Abstract

In this paper we present a new approach to solve a risk default, under asymmetric information, between Micorfinance Institutions MFIs and borrowers excluded from the conventional financial systems (financial exlusion). To solve this problem we propose the model, as a system of two differential equations to describe the evolution of some safe and risky borrowers. In fact, the population of borrowers is divided into two compartments: Safe and Risky having an interaction, it is a SR model. With numerical simulations of the SR model, we can describe the evolution of some safe and risky borrowers. The result provides to manage the portfolios of all agencies controlled from the MFIs, by predictions of safe and risky borrowers. Then, define or redefine the management strategies of development and investment, and thus strengthen financial inclusion.

Keywords

Introduction

Microcredit is one of the components of microfinance destined for poor populations. The largest of this population does not have access to conventional financial services. Thus, they exclude from the financial system of the country, it is the financial exclusion. This exclusion is one of the principal factors that may prevent the poor from completely participating in The Process of Economic Development, especially for the development of their countries. 1 Among the mechanisms to solve this financial exclusion, we find the microfinance industry. For more than 40 years, the objective of the microfinance industry has been to fight against poverty, improve the living conditions of the poor, and integrate this population into the development of their countries. 2

Today the more important challenge, for IMFs, is the design of lower-risk products caused by asymmetric information between MFI and the borrowers. The products or contracts 3 offered by MFI, in particular the microcredit, are intended for the population that does not have sufficient collateral and which helps to fight poverty.4,5

Asymmetric information is defined as the presence of adverse selection and moral hazards. The MFI searches to reveal all private information about borrowers. These include information on the entrepreneurial capacity to take risks on micro projects in the case of craft, industrial and commercial, or agricultural activities. To minimize the risk, the MFIs adopt the credit mechanism which makes the information seem less asymmetric. 6

Most often, the MFI provides types of credit of contracts: 7 individual lending and group lending with joint liability. In this last, each borrower commits to repay the part of the other default member(s) group in the maturity date. 8 Hence, this type of repayment is a collective decision of the members group. However, the decision of repayment in individual lending depends only on the borrower. Due to a lack of sufficient collateral, the MFI has created a mechanism of collect if and solidarity loans based on two measures: the joint liability between the group members and an incentive to the refinancing of its investment micro projects, which was considered as rewarding or premium,9,10 provided that all the members respect the contract.

Practically, the borrower chooses a contract with weak monetary and social charges such as the interest rate and the parameters of joint liability. In an econometric study, 11 based on a field survey; It was observed that the beliefs of MFI about the type of its borrowers (safe or risky) are some private information. In the joint liability, each member of the group hopes to avoid repaying the parts, of the other defaulting members. In this case, the group becomes defaulting, therefore all members are excluded, from future refinancing. In fact,12,13 the borrower prefers the group lending contract over the individual contract because the interest rate applied is always lower than the rate for individual lending. In Armendariz and Gollier 14 have demonstrated that the presence of mutual solidarity between group members and which takes the form of mutual monitoring thus reduce the interest rate. On the other hand, moral hazard pushes borrowers to invest in micro projects with higher risk. This implies that a borrower always has an interest in choosing group lending with joint liability. Hence, the risk that the eventual safe borrowers may associate with risky borrowers. 6

In the literature, the researchers and professionals claim that borrowers of the risky type could negatively affect the safe borrower and vice versa. 15 This negative influence in the sense of default generates portfolios at risk, 16 which threatens the sustainability of the MFI. As the portfolios are composed of the financial transactions of the borrowers, then the MFI should control the performance and efficiency of the borrower portfolios. The portfolio at risk is associated with the default risk, which is strongly linked to the number of safe and risky borrowers. This risk presents a strong challenge to have best practices in MFIs. 17

This article's main contribution is to propose a new approach to keep the risk default due to the asymmetric information and to defend theoretically and practically some measures to minimize the number of risky borrowers. In fact, if the rate of risk increases (daily, weekly, monthly, or yearly), then the portfolios at risk increase. The proposed model illustrates this problem, by a system of differential equations whose solution is a prediction of the number of safe and risky borrowers. The approach envisaged in our contribution is to understand the dynamic phenomenon of risk default, in a population of borrowers according to the solvency criterion, thus allowing MFI to predict in the medium and long term the numbers of safe and risky borrowers. Also, see the mutual impact between “Safe” and “Risky” borrowers, without considering the type of offered contracts. Thereby, the MFIs may choose to implement new agencies of proximity in the rural and urban areas or leave the areas where portfolios at risk are worrying.

The remainder of this article is structured as follows. The section “Literature review” reviews credit contracts to the microfinance markets as a dynamic system that requires control. In the section“The model,” we describe the model with the components and parameters as a system of differential equations. In the section “Numerical simulation and interpretations,” we present the solutions of the system using numerical simulation, by assigning values to the parameters of the models. In the section “Conclusion and discussion,” the simulation is accompanied by interpretations and some recommendations about MFI management strategies. We conclude by discussing the results in the financial and management context. Finally, we suggest some perspectives to academic researchers or professionals to improve this study.

Literature review

State of the art

Microfinance institutions (MFIs) are financial institutions that provide loans, savings, and other financial services to low-income borrowers. MFIs play an important role in poverty alleviation by providing access to financial services to people who would otherwise not be able to afford them.

However, MFIs face a number of risks, including the following: Credit risk: This is the risk that a borrower will not repay a loan. Credit risk is a major concern for MFIs because they often lend to borrowers who have no collateral. Operational risk: This is the risk of loss due to human error, system failure, or natural disaster. Operational risk can be a major problem for MFIs, especially those that operate in developing countries with limited infrastructure. Liquidity risk: This is the risk that an MFI will not be able to meet its obligations to its depositors or borrowers. Liquidity risk can be a problem for MFIs, especially those that experience rapid growth. Market risk: This is the risk of loss due to changes in market conditions, such as interest rates or exchange rates. Market risk can be a problem for MFIs, especially those that invest in assets that are sensitive to market fluctuations.

In terms of modeling, this risk was broached by several approaches of mathematical and social sciences to mitigate portfolios at risk. We can cite primarily, the game theory applied to the mechanism design theory, where the players are the MFI and the borrowers.12,18 The goal is to improve credit contracts and minimize the negative effect of asymmetric information. 19 This approach treats the adverse selection and moral hazard through the Nash equilibrium of the repayment game.

The other approach that can be cited is optimization models when the objective is to maximize the borrower welfare as an expected utility function under MFI budget constraints. 9 The constraints are formed as follows: (1) The incentive constraint which takes the form of future refinancing about investment projects if the borrower respects the contract. (2) The participation constraint where the repayments must not exceed the income generated by the micro project.10,15

Also, the data analysis15,20 where the objective is to have all general correlation structures (PCA, logistic regression, …), by determining characteristics of safe and risky borrowers. As well, we also added predictive models for solvency to design a credit scoring model, 21 based on artificial intelligence techniques or Machine Learning (support vector machine, neural network, fuzzy logic, KNN, K-forest, …).

On the management side, there are managerial mechanisms allowing the best management of risk default that is realized, 22 However, the number of academic works remains minimal relatively.

Other works are interested in the best practices of microfinance Armendariz de Agion 2010 with a prescription of successful experiences, where the positive impact manifests on borrower welfare and also on the MFIs portfolio quality. As any non-profit organization, the MFI seeks to ensure sustainability by minimizing the number of risks and expanding its activities in as many areas as possible. The aim is to ensure the broad expansion of the MFI services to poor populations.

The system of differential equations is important for modeling, describing, and control of dynamic phenomena. The asymmetric information generates chaos or randomness when the decision is made in uncertain environments. The concept of hazard is more used in academic studeis as well as mathematics, physics of the dynamic system, economics, chemestry, biology, medecine, and sociology, it is about how modeling approach could explain the social behavior in uncertain environments. 23

General context of the study

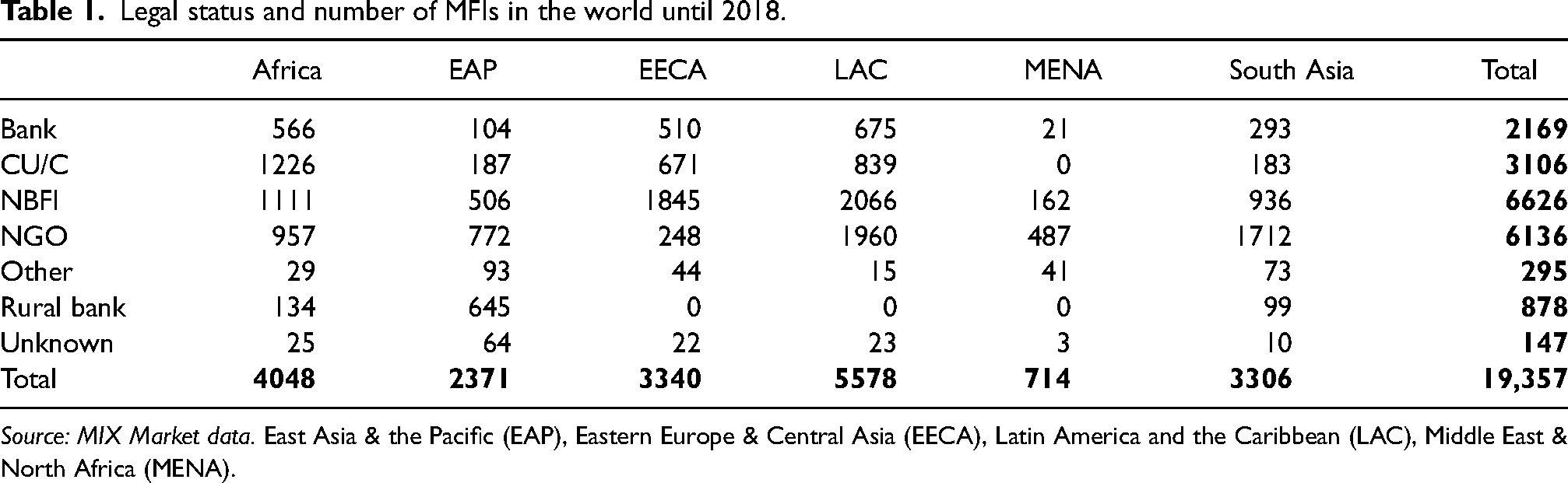

There are several types of MFIs (Microfinance Institutions) in the world (Table 1), dominated by Non-Bank Financial Institutions (NBFI), Non-Governmental Organizations (NGO), Credit Unions and Cooperatives (CU/C), and subsidiaries of commercial banks (Bank). However, NGOs are often transformed into NBFI since they are not authorized to collect savings and/or provide credit to their clients. They are focused on the social development of disadvantaged populations. 24 On the other hand, the activity of credit cooperatives (CU/C) primarily depends on the extent of clients’ savings. As for NBFI, rural, and commercial banks, they depend on both shareholder investments and client deposits.

Legal status and number of MFIs in the world until 2018.

Source: MIX Market data. East Asia & the Pacific (EAP), Eastern Europe & Central Asia (EECA), Latin America and the Caribbean (LAC), Middle East & North Africa (MENA).

Table 1 shows that the microfinance industry is quite prevalent in developing countries/regions. Africa is dominated by credit cooperatives, while Eastern Europe & Central Asia (EECA) and Latin America & the Caribbean (LAC) are dominated by NBFI. The MENA region, East Asia & the Pacific (EAP), and South Asia are dominated by NGOs.

Figure 1 shows the average number of active borrowers and new borrowers financed by MFIs worldwide during the period 2000–2018. Overall, the number of beneficiaries is continuously increasing, and on average, MFIs served between 40,000 and 60,000 borrowers from 2013 to 2018, compared to fewer than 20,000 borrowers during the years 2000–2005.

Average number of active and new borrowers per MFI.

During the global financial crisis, the MFI market stagnated. However, with the economic and financial recovery, the number of borrowers has significantly increased, indicating that MFIs are tapping into new markets (Md Aslam Mia, 2022).

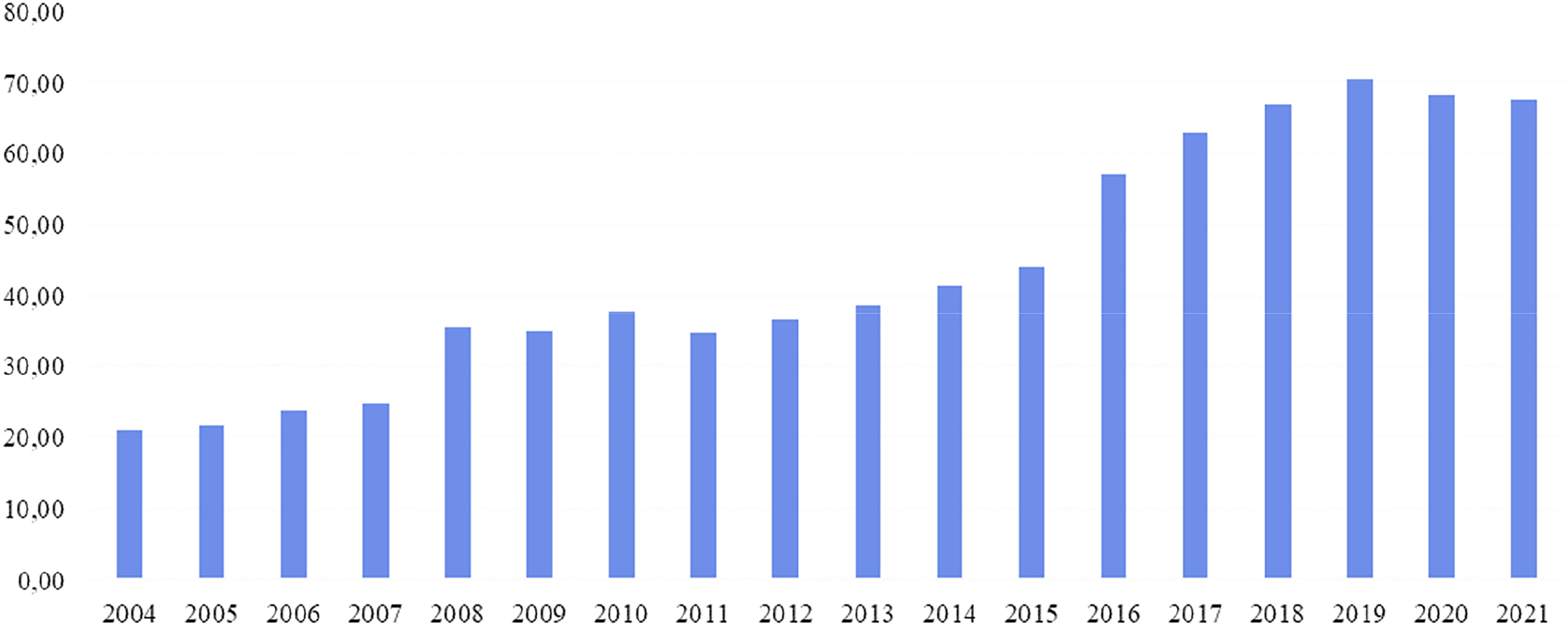

The data from Figure 2 indicate “the number of loan accounts with all microfinance institutions per 1000 adults” in each country, for the years 2004 to 2021. The global average of this number of loan accounts per 1000 adults has significantly increased, from 21.08 in 2004 to 67.51 in 2021. This increase may be attributed to the greater availability of microfinance services, as well as a growing demand for smaller and more accessible loans for vulnerable populations. This indicates that from 2004 to 2021, there has been an increase in the penetration of microfinance institutions in many countries.

Number of loan accounts with all microfinance institutions per 1000 adults, 2004–2021.

According to Figure 3, it can be observed that the average number of loan accounts in all microfinance institutions per 1000 adults is 67.5. Comparing the data of each country to the average reveals that the countries with the lowest numbers of loan accounts are Indonesia (0.26), Tanzania (0.29), Angola (0.35), Brazil (0.64), and Syria (0.94). This result could indicate funding challenges for small businesses and individuals in need of loans. The countries with the highest numbers of loan accounts compared to the average are Estonia (460), Bangladesh (193), and Georgia (158). These countries have well-developed microfinance systems that provide loans to a large number of people, which can help reduce poverty and promote economic and financial inclusion of the population.

Number of loan accounts with all microfinance institutions per 1000 adults, per country.

A high debt-consumption ratio (Figure 4) can be a sign of financial difficulty, as it means that the borrowers are struggling to make their debt payments. MFIs (microfinance institutions) typically have a maximum debt-to-consumption ratio that they will lend to borrowers, but typically around 50%. This ratio significantly increased between 2009 and 2017 to reach around 50%. A study by the Microfinance Information Exchange (MIX) found that the average debt-to-consumption ratio for borrowers in MFIs was 38% in 2021. This means that, on average, borrowers in MFIs were borrowing an amount that was equal to 38% of their annual income. The MIX study also found that the debt-to-consumption ratio varied by region. The highest debt-to-consumption ratios were in Sub-Saharan Africa, where the average ratio was 52%. The lowest debt-to-consumption ratios were in Asia, where the average ratio was 32%.

Average indebtedness relative to consumption has increased significantly in recent years.

A high percentage of indebted households can be a sign that MFIs are lending too much money to households that are unable to repay their loans. This can lead to loan defaults, which can damage the financial stability of MFIs and make it difficult for them to continue lending money to households (Figure 4). Figure 4 demonstrates that the percentage of indebted households in MFIs varied between 20% and 50% from 2009 to 2017, with the poorest households having the highest levels of debt. The percentage of indebted households in MFIs varies by country and region. According to the MIX, the percentage of indebted households in MFIs in 2023 was: Africa: 22.4%, Asia: 16.3%, Latin America and the Caribbean: 14.2%, Europe and Central Asia: 12.1%, Middle East and North Africa: 10.8%. The percentage of indebted households in MFIs is also affected by the type of loan. The percentage of households with loans for consumption purposes is higher than the percentage of households with loans for productive purposes.

Portfolio at risk (PAR) in MFIs is the amount of money that is at risk of not being repaid. It is calculated by taking the total amount of loans outstanding and multiplying it by the percentage of loans that are considered to be at risk of default.

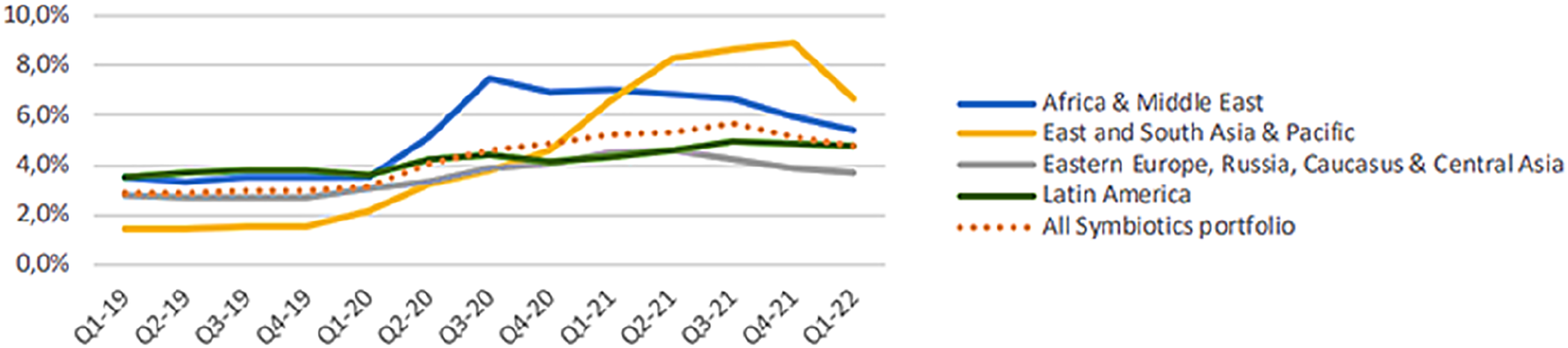

Figure 5 demonstrates that between 2019 and 2022, the PAR in MFIs experienced a significant increase in the East and South Asia & Pacific region, rising from 1.8% to 8.5%. The PAR in MFIs varies by country and region. According to the MIX, the PAR in MFIs in 2023 was: Africa: 12.1%, Asia: 9.4%, Latin America and the Caribbean: 8.2%, Europe and Central Asia: 7.1%, Middle East and North Africa: 6.0%. The PAR in MFIs is a complex issue that is affected by a number of factors, including the economic situation, the cost of microfinance loans, and the availability of microfinance loans. The portfolio at risk of MFIs exceeding 30 days was 6.4% in 2019, a rate slightly above 7% in 2018.

Evolution of portfolio at risk (PAR) by region.

This state of the data shows the importance of the sector and its consistent multichallenges. Therefore, the topic presents an important occupation for academic researchers, which offers some approaches to diagnose and resolve the risk of default.

The model

Microfinance as a system dynamic

In this article, the approach is based on the dynamic system corresponding to the financial system adapted to the microfinance system and the offered services. In our study, the process is supplied primarily by either input which is the distribution of probabilities and contributes to the evolution of the system, see Figure 6. The system is subjected to disturbances that are unobservable variables by MFIs, which means their private information, and that affects the process.

Diagram of the flows of individuals in the CI model.

The non-repayment loan to MFIs results from the borrower's inability to repay (insufficient funds) and also from contaminant contacts between safe and risky borrowers. Failure to repay the loan can lead to understanding how this scourge spreads among borrowers is crucial if we want to control it. For this reason, we propose a Safe-Risk Model that will be noted throughout the rest of this article by the SR model. In this model, the population considered is divided into two compartments at period compartment compartment

where S designates, within the population concerned, the number of safe individuals and R is the number of risky. S and R are observable variables in time, which can be modeled by two independent functions:

We will highlight the dynamics of a system, such as the evolution of borrowers according to their types Safe/Risky. It is modeled by a system of differential equations noted by

The description of model

The proposed model treats the dynamic of the borrowers’ population where the repayment of loans represents a fundamental criterion for the MFIs. Practically, the mutual impact strongly exists between the borrowers due to the social-cultural environment and coexistence. Thus, the influences are positive or negative to respect the credit contracts.

In the one area, Ƶ with population size is P, and

Let

The reformulation of the hypothesis leads us to model in time the evolution number of safe and risky borrowers noted

Numerical simulation and interpretations

In this section, we are proposing numerical simulation as well as

For

Evolution of solvent/insolvent borrowers with initial population (S0, R0) = (10,000, 2000).

Evolution of solvent/insolvent borrowers.

With

Evolution of solvent/insolvent borrowers with

In this scenario, the MFI strategy, for efficient management and development, should maintain the situation that generates these values for

In the period of [0,10], we choose as initial population (S0, R0) = (10,000, 1865), and

Evolution of solvent/insolvent borrowers with initial population (S0, R0) = (10,000, 1865).

With an initial population of (S0, R0) = (10,000, 2000), Figure 11 illustrates the worst scenarios that MFI can face, since the beginning of the period we visualize an acute drop of

Evolution of solvent/insolvent borrowers; the worst scenarios that MFI can face.

Conclusion and discussion

Microfinance is considered a new component in finance and support for sustainable development since its creation by Muhamud Yunus (Nobel Prize of Peace in 2006). Academic studies, until the present, focus on microcredit, to aim to diagnose the risk of default, 6 related to the asymmetric information, thereby designing optimal loan contracts to effectively manage the portfolios of MFI. 8

The different approaches, of mathematical and social sciences, are used to offer some practical solutions in the microfinance industry like game theory and data analysis. However, the design of loan contracts is, often, compromised by the type of borrowers (safe or risky). This risk of default generates a deficient portfolio in MFIs (portfolio at risk). So, the key to our contribution is to present a new applied mathematical approach to the risk of default. The results are significant and not limited and the model illustrates prove that the microfinance environment takes form as a system dynamic. It describes the interaction, mainly between MFIs and the borrowers and, on the other hand, by the borrowers themselves. Our model will be a fundamental decision-making tool for MFIs and decision-makers throughout the microfinance markets. 2 The model does not take into account the contract type, but it allows visualizing the evolution of safe and risky borrowers over time. Therefore, the MFIs will have a possibility to implicitly reveal private information such as the nature of mutual interactions between borrowers and the features of areas where MFI would install the proximity agencies. In this case, the game is considered a game with perfect and complete information. Thus, MFIs can redirect their management and development strategies with less risk of risk contracts or products. 3 The MFIs decide: (1) to create new proximity agencies or exit the areas, assessing over time the number of safe and risky borrowers; (2) to target people who have not yet integrated the microfinance system and to enhance their performance on financial inclusion; (3) to offer a mechanism of sustainable development to people need to improve their living conditions, to save them from poverty and be integrated into the economic development of their countries.

To go even further, and depending on the variation of the inputs of the model, the analysis of the system allows understanding, forecasting the system behaviors, and then measuring its performance, thereby controlling the output of the model, which ensures the MFIs mitigate the portfolios at risk and ensure sustainability.

The improvement of the proposed model leads to yield significant results by MFIs. This is done through the new works of dynamic systems namely the systems of differential equations and also by studying the stability of the system with associated bifurcation, which proposed solutions that meet the needs of MFIs. In another way, the model calibration requires the point estimate or confidence interval of the parameters of the model. The technical survey and empirical study, on one area, enable to calibrate model performance, and it allows the MFIs to decide to install or create the new proximity agencies. The area likely to have deficient portfolios would be excluded from the action plan of MFIs. 25

The comparison with recent works will be among the perspectives. In fact, our contribution is one of the research works to treat the risk by default, which is a new approach. Also, it is an initiation to introduce a hybridization of probabilities theory, data sciences, and dynamics systems to solve all problems in microfinance markets such as micro-insurance. This work is open to exploring other future works like portfolio assessment in microfinance markets.

On the other hand, tolerance and stability in differential equations refer to the concepts of how a numerical method handles errors and fluctuations over time, and how stable the solution remains despite perturbations or changes in input parameters. Tolerance relates to the acceptable level of error or deviation from the exact solution, while stability pertains to the behavior of the solution over time and its sensitivity to small changes in initial conditions or parameters. These considerations are crucial in designing and analyzing numerical methods for solving differential equations accurately and efficiently. This is one of the future perspectives that we can solve to significantly improve and calibrate the models with the multidimensional risk of non-reimbursement in microfinance institutions. Besides, we can investigate the bankruptcy prediction of Maghreb Companies. 26

Footnotes

Acknowledgments

The authors would like to express their gratitude to the editors and reviewers for their valuable contributions to the publication of this modest work.

Author contributions

The authors contributed equally to the writing of the article.

Availability of data and material

The data is valid upon request from the readers.

Declaration of conflicting interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.