Abstract

Historically, companies have communicated taxes as a burden, as the benefits provided by governments are not perceived to be in proportion to their payments. With sustainable development becoming central in many policy areas, new discourses including ‘fair’ or ‘sustainable’ tax have become omnipresent in public talk on taxes. This paper analyzes tax discourses in corporate annual reports within this changing context to examine the use of language in the construction of the meaning of tax. By analyzing tax reporting by a state-owned multinational company over two decades, we observe that the communication of taxes increased in both number and types of discourses. Importantly, this highlights the shift in tax discourses from one dominated by codified accounting discourse reinforcing the monolithic representation of tax as an unfair expense, to one where tax is given a multidimensional meaning within a broader discursive context, where tax is a meaningful corporate responsibility to society.

Keywords

Introduction

The idea of tax can be traced to ancient times when the growth of society, public needs and the beginning of administration led to voluntary offerings (donum, e.g. labor, property) by an individual to the leader. Seligman (1925) identified distinct stages of this etymological development where common funds were raised to finance leaders’ internal endeavors and war efforts. These include leaders imploring the people for support (precarium), or individuals providing assistance to the state (adjutorium) for the public good. With the advancement of civilization, the volition of the ‘taxpayer’ diminished with the idea of compulsion by the state, when these contributions became veritable impositions – a burden on the individual.

The word ‘tax’ (verb) originated from the Latin word taxare, to ‘evaluate, estimate, assess, handle’, also ‘censure and charge’. Tax (noun) is also understood as ‘obligatory contribution levied by a sovereign or government’ (On-line Etymology Dictionary, n.d.). In contemporary society, tax is generally understood as a compulsory, unrequited payment to the government (OECD, n.d.). Despite its importance as a source of public finance and its pivotal role as a policy instrument, tax is regarded as a burden, as the benefits provided by government are not normally perceived by taxpayers as being in proportion to their payments. In the field of corporate reporting, tax has traditionally been ‘talked about’ as an ‘unfair’ expense. For that reason, a significant number of companies have engaged in aggressive tax planning strategies to exploit gaps in the architecture of the international tax system in order to enhance shareholder value (Dover et al., 2015).

New perspectives on taxes emerged during the aftermath of the 2007 global financial crisis and the tax leaks, when various initiatives were instituted to enhance tax transparency and accountability by companies in order to counter tax avoidance. These initiatives include the Base Erosion and Profit Shifting (BEPS) initiative by the OECD and the Anti-Tax Avoidance Directive by the European Union (EU). In addition, there were a myriad of initiatives from non-state actors that emerged to foster more responsible tax behavior. These efforts gained greater momentum with sustainable development becoming a central organizing principle in both the public and private sectors. Today, terms such as ‘sustainable tax’ and ‘fair tax’ have become omnipresent in public discourses. Increasingly, it can be observed that these discourses have surfaced in the annual and sustainability reports of companies (De la Cuesta-González and Pardo, 2019).

Within this context, the aim of the paper is to enhance our understanding of the way language in corporate reporting plays a constitutive role in establishing and altering the tax concept. Accordingly, this study examines the use of language in the construction of the meaning of tax by analyzing the changing tax discourses in the corporate reports of one of the leading state-owned multinational companies in Sweden over the last two decades.

The paper contributes to discourse, tax, and accounting literature. First, through a longitudinal interpretive textual analysis, we identify important shifts in tax discourses from one dominated by codified accounting discourse, reinforcing the monolithic representation of tax as a burden, to one where tax is given a multidimensional meaning within a broader discursive context. We theorize how language use over time has performative effects on the meaning of tax. Second, the findings reveal how the word tax has been recontextualized in different corporate reporting discourses and has merged intertextually with sustainability discourses as the company enters a different realm of tax management. As such, we observe the coexistence between dominant and emerging discourses on tax within the corporate reporting genre.

External corporate reporting and language

The corporate annual report serves the purpose of communicating the performance of a company to its stakeholders. Whilst traditionally focused on financial performance, the scope has been extended in recent years to include other areas of performance, such as risk management and sustainability. The annual report is also a principal mechanism whereby companies position themselves and define the space within which the dialog with stakeholders takes place (Tregidga and Milne, 2006). What is communicated therefore goes beyond value-free information transfer and forms part of the discursive practice imbued with intention, working in ways to structure people’s perception of social reality (Khalifa and Mahama, 2017).

Discourse can be broadly defined as language in use which achieves meaning and coherence for those involved. In this paper, we analyze discourses, that is, texts (content, vocabulary, and message) on taxation in annual reports. The process of the discourse analysis begins with text – the overt linguistic trace of a discourse process. Certain discursive practices are codified, for instance, into standards that guide corporate reporting, thereby relating certain discourses to specific genres which essentially influence the linguistic form, structure, or style associated with specific communicative purposes, within a particular professional setting, social or institutional contexts (Fairclough, 2013). The corporate reporting ‘genre colony’ consists of different reports including financial, governance, as well as sustainability reports (Rajandran, 2018). Hence, within the genre of corporate reporting, one or several different discourses can exist or coexist (Bhatia, 2010).

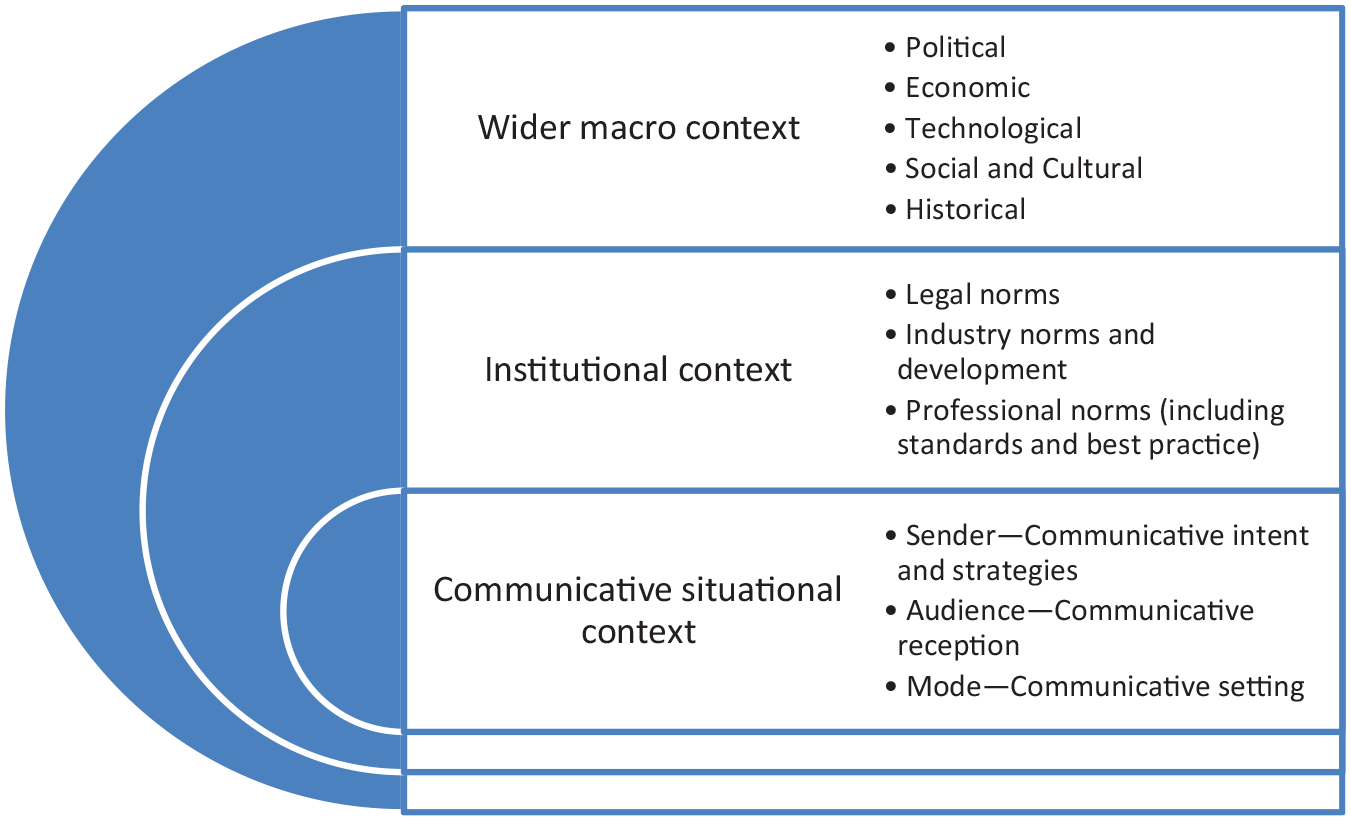

According to Kress (1995: 122), ‘Texts are the sites of the emergence of complexes of social meanings, produced in the particular history of the situation of production, that record in partial ways the histories of both the participants in the production of the text and of the institutions that are “invoked” or brought to play’. This perspective emphasizes the contexts within which different discourses emerge and need to be understood (Fairclough, 2013; Goodwin and Duranti, 1992; Hyland, 1996; Sandell, 2021). The context, in the words of Goodwin and Duranti (1992: 3), is ‘a frame that surrounds the event being examined and provides resources for its appropriate interpretation’. The context within which tax reporting take place, as illustrated in Figure 1, may be analyzed at different levels of social organization: the communicative situational context, the institutional context, and the wider macro contexts (Fairclough, 2013; Goodwin and Duranti, 1992; Wodak, 2011).

The context framing tax discourses and the concept of tax.

The communicative situational context includes the communicative setting, the participants, their identity, and goals that are relevant for the production and/or reception of the text. This draws attention to the actors’ use of the language. In this paper, we focus on the voices of those authoring the story of company taxation, and the communicative assimilation by the audience, the text being a trace of an ongoing dialog between the company representatives and its stakeholders (Brennan et al., 2013; Sandell and Svensson, 2016). The institutional context refers to the legal, industry, and professional norms at the meso level which have influence on a company’s tax reporting. The wider macro setting refers to the historical, economic, technological, political, social, and cultural forces shaping the larger environment within which the company operates. These contextual forces are dynamic and interplay within and between the various levels over time.

To analyze how tax discourses change over time, we pay attention to the concepts of emergence and recontextualization manifested in the intertextuality and interdiscursivity of texts (Wodak, 2011; Zappettini and Unerman, 2016). Texts are made meaningful through their interplay with other texts, the different discourses on which they draw, and the nature of their production, dissemination, and consumption. Hence, discourses are considered fluid as issues, meanings, and discursive practices can be reformulated by recontextualizing discourses to reflect the wider elements of practices in the professional domain. New discourses emerge in connection with the changing context in which a company operates. This entails reviewing relations between existing discourses and active appropriation or internalization of external discourses (Fairclough, 2013). In the process, text or meaning is recontextualized, that is, extracted from its original context and reused in another, implying a change of meaning and redefinition.

Intertextuality as a text-level phenomenon describes how a text refers to other, prior texts. A text can incorporate words or meaning from other texts through direct or indirect quotes or just alluding to what hearers or readers understand are words taken from other sources. It draws attention to the dependence of text upon society and history (Fairclough, 2013). Discourses are connected to other discourses which were produced earlier as well as those which are produced synchronically and subsequently (Fairclough and Wodak, 1997). Interdiscursivity, on the other hand, is understood as an appropriation of generic resources, primarily contextual in nature, focusing on specific relationships between and across discursive practices (Bhatia, 2010). An analysis of interdiscursivity requires combining linguistic analysis of a text with the analysis of social events and practices.

The notions of intertextuality and interdiscursivity provide an analytical framework to analyze changes in tax discourses in corporate reporting over time and space. Drawing on the above discussion, we map the contextual influences on tax reporting during the period studied and conduct an intertextual and interdiscursive analysis to analyze the changing tax discourses in corporate reporting over time.

Research design and material

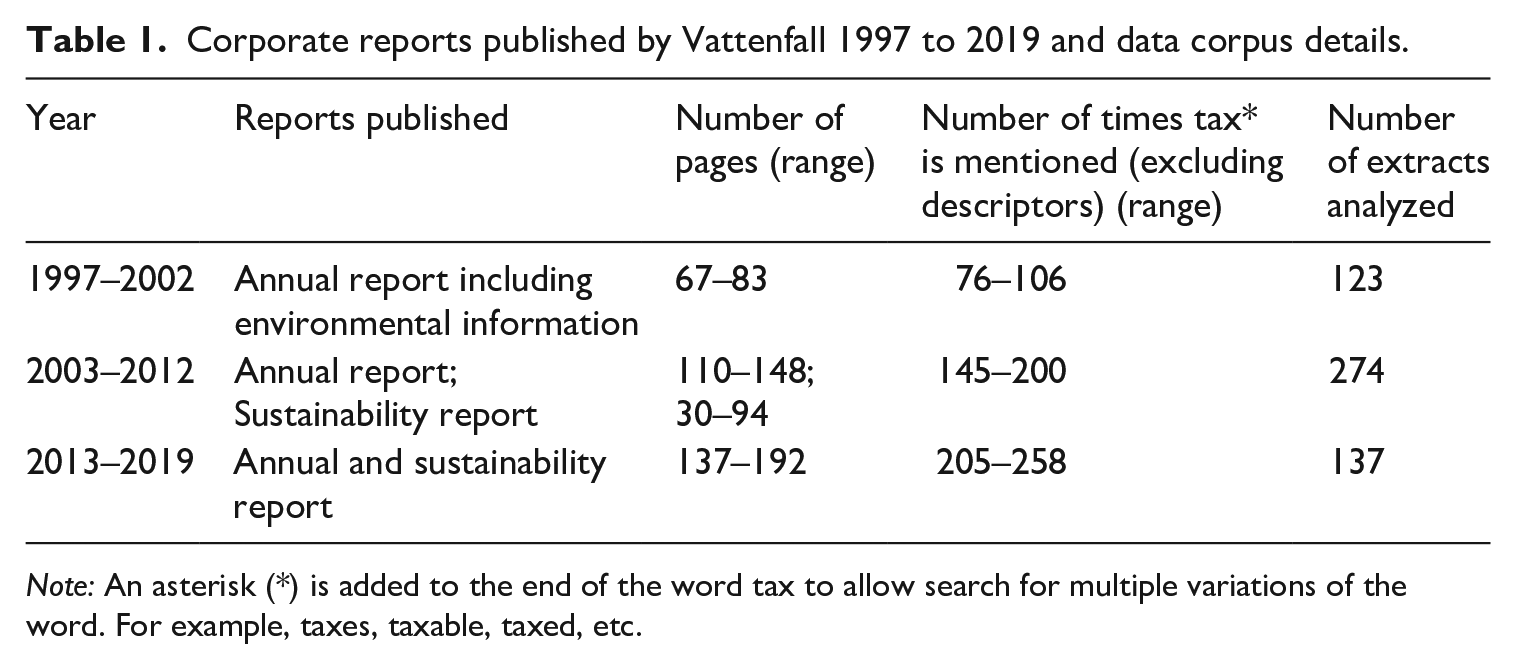

This study examines the tax discourses of a single company, which allows an in-depth analysis and interpretation of how tax discourses have developed over time. Here, the tax reporting, from 1997 to 2019, of Vattenfall, a Swedish state-owned multinational company, is analyzed. Vattenfall is one of Europe’s largest producers and retailers of electricity and heat, with main markets located in Sweden, Germany, the Netherlands, Denmark, and the United Kingdom. The net sales of Vattenfall accounts to approximately 40% of the net sales of all Swedish state-owned enterprises (Swedish Ministry of Enterprise and Innovation, 2019). The Swedish state requires state-owned companies to be actively and professionally managed, balancing and integrating economic and sustainable development as an overriding objective. Hence, Vattenfall pays taxes and competes on fair terms with private companies (Swedish Ministry of Enterprise and Innovation, 2017). Vattenfall was chosen, firstly, because it is a leading actor in public tax reporting and as a state-owned company it has the obligation to act in a manner that generates public confidence. Secondly, Vattenfall has disclosed information pertaining to taxes and tax management in several different corporate reports, thereby providing an opportunity to analyze the textual and discursive relationships that can be found within and across corporate reports over time.

The data corpus has been collected from corporate reports which include, annual reports, sustainability reports, and more recently, the integrated annual and sustainability reports (see Table 1). The focus of our analysis is not on details as to the content in each report; rather, through textual analysis of tax disclosures we trace the meaning of tax and how it has changed.

Corporate reports published by Vattenfall 1997 to 2019 and data corpus details.

Note: An asterisk (*) is added to the end of the word tax to allow search for multiple variations of the word. For example, taxes, taxable, taxed, etc.

The authors engaged in a first reading of the reports separately, followed by a discussion to gain a shared understanding of the context within which Vattenfall operates, and to identify the significant shifts in tax discourses linking text with context. The context has been defined through the mapping of changes in tax regulation and the emergence of professional norms via legal and other sources. The key contextual influences on tax reporting during the period studied are summarized in Appendix 1. Next, the authors separately performed a search for the root word tax with the truncation symbol (*) in each of the reports, from which relevant extracts were identified and mapped chronologically.

A close reading of the extracts was then performed, looking for themes and patterns. Through intertextual and interdiscursive analysis, the authors distinguished the different discourses on taxation by critically examining: the content of the text, language features (semantic relations: the way sentences are related: causal, conditional, temporal (when), additive, elaboration, contrastive), the voice of the company, and presumed audience of the extracts, to identify the nature and characteristics of the various discourses, as well as to draw out how tax has been conceptualized over time. The categorizations were guided by empiricism and context (Charmaz, 2006), whereby attention was given to how tax discourses have been articulated and the interplay with other discourses depicting the company’s relationship with society. The interpretation of the texts, voices that appear, and the intended audience are the researchers’ interpretation. It is the properties of the text, the text being a communicative vessel containing elements of discourses and social practices, which is subjected to discursive interpretation (Gallhofer et al., 2007; Myers, 1989).

The tax discourses of corporate reports

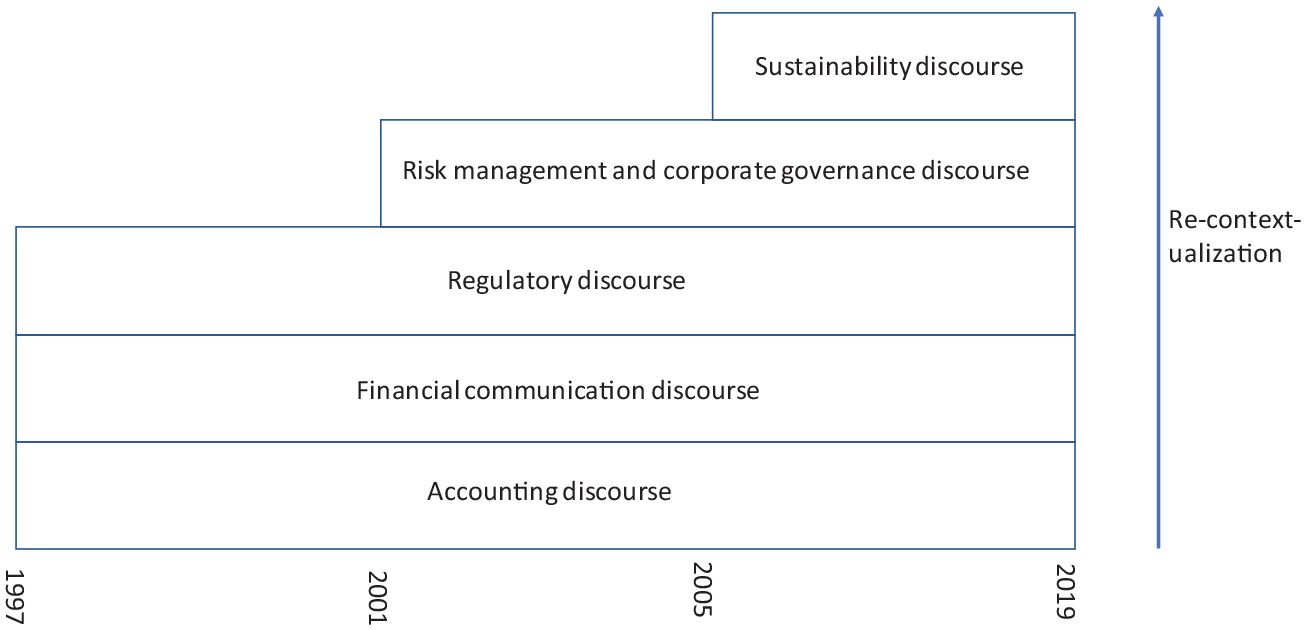

From the data corpus, we identified five tax discourses that emerged in the 22-year period studied (see Figure 2). From 1997 to 2000, we identified three types of discourses in the reports: the accounting, financial communication, and the regulatory discourses, all of which relate to tax as a burden. From 2001, the risk management and corporate governance discourse emerged. While taxes continued to be portrayed as a burden, it became something that entered the realm of management as manageable. From 2005, a fifth type of discourse surfaced, the sustainability discourse, adding another layer of meaning to the word tax. Taxes are not only portrayed as something negative, but as a meaningful corporate responsibility to society.

Identified discourses in tax reporting between 1997 and 2019.

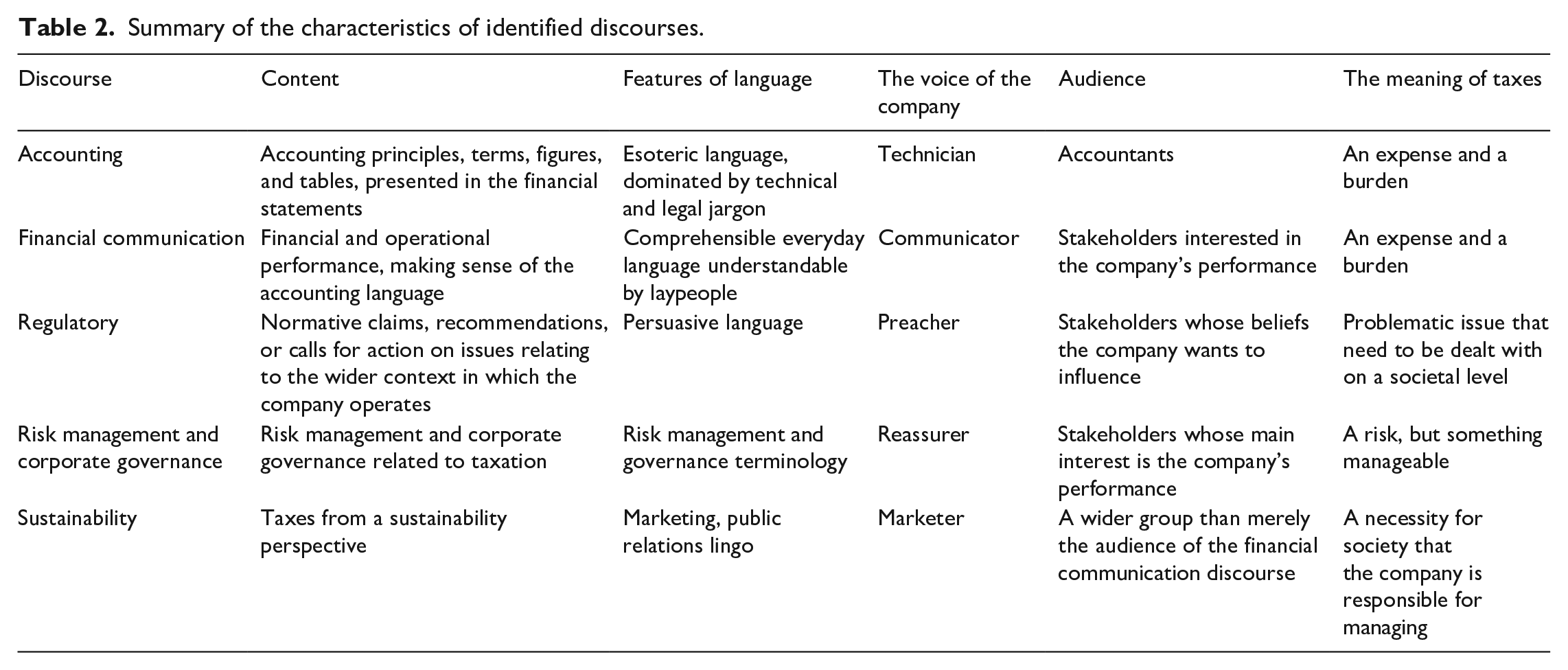

In the following section, the five identified discourse types (summarized in Table 2) are described in more detail. The content and features of language, together with the column ‘the meaning of taxes’ represents the discourse. The voice of the company (sender) and the presumed audience – the discourse community – represents the practitioners forming the communicative situational context, who apply professional norms in describing taxes within the wider institutional and macro context.

Summary of the characteristics of identified discourses.

The accounting discourse

The accounting discourse is a discourse we would expect to find in financial statements (income statement, balance sheet, cash flow, and notes to the accounts). While scholars have adopted a broader interpretation of accounting discourse (see Bhatia, 2010), we limit the accounting discourse to the ‘talk’ or language of the accountants, that is, the descriptions of the accounting principles applied, the explanations of accounting terms, presentation structures, and the application of accounting rules and regulations.

The accounting language, through its use of technical terminology, is an example of codified discourse (Llewellyn and Milne, 2007). It is full of esoteric terms that are not necessarily meant to be read by laypeople. Thus, accounting is ‘conceived of as a system of signification and symbols that needs to be read and interpreted by literate, native speakers who master the language of accounting’ (Sandell and Svensson, 2016: 7). The stakeholders of a company that uses the financial reports are interested in the accounting numbers, and by using accounting language the accountants explain how the numbers are calculated. However, these explanations are normally not easily comprehended for most stakeholders, even for those who are well-educated and financially literate. The stakeholders instead take part in the financial communication discourse, where the accounting numbers are normally accepted as correct.

The accounting language tends to be reduced to texts that are not read but can be pulled out from the drawer when a company is exposed to criticism for its numbers. In that respect, the accounting language serves to protect the management, the accountants, and the auditors. As a technical language, the accounting language is to a large extent restricted to accountants. The voice of the company is the voice of a technician. In excerpt 1 the accounting discourse is illustrated.

Excerpt 1: The accounting treatment of untaxed reserves Tax legislation in Sweden and some other countries allows companies to defer tax payments through transfers to untaxed reserves. The group balance sheet divides untaxed reserves into a deferred tax liability portion, which is reported as a provision, and an equity portion, which is included under non-distributable equity. The deferred tax liability portion is calculated on the basis of the anticipated tax rate for the following year in each country (in Sweden’s case 28%). The group profit and loss account includes no transfers to/from untaxed reserves. The group’s tax charge is calculated as the sum of the tax charges reported by the parent company and subsidiaries adjusted for the effects of transfers to/from untaxed reserves. This adjustment is equivalent to the year’s change in the deferred tax liability portion of these untaxed reserves and is reported under deferred tax liabilities in the group balance sheet. (Vattenfall Annual Report, 1997: 43 f)

The description in excerpt 1, including terms such as deferred tax, untaxed reserves, provisions, non-distributable equity, requires some understanding of the national tax rules applied, as well as of accounting regulation. For a Swedish accountant, the treatment of untaxed reserves is fairly basic, but for most readers the description is analogous to a badly written toaster manual. The technical jargon and esoteric language tend to exclude non-accountants and forces them to rely on the numbers presented by the accountants.

Over the period studied the accounting discourse has been fairly stable. Small changes were made due to developments in accounting regulation, not least the requirement for listed companies to prepare consolidated financial statement in accordance with International Financial Reporting Standards (IFRS), which state-owned companies also have to comply with. Overall, the accounting language is characterized by a high degree of intertextuality. The texts, once presented, are recycled over and over again. In the accounting discourse, income tax is understood as an expense, and not a distribution of profit. Hence, it is portrayed as a burden on the profit distributable to owners.

The financial communication discourse

The financial communication discourse encapsulates the dialog between the company and those stakeholders whose main interest is the company’s financial performance. The language is fairly simple in order to reach a wider number of stakeholders. The company is the communicator who tries to reach a wider audience – mainly investors, owners, and lenders – than what would be possible through mere accounting discourse. On the other hand, the discourse builds on the accounting language, but by the use of everyday language, the discourse strives to make the accounting numbers understandable (Crowther et al., 2006).

Even though few stakeholders fully understand the accounting discourse, it is generally accepted as a representation of company performance. The financial communication discourse, that is, the primary stakeholder dialog in terms of financial performance, is conditional on concepts, definitions, and numbers from the accounting discourse. The accounting discourse is recontextualized, rewritten for a wider audience based on a more well thought out communicative strategy with increased opportunities to influence perceptions of company performance.

In this respect the term tax – a technical term defined in the accounting discourse as an expense – is transferred to the context of financial communication, albeit still closely related to its origin. Hence, tax is presented as a charge affecting the financial statements – as well as key performance indicators. In excerpt 2 Vattenfall communicates how changes in tax rates affect return on equity.

Excerpt 2: Taxes affect KPI The return on equity decreased to 13.6% (17.6%). However, this decline is mainly attributable to a positive, nonrecurring effect on the preceding year’s earnings due to the reduction in the German company tax rate. (Vattenfall Annual Report, 2008: 4)

In the financial communication discourse the level of company taxes, as measured by the accounting language, is recontextualized to a more accessible language, used for describing the financial performance of the company. The premise established by the accounting language that taxes are an expense, and hence a burden, is not challenged by the emergence of another discourse.

The regulatory discourse

The regulatory discourse constitutes recommendations or calls for action – directly or indirectly – without any direct reference to the company’s performance, albeit relating to the wider context in which the company operates, especially to policies and regulations. The language is characterized by the inclusion of normative claims about the state of affairs in society, highlighting issues that the company views as problematic and needs to be dealt with on a societal level. Attending to stakeholders whose beliefs the company wants to influence, the voice in the discourse is that of a preacher, teaching the path of the righteous, based on the knowledge of the self-proclaimed expert.

In the 1990s, the European Union pursued a policy to deregulate the energy market which then consisted of mainly national monopolies. In 1996, the first liberalization directive on electricity was published, which was to be transposed into member states’ legal systems by 1998 (European Communities, 1996). In anticipation of new players entering the market and growing competition, two problematic issues were then brought to the fore in Vattenfall’s reports. First the direct call to action regarding the need to harmonize taxes. Second, the indirect call to action, as taxes are claimed to be a burden on consumer prices.

In the annual report of 1997, a claim is made that taxes must be harmonized in the context of deregulation of energy markets, a claim that is repeated in later reports. Excerpt 3 is an example, where the company makes the normative claim that ‘an efficient energy system’ requires that ‘power generation has to be taxed in the same way and at the same rates in each country’. An unharmonized tax system is claimed to have negative consequences on the environment.

Excerpt 3: Harmonized taxes a prerequisite for an efficient energy system A fundamental prerequisite for an efficient energy system like this is that power generation has to be taxed in the same way and at the same rates in each country. This means that taxes need to be levied on consumption rather than generation. Otherwise a situation can arise where, for instance, high levels of taxation on Norwegian hydro power during certain parts of the year make Norwegian hydro power less competitive than power from Danish coal-fired plants. In this scenario, a Swedish power company trading on the Nordic Power Exchange could end up buying in non-renewable power from Denmark even though there is spare capacity in the Norwegian hydro power system – with obvious environmental consequences. (Vattenfall Annual Report, 1997: 7)

Interestingly, a concern for the environment was used as an argument already in 1997. The regulatory discourse was influenced by the rising environmental agenda in the policy arena at the time when the Kyoto Protocol was signed, and environmental leadership was on Vattenfall’s strategic agenda (Vattenfall Annual Report, 1997: 5). It also served as a predecessor which later developed into the sustainability discourse. However, the expressed intention here was not about protecting the environment, but the need for a changed tax system.

Given the significant rise in energy prices for households in the mid-1990s (Vattenfall Annual Report, 1997; Swedish Energy Agency, 2021), Vattenfall also preaches that electricity prices, heavily affected by taxes, are a burden for consumers. Such a claim can be understood as a call for politicians to reduce taxes, as a way to legitimize current price levels in relation to customers, or as a rhetorical maneuver to refocus or switch the attention (Sandell and Svensson, 2016) of the customers, from the company to the regulatory arena.

Excerpt 4: Taxes increase consumer prices As regards electricity prices to private customers, various taxes and charges have increased continually since deregulation in 1998. They now constitute over 40 per cent of the total electricity price. (Vattenfall Annual Report, 2003: 44)

Since the 1990s, there had been a steady increase in the number of companies reporting on sustainability issues (Kolk, 2004), along with the development of sustainability reporting guidelines. Vattenfall adopted the Global Reporting Initiative (GRI) sustainability reporting standard and issued its first standalone sustainability report in 2003. Taxes were introduced under the section ‘Social performance’, which is defined by Global Reporting Initiative (GRI) as ‘an organisation’s impacts on the social systems within which it operates’. Vattenfall wrote: ‘During the last few years, consumer prices have been affected by steep increases in taxation’ (Vattenfall Sustainability Report, 2003: 25). Although introduced in the sustainability report under social performance, taxes were still portrayed as a problem, rather than as a solution. Classifying taxes as social performance, however, planted an embryo for the broader conception of tax which was realized in 2005.

Mainly addressing the regulator, income tax is portrayed as a problem on a societal level. In general, though, the traditional regulatory agenda, that is, the call for lower taxes, is toned down as the sustainability discourse on taxes later emerges. The emerging sustainability discourse affects and alters the preexisting regulatory discourse. Normative claims for lower tax rates then have to coexist with the attempt to portray the company as a responsible taxpayer.

The risk management and corporate governance discourse

Since the mid-1990s, pressures for change in organizational practices for dealing with uncertainty brought risk analysis within a larger accountability and control framework. Risk entered the realm of private and public sector management thinking becoming an organizing concept as risk management and corporate governance agendas become intertwined (Power, 2004). The perspective of tax governance and risk was introduced in Vattenfall’s 2001 report. What separates this discourse from the financial communication discourse is that the concept of tax is elaborated in the context of risk rhetoric and governance structures – risks being something that needs to be handled by the management. The audience is the same as for the financial communication discourse. However, the voice of the company is the voice of the reassurer, portraying the company and its management as being in control. Rhetorically, language is used to protect the decision makers.

The first tax related risk introduced in the annual reports is the political risk. Under the headline ‘Risk management and political risk’ the company writes (excerpt 5): Excerpt 5: Taxes and political risk The generation and distribution of electricity and heat is a capital-intensive business with long depreciation periods. Consequently, it is vital that political decisions taken to promote or discourage certain activities or the use of certain types of fuel, through tax control etc, should be sustainable. Otherwise, in spite of sound calculations, it may be difficult to justify an investment in new facilities. [. . .] One concrete problem is the Swedish tax on nuclear power which does not exist in other countries. In Vattenfall’s assessment, this situation is a long-term threat to Sweden’s electricity supply. (Vattenfall Annual Report, 2001: 29)

Even though presented under the risk section we notice the overlap with the regulatory discourse. Political decisions on tax control are presented as a risk, but more to the society as a whole than to the company. It is about the risk of lost investment opportunities and the electricity supply of the country. The text corresponds to the regulatory agenda, but is framed in a risk narrative. The political risk concerning taxes was brought up as late as in the 2011 report, but was thereafter toned down.

From 2013, the discourse of risk and governance rather focuses on the handling of tax risks, that is, traditional risk management. The tax policy is mentioned, as well as the reporting structure of the company. At the time, Vattenfall expresses improvements of its governance processes by fully integrating risk management in all parts of the group’s operations. From 2017 the section on tax risk and tax governance is heavily expanded, putting more emphasis on the responsibilities of being a state-owned company in line with the Swedish state ownership guidelines of 2016 (excerpt 6).

Excerpt 6: Tax governance Vattenfall has established a process for tax management and monitoring to ensure that its taxation is in accordance with the law and to manage our tax risk. The Group and Country Tax functions ensure that the Vattenfall Group’s business activities are conducted proactively and in accordance with laws and regulations, i.e. in a responsible manner. The Group Tax function reports to the Board of Directors and Audit Committee on tax strategy and provides updates on tax regulations and the main challenges we face. (Vattenfall Annual and Sustainability Report, 2017: 166)

The management of taxes now goes hand-in-hand with the ideas of sustainable tax. There are processes and governance structures to ensure that the ‘taxation is in accordance with the law’ and that the business activities are conducted ‘in a responsible manner’. The tax strategy of the company is presented and aligned with the idea of sustainable tax, and tax risk is defined as ‘the risk of a Vattenfall legal entity failing to meet compliance and reporting requirements in a tax jurisdiction and/or failing to pay or collect the correct amount of tax at the correct time’ (Vattenfall Annual and Sustainability Report, 2017: 166). We notice how the introduction of a sustainability discourse affects the risk management and governance discourse, in order to let them coexist, complementing rather than contradicting each other. The risk discourse, however, still portrays tax as a burden, since all compliance issues involve a risk dimension.

The sustainability discourse

In 2005, the company for the first-time acknowledged society, citizens in general and Swedish citizens in particular, as stakeholders. This is exemplified in excerpt 7: Excerpt 7: Recognizing the citizens as stakeholders Vattenfall has an effect on citizens in all countries of operations, mainly as a main provider of electricity and heat in the markets where we operate [. . .], but also as an employer and a tax payer. Vattenfall is owned by the Swedish state, which makes Swedish citizens stakeholders in even more aspects since they can be regarded as indirect owners of the company. (Vattenfall Sustainability Report, 2005: 71)

The journey toward sustainability continued in 2007 when the disclosure of total taxes was made under the heading ‘Payment to government – total taxes’. This was further developed the next year as the section ‘Payments to government’ was presented as a part of the total ‘Economic value distributed’. The change of wording is an effect of changes to GRI, which the company follows very strictly, but the use of another set of words creates an aura of something positive around taxes, namely, that taxes are an economic value that is distributed to the government, in contrast to the traditional view of taxes as merely a burden on the company’s profit.

This perspective was catalyzed and reinforced by developments in legal/quasi-legal and professional norms (Appendix 1). In Vattenfall, even though a mindset already had been established concerning taxes as something positive for society, the sustainability discourse really took shape in 2016. The company then describes its tax policy in which it defines itself as a good citizen (Vattenfall Annual and Sustainability Report, 2016: 161). This is further developed in excerpt 8, where Vattenfall describes itself as a taxpayer, and the impact of taxes paid on employees, local communities, and countries: Excerpt 8: Vattenfall as taxpayer The total taxes Vattenfall pays have a significant impact on our operating countries and in local communities. [. . .] In addition to corporate income taxes, Vattenfall pays taxes on production and property as well as social security charges and taxes for employees. In many of our operating countries, these non-income-based taxes account for a majority of the tax costs. (Vattenfall Annual and Sustainability Report, 2016: 161)

In 2016 when the tax policy was disclosed in the annual and sustainability report, the company also acknowledge the importance of paying taxes ‘in the country where the profit is generated and in accordance with local laws and regulations’ in that country (see excerpt 9).

Excerpt 9: Paying taxes in the country where the profit is generated Vattenfall is a major taxpayer in the markets in which we operate. According to our policy, we pay taxes in the country where the profit is generated and in accordance with local laws and regulations. (Vattenfall Annual and Sustainability Report, 2016: 161)

Being a state-owned company makes it extra important to ‘exhibit responsible conduct in the tax area’ (Vattenfall Annual and Sustainability Report, 2017: 74). Being responsible in the tax area is elaborated in the tax strategy, reproduced in the annual and sustainability report, in terms of what Vattenfall does not do: ‘Vattenfall does not engage in aggressive tax planning’ (Vattenfall Annual and Sustainability Report, 2017: 166). This statement is developed in 2018 where Vattenfall adds that the company ‘does not have any business activities in countries listed as tax havens’ (Vattenfall Annual and Sustainability Report, 2018: 158).

Over the years the sustainability discourse has grown in scope and significance. In 2018 Vattenfall recognized taxes as a key issue, and as an important component in order ‘to grow in a sustainable, responsible and socially inclusive way’.

The discourse develops from consisting of a few words vaguely indicating that taxes are something more than merely a burden on profits. Step-by-step the company recognizes itself as a tax-paying corporate citizen, the importance of paying taxes in the countries where profit is generated, and finally takes a stand against aggressive tax planning and the use of tax havens. In this process the language develops toward the language of marketing, the speaker being the marketer who is selling the idea of a responsible company running legitimate operations. Taxes are given positive connotations.

From simplicity to a complex multidimensional meaning

Tax as a concept has been transformed from a fairly simple term to a concept with multidimensional meanings. The word tax in corporate reporting emerges from the accounting discourse, which is still the core discourse of financial reporting. In 1997, the start of this study, the word tax had already been recontextualized into new discourses, that is, the financial communication discourse and the regulatory discourse. Each discourse contains different voices and specific language features depending on the norms applied and the presumed audience – those whom the company seeks to engage in a particular dialog – giving different meanings to the concept of tax. Adding to these three discourses, the risk management and corporate governance discourse emerged in 2001 and the sustainability discourse in 2005, that is, two distinctive shifts were identified in the period studied, concurring with shifts in the corporate reporting context. The discourses identified are not exclusive, not easily separated from each other but often overlapping. New discourses do not emerge in a vacuum. They are brought in from other contexts and are recontextualized in the genre of corporate reporting. They are influenced by and at the same time affects existing discourses.

It is reasonable to understand the emergence of new discourses through the process of recontextualization (Fairclough, 2013; Wodak, 2011) as a complex interplay between new reporting initiatives, more advanced governance structures incorporating tax issues on several executive levels, the mixing of genres (such as financial and sustainability reports), and stakeholder requirements – participating in a dialog with the company (Brennan et al., 2013; Sandell and Svensson, 2016) – and through texts that perform. It is not easy, perhaps even impossible, to sort this complex structure of influencing factors into causes and effects, an effect also being a cause. But it is important to note that language in itself performs, it has a productive quality (Sandell and Svensson, 2016; Vollmer et al., 2009). The texts in the annual report are not merely a representation of performances. The language thereby has a constitutive role, not merely a reflective one (Khalifa and Mahama, 2017).

The texts affect the mindset, not only of those who read the reports, but perhaps sometimes to an even larger extent those who author the reports. This study contributes to our understanding of how companies through language use – intentionally or unintentionally – create new spaces for negotiation, maintain as well as reconstruct relationships with stakeholders, strengthen legitimacy, alter the understanding of traditional business concepts in the context of changing societal expectations etc., alluding to normative professional, legal, or societal frameworks. Language use enables the reconstruction of relationships between companies and their stakeholders within the context of the developments of tax regulation and the mounting pressure to move toward more responsible tax management.

New discourses emerge due to internal changes, regulatory changes, and societal changes. These discourses build on present discourses but represent different views and values emanating from other contexts. New layers of meaning of the tax concept are added. The emerging discourses coexist with the old ones. The level of importance of each discourse tends to shift over time in an ongoing process reflecting, not least of all, societal norms, norms that companies at the same time take part in shaping. It is fair to assume that the professional management of taxes is dependent on which discourse is dominant, since it determines who in the company is brought into the discussion, authoring the texts.

Previous studies have observed interdiscursivity in corporate genres. Specifically, various kinds of discourses have been identified within different sections of the annual reports (discourses of accounting, economics, public relations, and law) (Bhatia, 2010), sustainability reports (discourses of public relations, sustainability, strategic management, compliance, and financial accounting) (Rajandran, 2018), and strategic communicative documents (Koskela, 2013). This paper contributes to the tax, accounting, and language literature, through a longitudinal interpretive textual analysis, identifying important shifts in tax discourses from one dominated by codified accounting discourse, reinforcing the monolithic representation of tax as a burden, to one where tax is given a multidimensional meaning within a broader discursive context. We show that language use has a performative effect on what tax is understood to be, and may contribute to changes not only in organizational communication, but also in organizational structures.

The findings also reveal how the word tax and the meaning of tax have been recontextualized in different corporate reporting discourses, and have intertextually merged with other discourses, such as the sustainability discourse. We have observed the coexistence and potential tensions between dominant and emerging discourses on tax in corporate reporting and how different manifestations of taxes are articulated and reconciled. We believe that future research on discourses within the field of financial communication and taxes would benefit from more longitudinal studies in order to address the transformative effects of language use.

Footnotes

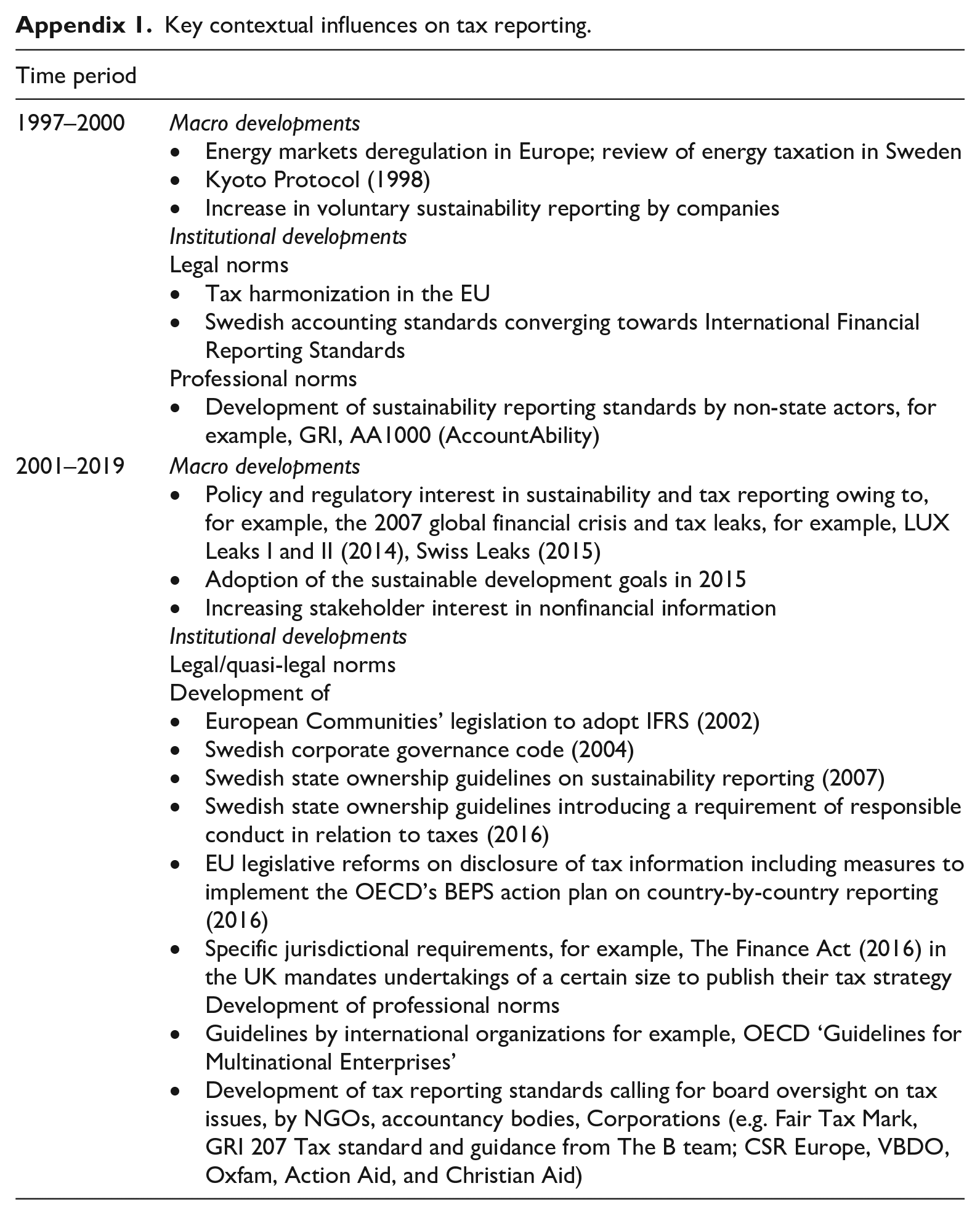

Appendix

Key contextual influences on tax reporting.

| Time period | |

|---|---|

| 1997–2000 | Macro developments

• Energy markets deregulation in Europe; review of energy taxation in Sweden • Kyoto Protocol (1998) • Increase in voluntary sustainability reporting by companies Institutional developments Legal norms • Tax harmonization in the EU • Swedish accounting standards converging towards International Financial Reporting Standards Professional norms • Development of sustainability reporting standards by non-state actors, for example, GRI, AA1000 (AccountAbility) |

| 2001–2019 | Macro developments

• Policy and regulatory interest in sustainability and tax reporting owing to, for example, the 2007 global financial crisis and tax leaks, for example, LUX Leaks I and II (2014), Swiss Leaks (2015) • Adoption of the sustainable development goals in 2015 • Increasing stakeholder interest in nonfinancial information Institutional developments Legal/quasi-legal norms Development of • European Communities’ legislation to adopt IFRS (2002) • Swedish corporate governance code (2004) • Swedish state ownership guidelines on sustainability reporting (2007) • Swedish state ownership guidelines introducing a requirement of responsible conduct in relation to taxes (2016) • EU legislative reforms on disclosure of tax information including measures to implement the OECD’s BEPS action plan on country-by-country reporting (2016) • Specific jurisdictional requirements, for example, The Finance Act (2016) in the UK mandates undertakings of a certain size to publish their tax strategy Development of professional norms • Guidelines by international organizations for example, OECD ‘Guidelines for Multinational Enterprises’ • Development of tax reporting standards calling for board oversight on tax issues, by NGOs, accountancy bodies, Corporations (e.g. Fair Tax Mark, GRI 207 Tax standard and guidance from The B team; CSR Europe, VBDO, Oxfam, Action Aid, and Christian Aid) |

Acknowledgements

We would like to thank Anna Eriksson for her excellent research assistance.

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: We gratefully acknowledge funding from ‘Jan Wallander och Tom Hedelius Stiftelse, Sweden’, grant number P19-139, Tax Reporting for a Sustainable Society.