Abstract

Research has shown how debt problems of individuals involved in the criminal justice system may hinder successful reintegration. In various jurisdictions, criminal law offers opportunities to support reducing debt problems, but insights into the experiences of tackling debt problems within a criminal law framework is limited. Using a qualitative research design, this study aims to understand considerations and implications of financial requirements imposed on offenders dealing with debt problems in the Netherlands. Our findings suggest that in the pre-sentencing, sentencing and execution phase of the criminal justice system, too little time, knowledge and attention is available on how to provide successful support to tackle debt problems. Recommendations for improvement are outlined.

Introduction

In countries worldwide, debt problems are common among people with convictions (Aaltonen et al., 2016; Evans, 2014; Gålnander, 2023; Harris et al., 2010; Koenraadt et al., 2020; Link, 2019; Link and Roman, 2017; Pleggenkuhle, 2018; Roman and Link, 2015). Estimates on the incidence of indebtedness among people in prison generally range from 50% up to 80%, and are even higher after incarceration (Harris et al., 2010; Koenraadt et al., 2020; Link, 2019; Pleggenkuhle, 2018). Also the vast majority of probation clients have debts problems, across all types of crime and sentence (Gålnander, 2023; van Beek et al., 2020). Debt among people with convictions is diverse in nature, including punishment-related debts, such as fines, as well as pre-existing debts such as consumer debts, rent arrears and private loans (Harper et al., 2020; Koenraadt et al., 2020; Weijters et al., 2018; van Beek et al., 2020, 2021).

Previous research has shown how debt problems are an important criminogenic factor and may hinder successful reintegration. The process of desistance and motivations for change, can be restrained by the constant stress and feelings of hopelessness of having debt problems (Evans, 2014; Gålnander, 2023; Harris et al., 2010; Link and Roman, 2017; Pleggenkuhle, 2018; van Beek et al., 2021). Yet, only a minority of (ex-)offenders receive debt counselling and even fewer are included in debt restructuring programmes (Weijters et al., 2018). This is worrisome as studies have shown how eliminating complex debt situations is almost impossible without assistance (Gålnander, 2023; van Beek et al., 2021).

It follows that tackling financial problems may well be an important pillar in supporting desistance and, indeed, such work is apparent in the criminal justice system. For example, Dutch criminal law allows criminal courts to impose specific requirements on an offender’s financial situation (hereafter financial requirements), such as providing insights into the debt situation and working towards debt restructuring. These financial requirements should oblige offenders to work on their financial problems and thus improve their reintegration and desistance process. However, little is known about the opportunities and obstacles of imposing and implementing financial requirements in different stages of the criminal justice system. This study seeks to address this gap by using a qualitative research design, based on case file analysis and 28 interviews with professionals involved in the imposition or execution of financial requirements, such as judges, prosecutors and probation officers. It aims to analyse considerations that influence financial requirements in sentencing decisions, as well as the outcomes of financial requirements within the context of supervision.

Financial problems, criminal behaviour and the criminal justice system

Research has shown how debt problems and crime are interrelated and may reinforce each other in a negative downwards spiral. However, having debt problems can increase the likelihood to commit crime (Aaltonen et al., 2016; Agnew, 2006; Felson et al., 2012; Hoeve et al., 2016; Olesen, 2016). In line with strain theory, financial difficulties can directly contribute to a greater likelihood of committing property or drug offences to gain income, provide for basic needs or pay off debts (de Jong, 2017; Felson et al., 2012; Hoeve et al., 2016; Turner et al., 2009; van Beek et al., 2022). In addition, experiencing financial hardship can impede cognitive functions, result in constant stress, feelings of hopelessness and (social) uncertainty (Mani et al., 2013; Shah et al., 2012). This may all negatively influence other life domains such as employment, housing and relationships, which are all important factors to refrain from crime (Gålnander, 2023; Pogrebin et al., 2016; van Beek et al., 2022; van Middendorp et al., 2017).

However, penal responses to criminal behaviour can by themselves increase debt problems (Aaltonen et al., 2016; Harris et al., 2010; Hoeve et al., 2016; Jungmann et al., 2014; Olesen, 2016; Pleggenkuhle, 2018). Previous studies have shown how debt problems can increase after a prison sentence, for example, through difficulties in finding employment and extra obligations such as rent arrears and consumer loans that are awaiting after return to the community (Allen et al., 2017; Harper et al., 2021; Koenraadt et al., 2020; Lewandoski, 2010; Olesen, 2016; Pogrebin et al., 2016). In addition, legal financial obligations (LFOs), that result from involvement in the criminal justice system, such as fines and victim compensations, can contribute to worsening debt problems (Bannon et al., 2010; Beckett et al., 2008; Beckett and Harris, 2011; Diller et al., 2010; Evans, 2014; Harper et al., 2021; Harris et al., 2010; McKernan, 2019; Martin et al., 2018; Pleggenkuhle, 2018). These legal financial obligations particularly may affect already poor offenders, adding to existing debts and increase the likelihood of ongoing criminal justice involvement (Evans, 2014; Harris et al., 2010; Pleggenkuhle, 2018).

In other words, financial difficulties can be both a cause and a consequence of criminal behaviour which may contribute to a process of cumulative disadvantage (Aaltonen et al., 2016; de Jong, 2017; Gålnander, 2023; Harris et al., 2010). Gålnander (2023) shows how debt problems can be a burden for a successful reintegration and how dealing with debt and financial problems is an integral part of desistance journeys. While financial problems are associated with shame and hopelessness, clearing debts can promote inclusion through a heightened sense of citizenship and belonging in society (Farrall et al., 2014; Gålnander, 2023). Working on and solving debt can thereby act as a way to break the process of cumulative disadvantage. However, in Sweden, Norway and the Netherlands, probation officers often lack effective discretionary methods to support clients with debt problems, while financial problems are common during supervision periods and improvement of a client’s financial situation is frequently listed as a goal of supervision plans (Gålnander, 2023; Todd-Kvam, 2019; van Beek et al., 2020, 2021). Consequently, probation officers mainly focus on monitoring and motivation, while experiencing significant uncertainty in handling financial matters This is problematic given that probation clients are generally unable to resolve these financial issues independently (Gålnander, 2023; van Beek et al., 2021).

In countries such as the Netherlands, Germany and the United States, criminal law offers several opportunities to support reducing debt problems. In these instances, specific financial requirements on an individual’s financial situation can be included in the sentencing decision, such as providing information about an offender’s financial situation to their supervising officer, or attending financial counselling or education programmes to address specific financial issues or behaviours. In most countries, supervision on these financial requirements, such as providing insights into the debt situation, is being carried out by the Probation Service (Kalmthout et al., 2003; United States Sentencing Commission, 2023). However, the literature provides limited information on whether sentencing decisions include supervision related to debt issues, and on how these requirements are implemented at different stages of the criminal justice system.

Current study

This article focuses on financial requirements at various stages of the criminal justice system in the Netherlands and provides unique insights into the prevalence, nature, experiences and bottlenecks of imposed financial requirements. In doing so, we make a distinction between two types of supervision of an offender’s financial situation. First, we analyse financial requirements that can be imposed by a criminal judge in a conditional framework of sanctions. This means that financial requirements can be imposed, for example, in the context of a suspension of pre-trial detention, a conditional sentence and a conditional release, with which the person must comply for a specified period.

In the Netherlands, sentencing aims to achieve objectives such as retribution, deterrence, rehabilitation and prevention. Sentences are determined based on various factors, including seriousness of the offence, culpability of the offender, impact on victims and the potential for rehabilitation. Judges and other decision-makers possess significant discretion in balancing these diverse sentencing aims. Conditional sentencing and release have been integrated into the penal legislation and were recently expanded, strengthening the role of rehabilitation (Boone, 2000; Schuyt, 2010). The Probation Service assumes a crucial role in the supervision and implementation of conditions associated with a conditional sentence or release. Based on information on the personal situation of the client, probation workers advise the criminal court on appropriate sanctions and/or specific conditions, such as debt counselling and participation in budgeting courses. The Probation Service also engages in supervision through monitoring, guidance and behavioural intervention for individuals subject to specific conditions imposed during conditional sentencing or release (Abraham et al., 2007; Hanrath et al., 2018).

Despite the association between financial problems and (further) crime, concrete behavioural conditions for dealing with financial problems are not included in the law. However, such conditions can be placed under a more general category of behavioural conditions, such as the broad residual category ‘conditions concerning the conduct of the convicted person’. Under this category, a criminal judge can impose conditions that relate to the financial problems of the convicted person, such as providing information about their financial situation or cooperating in a debt counselling process or administration order, which must subsequently be assessed by a civil court.

Second, financial problems can be included as goals in the context of the supervision plan by the probation officer. In those instances, the criminal judge imposes a general probation order, without including specific financial requirements in the sentencing decision. Subsequently, during probation supervision, debt problems can eventually be identified and similar to financial requirements in the sentencing decision, be included in the probation plan. In both cases, supervision on finances is carried out by the Probation Service.

In this article, we analyse considerations and results of financial requirements in the sentencing decision in different stages of the criminal justice system. We use the term financial problems to describe various problems with finances, such as not being able to make ends meet as well as having payment arrears or debts. The most common form of financial problems is debts and we use these terms interchangeably.

Methods

The data used in this study are collected as part of our research project ‘supervision on finances’ conducted in the Netherlands in 2020. For our study, we used two primary data sources: interviews and probation case files.

Interviews

First, data were obtained through semi-structured in-depth interviews. Interviews were conducted with professionals involved in the imposition or execution of financial requirements, to gain insight into the progress, results and bottlenecks of financial requirements in the Netherlands. For this study, we used a purposive sample. In total, 28 interviews were conducted with employees of seven organizations related to financial requirements: Ministry of Justice and Security (Policy officers; N = 3), Public Prosecution Service (N = 4), Criminal Court (Judges; N = 4), Dutch Probation Service (N = 8), Debt Counselling/municipality (N = 4), Administration (N = 4) and Child Protection Board (N = 1). Most of the respondents were situated in western and urban areas in the Netherlands, but some interviews were also conducted with respondents in eastern and less urban areas (N = 4). Respondents were involved in various positions in different stages of the criminal justice system, which allowed for detailed and varied insights on the process of financial supervision in the Netherlands. Unfortunately, because of COVID-19 measures at the time of this study, we were not able to include probation clients that have been imposed financial requirements themselves.

Using a purposive and snowball sample, respondents were approached through organizations that were in various ways involved in the process of financial supervision and through the network of the researchers. In order to retrieve a heterogenous group of respondents, requests to participate in an interview were sent out to people in varying functions, organizations and geographical locations. Respondents were first invited by mail, telephone or social media and informed by either e-mail or telephone about the purpose of the study and interview. Participation was voluntary and respondents could stop the interview or be excluded from the study at any moment. The first eight interviews were conducted in the work environment of the respondents. Due to COVID-19 measures, later interviews were all conducted through phone and/or video calls. Even though we would have preferred face-to-face interviews to establish trust relations more easily, we did not experience any difficulties during the phone and video interviews. The interview phase lasted until a point of saturation was reached.

The interviews were semi-structured in nature. A topic list was compiled for each organization in order to get sufficient information to answer the research questions. For example, with judges and prosecutors, we discussed legal requirements, considerations and ideas on imposing financial requirements in the sentencing decision, while with probation officers, debt counsellors and administrators, we mainly focused on their experiences with different trajectories, cooperation with other professionals and results on debt problems. Before every interview, participants were informed about the goals of the study and how confidentiality, anonymity and safety of data were assured. After informed consent and approval, all interviews were recorded by a voice recorder. The interviews took approximately 60–90 minutes.

Probation case files

Second, a case file analysis at the Dutch Probation Service was performed. Combining interview data and case file data allowed us to gain both in-depth insights about motivations and experiences of the involved actors as well as a broader understanding about the prevalence of imposed financial requirements. Furthermore, the case file analyses allowed us to acquire further insights into the backgrounds of probation clients under supervision on debts, considerations that play a part in the imposition and implementation of financial requirements as well as the scope, nature and possible results of different forms of financial supervision. Case files were made available at the Dutch probation office in IRIS, a digital client tracking system in which probation officers maintain all information during the probation period, including probation advisory reports of their clients during supervision trajectories. The case files are based on the Recidivism Assessment Scale, which includes information on various subscales such as the current offence, offending history, income and financial management (see Bosker, 2015 for more information on the RISc scales in Dutch Probation Service).

The Dutch Probation Service granted permission to access and analyse the case files and made available all files from probation clients who came under supervision between 2016 and 2018, which resulted in access to a total of 54,435 case files. It was not possible to specifically select files in which clients were subject to supervision on finances, therefore relevant keywords were used to retrieve information related to financial supervision, such as (1) administration, (2) budget, (3) debts, (4) (debt) restructuring and (5) payment plan. In the IRIS system, we were able to search for these keywords in two text fields: in the specific text of the sentencing decision that included the imposed financial requirements as well as the general text of the case file. In 19,607 files at least one of these keywords emerged. In 2543 of the 19,607 files, there was at least one of the keywords in the description of the imposed conditions. By using IBM SPSS Statistics, a sample was drawn of 5% of the 2543 selected cases supposedly involving financial requirements. This resulted in a stratified sample of 112 files from clients who started to receive supervision between 2016 and 2018. After inspection, 93 of the 112 files (83%) indeed concerned cases in which the judge imposed financial requirements.

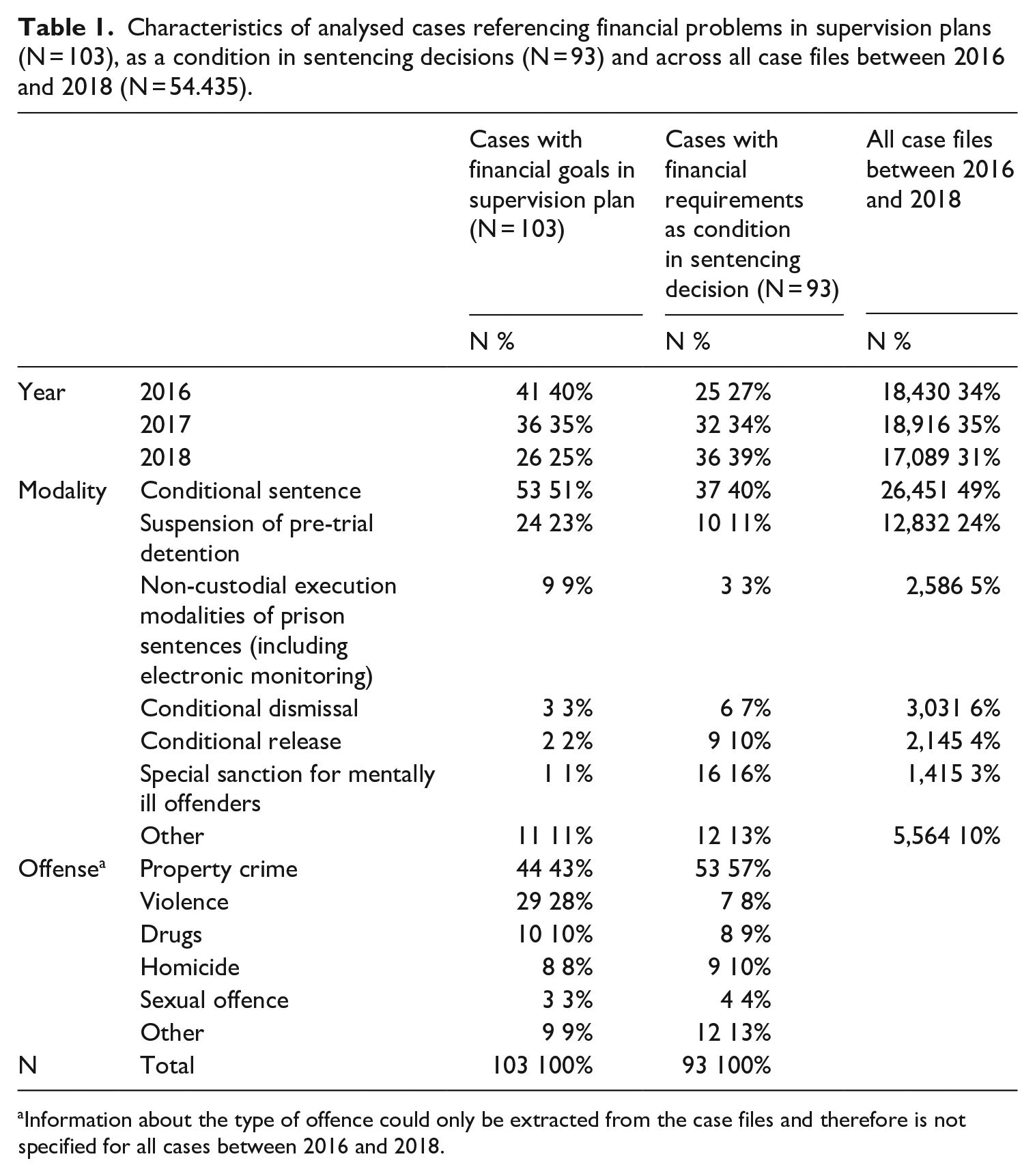

We also selected the same number of case files with financial goals in the supervision plan without specific financial measures in the sentencing decision. In 17,064 of the 19,607 case files at least one of the keywords were listed in the supervision plan or were in general mentioned in the case file. A similar amount of 112 files out of the 17,064 purposively selected files was drawn (0.5%). After inspection, 103 of the 112 selected files (92%) included addressing financial problems as a goal within the supervision plan. As such, we analysed 196 case files: 93 files in which financial requirements were included as a condition in the sentencing decision and 103 files that included financial goals in the supervision plan drawn up by the probation officer. Table 1 presents an overview of the year, judicial modalities and offences as described in the case files for the two types of financial supervision.

Characteristics of analysed cases referencing financial problems in supervision plans (N = 103), as a condition in sentencing decisions (N = 93) and across all case files between 2016 and 2018 (N = 54.435).

Information about the type of offence could only be extracted from the case files and therefore is not specified for all cases between 2016 and 2018.

A checklist was used during the case file analysis, in which all relevant information was listed. First, advisory reports were studied to understand motivations for advising the courts to incorporate financial requirements. Second, a number of background characteristics of persons who are under financial supervision, such as age, gender and type of offence, were noted. Third, a detailed description was given for each file to analyse considerations of why financial measures were imposed, what activities took place during the financial trajectories and to what extent the financial requirements and other conditions have been met.

Analysis

A qualitative analysis of the case file and interviews data has been carried out to outline the trajectories and results of various forms of supervision on financial problems. All interviews were transcribed verbatim, after which the excerpts were coded and thematically analysed, using both an inductive and grounded theory approach. For the analysis of the interviews, labels were assigned to the first available transcripts by means of open coding, after which all codes were subdivided into main and sub codes. Responses to the topics discussed in the first interviews led to inquiries about new topics in future interviews. Main topics included debt background, considerations to advise and impose financial requirements, supervision on debts with and without requirements. Ten of the 28 interviews were coded by two researchers in order obtain intercoder agreement. After consultation between the researchers, the codebook was completed. All transcripts were coded using the software programme NVivo 12.

Results

Considerations to advise financial requirements

Analysis of the case files and interviews showed a clear distinction in the prevalence of the two forms of supervision on the financial situation. All respondents in this study confirmed that hardly any financial requirements were incorporated in the sentencing decision, while the majority of offenders are dealing with debt problems. Indeed, based on the selection of our sample for the case file analysis, we were able to find a small proportion of only 5% of case files in which keywords on financial problems were included in the formulated imposed conditions (in 2543 of the 54,435 available case files). In around one third of the cases, in 17,064 of the 54,435 case files, keywords on financial problems were listed in the supervision plan or were in general mentioned in the case file.

Interestingly, financial requirements are hardly imposed by a judge if not advised by the probation officer prior to the judgement. Yet, while judges and prosecutors largely rely on the advisory report written by the Probation Service, in the pre-sentencing stage probation officers generally receive little information on financial problems of offenders. Here, we identified two main barriers. A first challenge faced by probation officers during the pre-sentencing is the limited accessibility and reliability of official financial records, necessitating reliance on information gathered directly from clients. In the Netherlands, due to operational constraints, the routine request of tax data is regarded impractical. Verification of financial information with the tax authorities may only occur in exceptional circumstances, in case there is reasonable doubt about the veracity of the information provided by the defendant, following the requisite ministerial authorization (see also Nauta and de Wilde, 2020). Depending on the juridical modality, probation officers generally only visit the defendant once or twice prior to the judgement and experience difficulties in gathering sufficient information about the sometimes precarious and complex financial situation in a short time span, as explained by a probation officer: I only try to get general information on the financial situation, not in detail. I simply do not have the opportunity to retrieve so much information on the financial situation within one conversation and also afterwards I do not have the time to figure it all out. (Probation officer advice)

Second, compared to issues in other areas such as employment, housing and healthcare, probation officers in the pre-sentencing phase often do not adequately address financial problems. They frequently lack sufficient knowledge about how these problems can impede reintegration and are often unaware of potential interventions they could recommend. As a result of complex financial situations and a lack of available interventions for addressing debt problems, probation officers often do not succeed in obtaining sufficient insights into the amount and types of debts for the advisory report: In my opinion there is not enough attention for debt problems and the risk for criminal behaviour [. . .]. It is also because we often advise to attend existing programs, but we do not have that for financial problems. We used to have a budgeting course, but this is not an official behavioural intervention anymore. (Probation officer advice)

Considerations in imposing financial requirements

While probation officers in the pre-sentencing phase do not always retrieve enough information on financial problems, during the next sentencing phase, judges and prosecutors do largely rely on this advisory report. Judges stated in the interviews that they seldom receive advisory reports recommending the imposition of financial measures. Consequently, due in part to the infrequent advice, they rarely include these requirements as a condition of the sentence. This was confirmed by the case file analysis.

Besides, similar to the probation officers in the pre-sentencing phase, judges and prosecutors themselves have limited time and attention to collect information on financial problems in the sentencing phase. Even if they are aware of the fact that financial problems might have contributed to criminal behaviour, in the absence of concrete financial programmes, financial requirements are generally not thought of or undesirable to include as a condition in their decisions. Some of the requirements are considered too vague, which could make the assessment of compliance during the execution phase arbitrary, as explained by a criminal judge: We generally do not think about the possibility to impose financial requirements as a condition. In case financial problems exist, specific programs are hardly advised by the Probation Service and therefore I think it is difficult to monitor compliance. When the requirement involves a budgeting course I can imagine it might be easier, because you just have to take the course, show up and do assignments. But cooperating in solving debt problems is not a concrete requirement. You can easily debate about whether or not you are complying. (Criminal judge)

Interestingly, prosecutors and judges revealed highly diverse ideas about the merits of using criminal law to tackle underlying financial problems as a way to prevent reoffending. Some judges stated that financial measures to tackle the financial problems are not compatible with other punitive measures, such as imposing fines or compensation for the victim. Other judges did, however, point out how tackling financial problems is vital for a successful reintegration process: It is pointless to try to remediate debts through criminal law, so I will not impose those financial requirements. Of course it can be desirable and helpful for someone. However, getting rid of debt is not a goal in itself for me. (Criminal judge) Debts may cause an awful lot of stress and that has a negative impact on everything. So, if people have their financial situation in order, it just gives a lot of stability. Then you hope that they will not make the wrong decisions they made before. We simply hope to prevent recidivism, which is what we are doing as a criminal court. (Criminal judge)

Finally, prosecutors and judges often assume that imposing a general probation order is sufficient to work on the financial problems during the supervision stage. As such, specific financial requirements are hardly included in the sentencing decision, even in cases in which the link between the criminal offence and financial problems is highly prevalent: Well, that’s what I find interesting about the research, because that’s actually something that doesn’t really comes to my mind. We usually impose a general probation order so that the probation officer decides what the exact indications are. (Public prosecutor)

Financial trajectories under supervision

During the execution phase, the actual implementation of financial requirements is largely determined by the supervising probation officer(s). All imposed requirements and conditions are translated into a supervision plan set up by the probation officer in cooperation with the client. Simple financial support can be offered by the probation officers themselves, while clients with more complex financial problems are referred to agencies with expertise in financial problems and debts. This includes the use of municipal debt assistance programmes or protective guardianship. In all cases, the probation officer acts as the project coordinator. Overall, both the case file analysis and the interviews showed that the financial problems were generally not reduced during the probationary period.

Probation officers experience difficulties in grasping insights into complex financial situations. It usually takes a long time before clients are willing to provide detailed information on their financial situation, until essential information has been collected and a client is registered and accepted for financial trajectories. Often these trajectories already transcend the probation period. In some cases, financial requirements are not concretely formulated and the probation officer has to decide what sort of programmes clients can be referred to. Analysis of the case files showed that the concrete financial requirements vary widely, ranging from providing insights in the debt situation to requiring to participating or working towards debt relief programmes. In case of admission to debt settlement and administration, a civil judge needs to grant permission first, which generally takes up to 6 months or longer. As such, financial trajectories often only form part of the probationary period and last longer.

Motivation, compliance and a big stick

Some clients respond well to working on their financial problems under supervision; either because they are already motivated or because they have been motivated by the probation officer or other professionals. Yet, generally probation officers experience resistance to talk about or work on monetary problems, as explained by one of the probation officers: We see that finances are very important for the client. We are generally not allowed to touch upon a number of things: not the children and not the money. This is difficult as finances are always in the foreground, because that is what a client has to deal with on a daily basis. (Probation officer supervision)

Depending on whether the court has included a financial requirement in its decision, probation officers reported some difference in their ability to exert more pressure on clients to work on their financial problems. In case of financial requirements, probation officers feel they have a ‘big stick’ available to encourage compliance because violation of the condition could, in theory, result in revocation, as explained by this probation officer: Nobody likes to outsource their finances, no matter how disastrous the situation is. Some of them have the idea that they are losing control over their lives by handing it over. That resisting behaviour is always present, but it helps if there is a legal condition. In those cases we can say: Well, if you do not cooperate, we will go back to the judge and see what they say about it. (Probation officer supervision)

Interestingly, if a client does not comply with the financial requirement that is imposed, in practice, probation officers generally do not consider it worthwhile to revoke them for non-compliance. In case they would, the suspended custodial sentence will be implemented and the client would disappear out of the Probation Service’s sight completely, terminating supervision on all other life domains as well. Therefore, probation officers rarely use this option.

Respondents indicated that some features could be important in motivating clients to work on their debt problems. These include generating quick results, establishing a good and trustful relationship between client and probation officer, and enabling clarity about the process. Especially in those cases in which clients wait for months until admission to municipal debt programmes is granted, clients can be discouraged while the precarious financial situation may become worse. Furthermore, in the Netherlands, debt assistance differs among municipalities. By far, not all organizations offering financial support have experience in working with probation clients and do not always have the skills to work with unmotivated clients in a juridical context.

Conclusion and discussion

Many offenders are dealing with financial problems. Despite the clear benefits for reintegration and crime prevention, identifying financial problems in the pre-sentence and sentencing phases remains challenging. This study reveals that financial requirements are hardly incorporated in the sentencing decision, even though financial problems are often included in the probation plan as set up by the probation officer. Earlier studies already showed that the debts of offenders are not always visible and estimated that at least 60% of former prisoners and even 80% of probation clients are dealing with debts (Koenraadt et al., 2020; Link, 2019; Pleggenkuhle, 2018; van Beek et al., 2020). According to van Beek et al. (2022), in at least one third of the probation files in which clients were dealing with debt problems, no financial goals were formulated.

Furthermore, this study provided unique insights into the process of financial supervision within different stages of the criminal justice system in the Netherlands. During the pre-sentence phase, probation officers retrieve little information about the financial problems of offenders. There are hardly objective sources to rely on when drawing up advisory reports which make them dependent on their clients for information. However, time constraints, lack of attention for debt problems and reluctance of probation clients to disclose their financial situation are obstacles to providing well-substantiated advices in this area. In the sentencing phase, judges largely rely on the advisory report and due in part to the infrequent advise to impose financial requirements, they are rarely imposed. In addition, judges hold diverse views on the necessity to impose financial requirements. Overall, a lack of attention to financial problems and a lack of concrete programmes or behavioural conditions are experienced in the sentencing phase, which causes judges to prefer other sentences or a general probation order over concrete financial requirements in the sentencing decision. And even if judges are aware of the impact of financial problems, they may still feel compelled to impose a fine for other reasons or prioritize other sentencing goals.

During the implementation of the sentence, probation officers are often not well equipped to provide sufficient help, guidance and supervision to clients facing (complex) financial problems, as this study corroborates with existing literature (Gålnander, 2023; Todd-Kvam, 2019; van Beek et al., 2021). While financial supervision is effective for some clients, particularly those already motivated or who become motivated during probation, a larger group exhibits high resistance. In the absence of a financial requirement, probation officers try to overcome this resistance by motivating, encouraging and convincing their clients. Generally, it works well to achieve quick results, fostering trust and to provide clarity about the process. Yet, a big stick is missed by some probation officers in the form of mandatory financial requirements, which would allow them to exert slightly more pressure and start financial aid more quickly. In case clients are not working on their financial situation and financial requirements are in place, probation officers have the option to revoke the case. In practice, however, this option is hardly used, especially when clients are progressing in other areas.

Earlier research addressed that probation officers should pay more attention to the impact of debt problems on resocialization and showed that probation officers often do not know where and how to assist probation clients with debt problems (Todd-Kvam, 2019; van Beek et al., 2021). While the majority of offenders are dealing with debt, only a small proportion is actually involved in debt assistance programmes (Beerthuizen et al., 2015; Gålnander, 2023; van Beek et al., 2021). Effective supervision of probation clients with debt problems seems to be hampered by a lack of practical support and slow processes in which clients often do not experience flexibility and customization (Gålnander, 2023; van Beek et al., 2021).

Our research highlights that in case a financial requirement is incorporated in the sentencing decision, some probation officers feel they can exert slightly more pressure and more effective support in addressing financial problems during the supervision phase. This aligns with other findings on the ‘threat of revocation’. Phelps and Ruhland (2022) describe how probation officers perceive ‘filing a revocation motion could be used as a way to provide leverage over people they perceived as not fully committed to the project of change’ (p. 810). Even though, from our study, it seems that revocation is very rarely used, in ultimate cases it is perceived as a helpful tool to stimulate compliance (Maguire and Boone, 2018). Nonetheless, the exact formulation of the requirements is important to minimize arbitrary assessments of compliance (Phelps and Ruhland, 2022). In the event that the condition is not complied with, there is a possibility that the suspended part of the sentence, such as a period of incarceration in case of a suspended sentence, will be enforced. Furthermore, while it is recognized that low-level offenders face various challenges such as housing insecurity and addiction (Appelman et al., 2021; Weijters et al., 2018), it is crucial to consider existing issues in other domains when crafting financial requirements and to refrain from imposing a large number of conditions simultaneously. It is within the discretion of the judge to determine whether the imposition of financial conditions is necessary and desirable, balancing this against the consequences of non-compliance with these conditions.

However, even though financial requirements might help to overcome some barriers, in earlier stages of the criminal justice system, there is too little time, knowledge and attention to the criminogenic potential of having financial problems and how to provide successful support to tackle debt problems. Similar to judges in problem-solving courts (McIvor, 2012; Miller et al., 2020), judges in this study were largely dependent on the information and advice from other professionals in case imposing financial requirements was relevant. Our research reveals significant variability in the attention given to financial problems during the pre-sentencing and sentencing phases. This finding is in line with earlier studies in which too little attention to financial obstacles in the sentencing phase was identified (Koenraadt et al., 2021; Nauta and de Wilde, 2020; Raine et al., 2003).

In addition, while this study showed several problems that make it difficult to obtain sufficient insights during the pre-sentencing phase, judges seem to hold highly diverse views on their role as ‘problem solver’. Whereas some judges perceive the imposition of financial requirements as undesirable and incompatible with punitive measures, others see it as their task to stimulate offenders to work on their debt problems, as it may contribute to a more successful reintegration. These different views are comparable to what David Garland identified as positive and negative forms of penal power (Garland, 2013). This is in line with the literature on Therapeutic Jurisprudence and problem solving courts in which the use of judicial power is endorsed to coerce and stimulate offenders to attend various programmes of treatment aiming to support rehabilitation and reduce recidivism (Casey, 2004; Slinger and Roesch, 2010). These judges have a more active role and need to be informed which programmes and treatments are fruitful by other professionals. Not all judges are in favour of taking these complex matters into account in the sentencing decision.

Finally, this study showed that in all phases of the criminal justice system, there is a lack of recognized programmes to tackle financial problems. In Dutch criminal law, no concrete financial conditions are included and there are no longer any recognized behavioural interventions aimed at resolving debt. Municipalities across the country offer different programmes for offenders with debt problems and not all participants in the process are aware of potential interventions or debt programmes. Other countries, including Norway and Sweden, show similar problems (Gålnander, 2023; Todd-Kvam, 2019). However, support on dealing with debt problems is not only problematic for the population of offenders. Interventions on resolving financial problems are often regarded as inadequate, with indefinite rules and regulations, too little money available while the government overestimates self-reliance of its citizens (Fernandes et al., 2014; Tiemeijer, 2016). In general, there is a lack of knowledge regarding effective interventions for addressing debt problems, which intersects with a broader societal issue affecting the general population (Jungmann, 2020).

This study enabled unique insights in the process of financial supervision within the criminal justice system. While the case files and interviews have provided highly useful insights, a few limitations should be outlined here. First, while nationally a large amount of people are involved in all different steps in the imposition and execution of financial supervision, this study is based on a first selection of interviews with respondents that mainly operate in urban areas. Insights from a larger group of respondents, as well as from other regions and districts would increase the generalizability of the results. Second, because of COVID-19 restrictions over the course of this study, we were not able to interview probation clients that were or have actually been under financial supervision. These groups of respondents are essential to include in future research as they may shed new light on how different forms of supervision on debts are experienced. Third, while many offenders are dealing with a wide range of problems, including housing and addiction, future research could focus on the effectiveness of financial requirements for different groups under supervision. Investigating how financial requirements affect various types of offenders, each dealing with a diverse array of issues, could provide valuable insights.

Even though debts and financial problems concern an extremely complex matter, in general, this study showed that financial supervision within the criminal justice system can still be improved on many points. At all stages in criminal proceedings, there is a lack of knowledge, skill and attention to financial problems in relation to criminal behaviour and rehabilitation.

Footnotes

Acknowledgements

The authors thank Silas Kappert for his assistance during the research process and Fergus McNeill for comments on the manuscript.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This research was funded by the WODC (Research and Data Centre of the Dutch Ministry of Justice and Security under project number 3103).