Abstract

This study examines how insurance salespeople employ a mapping question to promote life insurance as an additional service to their customers. The mapping question serves a double function, asking about the customer’s situation and creating a context in which transaction-related negotiation is projected to occur. Applying conversation analysis to study video-recorded insurance meetings in Finland, we explore how the mapping question is designed according to the customer’s estimated fit with the target group criteria and their assumed level of understanding of life insurance. We also discuss the trajectories of the negotiation after the customer’s response that expresses interest, conveys hesitation, or rejects the offer. It was found that only a customer’s justified blocking response forestalls further life insurance promotion. The study contributes to the research on questions as agenda-driving actions in institutional interaction and to the literature on question-answer sequences in service encounters.

Introduction

Question formulation and question-answer sequences have been a target of relatively much research in conversation analytic studies (e.g., De Ruiter, 2012; Enfield et al., 2010; Steensig and Drew, 2008). Questions have interested researchers as they are considered a fundamental interactional structure, exhibiting established lexical, syntactical, and grammatical forms across languages. In addition to seeking information, questions have been shown to serve many other functions, such as suggesting, criticizing, and challenging (e.g., Hayano, 2012; Steensig and Drew, 2008). In this study, we focus on a specific function of questions in insurance sales meetings in Finland. Drawing on conversation analysis, we study how salespeople, using questioning as their tool, promote life insurance to their customers.

A meta-analysis found that sales-related knowledge, including knowledge of customers, is the most important driver of sales performance (Verbeke et al., 2011). Thus, asking questions to gather information and understand a prospective customer’s needs is a crucial salesperson skill (Johlke, 2006). Although questioning is recognized as an important sales skill and life insurance selling for long has been considered a field where the salesperson is ‘the critical factor determining whether or not a sale was made’ (Davis and Silk, 1972: 61), research on life insurance selling has often deployed surveys or simulations of insurance sales meetings (Arndt et al., 2014; Singh et al., 2018).

By applying conversation analysis, we dig deep into the design and function of salespersons’ questions, as well as customer responses and their impact on the ensuing conversation. Unlike the relatively scant prior conversation analytic research on salespersons’ questioning (see Freed, 2010; Mazeland, 2004), we focus on consultative face-to-face sales interaction, consisting of extended negotiation between the salesperson and the customer. Studying the selling of life insurance as an additional service, we discuss potentially sensitive issues of life and death, as well as the financial security of family members in case the worst happens. We demonstrate that insurance salespeople carefully work their way toward the explicit promotion of life insurance, using questions as their tool. Our study contributes to the field of institutional interaction and research on questions as agenda-driving preliminary actions in salesperson-customer interactions, as well as to the literature on questions and question-answer sequences in interaction (Enfield et al., 2010; Steensig and Drew, 2008) and more specifically in service encounters (Shoemaker and Johlke, 2002; Singh et al., 2018).

Question-answer sequences in institutional interaction

Questions serve important tasks in institutional interaction. Medical doctors use questions to solicit patients’ problems and diagnose their illnesses (Heritage, 2010), and attorneys build a case for an overhearing audience by questioning the witnesses and the plaintiff (Drew, 1992; Drew and de Almeida, 2020). In many cases, the professional participant (e.g., a doctor or an attorney) asks most of the questions, and the layperson answers them. Crucially, questions of the professional participants are interpreted through the agenda of the institutional context, and thus they may be treated as being more than neutral requests for information.

In institutional interaction, an essential aspect of questioning is the course of action that the questioner is implementing with their question (Ehrlich and Freed, 2010; Hayano, 2012). Focusing on sales negotiations, Mazeland (2004) studied the telemarketers’ use of opinion queries (‘how does that sound to you’) in more or less scripted sales calls. It was found that recipients of such queries (i.e., the customers) orient both to a local preference to evaluate a telemarketer’s product (a savings plan) positively, as well as to a course of action or agenda that the opinion query is contributing to, that is, proposing a commercial transaction. Freed (2010) found that in company-initiated telephone sales calls, representatives of a telecommunications company used questions to achieve their institutional goals, such as gathering information on the customer’s current telephone service and building rapport with their customers.

Outside of sales, many institutional settings (e.g., medical and classroom interactions, courtroom sessions, and political interviews; see Clayman, 2012; Ehrlich and Freed, 2010) are based on questions and questioning. Maynard and Heritage (2005) observed that physicians’ questions have multiple implications: they establish agendas for patient response, they embody presuppositions about the patient’s health and the level of understanding of medicine, and they incorporate specific preferences (inviting one type of answer over another). In a similar vein, in the insurance negotiations, the questions asked by the insurance salesperson are not only requests for information but also have a strategic, sales-oriented function that reflects the commercial agenda of the situation.

Data and the overall structure of life insurance negotiation

Our analysis is based on 12 video-recorded, naturally occurring insurance sales meetings in Finland. The data were collected in a research project involving an insurance company (referred to by the pseudonym Kunto Insurance Company). Informed consent was obtained from all the participants, and personal details were removed from the data. The meetings were video recorded using two cameras facing each other diagonally over the negotiation table on the premises of Kunto Insurance Company (henceforth, KIC).

There were four different salespeople (SP1, SP2, SP3, and SP4) involved in our recordings, and each of the meetings had a different customer (in 8 meetings) or two customers (in 4 meetings, for example, a couple, or a mother with her child). The duration of a meeting varied from 34 to 68 minutes. Salespeople were aged between 25 and 40 years, and there were two males and two females. In half of our video-recorded meetings, the customers did not have an existing insurance agreement with KIC but were current customers of a competing insurance company. In most cases, KIC had invited the customer to discuss his or her insurance, but in some cases, the customer had proactively requested a meeting.

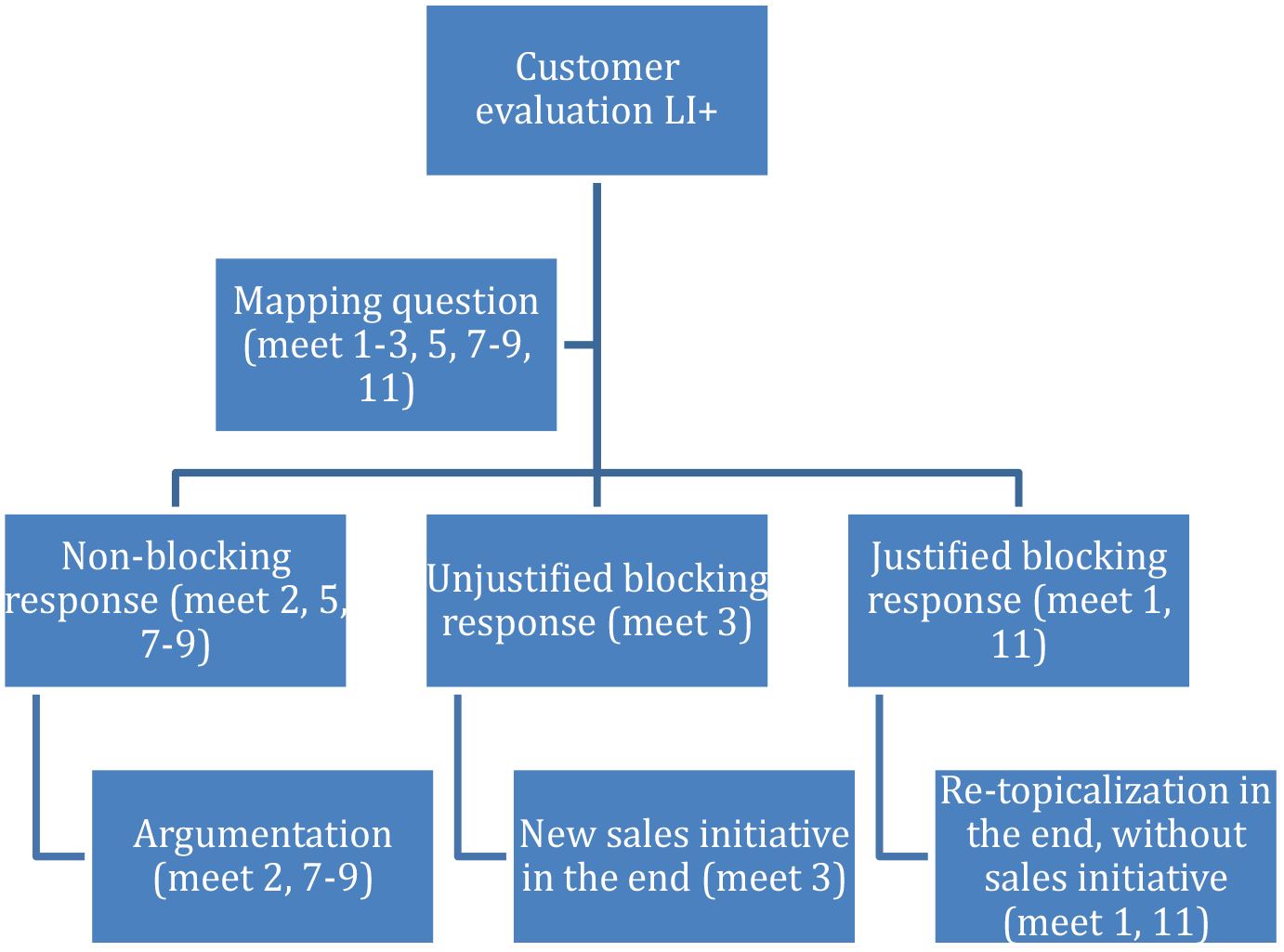

As a product, life insurance is a part of a larger group of personal insurance. Personal insurance includes, for example, designated insurance for permanent loss of ability to work, severe illness, or accidental death. Life insurance, on the other hand, covers death irrespective of reason. Overall, concerning life insurance negotiation, the meetings followed a structure that is presented in Figure 1.

The overall structure of life insurance negotiation.

Based on a salesperson’s evaluation of the customer fit with the target group criteria for life insurance (most importantly, customer’s age and social status), the customer was considered either a suitable target for life insurance promotion (LI+) or not suitable for it (LI−). In the case of a LI+ evaluation, the salesperson presented what we call a mapping question. Typically, it is a verb-initiated polar (yes/no) question, in which the question suffix -kO (or -ks in colloquial language) is attached to the verb (Sorjonen, 2001), such as ootteko vakuuttanu itteenne mitenkään, ‘have you insured yourself in any way.’

The mapping question is designed to determine if the customer currently has life insurance or if they would be interested in one. Thus, we distinguish between type 1 and type 2 mapping questions. Type 1 mapping questions target personal insurance in general (‘have you insured yourself in any way’, type 1a) or specifically life insurance (‘did you have any type of life insurance at the moment’, type 1b), whereas type 2 questions are always about life insurance (‘would you be interested in having a look at life insurance’). As Figure 1 depicts, depending on the customer’s response, each type of mapping question may lead to immediate sales-oriented argumentation, a later new sales initiative, or re-topicalization without explicit sales initiative. Also, the three types of mapping questions give rise to three different mapping question sequences: type 1a followed by type 1b, type 1a followed by type 2, and type 1b followed by type 2.

Next, we demonstrate how a mapping question is designed and presented to a customer, as well as how the negotiation continues after the mapping question and the customer’s response.

The mapping question: A salesperson’s resource for initiating life insurance promotion

Gathering information on the prospective customer’s current financial and social status is a vital task for an insurance sales representative (cf. Shoemaker and Johlke, 2002). To understand the customer’s situation, insurance sales representatives methodically draw on mapping questions, as discussed in the prior section. Out of 12 video-recorded insurance sales meetings, 8 include a mapping question.

In designing a mapping question, the salespeople consider specific factors. First, they consider the prospect’s overall fit (i.e., the prospect’s age and possible information already acquired about the prospect’s financial and social status) with the target group criteria for life insurance. If a particular prospect without a doubt does not need life insurance (e.g., the prospect is old or very young, lives alone, or does not have any loans), there is no mapping question at all. Second, the salespeople consider the prospect’s assumed level of understanding of life insurance, as it is a complicated service and may be mixed up with other personal insurance.

Our first example demonstrates how the evaluation of the prospect’s fit with the target group criteria may affect the real-time production of the mapping question. Here, the salesperson’s evaluation of the prospect’s fit with the criteria changes from positive (suitable for life insurance promotion, LI+) to negative (unsuitable, LI−). In this case, the prospect, an approximately 25-year-old single man, is a customer of another insurance company. Therefore, the salesperson can’t see the customer’s current insurance on her laptop, and she relies on a type 1 mapping question to find out if the prospect currently has life insurance. However, we see that during the production of the mapping question, she concludes that the prospect might not be interested in life insurance due to his overall social and financial status (see Appendix 1 for transcription symbols).

Example 1. The real-time design of a mapping question. (Meet 5, 04:37–04:56/33:19 min)

The salesperson initiates a type 1 mapping question (‘do you have’, line 1) but abandons it in favor of asking for additional information first. After the prospect informs the salesperson about his housing situation (a rented apartment), the salesperson reinitiates her mapping question (‘so do you have’, line 5). Nevertheless, she still does not complete this information-seeking type 1 mapping question (e.g., ‘life insurance currently’), most likely due to the overall evaluation of the prospect (young age, no family) and the just-received information on his housing situation, which does not imply any loans. Instead, we see that the salesperson repairs her interrogative (‘do you have’) into a declarative utterance (‘at the moment you probably don’t have life insurance’, lines 5–6), by which she seeks confirmation of her newly formed understanding that the prospect currently might not have life insurance. This implies a change of evaluation: at first, the customer was considered suitable for life insurance promotion, but additional consideration and a question-answer sequence (lines 1–3) deemed him unsuitable. Indeed, life insurance is no longer promoted to the prospect in this meeting.

The salesperson in her declarative utterance that seeks confirmation (lines 5–6) mentions life insurance as a service. The participants have earlier discussed the prospect’s existing personal insurance that covers physical accidents, and in his response, the prospect displays an understanding that life insurance would be included in that as well. However, this is likely incorrect, as life insurance differs from personal accident insurance in many important ways, as the salesperson explains (lines 10–13). Therefore, in Example 1, we see how the prospective customer’s understanding of life insurance can be an issue that salespeople need to consider and be ready to educate their customers.

In our second example, we demonstrate how salespeople can manage uncertainty about a prospect’s level of understanding of life insurance as a service. In Example 2, the prospect (similar to Example 1) is a customer of another insurance company. This approximately 30-year-old woman is accompanied by her son (approximately 7 years old) in the insurance sales meeting. Just before the beginning of Example 2, the salesperson has re-stated that the prospect currently has personal insurance that provides for medical expense compensation, and the prospect confirmed it.

The salesperson, considering the prospect as a suitable person to be presented with life insurance begins to move towards it. Here, we are interested in the careful way the salesperson presents the life insurance service as a topic and how the conversation then proceeds.

In formulating his mapping question, the salesperson on the one hand approaches the potentially sensitive topic casually, and on the other, carefully avoids presupposing any specific knowledge from the prospect on life insurance. That is, he designs his type 1 mapping question in a way that presents the life insurance service as a potentially new topic, drawing on the indefinite proadjective tämmöstä, ‘this kind of’, and henkivakuutustyyppistä ratkasua, ‘life insurance type of a solution’, both oriented to presenting a new referent as a member of an indefinite group of insurance solutions (Hakulinen et al., 2004; VISK § 1411). This can be contrasted with how the salesperson in Example 1 presented life insurance, simply mentioning the product and as such presupposing there will be no problems for the prospect to comprehend the referent. In Example 2, however, the salesperson seems to be oriented to the possibility that the prospect is not knowledgeable about the details of life insurance. This interpretation is supported in the salesperson’s next turn (lines 5 and 7), in which he gives basic information on life insurance and implies a difference between life insurance and other personal insurance.

The prospect, after displaying at least a rough understanding of life insurance, denies having such insurance (line 9). Importantly, the salesperson then proceeds to a type 2 mapping question, ‘have you then thought about it?’ (line 12), in which ‘then’ marks this new question as a follow-up to the prior question-answer sequence. With slight amusement in her voice, the prospect denies having thought about a life insurance service (lines 13–14) but gives an explicit go-ahead response (line 16). With her go-ahead response, she displays her understanding that the salesperson was steering the discussion toward a sales-oriented promotion of life insurance.

In this section, we have discussed the design of the mapping question, an important resource for sales representatives in introducing to a prospect the life insurance service and preparing for a more elaborate sales-oriented discussion at a later stage. In the next section, we discuss in more detail what happens after a mapping question. We are interested in how a prospect’s response to a mapping question guides the salesperson’s behavior and what resources the insurance sales representatives have at their disposal when trying to sell life insurance as an additional service.

From the mapping question to the negotiation

In this section, we show how different types of trajectories of selling life insurance are organized after SP’s mapping question. In our analysis, we focus on the customer’s response to a mapping question, which (a) provides the salesperson with additional information on the prospect’s orientation concerning buying life insurance and (b) drives the sequential construction of the next phases of the sales negotiation. As demonstrated earlier in Figure 1, we have identified three types of customer responses to a mapping question:

(1) A non-blocking (a go-ahead or neutral) response that leads to an SP’s immediate sales initiative via argumentative turns

(2) An unjustified blocking response that guides the salesperson to abandon the immediate sales initiative and make a new initiative later via another mapping question

(3) A justified blocking response that leads to stagnation of the sales initiative

Next, we will analyze in detail three cases (Examples 3a–b, 4a–b, and 5) that illustrate the organization of life insurance sales negotiation through a mapping question, its three different response types, and their follow-ups.

The first case (Examples 3a and 3b) originates from a negotiation where a married couple was invited to negotiate a possible insurance solution with KIC. The customers have their current insurance papers from a competing company on the table, and the participants are going through their contents. It is evident that the customers currently don’t have insurance that is specifically labeled as life insurance. Referring to personal insurance that the customers do have, the salesperson produces a type 1 mapping question (‘is this like a kind of life insurance then?’, Example 3a, line 2). Example 3a illustrates a non-blocking response to this mapping question: the customer provides his somewhat uncertain response to the salesperson’s question but leaves open whether he is interested in life insurance.

Example 3a. A non-blocking response (Meet 9, 8.53–09:11/61:36 min)

Through his non-blocking response, the customer denies the salesperson’s assumption (‘no but’, line 4). However, he does not explicitly block the sales-oriented function of the mapping question. Instead, the customer positions himself as uncertain about his current insurance (‘as I have understood it’, line 4). This gives the salesperson the possibility to go straight into life insurance promotion. After the salesperson has received the customer’s explanation (‘okay’, line 12), and the customer has read aloud an excerpt from his insurance papers, the salesperson begins to build an argument for life insurance by asking if the customers have a loan for their home (lines 44–45). The customers acknowledge the loan (lines 46–47), but as C1 still returns to his current insurance (line 48), the salesperson gives up the immediate life insurance promotion. Instead, the participants begin to discuss customers’ other insurance.

Roughly 15 minutes later, demonstrating his continuous interest in selling life insurance, the salesperson returns to argue for it (‘as you have a new home and a little child this kind of life insurance is very important to have’; data not shown), but customers are reserved. Finally, SP pursues an explicit attempt to include life insurance in the customers’ overall insurance package, using multiple argumentative turns in favor of it. Just before Example 3b, C2 mentioned her employer-provided insurance that potentially covers her accidents and illnesses. SP responded that he does not know about those (as it is a service offered by another company), and proceeded to recommend life insurance, as the following example illustrates.

Example 3b. Persuasion and decision-making after a non-blocking response. (Meet 9, 43.04–43.22/61:36 min)

In Example 3b, the salesperson suggests a minimum sum for life insurance (line 4), including a list of reasons originating from the customer’s situation (‘the house, the little one, each other’, lines 2–3) as well as highlighted expressions (‘absolutely’, line 1) to strengthen his point. When constructing a proposal for customers, he uses the verb ‘recommend’ (line 1), which occurs frequently in our data (30 occasions). It is often deployed when the customer should decide whether to consider specific insurance, and it conveys an attempt to direct the course of the customer’s actions. Typically, salespeople use the verb ‘recommend’ in situations where they echo the voice of the institution, for example, giving company-instructed recommendations on insurance coverage amounts.

The customer quickly acknowledges the proposal (line 5) and uses a common customer strategy in our data: he delays the decision-making to a later date. The customer suggests as a practical decision that the proposal would be included in the offer so that they could ‘think about it’ further (lines 14, 17). However, the request to include life insurance ‘as a separate point’ (line 13) implies that the customer likely does not intend to include life insurance in their insurance package, that is, a separate point is easy to exclude from the overall insurance package. After that, the other customer seems to align herself with her husband, explaining with a smile in her voice that she has always been an ‘anti-insurance’ person (not shown in the transcript), implying a general disinterest in buying insurance and thus resistance to life insurance.

In the previous case (Examples 3a and 3b), the salesperson was able to build a concrete life insurance offer after the customers’ non-blocking response to a mapping question. Next, we will analyze a case in which the customer seemingly blocks the salesperson’s initiative but does that in a way that leaves doors open for later salesperson initiatives. That is, the customer’s unjustified blocking response to a mapping question conveys her disinterest in buying life insurance but does not account for it with explicated facts (Example 4a). We will show how this response at first guides the salesperson to abandon his sales initiative, but later, towards the end of the meeting, she returns to it and makes a new life insurance initiative in the form of another mapping question (Example 4b).

The customer is a pregnant woman and a KIC customer, and she has arrived to negotiate short-term travel insurance for herself and health insurance for the unborn baby. At the beginning of Example 4a, the salesperson acts in a way that is common in our data: she first reviews the customer’s current insurance and refers to a lack of personal accident insurance (line 1; she can see the customer information, including the husband, on her laptop). Then, the salesperson extends her turn to cover personal insurance overall (‘have you insured yourselves in any way’, lines 3–4), thus posing a negatively polarized (‘in any way’, Heritage and Raymond, 2021) type 1 mapping question by which she evokes the customer’s sense of responsibility for her family. In our data, salespeople commonly promote life insurance as a part of a larger set of personal insurance. In Example 4a, the salesperson at first asks specifically about accident insurance (‘have you thought about those’, line 3), but then she opens her question to cover all types of personal insurance (‘or have you insured yourselves in any way’, lines 3–4).

Example 4a. An unjustified blocking response. (Meet 3, 6.21–6:40 / 35:45 min)

The negative formulations (‘you didn’t even have any kind of’, line 1, and ‘in any way’, line 5) imply a critical attitude to leaving the family completely without support, thus evoking the customer’s sense of responsibility. The customer’s unjustified blocking response has two parts. First, she denies having personal insurance (line 7). Then, demonstrating her understanding that the salesperson was moving toward proposing and orienting to a preference for the status quo, she reports a general disinterest in acquiring it (‘we don’t really feel that there would be a need for that’, line 9). However, her blocking response is not clearly justified but is ultimately based on an unspecified, albeit allegedly shared experience instead of explicated facts (e.g., they have other resources available in case of an accident, unemployment, or even death in the family). Thus, the customer’s response leaves the salesperson with an opportunity to return to the issue later.

After this, life insurance as a topic is brought up when the salesperson is about to print the insurance offer for inspection, as Example 4b illustrates. The salesperson presents another type 1 mapping question, this time about life insurance, although she has already been informed that the customers do not have any personal insurance. Thus, it is evident that she is first and foremost making a sales initiative rather than requesting information. Furthermore, in Example 4b, we see an effect of company-provided instructions: the salesperson pursues the promotion even though the customer-specific information does not support it.

Example 4b. A sales initiative in the end, after an unjustified blocking response. (Meet 3, 13:33–14:34 / 35:45 min)

Again, the question is negatively tilted (‘any type of life insurance’, lines 5–6), displaying the salesperson’s understanding that the customers are unlikely to have life insurance but also re-evoking the customer’s sense of responsibility to her family. It is marked with a misplacement marker (muuten, ‘by the way’, line 5; Schegloff and Sacks, 1973), which, on the one hand, indicates the question’s unexpected, out-of-the-place sequential position in the conversation and, on the other hand, frames it as a sideline to the current main line of the conversation. The salesperson thus takes the last opportunity in the negotiation (just before printing the insurance offer) to make a sales initiative on life insurance. After all, the customer’s first blocking reaction to personal insurance was based on intuition and not justified by hard facts. After the customer’s negative response, the salesperson continues with two detailed questions about the customer’s situation (lines 8, 12), both oriented toward creating grounds for selling life insurance.

The customer’s responses (no loan at all, right-of-residence housing) do not support or give additional resources for the salesperson in promoting life insurance. However, not giving up on the course of action that she initiated by her mapping question, the salesperson continues to promote life insurance. Also in this case, the salesperson uses the verb ‘recommend’ (see Example 2b), contributing to a line of argumentation that eventually makes relevant the customer’s decision. Here, the verb is in the passive voice (‘life insurance is something that is recommended’, line 15; cf. institutional ‘we’, Drew and Heritage, 1992), providing the salesperson an additional resource in speaking with the voice of the institution – it is not only the salesperson who recommends but also the institution behind her and all the experience it has serving customers.

The salesperson’s further argumentation relies on customer-specific details: underlining the family issues in the customer’s current life situation (line 16). The salesperson then visualizes a potential threat (‘so if something happens to either of you’, line 17) to demonstrate the need for the protection provided by life insurance and immediately, during the same turn, continues to a proposal (‘so would you like to have a look at that kind of thing here?’, lines 19–20). As in the previous Example 3b, the customer in her declination-implicative response (‘well not really’, line 22) delays the ultimate decision-making. However, different from Example 3b, the customer is now in a better position to delay the decision by being able to claim that the issue needs to be first discussed at home with the spouse, who is not present at the current meeting.

We have discussed two cases that demonstrate how the trajectory of life insurance sales negotiation develops from a mapping question and after a customer’s response. Both a customer’s non-blocking response (Example 3a) and an unjustified blocking response (Example 4a) led to a salesperson’s sales-oriented initiative and multiple argumentative turns in favor of life insurance. In case of the unjustified blocking response, the salesperson delayed the discussion on life insurance to the very end of the negotiation, which we interpret as reflecting (a) the customer’s unconvincing yet blocking response to the mapping question and (b) the company-provided education and an eventual behavioral schema of the salesperson in the insurance negotiation.

Finally, we have cases in our data where a customer produces a justified blocking response that stagnates the sales initiative. A justified blocking response offers accounts that eliminate common arguments for selling life insurance. In our final example, the participants have discussed the customer’s situation in detail. As they approach the end of their meeting, the salesperson initiates life insurance negotiation by producing a type 2 mapping question.

Example 5. A justified blocking response. (Meet 1, 47:59–48:30 / 51:36 min)

In her response, the customer refers rather formally to ‘a discussion’ that she has recently had with her husband (lines 3–5), resulting in a shared conclusion that they don’t need life insurance (line 7). Demonstrating her understanding of life insurance, she argues for this by eliminating a central argument for life insurance (‘the loans have been paid’) and by implying further preparations (‘and so forth’, line 12). The salesperson then asks if the customers also (‘yes and’, line 15) have some additional financial resources (‘nest egg’, line 16). As the customer confirms this and describes an executable plan for challenging times (lines 17, 19), the salesperson volunteers a conclusion that the customer’s situation is ‘good’ (line 21), implying life insurance is unnecessary in this case.

Example 5 demonstrates that a justified blocking response necessitates the customer to provide proof of knowledge about life insurance as well as evidence of preparation for unexpected situations. A justified blocking response is thus fitted to the institutional context, providing an account that is easy for a salesperson to accept. 1 This brief excerpt initiated and concluded the life insurance promotion, as the salesperson next moves to promote asset management services. However, about a minute later, wrapping up the meeting, he re-topicalizes life insurance without explicitly promoting it (‘we talked about life insurance and it is okay and you have planned it so that is the most important thing’; data not shown). Thus, the salesperson effectively asks the customer to confirm their decision, and the customer complies (‘yes’; data not shown).

Discussion

We have discussed the salesperson’s use of a mapping question as a resource in initiating the promotion of life insurance as an additional service. The overall trajectories of life insurance negotiations (Figure 1) highlight that salespeople do not rush into making a transaction proposal but first map the customer’s situation, interest, and level of understanding about life insurance. It was also found to be a common salesperson practice to review and explicate the customer’s current insurance and draw on resources offered by the customer’s situation before discussing life insurance. Overall, it was important for the salespeople to carefully work towards life insurance, as it was never the customer’s reason to visit the insurance company’s office.

We found that a mapping question is a double-barreled question – it requests information that the salesperson can use to their advantage but, above all, makes relevant a sales-oriented negotiation. Thus, different from an opinion query that follows service promotion (Mazeland, 2004), a mapping question precedes service promotion, arguably reflecting the difference between scripted sales calls and consultative insurance selling. However, also in our data, customers are aware of the sales-oriented agenda of the mapping questions (e.g., ‘have you insured yourselves in any way?’), and in their responses, they often tried to forestall the implied sales initiative, first responding to the request for information (e.g., ‘no we haven’t’) and then blocking a sales initiative (‘we don’t really feel that there would be a need for that’, Example 4a). This order of actions aligns with a generalization by Schegloff (2007: 75–76) on responding to a double-barreled first action: address the format or vehicle first and then the action implemented through it.

As a main point, we found that a salesperson’s mapping question serves above all an agenda-related function: they are deployed to lure the conversation into a sales-related direction. Both after a customer’s non-blocking response and an unjustified blocking response, the salesperson continued their institutional agenda of selling life insurance. Only a customer’s justified blocking response, fitted to the institutional context of life insurance negotiation, was enough to forestall explicit sales initiatives. However, when concluding the meeting, the salesperson still checked if the customer was sure about their decision by re-topicalizing life insurance. Arguably, the salesperson’s persistent behavior in promoting life insurance reflects the organization’s guidelines for the salespeople, derived from the strategic importance of life insurance service for KIC.

Overall, this study develops our understanding of the importance and specific function of salespersons’ questions as agenda-driving preliminary actions. We demonstrated that if the customer fits the target group criteria for life insurance, a salesperson uses questioning as a tool to initiate the service promotion. We distinguished between type 1 and type 2 mapping questions and observed the pivotal role of a mapping question for the further development of life insurance negotiation. To conclude, this study sheds light on questioning as a core structure of institutional interaction. It provides insights into the role that questions and their responses play in shaping the overall trajectory of negotiation in an institutional setting and the strategic function these actions serve for the participants.

Footnotes

Appendix 1: Transcription conventions

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by Business Finland under Grant 3571/31/2015.