Abstract

Many commentators have blamed Gazprom, Europe’s largest gas supplier, for contributing to the 2021–2 European natural gas price crisis through market manipulation and withholding the necessary gas supply volumes from the European market. Is there any substance to such claims? Is Gazprom really involved in manipulating the European gas market and prompting the record-breaking surge in European natural gas prices? The current article analyses the official figures on Gazprom’s production capabilities, and supply and demand, and offers some insights as to why exactly claims of market manipulation by Gazprom should be taken seriously. It argues that Gazprom did indeed have the ability to ease the pressure on the European gas market in 2021, but did not use it as one would expect of a company acting in good faith. Figures shown in the article lay out a detailed case that the EU authorities should open an investigation into Gazprom’s market manipulation.

Introduction

The European gas price crisis of 2021 caused an unprecedented surge in natural gas prices in the EU. At times prices exceeded $2,000 per thousand cubic metres, an absolute historic record, and nearly 20 times higher than the average European natural gas price in 2020 (TASS 2021a). A combination of unfavourable conditions contributed to the development of the crisis, including soaring demand for natural gas after the lifting of COVID-19–related restrictions, subsequent depletion of European underground stored gas stocks, sharply increasing liquefied natural gas prices in Asia which led its suppliers to prioritise exports to Asia over the European market, reduced renewable energy supplies and other factors.

While some of the causes of the price crisis may be attributed to objective market factors—the natural gas price surge in Asia, the particularly cold winter of 2020–1 and the related drawdown of European underground gas stocks—many commentators have also highlighted potential market manipulation by the Russian gas giant Gazprom, Europe’s key natural gas supplier, as a cause (e.g. Sheppard et al. 2022; Abnett 2021).

In this article some basic facts are provided to support the theory of deliberate European gas market manipulation by Gazprom. The article does not attempt to analyse the entire complex nature of the European natural gas price crisis of 2021, but focuses on one specific aspect: whether there was significant input from Gazprom in escalating the crisis by withholding available gas-production capacities and produced volumes from the European market. The specific question answered here is: did Gazprom do all it could to satisfy additional demand for gas in Europe against the backdrop of rocketing gas prices and insufficient stored gas stocks ahead of the 2021–2 winter season?

The clear answer is no, Gazprom did not do all that it was possible to avoid the crisis. Moreover, it supplied Europe with less gas in 2021 than in each year in the 2017–20 period, and it has significant excess upstream gas-production capacity and stored gas stocks that could help to resolve the European gas price crisis—but it is not using these capabilities as one would expect of a company acting in good faith.

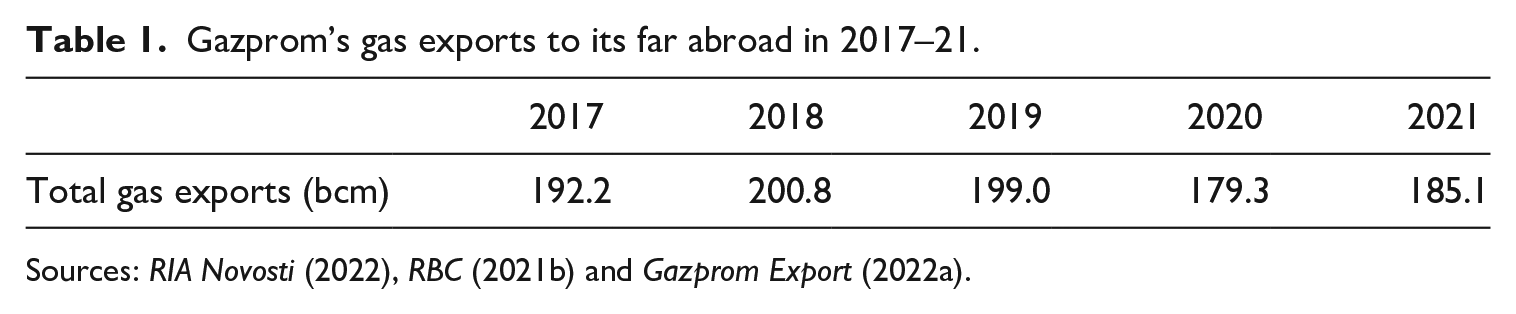

Did Gazprom deliver a ‘record breaking volume’ of gas to Europe in 2021?

Despite Gazprom’s aggressive public-relations claims about a ‘record-breaking’ level of gas exports to Europe in 2021 ( RIA Novosti 2021 ), the facts do not support these assertions. In reality, Gazprom supplied only 185.1 billion cubic metres (bcm) of gas to the so-called far abroad (countries beyond the former Soviet space) (Table 1). This is notably less than the annual exports of 2017–19 and only 3.2% (5.8 bcm) higher than in COVID-struck 2020 (RIA Novosti 2022).

Gazprom’s gas exports to its far abroad in 2017–21.

Sources: RIA Novosti (2022), RBC (2021b) and Gazprom Export (2022a).

At the time of writing, in early January 2022, Gazprom has not provided a detailed country-by-country breakdown of its gas exports, but it is clear that the EU has received a volume of Russian gas that is close to a five-year low. In contrast, gas exports to China have surged, more than doubling in 2021. Whereas during the 12 months of 2020, only 4.1 bcm of gas were transported to China via the ‘Power of Siberia’ gas pipeline, in January–September 2021 alone, 7.1 bcm were supplied to the country (Vozdvizhenskaya 2021). This means that the total annual gas supply to China will likely be around 10 bcm in 2021, exceeding the 5.8 bcm gain in total gas exports to the far abroad in 2021. Another sharp increase in Russian gas exports in 2021 was to Turkey: according to Gazprom, supplies to Turkey surged by 63%, or by 10.3 bcm (26.7 bcm in 2021 vs. 16.4 bcm in 2020) (RIA Novosti 2022).

The rest of Gazprom’s exports to its far abroad—besides China and Turkey—are mostly to the EU. This means that—if the Chinese and Turkish volumes are subtracted from the total figures—the volume of gas received by the EU from Russia in 2021 was more than 10 bcm smaller than that received in the COVID-impacted 2020, and far smaller than in 2017–19.

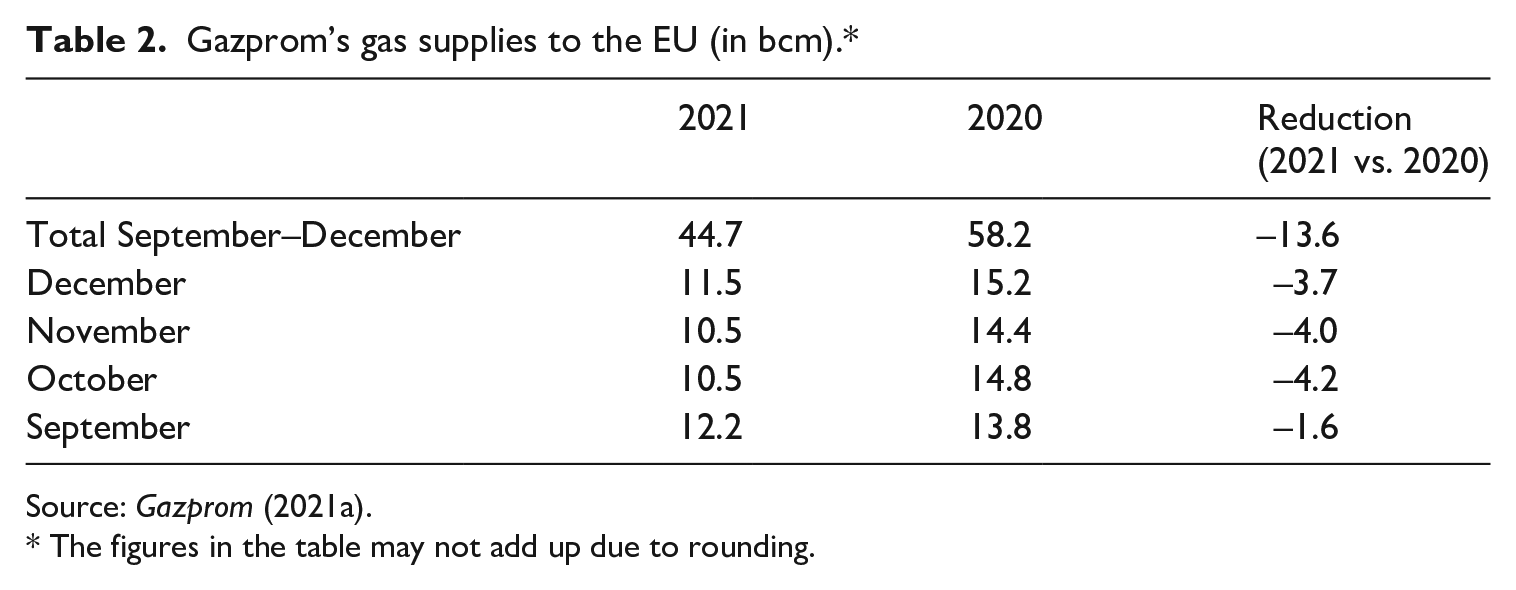

This conclusion is actually supported by the day-to-day EU gas-supply statistics provided by Gazprom on its website. According to this data, in September–December 2021 alone Gazprom reduced its supplies to the EU by 13.6 bcm (see Table 2). Throughout the year, the media reported that Gazprom had refused to book additional gas transit capacity via the Ukrainian gas transit network or via the Yamal–Europe gas pipeline that runs through Belarus and Poland; according to Gazprom’s own data (2021a), gas supplies via Ukraine and Belarus/Poland were reduced by an average of 58% and 51% respectively in the period September–December 2021. There is no reasonable explanation from Gazprom for this reduction in supply.

Gazprom’s gas supplies to the EU (in bcm).*

Source: Gazprom (2021a).

The figures in the table may not add up due to rounding.

In early 2022 Gazprom continued to reduce gas supplies to its European consumers. According to the company itself, between 1 and 15 January 2022, gas exports to countries beyond the former Soviet Union were 41.1% (or 3.7 bcm) lower than during the same period in 2021 (Gazprom 2022).

Gazprom has significant excess gas production capacity

Against this backdrop, Gazprom publicly admits that it possesses significant excess production capacity, which could easily be used to boost European gas supplies—but it is clearly being kept out of the market. A speech delivered by Gazprom’s Chief Executive Alexey Miller in September noted that, ‘our excess production capacities, which is to say, the production capacities that we secure for achieving peak production, amount to nearly 150 billion cubic meters of gas’ (Miller 2021). Mr Miller has openly underscored that this vast excess production capacity is a ‘competitive advantage’ capable of significantly influencing the market (Miller 2021). At the same time, Mr Miller admitted that Gazprom’s gas output in 2021 was the ‘best figure in the last 13 years’ (Gazprom 2021b); Gazprom therefore clearly has enough gas to provide additional supplies to the European market. In August 2021, Gazprom reported a fire at the Urengoy condensate treatment plant, which was mentioned as the cause of some production shut-ins (Interfax 2021). But this cannot be considered a significant factor against the backdrop of such excess production capacity and a reported overall surge in gas output.

However, the question of why Gazprom did not use these exceptional gas production capabilities to supply additional volumes to European consumers during 2021 remains unanswered. This paves the way for an investigation by the EU authorities into the possible withholding of gas volumes from the market in a critical period, given the fact that Gazprom publicly admits to massive excess upstream gas production capacity.

Excessive build-up of stored gas stocks in Russia

While claiming that Gazprom is simply ‘incapable’ of providing extra gas supply volumes to the European market beyond its minimum contractual commitments (Kommersant 2021), not only is the gas giant boasting about its 150 bcm excess gas production capacity but it has also reported a record-breaking injection of gas into Russian storage facilities of 72.6 bcm (RBC 2021a). This figure rises to 73.8 bcm when one includes what has been added to Gazprom-owned storage facilities in Belarus and Armenia (RBC 2021a). That is an increase of nearly 22%, or more than 13 bcm, on the storage reserves accumulated in Russian gas storage facilities in the winter of 2020–1, which Gazprom reported back then as a ‘record volume of injection’ (RBC 2021a). This 13 bcm of gas could have significantly eased the pressure on the European gas market: it almost exactly corresponds to the reduction in Gazprom’s supplies to the EU in September–December 2021 (see Table 2). During Alexey Miller’s meeting with President Vladimir Putin on 29 December 2021, he stated that by the end of December, stored gas volumes in Europe’s underground reservoirs were 21 billion cubic metres lower than for the same period in 2020 (President of Russia 2021), meaning that Gazprom’s additional supply of 13 bcm of gas would have reduced the European underground stored gas shortage by two-thirds. Therefore, an extra 13 bcm of gas from Russia would have significantly contributed to solving the problem.

Perhaps Russia needed a record-sized gas supply due to extremely cold weather? The winter of 2021–2 does indeed appear to be cold—but not to the extent that Russia needed to increase its underground gas reserves by 22% compared to the record-breaking 2020–1 injection season. Mr Miller himself reported to Putin on 29 December 2021 that, at that point, Russia’s underground storage facilities were still filled to 83% of their capacity, and only 17% of these record-breaking reserves had been drawn upon in November and December (President of Russia 2021).

Please note that Gazprom includes these domestic gas storage injection volumes when it calculates Russian domestic gas consumption—so when Gazprom reports an increase in Russian domestic gas consumption in 2021 of about 30 bcm (Gazprom 2021b), these volumes include the 13 bcm of gas injected into domestic storage facilities.

The bottom line is that, on top of maintaining enormous excess upstream gas production capacity, Gazprom has injected a record-breaking volume of gas into Russian gas storage facilities. This means that it has plenty of gas to satisfy additional European demand, if it only had the will to do so. But it does not.

Withholding gas from European gas storage facilities

Gazprom owns significant gas storage capacity in Europe—according to its own data, a total capacity of over 12 bcm (Gazprom Export 2022b). This is about 10% of the total European underground gas storage capacity, which totals about 120 bcm (GlobalData Energy 2021).

According to media reports, Gazprom filled its own European underground gas storage ahead of the 2021–2 winter season at a much slower pace than other European storage owners. In October 2021, The Financial Times reported that while European storage levels were low, an analysis of European gas industry data showed that the largest shortfalls were at sites owned or controlled by Gazprom, in what critics said increasingly pointed to an attempt to squeeze European energy supplies. ‘The big deficits are where Gazprom facilities are,’ said Domenicantonio Di Giorgio, adjunct professor of finance at the Università Cattolica del Sacro Cuore in Milan, who has analysed data from Gas Infrastructure Europe, an industry body (Sheppard et al. 2021). ‘Data from [Gas Infrastructure Europe] show that in countries where Gazprom does not own storage facilities, such as in France and Italy, the level of gas in storage has reached near-normal levels for this time of year’ (Sheppard et al. 2021).

Given the above-mentioned EU undersupply figures for 2021, it is quite clear that the shortfall of 21 bcm in European underground gas stocks at the end of December 2021, as mentioned by Alexey Miller (President of Russia 2021), can predominantly be attributed to Gazprom’s actions—both to the reduction of gas supplies to the EU in 2021, and to the deliberate policy of not injecting gas into Gazprom-owned storage facilities in Europe ahead of the 2021–2 winter season. It should be noted that Gazprom’s policy of emptying its own gas stores in Europe in 2021

cannot be considered normal commercial behaviour for underground gas storage companies, since normally they would be inclined to increase the amount of gas injected ahead of a potentially cold winter season in order to maximise profit; and

contradicts Gazprom’s own policy, illustrated by the record-breaking increase in the injection of gas into Russian storage facilities by nearly a quarter in 2021.

Did European companies actually ask Gazprom for extra supply volumes?

When accused of European gas market manipulation, Gazprom usually replies with the statement that it has satisfied the firm’s contractual supply obligations and has not received any additional gas supply requests from European consumers (TASS 2021b). This brings us to the issue of the non-transparent contractual relations between Gazprom and its main European counterparts—who see ‘exclusive’ relations with Gazprom and secured volumes of gas supply through long-term contracts as a major competitive advantage, and often prefer not to speak out against Gazprom in public.

When the international media asked Gazprom’s European counterparts whether they had sent requests to Gazprom asking for increased fuel supplies, most of them refused to provide a straightforward answer: ‘when asked by Reuters, European energy firms Wingas and Engie said they had not asked for extra gas, while Eni, Uniper, OMV and RWE did not elaborate apart from saying Gazprom had met contracted commitments’ (Golubkova and Soldatkin 2021).

This situation stresses the need to further investigate the contractual relations between Gazprom and its major European counterparts operating under long-term contracts. In the situation of a sizeable gas deficit in Europe leading to record-breaking price spikes, European gas companies should provide clear answers as to whether they actually demanded extra gas supplies from Gazprom, and if they did, what the response was. A European anti-trust investigation of alleged gas market manipulation by Gazprom could provide clear answers to these questions.

Conclusion

As can be seen from the figures provided above, in 2021 Gazprom significantly reduced the actual volumes of gas supplied to the EU against the backdrop of a significant increase in demand and shortfalls in European underground stored gas stocks.

Gazprom does possess significant excess upstream gas production capacity and has injected record-breaking volumes of gas into its own storage facilities in Russia, meaning that it had the ability to supply much bigger volumes of gas to the European market in 2021. But, despite this, it withheld gas from the European market.

Unlike other European underground gas storage operators, Gazprom—which owns about 10% of the European underground gas storage capacity—did not take sufficient measures to fill its stores with gas reserves ahead of the 2021–2 winter season. Much of the current shortfall in European underground gas stocks can be attributed to empty Gazprom-owned stores. The size of the shortfall is comparable to Gazprom’s undersupply of the EU in 2021.

Keeping its European gas stores near-empty is not normal commercial behaviour for storage facility operators, and contradicts Gazprom’s own policy, which is illustrated by the record-breaking increase in the injection of gas into Russian storage facilities by nearly a quarter in 2021.

There is a significant lack of transparency in relations between Gazprom and its European gas consumer counterparts, who refuse to publicly comment on whether they requested more gas from Gazprom under their long-term contracts ahead of the supply-tight winter. Moreover, if such requests were made, it is not known how Gazprom responded.

These circumstances and facts are significant enough to demand the launch of a full-scale investigation into Gazprom’s alleged manipulation of the European natural gas market ahead of the 2021–2 winter season by withholding available volumes of gas from the market, and thus forcing gas prices to surge. Withholding the necessary gas volumes from the European market directly violates Article 102 of the Treaty on the Functioning of the European Union: Any abuse by one or more undertakings of a dominant position within the internal market or in a substantial part of it shall be prohibited as incompatible with the internal market in so far as it may affect trade between Member States. Such abuse may, in particular, consist in: . . . (b) limiting production . . . to the prejudice of consumers.

Therefore, the EU should launch an investigation into Gazprom’s anti-competitive behaviour immediately.

Footnotes

Author biography