major contributor to the spike in food prices experienced in the EU in the 2022–3 period. The invasion of Ukraine by Russia led to an almost 60% increase in energy prices and a quadrupling of fertiliser prices, affecting food production costs in Europe (Eurostat 2024a). This increase in production costs drove food price inflation. Figure 1 presents data from the Eurostat Food Price Monitoring Tool showing the significant price inflation in all food items from mid-2022 to a peak in February 2023 before a gradual reduction thereafter. As the data make clear, the prices of milk, cheese and eggs were particularly inflated.

Monthly annual rate of change in prices for the EU27: all food; bread and cereals; meat; milk, cheese and eggs.

As commodity prices began to fall in late 2022, the sluggish transmission of price reductions across food supply chains through to the final consumer became a major issue of public and political discourse in 2023, with some commentators attributing the delayed response to complex supply chains while others speculated that some industry agents were engaged in ‘price gouging’. Such was the concern regarding high food prices that some governments in the EU, such as Croatia and Hungary, intervened in food markets by using legislation to limit food price increases, while governments in France and Ireland issued stark warnings to food industry executives regarding high prices. Furthermore, in 2024 the Consumers’ Association in Netherlands accused a number of food manufacturers of engaging in ‘cheapflation’, the practice of replacing the most expensive ingredients in food products with cheaper and lower-quality inputs while keeping the consumer price the same or increasing it (Walker 2024).

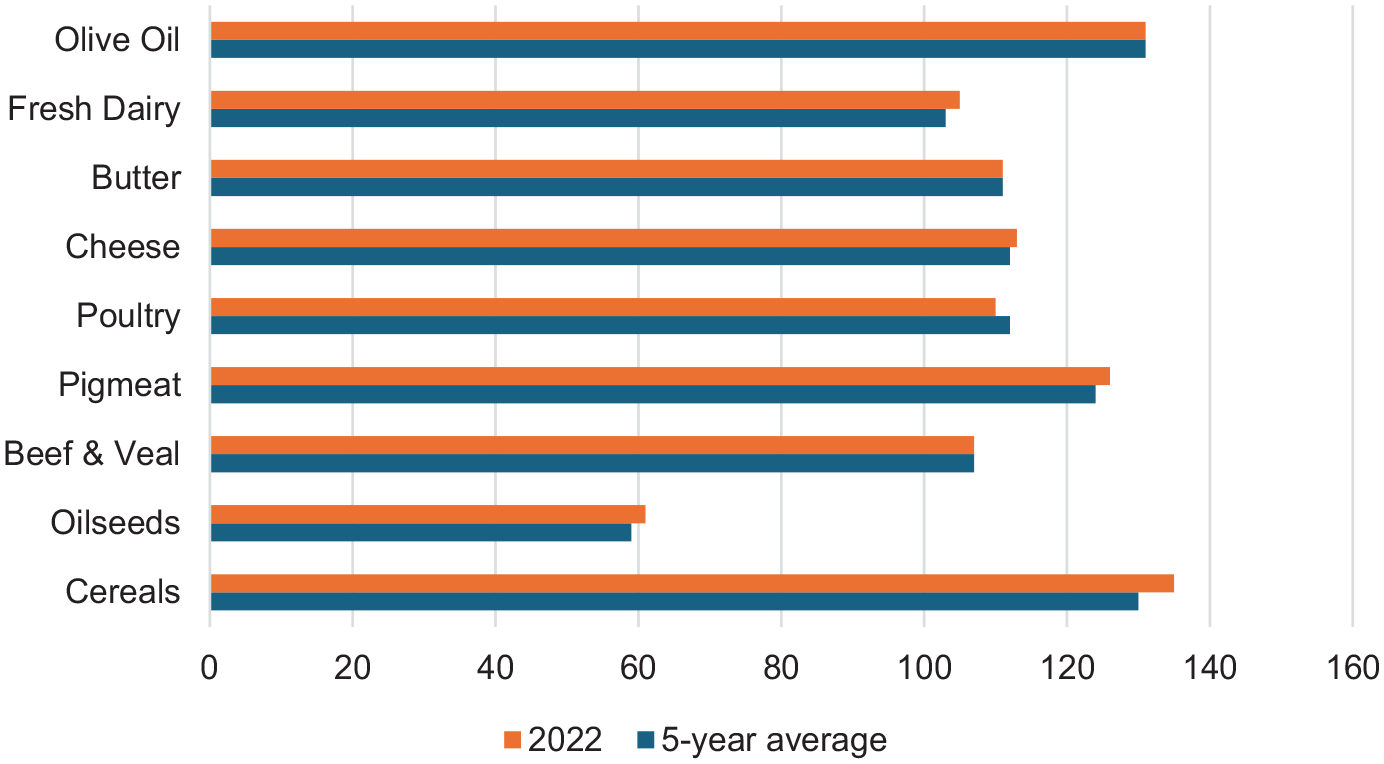

As food production costs and consumer prices increased, food exports from the EU did not decline. Figure 2 shows that EU self-sufficiency in key agricultural products was no worse in 2022 than the previous five-year average, despite the geopolitical unrest and inflated input prices. This suggests that the food security crisis experienced in the EU in the 2022–3 period was one of affordability rather than availability. As Figure 2 shows, the EU suffers from a deficit in oilseeds and, indeed, protein crops more generally. Further data show that the oilseed deficit increased by 16 percentage points and the protein crop deficit by 11 percentage points in the last decade (European Commission 2024). Much of the oilseed imported to the EU is used for animal feed, which raises doubts about the true self-sufficiency status of the dairy and meat sectors and the protein security of the EU more generally.

EU self-sufficiency for selected agricultural products (%).

The prolonged war in Ukraine and other geopolitical events continue to impact commodity markets and food supply chains while political unrest in the Red Sea area is causing supply chain disruption. It is estimated that 12%–15% of global trade transits through the Red Sea, and it is a major channel for transporting agricultural fertilisers, grains and oil from the Persian Gulf to Europe and North Africa. Houthi rebel attacks in the Red Sea area in 2024 have prompted the re-routing of ships around Africa’s Cape of Good Hope, leading to a 30% increase in transit times, further affecting food availability and affordability (JP Morgan 2024).

Climate change and climatic events have also contributed to recent food security scares as more frequent extreme weather events disrupt food supply chains. For example, the late frost in the Mediterranean in 2023, combined with the increased cost of powering greenhouses in the Netherlands, led to a shortage of fruit and salad vegetables across western Europe. Due to global warming, the regions of the world that are fertile and can feasibly produce food are shrinking. Sadly, these are the regions projected to have the greatest population growth, further hindering their ability to feed their citizens.

In a developing country context, geopolitical unrest and the affordability of food are matters of life and death. Despite significant progress in tackling hunger in recent years, the World Food Programme (2024) estimates that global food insecurity is now higher than pre-pandemic levels, with an increase of 160 million people facing acute levels of food insecurity compared to early 2020.

The analysis of the EU data confirms that self-sufficiency in key agricultural products did not decline in 2022, and thus, food security concerns in Europe stemmed from price and affordability issues rather than availability. As the proportion of disposable income that is spent on food has decreased across all developed economies, consumers have become accustomed to paying low prices for food. The public and political reaction to this price spike has shown us that consumers and governments will resist food price increases. This will continue to challenge farmers, food businesses and policymakers: how can we develop a food system that can produce a plentiful supply of safe, nutritious and affordable food with low to zero environmental impact and still support the livelihoods of our farmers and ensure the prosperity of our rural areas?

Policy background

Sustainability and, more particularly, environmental issues have featured strongly in recent reforms of the CAP and developments in corporate reporting. A brief overview of these policy developments is presented here, while the ensuing section considers the implications for food security.

The Paris Agreement, signed in 2015, is the most ambitious global climate agreement adopted to date, as well as the first legally binding one. The targets set in this agreement are implemented at the European level through the European Green Deal, with the specific goals of achieving climate neutrality by 2050 and a net reduction of greenhouse gas emissions by 55% by 2030 compared to 1990 levels (European Council 2024a). These targets are applied to the food and agricultural sector through the Farm to Fork Strategy, whose goal is to ‘make food systems fair, healthy and environmentally friendly’ (European Council 2024b). The policy vector related to the Farm to Fork Strategy, which has several overlaps with the EU Biodiversity Strategy, is the CAP. Three of the main elements of the Farm to Fork Strategy are the organic action plan, which aims to boost organic production to reach 25% of the EU’s agricultural land use by 2030, the aim to reduce the overall use and risk of chemical pesticides by 50% by 2030, and the aim to reduce the use of fertilisers by at least 20% by 2030.

While the Farm to Fork Strategy was broadly welcomed as the action required to move to a more sustainable food system, its implementation has been contentious and only partially successful. For example, the Commission put forward a proposal on the sustainable use of pesticides in 2022, but Parliament rejected it, and subsequently, the Commission announced its withdrawal in 2024. Legislation on nutrient thresholds (announced for 2022) has not yet been put forward, while a plan to introduce health-focused labels on food packaging was also postponed indefinitely following opposition led by Italy. Originally adopted in 1991 and further developed in relation to the European Green Deal and Farm to Fork Strategy, the Nitrates Directive, aimed at reducing water pollution stemming from nitrates used in the agricultural sector, was still not fully implemented in Ireland, Denmark and the Flanders region in Belgium in 2024. Euronews (2024) estimates that of the 31 initiatives proposed as part of the Farm to Fork Strategy, at least 15 of them have yet to be initiated. Some of the opposition or hesitancy regarding its implementation was likely prompted by concerns around food security given that the Ukraine invasion and consequent food price spikes followed the strategy’s launch. Criticism was fuelled by the lack of an accompanying impact analysis and by the subsequent publication of an impact analysis conducted by the US Department of Agriculture, as discussed below, which suggested significant implications for food prices.

In addition to and associated with the Farm to Fork policy, there have been a number of EU legislative and regulatory changes in 2023–4 which will impact businesses operating in the EU food system. Greater reporting obligations will require food companies to gather, verify and report more information on their own activities and those of other companies in their supply chains over the next number of years. These regulatory developments will likely lead to an increased cost of doing business and require greater investment in data systems, technology and potentially artificial intelligence.

Under the Corporate Sustainability Reporting Directive, companies are required to provide a range of information in compliance with the European Sustainability Reporting Standards. This will include information on (1) environmental matters (for example, climate impacts of business activities, resource and waste management, and biodiversity), (2) social matters (for example, equal opportunities, gender equality and equal pay, working conditions and human rights matters); and (3) governance matters (for example, business ethics and culture, anti-bribery and corruption measures, internal controls and risk management systems). The Corporate Sustainability Due Diligence Directive focuses on conducting due diligence on actual and potential human rights and environmental impacts in respect of (1) the in-scope company itself, (2) its subsidiaries and (3) its direct and indirect business partners throughout its chain of activities. The other key obligation being introduced by the Due Diligence Directive is that in-scope companies adopt and put into effect a climate transition plan which aims to ensure, through best efforts, the compatibility of the business model and the strategy of the company to achieve the transition to a sustainable economy and the limiting of global warming to 1.5°C. The Deforestation Free Regulation imposes a due diligence obligation on in-scope companies—that is, those that place or make available on the EU market or export the following commodities and derivative products: palm oil, cattle, soy, coffee, cocoa, timber and rubber as well as derived products such as beef, furniture or chocolate.

The Green Claims Directive (GCD) and Green Transition Directive are intended to tackle, more specifically, unsubstantiated and misleading environmental claims and labelling. The Green Transition Directive is already in force at the EU level and awaiting transposition by EU member states by 27 March 2026. The GCD is following swiftly behind it, to be voted on by the European Parliament in Q3 2024. Once introduced, the directives will impact all sectors, primarily at the business-to-consumer level, with exemptions provided under the GCD for ‘micro-enterprises’.

With consumer demand for more sustainable products and practices increasing, a study commissioned by the European Commission, although for non-food products only, found that significant proportions of environmental claims made by businesses were either vague, misleading, unfounded or entirely unsubstantiated (European Commission 2014). The same study also noted that ‘green labels’ used within the EU had varying levels of robustness regarding transparency and supervision. The GCD is intended to work in tandem with other initiatives to drive capital flows towards more sustainable activities by ensuring that stakeholders can assess commercial environmental claims in an objective manner. The GCD introduces minimum requirements to substantiate claims. Scientific evidence will be required to support environmental claims, and highlighting only positive environmental impacts is prohibited. In particular, the GCD targets explicit environmental claims made by businesses to consumers about the environmental impacts, aspects or performance of a product or the trader itself. This includes a proposed ban on the use of terms such as ‘eco’ and ‘green’ and climate-related terms such as ‘climate neutral’, ‘carbon neutral’ and ‘biodegradable’ without evidence to support the legitimacy of such claims.

The strong emphasis on the sustainability aspect of agricultural policy and corporate reporting, while welcomed from a public good perspective, has also led to concerns about potential increased costs of doing business and impacts on production and productivity levels. Furthermore, it is uncertain who will incur these costs—farmers, food businesses, retailers or consumers—and there are concerns about power, control and value sharing along the supply chain. To date, evidence of the impact of these policy changes and proposals, either ex ante or ex post, is limited. The following section reviews some ex ante policy impact studies on the potential impact on food security.

Implications for food security

A number of studies have examined the potential impacts of the Farm to Fork Strategy, such as Barreiro-Hurle et al. (2021), Beckman et al. (2020) and Bremmer et al. (2021). These are usefully reviewed by Wesseler (2022). One of the first and most controversial impact assessments published was Beckman et al. (2020), a study conducted for the US Department of Agriculture. It estimated that the adoption of the 2020 Farm to Fork and Biodiversity Strategies, with the associated decreases in pesticide, fertiliser, microbial and land usage, would lead to a decrease in EU food production of 12%, decreasing global food security by 20 million people and increasing global food prices by 9% by 2030, thus reducing food availability and affordability. Similarly, Barreiro-Hurle et al. (2021) found that the implementation of those two strategies, combined with the 2014–20 CAP format, could lead to a reduction in total crop supply of between 12% and 16% and a reduction in livestock product supply of between 10% and 17% by 2030. Meat exports would be reduced, which would have consequences on the global food supply. Furthermore, reduced exports of livestock commodities from the EU could lead to importing countries looking to compensate for the losses in supply with products from regions with production processes less constrained by environmental standards, leading to potential spillover effects in terms of emissions and environmental damage. Barreiro-Hurle et al. (2021) estimated that the implementation of the Farm to Fork and Biodiversity Strategies would lead to an increase in the EU’s dependence on oilseed, arable field crops and vegetable imports if the CAP structure were not revised.

Wesseler (2022) has reviewed five studies that have conducted impact assessments of the Farm to Fork Strategy. The summary conclusion is that the strategy reduces agricultural production within the EU and induces an increase in food prices. This is expected to further fuel consumer price inflation within the EU and beyond and result in a decline in welfare within the EU. Wesseler also notes that the decline in agricultural output within the EU may result in leakage effects in regions outside the EU—that is, an increase in production in regions with less environmentally friendly practices. Wesseler does highlight that the studies reviewed do not assume any significant technological developments; it is possible that technological developments could negate some of the productivity losses over time. Finally, Wesseler notes that the studies reviewed do not quantify the potential environmental and health benefits and whether these outweigh the economic costs of implementing the strategy.

There has been relatively little research published to date on the potential impact of developments in sustainability reporting for firms and the cost of doing business related to it. One exception is an ex ante cost–benefit assessment published in 2022 by the Centre for European Policy Studies (2022). They found that the costs associated with reporting, collection and verification of information and external assurance would outweigh the benefits in the short term, at least until sustainability improvements were realised and rewarded in the market. The report also considers the sectoral impact and concludes that sectors with more complex value chains are more likely to expect significant competitive disadvantages. Agriculture is specifically identified in this regard, with the difficulty and potential costs of collecting information about biodiversity, for example, from numerous farm holdings.

Discussion

Whether referring to the Farm to Fork Strategy or the Sustainability Reporting Directives, the analysis suggests that the policy developments will result in an increased cost of production and/or reduce productivity and output. The question of who bears the cost of sustainability is a challenging one. If the farmers’ productivity declines or their costs of production increase due to limits on fertiliser use, for example, or the food companies’ operational costs increase due to data collection, are those increases transmitted across the supply chain to the final consumer in the form of higher food prices or are they absorbed at source? Our recent experience of heightened food prices suggests that both governments and consumers will resist price hikes. This presents a real challenge for farmers, who rightly wonder who will pay for more sustainable production practices and what the implications will be for food security and food prices.

So what is the optimal balance between tackling sustainability issues and curbing food price inflation? Matthews (2023) argues against abandoning our sustainable policy ambitions for fear of higher food prices. He argues that food insecurity in Europe arises due to the inability to access food because of low incomes rather than due to the unavailability of food, and that it follows that providing targeted support to low-income families is a more appropriate response than aiming to limit food prices more generally. While this approach presents some solutions within the EU, it does not address the potential impact of a contracting agricultural output in the EU on global food security. For it is widely acknowledged that the impact of European policies on food security is regional but also global, given the role of the EU as an exporter and, indeed, importer of several key agricultural commodities.

Other analysis suggests that tackling dietary patterns may offer some solutions. A recent study by Schiavo et al. (2023) considered the impact of a deep agro-ecological transition in the EU by 2050, involving a phase-out of synthetic fertilisers, pesticides and antibiotics on the supply side and a shift towards more plant-based food regimes with a reduction of food waste on the demand side. The study found that when accompanied by a shift to more plant-based diets in the EU, an agro-ecological transition in the EU would not be detrimental to global food security and that without increasing its cropland areas, the EU could maintain the same level of exported calories as in a business-as-usual scenario while reducing its import needs. This suggests that dietary changes within the EU could help address regional and global food security issues.

In conclusion, then, it seems that strengthening the consumer focus of agriculture and food policy in Europe may offer some solutions, whether that is by nudging changes in dietary patterns or targeting economic support to those at risk of food insecurity. A number of policy impact analyses, as reviewed by Wesseler (see above), also point to the need to focus policy on innovation and technology change. Investment in the development of alternatives to synthetic fertilisers and plant protection products could boost sustainable productivity growth. More support for the development of green technologies and important targeted support for their implementation by farmers should be a key part of the policy response to the challenge of developing sustainable food systems.

Footnotes

Author biographies